North American Crop Protection Chemicals Market & Latin American Crop Protection Chemicals Market by Types (Herbicides, Fungicides, Insecticides, Bio-pesticides and Adjuvants), by Crop Types, by Geography: Trends and Forecast to 2018

[398 Pages Report] The North American crop protection chemicals market covers various types of products being used in the farms to safeguard the crops, by controlling the population of organisms considered harmful or those that can potentially damage or adversely affect the growth of crops. Crop protection chemicals are mainly divided into herbicides, insecticides and fungicides. Pesticides include both synthetic pesticides and bio-based pesticides, are the largest market segment owing to their wide-spread use in bulk quantities. Adjuvants are essentially pharmacological or immunological agents used to modify or enhance the effect of other vaccines and drugs.

Insecticides are widely used because insects and parasites cause maximum damage to the crops during cultivation. Insecticides are used in large volume and they show their action for a longer period of time as compared to others. But excessive use of any pesticide results in the development of chemical toxicity for humans, animals, and environment owing to soil leaching and water contamination. Overall, it is essential to use crop protection pesticides in appropriate quantity and time to minimize their adverse effects and to bring to maximum benefits. The North and Latin American crop protection chemicals market, in terms of active ingredient volume was estimated at 1,064.1 KT in 2011 and is expected to reach 1,322.5 KT by 2018.

The North American crop protection chemicals market has been divided into patented and generic pesticides. Almost over 67% of the market share belongs to patented or proprietary active ingredients, while 33% of this market is generic. The proprietary pesticides market has been built with a strong focus on North American crop protection chemicals based on stringent regulations, driven by the U.S. and European standards. In such situation, most of the major global players are focusing to slim down their production capacity of low-revenue ($million) off-patent proprietary products.

The basic notion behind taking patents for the agrochemicals is to encourage innovation akin to the pharmaceutical industry as well as to get rid off the problem of piracy and counterfeit products. Moving forward, many molecules are likely to become free from patent and become open for generic players.

This report estimates the market size of the global, North and Latin American crop protection chemicals market both in terms of active ingredient volume as well as revenue. The market has been further segmented on the basis of crop types such as cereals, grains, oilseeds, and vegetables as well as by sub-segmentation of insecticides, fungicides, and herbicides such as glyphosate, atrazine, and 2,4-D. This segmentation is given for major regions and key countries in those regions. Market drivers, restraints and challenges, raw material, and product price trends are discussed in detail. Market share by participants for the overall market is discussed in detail in the report. We have also profiled leading players of this industry including Bayer CropScience (Germany), BASF (Germany), Monsanto (U.S.), and Dow Agrosciences (U.S.).

Customer Interested in this report also can view

-

Crop Protection Chemicals Market By Types (Herbicides, Fungicides, Insecticides, Bio-Pesticides and Adjuvants), By Crop Types, By Geography: Global Trends and Forecast To 2018

-

Asia-Pacific Crop Protection Chemicals Market by Types (Herbicides, Fungicides, Insecticides, Bio-pesticides and Adjuvants), by Crop Types, by Geography: Trends and Forecast to 2018

-

European Crop Protection Chemicals Market by Types (Herbicides, Fungicides, Insecticides, Bio-pesticides and Adjuvants), by Crop Types, by Geography: Trends and Forecast to 2018

North & Latin American Crop protection chemicals: $27,806.4 million market by 2018, signifies a firm CAGR of 4.4% and 6.3% respectively

North America has traditionally been a high consumer of crop protection chemicals. However, in recent years, regulatory framework, controlled by the EPA and USDA has become highly stringent on the registration and commercialization of pesticides. Owing to the growing demand for animal feed and increasing use of corn for renewable chemicals and bio-fuels, arable land has been decreasing since 2005.

Latin America is the emerging agricultural powerhouse, growing at a rapid pace above the global growth average. Growth in this region is significantly contributed by the growth in Brazil and Argentina, which are the worlds most potent agricultural producers and is expected to grow well above the regional average.

The North and Latin American crop protection chemicals market, in terms of active ingredient volume was estimated at 1,064.1 KT in 2011 and is expected to reach 1,322.5 KT by 2018. Growth in revenue is expected to be higher than volume, owing to the increasing cost of pesticides. U.S. is the most dominant market in North America, accounting for over 80% of the total North American crop protection chemicals demand in 2010. Due to the expansion of farmlands and increasing use of pesticides, crop protection chemicals market in Brazil is moving at a rapid pace to become the most desirable growth market for crop protection chemical companies.

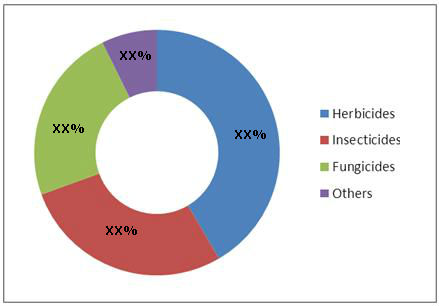

NORTH & LATIN AMERICAN CROP PROTECTION CHEMICALS MARKET REVENUE, BY TYPES, 2012

Source: MarketsandMarkets Analysis

North America Crop protection chemicals market dominates the global herbicide market and has the largest market share in terms of volume and revenue. Europe is the second largest market for herbicides. North America is a mature market and is dominated by a few major players. To survive intense competition, companies in this region are focused on new product development.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table Of Contents

1 Introduction (Page No. - 14)

1.1 Key Take-Aways

1.2 Report Description

1.3 Research Methodology

1.3.1 Market Size

1.3.2 Key Data Points Taken From Secondary Sources

1.3.3 Key Data Points Taken From Primary Sources

1.3.4 Assumptions Made For This Report

1.4 Stake Holders

1.5 Key Questions Answered

2 Executive Summary (Page No. - 20)

3 Market Overview (Page No. - 22)

3.1 Introduction

3.1.1 Types Of Pesticides On The Basis Of Mode Of Action

3.1.1.1 Contact Pesticides

3.1.1.2 Residual Pesticides

3.1.1.3 Systemic Pesticides

3.2 Value Chain Analysis

3.3 Winning Imperatives

3.3.1 Successful Introduction Of Pesticides Coming Off-Patents

3.4 Burning Issues

3.4.1 Battle Of �Patented� Vs �Generic� Pesticides

3.4.2 Ban On Endosulfan

3.5 Drivers

3.5.1 Crop Protection � Key To Food Security Of Ever Growing Population Of The World

3.5.2 Change In Farming Practices & Technology

3.5.3 Shrinking Arable Land

3.5.4 Growing Demand For Crop Protection Chemicals In South &Central America

3.6 Restraints

3.6.1 Use Of Bacillus Thuringiensis (BT), Genetically Modified Seeds/Crops & Advancement In Biotechnology

3.6.2 Growing Environmental Concerns

3.7 Opportunities

3.7.1 Rapid Growth In The Bio-Pesticides Market

3.7.2 Developing Countries Expected To Post Strong Growth

3.8 Porter�s Five Force Analysis

3.8.1 Bargaining Power Of Suppliers

3.8.2 Bargaining Power Of Buyers

3.8.3 Threat Of New Entrants

3.8.4 Threat Of Substitutes

3.8.5 Degree Of Competition

3.9 North & Latin American Patent Analysis

4 North & Latin American Crop Protection Chemicals Market, By Types (Page No. - 51)

4.1 Pesticides

4.2 Synthetic Pesticides

4.3 North America

4.4 Latin America

4.4.1 Herbicides

4.4.1.1 Glyphosate

4.4.1.2 Atrazine

4.4.1.3 Acetochlor

4.4.1.4 2,4-D

4.4.1.4.1 Metolachlor

4.4.1.4.2 Imazethapyr

4.4.2 Insecticides

4.4.2.1 Chlorpyrifos

4.4.2.2 Malathion

4.4.2.3 Pyrethrins & Pyrethroids

4.4.2.3.1 Types Of Pyrethroids

4.4.2.3.1.1 Bifenthrin

4.4.2.3.1.2 Cypermethrin

4.4.2.3.1.3 Deltamethrin

4.4.2.3.1.4 Lambda-Cyhalothrin

4.4.2.3.1.5 Permethrin

4.4.2.3.1.6 Resmethrin

4.4.2.3.1.7 Tetramethrin

4.4.2.3.1.8 Tralomethrin

4.4.2.4 Carbaryl

4.4.2.5 Others

4.4.2.5.1 Diazinon

4.4.2.5.2 Terbufos

4.4.2.5.3 Methoxychlor

4.4.3 Fungicides

4.4.3.1 Mancozeb

4.4.3.2 Chlorothalonil

4.4.3.3 Metalaxyl

4.4.3.4 Strobilurin

4.5 Biopesticides

4.5.1 Pros & Cons Of Biopesticide

4.5.2 North America

4.5.3 Latin America

4.6 Ajuvants

5 North & Latin American Crop Protection Chemicals Market, By Crop Types (Page No. - 99)

5.1 Introduction

5.2 Cereals & Grains

5.3 Oil Seeds

5.4 Fruits & Vegetables

5.5 Others

6 North & Latin American Crop Protection Chemicals Market, By Country (Page No. - 110)

6.1 U.S.

6.2 Canada

6.3 Brazil

7 Competitive Landscape (Page No. - 128)

7.1 Introduction

7.2 Agreements, Partnerships, Joint Ventures & Collaborations: Most Preferred Strategic Approach

7.3 Maximum Developments In 2011

7.4 Monsanto & FMC Corporation: Most Active Companies

8 Company Profiles (Overview, Financials, Products & Services, Strategy, And Developments)* (Page No. - 167)

8.1 American Vanguard Corporation

8.2 Chemtura Corporation

8.3 Cleary Chemical Corporation

8.4 Dow Chemical Company

8.5 Drexel Chemical Company

8.6 E.I. Dupont DE Nemours & Company

8.7 FMC Corporation

8.8 Monsanto Company

8.9 Mosaic

8.10 Wilbur-Ellis Company

*Details On Overview, Financials, Product & Services, Strategy, And Developments Might Not Be Captured In Case Of Unlisted Companies.

Appendix (Page No. - 215)

North & Latin America Patents

List Of Tables (57 Tables)

Table 1 Types Of Pesticides

Table 2 Active Substances - The Patents Of Which Will Expire Between 2013 � 2017

Table 3 Endosulfan & Alternatives � Cost Comparison,By Products ($)

Table 4 North America: Agricultural Area,2007 � 2011 (Million Hectares)

Table 5 Technology Penetration, By Revenue, 2001 � 2010

Table 6 GM Crops & Bio-Pesticides: Substitution Potential Of Synthetic Pesticides In Various Crops

Table 7 Major Pesticides & Crops

Table 8 North American Crop Protection Chemicals Market Revenue, By Types, 2011 � 2018 ($Million)

Table 9 North American Crop Protection Chemicals Market Volume,By Types, 2011 � 2018 (KT)

Table 10 Latin America: Crop Protection Chemicals Market Revenue,By Types, 2011 � 2018 ($Million)

Table 11 Latin America: Crop Protection Chemicals Market Volume,By Types, 2011 � 2018 (KT)

Table 12 Global Glyphosate Market, By Volume (KT) & By Revenue ($Million), 2009 � 2016

Table 13 Global Atrazine Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 14 Global Acetochlor Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 15 Global 2,4-D Market, By Volume (KT) & By Revenue ($Million),2011 � 2018

Table 16 Global Other Herbicides Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 17 Global Chlorpyrifos Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 18 Global Malathion Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 19 Global Pyrethrins And Pyrethroids Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 20 Global Carbaryl Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 21 Other Insecticides Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 22 Global Mancozeb Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 23 Global Chlorothalonil Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 24 Global Metalaxyl Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 25 Global Strobilurin Market, By Volume (KT) & By Revenue ($Million), 2011 � 2018

Table 26 New Biopesticide Active Ingredients Approved In 2012

Table 27 Upcoming Biopesticide Active Ingredients, 2012 � 2013

Table 28 Pros & Cons Of Biopesticide Active Ingredients In Comparison With Conventional Pesticides

Table 29 North America: Biopesticides Market Revenues, By Countries, 2011 � 2018 ($Million)

Table 30 Latin America: Biopesticides Market Revenues, By Countries, 2011 � 2018 ($Million)

Table 31 Adjuvants: Types & Features

Table 32 Popular Oilseeds & Applications

Table 33 U.S.: Crop Protection Chemicals Market Revenue, By Types, 2011 � 2018 ($Million)

Table 34 U.S,: Crop Protection Chemicals Market Volume, By Types, 2011 � 2018 (KT)

Table 35 U.S.: Crop Protection Chemicals Market Revenue, By Crop Types, 2011 � 2018 ($Million)

Table 36 U.S.: Crop Protection Chemicals Market Revenue, By Crop Types, 2011 � 2018 (KT)

Table 37 Canada: Crop Protection Chemicals Market Revenue, By Types, 2011 � 2018 ($Million)

Table 38 Canada: Crop Protection Chemicals Market Volume, By Types, 2011 � 2018 (KT)

Table 39 Canada: Crop Protection Chemicals Market Revenue, By Crop Types, 2011 � 2018 ($Million)

Table 40 Canada: Crop Protection Chemicals Market Revenue, By Crop Types, 2011 � 2018 (KT)

Table 41 Brazil: Crop Protection Chemicals Market Revenue, By Types, 2011 � 2018 ($Million)

Table 42 Brazil: Crop Protection Chemicals Market Volume, By Types, 2011 � 2018 (KT)

Table 43 Brazil: Crop Protection Chemicals Market Revenue, By Crop Types, 2011 � 2018 ($Million)

Table 44 Brazil: Crop Protection Chemicals Market Revenue, By Crop Types, 2011 � 2018 (KT)

Table 45 Mergers & Acquisitions, 2008 � 2011

Table 46 Agreements, Partnerships, Collaborations & Joint Ventures, 2009 � 2013

Table 47 New Product Launches, 2009 � 2013

Table 48 Investment, Expansion & Other Developments, 2009 � 2013

Table 49 American: Total Revenue, By Business Segments,2011 � 2012 ($Million)

Table 50 Chemtura: Total Revenue, By Business Segments,2011 � 2012 ($Million)

Table 51 Chemtura: Total Revenue, By Geography,2011 � 2012 ($Million)

Table 52 Dow Chemical: Total Revenue, By Business Segments,2011 � 2012 ($Million)

Table 53 Dow Chemical: Total Revenue, By Geography,2011 � 2012 ($Million)

Table 54 Dupont: Total Market Revenue, By Segments,2011 � 2012 ($Million)

Table 55 Dupont: Total Revenue, By Geography, 2011 - 2012 ($Million)

Table 56 FMC: Total Revenue, By Business Segments,2011 � 2012 ($Million)

Table 57 Monsanto: Total Revenue, By Business Segments,2011 � 2012 ($Million)

List Of Figures (23 Figures)

Figure 1 Research Methodology

Figure 2 North American Crop Protection Chemicals Market Revenues, By Types, 2012

Figure 3 Value Chain Analysis Of Crop Protection Chemicals Market

Figure 4 Sales Of Active Ingredients Coming Off-Patents,By Types, 2012 ($Million)

Figure 5 Impact Of Major Drivers And Restrains On Global Crop Protection Chemicals Market, 2011 � 2018

Figure 6 Arableland, 1950 � 2020 (Hectares/Person)

Figure 7 Arable Land, By Countries (Hectares/Person)

Figure 8 Porter�s Five Force Analysis

Figure 9 Patent Trends In North & Latin America, 2009 � 2013

Figure 10 Patent Analysis, By Companies, 2009 � 2013

Figure 11 Global Crop Protection Chemicals Market Volume,By Types, 2012

Figure 12 North America Adjuvants Market Revenue,2011 � 2018 ($Million)

Figure 13 Latin America Adjuvants Market Revenue, By Geography,2011 � 2018 ($Million)

Figure 14 North & Latin American Crop Protection Chemicals Market, By Crop Types, 2012 ($Million)

Figure 15 Major Cereals & Grians Production In North America,2011 (�000) Tons

Figure 16 Major Cereal & Grain Production In Latin America, 2011 (�000) Tons

Figure 17 Major Oilseed Production In North America, 2011 (�000) Tons

Figure 18 Major Oilseed Production In Latin America, 2011 (�000) Tons

Figure 19 Major Fruits & Vegetables Production In North America,By Countries, 2011 (�000) Tons

Figure 20 Major Fruits & Vegetables Production In Latin America,2011, (�000) Tons

Figure 21 North & Latin America Crop Protection Chemicals Market,By Growth Strategies, 2009 � 2013

Figure 22 North & Latin America Crop Protection Chemicals Market Developments, By Growth Strategies, 2009 � 2013

Figure 23 North & Latin America Crop Protection Chemicals Market Growth Strategies, By Companies, 2009 � 2013

Growth opportunities and latent adjacency in North American Crop Protection Chemicals Market