North American Healthcare Cloud Computing Market by Application (PACS, RCM, EMR), by Deployment (Private, Public), by Service (SaaS, PaaS), & by End-User (Providers, Payers, Life Sciences) - Analysis & Forecasts to 2020

Over the years, the adoption of cloud computing in healthcare has increased owing to the rising need to curtail healthcare costs and improve the quality of healthcare. Thus, the stakeholders in the healthcare cloud computing market have implemented Clinical Information System (CIS) such as Electronic Medical Record (EMR), Computerized Physician Order Entry (CPOE), and Radiology Information System (RIS), among others. This technology offers easier and faster access to data depending on the way it is stored, that is, on public, private, or hybrid cloud.

In 2014, the Clinical Information Systems (CIS) segment accounted for the largest share of the North American Healthcare Cloud Computing market, by application; the private cloud segment accounted for the largest share of the healthcare and life sciences cloud computing market, by deployment model; the Software-as-a-service (SaaS) segment accounted for the largest share of healthcare and life sciences cloud computing market, by service model; the pay-as-you-go segment accounted for the largest share of the healthcare and life sciences cloud computing market, by pricing model; the software segment accounted for the largest share of the healthcare and life sciences cloud computing market, by component; while the healthcare providers segment accounted for the largest share of the healthcare and life sciences cloud computing market, by end user.

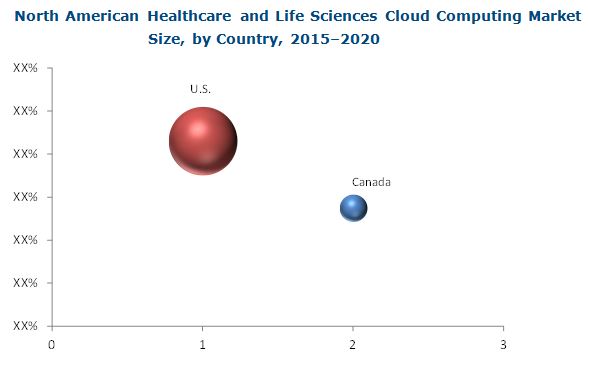

In 2014, the U.S. accounted for the largest share of the North American Healthcare Cloud Computing market and is expected to witness the highest growth rate. The market for healthcare cloud computing in the U.S. is expected to rise in insurance enrollments triggered by the Patient Protection and Affordable Care Act (March 2010), inadequate IT infrastructure among payers, and conference, symposia, and seminars conducted on cloud computing in the U.S.

The North American Healthcare and Life Sciences Cloud Computing market witnesses high competitive intensity as there are several big and many small firms with similar product offerings. These companies adopt various strategies (agreements, partnerships, collaborations, expansions, and new product launches) to increase their market shares and to establish a strong foothold in the North American Healthcare Cloud Computing market.

Scope of the Report:

This research report categorizes the North American healthcare and life sciences cloud computing market into the following segments and subsegments:

- North American Healthcare Cloud Computing Market, by Application

- Healthcare Cloud Computing Applications

- Clinical Information Systems (CIS)

- Electronic Medical Records (EMR)

- Picture Archiving and Communication System (PACS)

- Radiology Information System (RIS)

- Computerized Physician Order Entry (CPOE)

- Laboratory Information System (LIS)

- Pharmacy Information System (PIS)

- Others (point-of-care solutions, surgical information systems, intensive care information systems, emergency care solutions, specialty care information systems, nursing information systems, and diagnostic imaging systems)

- Non Clinical Information Systems

- Revenue Cycle Management (RCM)

- Automatic Patient Billing (APB)

- Cost Accounting

- Payroll

- Claims Management

- Others

- Clinical Information Systems (CIS)

- Life Sciences Cloud Computing Applications

- Clinical Research and R&D

- Supply Chain

- Payroll

- Others (Storage, Manufacturing, and Operations)

- North American Healthcare Cloud Computing Market, by Service Model

- Software-as-a-service (SaaS)

- Infrastructure-as-a-service (IaaS)

- Platform-as-a-service (PaaS)

- North American Healthcare Cloud Computing Market, by Deployment Model

- Private cloud

- Public cloud

- Hybrid cloud

- North American Healthcare Cloud Computing Market, by Pricing Model

- Pay-as-you-go

- Spot Pricing

- North American Healthcare Cloud Computing Market, by Component

- Hardware

- Software

- Services

- North American Healthcare Cloud Computing Market, by End User

- Healthcare Providers

- Healthcare Payers

- Life Sciences Companies

- North American Healthcare Cloud Computing Market, by Country

- U.S.

- Canada

Cloud computing helps store, manage, and process data from disparate locations, and delivers hosted services over the internet. In the healthcare industry, cloud computing as a technology is offered in four forms, namely, computation, storage, memory, and networking. Cloud computing is increasingly being adopted in the healthcare industry owing to the increasing pressure to curtail healthcare costs, while maintaining the quality of care provided to patients.

The North American healthcare and life sciences cloud computing market is segmented on the basis of application, deployment model, service model, pricing model, component, end-user, and region. By application, the healthcare and life sciences cloud computing market is categorized into Clinical Information System (CIS), Non-clinical Information System (NCIS), and life sciences applications. In 2015, the Clinical Information System (CIS) segment is expected to be the largest share of the healthcare and life sciences cloud computing market. This segment is expected to grow at the fastest rate during the forecast period (2015 to 2020).

On the basis of deployment model, the healthcare and life sciences cloud computing market is categorized into public cloud, private cloud, and hybrid cloud. In 2015, the private cloud segment is estimated to account for the largest share of the North American Healthcare and Life Sciences Cloud Computing market.

The North American Healthcare and Life Sciences Cloud Computing market, by service model, is segmented into software-as-a-service (SaaS), platform-as-a-service (PaaS), and information-as-a-service (IaaS). In 2015, the software-as-a-service segment is expected to account for the largest share of the North American Healthcare Cloud Computing market.

The healthcare and life sciences cloud computing market, by pricing model, is segmented into pay-as-you-go and spot pricing. In 2015, the pay-as-you-go segment is expected to account for the largest share of the North American Healthcare Cloud Computing market.

On the basis of component, the healthcare and life sciences cloud computing market is divided into hardware, software, and services. In 2015, the software segment is estimated to account for the largest share of the North American Healthcare and Life Sciences Cloud Computing.

On the basis of end user, the healthcare and life sciences cloud computing market is divided into healthcare providers, healthcare payers, and life sciences companies. In 2015, the healthcare provider segment is estimated to account for the largest share of the North American Healthcare Cloud Computing market.

The key factors that are expected to spur the growth of North American Healthcare Cloud Computing market are reforms of various countries benefiting healthcare IT, proliferation of new payment models and cost-efficiency of cloud technology, and implementation of the Patient Protection and Affordable Care Act (PPACA). Moreover, teleCloud and formation of Accountable Care Organizations (ACOs) are to create opportunities for healthcare cloud computing market. However, security of patient data on cloud is a crucial task and is likely to restrain the growth of this North American Healthcare and Life Sciences Cloud Computing market.

On the basis of country, North American Healthcare Cloud Computing market is classified into U.S. and Canada

Source: Cloud Computing Association (CCA), Healthcare Information and Management Systems Society (HIMSS), Centers for Disease Control and Prevention (CDC), California Association of Public Hospitals and Health Systems (CAPH), The Lowell General Physician Hospital Organization (PHO), Institute of Electrical and Electronics Engineers (IEEE), Certification Commission for Health Information Technology (CCHIT), Expert Interviews, and MarketsandMarkets Analysis

Note: The size of the bubble chart depicts the market size (USD Billion) in 2015

The North American healthcare and life sciences cloud computing market is expected to reach USD 11.43 Billion in 2020 from USD 4.49 Billion in 2015, growing at a CAGR of 20.5%. The market is expected to be dominated by the U.S.

Some of the major players in the North American Healthcare Cloud Computing market include athenahealth, Inc. (U.S.), CareCloud Corporation (U.S.), ClearData Networks, Inc. (U.S.), Carestream Health (U.S.), Dell Inc. (U.S.), GNAX Health (U.S.), IBM Corporation (U.S.), Iron Mountain, Inc. (U.S.), Oracle Corporation (U.S.) and VMware, Inc. (U.S.).

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 North American Healthcare Cloud Computing Market: Introduction (Page No. - 22)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Market Scope

1.3.1 Markets Covered

1.3.2 Years Considered for the Study

1.4 Currency

1.5 Limitations

1.6 Stakeholders

2 North American Healthcare Cloud Computing Market: Research Methodology (Page No. - 26)

2.1 Introduction

2.1.1 Research Methodology Steps

2.1.2 Secondary and Primary Research Methodology

2.1.2.1 Secondary Research

2.1.2.2 Key Data From Secondary Sources

2.1.2.3 Primary Research

2.1.2.4 Key Industry Insights

2.1.3 Key Data From Primary Sources

2.1.4 Key Insights From Primary Sources

2.1.5 North American Healthcare Cloud Computing Market Size Estimation Methodology

2.1.6 Research Design

2.1.7 North American Healthcare Cloud Computing Market Data Validation and Triangulation

2.1.8 Assumptions for the Study

3 North American Healthcare Cloud Computing Market: Executive Summary (Page No. - 35)

3.1 Introduction

3.2 Current and Future Scenario

3.3 Growth Strategies

4 North American Healthcare Cloud Computing Market: Premium Insights (Page No. - 43)

4.1 North American Healthcare Cloud Computing Market

4.2 North American Healthcare Cloud Computing Market, By Component & Deployment Model

4.3 North American Healthcare Cloud Computing Market: By Geography

4.4 North American Healthcare Cloud Computing Market, By Pricing Model (2015 vs 2020)

4.5 North American Healthcare and Life Sciences Cloud Computing Market, By Service Model

5 North American Healthcare Cloud Computing Market: Market Overview (Page No. - 47)

5.1 Introduction

5.2 The Need of Cloud Computing in the Healthcare Ecosystem

5.3 Evolution of Cloud Computing in Healthcare

5.4 North American Healthcare Cloud Computing Market Segmentation

5.5 MNorth American Healthcare Cloud Computing arket Dynamics

5.5.1 Drivers

5.5.1.1 Reforms Directly Benefiting Healthcare It in North America

5.5.1.2 Proliferation of New Payment Models and Cost-Efficiency of Cloud

5.5.1.3 Usage of Cloud Improves Storage, Flexibility, and Scalability of Data

5.5.1.4 Growing Adoption of Information Technology to Boost Cloud Adoption and Reduce Healthcare Costs

5.5.1.5 Implementation of the Patient Protection and Affordable Care Act (Ppaca)

5.5.1.6 Dynamic Nature of Health Benefit Plan Designs

5.5.2 Restraints

5.5.2.1 Issues Related to Interoperability & Standardization of Cloud

5.5.2.2 Concerns Over Security of Patient Information

5.5.2.3 Migration From Legacy Systems is Considered as A Tedious Task By Providers

5.5.3 Opportunities

5.5.3.1 Telecloud to Create Opportunities for the North American Healthcare Cloud Computing Market

5.5.3.2 Formation of Accountable Care Organizations to Enhance Scope for Healthcare Cloud Computing

5.5.4 Challenge

5.5.4.1 Lack of Skilled Healthcare It Professionals

6 North American Healthcare Cloud Computing Market: Adoption Assessment (Page No. - 58)

6.1 Introduction

6.2 Cloud Computing Adoption By Healthcare Providers

6.2.1 Categorical Segmentation of Healthcare Providers

6.2.2 North America: Cloud Computing Deployment

6.2.3 Cloud Computing Adoption Assessment, By Healthcare Provider

6.2.4 Cloud Computing Adoption Assessment, By Vendor

6.2.4.1 Athenahealth, Inc.

6.2.4.2 Carestream Health, Inc.

6.3 Merge Healthcare, Inc.

6.4 Oracle Corporation

6.5 Carecloud Corporation

6.5.1 Cloud Computing Adoption Assessment, By Solution

6.5.1.1 Athenacollector

6.5.1.2 Carestream Vue PACS

6.5.1.3 Athenacommunicator

6.5.1.4 Merge PACS

6.5.1.5 Athenaclarity

6.6 Cloud Adoption Among Healthcare Payers

6.6.1 Categorical Segmentation of Healthcare Payers

6.6.2 North America: Indicative List of Cloud Computing Deployment By Healthcare Payers

6.6.3 Cloud Computing Adoption Assessment, By Healthcare Payer

6.6.4 Cloud Computing Adoption Assessment for Healthcare Payers, By Vendor

7 North American Healthcare Cloud Computing Market - Deployment Outlook (Page No. - 81)

7.1 Introduction

7.2 Mercy Memorial Hospital System Switches to Cloud Hcm for Effective People Management

7.3 Mu Medical (U.S.) Achieves Infrastructure Reliability By Moving to the Cloud

7.4 Wellero (Subsidiary of Cambia Health Solutions) Develops and Launches Innovative Healthcare App Through the Use of Windows Azure PAAS

7.5 Group Health Centre (GHC) Delivers Fully Customizable Personal Desktops to 800 Healthcare Facility Users With the Vmware Horizon Platform and Virtual Desktops

7.6 The Orchard Recovery Centre Protects Confidential Patient Data Through the Use of Ricoh�s Rcloud Services

8 North American Healthcare and Life Sciences Cloud Computing Market, By Application (Page No. - 86)

8.1 Introduction

8.2 Clinical Information Systems

8.2.1 Electronic Medical Record (EMR)

8.2.2 Picture Archiving & Communication System (PACS)

8.2.3 Radiology Information System (RIS)

8.2.4 Computerized Physician Order Entry (Cpoe) Systems

8.2.5 Laboratory Information Management System (LIMS)

8.2.6 Pharmacy Information System (PIS)

8.2.7 Other Clinical Information Systems

8.3 Nonclinical Information Systems (NCIS)

8.3.1 Revenue Cycle Management (RCM)

8.3.2 Automatic Patient Billing (APB)

8.3.3 Payroll Management Systems

8.3.4 Claims Management

8.3.5 Cost Accounting

8.3.6 Other Nonclinical Information Systems

8.4 North American Healthcare Cloud Computing Market, By Application

8.4.1 Clinical Research and R&D

8.4.2 Supply Chain

8.4.3 Payroll

8.4.4 Other Applications

9 North American Healthcare and Life Sciences Cloud Computing Market, By Deployment Model (Page No. - 110)

9.1 Introduction

9.2 Private Cloud

9.2.1 Drivers & Challenges

9.2.1.1 Drivers

9.2.1.1.1 Interoperability and Sharing of Data

9.2.1.1.2 Low Capital Cost

9.2.1.2 Challenges

9.2.1.2.1 Appropriate Vendor Selection

9.2.2 North American Healthcare Cloud Computing Market Trends

9.3 Public Cloud

9.3.1 Drivers and Challenges

9.3.1.1 Drivers

9.3.1.1.1 Growing Interest of Healthcare Information Among Patients

9.3.1.1.2 Enhancing Administrative Efficiency at Low Cost

9.3.1.2 Challenges

9.3.1.2.1 Security and Privacy Concerns

9.3.2 North American Healthcare Cloud Computing Market Trends

9.4 Hybrid Cloud

9.4.1 Drivers & Challenges

9.4.1.1 Drivers

9.4.1.1.1 Security and Affordability

9.4.1.1.2 It Infrastructure Stays on Premise

9.4.1.2 Challenges

9.4.1.2.1 Networking

9.4.2 North American Healthcare Cloud Computing Market Trends

10 North American Healthcare and Life Sciences Cloud Computing Market, By Component (Page No. - 120)

10.1 Introduction

10.2 Software

10.2.1 Clinical Information Systems (CIS)

10.2.2 Nonclinical Information Systems (NCIS) Or Nonclinical Healthcare Systems (NCHS)

10.3 Hardware

10.3.1 Access Devices

10.3.2 Peripherals

10.3.3 Servers

10.3.4 Storage Devices

10.3.5 Networking Devices

10.4 Services

10.4.1 Consulting Services

10.4.2 Implementation Services

10.4.3 Post-Sale & Maintenance Services

10.4.4 Training Services

11 North American Healthcare and Life Sciences Cloud Computing Market, By Pricing Model (Page No. - 129)

11.1 Introduction

11.2 Pay-As-You-Go

11.3 Spot Pricing Model

12 North American Healthcare and Life Sciences Cloud Computing Market, By Service Model (Page No. - 136)

12.1 Introduction

12.2 Software-As-A-Service (SAAS)

12.2.1 Benefits of SAAS

12.3 Infrastructure-As-A-Service (IAAS)

12.3.1 Benefits of IAAS

12.4 Platform-As-A-Service (PAAS)

12.4.1 Benefits of PAAS

13 North American Healthcare and Life Sciences Cloud Computing Market, By End User (Page No. - 147)

13.1 Introduction

13.2 Healthcare Providers

13.3 Healthcare Payers

13.4 Life Sciences Cloud Computing Market, By End User

14 North American Healthcare Cloud Computing Market, By Country (Page No. - 154)

14.1 Introduction

14.2 North America

14.2.1 U.S.

14.2.1.1 Growing Volume of Data in Medical Imaging

14.2.1.2 Conferences Help Create Product Awareness

14.2.1.3 Rise in Insurance Enrollments Triggered By Ppaca

14.2.1.4 Rising Adoption of EMR Systems

14.2.1.5 Cloud Computing Solutions Help in Curbing Healthcare Costs

14.2.1.6 Inadequate It Infrastructure Among Payers

14.2.2 Canada

14.2.2.1 Increased Healthcare Spending

14.2.2.2 Availability of Free Cloud Computing Resources for Entrepreneurs in Canada

15 North American Healthcare Cloud Computing Market: Competitive Landscape (Page No. - 176)

15.1 Overview

15.2 Competitive Situation and Trends

15.2.1 Agreements, Alliances, Collaborations, and Partnerships

15.2.2 New Product Launches

15.2.3 Acquisitions

15.2.4 Expansions

15.2.5 Others

16 North American Healthcare Cloud Computing Market: Company Profiles (Page No. - 182)

16.1 Athenahealth, Inc.

16.2 Carecloud Corporation

16.3 Carestream Health, Inc.

16.4 Cleardata Networks, Inc.

16.5 Dell Inc.

16.6 Global Net Access (GNAX)

16.7 IBM Corporation

16.8 Iron Mountain, Inc.

16.9 Oracle Corporation

16.10 Vmware, Inc.

*Details on Financials, Products & Services, Key Strategy, & Recent Developments Might Not Be Captured in Case of Unlisted Companies.

17 Appendix (Page No. - 205)

17.1 Discussion Guide

17.2 Company Developments (2012�2015)

17.2.1 Athenahealth, Inc.

17.2.2 Carecloud Corporation

17.2.3 Cleardata Networks, Inc.

17.2.4 IBM Corporation

17.2.5 Iron Mountain, Inc.

17.2.6 Oracle Corporation

17.3 Introducing RT: Real-Time Market Intelligence

17.4 Available Customizations

17.5 Related Reports

List of Tables (139 Tables)

Table 1 Growing Adoption of Information Technology to Boost the North American Healthcare Cloud Computing Market

Table 2 Safeguarding Patient Information is A Crucial Task in Cloud Computing

Table 3 Formation of Accountable Care Organizations to Enhance Scope for Healthcare Cloud Computing

Table 4 Healthcare Providers Classification Based on Bed Capacity

Table 5 Indicative List of Cloud Computing Deployment By Healthcare Providers (January 2010�September 2015)

Table 6 Leading Solutions From Athenahealth, Inc.

Table 7 Leading Solutions From Carestream Health, Inc.

Table 8 Leading Solutions From Merge Healthcare, Inc.

Table 9 Leading Solutions From Oracle Corporation

Table 10 Leading Solutions From Carecloud Corporation

Table 11 Cloud Solutions Adopted By Healthcare Providers (January 2010 to September 2015)

Table 12 Carestream Vue PACS: Product Information

Table 13 Merge PACS: Product Information

Table 14 Healthcare Payers Classification Based on Revenue (USD Million)

Table 15 Indicative List of Cloud Computing Deployment Among Healthcare Payers (January 2010�September 2015)

Table 16 North American Healthcare Cloud Computing Market Size, By Application, 2013�2020 (USD Million)

Table 17 North American Healthcare Cloud Computing Market Size, By Application, 2013�2020 (USD Million)

Table 18 North America: Cloud-Based Clinical Information Systems Market Size, By Type, 2013�2020 (USD Million)

Table 19 North America: Cloud-Based Clinical Information Systems Market Size, By Country, 2013�2020 (USD Million)

Table 20 North America: Cloud-Based Electronic Medical Records Market Size, By Country, 2013�2020 (USD Million)

Table 21 North America: Cloud-Based Picture Archiving & Communication Systems Market Size, By Country, 2013�2020 (USD Million)

Table 22 North America: Cloud-Based Radiology Information Systems Market Size, By Country, 2013�2020 (USD Million)

Table 23 North America: Cloud-Based Computerized Physician Order Entry Systems Market Size, By Country, 2013�2020 (USD Million)

Table 24 North America: Cloud-Based Laboratory Information Management Systems Market Size, By Country, 2013�2020 (USD Million)

Table 25 North America: Cloud-Based Pharmacy Information Systems Market Size, By Country, 2013�2020 (USD Million)

Table 26 North America: Other Clinical Information Systems Market Size, By Country, 2013�2020 (USD Million)

Table 27 North America: Cloud-Based Nonclinical Information Systems Market Size, By Type, 2013�2020 (USD Million)

Table 28 North America: Cloud-Based Nonclinical Information Systems Market Size, By Country, 2013�2020 (USD Million)

Table 29 North America: Cloud-Based Revenue Cycle Management Market Size, By Country, 2013�2020 (USD Million)

Table 30 North America: Cloud-Based Automatic Patient Billing Market Size, By Country, 2013�2020 (USD Million)

Table 31 North America: Cloud-Based Payroll Management Systems Market Size, By Country, 2013�2020 (USD Million)

Table 32 North America: Cloud-Based Claims Management Market Size, By Country, 2013�2020 (USD Million)

Table 33 North America: Cloud-Based Cost Accounting Systems Market Size, By Country, 2013�2020 (USD Million)

Table 34 North America: Other Nonclinical Information Systems Market Size, By Country, 2013�2020 (USD Million)

Table 35 North America: Life Sciences Cloud Computing Market Size, By Application, 2013�2020 (USD Million)

Table 36 North America: Life Sciences Cloud Computing Applications Market Size, By Country, 2013�2020 (USD Million)

Table 37 North America: Life Sciences Cloud Computing Market Size for Clinical Research and R&D Applications, By Country, 2013�2020 (USD Million)

Table 38 North American North American Healthcare Cloud Computing Market Size for Supply Chain Applications, By Country, 2013�2020 (USD Million)

Table 39 North American Healthcare Cloud Computing Market Size for Payroll Applications, By Country, 2013�2020 (USD Million)

Table 40 North America: Life Sciences Cloud Computing Market Size for Other Applications, By Country, 2013�2020 (USD Million)

Table 41 North American Healthcare Cloud Computing Market Size, By Deployment Model, 2013�2020 (USD Million)

Table 42 North American Healthcare Cloud Computing Market Size, By Deployment Model, 2013�2020 (USD Million)

Table 43 North American Healthcare Cloud Computing Market Size, By Deployment Model, 2013�2020 (USD Million)

Table 44 North America: Healthcare and Life Sciences Private Cloud Market Size, By Country, 2013�2020 (USD Million)

Table 45 North American Healthcare Cloud Computing Market Size, By Country, 2013�2020 (USD Million)

Table 46 North America: Life Sciences Private Cloud Market Size, By Country, 2013�2020 (USD Million)

Table 47 North America: Healthcare and Life Sciences Public Cloud Market Size, By Country, 2013�2020 (USD Million)

Table 48 North America: Healthcare Public Cloud Market Size, By Country, 2013�2020 (USD Million)

Table 49 North America: Life Sciences Public Cloud Market Size, By Country, 2013�2020 (USD Million)

Table 50 North America: Healthcare and Life Sciences Hybrid Cloud Market Size, By Country, 2013�2020 (USD Million)

Table 51 North America: Healthcare Hybrid Cloud Market Size, By Country, 2013�2020 (USD Million)

Table 52 North America: Life Sciences Hybrid Cloud Market Size, By Country, 2013�2020 (USD Million)

Table 53 North America: Healthcare and Life Sciences Cloud Computing Market Size, By Component, 2013�2020 (USD Million)

Table 54 North America: Healthcare Cloud Computing Market Size, By Component, 2013�2020 (USD Million)

Table 55 North America: Life Sciences Cloud Computing Market Size, By Component, 2013�2020 (USD Million)

Table 56 North America: Healthcare and Life Sciences Cloud Computing Software Market Size, By Country, 2013�2020 (USD Million)

Table 57 North America: Healthcare Cloud Computing Software Market Size, By Country, 2013�2020 (USD Million)

Table 58 North America: Life Sciences Cloud Computing Software Market Size, By Country, 2013�2020 (USD Million)

Table 59 North America: Healthcare and Life Sciences Cloud Computing Hardware Market Size, By Country, 2013�2020 (USD Million)

Table 60 North America: Healthcare Cloud Computing Hardware Market Size, By Country, 2013�2020 (USD Million)

Table 61 North America: Life Sciences Cloud Computing Hardware Market Size, By Country, 2013�2020 (USD Million)

Table 62 North America: Healthcare and Life Sciences Cloud Computing Services Market Size, By Country, 2013�2020 (USD Million)

Table 63 North America: Healthcare Cloud Computing Services Market Size, By Country, 2013�2020 (USD Million)

Table 64 North America: Life Sciences Cloud Computing Services Market Size, By Country, 2013�2020 (USD Million)

Table 65 North America: Healthcare and Life Sciences Cloud Computing Market Size, By Pricing Model, 2013�2020 (USDmillion)

Table 66 North America: Healthcare Cloud Computing Market Size, By Pricing Model, 2013�2020 (USD Million)

Table 67 North America: Life Sciences Cloud Computing Market Size, By Pricing Model, 2013�2020 (USD Million)

Table 68 North America: Healthcare and Life Sciences Cloud Computing Market Size for Pay-As-You-Go Model, By Country, 2013�2020 (USD Million)

Table 69 North America Healthcare Cloud Computing Market Size for Pay-As-You-Go Model, By Country, 2013�2020 (USD Million)

Table 70 North America: Life Sciences Cloud Computing Market Size for Pay-As-You-Go Model, By Country, 2013�2020 (USD Million)

Table 71 North America North American Healthcare Cloud Computing Market Size for Spot Pricing Model, By Country, 2013�2020 (USD Million)

Table 72 North America Healthcare Cloud Computing Market Size for Spot Pricing Model, By Country, 2013�2020 (USD Million)

Table 73 North America North American Healthcare Cloud Computing Market Size for Spot Pricing Model, By Country, 2013�2020 (USD Million)

Table 74 North America: Healthcare and Life Sciences Cloud Computing Market Size, By Service Model, 2013�2020 (USD Million)

Table 75 North America Healthcare Cloud Computing Market Size, By Service Model, 2013�2020 (USD Million)

Table 76 North America: Life Sciences Cloud Computing Market Size, By Service Model, 2013�2020 (USD Million)

Table 77 North America: Healthcare and Life Sciences Cloud Computing Market Size for SAAS, By Country, 2013�2020 (USD Million)

Table 78 North America Healthcare Cloud Computing Market Size for SAAS, By Country, 2013�2020 (USD Million)

Table 79 North America: Life Sciences Cloud Computing Market Size for SAAS, By Country, 2013�2020 (USD Million)

Table 80 North America: Healthcare and Life Sciences Cloud Computing Market Size for IAAS, By Country, 2013�2020 (USD Million)

Table 81 North America Healthcare Cloud Computing Market Size for IAAS, By Country, 2013�2020 (USD Million)

Table 82 North America: Life Sciences Cloud Computing Market Size for IAAS, By Country, 2013�2020 (USD Million)

Table 83 North America: Healthcare and Life Sciences Cloud Computing Market Size for PAAS, By Country, 2013�2020 (USD Million)

Table 84 North America Healthcare Cloud Computing Market Size for PAAS, By Country, 2013�2020 (USD Million)

Table 85 North America: Life Sciences Cloud Computing Market Size for PAAS, By Country, 2013�2020 (USD Million)

Table 86 North America: Healthcare and Life Sciences Cloud Computing Market Size, By End User, 2013�2020 (USD Million)

Table 87 North America Healthcare Cloud Computing Market Size, By End User, 2013�2020 (USD Million)

Table 88 North America: Life Sciences Cloud Computing Market Size, By End User, 2013�2020 (USD Million)

Table 89 North America Healthcare Cloud Computing Market Size for Healthcare Providers, By Country, 2013�2020 (USD Million)

Table 90 North America: Cloud Computing Market Size for Healthcare Payers, By Country, 2013�2020 (USD Million)

Table 91 North America: Cloud Computing Market Size for Life Sciences, By Country, 2013�2020 (USD Million)

Table 92 North America Healthcare Cloud Computing Market Size for Life Sciences, By Type, 2013�2020 (USD Million)

Table 93 North America Healthcare Cloud Computing Market Size for Pharmaceutical Companies, By Country, 2013�2020 (USD Million)

Table 94 North America Healthcare Cloud Computing Market Size for Biopharmaceutical & Biotechnology Companies, By Country, 2013�2020 (USD Million)

Table 95 North America Healthcare Cloud Computing Market Size for Cros, By Country, 2013�2020 (USD Million)

Table 96 North America: Healthcare and Life Sciences Cloud Computing Market Size, By Country, 2013�2020 (USD Million)

Table 97 North America Healthcare Cloud Computing Market Size, By Country, 2013�2020 (USD Million)

Table 98 North America: Life Sciences Cloud Computing Market Size, By Country, 2013�2020 (USD Million)

Table 99 U.S.: Healthcare and Life Sciences Cloud Computing Market Size, By Application, 2013-2020 (USD Million)

Table 100 U.S.: Healthcare Cloud Computing Market Size, By Application, 2013-2020 (USD Million)

Table 101 U.S.: Life Sciences Cloud Computing Market Size, By Application, 2013-2020 (USD Million)

Table 102 U.S.: Healthcare and Life Sciences Cloud Computing Market Size, By Deployment Model, 2013-2020 (USD Million)

Table 103 U.S.: Healthcare Cloud Computing Market Size, By Deployment Model, 2013-2020 (USD Million)

Table 104 U.S.: Life Sciences Cloud Computing Market Size, By Deployment Model, 2013-2020 (USD Million)

Table 105 U.S.: Healthcare and Life Sciences Cloud Computing Market Size, By Service Model, 2013-2020 (USD Million)

Table 106 U.S.: Healthcare Cloud Computing Market Size, By Service Model, 2013-2020 (USD Million)

Table 107 U.S.: Life Sciences Cloud Computing Market Size, By Service Model, 2013-2020 (USD Million)

Table 108 U.S.: Healthcare and Life Sciences Cloud Computing Market Size, By Pricing Model, 2013-2020 (USD Million)

Table 109 U.S.: Healthcare Cloud Computing Market Size, By Pricing Model, 2013-2020 (USD Million)

Table 110 U.S.: Life Sciences Cloud Computing Market Size, By Pricing Model, 2013-2020 (USD Million)

Table 111 U.S.: Healthcare and Life Sciences Cloud Computing Market Size, By Component, 2013-2020 (USD Million)

Table 112 U.S.: Healthcare Cloud Computing Market Size, By Component, 2013-2020 (USD Million)

Table 113 U.S.: Life Sciences Cloud Computing Market Size, By Component, 2013-2020 (USD Million)

Table 114 U.S.: Healthcare and Life Sciences Cloud Computing Market Size, By End User, 2013-2020 (USD Million)

Table 115 U.S.: Healthcare Cloud Computing Market Size, By End User, 2013-2020 (USD Million)

Table 116 U.S.: Life Sciences Cloud Computing Market Size, By End User, 2013-2020 (USD Million)

Table 117 Canada: Healthcare and Life Sciences Cloud Computing Market Size, By Application, 2013-2020 (USD Million)

Table 118 Canada: Healthcare Cloud Computing Market Size, By Application, 2013-2020 (USD Million)

Table 119 Canada: Life Sciences Cloud Computing Market Size, By Application, 2013-2020 (USD Million)

Table 120 Canada: Healthcare and Life Sciences Cloud Computing Market Size, By Deployment Model, 2013-2020 (USD Million)

Table 121 Canada: Healthcare Cloud Computing Market Size, By Deployment Model, 2013-2020 (USD Million)

Table 122 Canada: Life Sciences Cloud Computing Market Size, By Deployment Model, 2013-2020 (USD Million)

Table 123 Canada: Healthcare and Life Sciences Cloud Computing Market Size, By Service Model, 2013-2020 (USD Million)

Table 124 Canada: Healthcare Cloud Computing Market Size, By Service Model, 2013-2020 (USD Million)

Table 125 Canada: Life Sciences Cloud Computing Market Size, By Service Model, 2013-2020 (USD Million)

Table 126 Canada: Healthcare and Life Sciences Cloud Computing Market Size, By Pricing Model, 2013-2020 (USD Million)

Table 127 Canada: Healthcare Cloud Computing Market Size, By Pricing Model, 2013-2020 (USD Million)

Table 128 Canada: Life Sciences Cloud Computing Market Size, By Pricing Model, 2013-2020 (USD Million)

Table 129 Canada: Healthcare and Life Sciences Cloud Computing Market Size, By Component, 2013-2020 (USD Million)

Table 130 Canada: Healthcare Cloud Computing Market Size, By Component, 2013-2020 (USD Million)

Table 131 Canada: Life Sciences Cloud Computing Market Size, By Component, 2013-2020 (USD Million)

Table 132 Canada: Healthcare and Life Sciences Cloud Computing Market Size, By End User, 2013-2020 (USD Million)

Table 133 Canada: Healthcare Cloud Computing Market Size, By End User, 2013-2020 (USD Million)

Table 134 Canada: Life Sciences Cloud Computing Market Size, By End User, 2013-2020 (USD Million)

Table 135 North American Healthcare Cloud Computing Market: Agreements, Partnerships, Collaborations, and Partnerships, 2012�2015

Table 136 North American Healthcare Cloud Computing Market: New Product Launches, 2012�2015

Table 137 North American Healthcare Cloud Computing Market: Acquisitions, 2012�2015

Table 138 North American Healthcare Cloud Computing Market: Expansions, 2012�2015

Table 139 North American Healthcare Cloud Computing Market: Others, 2012�2015

List of Figures (45 Figures)

Figure 1 North American Healthcare and Lifesciences Cloud Computing Market: Research Methodology Steps

Figure 2 Sampling Frame: Primary Research

Figure 3 Breakdown of Primary Interviews: By Company Type, Designation, and Region

Figure 4 North American Healthcare Cloud Computing Market: Size Estimation Methodology: Bottom-Up Approach

Figure 5 North American Healthcare Cloud Computing Market: Size Estimation Methodology: Top-Down Approach

Figure 6 North American Healthcare Cloud Computing Market: Research Design

Figure 7 North American Healthcare Cloud Computing Market: Data Triangulation Methodology

Figure 8 Healthcare It Delivery Modes

Figure 9 Clinical Information Systems Market to Witness the Higher CAGR From 2015 to 2020

Figure 10 Private Cloud Segment to Account for the Largest Market Size in 2015

Figure 11 Software Segment to Account for the Largest Market Size in 2015

Figure 12 Pay-As-You-Go Segment to Command the Largest Market Share in 2015

Figure 13 SAAS Segment Expected to Dominate the Healthcare and Life Sciences Cloud Computing Market During the Forecast Period

Figure 14 Healthcare Providers Segment Expected to Dominate the Healthcare and Life Sciences Cloud Computing Market During the Forecast Period

Figure 15 U.S. Slated to Witness the Highest Growth in the North American Healthcare and Life Sciences Cloud Computing Market in the Forecast Period

Figure 16 Reforms Across North American Countries Supporting the Use of Healthcare It to Drive Market Growth

Figure 17 The U.S. to Witness Highest Growth During the Forecast Period

Figure 18 Pay-As-You-Go Model to Command the Largest Share of the Market in 2015

Figure 19 Infrastructure-As-A-Service (IAAS) Segment to Witness Highest Growth From 2015 to 2020

Figure 20 Traditional Ecosystem vs the Cloud Ecosystem in Healthcare

Figure 21 North American Healthcare Cloud Computing: Market Segmentation

Figure 22 North American Life Sciences Cloud Computing: Market Segmentation

Figure 23 North American Healthcare Cloud Computing Market: Drivers, Restraints, and Opportunities

Figure 24 Cloud Computing Adoption Trend in the Healthcare Industry

Figure 25 Adoption of Cloud Computing Technologies, By Healthcare Provider (January 2010�September 2015)

Figure 26 Leading Vendors Providing Cloud Services to Healthcare Providers (January 2010�September 2015)

Figure 27 Top 5 Healthcare Cloud Solution Vendors (January 2010�September2015)

Figure 28 Adoption of Cloud Computing Technology Among Healthcare Payers (January 2010�September 2015)

Figure 29 Microsoft Corporation and Hewlett-Packard Were Leading Cloud Vendors for Healthcare Payers

Figure 30 Clinical Information Systems Segment to Dominate the North American Healthcare Cloud Computing Applications Market During the Forecast Period

Figure 31 Clinical Research and R&D Segment to Dominate the North American Life Sciences Cloud Computing Applications Market During the Forecast Period

Figure 32 Private Cloud Market to Grow at the Highest CAGR During the Forecast Period

Figure 33 Software Segment to Grow at the Highest Rate During the Forecast Period

Figure 34 Pay-As-You-Go Model Likely to Grow at A Higher Rate During the Forecast Period

Figure 35 SAAS Segment to Account for the Largest Share of the North American Healthcare and Life Sciences Cloud Computing Market in 2015

Figure 36 SAAS, IAAS, & PAAS Service Models

Figure 37 Healthcare Providers to Hold Larger Market Share in 2015

Figure 38 U.S. to Witness the Highest Growth in the Healthcare and Life Sciences Cloud Computing Market in North America

Figure 39 Battle for Market Share: Agreements, Alliances, Collaborations, and Partnerships Was the Key Strategy

Figure 40 Athenahealth, Inc.: Company Snapshot

Figure 41 Dell Inc.: Company Snapshot

Figure 42 IBM Corporation: Company Snapshot

Figure 43 Iron Mountain, Inc.: Company Snapshot

Figure 44 Oracle Corporation: Company Snapshot

Figure 45 Vmware, Inc.: Company Snapshot

Generating Response ...

Generating Response ...

Growth opportunities and latent adjacency in North American Healthcare Cloud Computing Market