Seed Treatment Fungicides Market by Type (Chemical (Benzimidazoles, Dithiocarbamates), Biological), Crop Type (Cereals & Grains, Oilseeds & Pulses), Application Technique (Coating, Dressing, Pelleting), Form, and Region - Global Forecast to 2022

[153 Pages Report] The seed treatment fungicides market was valued at USD 1.13 Billion in 2016. It is projected to grow at a CAGR of 9.24% from 2017, to reach 1.88 Billion by 2022. The base year considered for the study is 2016 and the forecast period is from 2017 to 2022. The objectives of the study are to define, segment, and measure the size of the seed treatment fungicides market with respect to its type, crop type, application technique, form, and region. The report also aims to provide detailed information about the crucial factors influencing the growth of the market, strategical analysis of micro-markets, opportunities for stakeholders, details of competitive landscape, and profile of the key players with respect to their market share and competencies.

This report includes estimations of the market size in terms of value (USD million). Both, top-down and bottom-up approaches have been used to estimate and validate the size of the global seed treatment fungicides market and to estimate the size of various other dependent submarkets in the overall market. Key players in the market have been identified through secondary research; some of the sources are press releases, annual reports, financial journals, and paid databases such as Factiva and Bloomberg. All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources. The figure below shows the breakdown of profiles of industry experts that participated in the primary discussions.

To know about the assumptions considered for the study, download the pdf brochure

The key players that have been profiled in this report include BASF SE (Germany), Syngenta AG (Switzerland), Bayer CropScience AG (Germany), Monsanto Company (U.S.), Nufarm Limited (Australia), The Dow Chemical Company (U.S.), FMC Corporation (U.S.), Novozymes A/S (Denmark), Platform Specialty Products Corporation (U.S.), and Sumitomo Chemical Company Ltd. (Japan).

This report is targeted at the existing players in the industry, which are as follows:

- Seed treatment fungicide manufacturers

- Seed treatment fungicide importers and exporters

- Seed treatment fungicide traders, distributors, and suppliers

- Government and research organizations

- Commercial research & development (R&D) institutions and financial institutions

“The study answers several questions for stakeholders, primarily which market segments to focus on in next two to five years for prioritizing efforts and investments”.

Scope of the report

On the basis of Type, the seed treatment fungicides market has been segmented as follows:

- Chemical (benzimidazoles, dithiocarbamates, phenylamides, chloronitriles, strobilurins, triazoles, and others)

- Biological (microbials and biochemical)

On the basis of Crop Type, the seed treatment fungicides market has been segmented as follows:

- Cereals & grains

- Oilseeds & pulses

- Others (fruits & vegetables, turf & ornamentals, plantation crops, fiber crops, and silage & forage crops)

On the basis of Application Technique, the seed treatment fungicides market has been segmented as follows:

- Coating

- Dressing

- Pelleting

On the basis of Form, the seed treatment fungicides market has been segmented as follows:

- Liquid

- Powder

On the basis of Region, the seed treatment fungicides market has been segmented as follows:

- North America

- Europe

- Asia-Pacific

- South America

- Rest of the World (RoW)

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the company’s specific scientific needs.

The following customization options are available for the report:

Product Analysis

- Product matrix, which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

- Further breakdown of the Rest of Europe seed treatment fungicides market into the Netherlands, Finland, Ireland, Greece, Austria, and Denmark.

- Further breakdown of the Rest of Asia-Pacific seed treatment fungicides market into Indonesia, Bangladesh, and Vietnam.

- Further breakdown of the Rest of South America seed treatment fungicides market into Chile, Venezuela, and Peru

Company Information

- Detailed analyses and profiling of additional market players (up to five)

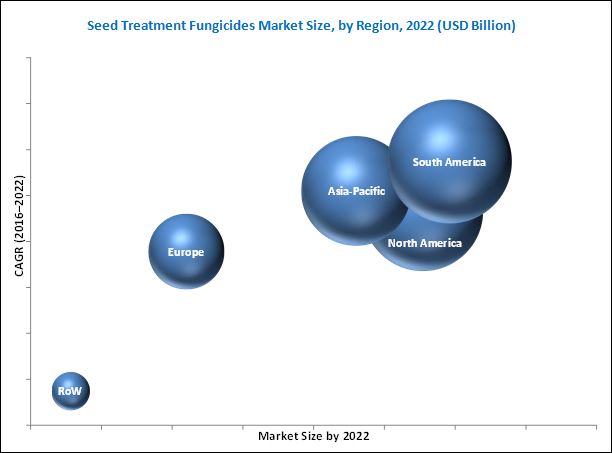

The seed treatment fungicides market is projected to grow at a CAGR of 9.24% from 2017, to reach a projected value of USD 1.88 Billion by 2022. Increasing usage of seed treatment solutions on expensive GM seeds, growth in the area under GM crops, increasing crop demand for biofuel and feed, and the use of fungicides as a low-cost crop protection solution are enhancing the market for seed treatment fungicides, globally. The growth in the fungicide seed treatment market is also driven by advanced farming technologies which ensure safe and reliable application of seed treatment formulas.

The market for cereals & grains is projected to grow at the highest rate due to the rise in demand for agricultural production. Increasing demand from downstream markets in the food & beverage and feed industries has boosted the overall demand for seed treatment fungicides across the globe.

The seed dressing segment accounted for more than half of the total application technique market in 2016. Since it a low-cost technique compared to other techniques (such as coating and pelleting), it is economical to use on low-cost cereals and grains, such as wheat and corn, which are the major crop types dominating the seed treatment fungicides market.

The biological seed treatment market is expected to have a high CAGR during the forecast period, since it is an eco-friendly method for crop protection; consumers also show a preference for these fungicides as they are obtained from natural resources.

South America led the seed treatment fungicides market in 2016 and is also the fastest-growing market owing to increased area under major seed treatment crops, such as corn and soybean. The demand for seed treatment products in the Asia-Pacific region is expected to be primarily driven by countries such as China and India.

Multiple registrations of seed treatment products in different countries has been a matter of concern in the seed treatment fungicides market since the assessment and understanding of requirements of different markets and then complying with them involves a significant investment of time and money.

The market for seed treatment fungicides consists of key players in the agricultural industry, such as BASF SE (Germany), Syngenta AG (Switzerland), Nufarm Limited (Australia), Bayer Crop Science AG (Germany), and Platform Specialty Products Company (U.S.). New product launches and expansion into different regions across the globe are the most preferred strategies adopted by key players to gain a larger share of the market.

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 15)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Market Scope

1.4 Periodization Considered for the Study

1.5 Currency Considered for the Study

1.6 Stakeholders

2 Research Methodology (Page No. - 19)

2.1 Research Data

2.1.1 Secondary Data

2.1.2 Primary Data

2.1.2.1 Breakdown of Primaries

2.1.2.2 Key Industry Insights

2.2 Market Size Estimation

2.2.1 Bottom-Up Approach

2.2.2 Top-Down Approach

2.3 Market Breakdown & Data Triangulation

2.4 Research Assumptions & Limitations

2.4.1 Assumptions

2.4.2 Limitations

3 Executive Summary (Page No. - 26)

4 Premium Insights (Page No. - 31)

4.1 Attractive Opportunities in the Seed Treatment Fungicides Market

4.2 Seed Treatment Fungicides Market, By Form

4.3 South American Seed Treatment Fungicides Market, By Country and Crop Type

4.4 Seed Treatment Fungicides Market, By Type

4.5 Seed Treatment Fungicides Market, Market Share of Top Countries

5 Market Overview (Page No. - 36)

5.1 Introduction

5.2 Macro Indicators

5.2.1 Reduction of Arable Land

5.2.2 Growing Environmental Concerns

5.2.3 Global Rise in Export of Pesticides

5.3 Market Dynamics

5.3.1 Drivers

5.3.1.1 Fungicides as A Low-Cost Crop Protection Solution

5.3.1.2 Increased Usage of Seed Treatment Solutions on High Priced GM Seeds and Increase in Area Under GM Crops

5.3.1.3 Increasing Crop Demand for Biofuel and Feed

5.3.2 Restraints

5.3.2.1 Stringent Government Regulations

5.3.2.2 Depressed Commodity Prices and Lower Farm Incomes

5.3.2.3 Structural Weakness of the Seed Treatment Industry in Asia-Pacific and African Economies

5.3.3 Opportunities

5.3.3.1 Rapid Growth in Biological Crop Protection Solutions

5.3.3.2 Technological Advancements in Seed Treatment

5.3.4 Challenges

5.3.4.1 Absence of Uniform International Policy Regarding Registration of Seed Treatment Fungicides

5.4 Value Chain Analysis

5.5 Supply Chain Analysis

6 Seed Treatment Fungicides Market, By Type (Page No. - 49)

6.1 Introduction

6.2 Synthetic Chemical

6.3 Biological

7 Seed Treatment Fungicides Market, By Crop Type (Page No. - 54)

7.1 Introduction

7.2 Cereals & Grains

7.2.1 Corn

7.2.2 Wheat

7.2.3 Rice

7.2.4 Other Cereals & Grains

7.3 Oilseeds & Pulses

7.3.1 Soybean

7.3.2 Canola

7.3.3 Other Oilseeds & Pulses

7.4 Other Crop Types

8 Seed Treatment Fungicides Market, By Application Technique (Page No. - 63)

8.1 Introduction

8.2 Seed Dressing

8.3 Seed Coating

8.4 Seed Pelleting

9 Seed Treatment Fungicides Market, By Form (Page No. - 69)

9.1 Introduction

9.2 Liquid

9.3 Powder

10 Seed Treatment Fungicides Market, By Region (Page No. - 73)

10.1 Introduction

10.2 North America

10.2.1 U.S.

10.2.2 Canada

10.2.3 Mexico

10.3 Europe

10.3.1 France

10.3.2 Germany

10.3.3 Russia

10.3.4 Rest of Europe

10.4 Asia-Pacific

10.4.1 China

10.4.2 India

10.4.3 Japan

10.4.4 Australia

10.4.5 Rest of Asia-Pacific

10.5 South America

10.5.1 Brazil

10.5.2 Argentina

10.5.3 Rest of South America

10.6 Rest of the World (RoW)

10.6.1 South Africa

10.6.2 Others in RoW

11 Competitive Landscape (Page No. - 104)

11.1 Introduction

11.2 Vendor Dive Analysis

11.2.1 Vanguard

11.2.2 Innovator

11.2.3 Dynamic

11.2.4 Emerging

11.3 Competitive Benchmarking

11.3.1 Product Offerings (For 25 Players)

11.3.2 Business Strategy (For 25 Players)

*Top 25 Companies Analyzed for This Study are – BASF SE (Germany), Syngenta AG (Switzerland), Bayer Cropscience AG (Germany), Monsanto Company (U.S.), Nufarm Limited (Australia), Platform Specialty Products Company (U.S.), Sumitomo Corporation (Japan), E.I. Du Pont De Nemours and Company (U.S.), the DOW Chemical Company (U.S.), FMC Corporation (U.S.), Incotec Group Bv (The Netherlands), Certis Europe LLC (U.S.), Adama Agricultural Solutions Ltd. (Israel), Arysta Lifescience (U.S.), Novozymes A/S (Denmark), Upl (India), Rallis India Limited (India), Tagros Chemicals India Ltd., (India), Germains Seed Technology (U.K.), Wilbur-Ellis Holdings, Inc (U.S.), Helena Chemical Company (U.S.), Loveland Products, Inc (U.S.), Rotam (China), Winfield Solutions, LLC. (U.S.), Auswest Seeds (Australia)

11.4 Market Share Analysis

12 Company Profiles (Page No. - 109)

(Business Overview, Company Scorecard, Product Offering, Business Strategy & Recent Developments)*

12.1 Bayer Cropscience AG

12.2 BASF SE

12.3 Syngenta AG

12.4 Du Pont

12.5 Nufarm Limited

12.6 Monsanto Company

12.7 FMC Corporation

12.8 Novozymes

12.9 Platform Specialty Products Corporation

12.10 Sumitomo Corporation

12.11 Adama Agricultural Solutions Ltd

*Details on Business Overview, Company Scorecard, Product Offering, Business Strategy & Recent Developments Might Not Be Captured in Case of Unlisted Companies.

13 Appendix (Page No. - 146)

13.1 Discussion Guide

13.2 Knowledge Store: Marketsandmarkets’ Subscription Portal

13.3 Introducing RT: Real-Time Market Intelligence

13.4 Available Customizations

13.5 Related Reports

13.6 Author Details

List of Tables (75 Tables)

Table 1 Seed Treatment Fungicides Market Scope

Table 2 World Protein Production, Fao Forecast Until 2050 (Million Metric Tons)

Table 3 Seed Treatment Fungicides Market Size, By Type, 2015-2022 (USD Million)

Table 4 Synthetic Chemical Seed Treatment Fungicides Market Size, By Region, 2015-2022 (USD Million)

Table 5 Synthetic Chemical Seed Treatment Fungicides Market Size, By Type, 2015-2022 (USD Million)

Table 6 Biological Seed Treatment Fungicides Market Size, By Region, 2015-2022 (USD Million)

Table 7 Biological Seed Treatment Fungicides Market Size, By Type, 2015-2022 (USD Million)

Table 8 Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 9 Seed Treatment Fungicides Market Size in Cereals & Grains, By Region, 2015–2022 (USD Million)

Table 10 Seed Treatment Fungicides Market Size in Cereals & Grains, By Crop, 2015–2022 (USD Million)

Table 11 Seed Treatment Fungicides Market Size in Oilseeds & Pulses, By Region, 2015–2022 (USD Million)

Table 12 Seed Treatment Fungicides Market Size in Oilseeds & Pulses, By Crop, 2015–2022 (USD Million)

Table 13 Seed Treatment Fungicides Market Size in Other Crop Types, By Region, 2015–2022 (USD Million)

Table 14 Seed Treatment Fungicides Market Size, By Application Technique, 2015-2022 (USD Million)

Table 15 Seed Dressing Market Size, By Region, 2015–2022 (USD Million)

Table 16 Seed Coating Market Size, By Region, 2015–2022 (USD Million)

Table 17 Seed Pelleting Market Size, By Region, 2015–2022 (USD Million)

Table 18 Seed Treatment Fungicides Market Size, By Form, 2015–2022 (USD Million)

Table 19 Liquid Seed Treatment Fungicides Market Size, By Region, 2015–2022 (USD Million)

Table 20 Powder Seed Treatment Fungicides Market Size, By Region, 2015–2022 (USD Million)

Table 21 Seed Treatment Fungicides Market Size, By Region, 2015–2022 (USD Million)

Table 22 North America: Seed Treatment Fungicides Market Size, By Country, 2015–2022 (USD Million)

Table 23 North America: Seed Treatment Fungicides Market Size, By Type, 2015–2022 (USD Million)

Table 24 North America: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 25 North America: Seed Treatment Fungicides Market Size, By Application Technique, 2015–2022 (USD Million)

Table 26 North America: Seed Treatment Fungicides Market Size, By Form, 2015–2022 (USD Million)

Table 27 U.S.: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 28 Canada: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 29 Mexico: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 30 Europe: Seed Treatment Fungicides Market Size, By Country, 2015–2022 (USD Million)

Table 31 Europe: Seed Treatment Fungicides Market Size, By Type, 2015–2022 (USD Million)

Table 32 Europe: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 33 Europe: Seed Treatment Fungicides Market Size, By Application Technique, 2015–2022 (USD Million)

Table 34 Europe: Seed Treatment Fungicides Market Size, By Form, 2015–2022 (USD Million)

Table 35 France: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 36 Germany: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 37 Russia: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 38 Rest of Europe: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 39 Key Crops Cultivated, By Country/Region

Table 40 Asia-Pacific: Seed Treatment Fungicides Market Size, By Country, 2015–2022 (USD Million)

Table 41 Asia-Pacific: Seed Treatment Fungicides Market Size, By Type, 2015–2022 (USD Million)

Table 42 Asia-Pacific: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 43 Asia-Pacific: Seed Treatment Fungicides Market Size, By Application Technique, 2015–2022 (USD Million)

Table 44 Asia-Pacific: Seed Treatment Fungicides Market Size, By Form, 2015–2022 (USD Million)

Table 45 China: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 46 India: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 47 Japan: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 48 Australia: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 49 Rest of Asia-Pacific: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 50 South America: Seed Treatment Fungicides Market Size, By Country, 2015–2022 (USD Million)

Table 51 South America: Seed Treatment Fungicides Market Size, By Type, 2015–2022 (USD Million)

Table 52 South America: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 53 South America: Seed Treatment Fungicides Market Size, By Application Technique, 2015–2022 (USD Million)

Table 54 South America: Seed Treatment Fungicides Market Size, By Form, 2015–2022 (USD Million)

Table 55 Brazil: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 56 Argentina: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 57 Rest of South America: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 58 RoW: Seed Treatment Fungicides Market Size, By Country, 2015–2022 (USD Million)

Table 59 RoW: Seed Treatment Fungicides Market Size, By Type, 2015–2022 (USD Million)

Table 60 RoW: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 61 RoW: Seed Treatment Fungicides Market Size, By Application Technique, 2015–2022 (USD Million)

Table 62 RoW: Seed Treatment Fungicides Market Size, By Form, 2015–2022 (USD Million)

Table 63 South Africa: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 64 Others in RoW: Seed Treatment Fungicides Market Size, By Crop Type, 2015–2022 (USD Million)

Table 65 Bayer Cropscience AG: Products Offered

Table 66 BASF SE: Products Offered

Table 67 Syngenta AG: Products Offered

Table 68 Du Pont: Products Offered

Table 69 Nufarm Limited: Products Offered

Table 70 Monsanto Company: Products Offered

Table 71 FMC Corporation: Products Offered

Table 72 Novozymes: Products Offered

Table 73 Platform Specialty Products Corporation: Products Offered

Table 74 Sumitomo Corporation: Products Offered

Table 75 Adama Agricultural Solutions Ltd: Products Offered

List of Figures (66 Figures)

Figure 1 Seed Treatment Fungicides Market: Research Design

Figure 2 Breakdown of Primary Interviews: By Company Type, Designation & Region

Figure 3 Market Size Estimation Methodology: Bottom-Up Approach

Figure 4 Market Size Estimation Methodology: Top-Down Approach

Figure 5 Data Triangulation

Figure 6 Cereals & Grains Segment Projected to Be the Fastest-Growing Crop Type During the Forecast Period (2017 vs 2022)

Figure 7 Seed Dressing: Most Attractive Application Technique in the Seed Treatment Fungicides Market 2016

Figure 8 Synthetic Chemical Seed Treatment Fungicides is Projected to Account for the Largest Share During the Forecast Period (2017-2022)

Figure 9 Liquid Form of Seed Treatment Fungicides to Be More Widely Used During the Forecast Period (2017 vs 2022)

Figure 10 South America is Projected to Register Highest Growth Rate During the Forecast Period (2017 vs 2022)

Figure 11 Attractive Opportunities in the Seed Treatment Fungicides Market

Figure 12 Liquid Segment to Dominate the Market During the Forecast Period (2017-2022)

Figure 13 Cereals & Grains Segment Accounted for the Largest Share in the South American Seed Treatment Fungicides Market in 2016

Figure 14 Synthetic Chemical Seed Treatment Fungicides to Dominate the Market Across All Regions in 2017

Figure 15 Brazil Dominated the Seed Treatment Fungicides Market in 2016

Figure 16 Per Capita Arable Land, 2000–2014

Figure 17 Export Value of Pesticides, 2004–2014 (USD Million)

Figure 18 Seed Treatment Fungicides Market: Drivers, Restraints, Opportunities, and Challenges

Figure 19 Increase in Global Area Under GM Crops, 1996-2016 (Million Hectares)

Figure 20 Biofuels Market, By Type, 2015 - 2022

Figure 21 U.S. Commodity Price for Crop Production and Net Farm Income, 2010-2017 (USD Billion)

Figure 22 Value Chain Analysis: Significant Value Added During R&D and Production Phases

Figure 23 Supply Chain: Research & Development Plays A Key Role in Seed Treatment Market

Figure 24 Synthetic Chemical Segment is Projected to Dominate the Market Through 2022

Figure 25 Synthetic Chemical Seed Treatment Fungicides Market Size, By Region, 2017 vs 2022 (USD Million)

Figure 26 Cereals & Grains to See Highest Growth in the Seed Treatment Market During Forecast Period

Figure 27 Seed Dressing to Dominate the Seed Treatment Fungicides Market By 2022 (USD Million)

Figure 28 Liquid Form Segment to Dominate the Seed Treatment Fungicides Market Throughout the Forecast Period (2017 vs 2022)

Figure 29 Geographical Snapshot (2017–2022): Rapidly Growing Markets are Emerging as New Hotspots

Figure 30 South America is Projected to Dominate the Seed Treatment Fungicides Market During the Forecast Period

Figure 31 South American Seed Treatment Fungicides Market Snapshot

Figure 32 Dive Chart

Figure 33 Market Share Analysis, By Segmental Revenue 2016

Figure 34 Bayer Cropscience AG: Company Snapshot

Figure 35 Bayer Crop Science AG: Product Offering Scorecard

Figure 36 Bayer Crop Science AG: Business Strategy Scorecard

Figure 37 BASF SE: Company Snapshot

Figure 38 BASF SE: Product Offering Scorecard

Figure 39 BASF SE: Business Strategy Scorecard

Figure 40 Syngenta AG: Company Snapshot

Figure 41 Syngenta AG: Product Offering Scorecard

Figure 42 Syngenta AG: Business Strategy Scorecard

Figure 43 Du Pont: Company Snapshot

Figure 44 Du Pont: Product Offering Scorecard

Figure 45 Du Pont: Business Strategy Scorecard

Figure 46 Nufarm Limited: Company Snapshot

Figure 47 Nufarm Limited: Product Offering Scorecard

Figure 48 Nufarm Limited: Business Strategy Scorecard

Figure 49 Monsanto Company: Company Snapshot

Figure 50 Monsanto Company: Product Offering Scorecard

Figure 51 Monsanto Company: Business Strategy Scorecard

Figure 52 FMC Corporation: Company Snapshot

Figure 53 FMC Corporation: Product Offering Scorecard

Figure 54 FMC Corporation: Business Strategy Scorecard

Figure 55 Novozymes (Novozymes Bioag): Company Snapshot

Figure 56 Novozymes: Product Offering Scorecard

Figure 57 Novozymes: Business Strategy Scorecard

Figure 58 Platform Specialty Products Corporation: Company Snapshot

Figure 59 Platform Specialty Products Corporation: Product Offering Scorecard

Figure 60 Platform Specialty Products Corporation: Business Strategy Scorecard

Figure 61 Sumitomo Corporation: Company Snapshot

Figure 62 Sumitomo Corporation: Product Offering Scorecard

Figure 63 Sumitomo Corporation: Business Strategy Scorecard

Figure 64 Adama Agricultural Solutions Ltd: Company Snapshot

Figure 65 Adama Agricultural Solutions Ltd: Product Offering Scorecard

Figure 66 Adama Agricultural Solutions Ltd: Business Strategy Scorecard

Growth opportunities and latent adjacency in Seed Treatment Fungicides Market