Network Transformation Market by Solution (SDN and NFV, C-RAN, Network Automation and 5G Networks), Professional Service, Managed Services (Network Monetization, Network Management, Network Testing),Vertical, and Region - Global Forecast to 2022

[153 Pages Report] The network transformation market size is expected to grow from USD 4.28 Billion in 2016 to USD 66.86 Billion by 2022, at a Compound Annual Growth Rate (CAGR) of 61.9% during 2017�2022. The base year considered for the study is 2016 and the forecast period is from 2017 to 2022.

Objectives of the Study

The main objective of the report is to define, describe, and forecast the network transformation market size by components (solutions and services), organization sizes, verticals, and regions. The report provides detailed information on the major factors (drivers, restraints, opportunities, and challenges) influencing the growth of the market. The report attempts to forecast the market size with respect to the 5 main regions, namely, North America, Europe, Asia Pacific (APAC), Middle East and Africa (MEA), and Latin America. The report strategically profiles the key market players and comprehensively analyzes their core competencies. It also tracks and analyzes the competitive developments, such as joint ventures, mergers and acquisitions, and new product developments, in the market.

The research methodology used to estimate and forecast the network transformation market size began with the collection and analysis of data on the key vendor revenues through secondary sources, including annual reports, press releases, investor presentations, conferences, and associations (IEEE International 5G submit, 20th Innovation on cloud, Internet, and Networks [ICIN 2017], and 3rd IEEE conference on network standardization), technology journals, certified publications, articles from recognized authors, directories, and databases. The vendor offerings were also taken into consideration to determine the market segmentations. The bottom-up procedure was employed to arrive at the overall market size of the market from the revenue of the key players and their market shares. The market spending across all the regions, along with the geographic split in various verticals, was considered to arrive at the overall market size. After arriving at the overall market size, the total market was split into several segments and subsegments, which were then verified through primary research by conducting extensive interviews with key personnel, such as Chief Executive Officers (CEOs), Vice Presidents (VPs), directors, and executives. The data triangulation and market breakdown procedures were employed to complete the overall market engineering process and arrive at the exact statistics for all the segments and subsegments. The breakdown of the profiles of the primary participants is depicted in the following figure:

To know about the assumptions considered for the study, download the pdf brochure

The network transformation market includes various vendors providing network transformation solutions, including C-Ran, SDN & NFV, and Network Automation to commercial clients across the globe. Major market players such as Cisco, Juniper Networks, HPE, Huawei, IBM, Dell EMC, NEC, Intel, Nokia Networks, Ericsson, Samsung, FUJITSU, Ciena, Accenture, GENBAND, AT&T, Arista Networks, and 6WINDS have adopted partnerships, agreements, and collaborations as key strategies to expand their market reach. These Network Transformation Solutions Vendors are rated and listed by us on the basis of product quality, reliability, and their business strategy. Please visit 360Quadrants to see the vendor listing of Network Transformation Solutions.

Key Target Audience for Network Transformation Market

- Network solution providers

- Telecommunication providers

- Mobile network operators

- Cloud service providers

- Enterprise data center professionals

- Third-party network testing service providers

- Managed Security Service Providers (MSSPs)

- IT suppliers

- Consultancy firms and advisory firms

- Regulatory agencies

- Technology consultants

- Government

The study answers several questions for the stakeholders, primarily, which market segments to focus on in the next 2 to 5 years for prioritizing efforts and investments.

Scope of the Report

The research report segments the network transformation market into the following submarkets:

By Component:

- Solutions

- Services

By Solution:

- SDN & NFV

- Software

- Physical Appliances

- C-RAN

- Centralization

- Virtualization

- Network Automation

- 5G Networks

By Services:

- Professional Service

- Deployment and Provisioning

- Consulting

- Integration

- Transformation Optimization

- Wireless Infrastructure Management

- By Managed Service:

- Network Monetization

- Network Management

- Network Testing

- Network Audit

By Organization Size:

- SMEs

- Large Enterprises

By Vertical:

- Telecom

- Manufacturing

- Energy and Utilities

- IT

- Media and Entertainment

- Others

By Region:

- North America

- Europe

- APAC

- MEA

- Latin America

Available Customizations

With the given market data, MarketsandMarkets offers customizations as per the company�s specific needs. The following customization options are available for the report:

Geographic Analysis for Network Transformation Market

- Further breakdown of the US and Canada markets into solutions, services, organization sizes, and verticals.

- Further breakdown of the UK, Germany, and France markets into solutions, services, organization sizes, and verticals.

Company Information

- Detailed analysis and profiling of additional market players

MarketsandMarkets forecasts the global network transformation market size to grow from USD 6.01 Billion in 2017 to USD 66.86 Billion by 2022, at a Compound Annual Growth Rate (CAGR) of 61.9%, due to increase in the adoption of BYOD policy, rise in adoption of ITaaS and virtualization, and the collaboration among market players for the development and promotion of next-generation networking solutions.

The network transformation market is segmented on the basis of components (solutions and services), organization sizes, verticals, and regions. The solutions segment is further segmented into SDN & NFV, C-RAN, and Network Automation. The SDN & NFV solution segment is further segmented into Software and Physical Appliances. The C-RAN solution segment is further categorized into Centralization and Virtualization solutions.

The SDN & NFV solution segment is expected to hold the largest market size during the forecast period. SDN transforms the Wide Area Network (WAN) design by decoupling the control and data planes, centralizing network intelligence, and abstracting applications from the underlying network infrastructure. By leveraging SDN data centers, telecom operators can gain enhanced network programmability, automation, and control over their network. Moreover, SDN enhances the scalability and flexibility of WAN which further improves the network performance and availability. NFV is implemented by decoupling software and hardware as an abstraction of the network function.

The network transformation market is expected to witness a traction, due to the collaboration among market players for the development and promotion of next-generation networking solutions; and a growing adoption rate of ITaaS, BYOD policy, and virtualization. The network transformation reconstructs the network architecture based on data center-centric ICT infrastructure, where information is stored, processed, and exchanged as well as service processing and business transactions are conducted in data centers. Data center-centric virtualized infrastructure is the foundation of the future network architecture.

The global network transformation market is in the growing stage. One of the core parts of Network transformation is 5G Networks. They are in the development and testing phase. Leading telecom operators and technology players are testing various 5G networking solutions. The roadmap toward 5G comprises the common motive to support multiple access networks that are transparent to end-users. Multi-connectivity and aggregation solutions are the key ingredients for the development of 5G networks.

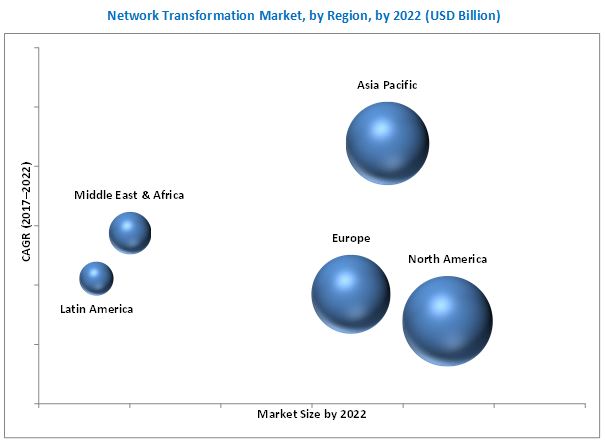

In 2017, North America is estimated to have the largest market share in the network transformation market owing to growing trends, such as BYOD; and increasing adoption of smart connected devices and IIoE. The US is the early adopter of new technologies. Enterprises in the country have adopted new technology solutions for enhancing the manageability and flexibility required for adding new network capabilities and capacity. Moreover, increased budgets and grants have encouraged various leading players to make significant investments in the region. Network transformation has seen vast applications across various verticals in the US. For instance, UBM Tech, a US-based global media company, has deployed network automation solutions to enhance the manageability and flexibility of its networking environment for its flagship network technology trade show, Interop ITX. Following the US, Canada is expected to have a major share in the network transformation market in North America. Canadian companies are improving and optimizing their business networks by utilizing network transformation solutions.

APAC is expected to witness growth at the highest rate, owing to the rapid development of the IT infrastructure and the adoption of new technologies, along with increased investments in large scale infrastructure and R&D projects by vendors in the APAC region. Europe, MEA, and Latin America are also adopting network transformation solutions at a significant pace.

Lack of skills and expertise in next-generation networking solutions is likely to be the main restraining factor for the growth of the network transformation market. However, the recent developments, new product launches, and acquisitions undertaken by the major market players are expected to boost the growth of the market.

The study measures and evaluates the major offerings and key strategies of the major market vendors, including Cisco, Juniper Networks, HPE, Huawei, IBM, Dell EMC, NEC, Intel, Nokia Networks, Ericsson, Samsung, FUJITSU, Ciena, Accenture, GENBAND, AT&T, Arista Networks, and 6WINDS. These companies have been at the forefront in offering reliable network transformation solutions to commercial clients across regions.

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 15)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Market Scope

1.4 Years Considered for the Study

1.5 Currency

1.6 Stakeholders

2 Research Methodology (Page No. - 18)

2.1 Research Data

2.1.1 Secondary Data

2.1.2 Primary Data

2.1.2.1 Breakdown of Primaries

2.1.2.2 Key Industry Insights

2.2 Market Size Estimation

2.3 Microquadrant Research Methodology

2.3.1 Microquadrant: Weightage Criteria

2.3.2 Quadrant Description

2.4 Research Assumptions

2.5 Limitations

3 Executive Summary (Page No. - 26)

4 Premium Insights (Page No. - 30)

4.1 Attractive Market Opportunities in the Network Transformation Market

4.2 Market, By Solution and Region, 2017

4.3 Lifecycle Analysis, By Region

4.4 Market, By Region, 2017 vs 2022

4.5 Market Investment Scenario

4.6 Market: Top 3 Verticals, 2017�2022

5 Market Overview (Page No. - 35)

5.1 Introduction

5.2 Market Dynamics

5.2.1 Drivers

5.2.1.1 Rapid Demand in Bandwidth Requirement

5.2.1.2 Increase in the Adoption of the Byod Policy

5.2.1.3 Collaboration Among Industry Leaders for the Development and Promotion of Next-Generation Networking Solutions

5.2.1.4 Rise in the Adoption of Itaas and Virtualization in the IT Industry

5.2.2 Restraints

5.2.2.1 Security Threats are Hampering the Adoption of Next-Generation Networking Solutions

5.2.2.2 Lack of Skills and Expertise in Next-Generation Networking Solutions

5.2.3 Opportunities

5.2.3.1 Adoption of Advanced Networking Solutions in SMEs

5.2.3.2 Investments in R&D and Positive Outcomes From the Testing Phase of 5G Networks

5.2.4 Challenges

5.2.4.1 Network Scalability is A Concern in Large Network Deployments

6 Network Transformation Market Analysis, By Component (Page No. - 40)

6.1 Introduction

6.2 Solutions

6.3 Services

7 Market Analysis, By Solution (Page No. - 44)

7.1 Introduction

7.2 SDN and NFV

7.2.1 Software

7.2.2 Physical Appliances

7.3 C-Ran

7.3.1 Centralization

7.3.2 Virtualization

7.4 Network Automation

7.5 5G Networks

8 Market Analysis, By Service (Page No. - 55)

8.1 Introduction

8.2 Professional Services

8.2.1 Deployment and Provisioning

8.2.2 Consulting

8.2.3 Integration

8.2.4 Transformation Optimization

8.2.5 Wireless Infrastructure Management

8.3 Managed Services

8.3.1 Network Monetization

8.3.2 Network Management

8.3.3 Network Testing

8.3.4 Network Audit

9 Market Analysis, By Organization Size (Page No. - 65)

9.1 Introduction

9.2 Large Enterprises

9.3 Small and Medium-Sized Enterprises

10 Network Transformation Market Analysis, By Vertical (Page No. - 69)

10.1 Introduction

10.2 Manufacturing

10.3 Information Technology (IT)

10.4 Telecom

10.5 Media and Entertainment

10.6 Energy and Utilities

10.7 Others

11 Geographic Analysis (Page No. - 77)

11.1 Introduction

11.2 North America

11.3 Europe

11.4 Asia Pacific

11.5 Middle East and Africa

11.6 Latin America

12 Company Profiles (Page No. - 101)

(Overview, Strength of Product Portfolio, Business Strategy Excellence, Recent Developments)*

12.1 Cisco Systems

12.2 Juniper Networks

12.3 HPE

12.4 Huawei

12.5 IBM

12.6 NEC

12.7 Intel

12.8 Nokia Networks

12.9 Ericsson

12.10 Fujitsu

12.11 Accenture

12.12 Mavenir

*Details on Overview, Strength of Product Portfolio, Business Strategy Excellence, Recent Developments Might Not Be Captured in Case of Unlisted Companies.

13 Appendix (Page No. - 143)

13.1 Industry Experts

13.2 Discussion Guide

13.3 Knowledge Store: MarketsandMarkets� Subscription Portal

13.4 Introducing RT: Real-Time Market Intelligence

13.5 Available Customizations

13.6 Related Reports

13.7 Author Details

List of Tables (79 Tables)

Table 1 Evaluation Criteria

Table 2 Network Transformation Market Size and Growth Rate, 2017�2022 (USD Million, Y-O-Y %)

Table 3 Market Size, By Component, 2017�2022 (USD Million)

Table 4 Market Size, By Solution, 2015�2022 (USD Million)

Table 5 Solutions: Market Size, By SDN and NFV, 2015�2022 (USD Million)

Table 6 Software Market Size, By Region, 2015�2022 (USD Million)

Table 7 Physical Appliances Market Size, By Region, 2015�2022 (USD Million)

Table 8 Solutions: Market Size, By C-Ran, 2015�2022 (USD Million)

Table 9 Centralization Market Size, By Region, 2015�2022 (USD Million)

Table 10 Virtualization Market Size, By Region, 2015�2022 (USD Million)

Table 11 Network Automation: Market Size, By Region, 2015�2022 (USD Million)

Table 12 Network Transformation Market Size, By Service, 2015�2022 (USD Million)

Table 13 Professional Services: Market Size, By Type, 2015�2022 (USD Million)

Table 14 Deployment and Provisioning Market Size, By Region, 2015�2022 (USD Million)

Table 15 Consulting Market Size, By Region, 2015�2022 (USD Million)

Table 16 Integration Market Size, By Region, 2015�2022 (USD Million)

Table 17 Transformation Optimization Market Size, By Region, 2015�2022 (USD Million)

Table 18 Wireless Infrastructure Management Market Size, By Region, 2015�2022 (USD Million)

Table 19 Managed Services: Market Size, By Type, 2015�2022 (USD Million)

Table 20 Network Monetization Market Size, By Region, 2015�2022 (USD Million)

Table 21 Network Management Market Size, By Region, 2015�2022 (USD Million)

Table 22 Network Testing Market Size, By Region, 2015�2022 (USD Million)

Table 23 Network Audit Market Size, By Region, 2015�2022 (USD Million)

Table 24 Network Transformation Market Size, By Organization Size, 2015�2022 (USD Million)

Table 25 Large Enterprises: ormation Market Size, By Region, 2015�2022 (USD Million)

Table 26 Small and Medium-Sized Enterprises: Market Size, By Region, 2015�2022 (USD Million)

Table 27 Market Size, By Vertical, 2015�2022 (USD Million)

Table 28 Manufacturing: Market Size, By Region, 2015�2022 (USD Million)

Table 29 Information Technology: Market Size, By Region, 2015�2022 (USD Million)

Table 30 Telecom: Market Size, By Region, 2015�2022 (USD Million)

Table 31 Media and Entertainment: Market Size, By Region, 2015�2022 (USD Million)

Table 32 Energy and Utilities: Market Size, By Region, 2015�2022 (USD Million)

Table 33 Others: Market Size, By Region, 2015�2022 (USD Million)

Table 34 Market Size, By Region, 2015�2022 (USD Million)

Table 35 North America: Network Transformation Market Size, By Component, 2015�2022 (USD Million)

Table 36 North America: Market Size, By Solution, 2015�2022 (USD Million)

Table 37 North America: Market Size, By SDN and NFV, 2015�2022 (USD Million)

Table 38 North America: Market Size, By C-Ran, 2015�2022 (USD Million)

Table 39 North America: Market Size, By Service, 2015�2022 (USD Million)

Table 40 North America: Market Size, By Professional Service, 2015�2022 (USD Million)

Table 41 North America: Market Size, By Managed Service, 2015�2022 (USD Million)

Table 42 North America: Market Size, By Organization Size, 2015�2022 (USD Million)

Table 43 North America: Market Size, By Vertical, 2015�2022 (USD Million)

Table 44 Europe: Network Transformation Market Size, By Component, 2015�2022 (USD Million)

Table 45 Europe: Market Size, By Solution, 2015�2022 (USD Million)

Table 46 Europe: Market Size, By SDN and NFV, 2015�2022 (USD Million)

Table 47 Europe: Market Size, By C-Ran, 2015�2022 (USD Million)

Table 48 Europe: Market Size, By Service, 2015�2022 (USD Million)

Table 49 Europe: Market Size, By Professional Service, 2015�2022 (USD Million)

Table 50 Europe: Market Size, By Managed Service, 2015�2022 (USD Million)

Table 51 Europe: Market Size, By Organization Size, 2015�2022 (USD Million)

Table 52 Europe: Market Size, By Vertical, 2015�2022 (USD Million)

Table 53 Asia Pacific: Network Transformation Market Size, By Component, 2015�2022 (USD Million)

Table 54 Asia Pacific: Market Size, By Solution, 2015�2022 (USD Million)

Table 55 Asia Pacific: Market Size, By SDN and NFV, 2015�2022 (USD Million)

Table 56 Asia Pacific: Market Size, By C-Ran, 2015�2022 (USD Million)

Table 57 Asia Pacific: Market Size, By Service, 2015�2022 (USD Million)

Table 58 Asia Pacific: Market Size, By Professional Service, 2015�2022 (USD Million)

Table 59 Asia Pacific: Market Size, By Managed Service, 2015�2022 (USD Million)

Table 60 Asia Pacific: Market Size, By Organization Size, 2015�2022 (USD Million)

Table 61 Asia Pacific: Market Size, By Vertical, 2015�2022 (USD Million)

Table 62 Middle East and Africa: Network Transformation Market Size, By Component, 2015�2022 (USD Million)

Table 63 Middle East and Africa: Market Size, By Solution, 2015�2022 (USD Million)

Table 64 Middle East and Africa: Market Size, By SDN and NFV, 2015�2022 (USD Million)

Table 65 Middle East and Africa: Market Size, By C-Ran, 2015�2022 (USD Million)

Table 66 Middle East and Africa: Market Size, By Service, 2015�2022 (USD Million)

Table 67 Middle East and Africa: Market Size, By Professional Service, 2015�2022 (USD Million)

Table 68 Middle East and Africa: Market Size, By Managed Service, 2015�2022 (USD Million)

Table 69 Middle East and Africa: Market Size, By Organization Size, 2015�2022 (USD Million)

Table 70 Middle East and Africa: Market Size, By Vertical, 2015�2022 (USD Million)

Table 71 Latin America: Network Transformation Market Size, By Component, 2015�2022 (USD Million)

Table 72 Latin America: Market Size, By Solution, 2015�2022 (USD Million)

Table 73 Latin America: Market Size, By SDN and NFV, 2015�2022 (USD Million)

Table 74 Latin America: Market Size, By C-Ran, 2015�2022 (USD Million)

Table 75 Latin America: Market Size, By Service, 2015�2022 (USD Million)

Table 76 Latin America: Market Size, By Professional Service, 2015�2022 (USD Million)

Table 77 Latin America: Market Size, By Managed Service, 2015�2022 (USD Million)

Table 78 Latin America: Market Size, By Organization Size, 2015�2022 (USD Million)

Table 79 Latin America: Network Transformation Market Size, By Vertical, 2015�2022 (USD Million)

List of Figures (47 Figures)

Figure 1 Network Transformation Market: Market Segmentation

Figure 2 Market: Research Design

Figure 3 Data Triangulation

Figure 4 Market Size Estimation Methodology: Bottom-Up Approach

Figure 5 Market Size Estimation Methodology: Top-Down Approach

Figure 6 Market: Assumptions

Figure 7 North America is Estimated to Have the Largest Market Share in 2017

Figure 8 Segments Dominating the Global Network Transformation Market, 2017

Figure 9 Solutions Segment is Estimated to Have A Larger Market Share in 2017

Figure 10 Rapid Demand for Bandwidth and Collaboration Among Market Leaders are Driving the Network Transformation Market

Figure 11 SDN and NFV Solution, and North America are Estimated to Have the Largest Market Shares in 2017

Figure 12 Asia Pacific is Expected to Grow at A Significant Pace During the Forecast Period

Figure 13 North America is Expected to Have the Largest Market Size During the Forecast Period

Figure 14 Asia Pacific is Expected to Emerge as the Best Market for Investments in the Next 5 Years

Figure 15 Telecom, Manufacturing, and Energy and Utilities Verticals are Expected to Witness Impressive Growth Rates During the Forecast Period

Figure 16 Network Transformation Market: Drivers, Restraints, Opportunities, and Challenges

Figure 17 Solutions Segment is Expected to Dominate the Market During the Forecast Period

Figure 18 North America is Expected to Dominate the Solutions Segment During the Forecast Period

Figure 19 Asia Pacific is Expected to Grow at the Highest CAGR in the Services Segment During the Forecast Period

Figure 20 SDN and NFV Solution is Expected to Dominate the Network Transformation Market During the Forecast Period

Figure 21 Software Solution is Expected to Hold A Larger Market Size in the SDN and NFV Segment During the Forecast Period

Figure 22 Asia Pacific is Expected to Grow at the Highest CAGR in the Software Segment of the SDN and NFV Solution During the Forecast Period

Figure 23 Virtualization is Expected to Hold A Larger Market Size in the C-Ran Segment During the Forecast Period

Figure 24 MEA is Expected to Grow at the Highest CAGR in the Centralization Segment During the Forecast Period

Figure 25 North America is Expected to Hold the Largest Market Size in the Network Automation Segment During the Forecast Period

Figure 26 Professional Services Segment is Expected to Hold A Larger Market Size in 2017

Figure 27 Deployment and Provisioning Service is Expected to Dominate the Professional Services Segment During the Forecast Period

Figure 28 Network Audit Service is Expected to Grow at the Highest CAGR in the Managed Services Segment During the Forecast Period

Figure 29 Large Enterprises Segment is Expected to Hold A Larger Market Size During the Forecast Period

Figure 30 North America is Expected to Dominate the Large Enterprises Segment During the Forecast Period

Figure 31 Telecom Vertical is Expected to Hold the Largest Market Size in 2022

Figure 32 Asia Pacific is Expected to Lead in the Manufacturing Vertical in 2022

Figure 33 Asia Pacific is Expected to Grow at the Highest CAGR in the Media and Entertainment Vertical During the Forecast Period

Figure 34 Asia Pacific is Expected to Exhibit the Highest CAGR in the Network Transformation Market During the Forecast Period

Figure 35 North America: Market Snapshot

Figure 36 Network Automation Solution is Expected to Exhibit the Highest CAGR in the Solutions Segment During the Forecast Period

Figure 37 Asia Pacific: Market Snapshot

Figure 38 Cisco Systems: Company Snapshot

Figure 39 Juniper Networks: Company Snapshot

Figure 40 HPE: Company Snapshot

Figure 41 Huawei: Company Snapshot

Figure 42 IBM: Company Snapshot

Figure 43 NEC: Company Snapshot

Figure 44 Intel: Company Snapshot

Figure 45 Ericsson: Company Snapshot

Figure 46 Fujitsu: Company Snapshot

Figure 47 Accenture: Company Snapshot

Growth opportunities and latent adjacency in Network Transformation Market