Photonic Integrated Circuit (IC) & Quantum Computing Market (2012 � 2022): By Application (Optical Fiber Communication, Optical Fiber Sensors, Biomedical); Components (Lasers, Attenuators); Raw Materials (Silica on Silicon, Silicon on Insulator)

Photonic Integrated circuits (PIC) is a breakthrough technology as it uses photons (smallest unit of light) as the data carrier instead of electrons (smallest unit of electricity) used in electronic ICs. As light travels at very high speeds, PIC technology is widely used to transfer huge amounts of data at a very high speed. Thus the PIC based products are primarily deployed in the field of optical fiber communications. The Photonic integrated circuits market is growing at a phenomenal rate as it provides significant improvements in system size, power consumption, reliability and cost. The development of silicon photonics technology has helped in large scale manufacturing of PICs at low cost. Also current leading players have developed monolithically integrated Indium Phosphide (InP) based PICs that can integrate more than 600 components/functions in a single chip. Thus there is a huge competition in the market as each player is trying to innovate PIC based products which would be able to integrate large amounts of functions/components at low cost.

Optical sensors application is the other promising application in this market. It is used in fields like defense, aerospace, energy, transportation, medicine and other emerging fields. Quantum computing is another application of PICs which is forecasted to be commercialized in 2017. This technology is expected to completely revolutionize the computing industry. PICs are also used in biomedical field. InP-based application specific photonic ICs are being used for the diagnostic analysis of opaque skin tissue. The technique principally used here is Optical Coherence Tomography (OCT) or Raman Scatterometry.

At present North America has the largest market for PIC based products, especially in data centers and WAN applications of optical fiber communications. However, APAC is the largest player in the access network application of optical fiber communications right now. North America is the leader in a PIC market with 49% market share however it is estimated that APAC will emerge as the market leader by 2022 growing at a CAGR of 35.9% from 2012 to 2022.

The report covers recent developments in the PIC industry like NeoPhotonics (U.S.) acquiring Santur Corporation (U.S.) in October 2011 and the acquisition of Opnext (U.S.) by Oclaro(U.S.). Several other acquisitions, mergers, new product launch, agreements etc. have taken place recently and are discussed in the report.

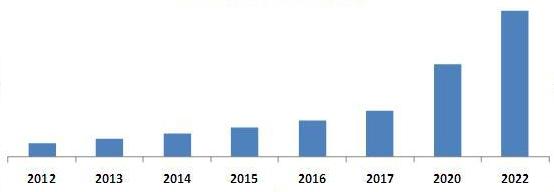

The growth of the Photonic IC market is expected to be phenomenal with the revenue growth from $150.4 million in 2012 to $1,547.6 million by 2022, at an estimated CAGR of 26.3% from 2012 to 2022. The major players in the PICs industry are Infinera Corporation (U.S.), NeoPhotonics Corporation (U.S.), Oclaro (U.S.), Luxtera (U.S.), Kotura (U.S.), OneChip Photonics (CA) etc These players have played a great role in changing the market dynamics. For example Infinera has introduced 500 Gb/s PICs used in long haul flex coherent super channels. The main features of this product are simplicity, scalability, efficiency and reliability. On the other hand Neophotonics has developed an Optical Line Terminal Transceiver using Photonic Integrated Circuit Technology which is designed to lower the overall cost of FTTH network installation.

Scope of the report

This research report categorizes the global PIC market, based on integration, raw materials and applications; it also covers the forecasted revenue from 2012 to 2022 and future applications of PIC. It describes the deployments of PIC technology in various regions. The report describes the application mapping of the PIC market with respect to the growth potential and adoption by the users.

On the basis of Integration

The global PIC market on the basis of integration consists of module, hybrid and monolithic PICs. The report covers the market of PICs based on these integration techniques across North America, Europe, Asia-Pacific, and ROW.

On the basis of Raw Materials

The PIC market has also been segregated based on raw materials used to fabricate PICs such as Lithium Niobate, Silica on Silicon, silicon on Insulator, Indium Phosphide and allium Arsenide.

On the basis of application areas

Application areas of Photonic Integrated Circuit have been categorized into Optical Fiber communication, optical fiber sensors, Biomedical and quantum computing. The market trend for these applications is discussed

On the basis of geography

Geographical analysis covers North America, Europe, Asia-Pacific, and ROW.

Photonic integrated circuit (PIC) is an innovative technology which simplifies the optical system design, reduces the size, power consumption and also improves reliability. Photonic integrated circuit is conceptually very similar to an electronic IC. It is on the edge of computing with the advent of smaller, not expensive optical interconnects, covering fields from communications and security to biomedicine and entertainment.

Optical fiber communication is the major application of photonic integrated circuit. The massive data generated by bandwidth heavy multimedia content, growing number of users, is creating a need for network to support gigabit transmission speeds. The demand of high speed communication is driving the market of optical fiber communication. Photonic IC is also being used in optical sensor. The sensing photonic integrated circuit is powered by fiber or free space enabling applications requiring wireless operation of the sensing-PIC, as in wind turbines, airplane propellers or rotor blades of helicopters. Such applications make use of receivers and transmitters which are specially designed for free-space optical communication. Photonic ICs are also being used in biomedical for the diagnostic analysis of opaque skin tissue.

Indium Phosphide is one of the major raw materials used in photonic ICs. Indium Phosphide has the capability of cost-effective mass production using standard high-yield, batch semiconductor manufacturing processes; whereas silicon based Photonic IC has the highest growth potential as it is easy to fabricate and multiple function can be integrated in the chip. Silicon based photonic IC is easy to manufacture as the existing foundries for electronic ICs can be utilized with a small modification.

The report illuminates the reader of how it is different from electronic processor. The major components and application of photonic processors are being discussed. The report also highlights the development of prototypes of photonic processors. For Example H.P (U.S) is developing a photonic processor which would be commercialized by 2017 and Intel (U.S) has developed a prototype of photonic processor capable of processing data at a speed of 1 terabit/second.

This report also deals with all the driving factors, restraints, and opportunities with respect to the PIC market, which are helpful in identifying trends and key success factors for the industry. It also profiles companies active in the field of PIC technology. The report provides the competitive landscape of the players, which covers key growth strategies followed by all the major players. It also highlights the winning imperatives and burning issues pertaining to the PIC industry. It does analyze the PIC technology market with the help of Porter�s five-force model.

Hybrid, monolithic and module are the three integration technique of photonic integrated circuit. Currently hybrid and module is the major integration technology used in photonic ICs but in the coming ten year it is expected that monolithic will have highest growth potential as it has the ability to integrate medium and large scale PICs. Some of the major players in the photonic integrated circuit market are Infinera (U.S.), Alcatel Liucent (U.S.), Neophotonics (U.S.), JDSU (U.S.) Kotura (U.S.), and many more

Source: MarketsandMarkets Analysis

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 KEY TAKE-AWAYS

1.2 REPORT DESCRIPTION

1.3 MARKETS COVERED

1.4 STAKEHOLDERS

1.5 RESEARCH METHODOLOGY

1.5.1 MARKET SIZE

1.5.2 KEY DATA POINTS TAKEN FROM PRIMARY SOURCES

1.5.3 ASSUMPTIONS MADE FOR THIS REPORT

1.5.4 LIST OF COMPANIES COVERED DURING STUDY

2 EXECUTIVE SUMMARY

3 MARKET OVERVIEW

3.1 INTRODUCTION

3.2 MARKET DEFINITION

3.3 EVOLUTION AND HISTORY OF PHOTONIC ICS (PICS)

3.4 ADVANTAGES OF PHOTONIC ICS OVER CONVENTIONAL ICS

3.5 MARKET DYNAMICS

3.5.1 DRIVERS

3.5.1.1 COST REDUCTION

3.5.1.2 SIZE REDUCTION

3.5.1.3 INCREASED FUNCTIONALITY

3.5.1.4 HIGHER POWER EFFICIENCY

3.5.2 RESTRAINTS

3.5.2.1 LACK OF DIGITIZATION

3.5.2.2 LACK OF STANDARDIZATION IN THE COMMON FABRICATION AND PROCESS TECHNIQUES

3.5.3 OPPORTUNITIES

3.5.3.1 PHOTONIC COMPUTING

3.5.4 BURNING ISSUE

3.5.4.1 LACK OF FOUNDRIES

3.5.5 WINNING IMPERATIVES

3.5.5.1 PHOTONS AS THE DATA CARRIER

3.6 PORTER�S FIVE FORCES MODEL

3.6.1 INTENSITY OF THE RIVALRY

3.6.2 THREAT OF NEW ENTRANTS

3.6.3 THREAT OF SUBSTITUTES

3.6.4 BARGAINING POWER OF SUPPLIERS

3.6.5 BARGAINING POWER OF CUSTOMERS

4 PHOTONIC PROCESSORS

4.1 ABOUT PHOTONIC PROCESSOR

4.2 PHOTONIC PROCESSORS: OPTICAL VS ELECTRONIC PROCESSORS

4.3 FUTURE APPLICATIONS OF PHOTONIC PROCESSORS

4.3.1 PHOTONIC COMPUTING

4.3.1.1 ADVANTAGES OF PHOTONIC COMPUTING

4.4 COMPONENTS OF PHOTONIC PROCESSORS

4.4.1 OPTICAL TRANSISTOR

4.4.2 OPTICAL GATE AND SWITCH

4.4.2.1 OPERATION

4.4.2.2 TYPES OF OPTICAL SWITCHES

4.4.2.3 USES OF OPTICAL SWITCHES

4.4.3 HOLOGRAPHIC MEMORY

4.4.3.1 WORKING PRINCIPLE OF HOLOGRAPHY

4.4.4 INPUT-OUTPUT DEVICES

5 PHOTONIC IC MARKET BY TYPE OF INTEGRATION

5.1 INTRODUCTION

5.2 HYBRID

5.2.1 NORTH AMERICA IS THE LEADING MARKET OF HYBRID PHOTONIC IC

5.2.2 U.S CONTRIBUTES THE MAJOR PART IN THE HYBRID PHOTONIC IC MARKET IN NORTH AMERICA

5.3 MONOLITHIC

5.3.1 MONOLITHIC PHOTONIC IC MARKET BY GEOGRAPHY

5.3.2 MONOLITHIC PHOTONIC IC MARKET BY COUNTRY

5.4 MODULE

5.4.1 MODULE PHOTONIC IC MARKET BY GEOGRAPHY

5.4.1 MODULE PHOTONIC IC MARKET BY COUNTRY

6 PHOTONIC INTEGRATED CIRCUIT BY COMPONENTS

6.1 LASERS

6.1.1 WORKING PRINCIPLE OF A LASER

6.1.1.1 THE WORKING OF LASERS WITH RESPECT TO GAIN AND RESONATOR LOSSES

6.1.1.2 ADVANTAGE OF FIBER LASER

6.1.1.3 ADVANTAGE OF CARBON DIOXIDE LASERS

6.1.1.4 IMPORTANT ASPECTS OF LASER

6.2 MODULATORS

6.2.1 TYPES OF OPTICAL MODULATORS

6.3 PHOTO DETECTORS

6.3.1 IMPORTANT PROPERTIES OF PHOTO DETECTORS

6.4 ATTENUATORS

6.4.1 FIXED FIBER-OPTIC ATTENUATORS

6.4.2 BUILT-IN VARIABLE FIBER-OPTIC ATTENUATORS

6.4.3 VARIABLE FIBER-OPTIC TEST ATTENUATORS:

6.5 OPTICAL AMPLIFIERS

6.5.1 LASER AMPLIFIERS VERSUS AMPLIFIERS BASED ON OPTICAL NONLINEARITIES

6.5.2 MULTIPASS ARRANGEMENTS, REGENERATIVE AMPLIFIERS, AND AMPLIFIER CHAINS

6.5.3 IMPORTANT ATTRIBUTES OF AMPLIFIERS

6.5.3.1 IMPORTANT PARAMETERS OF AN OPTICAL AMPLIFIER

6.5.3.2 TYPICAL BENEFITS OF OPTICAL AMPLIFIERS

7 PHOTONIC IC MARKET BY RAW MATERIALS

7.1 INTRODUCTION

7.2 LITHIUM NIOBATE

7.2.1 LITHIUM NIOBATE PHOTONIC IC MARKET BY GEOGRAPHY

7.3 SILICA-ON-SILICON

7.3.1 SILICA ON SILICON PHOTONIC IC MARKET BY GEOGRAPHY

7.4 SILICON-ON-INSULATOR

7.4.1 MAJOR PLAYER OF SILICON PHOTONICS

7.4.2 SILICON-ON-INSULATOR PHOTONIC IC MARKET BY GEOGRAPHY

7.5 GALIUM ARSENIDE

7.5.1 GALIUM ARSENIDE PHOTONIC IC MARKET BY GEOGRAPHY

7.6 INDIUM PHOSPHIDE

7.6.1 COMPARISON MATRIX OF DIFFERENT RAW MATERIAL USED FOR PIC

7.6.2 COMPONENTS USED IN DIFFERENT PHOTONIC IC

7.6.3 INDIUM PHOSPHIDE PHOTONIC IC MARKET BY GEOGRAPHY

8 PHOTONIC IC MARKET BY APPLICATIONS

8.1 INTRODUCTION

8.2 OPTICAL FIBER COMMUNICATIONS

8.2.1 ADVANTAGES OF OPTICAL FIBER COMMUNICATION

8.2.2 WAVELENGTH RANGE FOR OPTICAL FIBER COMMUNICATIONS

8.2.3 PIC MARKET FOR OPTICAL FIBER COMMUNICATIONS BY GEOGRAPHY

8.3 OPTICAL FIBER SENSOR

8.3.1 PIC MARKET FOR OPTICAL FIBER SENSOR BY GEOGRAPHY

8.4 BIOMEDICAL

8.4.1 PIC MARKET FOR BIOMEDICAL BY GEOGRAPHY

8.5 QUANTUM COMPUTING

8.5.1 COMPARISON OF CLASSICAL AND QUANTUM COMPUTING

8.5.2 PIC MARKET FOR QUANTUM COMPUTING BY GEOGRAPHY

8.6 OTHERS

8.6.1 METROLOGY

8.6.2 SUBMARINES

9 PHOTONIC IC MARKET BY GEOGRAPHY

9.1 INTRODUCTION

9.2 NORTH AMERICA

9.2.1 NORTH AMERICA PHOTONIC IC MARKET BY APPLICATIONS

9.2.2 NORTH AMERICA PHOTONIC IC MARKET BY RAW MATERIALS

9.3 EUROPE

9.3.1 EUROPE PHOTONIC IC MARKET BY APPLICATIONS

9.3.2 EUROPE PHOTONIC IC MARKET BY RAW MATERIALS

9.4 APAC

9.4.1 APAC PHOTONIC IC MARKET BY APPLICATIONS

9.4.2 APAC PHOTONIC IC MARKET BY RAW MATERIALS

9.5 ROW

9.5.1 ROW PHOTONIC IC MARKET BY APPLICATIONS

9.5.2 ROW PHOTONIC IC MARKET BY RAW MATERIALS

10 COMPETITIVE LANDSCAPE

10.1 LEADING COMPANIES IN PHOTONIC INTEGRATED CIRCUIT

10.2 KEY GROWTH STRATEGIES

10.3 NEW PRODUCT LAUNCH/DEVELOPMENT

10.4 MERGERS & ACQUISITIONS

10.5 PARTNERSHIPS/AGREEMENTS/STRATEGIC ALLIANCE/ COLLABORATION

11 COMPANY PROFILES (OVERVIEW, FINANCIALS, PRODUCTS & SERVICES, STRATEGY, & DEVELOPMENTS)*

11.1 AGILENT TECHNOLOGIES

11.2 AIFOTEC AG

11.3 ALCATEL-LUCENT

11.4 AVAGO TECHNOLOGIES

11.5 CIENA CORPORATION

11.6 CYOPTICS

11.7 EMCORE CORPORATION

11.8 ENABLENCE TECHNOLOGIES

11.9 FINISAR CORPORATION

11.10 HEWLETT-PACKARD

11.11 INFINERA CORPORATION

11.12 INTEL CORPORATION

11.13 JDS UNIPHASE CORPORATION

11.14 KAIAM CORPORATION

11.15 KOTURA

11.16 LUXTERA

11.17 NEOPHOTONICS CORPORATION

11.18 OCLARO

11.19 ONECHIP PHOTONICS

11.20 TE CONNECTIVITY

*DETAILS ON FINANCIALS, PRODUCT & SERVICES, STRATEGY, & DEVELOPMENTS MIGHT NOT BE CAPTURED IN CASE OF UNLISTED COMPANIES.

LIST OF TABLES

TABLE 1 RESEARCH METHODOLOGY ADOPTED

TABLE 2 GLOBAL PHOTONIC IC MARKET REVENUE, BY APPLICATIONS,2012 � 2022 ($MILLION)

TABLE 3 GLOBAL PHOTONIC IC MARKET REVENUE, BY GEOGRAPHY,2012 � 2022 ($MILLION)

TABLE 4 GLOBAL PHOTONIC IC MARKET REVENUE, BY INTEGRATION,2012 � 2022 ($MILLION)

TABLE 5 GLOBAL PHOTONIC IC MARKET REVENUE, BY RAW MATERIALS,2012 � 2022 ($MILLION)

TABLE 6 ADVANTAGE OF PHOTONIC IC

TABLE 7 COMPARISON BETWEEN ELECTRONIC AND PHOTONIC IC

TABLE 8 TYPE OF OPTICAL SWITCHES

TABLE 9 HOLOGRAPHIC MEMORY VS CONVENTIONAL STORAGE DEVICES

TABLE 10 PHOTONIC IC MARKET REVENUE, BY INTEGRATION,2012 � 2022 ($MILLION)

TABLE 11 COMPARISON OF INTEGRATION TECHNIQUES

TABLE 12 GLOBAL HYBRID PHOTONIC IC MARKET REVENUE, BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 13 NORTH AMERICA: HYBRID PHOTONIC IC MARKET REVENUE,BY COUNTRY, 2012 � 2022 ($MILLION)

TABLE 14 EUROPE: HYBRID PHOTONIC IC MARKET REVENUE, BY COUNTRY,2012 � 2022 ($MILLION)

TABLE 15 APAC: HYBRID PHOTONIC IC MARKET REVENUE, BY COUNTRY, 2012 � 2022 ($MILLION)

TABLE 16 ROW: HYBRID PHOTONIC IC MARKET REVENUE, BY COUNTRY,2012 � 2022 ($MILLION)

TABLE 17 GLOBAL MONOLITHIC PHOTONIC IC MARKET REVENUE,BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 18 NORTH AMERICA: MONOLITHIC PHOTONIC IC MARKET REVENUE,BY COUNTRY, 2012 � 2022 ($MILLION)

TABLE 19 EUROPE: MONOLITHIC PHOTONIC IC MARKET REVENUE, BY COUNTRY, 2012 � 2022 ($MILLION)

TABLE 20 APAC: MONOLITHIC PHOTONIC IC MARKET REVENUE, BY COUNTRY, 2012 � 2022 ($MILLION)

TABLE 21 ROW: MONOLITHIC PHOTONIC IC MARKET REVENUE, BY COUNTRY, 2012 � 2022 ($MILLION)

TABLE 22 FEATURES OF DIFFERENT TYPE OF PHOTONIC INTEGRATION

TABLE 23 GLOBAL MODULE PHOTONIC IC MARKET REVENUE, BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 24 NORTH AMERICA: MODULE PHOTONIC IC MARKET REVENUE,BY COUNTRY, 2012 � 2022 ($MILLION)

TABLE 25 EUROPE: MODULE PHOTONIC IC MARKET REVENUE, BY COUNTRY,2012 � 2022 ($MILLION)

TABLE 26 APAC: MODULE PHOTONIC IC MARKET REVENUE, BY COUNTRY,2012 � 2022 ($MILLION)

TABLE 27 ROW: MODULE PHOTONIC IC MARKET REVENUE, BY COUNTRY,2012 � 2022 ($MILLION)

TABLE 28 ADVANTAGE OF FIBER LASER

TABLE 29 ADVANTAGE OF CARBON DIOXIDE LASERS

TABLE 30 TYPE OF LASERS

TABLE 31 TYPES OF OPTICAL MODULATORS

TABLE 32 IMPORTANT ATTRIBUTES OF AMPLIFIERS

TABLE 33 GLOBAL PHOTONIC IC MARKET REVENUE, BY RAW MATERIALS,2012 � 2022 ($MILLION)

TABLE 34 LITHIUM NIOBATE PHOTONIC IC MARKET REVENUE, BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 35 SILICA-ON-SILICON PHOTONIC IC MARKET REVENUE, BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 36 APPLICATIONS OF PASSIVE COMPONENTS

TABLE 37 MAJOR PLAYER OF SILICON PHOTONICS

TABLE 38 SILICON-ON-INSULATOR PHOTONIC IC MARKET REVENUE,BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 39 GALLIUM ARSENIDE PHOTONIC IC MARKET REVENUE, BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 40 CHARACTERISTICS ASSOCIATED WITH RAW MATERIAL USED FOR PIC

TABLE 41 COMPONENTS USED IN DIFFERENT PIC

TABLE 42 INDIUM PHOSPHIDE PHOTONIC IC MARKET REVENUE, BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 43 PHOTONIC IC MARKET REVENUE, BY APPLICATIONS,2012 � 2022 ($MILLION)

TABLE 44 WAVELENGTH RANGE FOR OPTICAL FIBER COMMUNICATION

TABLE 45 PHOTONIC IC MARKET REVENUE FOR OPTICAL FIBER COMMUNICATION APPLICATION, BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 46 NORTH AMERICA: PHOTONIC IC MARKET REVENUE FOR OPTICAL FIBER COMMUNICATION APPLICATION, BY COUNTRY,2012 � 2022 ($MILLION)

TABLE 47 EUROPE: PHOTONIC IC MARKET REVENUE FOR OPTICAL FIBER COMMUNICATION APPLICATION, BY COUNTRY,2012 � 2022 ($MILLION)

TABLE 48 APAC: PHOTONIC IC MARKET REVENUE FOR OPTICAL FIBER COMMUNICATION APPLICATION, BY COUNTRY,2012 � 2022 ($MILLION)

TABLE 49 ROW: PHOTONIC IC MARKET REVENUE FOR OPTICAL FIBER COMMUNICATION APPLICATION, BY COUNTRY, 2012 � 2022 ($MILLION)

TABLE 50 GLOBAL OPTICAL FIBER COMMUNICATION MARKET REVENUE,BY APPLICATIONS, 2012 � 2022 ($BILLION)

TABLE 51 OPTICAL FIBER COMMUNICATION MARKET REVENUE FOR WAN APPLICATION, BY GEOGRAPHY, 2012 � 2022 ($BILLION)

TABLE 52 OPTICAL FIBER COMMUNICATION MARKET REVENUE FOR DATACOM APPLICATION, BY GEOGRAPHY, 2012 � 2022 ($BILLION)

TABLE 53 OPTICAL FIBER COMMUNICATION MARKET REVENUE FOR ACCESS APPLICATION, BY GEOGRAPHY, 2012 � 2022 ($BILLION)

TABLE 54 PHOTONIC SENSORS MARKET REVENUE, BY GEOGRAPHY,2012 � 2017 ($BILLION)

TABLE 55 PHOTONIC IC MARKET REVENUE FOR OPTICAL FIBER SENSOR APPLICATION, BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 56 PHOTONIC IC MARKET REVENUE FOR BIOMEDICAL APPLICATION,BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 57 PHOTONIC IC MARKET REVENUE FOR QUANTUM COMPUTING APPLICATION, BY GEOGRAPHY, 2012 � 2022 ($MILLION)

TABLE 58 SIGNIFICANT GROWTH OF APAC MARKET

TABLE 59 GLOBAL PHOTONIC IC MARKER REVENUE, BY GEOGRAPHY,2012 � 2022 ($MILLION)

TABLE 60 NORTH AMERICA: PHOTONIC IC MARKET REVENUE, BY INTEGRATION, 2012 � 2022 ($MILLION)

TABLE 61 NORTH AMERICA: PHOTONIC IC MARKET REVENUE, BY APPLICATIONS, 2012 � 2022 ($MILLION)

TABLE 62 NORTH AMERICA: PHOTONIC IC MARKET REVENUE,BY RAW MATERIALS, 2012 � 2022 ($MILLION)

TABLE 63 EUROPE: PHOTONIC IC MARKET REVENUE, BY INTEGRATION,2012 � 2022 ($MILLION)

TABLE 64 EUROPE: PHOTONIC IC MARKET REVENUE, BY APPLICATIONS,2012 � 2022 ($MILLION)

TABLE 65 EUROPE: PHOTONIC IC MARKET REVENUE, BY RAW MATERIALS,2012 � 2022 ($MILLION)

TABLE 66 APAC: PHOTONIC IC MARKET REVENUE, BY INTEGRATION,2012 � 2022 ($MILLION)

TABLE 67 APAC: PHOTONIC IC MARKET REVENUE, BY APPLICATIONS,2012 � 2022 ($MILLION)

TABLE 68 APAC: PHOTONIC IC MARKET REVENUE, BY RAW MATERIALS, 2012 � 2022 ($MILLION)

TABLE 69 ROW: PHOTONIC IC MARKET REVENUE, BY INTEGRATION,2012 � 2022 ($MILLION)

TABLE 70 ROW: PHOTONIC IC MARKET REVENUE, BY APPLICATIONS,2012 � 2022 ($MILLION)

TABLE 71 ROW: PHOTONIC IC MARKET REVENUE, BY RAW MATERIALS,2012 � 2022 ($MILLION)

TABLE 72 RANKING OF PIC BASED COMPANIES

TABLE 73 NEW PRODUCT LAUNCH/DEVELOPMENT (2009 � 2012)

TABLE 74 MERGERS & ACQUISITIONS (2009 � 2012)

TABLE 75 PARTNERSHIPS/AGREEMENTS/STRATEGIC ALLIANCE/COLLABORATION (2009 � 2012)

TABLE 76 PRODUCT OFFERED BY AGILENT TECHNOLOGIES

TABLE 77 AGILENT TECHNOLOGIES: OVERALL REVENUE,2010 � 2012 ($MILLION)

TABLE 78 AGILENT TECHNOLOGIES: OVERALL REVENUE, BY BUSINESS SEGMENTS, 2010 � 2011 ($MILLION)

TABLE 79 ALCATEL-LUCENT: OVERALL REVENUE, 2010 � 2011 ($MILLION)

TABLE 80 AVAGO TECHNOLOGIES : OVERALL REVENUE, 2010 � 2011 ($MILLION)

TABLE 81 PRODUCT PORTFOLIO OF CIENA CORPORATION

TABLE 82 CIENA CORPORATION: OVERALL REVENUE, 2010 � 2011 ($MILLION)

TABLE 83 CYOPTICS : OVERALL REVENUE, 2009 � 2010 ($MILLION)

TABLE 84 PRODUCT OFFERED BY EMCORE CORPORATION

TABLE 85 EMCORE CORPORATION: OVERALL REVENUE, 2010 � 2011 ($MILLION)

TABLE 86 ENABLENCE TECHNOLOGIES : OVERALL REVENUE,2010 � 2012 ($MILLION)

TABLE 87 PRODUCT PORTFOLIO OF FINISAR CORPORATION

TABLE 88 FINISAR CORP: OVERALL REVENUE, 2011 � 2012 ($MILLION)

TABLE 89 PRODUCT OFFERINGS OF HP

TABLE 90 HP: OVERALL REVENUE, 2010 � 2011 ($MILLION)

TABLE 91 INFINERA CORPORATION: OVERALL REVENUE, 2010 � 2011 ($MILLION)

TABLE 92 INFINERA CORPORATION: MARKET REVENUE BY GEOGRAPHY,2010 � 2011 ($MILLION)

TABLE 93 INTEL PRODUCTS & THEIR RANGE

TABLE 94 PRODUCT PORTFOLIO OF INTEL CORPORATION

TABLE 95 INTEL CORPORATION: OVERALL REVENUE, 2010 � 2011($MILLION)

TABLE 96 JDS UNIPHASE CORPORATION: OVERALL REVENUE,2010 � 2012 ($MILLION)

TABLE 97 PRODUCT OFFERINGS OF NEOPHOTONICS CORPORATION

TABLE 98 NEOPHOTONICS CORPORATION: OVERALL REVENUE,2010 � 2011 ($MILLION)

TABLE 99 NEOPHOTONIC CORPORATION: MARKET REVENUE, BY COUNTRY,2010 � 2011 ($MILLION)

TABLE 100 OCLARO : OVERALL REVENUE, 2010 � 2012 ($MILLION)

TABLE 101 OCLARO: MARKET REVENUE, BY COUNTRY, 2010 � 2012 ($MILLION)

TABLE 102 TE CONNECTIVITY : OVERALL REVENUE, 2009 � 2011 ($MILLION)

TABLE 103 TE CONNECTIVITY: MARKET REVENUE, BY GEOGRAPHY,2009 � 2011 ($MILLION)

TABLE 104 TE CONNECTIVITY: MARKET REVENUE, BY BUSINESS SEGMENT,2009 � 2011 ($MILLION)

LIST OF FIGURES

FIGURE 1 STEPS IN RESEARCH METHODOLOGY

FIGURE 2 PHOTONIC IC MARKET RESEARCH STRATEGY

FIGURE 3 OVERVIEW OF PHOTONIC IC MARKET

FIGURE 4 EVOLUTION OF PICS

FIGURE 5 IMPACT ANALYSIS OF DRIVERS OF PIC

FIGURE 6 PACKAGING OF PHOTONIC IC AND ELECTRONIC IC

FIGURE 7 SIZE OF PHOTONIC INTEGRATED CIRCUIT AND ELECTRONIC INTEGRATED CIRCUIT

FIGURE 8 PIC INCORPORATED WITH OPTICAL DEVICES OF DIFFERENT FUNCTIONS

FIGURE 9 IMPACT ANALYSIS OF RESTRAINTS OF PIC

FIGURE 10 PORTER�S FIVE FORCE MODEL

FIGURE 11 OPTICAL PROCESSOR

FIGURE 12 PHOTONIC PROCESSOR VS ELECTRONIC PROCESSOR

FIGURE 13 SINGLE-MOLECULE OPTICAL TRANSISTOR

FIGURE 14 UNDERLYING PRINCIPLE BEHIND DEVELOPING A TRANSISTOR

FIGURE 15 OPTICAL SWITCH

FIGURE 16 SETUP OF A SIMPLE OPTICALLY PUMPED LASER

FIGURE 17 OPTICAL MODULATORS

FIGURE 18 PHOTO DETECTOR

FIGURE 19 OPTICAL ATTENUATOR

FIGURE 20 SETUP OF A MULTIPASS FEMTOSECOND AMPLIFIER

FIGURE 21 LITHIUM NIOBATE

FIGURE 22 SILICA ON SILICON

FIGURE 23 SILICON OR SILICON-ON-INSULATOR

FIGURE 24 GALLIUM ARSENIDE

FIGURE 25 INDIUM PHOSPHIDE

FIGURE 26 OPTICAL FIBER SENSING SYSTEM

FIGURE 27 CLASSIFICATION OF OPTICAL FIBER SENSORS

FIGURE 28 PIC-BASED OPTICAL SENSOR FOR HELICOPTER ROTOR BLADE MONITORING

FIGURE 29 DISTRIBUTED SENSING OF STRAIN AND TEMPERATURE USING AN OPTICAL FIBER AS SENSOR

FIGURE 30 KEY GROWTH STRATEGIES

Growth opportunities and latent adjacency in Photonic Integrated Circuit (IC) & Quantum Computing Market