Voice over LTE Market by Long-Term Evolution (Technology-FDD and TDD, End User Devices-Smart Phones, Dongles, and Routers), by Technology (CSFB, VOIMS, and Dual Radio/SVLTE), and by Geography - Analysis & Forecast to 2014 - 2020

Voice over LTE (VoLTE) empowers mobile network operators to offer rich voice, video, and messaging services as a core offering. Voice over LTE enables the operators to use data network to transmit voice services in small sized packets. It helps to increase spectrum efficiency and reduce operational and maintenance costs as only one network is used. Voice over LTE also enables operators to offer new set of standards based services referred to as Rich Communication Services or RCS which include video calling, real time language translation, video voice mail, and instant messaging. These advanced features will help mobile network operators to compete against OTT providers.

The major market for LTE is in the Americas and that for voice over Long-Term Evolution is in the Asia-Pacific region, which is expected to grow at a CAGR of 54.20% from 2014 to 2020. Based on the technology, the voice over LTE market can be divided into Circuit Switched Fallback (CSFB), Voice over IP multimedia subsystem (VoIMS), and Dual radio or Simultaneous Voice and LTE (SV LTE). The CSFB market accounted for the major share in 2013, but the VoIMS is expected to grow faster as compared to CSFB and SV LTE in the next 6 years.

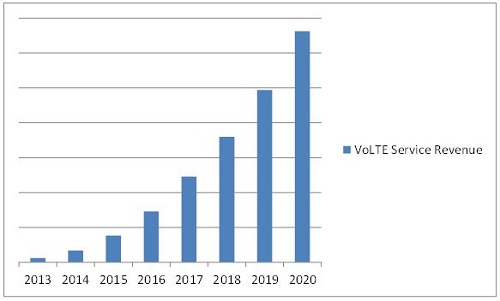

The report provides the profiles of all the major companies in the LTE and voice over Long-Term Evolution market. The report also provides the competitive landscape of the key players, which indicates the growth strategy of the Voice over LTE Market in the industry. The report also covers the entire value chain for the market, right from the infrastructure provider to the subscriber. Along with the value chain, this report also provides an in-depth view on the technology, end-user devices; geographic analysis of the Long-Term Evolution market and technology; and geographic analysis of the voice over Long-Term Evolution market. The market for VoLTE is estimated to reach up to $6,624.04 million by 2020, at a CAGR of 64.40% from 2014 to 2020.

The report also provides the market dynamics such as drivers, restraints, opportunities and challenges for the voice over LTE market. Apart from the market segmentation, thereport also includes the critical market data and qualitative information with regard tovoice over Long-Term Evolution; along with the qualitative analysis, such as the Porter�s five force analysis, value chain analysis, and the market crackdown analysis.

Key players in the LTE and voice over LTE market include Huawei Technologies Co. Ltd.(China), Nokia Solutions and Networks (Finland), Ericsson (Sweden), Alcatel-Lucent (France),LG Uplus (South Korea), SK Telecom (South Korea), Metro PCS (U.S.), AT&T Inc. (U.S.), KT Corp. (South Korea), and Verizon Wireless (U.S.),among others. The detailed explanation of the different market segments is given below:

LTE market, by technology:

LTE market by technology is segmented into Frequency Division Duplexing (FDD) and Time Division Duplexing (TDD).

LTE market, by end user device:

End-user devices in LTE market are smartphones, routers, dongles; and others such as notebooks, tablets, and modules.

VoLTE market, by technology:

Based on technology, the VoLTE market is segmented into three technologies, namely Circuit Switched Fallback (CSFB), Voice over IP Multimedia Subsystem (VoIMS), and Dual Radio or Simultaneous Voice and LTE (SVLTE)

LTE and VoLTE market, by geography:

LTE and VoLTE market is segmented by geography into four different regions; namely Americas, Europe, APAC, and the Rest of world.

Voice over LTE Market is perceived as a long term strategic solution for LTE, which makes use of IMS call control as defined by 3GPP TS 23.228 for LTE voice services delivery. IMS offers legacy voice services such as call originating or terminating, calling line identification, and supplementary services; as well as value added, advanced multimedia services such as video sharing. Voice over LTE is becoming a popular technology as it provides win-win situation for both the entities; that is, the mobile network operators and the subscribers.LTE offers twice the spectral efficiency of 3G/HSPA and more than six times efficiency as that of the GSM technology; this allows allocating more bandwidth for more data services. Reuse of existing 2G and 3G spectrum reduces the need for new spectrum.Optimization of network and simplification of service delivery help to reduce costs.

Operators are able to deliver new set of standards-based services referred to as rich communication services, which include services such as video calling, file transferring, real time language translation, video voice mail, and instant messaging. It reduces time to connect voice over LTE call and it also has improved battery life over other VoIP applications; these parameters help to gain a competitive position in the market against OTT providers.

This report describes the market trends, drivers, restraints, opportunities, and challenges for the voice over LTE market; and forecasts the LTE and voice over LTEmarket from 2014 to 2020 on the basis of the technology, end-user devices, and geography. This report covers geographies such as Americas, Europe, APAC, and ROW (Rest of the World).

In the long term evolution subscriptions market, FDD LTE subscriptions held the largest share; while in voice over LTE market,the CSFB technology accounted for the largest share, followed by VoIMS, in 2013;the situation is expected to reverse by 2020.Americas is the leader in the LTE market whilethe APAC region is the leader in the voice over LTE market.

The major companies involved in the LTE and voice over LTE market are Huawei Technologies Co. Ltd.(China), Nokia Solutions and Networks (Finland), Ericsson (Sweden), Alcatel-Lucent (France),LG Uplus (South Korea), SK Telecom (South Korea), Metro PCS (U.S.), AT&T Inc. (U.S.), KT Corp. (South Korea), and Verizon Wireless (U.S.).

Voice over LTE Services Market 2014 - 2020

Source: MarketsandMarkets

The overall voice over LTE market is expected to increase at a CAGR of 64.40% from 2014 to 2020. Rich communication services, reduced latency, and increased revenue per user are the main reasons behind the increased adoption of the voice over long term evolution services.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No.- 16)

1.1 Objectives of The Study

1.2 Markets Covered

1.3 Stakeholders

1.4 Market Scope

2 Research Methodology (Page No.- 19)

2.1 Factor Analysis

2.1.1 Increased Spectrum Efficiency

2.1.2 Others, Such As No Carrier Interoperability

2.2 Market Size Estimation

2.3 Market Crackdown & Data Triangulation

2.4 Market Share Estimation

2.4.1 Key Data Taken From Secondary Sources

2.4.2 Key Data From Primary Sources

2.4.2.1 Key Industry Insights

2.4.3 Assumptions

3 Executive Summary (Page No.- 26)

4 Premium Insights-VOLTE And LTE Market (Page No.- 31)

4.1 Attractive Market Opportunity In VOLTE Market

4.2 VOLTE Market- Top Three Technology Segments

4.3 VOLTE Market in Different Regions

4.4 APAC Commanded The Largest Share Among All Regions in 2013

4.5 VOLTE Market, By Technology

4.6 VOLTE Services Market, By Application

4.7 VOLTE Market, By Technology: By Region

4.8 Attractive Market Opportunity in LTE Market

4.9 LTE Market : End User Devices

4.10 LTE Market in Different Regions

4.11 Americas Commands The Largest Share Among All Regions

4.12 LTE End User Devices� Market: By Geography

4.13 LTE Market: Smartphones Vs Dongles

4.14 LTE Market, By End User Device : Top Three Devices

5 Market Overview (Page No.- 44)

5.1 Introduction

5.2 History And Evolution

5.3 Market Segmentation

5.4 Voice Over LTE Market Segmentation

5.4.1 Voice Over LTE Market, By Technology

5.4.2 Voice Over LTE Market By Geography

5.5 LTE Market Segmentation

5.5.1 LTE Market, By Technology

5.5.2 LTE Market, By End User Device

5.6 Market Dynamics

5.7 Market Drivers

5.7.1 Increased Spectrum Efficiency is Motivating The Telecom Operators To Adopt VOLTE Solutions

5.7.2 Faster Call Set Up Time Due To Reduced Latency is Attracting Subscribers Toward The VOLTE Services

5.7.3 Reduced Operational And Maintenance Costs Are Driving The VOLTE Market

5.7.4 Increased Adoption of VOLTE By Operators Has Been Fuelling The Growth of The VOLTE Services

5.8 Market Restraints

5.8.1 Less Availability of VOLTE Enabled Devices is An Obstacle For The Growth of VOLTE Market

5.8.2 No Carrier Inter-Operability is A Restraining Factor For VOLTE

5.9 Market Opportunities

5.9.1 True Device Interoperability Will Provide Operators With Opportunities To Increase Their Customer Base

5.9.2 Variable Pricing Strategies By Operators Will Provide Opportunities For Early Adopters To Increase Their Market Share

5.9.3 Network Function Virtualization Solutions For VOLTE Provide Opportunities For Operators And Network Infrastructure Providers To Establish Competent Position in The Emerging VOLTE Market

5.9.3.1 Advantages of Network Function Virtualized Ims

5.9.3.2 Virtualized Multitenant Model For Ims Core

5.9.4 Growing Demand For Mobile Uc is Fuelling The Growth of The VOLTE Market

5.9.5 Integration of VOLTE With Voice Over Wi-Fi Service Will Help The Operators To Attract More Subscribers

5.1 Challenges

5.10.1 Competition Against Over-The-Top(Ott) Applications Such As Skype, Whatsapp, Viber, Line, Or Imessage

5.10.2 Implementation Challenges For VOLTE

5.10.3 Voice Over LTE Network Carriers Are Facing issues in Defining The Quality of Service (Qos) Parameters For LTE Network

5.10.4 Small Sized Packets Required in Delivering Voice Over LTE Network Are One of The Key Challenges For Carriers

5.10.5 Limitations For Smaller Players

5.10.6 Consumer Satisfaction is A Challenge For VOLTE

5.10.7 Billing issues In Roaming

5.11 Spectrum Band Differentiation of Major U.S. Carriers And Its Impact On Interoperability

5.12 Comparison of VOLTE Solutions offered By Major U.S. Carriers

5.13 Key Activities Related To The VOLTE Market in The Telecom Industry

5.14 VOLTE Market: Qos Class Identifier Values For Bearer

5.15 Comaprison Between Voip And VOLTE

6 Industry Trends (Page No.- 67)

6.1 Introduction

6.2 Value Chain Analysis

6.3 Industry Trends

6.4 Porter�s Five Forces Analysis

6.4.1 Degree of Competition

6.4.2 Bargaining Power of Buyers

6.4.3 Bargaining Power of Suppliers

6.4.4 Threat From Substitutes

6.4.5 Threat From New Entrants

7 Long Term Evolution(LTE) Market (Page No.- 76)

7.1 Introduction

7.2 Mobile Subcriptions Worldwide

7.2.1 Wcdma/Hspa Subsciptions

7.2.1.1 Comparison Between Wcdma And Hspa

7.2.2 LTE Subcriptions

7.3 LTE Networks

7.3.1 Comparison Between Wcdma And LTE

7.3.2 Comparison Between Hspa And LTE

7.3.3 VOLTE Subscriptions

7.4 LTE Market, By Technology

7.4.1 Frequency Division Duplexing(Fdd)

7.4.2 Time-Division Duplexing(Tdd)

7.5 LTE Market Analysis And Forecast

7.6 LTE Market

7.6.1 LTE Infrastructure

7.6.2 LTE Services

7.6.3 LTE End User Devices

7.6.3.1 Smartphones

7.6.3.2 Routers

7.6.3.3 Dongles

7.6.3.4 Others

7.7 LTE Market, By Geography

7.7.1 Americas

7.7.1.1 North America

7.7.1.2 Latin America

7.7.2 Europe

7.7.3 APAC

7.7.4 Row

8 Market By Technology (Page No.- 118)

8.1 Introduction

8.1.1 Limitations of VOLTE

8.1.1.1 VOLTE is Limited To Certain Devices

8.1.1.2 No Carrier Interoperability

8.2 Voice Over Ip Multimedia Subsystem (VOMis)

8.2.1 Benefits of VOIMS To Operators

8.2.1.1 Spectral Efficiency

8.2.1.2 Simplification of Network

8.2.2 Benefits of VOIMS To Consumers

8.2.2.1 High Definition Voice

8.2.2.2 Rich Communication Services (RCS)

8.2.2.3 Reduced Call Setup Times

8.2.2.4 Improved Battery Life Over Other Voip Applications

8.2.2.5 Integration of VOLTE With Voice Over Wi-Fi Service

8.3 Circuit Switched Fall Back (CFSB)

8.3.1 Overview of Circuit Switched Fall Back

8.3.2 Architecture of Circuit Switched Fall Back Network

8.3.3 Call Originating Procedure In Circuit Switched Fall Back

8.3.4 Advantages And Disadvantages of Circuit Switched Fallback Network

8.3.4.1 Advantages of Circuit Switched Fallback Network

8.3.4.2 Disadvantages of The Circuit Switched Fallback Network

8.4 Dual Radio/Simultaneous Voice And LTE (SVLTE)

8.5 Voice Over LTE Via Generic Access Network (VOLGA)

8.5.1 Network Set Up of Voice Over LTE Via Generic Access(VOLGA)

8.5.2 Call Originating Procedure of The Voice Over LTE Via Generic Access Network

8.5.3 Advantages And Disadvantages of Volga

8.5.3.1 Advantages of Volga

8.5.3.2 Disadvantages of Volga

8.6 Single Radio Voice Call Continuity (SRVCC)

8.6.1 LTE To Legacy Network Handover

8.6.2 Legacy Network To LTE Handover

8.6.3 Interruption Time issue In SRVCC

9 Market By Geography (Page No.- 135)

9.2 Introduction

9.2.1 LTE Network Launches Worldwide, 2013- 2020

9.2.2 VOLTE Launches In Different Countries

9.3 Americas

9.3.1 North America

9.3.2 VOLTE Services Launch Status in North America, By Country

9.4 Rest of Americas

9.4.1 VOLTE Services Launch Status in Rest of The Americas, By Country

9.5 Europe

9.5.1 VOLTE Services Launch Status in Europe, By Country

9.6 APAC

9.7 Row

9.7.1 VOLTE Services Launch Status in Row, By Country

10 Competitive Landscape (Page No.- 148)

10.1 Overview

10.2 Market Share Analysis LTE Market

10.3 Major LTE Infrastructure Vendor Ranking Based On The LTE Contract Value

10.4 Market Share Analysis, By LTE Contracts

10.5 Competitive Situation And Trends

10.5.1 New Product Launches

10.5.2 Agreements,Partnerships,Collaborations,& Joint Ventures

10.5.3 Mergers And Acquisitions

10.5.4 Expansions

11 Company Profiles (Overview, Products And Services, Financials, Strategy & Development)* (Page No.- 159)

11.1 Introduction

11.2 Alcatel-Lucent

11.3 At & T Inc.

11.4 Ericsson

11.5 Huawei Technologies Co., Ltd.

11.6 Kt Corporation

11.7 Lg Uplus Corp.

11.8 Metropcs

11.9 Nokia Solutions And Networks

11.10 Sk Telecom

11.11 Verizon Wireless

*Details On Overview, Products And Services, Financials, Strategy & Development Might Not Be Captured in Case of Unlisted Companies.

12 Appendix (Page No.- 197)

12.1 Insights of Industry Experts

12.2 Discussion Guide

12.3 Introducing Rt: Real Time Market Intelligence

12.4 Available Customizations

12.5 Related Reports

List of Tables (77 Tables)

Table 1 List of Mobile Network Operators And Their VOLTE Status

Table 2 Increased Adoption of VOLTE By Operators is Driving The VOLTE Market Growth

Table 3 No Carrier Interoperability And Less Availibilty of VOLTE Enabled Devices Are The Restraining Factors For The VOLTE Market

Table 4 True Device Interoperability And Variable Pricing Strategies By Operators Will Spur The Growth of The Voice Over LTE Market

Table 5 Competition Against Ott Players And Implementaion of Network Are The Major Challenges in The VOLTE Market

Table 6 Frequency And LTE Band Comparison of Major U.S. Carriers

Table 7 Comparison Among Major U.S. Carriers With Respect To VOLTE Services offered By Them

Table 8 Key Activities Related To VOLTE Industry

Table 9 Qci Values For Bearer Corresponding To Service Provided

Table 10 Comparison Between Voip (Voice Over Internet Protocol) And VOLTE (Voice Over LTE )

Table 11 Difference Between Wcdma Vs Hspa Vs LTE

Table 12 Mobile Subscriptions, 2013-2020 (Million)

Table 13 Mobile Subscriptions, By Type, 2013-2020 (Million)

Table 14 Mobile Subscriptions, By Geography, 2013-2020 (Million)

Table 15 Mobile Subscriptions, By Devices, 2013-2020 (Million)

Table 16 Mobile Services Market Size, 2013-2020 ($Billion)

Table 17 Mobile Services Market Size, By Segment, 2013-2020 ($Billion)

Table 18 Mobile Data Traffic , 2013-2020 (Mb/Month)

Table 19 Comparison Between Wcdma And Hspa

Table 20 LTE Subscriptions Worldwide, 2013-2020 (Million)

Table 21 LTE Subscriptions, By Technology, 2013-2020 (Million)

Table 22 LTE Subscriptions, By End User Device, 2013-2020 (Million)

Table 23 LTE Subscriptions, By Geography. 2013-2020 (Million)

Table 24 LTE Networks, 2013-2020

Table 25 LTE Networks, By Technology, 2013-2020 (Million)

Table 26 LTE Devices, 2013-2020

Table 27 LTE Devices, By Technology, 2013-2020

Table 28 LTE Devices, By Type, 2013-2020

Table 29 Comparison Between Wcdma And LTE

Table 30 Comparison Between Hspa Vs LTE

Table 31 VOLTE Subscriptions, 2013-2020 (Million)

Table 32 VOLTE Subscribtions, By LTE Technology Type, 2013-2020 (Millon)

Table 33 VOLTE Subscriptions, By Technology, 2013-2020 (Million)

Table 34 VOLTE Subscriptions, By Geography, 2013 To 2020 (Million)

Table 35 VOLTE Service Launches, 2013-2020

Table 36 VOLTE Devices, 2013-2020

Table 37 Difference Between Fdd And Tdd

Table 38 LTE Devices, By Fdd Technology, 2013-2020

Table 39 LTE Devices, By Tdd Technology, 2013-2020

Table 40 LTE Market Size, 2013-2020 ($Billion)

Table 41 LTE Market Size, By Segment, 2013-2020 ($Billion)

Table 42 LTE Market Size, By End User Device, 2013-2020 ($Billion)

Table 43 LTE Market Size, By Geography, 2013-2020 ($Billion)

Table 44 LTE Infrastructure Market Size, By Geography 2013-2020 ($Billion)

Table 45 LTE Services Market Size, By Geography, 2013-2020 ($Billion)

Table 46 LTE End User Devices Market Size, By Geography, 2013-2020 ($Billion)

Table 47 LTE Smartphones Market Size, By Geography, 2013 And 2020 ($Billion)

Table 48 LTE Routers Market Size, By Geography, 2013-2020 ($Billion)

Table 49 LTE Dongles Market Size, By Geography 2013-2020 ($Billion)

Table 50 LTE Others Market Size, By Geography 2013-2020 ($Billion)

Table 51 Americas: LTE Market Size, 2013-2020 ($Billion)

Table 52 Americas: LTE Market Size, 2013-2020 ($Billion)

Table 53 Europe: LTE Market Size, 2013-2020 ($Billion)

Table 54 Europe: LTE Market Size, 2013-2020 ($Billion)

Table 55 APAC:LTE Market Size, 2013-2020 ($Billion)

Table 56 APAC: LTE Market Size, 2013-2020 ($Billion)

Table 57 Row: LTE Market Size, 2013-2020 ($Billion)

Table 58 Row: LTE Market Size, 2013-2020 ($Billion)

Table 59 VOLTE Services Market Size, 2013-2020 ($Million)

Table 60 Voice Over LTE Market, By Technology, 2013-2020 ($Million)

Table 61 VOIMS Technology Market, By Geography, 2013-2020 ($Million)

Table 62 CSFB Technology Market, By Geography, 2013-2020 ($Million)

Table 63 Dual Radio/SvLTE Technology Market, By Geography, 2013-2020 ($Million)

Table 64 VOLTE Launches in Various Countries

Table 65 Americas: VOLTE Services Market Value, By Technology, 2013-2020 ($Million)

Table 66 VOLTE Services Launch Status in North America, By Country

Table 67 VOLTE Services Launch Status in Rest of The Americas, By Countries

Table 68 VOLTE Services Launch Status in Europe, By Country

Table 69 Europe: VOLTE Services Market, By Technology, 2014-2020 ($Million)

Table 70 VOLTE Services Launch Status in APAC, By Country

Table 71 APAC: VOLTE Services Market, By Technology, 2013-2020 ($Million)

Table 72 VOLTE Services Launch Status in Row, By Country

Table 73 Row: VOLTE Services Market, By Technology ($Million)

Table 74 New Product Launches, 2014

Table 75 Agreements, Partnerships, Collaborations, & Joint Ventures, 2013-2014

Table 76 Mergers And Aquisitions,2013-2014

Table 77 Expansions, 2012-2014

List of Figures (108 Figures)

Figure 1 Voice Over LTE Market, By Technology

Figure 2 Voice Over LTE Market: Research Methodology

Figure 3 Market Size Estimation Methodology: Bottom-Up Approach

Figure 4 Market Size Estimation Methodology: Top-Down Approach

Figure 5 Break Down of Primary Interviews: By Company Type, Designation, & Region

Figure 6 LTE Mobile Subscriptions Market Snapshot (2013 Vs 2020) : Tdd LTE Mobile Subscriptions Are Expected To Grow Faster As Compared To Fdd LTE Mobile Subscriptions in The Next Six Years

Figure 7 Voice Over LTE Market Value Snapshot (2013 Vs 2020) : Market For VOIMS Technology is Expected To Grow Rapidly in The Next Six Years

Figure 8 LTE Market Value, By End User Device, 2013

Figure 9 LTE Market Share, By Geography, 2013

Figure 10 VOLTE Market Share, By Geography, 2013

Figure 11 Attractive Market Opprtunity in VOLTE Market

Figure 12 VOIMS To Grow At The Fastest Rate Among All VOLTE Technologies

Figure 13 CSFB Accounts For The Largest Share in The VOLTE Market

Figure 14 APAC is The Largest Share Holder in The VOLTE Market

Figure 15 VOIMS Technology is Expected To Dominate The Market By 2020

Figure 16 Video Calling Service is Expected To Experience The Fastest Growth in The VOLTE Services Market

Figure 17 VOLTE Market, By Technology, is Expected To Grow At The Highest Cagr in The Europe Region

Figure 18 Attractive Market Opportunity in LTE Market

Figure 19 LTE Smartphone Market is Expected To Grow At The Highest Cagr And Holds The Highest Market Share

Figure 20 LTE Smartphones is Expected To Hold The Largest Share From 2013 To 2020 in The LTE Market, By End User Device

Figure 21 Americas is The Largest Share Holder in The LTE Market

Figure 22 Smartphone Will Continue To Dominate The LTE End User Devices Market Among All Geographic Regions

Figure 23 Smartphones is Expected To Grow At The Highest Rate Among All Geographic Regions

Figure 24 Smartphones Dominates The Overall End User Devices Market of LTE

Figure 25 Evolution of Cellular Generations: VOLTE is Expected To Play A Crucial Role in The Telecom Industry

Figure 26 Voice Over LTE Market Segmentation: By Technology

Figure 27 Voice Over LTE Market Segmentation: By Geography

Figure 28 LTE Market Segmentation: By Technology

Figure 29 LTE Market Segmentation: By End User Device

Figure 30 Increased Spectrum Efficiency And Rapid Deployment of Smart Devices is Driving The VOLTE Market

Figure 31 Virtualized Multitenant Ims Core Model

Figure 32 Value Chain Analysis: Major Value is Added By Infrastructure Providers And Mobile Network Operators

Figure 33 High Demand For LTE And VOLTE Market

Figure 34 Porter�s Five Forces Analysis For The Voice Over LTE Market

Figure 35 Degree of Competition in The Voice Over LTE Market

Figure 36 Bargaining Power of The Buyers in The Voice Over LTE Market

Figure 37 Bargaining Power of The Suppliers in The Voice Over LTE Market

Figure 38 Threat From Substitutes in The Voice Over LTE Market

Figure 39 Threat of New Entrants in The Voice Over LTE Market

Figure 40 Mobile Subscriptions Worldwide

Figure 41 Mobile Subscriptions, By Geography, 2013 And 2020

Figure 42 Mobile Services Market Size, 2013-2020 ($Billion)

Figure 43 Mobile Services Market Size, By Segment, 2013 And 2020 ($Billion)

Figure 44 Uplink And Downlink

Figure 45 LTE Subscriptions

Figure 46 LTE Subscriptions, By Geography, 2013 And 2020 (Million)

Figure 47 LTE Networks, 2013-2020

Figure 48 LTE Devices, 2013-2020

Figure 49 LTE Devices, By Type, 2013 And 2020

Figure 50 VOLTE Subscriptions

Figure 51 VOLTE Subscriptions, By LTE Technology Type, 2013 And 2020 (Million)

Figure 52 VOLTE Subscriptions, By Technology, 2013 And 2020 (Million)

Figure 53 VOLTE Subscriptions, By Geography, 2014 And 2020 (Milllion)

Figure 54 VOLTE Service Launches, 2013-2020

Figure 55 Fdd LTE Vs Tdd LTE

Figure 56 VOLTE Devices, 2013-2020

Figure 57 LTE Market Size, 2013-2020 ($Billion)

Figure 58 LTE Market Size, By End User Device, 2013 And 2020 ($Billion)

Figure 59 LTE Market Size, By Geography, 2013-2020 ($Billion)

Figure 60 LTE Infrastructure

Figure 61 LTE Infrastructure Market Size, By Geography, 2013 And 2020 ($Billion)

Figure 62 LTE Services Market Size, 2013 And 2020 ($Billion)

Figure 63 LTE End User Devices Market Size, 2013 And 2020 ($Billion)

Figure 64 Americas: LTE Market Size, 2013 And 2020 ($Billion)

Figure 65 Americas: LTE Market Size, 2013 And 2020 ($Billion)

Figure 66 Europe: LTE Market Size, 2013 And 2020 ($Billion)

Figure 67 Europe: LTE Market Size, 2013 And 2020 ($Billion)

Figure 68 APAC: LTE Market Size, 2013 And 2020 ($Billion)

Figure 69 APAC: LTE Market Size, 2013 And 2020 ($Billion)

Figure 70 LTE Market Size, Row, 2013 And 2020 ($Billion)

Figure 71 Row: LTE Market Size, 2013 And 2020 ($Billion)

Figure 72 VOLTE Services Market Size, 2013-2020 ($Million)

Figure 73 VOIMS Technology is Expected To Grow At A Faster Rate As Compared To Other Technologies

Figure 74 Network Architecture of Voice Over Ip Multimedia Subsystem (VOIMS)

Figure 75 Asia-Pacific Region Dominates The Voice Over Ims Market

Figure 76 Overview of The Circuit Switched Fall Back Network

Figure 77 Architecture of Circuit Switched Fall Back Network

Figure 78 Call Originating Procedure in Circuit Switched Fall Back Network

Figure 79 Asia-Pacific Region Held The Largest Share of The CSFB Technology Market in 2013

Figure 80 Architecture of Voice Over LTE Via Generic Access Network

Figure 81 Call Originating Procedure of Voice Over LTE Via Generic Access Network

Figure 82 Network Implementation of Single Radio Voice Call Continuity (Srvcc) Functionality

Figure 83 Geographic Snapshot(2013)-Rapid Growth in VOLTE Service Market Are Emerging As The New Hot Spots

Figure 84 LTE Network Launches Worldwide, 2013- 2020

Figure 85 VOIMS is Expected To Grow At The Highest Cagr As Compared To Other Technologies

Figure 86 Americas Market Snapshot:Demand Will Be Driven By The Increasing LTE Subscriptions And VOLTE Service Launches By Operators

Figure 87 Asia-Pacific LTE And Voice Over LTE Market Snapshot- Largest Shareholder in The VOLTE Market

Figure 88 Companies Adopted Product Innovation And Partnerships, Agreements, And Collaborations As The Key Growth Strategies Over The Last Three Years

Figure 89 Huawei Technologies Co., Ltd. Technologies Grew At A Faster Rate Between 2011 And 2013

Figure 90 LTE Infrastructure Market Share, By Key Player, 2013

Figure 91 Share Analysis of LTE Contracts, By Key Player

Figure 92 Battle For Market Share: New Product Launches And Partnerships, Agreements, Joint Ventures And Collaborations Were Seen As Key Strategies For 2011-2014

Figure 93 Geographic Revenue Mix of Top 4 Market Players

Figure 94 Competitive Benchmarking of Key Market Players (2010-2013): Huawei Technologies Co., Ltd. Emerged As The Champion

Figure 95 Alcatel-Lucent: Business Overview

Figure 96 Alcatel Lucent: Swot Analysis

Figure 97 At & T Inc. : Business Overview

Figure 98 Ericsson: Business Overview

Figure 99 Ericsson:Swot Analysis

Figure 100 Huawei Technologies Co., Ltd.: Business Overview

Figure 101 Huawei Technologies Co., Ltd. : Swot Analysis

Figure 102 KT Corporation: Business Overview

Figure 103 LG Uplus Corp.: Business Overview

Figure 104 Metropcs : Business Overview

Figure 105 Nokia Solutions And Networks: Business Overview

Figure 106 Nokia Solutions And Networks: Swot Analysis

Figure 107 SK Telecom : Business Overview

Figure 108 Verizon Wireless Business Overview

Growth opportunities and latent adjacency in Voice over LTE Market