This study involved four major activities in estimating the current size of the stem cell therapy market. Exhaustive secondary research was carried out to collect information on the market, its peer markets, and its parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation procedures were used to estimate the market size of segments and subsegments.

Secondary Research

Secondary research was used mainly to identify and collect information for the extensive technical, market-oriented, and commercial study of the stem cell therapy market. The secondary sources used for this study include Some of the key secondary sources referred to for this study include publications from government sources World Health Organization, Organisation for Economic Co-operation and Development, The World Bank, US Census Bureau, International Society for Stem Cell Research (US), National Stem Cell Foundation (US), International Society for Cellular Therapy (ISCT), EuroStemCell, European Society of Gene and Cell Therapy, German Stem Cell Network, Japan Human Cell Society, Chinese Stem Cell Foundation, Brazilian Association of Cell Therapy, Alliance for Regenerative Medicine (ARM)]. These sources were also used to obtain key information about major players, market classification, and segmentation according to industry trends, regional/country-level markets, market developments, and technology perspectives.

Primary Research

In-depth interviews were conducted with various primary respondents, including key industry participants, subject-matter experts (SMEs), C-level executives of key market players, and industry consultants, among other experts, to obtain and verify the critical qualitative and quantitative information as well as assess future prospects of the market. Various primary sources from both the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information. The following is a breakdown of the primary respondents:

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

The global size of the stem cell therapy market was estimated through multiple approaches. A detailed market estimation approach was followed to estimate and validate the value of the market and other dependent submarkets. These methods were also used extensively to estimate the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

-

The major players in the industry and market have been identified through extensive primary and secondary research.

-

The revenues generated from the stem cell therapy business of players operating in the market have been determined through secondary research and primary analysis.

-

All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

Market Size Estimation Methodology-Bottom-up approach

To know about the assumptions considered for the study, Request for Free Sample Report

Top-down Approach-

Data Triangulation

After estimating the overall market size from the market size estimation process, the total market was split into several segments and subsegments. To complete the overall market engineering process and arrive at the exact statistics for all segments and subsegments, data triangulation and market breakdown procedures were employed, wherever applicable. The data was triangulated by studying various factors and trends from both the demand and supply sides.

Market Definition

Stem cells, characterized by their undifferentiated nature, possess a distinct capacity to transform into specialized cell types with specific functions. Stem cell therapy, a medical intervention, utilizes these cells to address and mitigate diseases and injuries. These stem cells can be procured from various sources such as umbilical Cord, bone-marrow, embryo, adipose (fat) tissue, blood, and the brain among others. Stem cell therapy is currently being utilized for a diverse range of disease conditions.

Key Stakeholders

-

Stem cell Research Institutes

-

Cancer research institutes

-

Stem cell therapy raw material suppliers

-

Biotechnology & biopharmaceutical companies

-

Drug manufacturers, vendors, and distributors

-

Academic & government research institutes

-

Venture capitalists & investors

-

Government organizations

-

Private research firms

-

Academic & Research Institutes

-

Research & development (R&D) companies

-

Hospitals and Speciality Clinics

The main objectives of this study are as follows:

-

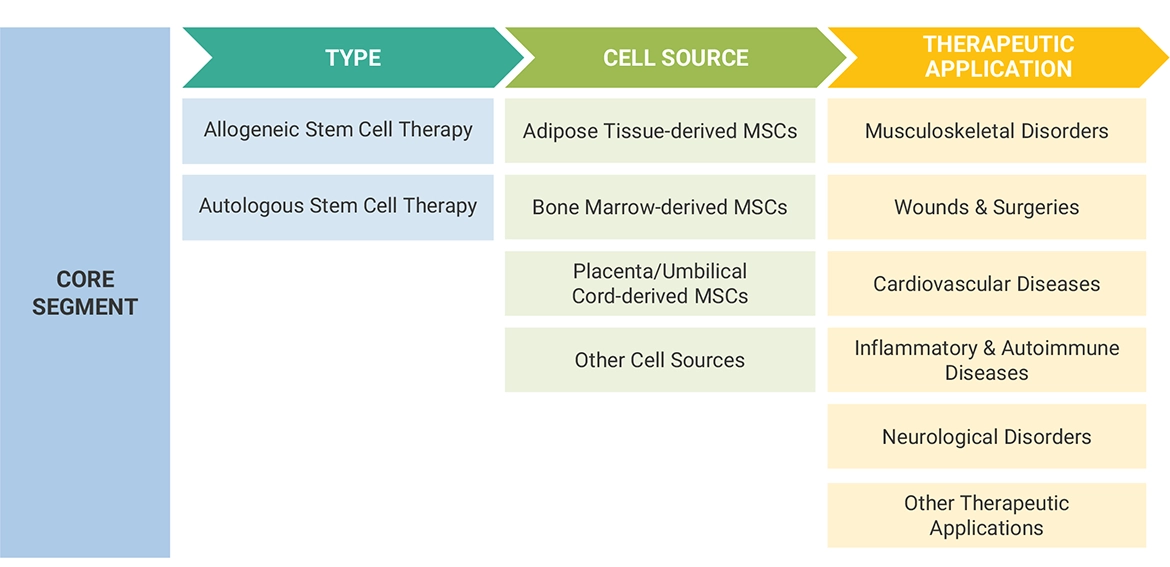

To define, describe, and forecast the stem cell therapy market based on type, cell source, therapeutic application and region

-

To provide detailed information regarding the major factors influencing the growth of the market (such as drivers, restraints, challenges, opportunities and trends)

-

To strategically analyze micromarkets with respect to individual growth trends, future prospects, and contributions to the overall stem cell therapy market

-

To analyze opportunities in the market for stakeholders and provide details of the competitive landscape for market leaders

-

To forecast the size of the market segments with respect to five main regions, namely, North America, Europe, Asia Pacific, Rest of the World

-

To strategically profile the key players and comprehensively analyze their product portfolios, market positions, and core competencies

-

To track and analyze competitive developments such as acquisitions, product launches, expansions, agreements, partnerships, and R&D activities in the stem cell therapy market.

Available Customizations

With the given market data, MarketsandMarkets offers customizations as per the company’s specific needs. The following customization options are available for this report:

-

Country-wise Information: Analysis for additional countries (up to five)

-

Company Information: Detailed analysis and profiling of additional market players (up to five)

Growth opportunities and latent adjacency in Stem Cell Therapy Market