China Semiconductor Industry � Expansion Plans Analysis and Trends (Government Policies and Guidelines, Import and Export Impact on Trade Partners, Key Concepts, Case Study, Key Strategies Adopted, Future Plans, and Recommendation to Players)

The China semiconductor industry is expected to grow from USD 83.67 Billion in 2015 to USD 157.66 Billion by 2020, at a CAGR of 12.8% between 2016 and 2020. The base year considered for the study is 2015, and the forecast is provided for the period between 2016 and 2020.

Objectives of Study:

- To define, describe, and forecast the China semiconductor industry and market on the basis of components and end users, respectively

- To strategically analyze the growth trends, prospects, and contribution of the government initiatives for the expansion of the China semiconductor industry

- To analyze the impact of the China semiconductor industry expansion on neighboring countries

- To study the impact of the key technological advancements on the expansion of the China semiconductor industry

- To provide detailed information regarding the major factors influencing the growth of the industry (drivers, restraints, opportunities, and industry-specific challenges)

- To conduct a detailed value chain, Porter’s five forces, and PESTEL analysis of the China semiconductor industry

- To analyze the opportunities in the China semiconductor industry for stakeholders and provide the details of a competitive landscape for market leaders

- To strategically profile key players in the China semiconductor industry and comprehensively analyze their market shares and expansion strategies

- To analyze various developments such as joint ventures, mergers and acquisitions, collaborations, and investments in the China semiconductor industry

The China semiconductor industry is expected to have a high growth potential till 2020. The total market is expected to reach USD 157.66 Billion by 2020 from USD 83.67 Billion in 2015, at a CAGR of 12.8% between 2016 and 2020. The major driving factors for the growth of the China semiconductor industry are the growing demand for semiconductors from major verticals and favorable government initiatives.

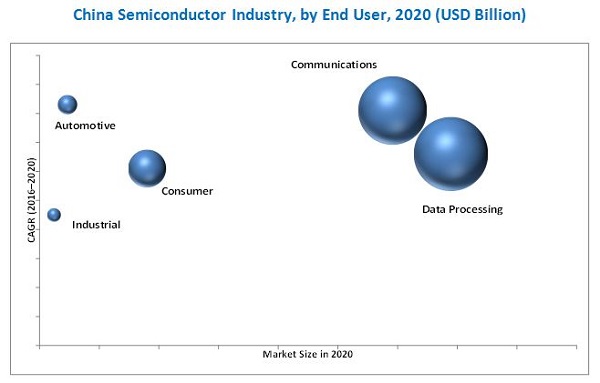

This report covers the China semiconductor industry on the basis of end user and component. Data processing holds the largest share of the China semiconductor industry on the basis of end user. Among the five key end-user segments of the semiconductor industry (data processing, communications, industrial, automotive, and consumer), data processing is the major consumer of semiconductors in China. It includes notebooks, PCs, and tablets. The increasing demand for tablets is expected to drive the growth of the data processing market. Many domestic manufacturers have come out with their own tablet device, creating a market for low-priced tablets. This has had a positive impact on the growth of the data processing segment.

The market for ICs is expected to grow at the highest CAGR and hold the largest share during the forecast period. The semiconductor industry is the summation of integrated circuits (ICs) and optoelectronic, sensor, and discrete (O-S-D) devices. The IC segment holds almost two-thirds of the total semiconductor industry in China. The IC industry includes the manufacturing of logic ICs, memory ICs, processors, and analog ICs. The increasing demand for smartphones and tablets as well as applications in consumer electronics and the automotive sector are expected to be the key drivers for the growth of the logic ICs segment. The demand for analog ICs is expected to be driven by the growth in the automotive and telecommunications sector.

The increasing labor cost and huge financial investment required for establishing the manufacturing base are the major restraining factors for the China semiconductor industry.

The China semiconductor industry includes companies for such as SK Hynix Inc. (South Korea), HiSilicon Technologies Co., Ltd. (China), Semiconductor Manufacturing International Corp. (SMIC) (China), Samsung Electronics Co., Ltd. (South Korea), Micron Technology Inc. (U.S.), Intel Corp. (U.S.), Qualcomm Inc. (U.S.), Jiangsu Changjiang Electronics Technology Co. Ltd. (JCET) (China), Tianjin Zhonghuan Semiconductor Co., Ltd. (China), and Spreadtrum Communications Inc. (China).

These players adopted various strategies such as mergers, acquisitions, expansions, investments, alliances, partnerships, joint ventures, agreements, collaborations, and contracts to achieve growth in the market.

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 12)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Study Scope

1.3.1 Markets Covered

1.3.2 Years Considered for the Study

1.4 Currency

1.5 Market Stakeholders

2 Research Methodology (Page No. - 15)

2.1 Research Data

2.1.1 Secondary Data

2.1.1.1 Key Data From Secondary Sources

2.1.2 Primary Data

2.1.2.1 Key Data From Primary Sources

2.1.2.2 Key Industry Insights

2.1.2.3 Breakdown of Primaries

2.2 Market Size Estimation

2.2.1 Bottom-Up Approach

2.2.2 Top-Down Approach

2.3 Market Breakdown and Data Triangulation

2.4 Research Assumptions

3 Executive Summary (Page No. - 24)

4 Premium Insights (Page No. - 29)

4.1 Attractive Market Opportunities in Chiina Semiconductor Industry

4.2 China Semiconductor IC Industry, By Sector

4.3 List of Key Players in the Semiconductor Industry

4.3.1 Global Semiconductor Players

4.3.2 China Semiconductor Players

4.4 List of Favorable Plans for the Semiconductor Industry By the Government of China

4.4.1 Key Government Action Plans for China Semiconductor Industry

4.4.2 Other Government Regulations for China Semiconductor Industry

5 China Semiconductor Industry: Expansion Roadmap (Page No. - 34)

5.1 Policies and Guidelines Impacting the China Semiconductor Industry

5.1.1 China 12th Five–Year Plan

5.1.2 China 13th Five–Year Plan

5.1.3 Made in China 2025

5.1.4 National Semiconductor Industry Development Guidelines

5.1.5 Foreign Investment Industrial Guidance Catalogue, 2015

5.1.6 Others

5.2 Import and Export Impact on Neighboring Countries and Key Trade Partners

5.2.1 U.S.

5.2.2 Taiwan

5.2.3 Japan

5.2.4 South Korea

5.2.5 India

5.3 Key Concepts

5.3.1 IoT

5.3.2 5G, 4.5G, and LTE

5.3.3 Big Data

5.3.4 Cloud Computing

6 Market Overview (Page No. - 51)

6.1 Introduction

6.2 Industry Evolution

6.3 Market Segmentation

6.3.1 China Semiconductor Industry, By Component

6.3.2 China Semiconductor Market, By End User

6.4 Industry Dynamics

6.4.1 Drivers

6.4.1.1 Growing demand for semiconductors from major end-use verticals

6.4.1.2 Favorable government initiatives

6.4.2 Restraints

6.4.2.1 Increasing labor cost

6.4.2.2 Huge financial investment required for establishing a manufacturing base

6.4.3 Opportunities

6.4.3.1 Investment from foreign players

6.4.3.2 New emerging technological concepts

6.4.4 Challenges

6.4.4.1 IP Security Issue

6.4.4.2 Lack of advanced manufacturing capacities

7 Industry Trends (Page No. - 63)

7.1 Introduction

7.2 China Semiconductor Industry: Value Chain Analysis

7.3 Porter’s Five Forces Analysis

7.3.1 Threat of New Entrants

7.3.2 Threat of Substitutes

7.3.3 Bargaining Power of Suppliers

7.3.4 Bargaining Power of Buyers

7.3.5 Competitive Rivalry

7.4 China Semiconductor Industry PESTEL Analysis

7.4.1 Introduction

7.4.2 Political Factors

7.4.3 Economic Factors

7.4.4 Social Factors

7.4.5 Technological Factors

7.4.6 Environmental Factors

7.4.7 Legal Factors

7.4.8 Conclusion

8 China Semiconductor Industry Segments (Page No. - 79)

8.1 Introduction

8.2 China Semiconductor Market

8.2.1 Data Processing

8.2.2 Communications

8.2.3 Consumer Electronics

8.2.4 Automotive

8.2.5 Industrial

8.3 China Semiconductor Industry

8.3.1 IC Industry

8.3.1.1 IC Testing and Packaging

8.3.1.2 IC Manufacturing

8.3.1.3 IC Design

8.3.2 O-S-D Industry

9 Competitive Landscape (Page No. - 86)

9.1 Overview

9.2 Market Share Analysis

9.3 Competitive Scenario

9.3.1 Mergers & Acquisitions

9.3.2 Expansions and Investments

9.3.3 Alliances, Partnerships, and Joint Ventures

9.3.4 Agreements, Collaborations, and Contracts

10 Company Profiles (Page No. - 97)

(Business overview and financials, Products offered, Recent expansions, Future plans, Importers’ and exporters’ profile, and MnM view)*

10.1 Introduction

10.2 Global Players

10.2.1 Intel Corp.

10.2.2 Samsung Electronics Co., Ltd.

10.2.3 SK Hynix Inc.

10.2.4 Qualcomm Inc.

10.2.5 Micron Technology Inc.

10.3 Domestic Players

10.3.1 Hisilicon Technologies Co., Ltd.

10.3.2 Semiconductor Manufacturing International Corp. (SMIC)

10.3.3 Tianjin Zhonghuan Semiconductor Co., Ltd.

10.3.4 Jiangsu Changjiang Electronics Technology Co., Ltd. (JCET)

10.3.5 Spreadtrum Communications Inc.

*Details on financials might not be captured in case of unlisted companies

11 Conclusion (Page No. - 138)

11.1 Introduction

11.2 Case Study

11.2.1 Recommendation to Global Players

11.2.2 Recommendation to Domestic Players

12 Appendix (Page No. - 145)

12.1 Insights of Industry Experts

12.2 Discussion Guide

12.3 Knowledge Store: Marketsandmarkets’ Subscription Portal

12.4 Introducing RT: Real-Time Market Intelligence

12.5 Available Customizations

12.6 Related Reports

List of Tables (26 Tables)

Table 1 List of Top 20 Global Semiconductor Players

Table 2 Comparison of Targets Set and Achieved for the 12th Five-Year Plan

Table 3 13th Five-Year Plan Targets

Table 4 China's 2014 National IC Guideline Targets for Its Chip Industry

Table 5 Manufacturing Sectors Encouraged in Computer, Communication, and Other Electronic Equipment Manufacturing Segment

Table 6 U.S. Economic Factors Snapshot (2011–2015)

Table 7 Taiwan Economic Factors Snapshot (2011–2015)

Table 8 Japan Economic Factors Snapshot (2011–2015)

Table 9 South Korea Economic Factors Snapshot (2011–2015)

Table 10 India Economic Factors Snapshot (2011–2015)

Table 11 Porter’s Five Forces Analysis With Their Weightage Impact

Table 12 China: Country Snapshot

Table 13 Political Background of China (2015)

Table 14 Comparison of Economic Factors of China for 2013, 2014, and 2015

Table 15 Demographics of China (2015)

Table 16 Analysis of Technological Influence on China (2015)

Table 17 Analysis of Environment of China

Table 18 Global Semiconductor Industry Size, 2011–2020 (USD Billion)

Table 19 China Semiconductor Market, By End User, 2011–2020 (USD Billion)

Table 20 China Semiconductor Industry, By Component, 2011–2020 (USD Billion)

Table 21 China Semiconductor IC Industry, By Player Type, 2011–2020 (USD Billion)

Table 22 China Semiconductor IC Industry, By Sector, 2011–2020 (USD Billion)

Table 23 Mergers & Acquisitions in the China Semiconductor Market (January 2015–June 2016)

Table 24 Expansions and Investments in China Semiconductor Market (January 2015–June 2016)

Table 25 Alliances, Partnerships, and Joint Ventures in China Semiconductor Market (January 2015–June 2016)

Table 26 Agreements, Collaborations, and Contracts in China Semiconductor Market (January 2015–June 2016)

List of Figures (57 Figures)

Figure 1 China Semiconductor Industry: Research Design

Figure 2 Process Flow of Market Size Estimation

Figure 3 Market Size Estimation Methodology: Bottom-Up Approach

Figure 4 Market Size Estimation Methodology: Top-Down Approach

Figure 5 Data Triangulation

Figure 6 China Semiconductor Industry to Grow at A Higher Rate Than China Semiconductor Market During the Forecast Period

Figure 7 Global IC Manufacturers Expected to Hold the Largest Size of the China Semiconductor Industry Throughout the Forecast Period

Figure 8 China Semiconductor Industry, By Component and Sector, in 2016

Figure 9 China Semiconductor Market for Consumer Segment to Grow at the Highest Rate During the Forecast Period

Figure 10 Government Offerings in Terms of Incentives and Standards Expected to Attract Foreign and Domestic Players to the China Semiconductor Industry

Figure 11 IC Pacakaging & Testing to Dominate the China Semiconductor Industry During the Forecast Period

Figure 12 China IC's Fund Structure

Figure 13 Comparison Between Semiconductor Imports By China From Key Trade Countries, Between 2011 and 2015

Figure 14 Comparison Between Semiconductor Exports By China to Key Trade Countries, Between 2011 and 2015

Figure 15 Evolution of the Semiconductor Industry in China

Figure 16 Favorable Government Initiatives to Drive the Semiconductor Industry in China

Figure 17 Increasing Consumption of Semiconductors in the Consumer Sector in China (2014–2020)

Figure 18 Increasing Consumption of Semiconductors in the Communication Sector in China (2014–2020)

Figure 19 Increasing Consumption of Semiconductors in the Automotive Sector in China (2014–2020)

Figure 20 Increasing Consumption of Semiconductors in the Data Processing Sector in China (2014–2020)

Figure 21 Average Yearly Wages in the Manufacturing Sector in China (2008–2014)

Figure 22 Value Chain Analysis: Testing & Packaging Sector Contributes the Major Value in the China Semiconductor Industry

Figure 23 Porter’s Five Force Model for China Semiconductor Industry, 2016

Figure 24 Porter’s Five Forces Analysis

Figure 25 Medium Impact of Threat of New Entrants Because of Favorable Government Regulations

Figure 26 Low Impact of the Threat of Substitutes Due to Lack of Viable Alternatives

Figure 27 Low Impact of Bargaining Power of Suppliers Due to High Supplier Concentration

Figure 28 High Impact of Buyers’ Bargaining Power Owing to Price Sensitivity and Buyer Concentration vs Industry

Figure 29 High Degree of Competitive Rivalry in the Industry Because of High Industry Growth Rate

Figure 30 Semiconductor Industry Snapshot (2011–2020)

Figure 31 Data Processing Segment is the Major End User of Semiconductors in China During the Forecast Period

Figure 32 IC Holds Almost Two-Thirds of the Total Semiconductor Industry in China

Figure 33 Global Players Hold a Major Share of the China IC Industry

Figure 34 IC Design is the Fastest-Growing Sector of the China Semiconductor IC Industry

Figure 35 China Semiconductor Industry Global Players Adopted Mergers & Acquisition as the Key Growth Strategy Between January 2015 and June 2016

Figure 36 Industry Domestic Players Adopted Mergers and Acquisition as the Key Growth Strategy Between January 2015 and June 2016

Figure 37 Share of Top 5 Players in the China Semiconductor Industry, in 2015

Figure 38 China Semiconductor Market Evaluation Framework

Figure 39 Battle for the Market Share

Figure 40 Geographic Revenue Mix of Top 5 Semiconductor Manufacturers of China

Figure 41 Intel Corp.: Company Snapshot

Figure 42 Samsung Electronics Co., Ltd.: Company Snapshot

Figure 43 SK Hynix Inc.: Company Snapshot

Figure 44 Qualcomm Inc.: Company Snapshot

Figure 45 Micron Technology Inc. :Company Snapshot

Figure 46 Hisilicon Technologies Co., Ltd.: Company Snapshot

Figure 47 Semiconductor Manufacturing International Corp.: Company Snapshot

Figure 48 Tianjin Zhonghuan Semiconductor Co., Ltd.: Company Snapshot

Figure 49 Jiangsu Changjiang Electronics Technology Co., Ltd.: Company Snapshot

Figure 50 Industry Growth Analysis

Figure 51 China Semiconductor IC Industry Growth Analysis

Figure 52 China Semiconductor O-S-D Industry Growth Analysis

Figure 53 China Semiconductor IC Design Industry Growth Analysis

Figure 54 China Semiconductor IC Manufacturing Industry Growth Analysis

Figure 55 China Semiconductor IC Packaging and Testisng Industry Growth Analysis

Figure 56 Global Players in the China Semiconductor IC Industry

Figure 57 Domestic Players in the China Semiconductor IC Industry

Research Methodology:

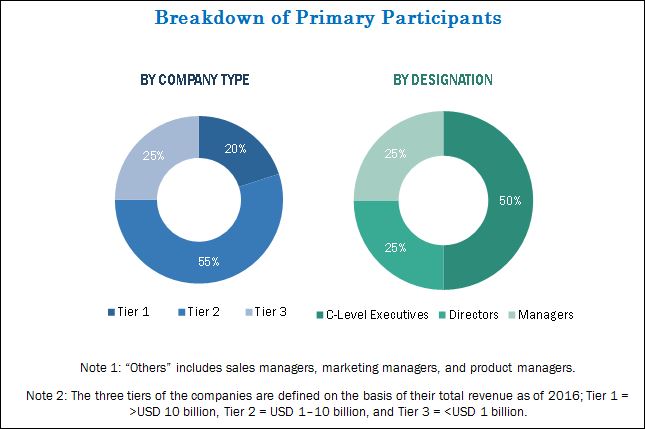

This research involves the use of secondary sources, directories, and databases such as Hoovers, Bloomberg Businessweek, Factiva, and OneSource to identify and collect information useful for the extensive technical, market-oriented, and commercial study of the China semiconductor industry. Primary sources mainly comprise several industry experts from the core and related industries, along with preferred suppliers, manufacturers, distributors, service providers, reimbursement providers, technology developers, alliances, standards, and certification organizations related to various parts of the value chain of the industry. In-depth interviews have been conducted with various primary respondents, such as key industry participants, subject matter experts (SMEs), C-level executives of key players, and industry consultants, to obtain and verify critical qualitative and quantitative information as well as to assess prospects. The breakdown of the profiles of primaries has been depicted in the figure below:

To know about the assumptions considered for the study, download the pdf brochure

In 2015, the China semiconductor industry was dominated by SK Hynix Inc. (South Korea), HiSilicon Technologies Co., Ltd. (China), Semiconductor Manufacturing International Corp. (SMIC) (China), Samsung Electronics Co., Ltd. (South Korea), and Micron Technology Inc. (US).

Key Target Audience:

- Semiconductor wafer and raw material suppliers

- Semiconductor design providers

- Semiconductor fabless and foundry players

- Packaging and testing players

- Integrated device manufacturers (IDMs)

- Electronic design automation (EDA) vendor

- OEMs

- Technology, service, and solution providers

- Suppliers and distributors

- Intellectual property (IP) core and licensing providers

- System integrators and device manufacturers

- Middleware providers

- Government and other regulatory bodies

- Technology investors

- Research institutes and organizations

- Market research and consulting firms

Scope of the Report:

In this research report, the China semiconductor industry is segmented as follows:

China Semiconductor Market, by End User

- Data Processing

- Communications

- Consumer

- Automotive

- Industrial

China Semiconductor Industry, by Component

-

IC

- IC Design

- IC Manufacturing

- IC Packaging and Testing

- O-S-D

Available Customizations:

With the given market data, MarketsandMarkets offers customizations according to the company’s specific needs. The following customization options are available for the report:

Company Information

Detailed analysis and profiling of additional market players on the basis of various blocks of the value chain

Growth opportunities and latent adjacency in China Semiconductor Industry

I am writing a thesis on the international impacts of China's semiconductor industry. I believe, this report would be instrumental to improving my background knowledge and research outcomes.

China Semiconductor Industry: Expansion Plans Analysis and Trends (Government Policies and Guidelines), Import and Export Impact on Trade Partners, Key Concepts, Case Study, Key Strategies Adopted, Future Plans, and Recommendation to Players are included in this study?