The study involved four major activities in estimating the current size of the polymer foam market—exhaustive secondary research collected information on the market, peer markets, and parent markets. The next step was to validate these findings, assumptions, and sizing with the industry experts across the polymer foam value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation were used to estimate the market size of segments and subsegments.

Secondary Research

Secondary sources for this research study include annual reports, press releases, and investor presentations of companies; white papers; certified publications; and articles by recognized authors; gold- and silver-standard websites; polymer foam manufacturing companies, regulatory bodies, trade directories, and databases. The secondary research was mainly used to obtain critical information about the industry’s supply chain, the pool of key players, market classification, and segmentation according to industry trends to the bottom-most level and regional markets. It has also been used to obtain information about key developments from a market-oriented perspective.

Primary Research

The polymer foam market comprises several stakeholders, such as raw material suppliers, technology support providers, manufacturers, and regulatory organizations in the supply chain. Various primary sources from the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information. Primary sources from the supply side included industry experts such as Chief Executive Officers (CEOs), vice presidents, marketing directors, technology and innovation directors, and related key executives from various companies and organizations operating in the polymer foam market. Primary sources from the demand side included directors, marketing heads, and purchase managers from various sourcing industries.

Following is the breakdown of the primary respondents:

To know about the assumptions considered for the study, download the pdf brochure

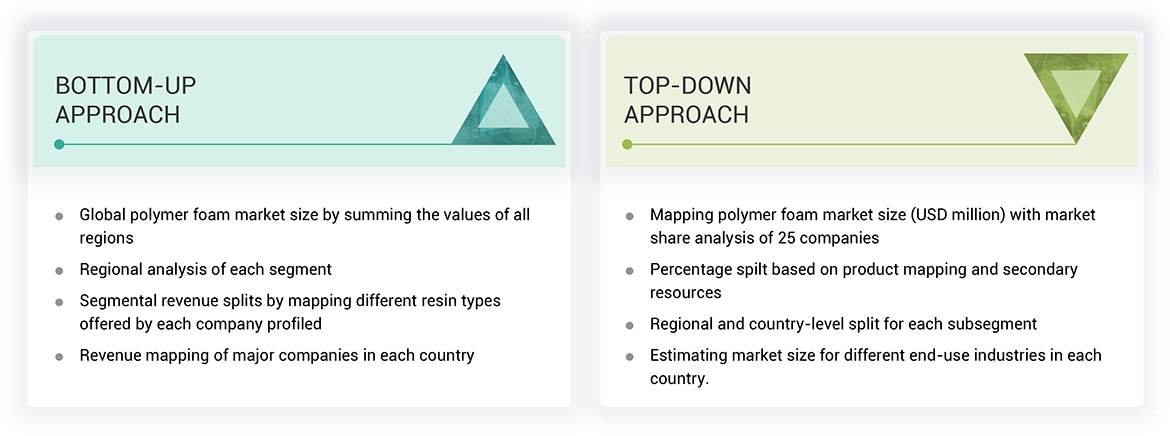

Market Size Estimation

Both the top-down and bottom-up approaches have been used to estimate and validate the total size of the polymer foam market. These approaches have also been used extensively to estimate the size of various dependent market subsegments. The research methodology used to estimate the market size included the following:

The following segments provide details about the overall market size estimation process employed in this study

-

The key players in the market were identified through secondary research.

-

The market shares in the respective regions were identified through primary and secondary research.

-

The value chain and market size of the polymer foam market, in terms of value, were determined through primary and secondary research.

-

All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources.

-

All possible parameters that affect the market covered in this research study were accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data.

-

The research included the study of annual and financial reports of the top market players and interviews with industry experts, such as CEOs, VPs, directors, sales managers, and marketing executives, for critical insights, both quantitative and qualitative

Data Triangulation

The market was split into several segments and sub-segments after arriving at the overall market size using the market size estimation processes as explained above. Data triangulation and market breakdown procedures were employed to complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment. The data was triangulated by studying various factors and trends from both the demand and supply sides in the polymer foam sector.

Market Definition

Polymer foams are made of polymers, blowing agents, and additives. They are produced using different processing methods, such as slab-stock by pouring, extrusion, and other molding forms. They are used in various industries, such as packaging, furniture and bedding, building and construction, and automotive. These foams are classified based on their structures as closed and open cells. Closed-cell foam is rigid, whereas open-cell foam is flexible.

Stakeholders

-

Raw material manufacturers

-

Technology support providers

-

Manufacturers of polymer foam

-

Traders, distributors, and suppliers

-

Regulatory Bodies and Government Agencies

-

Research & Development (R&D) Institutions

-

End-use Industries

-

Consulting Firms, Trade Associations, and Industry Bodies

-

Investment Banks and Private Equity Firms

Report Objectives

-

To analyze and forecast the market size of the polymer foam market in terms of value

-

To provide detailed information regarding the major factors (drivers, restraints, challenges, and opportunities) influencing the regional market

-

To analyze and forecast the global polymer foam market based on foam type, resin type, end-use industry, and region

-

To analyze the opportunities in the market for stakeholders and provide details of a competitive landscape for market leaders

-

To forecast the size of various market segments based on five major regions: North America, Europe, Asia Pacific, Middle East & Africa, and South America, along with their respective key countries

-

To track and analyze the competitive developments, such as acquisitions, partnerships, collaborations, agreements, and expansions in the market

-

To strategically profile the key players and comprehensively analyze their market shares and core competencies

HIGHEST CAGR MARKET IN 2023

HIGHEST CAGR MARKET IN 2023 INDIA FASTEST GROWING MARKET IN THE REGION

INDIA FASTEST GROWING MARKET IN THE REGION

Tom

Jul, 2022

Need market intelligence on materials used to make composites, including resins, reinforcements, fillers, etc. in the US..