U.S. Healthcare BPO Market - Payer (Claims Processing, HR Services, and Finance and Accounts), Provider (Medical Billing and Coding), and Pharmaceutical (Clinical Trials, Contract Manufacturing, and Non-Clinical Services) - Trends and Global Forecasts to 2018

The U.S. healthcare BPO outsourcing market has great potential for growth owing to the measures taken by the government to curb the ever-increasing healthcare costs. The other factors that have led to the growth of the market are: developments and innovation in information technology and regulatory changes. Approximately 75% of U.S. healthcare companies outsource their work to external locations. This is due to the shortage of qualified staff in key positions, such as nurses and coders, and due to the new set of rules and regulations that they need to comply with. Some services that are commonly outsourced are insurance claims processing, adjudication and receivables management, billing and coding services, radiology reporting, transcription services, and clinical outsourcing, among others.

Implementation of various reforms such as the American Recovery and Reinvestment Act of 2009 and the Health Information Technology for Economic and Clinical Health Act (HITECH) as well as the conversion from the ICD-9 coding system to the ICD-10 coding system (to be implemented by October 2014) has created an upward growth trend. Furthermore, constant improvements in the quality of work from destination countries have reinforced the confidence of various healthcare payers, providers, and pharmaceutical companies in outsourcing. This is considered as the key driver of the healthcare process outsourcing market. On the other hand, data security and confidentiality concerns are the restraints for the growth of the market.

The key players in this market are Accenture (Ireland), GeBBS Healthcare (U.S.), Quintiles (U.S.), Covance (U.S.), PPD (U.S.), Parexel International (U.S.), Lonza (Switzerland), Catalent (U.S.), Boehringer Ingelheim (Germany), and DSM Pharma (U.S.).

In this report, the U.S. healthcare BPO market is categorized into three segments, namely, payer outsourcing, provider outsourcing, and pharmaceutical outsourcing. Each segment is further sub-segmented on the basis of services provided. Payer services consist of claims processing, HR services, member services/customer care, and finance and accounts. Provider services include medical billing, medical coding, medical transcription, and finance and accounts. Pharmaceutical services comprise clinical research organizations (CROs), contract manufacturing organizations (CMOs), and non-clinical services. An exhaustive value analysis for all these markets is provided for 2011, 2012, and 2013, with forecast till 2018.

Scope of the Report

This research report categorizes the U.S. healthcare BPO market into the following segments and sub-segments. Each market segment is further categorized on the basis of the services provided.

The U.S. Healthcare BPO Market, by Segment:

- Payer

- Provider

- Pharmaceutical

The U.S Healthcare Payer Outsourcing Market, by Services:

- Claims Processing

- HR Services

- Member Services/Customer Care

- Finance and Accounts

The U.S Healthcare Provider Outsourcing Market, by Services:

- Medical Billing

- Medical Coding

- Medical Transcription

- Finance and Accounts

The U.S Healthcare Pharmaceutical Outsourcing Market, by Services:

- CRO Market

- Drug Discovery

- Pre-clinical

- Phase I

- Phase II

- Phase III

- Phase IV

- Clinical Data Management and Biostatistics

- Medical Writing

- Regulatory Services Outsourcing

- Other Services

- API Manufacturing

- Formulation & Packaging

- Supply Chain Management and Logistics

- Sales and Marketing Management

- Other Non-clinical Functions

Customer Interested in this report also can view

-

Healthcare BPO Market - Payer (Claims processing), Provider (Medical Billing & Coding) and Pharmaceutical (Clinical trial & Contract manufacturing) Outsourcing - Global analysis & Forecasts (2011-2016)

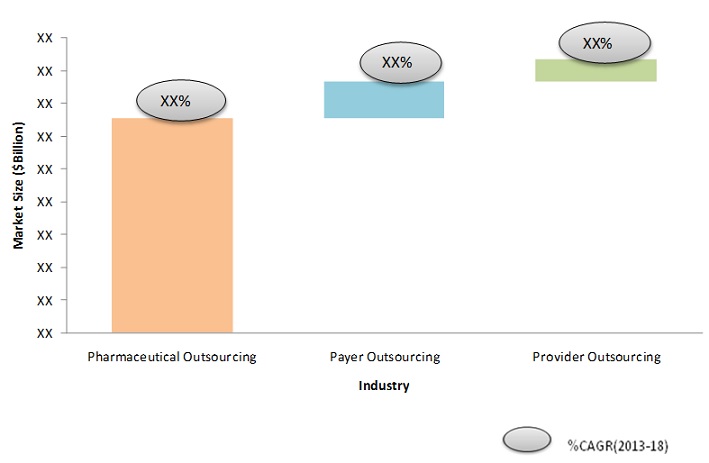

The U.S. healthcare BPO market is undergoing significant transformation with the changing landscape of the U.S. healthcare system. The U.S. pharmaceutical outsourcing market is the largest market in terms of market value, followed by payer and provider outsourcing. The U.S. provider outsourcing market is the fastest-growing segment of the U.S. healthcare BPO market, owing to the implementation of the ICD-10 conversion reform and the shortage of skilled personnel, particularly medical coders in the U.S.

The U.S. healthcare payer, provider, and pharmaceutical outsourcing markets are valued at $11.1 billion, $6.8 billion and $65.6 billion, respectively, in the year 2013. The U.S. healthcare payer market has been greatly impacted by the introduction of the Patient Protection and Affordable Care Act (PPACA). This market is particularly driven by claims processing services. As the act expanded insurance access to more than 30 million U.S. citizens, the increased claims processing workload led to large-scale outsourcing of these services by payers. Medical billing dominates the U.S. healthcare provider outsourcing market, while contract manufacturing organizations hold the largest share in the U.S. pharmaceutical outsourcing market in the year 2013.

The overall healthcare BPO market is highly fragmented with various players trying to gain a competitive edge and increase their market share. The players in the payer and provider outsourcing market are Accenture (Ireland), Medusind (U.S.), GeBBS Healthcare (U.S.), and Genpact Limited (Bermuda). The players in the pharmaceutical outsourcing market space include Lonza (Switzerland), Catalent (U.S.), Boehringer Ingelheim (Germany), DSM Pharma (U.S.), Quintiles (U.S.), and Covance (U.S.), among others.

U.S. Healthcare BPO Market ($Billion), 2013,

By Industry

Source: Annual Reports, SEC Filings, Press Releases, Investor Presentations, Expert Interviews, MnM Analysis

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table Of Contents

1 Introduction (Page No . - 16)

1.1 Key Take-Aways

1.2 Report Description

1.3 Markets Covered

1.4 Stakeholders

1.5 Research Methodology

1.5.1 Market Size

1.5.2 Key Data Points From Secondary Sources

1.5.3 Key Data Points From Primary Sources

1.5.4 Assumptions

2 Executive Summary (Page No . - 22)

3 Market Overview (Page No . - 25)

3.1 Introduction

3.2 Market Dynamics

3.2.1 Drivers

3.2.1.1 Introduction Of The Patient Protection And Affordable Care Act (PPACA)

3.2.1.2 Need To Reduce Rising Healthcare Costs

3.2.1.3 Shortage Of Skilled Personnel

3.2.2 Restraints

3.2.2.1 Unforeseen Costs

3.2.2.2 Confidentiality And Security Of Data Is A Major Concern

3.2.2.3 Loss Of Managerial Control

3.2.3 Opportunities

3.2.3.1 Consolidation Of The Healthcare System

3.2.3.2 ICD-10 Conversion

4 U.S. Healthcare Payer Outsourcing Market, By Services (Page No . - 33)

4.1 Introduction

4.1.1 Vendors With Complete Range Of Services Attract Insurance Providers

4.1.2 PPACA Will Add Approximately 30 Million Americans To The Insurance System

4.1.3 Errors During Client Interaction Could Affect A Company�s Reputation

4.2 Claims Processing

4.3 Member Services/Customer Care

4.4 HR Services

4.5 Finance And Accounts

5 U.S. Healthcare Provider Outsourcing Market, By Services (Page No . - 43)

5.1 Introduction

5.1.1 Outsourcing Saves Time And Costs

5.1.2 Concerns Regarding Quality Of Services

5.2 Medical Billing

5.3 Medical Coding

5.4 Medical Transcription

5.5 Finance And Accounts

6 U.S. Pharmaceutical Outsourcing Market, By Type (Page No . - 53)

6.1 Introduction

6.1.1 Outsourcing: A Cost-Effective Approach To Concentrate On Core Competencies

6.1.2 Off-Patenting Of Drugs Will Drive The Outsourcing Market

6.1.3 Emergence Of Biologics As A Major Opportunity In The Future

6.1.4 Quality Control Issues Limit Outsourcing

6.2 U.S. CRO Market

6.2.1 Introduction

6.2.2 Drug Discovery

6.2.3 Pre-Clinical Services

6.2.4 Clinical Development Phase I

6.2.5 Clinical Development Phase Ii

6.2.6 Clinical Development Phase Iii

6.2.7 Clinical Development Phase Iv

6.2.8 Clinical Data Management And Biostatistics

6.2.9 Medical Writing

6.2.10 Regulatory Services

6.2.11 Other Services

6.3 U.S. CMO Market

6.3.1 Introduction

6.3.2 API Manufacturing

6.3.3 Formulation And Packaging

6.4 U.S. Non-Clinical Services Outsourcing Market

6.4.1 Introduction

6.4.2 Supply Chain Management And Logistics

6.4.3 Sales And Marketing Management

6.4.4 Other Non-Clinical Functions

7 Geographic Analysis (Page No . - 82)

7.1 U.S.

7.1.1 Payer

7.1.2 Provider

7.1.3 Pharmaceutical

8 Competitive Landscape (Page No . - 91)

8.1 Introduction

8.2 Mergers & Acquisitions

8.3 Agreements, Partnerships, Collaborations, And Joint Ventures

8.4 New Product Launches

8.5 Expansion

9 Company Profiles (Overview, Financials, Services, Strategy & Development)* (Page No . - 145)

9.1 Accenture Plc

9.2 Accretive Health, Inc.

9.3 Anthelio Healthcare Solutions, Inc.

9.4 Boehringer Ingelheim Gmbh

9.5 Catalent Pharma Solutions, Inc.

9.6 Cognizant Technology Solutions Corporation

9.7 Covance, Inc.

9.8 GEBBS Healthcare Solutions, Inc.

9.9 Genpact Limited

9.10 IBM Corporation

9.11 ICON Plc

9.12 Infosys Bpo Limited

9.13 LONZA Group Ltd.

9.14 Parexel International Corporation

9.15 Quintiles Transnational Holdings, Inc.

9.16 WNS (Holdings) Limited

*Details On Overview, Financials, Services, Strategy& Development Might Not Be Captured In Case Of Unlisted Companies.

List Of Tables (26 Tables)

Table 1 U.S. Healthcare BPO Payer Outsourcing Market, By Services, 2011 � 2018 ($Billion)

Table 2 U.S. Healthcare Provider Outsourcing Market, By Services, 2011 � 2018 ($Billion)

Table 3 U.S. Pharmaceutical Outsourcing Market, By Type, 2011 � 2018 ($Billion)

Table 4 U.S. Cro Market, By Services, 2011 � 2018 ($Billion)

Table 5 U.S. Cmo Market, By Services, 2011 � 2018 ($Billion)

Table 6 U.S.Non-Clinical Services Outsourcing Market, By Services, 2011 � 2018 ($Billion)

Table 7 U.S.Healthcare Bpo Market, By Segments, 2011 � 2018 ($Billion)

Table 8 Mergers & Acquisitions, January 2011 � June 2013

Table 9 Agreements, Partnerships, Collaborations, Contracts & Joint Ventures, January 2011 � June 2013

Table 10 New Product Launches, January 2011- June 2013

Table 11 Expansion, January 2011 � June 2013

Table 12 Accenture Plc: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 13 Accretive Health, Inc.: Total Revenue, By Segment, 2009 � 2011 ($Million)

Table 14 Boehringer Ingelheim Gmbh: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 15 Catalent Pharma Solutions, Inc.: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 16 Cognizant Technology Solutions Corporation: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 17 Covance, Inc.: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 18 Genpact Limited: Total Revenue, By Service Type, 2010 � 2012 ($Million)

Table 19 Genpact Limited: Total Revenue, By Industry, 2010 � 2012 ($Million)

Table 20 IBM Corporation: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 21 ICON Plc: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 22 Infosys Limited: Total Revenue, By Segment, 2011 � 2013 ($Million)

Table 23 LONZA Group Ltd.: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 24 Parexel International Corporation: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 25 Quintiles Transnational Holdings, Inc.: Total Revenue, By Segment, 2010 � 2012 ($Million)

Table 26 WNS Holdings Ltd: Total Revenue, By Segment, 2011 � 2013 ($Million)

List Of Figures (36 Figures)

Figure 1 U.S. Healthcare BPO Market Segmentation

Figure 2 U.S. Healthcare BPO Market ($Billion), 2013, By Industry

Figure 3 Market Dynamics

Figure 4 Components Of Ppaca

Figure 5 U.S. Healthcare BPO Payer Outsourcing Market, By Services

Figure 6 U.S. Claims Processing Market, 2011 � 2018 ($Billion)

Figure 7 U.S. Member Services/Customer Care Market, 2011 � 2018 ($Billion)

Figure 8 U.S. Hr Services Market, 2011 � 2018 ($Billion)

Figure 9 U.S. Finance And Accounts Market, 2011 � 2018 ($Billion)

Figure 10 U.S. Healthcare Provider Outsourcing Market, By Services

Figure 11 U.S. Medical Billing Market, 2011 � 2018 ($Billion)

Figure 12 U.S. Medical Coding Market, 2011 � 2018 ($Billion)

Figure 13 U.S. Medical Transcription Market, 2011 � 2018 ($Billion)

Figure 14 U.S. Finance And Accounts Market, 2011 � 2018 ($Billion)

Figure 15 U.S. Pharmaceutical Outsourcing Market, By Services

Figure 16 U.S. Drug Discovery Market, 2011 � 2018 ($Billion)

Figure 17 U.S. Pre-Clinical Services Market, 2011 � 2018 ($Billion)

Figure 18 U.S. Clinical Development Phase I Market, 2011 � 2018 ($Billion)

Figure 19 U.S. Clinical Development Phase Ii Market, 2011 � 2018 ($Billion)

Figure 20 U.S. Clinical Development Phase Iii Market, 2011 � 2018 ($Billion)

Figure 21 U.S. Clinical Development Phase Iv Market, 2011 � 2018 ($Billion)

Figure 22 U.S. Clinical Data Management And Biostatistics Market, 2011 � 2018 ($Billion)

Figure 23 U.S. Medical Writing Market, 2011 � 2018 ($Billion)

Figure 24 U.S. Regulatory Services Market, 2011 � 2018 ($Billion)

Figure 25 U.S. Other Services Market, 2011 � 2018 ($Billion)

Figure 26 U.S. API Manufacturing Market, 2011 � 2018 ($Billion)

Figure 27 U.S. Formulation And Packaging Market, 2011 � 2018 ($Billion)

Figure 28 U.S. Supply Chain Management And Logistics Market, 2011 � 2018 ($Billion)

Figure 29 U.S. Sales And Marketing Management Market, 2011 � 2018 ($Billion)

Figure 30 U.S. Other Non-Clinical Functions Market, 2011 � 2018 ($Billion)

Figure 31 U.S. Healthcare BPO Payer Market, By Services, 2013 � 2018 ($Billion)

Figure 32 U.S. Healthcare Provider Market, By Services, 2013 � 2018 ($Billion)

Figure 33 U.S. Pharmaceutical Outsourcing Market, By Types

Figure 34 Key Growth Strategies Of The U.S. Healthcare Bpo Market, 2011 � 2013

Figure 35 Key Players Focusing On Agreements, Partnerships, Collaborations, Contracts, And Joint Ventures Strategy, 2011 � 2013

Figure 36 Key Players Focusing On The Expansion Strategy, 2011 � 2013

Generating Response ...

Generating Response ...

Growth opportunities and latent adjacency in U.S. Healthcare BPO Market