Thermoforming Plastic Market by Plastic Type (PP, PS, PET, PE, PVC, Bio-plastics, ABS), Thermoforming Type (Vacuum Formed, Pressure Formed, Mechanical Formed), Parts Type (Thin Gauge, Thick Gauge), End-use Industry, and Region - Global Forecast to 2024

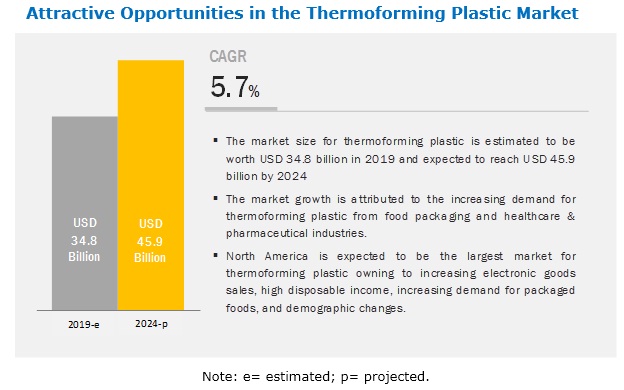

[173 Pages Report] The thermoforming plastic market is projected to grow from USD 34.8 billion in 2019 to USD 45.9 billion by 2024, at a CAGR of 5.7% between 2019 and 2024. The thermoforming plastic industry is growing due to the rising healthcare & pharmaceuticals and food & agriculture packaging industries and increasing manufacturing activities. The increasing popularity of retail shopping and rising consumer spending for processed & packed goods are fuelling the demand for thermoforming plastic. Factors such as changing demographics and lifestyles have shifted the market toward e-retailing channels and convenient packaging, which in turn will drive the demand for thermoforming plastic.

The food & agriculture packaging end-use industry is expected to be the largest consumer of thermoforming plastic, globally.

Thermoforming plastic finds application in food & agriculture packaging, healthcare & pharmaceutical, construction, electrical & electronics, automotive packaging & structures, consumer goods & appliances, and others. Food & agriculture packaging industry dominated the thermoforming plastic market in terms of value in 2018. This growth is attributed mainly to the huge demand for packaged and branded products. Thermoforming plastic provides better protection during transportation and uses safe packaging materials; hence, they are preferred in the food & agriculture packaging industry.

The PP-based thermoforming plastic segment is expected to account for a major share of the thermoforming plastic market, in terms of value and volume, during the forecast period.

The thermoforming plastic market is segmented based on plastic-type as polypropylene (PP), polystyrene (PS), polyethylene terephthalate (PET), polyethylene (PE), polyvinyl chloride (PVC), bioplastics, acronytrile butadiene styrene (ABS), and others. The global thermoforming plastic market is dominated by the PP, in terms of value and volume. This is due to the extensive use of this plastic in packaging applications such as food, medical device, and automotive. The excellent strength-to-weight ratio, excellent energy management, resilient, good chemical resistance, and durability make it an ideal choice for packaging applications.

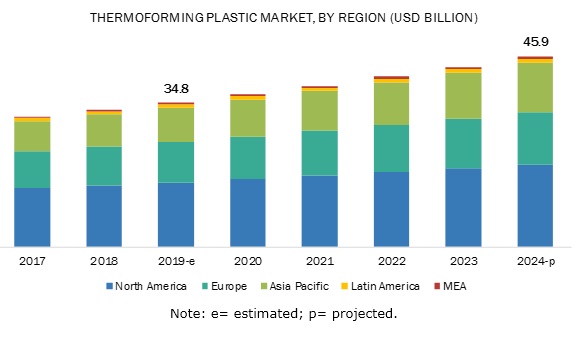

North America is expected to lead the thermoforming plastic market during the forecast period.

North America accounted for the largest share in the global thermoforming plastic market in 2018. Technological advancements in the packaging industry primarily drive the market in this region. The demand for thermoforming plastic will be driven by factors such as increasing electronic goods sales, high disposable income, increasing demand for packaged foods, and demographic changes. The region is characterized by continuous technological advancements in the thermoforming plastic industry with the presence of some key regional players such as Pactiv LLC, Sonoco Products Company, D&W Fine Pack LLC, Fabri-Kal Corporation and Dart Container Corporation.

The US is a key market in North America. The increasing demand for consumer durables will drive the market for in the U.S. as thermoforming plastic finds growing use in it. The demand for thermoforming plastic in the US is likely to witness robust growth during the forecast period, as a result of the rising trend of retail shopping.

Key Market Players

The thermoforming plastic market comprises major solution providers, such as Fabri-Kal Corp. (US), Berry Global Inc. (US), Genpak LLC (US), Pactiv LLC (US), D&W Fine Pack LLC (US), Amcor Ltd. (Australia), Dart Container Corp. (US), Anchor Packaging (US), Sabert Corporation (US), Sonoco Products Company (US). The study includes an in-depth competitive analysis of these key players in the thermoforming plastic market, with their company profiles, recent developments, and key market strategies.

Sabert Corporation (US) is one of the prime manufacturers of thermoforming plastic in the North American region. Sabeart Corporation is a leading manufacturer of innovative food packaging products and solutions for food distributors, restaurants & caterers, grocery stores, national food chains, and consumer entertaining. The company provides a variety of food packaging for displaying, serving, & storing fine food. The company also recycles plastics going to landfill in Riverside, CA facility. The main products provided by the company include Catering Collection Packaging, Green Collection Packaging, Hot Collection Packaging, Cold Collection Packaging, and Bakery Collection Packaging. It is involved in implementing business strategies such as expansion, and acquisition to increase its market share around the globe. For instance, in February 2018, Sabert Corporation expanded its manufacturing facility, located in Greenville, Texas, for manufacturing 100% compostable packaging made from plant-based materials. This helped the company to deliver more options to its customers.

Scope of the Report

|

Report Metric |

Details |

|

Years considered for the study |

2019�2024 |

|

Base year |

2018 |

|

Forecast period |

2019�2024 |

|

Units considered |

Value (USD Million), Volume (Kiloton) |

|

Segments |

Plastic-type, thermoforming type, thickness, and end-use industry and region |

|

Regions |

Europe, North America, APAC, MEA, and Latin America |

|

Companies |

Fabri-Kal Corp. (US), Berry Global Inc. (US), Genpak LLC (US), Pactiv LLC (US), D&W Fine Pack LLC (US), Amcor Ltd. (Australia), Dart Container Corp. (US), Anchor Packaging (US), Sabert Corporation (US), Sonoco Products Company (US) |

This research report categorizes the thermoforming plastic market based on plastic-type, thermoforming type, thickness, end-use industry, and region.

Based on plastic-type, the thermoforming plastic market has been segmented as follows:

- PP

- Polystyrene

- PET

- PE

- PVC

- Bio-plastics

- ABS

Based on thermoforming type, the thermoforming plastic market has been segmented as follows:

- Vacuum Forming

- Pressure Forming

- Mechanical Forming

Based on thickness, the thermoforming plastic market has been segmented as follows:

- Thin Gauge

- Thick Gauge

Based on end-use industry, the thermoforming plastic market has been segmented as follows:

- Food & Agricultural Packaging

- Consumer Goods & Appliances

- Healthcare & Pharmaceutical

- Construction

- Electrical & Electronics

- Automotive Packaging & Structures

- Others (industrial and aerospace)

Based on the region, the thermoforming plastic market has been segmented as follows:

- North America

- Europe

- APAC

- MEA

- Latin America

Recent Developments

- In October 2018, Genpak LLC launched new product Clover, which is a microwavable, reusable, and recyclable container that was created as a sustainable, affordable option. This helped the company to make a significant contribution to innovative dining concepts like home delivery and upscale catering.

- In December 2018, Fabri-Kal Corporation expanded the production line of its SideKicks Containers. The company is now providing new 12 and 16 oz. SideKicks Containers. This helped the company to meet the demand of its customers.

- In July 2019, Berry Global acquired RPC Group Plc at approximately $6.5 billion. This gave the company an opportunity to leverage their combined know-how in innovative material science, product development, and manufacturing technologies.

Key Questions Addressed By The Report

- Which are the major end-use industries of thermoforming plastic?

- Which industry is the major consumer of thermoforming plastic?

- Which region is the largest and fastest-growing market for thermoforming plastic?

- What are the major plastic types of thermoforming plastic?

- What are the major thermoforming types of thermoforming plastic?

- What are the major thickness types of thermoforming plastic?

- What are the major strategies adopted by leading market players?

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 17)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Market Scope

1.3.1 Thermoforming Plastic Market: Market Segmentation

1.3.2 Years Considered for the Report

1.4 Currency

1.5 Unit Considered

1.6 Stakeholders

1.7 Limitations

2 Research Methodology (Page No. - 21)

2.1 Research Data

2.2 Secondary Data

2.2.1.1 Key Data From Secondary Sources

2.2.2 Primary Data

2.2.2.1 Key Data From Primary Sources

2.2.2.2 Key Industry Insights

2.2.2.3 Breakdown of Primary Interviews

2.3 Market Size Estimation

2.3.1 Supply Side Analysis

2.4 Data Triangulation

2.5 Research Assumptions

2.6 Limitations

3 Executive Summary (Page No. - 29)

4 Premium Insights (Page No. - 34)

4.1 Attractive Opportunities in the Thermoforming Plastic Market

4.2 Thermoforming Plastic Market, By Thickness

4.3 Thermoforming Plastic Market, By Thermoforming Type

4.4 Thermoforming Plastic Market Size, By Plastic Type

4.5 Thermoforming Plastic Market, By End-Use Industry and Region

4.6 Thermoforming Plastic Market, By Country

5 Market Overview (Page No. - 38)

5.1 Introduction

5.2 Market Dynamics

5.2.1 Drivers

5.2.1.1 Growing Demand From Food Packaging Industry

5.2.1.2 Growing Demand From Healthcare & Pharmaceutical Industry

5.2.1.3 Reduced Packaging Waste

5.2.1.4 Cost Effectiveness

5.2.2 Restraints

5.2.2.1 Not Supportive to Package Heavy Items

5.2.3 Opportunities

5.2.3.1 Increasing Demand of In-Mold Labelling in Packaging

5.2.3.2 Potential Opportunities of Thermoforming Plastic in Emerging Economies

5.2.3.3 Investment in R&D Activities

5.2.4 Challenges

5.2.4.1 Compliance With Stringent Regulations

5.3 Porter�s Five Forces Analysis

5.3.1 Threat of New Entrants

5.3.2 Threat of Substitutes

5.3.3 Bargaining Power of Suppliers

5.3.4 Bargaining Power of Buyers

5.3.5 Intensity of Competitive Rivalry

6 Macroeconomic Overview and Key Trends (Page No. - 45)

6.1 Introduction

6.2 Trends and Forecast of Gdp

6.3 Trends in Aerospace Industry

6.4 Trends in Automotive Industry

7 Thermoforming Plastic Market, By Plastic Type (Page No. - 49)

7.1 Introduction

7.2 Polypropylene (PP)

7.3 Polystyrene (PS)

7.4 Polyethylene Terephthalate (PET)

7.5 Polyethylene (PE)

7.6 Poly Vinyl Chloride (PVC)

7.7 Bio-Plastics

7.8 Acronytrile Butadene Styrene (ABS)

7.9 Others

8 Thermoforming Plastic Market, By Thermoforming Type (Page No. - 61)

8.1 Introduction

8.2 Vacuum Forming

8.3 Pressure Forming

8.4 Mechanical Forming

9 Thermoforming Plastic Market, By Thickness (Page No. - 67)

9.1 Introduction

9.2 Thin Gauge

9.3 Thick Gauge

10 Thermoforming Plastic Market, By End-Use Industry (Page No. - 72)

10.1 Introduction

10.2 Food & Agriculture Packaging

10.3 Consumer Goods & Appliances

10.4 Healthcare & Pharmaceautical

10.5 Construction

10.6 Electrical & Electronics

10.7 Automotive Packaging & Structures

10.8 Others

11 Thermoforming Plastic Market, By Region (Page No. - 85)

11.1 Introduction

11.2 North America

11.2.1 US

11.2.1.1 Increasing Sales of Consumer Durables and Presence of Large Thermoforming Plastic Manufacturers in the US are Driving the Market

11.2.2 Canada

11.2.2.1 Flourishing Food & Beverage and Consumer Durables Industries are Propelling the Market

11.3 Europe

11.3.1 Germany

11.3.1.1 Large Food Processing Industry is A Major Driving Factor for the Thermoforming Plastic Market in Germany

11.3.2 UK

11.3.2.1 High Spending on Healthcare Sector is Fueling the Market Growth in the UK

11.3.3 France

11.3.3.1 Large Electrical & Electronics and Automotive Industries in the Country is Helping the Market Growth

11.3.4 Italy

11.3.4.1 Growth of Major End-Use Industries, Including Consumer Goods & Appliances and Electrical & Electronics is Expected to Support the Market Growth

11.3.5 Netherlands

11.3.5.1 Thermoforming Plastic Finds Wide Use in the Netherlands Food & Agriculture Packaging and Healthcare & Pharmaceutical Packaging Industries 104

11.3.6 Rest of Europe

11.4 APAC

11.4.1 China

11.4.1.1 Growing Food & Beverages Industry and Large Population are Expected to Drive the Market

11.4.2 Japan

11.4.2.1 Technology Advancements and Large Retail Industry are the Two Major Factors That are Driving the Market

11.4.3 India

11.4.3.1 Rising Middle-Class Population, Rapid Industrialization, Continuous Influx of Multinational Companies Will Influence the Market Positively

11.4.4 Australia

11.4.4.1 Rising Consumption of Packed Foods and Presence of Prominent Thermoforming Plastic Manufacturers Will Influence the Market Positively

11.4.5 South Korea

11.4.5.1 Heavy Investment in Automotive and Consumer Electronics Sectors is Anticipated to Increase Thermoforming Plastic Consumption

11.4.6 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.1.1 Advantages Associated With Use of Thermoforming Plastic is Driving the Market

11.5.2 Mexico

11.5.2.1 Increasing Demand From Automotive and Electrical & Electronics Industries is Expected to Drive the Market

11.5.3 Argentina

11.5.3.1 Rapid Urbanization is Fueling the Thermoforming Plastic Market Growth

11.6 Middle East & Africa (MEA)

11.6.1 South Africa

11.6.1.1 The Growth of the Middle Class Population is Increasing the Demand for Thermoforming Plastic

11.6.2 UAE

11.6.2.1 High Investments in Infrastructure Projects and Changing Consumer Preferences are Driving the Market

11.6.3 Saudi Arabia

11.6.3.1 Large Middle Class Population is Driving the Market

12 Competitive Landscape (Page No. - 131)

12.1.1 Partnerships

12.1.2 Expansions

12.1.3 New Product Launches

12.1.4 Acquisitions

13 Competitive Landscape (Page No. - 135)

13.1 Introduction

13.1.1 Dynamic Differentiators

13.1.2 Innovators

13.1.3 Visionary Leaders

13.1.4 Emerging Companies

13.2 Competitive Benchamarking

1.3.1 Product Offering 137

1.3.2 Business Strategy 138

13.2.1 Market Ranking

14 Company Profiles (Page No. - 140)

14.1 Pactiv LLC

14.1.1 Business Overview

14.1.2 Products Offered

14.1.3 Recent Developments

14.1.4 Pactiv LLC: SWOT Analysis

14.1.5 MnM View

14.2 Amcor Limited

14.2.1 Business Overview

14.2.2 Products Offered

14.2.3 Recent Developments

14.2.4 Amcor Limited: SWOT Analysis

14.2.5 MnM View

14.3 Dart Container Corporation

14.3.1 Business Overview

14.3.2 Products Offered

14.3.3 SWOT Analysis

14.3.4 MnM View

14.4 Sonoco Products Company

14.4.1 Business Overview

14.4.2 Products Offered

14.4.3 Recent Developments

14.4.4 SWOT Analysis

14.4.5 MnM View

14.5 D&W Fine Pack LLC

14.5.1 Business Overview

14.5.2 Products Offered

14.5.3 Recent Developments

14.5.4 SWOT Analysis

14.5.5 MnM View

15 Company Profiles (Page No. - 153)

15.5 Sabert Corporation

15.5.1 Business Overview

15.5.2 Products Offered

15.5.3 Recent Developments

15.5.4 MnM View

15.6 Genpak LLC

15.6.1 Business Overview

15.6.2 Products Offered

15.6.3 Recent Developments

15.6.4 MnM View

15.7 Fabri-Kal Corporation

15.7.1 Business Overview

15.7.2 Products Offered

15.7.3 Recent Developments

15.7.4 MnM View

15.8 Anchor Packaging

15.8.1 Business Overview

15.8.2 Products Offered

15.8.3 Recent Developments

15.8.4 MnM View

15.9 Berry Global Group Inc.

15.9.1 Business Overview

15.9.2 Products Offered

15.9.3 Recent Developments

15.9.4 MnM View

15.10 Other Key Players

15.10.1 Consolidated Container Company

15.10.2 Brentwood Industries

15.10.3 Placon Corporation

15.10.4 Winpak Ltd.

15.10.5 Spencer Industries Incorporated

15.10.6 Display Pack Inc.

15.10.7 Greiner Packaging International GmbH

15.10.8 Penda Corporation

15.10.9 Huntamaki

15.10.10 Zhuhai Zhongfu Enterprise Co. Limited.

16 Appendix (Page No. - 165)

16.1 Discussion Guide

16.2 Knowledge Store: Marketsandmarkets Subscription Portal

16.3 Available Customizations

16.4 Related Reports

16.5 Author Details

List of Tables (143 Tables)

Table 1 Thermoforming Plastic Market Size, 2017�2024

Table 1 Trends and Forecast of Gdp, 2017�2024 (USD Billion)

Table 2 Number of New Airplane Deliveries, By Region, 2017

Table 3 Automotive Production, Million Units (2017�2018)

Table 4 Thermoforming Plastic Market Size, By Plastic Type, 2017�2024 (USD Million)

Table 5 Thermoforming Plastics Market Size, By Plastic Type, 2017�2024 (Kiloton)

Table 6 PP Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 7 PP Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 8 PS Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 9 PS Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 10 PET Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 11 PET Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 12 PE Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 13 PE Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 14 Pvc Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 15 Pvc Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 16 Bio-Plastics Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 17 Bio-Plastics Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 18 ABS Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 19 ABS Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 20 Others Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 21 Others Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 22 Thermoforming Plastic Market Size, By Thermoforming Type, 2017�2024 (USD Million)

Table 23 Thermoforming Plastics Market Size, By Thermoforming Type, 2017�2024 (Kiloton)

Table 24 Vacuum Forming Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 25 Vacuum Forming Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 26 Pressure Forming Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 27 Pressure Forming Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 28 Mechanical Forming Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 29 Mechanical Forming Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 30 Thermoforming Plastic Market Size, By Parts, 2017�2024 (USD Million)

Table 31 Thermoforming Plastics Market Size, By Parts, 2017�2024 (Kiloton)

Table 32 Thin Gauge Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 33 Thin Gauge Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 34 Thick Gauge Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 35 Thick Gauge Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 36 Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 37 Thermoforming Plastics Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 38 Food & Agriculture Packaging Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 39 Food & Agriculture Packaging Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 40 Consumer Goods & Appliances Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 41 Consumer Goods & Appliances Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 42 Healthcare & Pharmaceautical Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 43 Healthcare & Pharmaceautical Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 44 Construction Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 45 Construction Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 46 Electrical & Electronics Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 47 Electrical & Electronics Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 48 Automotive Packaging & Structures Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 49 Automotive Packaging & Structures Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 50 Others Thermoforming Plastic Market, By Region, 2017�2024 (USD Million)

Table 51 Others Thermoforming Plastics Market, By Region, 2017�2024 (Kiloton)

Table 52 Thermoforming Plastic Market Size, By Region, 2017�2024 (Kiloton)

Table 53 Thermoforming Plastics Market Size, By Region, 2017�2024 (USD Million)

Table 54 North America: Thermoforming Plastic Market Size, By Country, 2017�2024 (Kiloton)

Table 55 North America: Market Size, By Country, 2017�2024 (USD Million)

Table 56 North America: Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 57 North America: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 58 North America: Market Size, By Plastic Type, 2017�2024 (USD Million)

Table 59 North America: Market Size, By Plastic Type, 2017�2024 (Kiloton)

Table 60 North America: Market Size, By Thermoforming Type, 2017�2024 (USD Million)

Table 61 North America: Market Size, By Thermoforming Type, 2017�2024 (Kiloton)

Table 62 North America: Market Size, By Parts Type, 2017�2024 (USD Million)

Table 63 North America: Market Size, By Parts Type, 2017�2024 (Kiloton)

Table 64 US: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 65 US: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 66 Canada: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 67 Canada: Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 68 Europe: Thermoforming Plastic Market Size, By Country, 2017�2024 (USD Million)

Table 69 Europe: Market Size, By Country, 2017�2024 (Kiloton)

Table 70 Europe: Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 71 Europe: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 72 Europe: Market Size, By Plastic Type, 2017�2024 (USD Million)

Table 73 Europe: Market Size, By Plastic Type, 2017�2024 (Kiloton)

Table 74 Europe: Market Size, By Thermoforming Type, 2017�2024 (USD Million)

Table 75 Europe: Market Size, By Thermoforming Type, 2017�2024 (Kiloton)

Table 76 North America: Market Size, By Parts Type, 2017�2024 (USD Million)

Table 77 Europe: Market Size, By Parts Type, 2017�2024 (Kiloton)

Table 78 Germany: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 79 Germany: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 80 UK: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 81 UK: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 82 France: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 83 France: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 84 Italy: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 85 Italy: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 86 Thermoforming Plastics: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 87 Thermoforming Plastics: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 88 APAC: Thermoforming Plastic Market Size, By Country, 2017�2024 (USD Million)

Table 89 APAC: Market Size, By Country, 2017�2024 (Kiloton)

Table 90 APAC: Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 91 APAC: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 92 APAC: Market Size, By Plastic Type, 2017�2024 (USD Million)

Table 93 APAC: Market Size, By Plastic Type, 2017�2024 (Kiloton)

Table 94 APAC: Market Size, By Thermoforming Type, 2017�2024 (USD Million)

Table 95 APAC: Market Size, By Thermoforming Type, 2017�2024 (Kiloton)

Table 96 APAC: Market Size, By Parts Type, 2017�2024 (USD Million)

Table 97 APAC: Market Size, By Parts Type, 2017�2024 (Kiloton)

Table 98 China: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 99 China: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 100 Japan: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 101 Japan: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 102 India: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 103 India: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 104 Australia: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 105 Australia: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 106 South Korea: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 107 South Korea: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 108 Latin America: Thermoforming Plastic Market Size, By Country, 2017�2024 (USD Million)

Table 109 Latin America: Market Size, By Country, 2017�2024 (Kiloton)

Table 110 Latin America: Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 111 Latin America: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 112 Latin America: Market Size, By Plastic Type, 2017�2024 (USD Million)

Table 113 Latin America: Market Size, By Plastic Type, 2017�2024 (Kiloton)

Table 114 Latin America: Market Size, By Thermoforming Type, 2017�2024 (USD Million)

Table 115 Latin America: Market Size, By Thermoforming Type, 2017�2024 (Kiloton)

Table 116 Latin America: Market Size, By Parts Type, 2017�2024 (USD Million)

Table 117 Latin America: Market Size, By Parts Type, 2017�2024 (Kiloton)

Table 118 Brazil: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 119 Brazil: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 120 Mexico: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 121 Mexico: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 122 Argentina: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 123 Argentina: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 124 MEA: Thermoforming Plastic Market Size, By Country, 2017�2024 (USD Million)

Table 125 MEA: Market Size, By Country, 2017�2024 (Kiloton)

Table 126 MEA: Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 127 MEA: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 128 MEA: Market Size, By Plastic Type, 2017�2024 (USD Million)

Table 129 MEA: Market Size, By Plastic Type, 2017�2024 (Kiloton)

Table 130 MEA: Market Size, By Thermoforming Type, 2017�2024 (USD Million)

Table 131 MEA: Market Size, By Thermoforming Type, 2017�2024 (Kiloton)

Table 132 MEA: Market Size, By Parts Type, 2017�2024 (USD Million)

Table 133 MEA: Market Size, By Parts Type, 2017�2024 (Kiloton)

Table 134 South Africa: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 135 South Africa: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 136 UAE: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 137 UAE: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 138 Saudi Arabia: Thermoforming Plastic Market Size, By End-Use Industry, 2017�2024 (USD Million)

Table 139 Saudi Arabia: Market Size, By End-Use Industry, 2017�2024 (Kiloton)

Table 140 Partnerships, 2015�2019

Table 141 Expansions, 2015�2019

Table 142 New Product Launches, 2015�2019

Table 143 Acquisitions, 2015�2019

List of Figures (50 Figures)

Figure 1 Thermoforming Plastic Market: Research Design

Figure 2 Market Number Estimation

Figure 3 Methodology: Supply Side Sizing

Figure 4 Thermoforming Plastic Market: Data Triangulation

Figure 5 Vacuum Forming Segment Dominated Overall Market in 2018

Figure 6 Thin Gauge Segment Dominated Overall Market in 2018

Figure 7 PP Based Thermoforming Plastic Dominated Overall Market in 2018

Figure 8 Food & Agriculture Packaging Dominates Overall Thermoforming Plastic Market

Figure 9 US to Be the Largest Market for Thermoforming Plastic, in Terms of Value

Figure 10 North America to Be the Largest Thermoforming Plastic Market

Figure 11 High Demand From Healthcare & Pharmaceautical and Automotive Industries to Drive the Market

Figure 12 Thin Gauge Thermoforming Plastic to Dominate Overall Thermoforming Plastic Market

Figure 13 Vacuum Forming Plastic to Be Fastest-Growing Segment in Overall Market

Figure 14 PP Segment to Be Dominant Plastic Type of Thermoforming Plastic Market

Figure 15 Food & Agriculture Packaging Segment to Dominate Overall Thermoforming Plastic Market

Figure 16 China to Register Highest CAGR in Thermoforming Plastic Market

Figure 17 Drivers, Restraints, Opportunities, and Challenges in the Thermoforming Plastic Market

Figure 18 Porter�s Five Forces Analysis

Figure 19 Trends and Forecast of Gdp, 2019�2024 (USD Billion)

Figure 20 New Airplane Deliveries, By Region, 2017

Figure 21 Automotive Production in Key Countries, Million Units (2017 vs. 2018)

Figure 22 PP to Dominate the Overall Thermoforming Plastic Market, in Terms of Value, During Forecast Period

Figure 23 North America to Dominate the Overall PP Market, in Terms of Value, During Forecast Period

Figure 24 North America to Dominate the PS Market, in Terms of Value, During Forecast Period

Figure 25 North America to Dominate the PET Market, in Terms of Value, During Forecast Period

Figure 26 Vacuum Forming to Dominate the Overall Thermoforming Plastic Market, in Terms of Value, During Forecast Period

Figure 27 Thin Gauge to Dominate the Overall Thermoforming Plastic Market, in Terms of Value, During Forecast Period

Figure 28 Food & Agriculture Packaging to Dominate the Overall Thermoforming Plastic Market, in Terms of Value, During Forecast Period

Figure 29 North America to Dominate the Food & Agriculture Packaging Market, in Terms of Value, During Forecast Period

Figure 30 North America to Dominate the Consumer Goods & Appliances Market, in Terms of Value, During Forecast Period

Figure 31 North America to Dominate the Healthcare & Pharmaceautical Market, in Terms of Value, During Forecast Period

Figure 32 China to Register the Highest CAGR

Figure 33 North America: Thermoforming Plastic Market Snapshot

Figure 34 Europe: Thermoforming Plastic Market Snapshot

Figure 35 APAC: Thermoforming Plastic Market Snapshot

Figure 36 Acquisition is the Most Preferred Growth Strategies Adopted By Major Players Between 2015 and 2019

Figure 37 Dive Chart

Figure 38 Pactiv LLC: Company Snapshot

Figure 39 Amcor Limited: Company Snapshot

Figure 40 Dart Container Corporation: Company Snapshot

Figure 41 Dart Container Corporation: SWOT Analysis

Figure 42 Sonoco Products Company: Company Snapshot

Figure 43 Sonoco Products Company: SWOT Analysis

Figure 44 D&W Fine Pack LLC: Company Snapshot

Figure 45 D&W Fine Pack LLC: SWOT Analysis

Figure 46 Sabert Corporation: Company Snapshot

Figure 47 Genpak LLC: Company Snapshot

Figure 48 Fabri-Kal Corporation: Company Snapshot

Figure 49 Anchor Packaging: Company Snapshot

Figure 50 Berry Global Group Inc.: Company Snapshot

The study involved four major activities in estimating the current size for thermoforming plastic market. Exhaustive secondary research was done to collect information on the market, the peer market, and the parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both the top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation procedures were used to estimate the size of market segments and sub-segments.

Secondary Research

In the secondary research process, various secondary sources such as Hoovers, Bloomberg BusinessWeek, and Factiva were referred to, to identify and collect information for this study. These secondary sources included annual reports, press releases & investor presentations of companies, white papers, certified publications, articles by recognized authors, gold standard & silver standard websites, regulatory bodies, trade directories, and databases.

Primary Research

The thermoforming plastic market comprises several stakeholders such as raw material suppliers, processors, end-product manufacturers, and regulatory organizations in the supply chain. The demand side of this market is characterized by the development of various industries such as food & agriculture packaging, healthcare & pharmaceutical, construction, electrical & electronics, automotive packaging & structures, consumer goods & appliances, and other industries. Advancements in technology and diverse applications characterize the supply side. Various primary sources from both the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information.

Following is the breakdown of primary respondents:

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

Both the top-down and bottom-up approaches were used to estimate and validate the total thermoforming plastic market. These methods were also used extensively to estimate the size of various sub-segments in the market. The research methodology used to estimate the market size included the following:

- The key players in the industry and markets were identified through extensive secondary research.

- The industry�s supply chain and market size, in terms of value, were determined through primary and secondary research processes.

- All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources.

Data Triangulation

After arriving at the overall market size using the market size estimation processes as explained above, the market was split into several segments and sub-segments. To complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment, the data triangulation, and market breakdown procedures were employed, wherever applicable. The data was triangulated by studying various factors and trends from both the demand and supply sides in the food & agriculture packaging, healthcare & pharmaceutical, construction, electrical & electronics, automotive packaging & structures, consumer goods & appliances, and other industries.

Report Objectives

- To define, describe, and forecast the market size of the thermoforming plastic market, in terms of value and volume

- To provide detailed information about the key factors (drivers, restraints, opportunities, and challenges) influencing the growth of the market

- To analyze and forecast the market based on plastic-type, thermoforming type, Thickness, and end-use industry

- To analyze and forecast the market based on five regions, namely, Europe, North America, APAC, the MEA, and Latin America

- To strategically analyze micromarkets with respect to individual growth trends, prospects, and their contribution to the overall market

- To analyze the opportunities in the market for stakeholders and provide a competitive landscape for market leaders

- To strategically profile the key players and comprehensively analyze their market share and core competencies

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the company�s specific needs.

The following customization options are available for the report:

Product Analysis

- Product matrix, which gives a detailed comparison of the product portfolio of each company

Regional Analysis

- Further breakdown of Rest of Europe thermoforming plastic market

- Further breakdown of Rest of APAC thermoforming plastic market

- Further breakdown of Rest of Latin American thermoforming plastic market

- Further breakdown of Rest of MEA thermoforming plastic market

Company Information

- Detailed analysis and profiling of additional market players (up to 10)

Growth opportunities and latent adjacency in Thermoforming Plastic Market