Additive Masterbatch Market

Additive Masterbatch Market by Type (Antimicrobial, Antioxidant, Flame Retardants), Carrier Resin (PE, PP, PS), Application (Packaging, Building & Construction, Consumer Goods, Automotive, Agriculture), and Region - Global Forecasts to 2030

OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

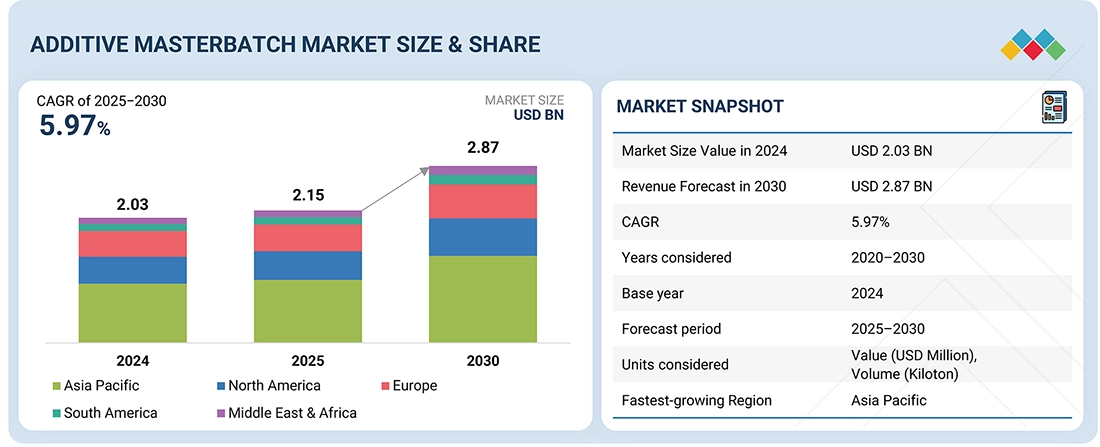

The additive masterbatch market is projected to grow from USD 2.15 billion in 2025 to USD 2.87 billion by 2030, at a CAGR of 5.97%, in terms of value. One of the major drivers of the additive masterbatch market is the growing demand of high-quality plastic products with advanced characteristics like UV resistance, flame retardancy, antimicrobial and color stability, where additive masterbatches can be effective to attain the desired attributes. Also, the increasing use of plastics in industries such as automotive, packaging, electronics, and building & construction drives the demand, as manufacturing companies are adopting effective and efficient methods to improve the life span and functionality of the products by using advanced additve masterbatches.

KEY TAKEAWAYS

-

BY TYPEAdditive masterbatch market is segmented into antimicrobial additive, antioxidant additive, flame retardant, UV stabilizer, foaming agent/blowing agent, optical brightener, nucleating agent, and other types. Flame retardants dominate the market, as they ensure fire safety, regulatory compliance, and material performance across key industries such as construction, automotive, and packaging.

-

BY CARRIER RESINThe additive Masterbatch market is segmented into PP, LDPE & LLDPE, HDPE, PVC, PU, PS, and Other Carrier Resins. The PP (polypropylene) segment accounted for the largest share of the additive masterbatch market due to its versatility, cost-effectiveness, and compatibility with a wide range of additives.

-

BY APPLICATIONKey applications include packaging, building & construction, consumer goods, automotive, textiles, agriculture, and other applications. Packaging leads the market owing to rising e-commerce and food & beverage demand.

-

BY REGIONThe additive masterbatch market covers Europe, North America, Asia Pacific, South America, the Middle East, and Africa. Asia Pacific is expected to grow fastest, with a CAGR of 6.68%, supported by booming packaging, construction, and manufacturing industries in countries such as China, India, and Southeast Asian economies. Rapid urbanization and the expansion of e-commerce logistics strengthen demand.

-

COMPETITIVE LANDSCAPEThe major market players adopt both organic and inorganic strategies, including partnerships, acquisitions, and product launches. For instance, Avient Corporation (US), Ampacet Corporation (US), LyondellBasell Industries Holdings B.V. (US), and Tosaf Compounds Ltd. (Israel) are expanding their additive masterbatch portfolios and investing in sustainable formulations to meet rising demand across multiple end-use industries.

The additive masterbatch market is projected to witness robust growth in the coming years, driven by rising demand across packaging, automotive, construction, and consumer goods industries. With a growing emphasis on enhancing plastic performance through properties such as UV resistance, flame retardancy, antimicrobial protection, and recyclability, additive masterbatches are gaining strong global adoption. Furthermore, increasing regulatory and consumer focus on sustainable and recyclable plastic solutions is accelerating the use of advanced formulations, reinforcing the role of additive masterbatches as essential, value-adding solutions for diverse end-use applications.

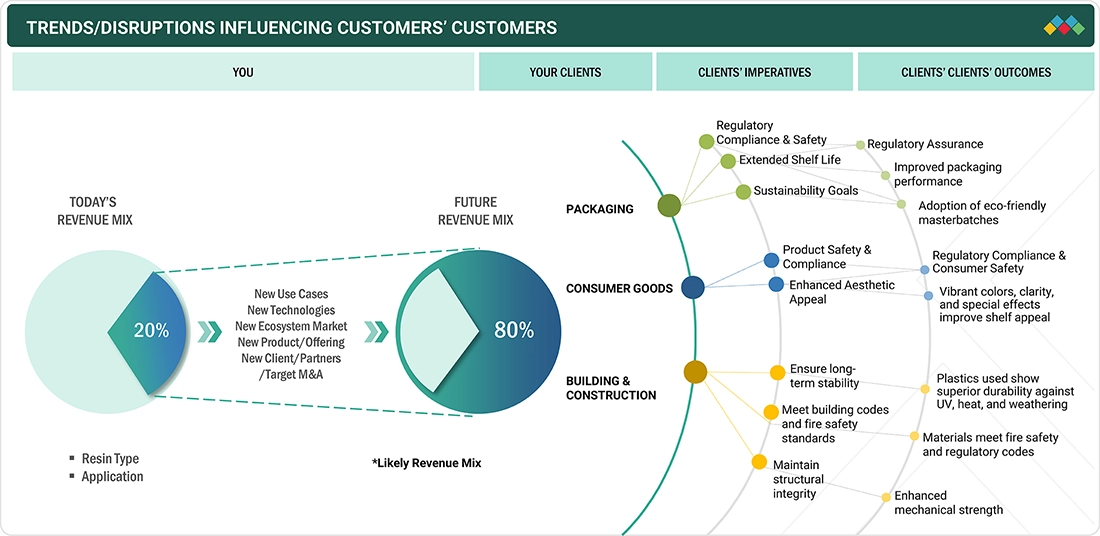

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The impact on consumers' business emerges from customer trends or disruptions. Plastic product manufacturers, such as those in packaging, agriculture, automotive, and consumer goods, are the clients of additive masterbatch producers. The target end-use applications are the customers of additive masterbatch manufacturers. Shifts, which are changing trends or disruptions, will impact the revenues of end users. The revenue impact on end users will affect the revenue of hotbets, which will further affect the revenues of additive manufacturers.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Level

-

Growing Priority on Quality Retention and Extended Shelf Life

-

Advancement in packaging solutions

Level

-

Stringent Environmental and Compliance Regulations

-

High cost of advanced additives

Level

-

Growth in Agriculture Films & Greenhouse Applications

-

Rising demand for sustainable & eco-friendly solutions

Level

-

Recyclability Concerns in Additive Use

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Growing Priority on Quality Retention and Extended Shelf Life

The additive masterbatch market is strongly driven by the rising demand for enhanced product protection and the extension of shelf life. The packaging materials used in the food and beverage sector should not only shield products against external contamination but also ensure freshness and prevent depreciation. Oxygen scavengers, antimicrobial agents, and antioxidants are additives that are currently being incorporated into packaging solutions to satisfy these requirements. E.g., antimicrobial masterbatches prevent bacterial and fungal proliferation in films and containers, making them safe and prolonging their shelf life. On the same note, antioxidants inhibit the degradation of polymers in processing and storage, which is particularly important to oils, dairy products, and packaged snacks. UV stabilizers and oxygen barrier additives play a crucial role in the pharmaceutical industry, ensuring that sensitive formulations are protected from light and oxygen exposure. This is a protection and a long shelf-life orientation, not only due to consumer demand but also because of the strict food safety and pharmaceutical regulations worldwide. This is beneficial to retailers and brand owners, as the extended shelf life not only decreases waste but also enhances logistics efficiency. Accordingly, the increased focus on safety, freshness, and quality assurance is gaining momentum, driving up demand for additive masterbatch in various industries, especially in areas where packaged food consumption is rapidly increasing.

Restraint: Stringent Environmental and Compliance Regulations

The additive masterbatch market is under threat due to the stringent global environmental and sustainability regulations. Governments in various regions are not only putting bans on single use plastics but are also investigating the safety of chemicals in the food packaging and packaging of consumer goods and construction materials. As an example, some flame retardants, heavy metal stabilizers and phthalate-based plasticizers are restricted or prohibited because of their human health and environmental toxicity. This presents a dual challenge to manufacturers of masterbatches: to meet the constantly changing rules and at the same time not to spoil the performance of the products. Moreover, the packaging materials used in end-use industries, particularly the food and pharmaceutical industries, must be of high safety standards requiring the use of BPA-free, food-contact-safe, and non-toxic additives. These regulatory measures compel companies to spend a lot of money in research and development, testing and reformulation which hikes the cost and period of operation. Meanwhile, the level of consumer understanding of sustainability has increased, which compels brand owners to require environmentally friendly and recyclable solutions, usually at competitive prices. Such pressure of compliance, cost, and performance is a constant factor and, therefore, makes environmental and regulatory requirements one of the most limiting factors in the additive masterbatch market. With regulations getting even stricter in most parts of the world, manufacturers that are not able to adjust fast would be forced to lose out on market share particularly in highly regulated markets such as Europe and North America.

Opportunity: Growth in Agriculture Films & Greenhouse Applications

The additive masterbatch market is discovering a new opportunity in the agriculture industry, which is proving to be a key growth driver, owing to the increased use of plastic films and greenhouse coverings to boost crop production and resource efficiency. Agricultural films, such as mulch films, greenhouse and silage wraps, and irrigation pipes, require an additive that ensures the films can withstand extreme environmental forces, including prolonged UV exposure, temperature fluctuations, and moisture. Masterbatches, such as UV stabilizers, anti-fog agents, antioxidants, and antimicrobial formulations, are additive masterbatches that contribute to the longevity and efficacy of these films. For instance, UV stabilizers help prevent degradation of greenhouse covers under strong sunlight conditions, and anti-fog additives maintain light transmission by preventing the formation of water droplets, thereby enhancing plant growth. Antimicrobial masterbatches minimize the risk of bacterial and fungal growth on films, thereby enhancing crop hygiene. Additionally, there are foaming agents and processing aids that enable the lightweight production of films at a low cost without compromising their strength. As the world focuses on food security and sustainable agriculture, farmers are increasingly investing in advanced agricultural plastics to conserve water, improve harvesting efficiency, and extend the growing season. This is more pronounced in the Asia-Pacific, the Middle East, and Latin America, where greenhouse farming is experiencing rapid growth.

Challenge: Recyclability Concerns in Additive Use

One of the significant issues related to the additive masterbatch market is that it may adversely affect the recyclability of plastics. Although additives enhance various properties, such as UV stability, flame resistance, antimicrobial action, or color brightness, they may occasionally complicate the recycling process. Some additives can alter the melting characteristics, viscosity, or thermal stability of polymers, making it challenging to reprocess plastics without compromising their performance. For instance, flame retardants or incompatible pigments used in large quantities can decrease the mechanical strength or clarity of the recycled plastics, thereby restricting their use in high-value applications. Additionally, certain additives generate hazardous waste products during the recycling process, which can lead to increased safety and compliance issues. The reflection of several additives in multilayer packaging films and complex products also makes them more challenging to sort and recycle, as they do not quickly segregate and are difficult to identify. As the world transitions to a more circular economy, with a growing focus on its principles and stringent control of plastic waste, recyclability becomes a threat to a manufacturer's reputation and operations. To mitigate this, businesses are investing in recyclable or similar additives and bio-based alternatives that retain their functionality without interfering with reuse. Addressing this difficulty is essential to the additive masterbatch sector to be sustainable and contribute to a global process of switching to closed-loop plastic systems.

Additive Masterbatch Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Antimicrobial additive masterbatches for food packaging and healthcare products | Enhanced hygiene| Reduced microbial growth| Improved shelf-life| Compliance with safety regulations |

|

Flame-retardant masterbatches for electrical & electronic housings | Improved fire safety| Regulatory compliance| Stable mechanical properties| Long-term durability |

|

Antifog and slip additive masterbatches for fresh produce packaging films | Clear visibility| Reduced condensation| Better product presentation| Ease of handling and packaging |

|

Antioxidant and UV stabilizer masterbatches for automotive interiors and exteriors | Longer material lifespan| Color stability| Resistance to heat and light| Enhanced vehicle aesthetics |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The additive masterbatch market ecosystem consists of raw material suppliers (BASF SE,3M, Covestro AG, and Arkema SA), manufacturers (Avient Corporation, Ampacet Corporation, LyondellBasell Industries Holdings B.V., Tosaf Compounds Ltd., and Plastika Kritis S.A.), and end users (Procter & Gamble, Ford, Amcor Limited, Volkswagen, General Electric Company, and Syngenta AG ). Raw materials such as polymers, dispersants, hindered amine light stabilizers (HALS), and brominated compounds are compounded into masterbatches that impart color, durability, UV resistance, or antimicrobial properties to plastics. End users in packaging, automotive, construction, and consumer goods drive demand for functional and sustainable materials, while producers ensure consistent dispersion and tailored performance. Collaboration across the value chain is crucial for advancing recyclability, ensuring compliance with regulations, and driving the growth of specialty additive solutions.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Additive Masterbatch Market, By Type

Flame retardant segment represented the largest type of the global additive masterbatch market, in terms of value, in 2024. This dominance is driven by its indispensable role in meeting stringent fire safety regulations across construction, automotive, electrical, and packaging sectors. As industries increasingly replace metals with lightweight polymers, the need for advanced flame-retardant solutions has intensified to ensure compliance and performance. This segment also commands higher value due to the complexity and specialization of formulations, making it a critical revenue driver and a strategic focus area for producers targeting safety-driven applications.

Additive Masterbatch Market, By Carrier Resin

The polypropylene (PP) segment was the largest carrier resin of the global additive masterbatch market in 2024, due to its broad range of use, low cost, and good performance profile. PP has a very good balance of mechanical strength, chemical resistance and processability and is therefore a good carrier of dispersible functional additive in various applications. Its easy weight and the ability to be combined with a wide variety of additives like UV stabilizers, antioxidants, flame retardants and antimicrobial agents have helped to strengthen its supremacy. Industries such as automotive, consumer goods, textiles, and especially packaging heavily utilize PP-based masterbatches in order to make products durable, improve their safety, and appearance.

Additive Masterbatch Market, By Application

In 2024, the packaging application dominated the additive masterbatch market, in terms of value. This dominance is led by its core presence in consumer-driven markets that include food and beverage, pharmaceutical, personal care, and e-commerce. Due to the growing use of packaging as a protective coating as well as a branding and marketing device, the demand for performance improved materials has become extremely high. Additive masterbatches are important solutions because they enhance UV resistance, mechanical strength, antimicrobial protection and stability. These improved packaging formats are used in both flexible and rigid packaging, especially in films, bags, containers and bottles to satisfy the high standards of the modern supply chains. The increased customer demand for safe packaging with high durability and aesthetic appeals further increases the use of advanced additive formulations.

REGION

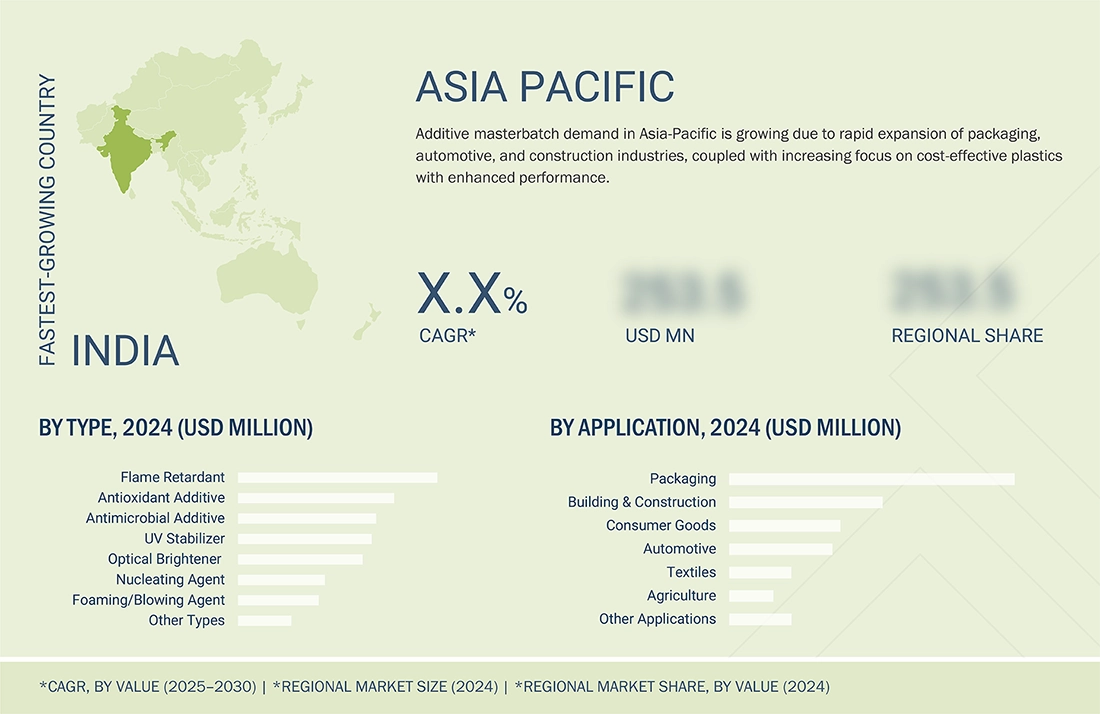

Asia Pacific to be the fastest-growing region in global additive masterbatch market during forecast period

Asia Pacific additive masterbatch market is expected to register the highest CAGR during the forecast period, driven by rapid industrialization, increased manufacturing capacity, and robust demand across end-use applications. Its superiority is mainly due to its well-developed plastics and polymer processing business, which supports a wide range of packaging, automotive, consumer goods, construction, and agricultural market segments. Packaging is one of the major growth drivers, such as increasing urbanization, growing e-commerce penetration, and evolving consumer behavior, which drive demand for high-performance and eco-friendly packaging solutions. Furthermore, the automotive industry in countries such as China, India, Japan, and South Korea is rapidly adopting additive masterbatch for weight reduction, enhanced aesthetics, and improved material properties to meet global fuel efficiency and emissions standards. Another sector that drives market growth is the construction sector, where there is a growing use of plastics in pipes, films, and insulation materials. Competitively low production costs, raw material availability, and an expanding roster of regional producers further enhance Asia Pacific's dominance in this market.

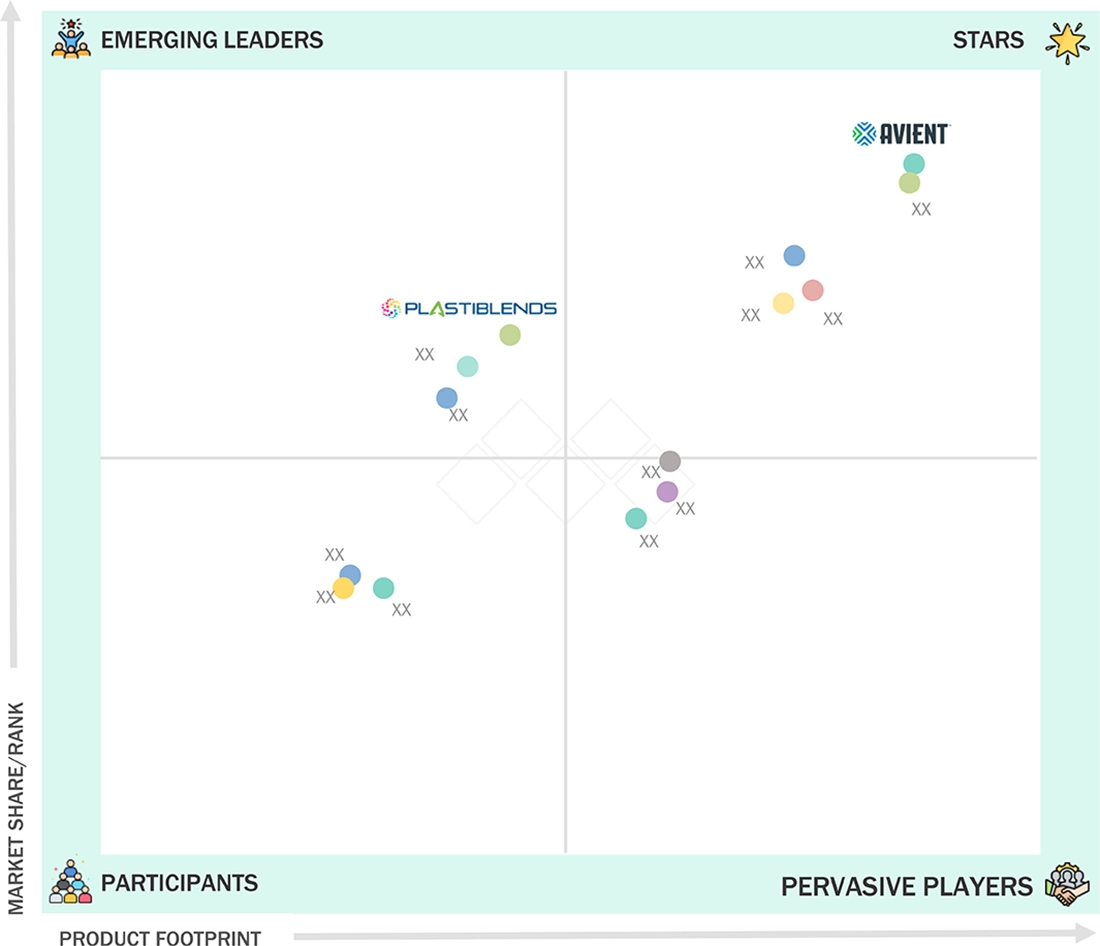

Additive Masterbatch Market: COMPANY EVALUATION MATRIX

In the additive masterbatch market matrix, Avient Corporation (Star) leads with a strong market share and broad product portfolio, underpinned by its advanced specialty additive masterbatches that cater to packaging, automotive, healthcare, and consumer goods. Its ability to deliver high-performance, sustainable, and regulatory-compliant solutions has positioned it as a preferred partner for global brand owners and converters. Plastiblends (Emerging Leader) is gaining traction with its cost-competitive formulations and growing presence in functional additive solutions, particularly in Asia Pacific. While Avient Corporation dominates through scale, global reach, and innovation-driven offerings, Plastiblends demonstrates strong potential to advance toward the leaders’ quadrant as demand for region-specific, high-performance, and value-driven additive masterbatches accelerates.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size Value in 2024 | USD 2.03 Billion |

| Revenue Forecast in 2030 | USD 2.87 Billion |

| Growth Rate | CAGR of 5.97% from 2025–2030 |

| Actual data | 2020–2030 |

| Base year | 2024 |

| Forecast period | 2025–2030 |

| Units considered | Value (USD Million), Volume (Kiloton) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered | By Type: Antimicrobial Additive, Antioxidant Additive, Flame Retardant, UV Stabilizer, Foaming Agent/Blowing Agent, Optical Brightener, Nucleating Agent, and Other Types By Carrier Resin: PP, LDPE & LLDPE, HDPE, PVC, PU, PS, Other Carrier Resins By Application: Packaging, Building & Construction, Consumer Goods, Automotive, Textiles, Agriculture, and Other Applications |

| Regional Scope | Asia Pacific, Europe, North America, Middle East & Africa, and South America |

WHAT IS IN IT FOR YOU: Additive Masterbatch Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Market size and forecast for selected countries in Asia Pacific | Provided individual market sizing, CAGR, and demand drivers for each country | Helps client tap into fast-growing markets and design country-level entry strategies |

| Customer intelligence on key end-use sectors | Delivered insights on buying patterns, price sensitivity, and key selection criteria from major customer groups | Enables client to tailor product positioning and pricing strategies to match customer expectations |

RECENT DEVELOPMENTS

- July 2025 : Avient Corporation launched new oxygen scavenger additives formulated to enhance the recyclability of PET packaging. Works with up to 100 % rPET, supports direct food contact, maintains clarity, and is suitable for mono or multilayer bottles.

- November 2023 : Sukano AG formed a partnership with PlastiColors to meet the growing market demand for PET packaging in South Africa.

- September 2022 : Avient Corporation opened a new production plant in Brembate (BG), Italy in response to increased product demand. The new site doubles additive capacity. This new site with its cutting-edge technologies will further improve the service provided to our customers by speeding up the innovation process, thus helping to bring products to market more quickly.

- April 2022 : Avantium N.V. and Sukano AG signed an offtake agreement to develop masterbatches for PEF.

- September 2020 : Americhem acquired Controlled Polymers in Denmark. Controlled Polymers seamlessly integrates with Americhem and its Engineered Compounds division (AEC) by combining the companies’ product lines to create a comprehensive range of offerings for customers in the medical plastics and other industries.

Table of Contents

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Methodology

The study involved four major activities in estimating the market size for the additive masterbatch market. Exhaustive secondary research was done to collect information on the market, the peer market, and the parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, the market breakdown and data triangulation procedures were used to estimate the market size of the segments and subsegments.

Secondary Research

Secondary sources used in this study included annual reports, press releases, and investor presentations of companies; white papers; certified publications; articles from recognized authors; and gold-standard and silver-standard websites, such as Factiva, ICIS, Bloomberg, and others. The findings of this study were verified through primary research, which involved conducting extensive interviews with key officials, including CEOs, VPs, directors, and other executives. The breakdown of profiles of the primary interviewees is illustrated in the figure below:

Primary Research

The additive masterbatch market comprises several stakeholders, such as raw material suppliers, end-product manufacturers, and regulatory organizations in the supply chain. The demand side of this market is characterized by key opinion leaders in various applications for the additive masterbatch market. The supply side is characterized by advancements in technology and diverse application industries. Various primary sources from both the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information.

The following is a breakdown of the primary respondents:

Note: Tier 1, Tier 2, and Tier 3 companies are classified based on their market revenue in 2023/2024, available in the public domain, product portfolios, and geographical presence.

Other designations include consultants and sales, marketing, and procurement managers.

To know about the assumptions considered for the study, download the pdf brochure

| COMPANY NAME | DESIGNATION | |

|---|---|---|

| Avient Corporation | Senior Manager | |

| Ampacet Corporation | Innovation Manager | |

| LyondellBasell Industries Holdings B.V. | Vice-President | |

| Tosaf Compounds Ltd. | Production Supervisor | |

| Plastika Kritis S.A. | Sales Manager | |

Market Size Estimation

Both top-down and bottom-up approaches were used to estimate and validate the total size of the additive masterbatch market. These methods were also used extensively to estimate the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

- The key players in the industry have been identified through extensive secondary research.

- The supply chain of the industry has been determined through primary and secondary research.

- All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

- All possible parameters that affect the markets covered in this research study have been accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data.

Data Triangulation

After determining the overall market size using the market size estimation processes explained above, the market was divided into several segments and subsegments. To complete the overall market engineering process and determine the exact statistics for each market segment and subsegment, data triangulation and market breakdown procedures were employed, as applicable. The data was triangulated by studying various factors and trends from both the demand and supply sides in the additive masterbatch industry.

Market Definition

According to the Polymer Technology Dictionary, an Additive masterbatch is a concentrated mixture of functional additives encapsulated in a polymer carrier, used to modify plastic properties, enhance performance, durability, functionality, and processability across various applications. It is used in various carrier resins, including Polypropylene (PP), Low-Density Polyethylene (LDPE), Linear Low-Density Polyethylene (LLDPE), High-Density Polyethylene (HDPE), Polyvinyl Chloride (PVC), Polyethylene Terephthalate (PET), Polystyrene (PS), and Polyurethane (PUR). Various types of additive masterbatches, including antimicrobial additives, antioxidant additives, flame retardants, UV stabilizers, foaming agents/blowing agents, optical brighteners, nucleating agents, and others, are used in packaging, building & construction, consumer goods, automotive, textile, and agricultural applications.

Stakeholders

- Additive masterbatch manufacturers

- Additive masterbatch distributors

- Raw material suppliers

- Government and research organizations

- Investment banks and private equity firms

Report Objectives

- To analyze and forecast the size of the global additive masterbatch market in terms of value and volume

- To provide detailed information about the important drivers, restraints, challenges, and opportunities influencing market growth

- To define, describe, and segment the market based on type, carrier resin, application, and region

- To forecast the size of the market segments based on regions such as Asia Pacific, North America, Western Europe, Central & Eastern Europe, the Middle East & Africa, and South America

- To strategically analyze the segmented markets with respect to individual growth trends, prospects, and contributions to the overall market

- To identify and analyze opportunities for stakeholders in the market

- To analyze competitive developments such as expansions, partnerships & collaborations, mergers & acquisitions, agreements, and product launches in the market

- To strategically profile the key companies and comprehensively analyze their core competencies

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This ReportPersonalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Additive Masterbatch Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free Customisation

Growth opportunities and latent adjacency in Additive Masterbatch Market