Download PDF

Download PDF Request Customisation

Request Customisation

Occupancy Sensor Market Size, Share & Analysis

Report Code

SE 2758

Published in

Feb, 2025, By MarketsandMarkets™

Occupancy Sensor Market by Type (Wall Mount, Ceiling Mount, Desk), Operation (Indoor, Outdoor), Connectivity (Wireless, ZigBee, Z-wave), Technology (Passive Infrared, Ultrasonic, Dual Technology, Image Processing), Installation - Global Forecast to 2030

USD 5.20 BN

MARKET SIZE, 2030

CAGR 11.2%

(2024-2030)

225

REPORT PAGES

200

MARKET TABLES

OCCUPANCY SENSOR MARKET OVERVIEW

The occupancy sensor market is projected to reach USD 5.20 billion by 2030 from USD 2.75 billion in 2024, at a CAGR of 11.2% from 2024 to 2030. Occupancy sensor demand is growing due to the rising need for energy-efficient buildings that automatically control lighting, HVAC, and security systems. Additionally, smart home adoption and stringent building energy regulations are accelerating the integration of advanced sensing technologies.

OCCUPANCY SENSOR MARKET KEY TAKEAWAYS

-

By RegionThe North America in occupancy sensor Market market dominated with a share of 38.2% in 2023.

-

By OperationBy operation, the outdoor segment is expected to register the highest CAGR of 14.3%.

-

By Installation TypeBy installation type, the new segment is projected to grow at the fastest rate from 2024 to 2030.

-

By TechnologyBy technology, the PIR segment is expected to dominate the market.

-

By End UserBy end user, the commercial building segment will grow the fastest during the forecast period.

-

Competitive LandscapeLegrand, Johnson Controls, Eaton, Honeywell, Acuity Brands, and Leviton Manufacturing were identified as some of the star players in the ocupancy sensor market (global), given their strong market share and product footprint.

-

Competitive LandscapeEnerlits Inc., Avuity, Butlr,XY Sense and Density among others, have distinguished themselves among startups and SMEs by securing strong footholds in specialized niche areas, underscoring their potential as emerging market leaders

Occupancy sensors market are witnessing steady growth driven by the increasing focus on energy efficiency and automated building management systems. Growing adoption of smart homes, IoT-enabled devices, and stricter building energy codes further accelerates their demand across residential, commercial, and industrial spaces.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The occupancy sensor industry is evolving rapidly as buildings become smarter and more connected. IoT-enabled and networked sensors are enabling real-time monitoring and seamless integration with building management systems. Multi-technology sensing—combining PIR, ultrasonic, and microwave—improves accuracy in complex indoor environments. Disruptive innovations such as AI-powered presence detection and mmWave radar are enhancing precision by detecting micro-movements. At the same time, wireless, battery-efficient designs and cloud-based analytics are transforming space optimization, safety, and energy management.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

OCCUPANCY SENSOR MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Growing demand for energy-efficient devices

-

Increasing deployment of lighting controllers in smart homes

RESTRAINTS

Impact

Level

Level

-

Technical limitations of occupancy sensors

-

Inconsistency issues related to wireless network systems

OPPORTUNITIES

Impact

Level

Level

-

Growing initiatives of governments for green buildings

-

Increasing demand for smart buildings in urban areas

CHALLENGES

Impact

Level

Level

-

Lack of awareness regarding benefits of occupancy sensors.

-

Privacy concerns, particularly with camera-based or AI-powered sensors used in offices and public spaces.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Growing demand for energy-efficient devices.

The growing demand for energy-efficient devices is a major driver for the occupancy sensor market, as buildings increasingly prioritize automation to reduce electricity consumption and operational costs. Occupancy sensors help eliminate unnecessary lighting and HVAC usage by ensuring systems run only when spaces are in use, making them essential for meeting modern energy-efficiency goals. With governments enforcing stricter energy codes and businesses aiming to cut carbon emissions, these sensors are becoming a standard feature in both new constructions and retrofitted buildings. This push toward sustainable infrastructure continues to accelerate adoption across residential, commercial, and industrial environments.

Restraint: Technical limitations of occupancy sensors.

Occupancy sensors face several technical limitations that can affect their accuracy and reliability. PIR sensors struggle with detecting stationary occupants and require a clear line of sight, leading to missed detections in obstructed or partitioned spaces. Ultrasonic and microwave sensors, while more sensitive, can cause false triggers due to vibrations, airflow, or movement outside the intended detection zone. Multi-technology sensors improve accuracy but introduce higher complexity, calibration needs, and cost. Additionally, environmental factors such as temperature changes, reflective surfaces, and background noise can interfere with sensor performance, making consistent detection challenging in diverse real-world conditions.

Opportunity: Growing initiatives of governments for green buildings.

Government initiatives promoting green buildings are creating strong momentum for the occupancy sensor market, as policies increasingly mandate energy-efficient lighting and automated building controls. Many countries have introduced building energy codes, green certification programs, and incentives that require or encourage the use of smart sensors to reduce electricity consumption in commercial and residential structures. These initiatives support the shift toward sustainable infrastructure by driving the adoption of intelligent lighting, HVAC optimization, and real-time energy management. As governments push for lower carbon emissions and smarter urban development, occupancy sensors are becoming a critical component of compliant and eco-friendly building designs.

Challenge: Lack of awareness regarding benefits of occupancy sensors.

A key challenge for the occupancy sensor market is the lack of awareness regarding their long-term benefits. Many building owners and small enterprises are still unfamiliar with how occupancy sensors can significantly reduce energy costs, improve automation, and enhance overall building efficiency. This limited understanding often leads to hesitation in adoption, especially in regions where upfront cost sensitivity is high. As a result, potential users may overlook the substantial operational savings and sustainability advantages these sensors provide, slowing market growth.

OCCUPANCY SENSOR MARKET SIZE, SHARE & ANALYSIS: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Deployment of PIR, ultrasonic, and dual-technology occupancy sensors in commercial buildings, office spaces, and educational institutions. | Enhances energy efficiency by automating lighting and HVAC, reduces operational costs, and improves overall building comfort. |

|

Integration of smart occupancy sensors with building management systems (BMS) for real-time monitoring of space usage and automated environmental control | Improves space optimization, increases energy savings, and enables intelligent facility management through data-driven insights. |

|

Use of wired and wireless occupancy sensors in industrial facilities and commercial lighting systems for automated control and safety compliance. | Reduces energy waste in large facilities, enhances worker safety, and supports compliance with energy and building codes |

|

Advanced occupancy and presence sensors integrated into HVAC, security, and smart building platforms for industrial, commercial, and healthcare environments | Increases operational efficiency, enables predictive building control, and enhances comfort with precise occupancy-based adjustments. |

|

Deployment of networked lighting control sensors and ceiling-mounted occupancy detectors in retail, office, and residential applications. | Delivers high energy savings, supports smart lighting ecosystems, and enhances user experience with seamless automation. |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

OCCUPANCY SENSOR MARKET ECOSYSTEM

The ecosystem of occupancy sensor includes raw material suppliers, manufacturers, and distributors. Raw material suppliers provide key components such as PIR elements, ultrasonic transducers, microwave modules, lenses, circuit boards, and casings that form the core of occupancy sensor technology. Manufacturers design and assemble occupancy sensors by integrating detection technologies, control circuits, and communication modules into complete, ready-to-install products. Distributors bridge the gap between manufacturers and customers by ensuring efficient regional availability of occupancy sensors through retail, wholesale, and project-based supply channels.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

OCCUPANCY SENSOR MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Occupancy Sensor Market, By Type

Ceiling-mount occupancy sensors dominate the market because they provide the widest and most uniform coverage, enabling a single sensor to accurately monitor large or irregular rooms. Their elevated position reduces blind spots and enhances detection reliability for both motion and presence sensing. They are also easier to integrate into modern building layouts, especially in commercial spaces with standardized ceiling grids. Additionally, they require fewer units per room, lowering installation and maintenance costs for end users.

Occupancy Sensor Market, By Technology

PIR (Passive Infrared) occupancy sensors dominate because they offer high reliability and low false-trigger rates by detecting actual body heat movement rather than noise or vibrations. They are also cost-effective, energy efficient, and easy to install, making them the preferred choice across residential and commercial buildings. Additionally, PIR technology performs well in enclosed indoor spaces where temperature contrast helps deliver accurate detection, strengthening its adoption in mainstream applications.

Occupancy Sensor Market, By End User

Commercial buildings dominate the occupancy sensor market due to their high demand for automated lighting and HVAC systems aimed at reducing energy consumption and operating costs. These spaces—such as offices, retail stores, and educational institutions—have frequent foot traffic and varying occupancy patterns, making sensors essential for efficient control. Additionally, stricter building energy codes and green certification requirements drive widespread adoption of occupancy sensors in new and retrofitted commercial infrastructures.

OCCUPANCY SENSOR MARKET BY REGION

Asia Pacific to be fastest-growing region in global occupancy sensor market during forecast period

Asia Pacific is growing the fastest in the occupancy sensor market because the region is experiencing rapid construction of commercial buildings, smart homes, and industrial facilities driven by urbanization and digitalization. Governments are increasingly enforcing energy-efficiency regulations and promoting green building standards, which accelerates sensor adoption. The strong presence of electronics manufacturing, lower installation costs, and expanding smart city projects in China, India, Japan, and Southeast Asia further boost demand. Additionally, rising awareness of automation and energy savings is pushing both residential and commercial users to deploy occupancy sensors at a faster pace.

OCCUPANCY SENSOR MARKET SIZE, SHARE & ANALYSIS: COMPANY EVALUATION MATRIX

In the occupancy sensor companies matrix, Legrand (Star) leads with a strong global footprint and a versatile range of high-precision sensors that integrate seamlessly into modern lighting control and building automation systems. Its reliability, breadth of solutions, and focus on energy efficiency solidify its dominant position. Schneider Electric (Emerging Leader) is rapidly gaining traction with its IoT-enabled, data-driven sensing technologies that support smart-building analytics and dynamic energy optimization. While Legrand maintains a clear lead, Schneider Electric shows strong potential to move toward the leaders’ quadrant as demand grows for connected, intelligent occupancy sensing solutions.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

OCCUPANCY SENSOR MARKET KEY PLAYERS

- Legrand (France)

- Johnson Controls Inc (US)

- Eaton (Ireland)

- Honeywell International Inc (US)

- Schneider Electric (France)

- Acuity Brands (US)

- Signify Holdings (Netherlands)

- Hubbell (US)

- Leviton Manufacturing Co Inc. (US)

- Lutron Electronics Co Inc. (US)

OCCUPANCY SENSOR MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2023 (Value) | USD 2.53 Billion |

| Market Forecast in 2030 (Value) | USD 5.20 Billion |

| Growth Rate | CAGR of 11.2% from 2024-2030 |

| Years Considered | 2020-2030 |

| Base Year | 2023 |

| Forecast Period | 2024-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Million Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, South America, Middle East & Africa |

WHAT IS IN IT FOR YOU: OCCUPANCY SENSOR MARKET SIZE, SHARE & ANALYSIS REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Leading Building Automation OEM |

|

|

| Smart Lighting Solutions Provider |

|

|

| Commercial Real Estate Developer |

|

|

| Industrial Facility & Warehouse Operator |

|

|

RECENT DEVELOPMENTS

- May 2024 : Vantage, the Legrand brand for lighting control, announced its partnership with WALL-SMART, the provider of flush wall mount solutions. Through this cooperation, WALL-SMART will integrate the Vantage brand into its products to be seamlessly installed in any space, promoting an added aesthetic look and functionality

- April 2024 : Leviton has expanded its Smart Sensor line to include Smart Ceiling Mount Room Controllers (SRC) and Smart Ceiling Mount Sensors (CMS). These innovations make advanced lighting control easier to deploy. Advanced control strategies are combined into one device for cost-effectiveness and the ability to easily install them. By comparison, these solutions require only two devices against an industry standard four for code compliance, streamlining installation.

- February 2024 : Eaton has renewed its commitment to modernizing its manufacturing operations through the advancement of smart factories in Juarez, Mexico, and Changzhou, China. one a greenfield site and another a legacy site, each of them implemented Industry 4.0 technology into their processes to facilitate their respective upgrading and digitization

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

24

2

RESEARCH METHODOLOGY

29

3

EXECUTIVE SUMMARY

40

4

PREMIUM INSIGHTS

44

5

MARKET OVERVIEW

Surging smart building demand and IoT integration drive occupancy sensor market transformation.

47

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

GROWING DEMAND FOR ENERGY-EFFICIENT DEVICES

5.2.1.2

INCREASING DEPLOYMENT OF LIGHTING CONTROLLERS IN SMART HOMES

5.2.1.3

SURGING NEED FOR CONFIGURABLE AND PROGRAMMABLE SENSORS FOR HVAC SYSTEMS

5.2.2

RESTRAINTS

5.2.2.1

TECHNICAL LIMITATIONS OF OCCUPANCY SENSORS

5.2.2.2

INCONSISTENCY ISSUES RELATED TO WIRELESS NETWORK SYSTEMS

5.2.3

OPPORTUNITIES

5.2.3.1

GROWING INITIATIVES OF GOVERNMENTS FOR GREEN BUILDINGS

5.2.3.2

INCREASING DEMAND FOR SMART BUILDINGS IN URBAN AREAS

5.2.4

CHALLENGES

5.2.4.1

LACK OF AWARENESS REGARDING BENEFITS OF OCCUPANCY SENSORS

5.3

VALUE CHAIN ANALYSIS

5.4

ECOSYSTEM ANALYSIS

5.5

INVESTMENT AND FUNDING SCENARIO

5.6

PRICING ANALYSIS

5.6.1

INDICATIVE PRICING OF OCCUPANCY SENSORS OFFERED BY KEY PLAYERS, BY TYPE, 2023

5.6.2

AVERAGE SELLING PRICE TREND OF OCCUPANCY SENSORS, BY TYPE, 2019–2023

5.6.3

AVERAGE SELLING PRICE TREND OF OCCUPANCY SENSORS, BY REGION, 2019–2023

5.7

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.8

TECHNOLOGY ANALYSIS

5.8.1

KEY TECHNOLOGIES

5.8.1.1

INTERNET OF THINGS (IOT)

5.8.2

COMPLEMENTARY TECHNOLOGIES

5.8.2.1

WIRELESS COMMUNICATION

5.8.3

ADJACENT TECHNOLOGIES

5.8.3.1

ARTIFICIAL INTELLIGENCE

5.9

PORTER’S FIVE FORCES ANALYSIS

5.9.1

INTENSITY OF COMPETITIVE RIVALRY

5.9.2

BARGAINING POWER OF SUPPLIERS

5.9.3

BARGAINING POWER OF BUYERS

5.9.4

THREAT OF SUBSTITUTES

5.9.5

THREAT OF NEW ENTRANTS

5.10

KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2

BUYING CRITERIA

5.11

CASE STUDY ANALYSIS

5.11.1

GLOBAL COMPANY INSTALLS SENZOLIVE’S OCCUPANCY SENSORS FOR ENERGY SAVINGS AND WORKSPACE IMPROVEMENT

5.11.2

MULTINATIONAL BANK DEPLOYS SENZOLIVE’S OCCUPANCY SENSORS TO MEASURE SPACE UTILIZATION

5.11.3

BI NORWEGIAN BUSINESS SCHOOL ADOPTS PRESSAC’S OCCUPANCY SENSORS TO MEASURE OCCUPANCY BASED ON CAPACITY AND TIMING

5.12

TRADE ANALYSIS

5.12.1

IMPORT SCENARIO (HS CODE 853690)

5.12.2

EXPORT SCENARIO (HS CODE 853690)

5.13

PATENT ANALYSIS

5.14

KEY CONFERENCES AND EVENTS, 2025–2026

5.15

TARIFF AND REGULATORY LANDSCAPE

5.15.1

TARIFF ANALYSIS

5.15.2

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.15.3

GLOBAL SAFETY STANDARDS

5.16

IMPACT OF AI ON OCCUPANCY SENSOR MARKET

5.16.1

INTRODUCTION

5.16.2

USE CASES

6

OCCUPANCY SENSOR MARKET, BY TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 10 Data Tables

79

6.1

INTRODUCTION

6.2

WALL-MOUNTED

6.2.1

INCREASING FOCUS ON SUSTAINABILITY AND ENERGY EFFICIENCY TO BOOST DEMAND

6.3

CEILING-MOUNTED

6.3.1

RISING TREND OF SMART BUILDINGS TO ACCELERATE ADOPTION

6.4

DESK

6.4.1

GROWING FOCUS ON ENHANCING WORK ENVIRONMENT TO DRIVE IMPLEMENTATION

7

OCCUPANCY SENSOR MARKET, BY OPERATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

85

7.1

INTRODUCTION

7.2

INDOOR

7.2.1

RISING ADOPTION OF SMART BUILDING AND HOME AUTOMATION TECHNOLOGIES TO SUPPORT MARKET GROWTH

7.3

OUTDOOR

7.3.1

INCREASING FOCUS ON DEVELOPING ENERGY-EFFICIENT INFRASTRUCTURE AND SMART CITY PROJECTS TO CREATE OPPORTUNITIES

8

OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 10 Data Tables

89

8.1

INTRODUCTION

8.2

NEW

8.2.1

INCREASING SMART CITY PROJECTS AND SUSTAINABLE URBAN DEVELOPMENT INITIATIVES TO FUEL SEGMENTAL GROWTH

8.3

RETROFIT

8.3.1

PRESSING NEED TO UPGRADE EXISTING BUILDING INFRASTRUCTURE TO FOSTER SEGMENTAL GROWTH

9

OCCUPANCY SENSOR MARKET, BY COVERAGE AREA

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

95

9.1

INTRODUCTION

9.2

LESS THAN 90°

9.2.1

RISING DEPLOYMENT IN SMALL SPACE STOREROOMS, RESTROOMS, HALLWAYS, AND CORRIDORS TO CONTRIBUTE TO MARKET GROWTH

9.3

90–179°

9.3.1

ELEVATING ADOPTION OF SMART HOME SOLUTIONS AND SUSTAINABILITY INITIATIVES TO BOOST SEGMENTAL GROWTH

9.4

180–360°

9.4.1

INCREASING COMMERCIAL BUILDING PROJECTS TO CREATE LUCRATIVE OPPORTUNITIES FOR WIDE-COVERAGE SENSOR PROVIDERS

10

OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 8 Data Tables

99

10.1

INTRODUCTION

10.2

WIRED

10.2.1

CONSISTENT PERFORMANCE WITHOUT NEED FOR BATTERIES TO DRIVE ADOPTION

10.3

WIRELESS

10.3.1

WI-FI

10.3.1.1

ABILITY TO SEAMLESSLY INTEGRATE WITH SMART DEVICES AND PLATFORMS TO ACCELERATE SEGMENTAL GROWTH

10.3.2

ENOCEAN

10.3.2.1

LOW MAINTENANCE COST AND LESS POWER CONSUMPTION TO DRIVE ADOPTION

10.3.3

ZIGBEE

10.3.3.1

COMPATIBILITY WITH MESH NETWORKS AND LOW INSTALLATION AND MAINTENANCE COSTS TO FUEL SEGMENTAL GROWTH

10.3.4

Z-WAVE

10.3.4.1

INCREASING INCLINATION TOWARD HOME AUTOMATION SYSTEMS TO FOSTER SEGMENTAL GROWTH

10.3.5

OTHER PROTOCOLS

11

OCCUPANCY SENSOR MARKET, BY TECHNOLOGY

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 34 Data Tables

105

11.1

INTRODUCTION

11.2

PIR

11.2.1

ABILITY TO SENSE INFRARED RADIATION AND HEAT CREATED BY MOVING HUMAN BEINGS TO BOOST DEMAND

11.3

ULTRASONIC

11.3.1

HIGHER ACCURACY OF ULTRASONIC TECHNOLOGY TO FUEL ADOPTION IN COMPLEX SPACES

11.4

DUAL TECHNOLOGY

11.4.1

ENHANCED ACCURACY AND DECREASED FALSE DETECTIONS TO BOOST DEPLOYMENT IN COMMERCIAL SPACES

11.5

OTHER TECHNOLOGIES

12

OCCUPANCY SENSOR MARKET, BY APPLICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 34 Data Tables

119

12.1

INTRODUCTION

12.2

LIGHTING SYSTEMS

12.2.1

RISING NEED TO OPTIMIZE ENERGY USAGE IN COMMERCIAL APPLICATIONS TO SPIKE DEMAND

12.3

HVAC SYSTEMS

12.3.1

GROWING TREND OF SMART BUILDINGS TO ACCELERATE DEMAND

12.4

SECURITY AND SURVEILLANCE SYSTEMS

12.4.1

INCREASING PENETRATION OF SMART HOME AND IOT TECHNOLOGIES TO SUPPORT MARKET GROWTH

12.5

OTHER APPLICATIONS

13

OCCUPANCY SENSOR MARKET, BY END USE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 28 Data Tables

133

13.1

INTRODUCTION

13.2

RESIDENTIAL BUILDINGS

13.2.1

INDEPENDENT HOMES

13.2.1.1

INCREASING FOCUS ON HOMEOWNERS ON SETTING RESPONSIVE LIVING ENVIRONMENTS TO FUEL GROWTH

13.2.2

APARTMENTS

13.2.2.1

RISING ADOPTION OF SECURITY AND SURVEILLANCE SYSTEMS TO CONTRIBUTE TO MARKET GROWTH

13.3

COMMERCIAL BUILDINGS

13.3.1

OFFICES

13.3.1.1

STRINGENT GOVERNMENT REGULATIONS AND STANDARDS TO REDUCE ENERGY CONSUMPTION TO BOOST DEMAND

13.3.2

EDUCATIONAL INSTITUTIONS

13.3.2.1

RISING ADOPTION OF ENERGY-SAVING TECHNOLOGIES IN EDUCATIONAL FACILITIES TO PROPEL MARKET

13.3.3

INDUSTRIAL FACILITIES

13.3.3.1

INCREASING INTEGRATION OF IOT AND AUTOMATION IN INDUSTRIAL SETTINGS TO BOOST DEMAND

13.3.4

HEALTHCARE FACILITIES

13.3.4.1

INCREASING FOCUS ON ENHANCING PATIENT EXPERIENCE TO SUPPORT MARKET GROWTH

13.3.5

OTHER COMMERCIAL BUILDING TYPES

14

OCCUPANCY SENSOR MARKET, BY REGION

Comprehensive coverage of 10 Regions with country-level deep-dive of 10 Countries | 20 Data Tables.

147

14.1

INTRODUCTION

14.2

NORTH AMERICA

14.2.1

MACROECONOMIC OUTLOOK FOR NORTH AMERICA

14.2.2

US

14.2.2.1

INCREASING FOCUS OF GOVERNMENT ON REDUCING ENERGY CONSUMPTION TO ACCELERATE MARKET GROWTH

14.2.3

CANADA

14.2.3.1

GROWING ADOPTION OF SMART TECHNOLOGIES DUE TO RISING AWARENESS AMONG CONSUMERS TO DRIVE MARKET

14.2.4

MEXICO

14.2.4.1

RAPID URBANIZATION TO BOOST DEMAND FOR SMART TECHNOLOGIES

14.3

EUROPE

14.3.1

MACROECONOMIC OUTLOOK FOR EUROPE

14.3.2

GERMANY

14.3.2.1

GROWING CONSTRUCTION OF NEW RESIDENTIAL BUILDINGS TO DRIVE DEMAND

14.3.3

UK

14.3.3.1

BOOMING COMMERCIAL REAL ESTATE SECTOR TO CREATE LUCRATIVE OPPORTUNITIES

14.3.4

FRANCE

14.3.4.1

RISING INVESTMENTS IN SMART CITY TECHNOLOGIES TO BOOST DEMAND

14.3.5

REST OF EUROPE

14.4

ASIA PACIFIC

14.4.1

MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

14.4.2

CHINA

14.4.2.1

RISING INVESTMENTS IN SMART CITY PROJECTS TO DRIVE MARKET

14.4.3

JAPAN

14.4.3.1

GROWING ADOPTION OF BUILDING ENERGY MANAGEMENT SYSTEMS TO FUEL MARKET GROWTH

14.4.4

SOUTH KOREA

14.4.4.1

CONTINUOUS DEVELOPMENTS IN SENSOR TECHNOLOGIES TO DRIVE MARKET

14.4.5

AUSTRALIA

14.4.5.1

GOVERNMENT INITIATIVES PROMOTING SUSTAINABLE BUILDING PRACTICES TO FOSTER MARKET GROWTH

14.4.6

REST OF ASIA PACIFIC

14.5

ROW

14.5.1

MACROECONOMIC OUTLOOK FOR ROW

14.5.2

MIDDLE EAST & AFRICA

14.5.2.1

INCLINATION TOWARD ENERGY CONSERVATION INITIATIVES TO DRIVE MARKET

14.5.2.2

GCC

14.5.2.3

AFRICA & REST OF MIDDLE EAST

14.5.3

SOUTH AMERICA

14.5.3.1

GREEN BUILDING INITIATIVES TO BOOST DEMAND

15

COMPETITIVE LANDSCAPE

Discover how key players outpace competitors with strategic wins and market dominance insights.

163

15.1

OVERVIEW

15.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021–2024

15.3

REVENUE ANALYSIS, 2019–2023

15.4

MARKET SHARE ANALYSIS, 2O23

15.5

COMPANY VALUATION AND FINANCIAL METRICS, 2023

15.6

COVERAGE AREA/RESPONSE TIME COMPARISON

15.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

15.7.1

STARS

15.7.2

EMERGING LEADERS

15.7.3

PERVASIVE PLAYERS

15.7.4

PARTICIPANTS

15.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2023

15.7.5.1

COMPANY FOOTPRINT

15.7.5.2

REGION FOOTPRINT

15.7.5.3

TYPE FOOTPRINT

15.7.5.4

TECHNOLOGY FOOTPRINT

15.7.5.5

APPLICATION FOOTPRINT

15.8

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

15.8.1

PROGRESSIVE COMPANIES

15.8.2

RESPONSIVE COMPANIES

15.8.3

DYNAMIC COMPANIES

15.8.4

STARTING BLOCKS

15.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

15.8.5.1

DETAILED LIST OF KEY STARTUPS/SMES

15.8.5.2

COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

15.9

COMPETITIVE SCENARIO

15.9.1

PRODUCT LAUNCHES

15.9.2

DEALS

15.9.3

EXPANSIONS

16

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

183

16.1

KEY PLAYERS

16.1.1

LEGRAND

16.1.1.1

BUSINESS OVERVIEW

16.1.1.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

16.1.1.3

RECENT DEVELOPMENTS

16.1.1.3.1

DEALS

16.1.1.4

MNM VIEW

16.1.1.4.1

RIGHT TO WIN

16.1.1.4.2

STRATEGIC CHOICES

16.1.1.4.3

WEAKNESSES AND COMPETITIVE THREATS

16.1.2

JOHNSON CONTROLS INC.

16.1.3

EATON

16.1.4

HONEYWELL INTERNATIONAL INC.

16.1.5

SCHNEIDER ELECTRIC

16.1.6

ACUITY BRANDS, INC.

16.1.7

SIGNIFY HOLDING

16.1.8

HUBBELL

16.1.9

LEVITON MANUFACTURING CO., INC.

16.1.10

LUTRON ELECTRONICS CO., INC

16.2

OTHER PLAYERS

16.2.1

SIEMENS

16.2.2

ALAN MANUFACTURING, INC.

16.2.3

ENERLITES, INC.

16.2.4

FUNCTIONAL DEVICES, INC

16.2.5

PYROTECH ELECTRONICS PVT. LTD.

16.2.6

B.E.G. BRÜCK ELECTRONIC GMBH

16.2.7

HAGER GROUP

16.2.8

CRESTRON ELECTRONICS, INC.

16.2.9

OPTEX CO., LTD.

16.2.10

PRESSAC COMMUNICATIONS LIMITED

16.2.11

AVUITY

16.2.12

ENOCEAN GMBH

16.2.13

IR-TEC INTERNATIONAL LTD.

16.2.14

WIPRO LIGHTING

16.2.15

INTERMATIC INCORPORATED

16.2.16

OCTIOT

16.2.17

RAYZEEK

16.2.18

FM: SYSTEMS

17

APPENDIX

225

17.1

INSIGHTS FROM INDUSTRY EXPERTS

17.2

DISCUSSION GUIDE

17.3

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

17.4

CUSTOMIZATION OPTIONS

17.5

RELATED REPORTS

17.6

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

ROLE OF COMPANIES IN ECOSYSTEM

TABLE 2

INDICATIVE PRICING OF OCCUPANCY SENSORS PROVIDED BY KEY PLAYERS, BY TYPE, 2023

TABLE 3

OCCUPANCY SENSOR MARKET: PORTER’S FIVE FORCES ANALYSIS

TABLE 4

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS (%)

TABLE 5

KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

TABLE 6

IMPORT SCENARIO FOR HS CODE 853690-COMPLIANT PRODUCTS, BY COUNTRY, 2019–2023 (USD MILLION)

TABLE 7

EXPORT SCENARIO FOR HS CODE 853690-COMPLIANT PRODUCTS, BY COUNTRY, 2019–2023 (USD MILLION)

TABLE 8

MAJOR PATENTS IN OCCUPANCY SENSOR MARKET, 2021–2024

TABLE 9

OCCUPANCY SENSOR MARKET: MAJOR CONFERENCES AND EVENTS, 2025–2026

TABLE 10

MFN TARIFF FOR HS CODE 853690-COMPLIANT PRODUCTS EXPORTED BY US, 2023

TABLE 11

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 12

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 13

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 14

ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 15

SAFETY STANDARDS FOR OCCUPANCY SENSORS, BY REGION

TABLE 16

OCCUPANCY SENSOR MARKET, BY TYPE, 2020–2023 (USD MILLION)

TABLE 17

OCCUPANCY SENSOR MARKET, BY TYPE, 2024–2030 (USD MILLION)

TABLE 18

OCCUPANCY SENSOR MARKET, BY TYPE, 2020–2023 (THOUSAND UNITS)

TABLE 19

OCCUPANCY SENSOR MARKET, BY TYPE, 2024–2030 (THOUSAND UNITS)

TABLE 20

WALL-MOUNTED: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2020–2023 (USD MILLION)

TABLE 21

WALL-MOUNTED: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2024–2030 (USD MILLION)

TABLE 22

CEILING-MOUNTED: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2020–2023 (USD MILLION)

TABLE 23

CEILING-MOUNTED: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2024–2030 (USD MILLION)

TABLE 24

DESK: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2020–2023 (USD MILLION)

TABLE 25

DESK: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2024–2030 (USD MILLION)

TABLE 26

OCCUPANCY SENSOR MARKET, BY OPERATION, 2020–2023 (USD MILLION)

TABLE 27

OCCUPANCY SENSOR MARKET, BY OPERATION, 2024–2030 (USD MILLION)

TABLE 28

OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2020–2023 (USD MILLION)

TABLE 29

OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2024–2030 (USD MILLION)

TABLE 30

NEW: OCCUPANCY SENSOR MARKET, BY TYPE, 2020–2023 (USD MILLION)

TABLE 31

NEW: OCCUPANCY SENSOR MARKET, BY TYPE, 2024–2030 (USD MILLION)

TABLE 32

NEW: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2020–2023 (USD MILLION)

TABLE 33

NEW: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2024–2030 (USD MILLION)

TABLE 34

RETROFIT: OCCUPANCY SENSOR MARKET, BY TYPE, 2020–2023 (USD MILLION)

TABLE 35

RETROFIT: OCCUPANCY SENSOR MARKET, BY TYPE, 2024–2030 (USD MILLION)

TABLE 36

RETROFIT: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2020–2023 (USD MILLION)

TABLE 37

RETROFIT: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2024–2030 (USD MILLION)

TABLE 38

OCCUPANCY SENSOR MARKET, BY COVERAGE AREA, 2020–2023 (USD MILLION)

TABLE 39

OCCUPANCY SENSOR MARKET, BY COVERAGE AREA, 2024–2030 (USD MILLION)

TABLE 40

OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2020–2023 (USD MILLION)

TABLE 41

OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2024–2030 (USD MILLION)

TABLE 42

WIRED: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2020–2023 (USD MILLION)

TABLE 43

WIRED: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2024–2030 (USD MILLION)

TABLE 44

WIRELESS: OCCUPANCY SENSOR MARKET, BY PROTOCOL, 2020–2023 (USD MILLION)

TABLE 45

WIRELESS: OCCUPANCY SENSOR MARKET, BY PROTOCOL, 2024–2030 (USD MILLION)

TABLE 46

WIRELESS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2020–2023 (USD MILLION)

TABLE 47

WIRELESS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2024–2030 (USD MILLION)

TABLE 48

OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2020–2023 (USD MILLION)

TABLE 49

OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2024–2030 (USD MILLION)

TABLE 50

PIR: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2020–2023 (USD MILLION)

TABLE 51

PIR: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2024–2030 (USD MILLION)

TABLE 52

PIR: OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2020–2023 (USD MILLION)

TABLE 53

PIR: OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2024–2030 (USD MILLION)

TABLE 54

PIR: OCCUPANCY SENSOR MARKET FOR WIRELESS NETWORK CONNECTIVITY, BY PROTOCOL, 2020–2023 (USD MILLION)

TABLE 55

PIR: OCCUPANCY SENSOR MARKET FOR WIRELESS NETWORK CONNECTIVITY, BY PROTOCOL, 2024–2030 (USD MILLION)

TABLE 56

PIR: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 57

PIR: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 58

ULTRASONIC: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2020–2023 (USD MILLION)

TABLE 59

ULTRASONIC: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2024–2030 (USD MILLION)

TABLE 60

ULTRASONIC: OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2020–2023 (USD MILLION)

TABLE 61

ULTRASONIC: OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2024–2030 (USD MILLION)

TABLE 62

ULTRASONIC: OCCUPANCY SENSOR MARKET FOR WIRELESS NETWORK CONNECTIVITY, BY PROTOCOL, 2020–2023 (USD MILLION)

TABLE 63

ULTRASONIC: OCCUPANCY SENSOR MARKET FOR WIRELESS NETWORK CONNECTIVITY, BY PROTOCOL, 2024–2030 (USD MILLION)

TABLE 64

ULTRASONIC: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 65

ULTRASONIC: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 66

DUAL TECHNOLOGY: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2020–2023 (USD MILLION)

TABLE 67

DUAL TECHNOLOGY: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2024–2030 (USD MILLION)

TABLE 68

DUAL TECHNOLOGY: OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2020–2023 (USD MILLION)

TABLE 69

DUAL TECHNOLOGY: OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2024–2030 (USD MILLION)

TABLE 70

DUAL TECHNOLOGY: OCCUPANCY SENSOR MARKET FOR WIRELESS NETWORK CONNECTIVITY, BY PROTOCOL, 2020–2023 (USD MILLION)

TABLE 71

DUAL TECHNOLOGY: OCCUPANCY SENSOR MARKET FOR WIRELESS NETWORK CONNECTIVITY, BY PROTOCOL, 2024–2030 (USD MILLION)

TABLE 72

DUAL TECHNOLOGY: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 73

DUAL TECHNOLOGY: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 74

OTHER TECHNOLOGIES: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2020–2023 (USD MILLION)

TABLE 75

OTHER TECHNOLOGIES: OCCUPANCY SENSOR MARKET, BY INSTALLATION TYPE, 2024–2030 (USD MILLION)

TABLE 76

OTHER TECHNOLOGIES: OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2020–2023 (USD MILLION)

TABLE 77

OTHER TECHNOLOGIES: OCCUPANCY SENSOR MARKET, BY NETWORK CONNECTIVITY, 2024–2030 (USD MILLION)

TABLE 78

OTHER TECHNOLOGIES: OCCUPANCY SENSOR MARKET FOR WIRELESS NETWORK CONNECTIVITY, BY PROTOCOL, 2020–2023 (USD MILLION)

TABLE 79

OTHER TECHNOLOGIES: OCCUPANCY SENSOR MARKET FOR WIRELESS NETWORK CONNECTIVITY, BY PROTOCOL, 2024–2030 (USD MILLION)

TABLE 80

OTHER TECHNOLOGIES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 81

OTHER TECHNOLOGIES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 82

OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 83

OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 84

LIGHTING SYSTEMS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2020–2023 (USD MILLION)

TABLE 85

LIGHTING SYSTEMS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2024–2030 (USD MILLION)

TABLE 86

LIGHTING SYSTEMS: OCCUPANCY SENSOR MARKET, BY END USE, 2020–2023 (USD MILLION)

TABLE 87

LIGHTING SYSTEMS: OCCUPANCY SENSOR MARKET, BY END USE, 2024–2030 (USD MILLION)

TABLE 88

LIGHTING SYSTEMS: OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 89

LIGHTING SYSTEMS: OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 90

LIGHTING SYSTEMS: OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 91

LIGHTING SYSTEMS: OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 92

HVAC SYSTEMS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2020–2023 (USD MILLION)

TABLE 93

HVAC SYSTEMS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2024–2030 (USD MILLION)

TABLE 94

HVAC SYSTEMS: OCCUPANCY SENSOR MARKET, BY END USE, 2020–2023 (USD MILLION)

TABLE 95

HVAC SYSTEMS: OCCUPANCY SENSOR MARKET, BY END USE, 2024–2030 (USD MILLION)

TABLE 96

HVAC SYSTEMS: OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 97

HVAC SYSTEMS: OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 98

HVAC SYSTEMS: OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 99

HVAC SYSTEMS: OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 100

SECURITY AND SURVEILLANCE SYSTEMS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2020–2023 (USD MILLION)

TABLE 101

SECURITY AND SURVEILLANCE SYSTEMS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2024–2030 (USD MILLION)

TABLE 102

SECURITY AND SURVEILLANCE SYSTEMS: OCCUPANCY SENSOR MARKET, BY END USE, 2020–2023 (USD MILLION)

TABLE 103

SECURITY AND SURVEILLANCE SYSTEMS: OCCUPANCY SENSOR MARKET, BY END USE, 2024–2030 (USD MILLION)

TABLE 104

SECURITY AND SURVEILLANCE SYSTEMS: OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 105

SECURITY AND SURVEILLANCE SYSTEMS: OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 106

SECURITY AND SURVEILLANCE SYSTEMS: OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 107

SECURITY AND SURVEILLANCE SYSTEMS: OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 108

OTHER APPLICATIONS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2020–2023 (USD MILLION)

TABLE 109

OTHER APPLICATIONS: OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, 2024–2030 (USD MILLION)

TABLE 110

OTHER APPLICATIONS: OCCUPANCY SENSOR MARKET, BY END USE, 2020–2023 (USD MILLION)

TABLE 111

OTHER APPLICATIONS: OCCUPANCY SENSOR MARKET, BY END USE, 2024–2030 (USD MILLION)

TABLE 112

OTHER APPLICATIONS: OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 113

OTHER APPLICATIONS: OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 114

OTHER APPLICATIONS: OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 115

OTHER APPLICATIONS: OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 116

OCCUPANCY SENSOR MARKET, BY END USE, 2020–2023 (USD MILLION)

TABLE 117

OCCUPANCY SENSOR MARKET, BY END USE, 2024–2030 (USD MILLION)

TABLE 118

OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 119

OCCUPANCY SENSOR MARKET, BY RESIDENTIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 120

OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2020–2023 (USD MILLION)

TABLE 121

OCCUPANCY SENSOR MARKET, BY COMMERCIAL BUILDING TYPE, 2024–2030 (USD MILLION)

TABLE 122

RESIDENTIAL BUILDINGS: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 123

RESIDENTIAL BUILDINGS: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 124

RESIDENTIAL BUILDINGS: OCCUPANCY SENSOR MARKET, BY REGION, 2020–2023 (USD MILLION)

TABLE 125

RESIDENTIAL BUILDINGS: OCCUPANCY SENSOR MARKET, BY REGION, 2024–2030 (USD MILLION)

TABLE 126

INDEPENDENT HOMES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 127

INDEPENDENT HOMES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 128

APARTMENTS: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 129

APARTMENTS: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 130

COMMERCIAL BUILDINGS: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 131

COMMERCIAL BUILDINGS: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 132

COMMERCIAL BUILDINGS: OCCUPANCY SENSOR MARKET, BY REGION, 2020–2023 (USD MILLION)

TABLE 133

COMMERCIAL BUILDINGS: OCCUPANCY SENSOR MARKET, BY REGION, 2024–2030 (USD MILLION)

TABLE 134

OFFICES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 135

OFFICES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 136

EDUCATIONAL INSTITUTIONS: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 137

EDUCATIONAL INSTITUTIONS: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 138

INDUSTRIAL FACILITIES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 139

INDUSTRIAL FACILITIES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 140

HEALTHCARE FACILITIES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 141

HEALTHCARE FACILITIES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 142

OTHER COMMERCIAL BUILDING TYPES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 143

OTHER COMMERCIAL BUILDING TYPES: OCCUPANCY SENSOR MARKET, BY APPLICATION, 2024–2030 (USD MILLION)

TABLE 144

OCCUPANCY SENSOR MARKET, BY REGION, 2020–2023 (USD MILLION)

TABLE 145

OCCUPANCY SENSOR MARKET, BY REGION, 2024–2030 (USD MILLION)

TABLE 146

NORTH AMERICA: OCCUPANCY SENSOR MARKET, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 147

NORTH AMERICA: OCCUPANCY SENSOR MARKET, BY COUNTRY, 2024–2030 (USD MILLION)

TABLE 148

NORTH AMERICA: OCCUPANCY SENSOR MARKET, BY END USE, 2020–2023 (USD MILLION)

TABLE 149

NORTH AMERICA: OCCUPANCY SENSOR MARKET, BY END USE, 2024–2030 (USD MILLION)

TABLE 150

EUROPE: OCCUPANCY SENSOR MARKET, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 151

EUROPE: OCCUPANCY SENSOR MARKET, BY COUNTRY, 2024–2030 (USD MILLION)

TABLE 152

EUROPE: OCCUPANCY SENSOR MARKET, BY END USE, 2020–2023 (USD MILLION)

TABLE 153

EUROPE: OCCUPANCY SENSOR MARKET, BY END USE, 2024–2030 (USD MILLION)

TABLE 154

ASIA PACIFIC: OCCUPANCY SENSOR MARKET, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 155

ASIA PACIFIC: OCCUPANCY SENSOR MARKET, BY COUNTRY, 2024–2030 (USD MILLION)

TABLE 156

ASIA PACIFIC: OCCUPANCY SENSOR MARKET, BY END USE, 2020–2023 (USD MILLION)

TABLE 157

ASIA PACIFIC: OCCUPANCY SENSOR MARKET, BY END USE, 2024–2030 (USD MILLION)

TABLE 158

ROW: OCCUPANCY SENSOR MARKET, BY REGION, 2020–2023 (USD MILLION)

TABLE 159

ROW: OCCUPANCY SENSOR MARKET, BY REGION, 2024–2030 (USD MILLION)

TABLE 160

ROW: OCCUPANCY SENSOR MARKET, BY END USE, 2020–2023 (USD MILLION)

TABLE 161

ROW: OCCUPANCY SENSOR MARKET, BY END USE, 2024–2030 (USD MILLION)

TABLE 162

MIDDLE EAST & AFRICA: OCCUPANCY SENSOR MARKET, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 163

MIDDLE EAST & AFRICA: OCCUPANCY SENSOR MARKET, BY COUNTRY, 2024–2030 (USD MILLION)

TABLE 164

OCCUPANCY SENSOR MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2021–2024

TABLE 165

OCCUPANCY SENSOR MARKET: DEGREE OF COMPETITION, 2023

TABLE 166

OCCUPANCY SENSOR MARKET: REGION FOOTPRINT

TABLE 167

OCCUPANCY SENSOR MARKET: TYPE FOOTPRINT

TABLE 168

OCCUPANCY SENSOR MARKET: TECHNOLOGY FOOTPRINT

TABLE 169

OCCUPANCY SENSOR MARKET: APPLICATION FOOTPRINT

TABLE 170

OCCUPANCY SENSOR MARKET: LIST OF KEY STARTUPS/SMES

TABLE 171

OCCUPANCY SENSOR MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 172

OCCUPANCY SENSOR MARKET: PRODUCT LAUNCHES, JANUARY 2021−SEPTEMBER 2024

TABLE 173

OCCUPANCY SENSOR MARKET: DEALS, JANUARY 2021–SEPTEMBER 2024

TABLE 174

OCCUPANCY SENSOR MARKET: EXPANSIONS, JANUARY 2021–SEPTEMBER 2024

TABLE 175

LEGRAND: COMPANY OVERVIEW

TABLE 176

LEGRAND: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 177

LEGRAND: DEALS

TABLE 178

JOHNSON CONTROLS INC.: COMPANY OVERVIEW

TABLE 179

JOHNSON CONTROLS INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 180

EATON: COMPANY OVERVIEW

TABLE 181

EATON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 182

EATON: EXPANSIONS

TABLE 183

HONEYWELL INTERNATIONAL INC.: COMPANY OVERVIEW

TABLE 184

HONEYWELL INTERNATIONAL INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 185

SCHNEIDER ELECTRIC: COMPANY OVERVIEW

TABLE 186

SCHNEIDER ELECTRIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 187

ACUITY BRANDS, INC.: COMPANY OVERVIEW

TABLE 188

ACUITY BRANDS, INC.: PRODUCT LAUNCHES

TABLE 189

SIGNIFY HOLDING: COMPANY OVERVIEW

TABLE 190

SIGNIFY HOLDING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 191

SIGNIFY HOLDING: PRODUCT LAUNCHES

TABLE 192

HUBBELL: COMPANY OVERVIEW

TABLE 193

HUBBELL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 194

LEVITON MANUFACTURING CO., INC.: COMPANY OVERVIEW

TABLE 195

LEVITON MANUFACTURING CO., INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 196

LEVITON MANUFACTURING CO., INC.: PRODUCT LAUNCHES

TABLE 197

LEVITON MANUFACTURING CO., INC.: EXPANSIONS

TABLE 198

LUTRON ELECTRONICS CO., INC: COMPANY OVERVIEW

TABLE 199

LUTRON ELECTRONICS CO., INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 200

LUTRON ELECTRONICS CO., INC: PRODUCT LAUNCHES

LIST OF FIGURES

FIGURE 1

OCCUPANCY SENSOR MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

OCCUPANCY SENSOR MARKET: RESEARCH DESIGN

FIGURE 3

REVENUE GENERATED BY COMPANIES FROM SALES OF OCCUPANCY SENSORS

FIGURE 4

OCCUPANCY SENSOR MARKET: BOTTOM-UP APPROACH

FIGURE 5

MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

FIGURE 6

DATA TRIANGULATION

FIGURE 7

CEILING-MOUNTED SEGMENT TO EXHIBIT HIGHEST CAGR IN OCCUPANCY SENSOR MARKET, BY TYPE, DURING FORECAST PERIOD

FIGURE 8

PIR SEGMENT TO DOMINATE OCCUPANCY SENSOR MARKET, BY TECHNOLOGY, IN 2024

FIGURE 9

HVAC SYSTEMS SEGMENT TO RECORD HIGHEST CAGR IN OCCUPANCY SENSOR MARKET, BY APPLICATION, DURING FORECAST PERIOD

FIGURE 10

ASIA PACIFIC TO WITNESS HIGHEST CAGR IN OCCUPANCY SENSOR MARKET BETWEEN 2024 AND 2030

FIGURE 11

RISE OF SMART BUILDINGS AND INTERNET OF THINGS (IOT) TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

FIGURE 12

WIRELESS SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE IN 2024

FIGURE 13

DUAL TECHNOLOGY TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 14

COMMERCIAL BUILDINGS AND NORTH AMERICA TO CLAIM LARGEST MARKET SHARE IN 2030

FIGURE 15

CHINA TO REGISTER HIGHEST CAGR IN GLOBAL OCCUPANCY SENSOR MARKET DURING FORECAST PERIOD

FIGURE 16

OCCUPANCY SENSOR MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 17

IMPACT OF DRIVERS ON OCCUPANCY SENSOR MARKET

FIGURE 18

IMPACT OF RESTRAINTS ON OCCUPANCY SENSOR MARKET

FIGURE 19

IMPACT OF OPPORTUNITIES ON OCCUPANCY SENSOR MARKET

FIGURE 20

IMPACT OF CHALLENGES ON OCCUPANCY SENSOR MARKET

FIGURE 21

VALUE CHAIN ANALYSIS: OCCUPANCY SENSOR MARKET

FIGURE 22

OCCUPANCY SENSOR ECOSYSTEM

FIGURE 23

SMART HOME AND SMART BUILDING FUNDINGS IN US STARTUPS, 2019–2023

FIGURE 24

INDICATIVE PRICING OF OCCUPANCY SENSOR TYPES OFFERED BY KEY PLAYERS, 2023

FIGURE 25

AVERAGE SELLING PRICE TREND OF OCCUPANCY SENSORS, BY TYPE, 2019–2023

FIGURE 26

AVERAGE SELLING PRICE TREND OF OCCUPANCY SENSORS, BY REGION, 2019–2023

FIGURE 27

TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

FIGURE 28

OCCUPANCY SENSOR MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 29

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS

FIGURE 30

KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

FIGURE 31

IMPORT DATA FOR HS CODE 853690-COMPLIANT PRODUCTS FOR TOP 5 COUNTRIES, 2019–2023

FIGURE 32

EXPORT DATA FOR HS CODE 853690-COMPLIANT PRODUCTS FOR TOP 5 COUNTRIES, 2019–2023 (USD MILLION)

FIGURE 33

OCCUPANCY SENSOR MARKET: PATENT ANALYSIS, 2014−2024

FIGURE 34

USE CASES OF AI-POWERED OCCUPANCY SENSORS

FIGURE 35

CEILING-MOUNTED SENSORS TO LEAD OCCUPANCY SENSOR MARKET THROUGHOUT FORECAST PERIOD

FIGURE 36

OUTDOOR SEGMENT TO EXHIBIT HIGHER CAGR DURING FORECAST PERIOD

FIGURE 37

NEW INSTALLATIONS TO COMMAND OCCUPANCY SENSOR MARKET DURING FORECAST PERIOD

FIGURE 38

180–360° SEGMENT TO DOMINATE OCCUPANCY SENSOR MARKET DURING FORECAST PERIOD

FIGURE 39

WIRELESS NETWORK CONNECTIVITY TO LEAD OCCUPANCY SENSOR MARKET DURING FORECAST PERIOD

FIGURE 40

PIR TECHNOLOGY TO ACCOUNT FOR LARGEST SHARE OF OCCUPANCY SENSOR MARKET THROUGHOUT FORECAST PERIOD

FIGURE 41

LIGHTING SYSTEMS TO CAPTURE LARGEST MARKET SHARE IN 2030

FIGURE 42

COMMERCIAL BUILDINGS TO LEAD OCCUPANCY SENSOR MARKET FROM 2024 TO 2030

FIGURE 43

NORTH AMERICA TO DOMINATE OCCUPANCY SENSOR MARKET DURING FORECAST PERIOD

FIGURE 44

NORTH AMERICA: OCCUPANCY SENSOR MARKET SNAPSHOT

FIGURE 45

EUROPE: OCCUPANCY SENSOR MARKET SNAPSHOT

FIGURE 46

ASIA PACIFIC: OCCUPANCY SENSOR MARKET SNAPSHOT

FIGURE 47

OCCUPANCY SENSOR MARKET: REVENUE ANALYSIS OF TOP 5 PLAYERS, 2019–2023

FIGURE 48

MARKET SHARE ANALYSIS OF KEY PLAYERS, 2023

FIGURE 49

COMPANY VALUATION, 2023

FIGURE 50

FINANCIAL METRICS (EV/EBITDA), 2024

FIGURE 51

COVERAGE AREA/RESPONSE TIME COMPARISON

FIGURE 52

OCCUPANCY SENSOR MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

FIGURE 53

OCCUPANCY SENSOR MARKET: COMPANY FOOTPRINT

FIGURE 54

OCCUPANCY SENSOR MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

FIGURE 55

LEGRAND: COMPANY SNAPSHOT

FIGURE 56

JOHNSON CONTROLS INC.: COMPANY SNAPSHOT

FIGURE 57

EATON: COMPANY SNAPSHOT

FIGURE 58

HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

FIGURE 59

SCHNEIDER ELECTRIC: COMPANY SNAPSHOT

FIGURE 60

ACUITY BRANDS, INC.: COMPANY SNAPSHOT

FIGURE 61

SIGNIFY HOLDING: COMPANY SNAPSHOT

FIGURE 62

HUBBELL: COMPANY SNAPSHOT

Methodology

The study used four major activities to estimate the market size of the occupancy sensor. Exhaustive secondary research was conducted to gather information on the market and its peer and parent markets. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the total market size. Finally, market breakdown and data triangulation methods were utilized to estimate the market size for different segments and subsegments.

Secondary Research

The research methodology used to estimate and forecast the size of the occupancy sensor market began with the acquisition of data related to the revenues of key vendors in the market through secondary research. Various secondary sources have been referred to in the secondary research process for identifying and collecting information for this study. Secondary sources include annual reports, press releases, and investor presentations of companies; white papers, journals, certified publications, and articles by recognized authors; websites; directories; and databases. Secondary research has mainly been used to obtain key information about the value chain of the occupancy sensor market, key players, market classification, and segmentation according to the industry trends to the bottom-most level, geographic markets, and key developments from both market and technology-oriented perspectives. Secondary data has been collected and analyzed to determine the overall market size, further validated through primary research. The secondary research referred to for this research study involves the Semiconductor Industry Association (SIA), Electronic System Design Alliance (ESD Alliance), Institute of Electrical and Electronics Engineers (IEEE), Taiwan Semiconductor Industry Association (TSIA), European Semiconductor Industry Association (ESIA), and Korea Semiconductor Industry Association (KSIA). Moreover, the study involved extensive use of secondary sources, directories, and databases, such as Hoovers, Bloomberg Businessweek, Factiva, and OneSource, to identify and collect valuable information for a technical, market-oriented, and commercial study of the occupancy sensor market. Vendor offerings have been taken into consideration to determine market segmentation.

Primary Research

In the primary research, various primary sources from both the supply and demand sides have been interviewed to obtain the qualitative and quantitative information relevant to this report. Primary sources from the supply side include the key industry participants, subject-matter experts (SMEs), and C-level executives and consultants from various key companies and organizations in the occupancy sensor ecosystem. After the complete market engineering (including calculations for the market statistics, the market breakdown, the market size estimations, the market forecasting, and the data triangulation), extensive primary research has been conducted to verify and validate the critical market numbers obtained. Extensive qualitative and quantitative analyses have been performed during the market engineering process to list key information/insights throughout the report. Extensive primary research has been conducted after understanding the occupancy sensor market scenario through secondary research. Several primary interviews have been conducted with market experts from the demand and supply-side players across key regions, namely, North America, Europe, Asia Pacific, and the Rest of the World (Middle East, Africa, and South America). Various primary sources from both the supply and demand sides of the market have been interviewed to obtain qualitative and quantitative information. Following is the breakdown of the primary respondents.

Primary data has been collected through questionnaires, emails, and telephonic interviews. In the canvassing of primaries, various departments within organizations, such as sales, operations, and administration, were covered to provide a holistic viewpoint in our report. After interacting with industry experts, brief sessions were conducted with highly experienced independent consultants to reinforce the findings from our primaries. This and the in-house subject matter experts’ opinions have led us to the findings described in the remainder of this report.

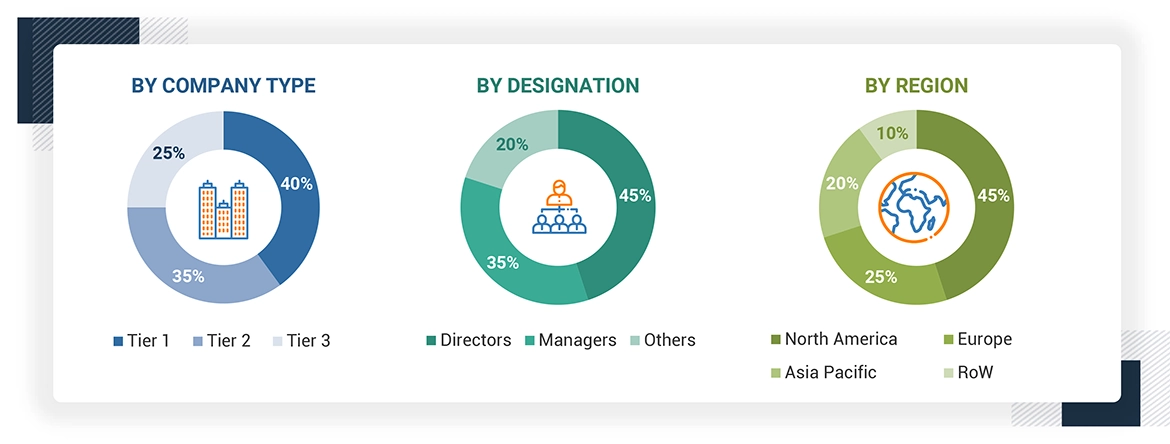

Note: The three tiers of the companies are defined based on their total revenue in 2023: Tier 1 - revenue greater than or equal to USD 1 billion; Tier 2 - revenue between USD 100 million and USD 1 billion; and Tier 3 revenue less than or equal to USD 100 million. Other designations include sales managers, marketing managers, and product managers.

About the assumptions considered for the study, To know download the pdf brochure

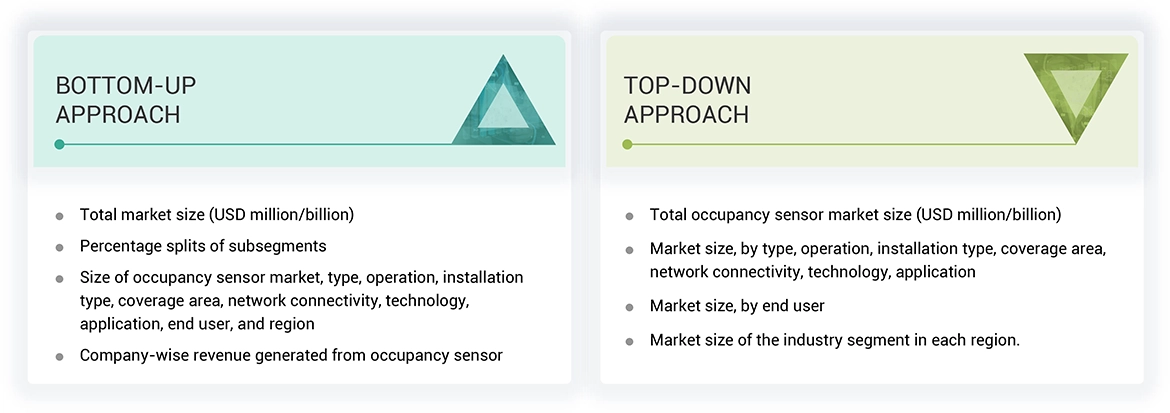

Market Size Estimation

To estimate and validate the size of the occupancy sensor market and its submarkets, both top-down and bottom-up approaches were utilized. Secondary research was conducted to identify the key players in the market, and primary and secondary research was used to determine their market share in specific regions. The entire process involved studying top players' annual and financial reports and conducting extensive interviews with industry leaders such as CEOs, VPs, directors, and marketing executives. Secondary sources were used to determine all percentage shares and breakdowns, which were verified through primary sources. All parameters that could impact the markets covered in this research study were accounted for, analyzed in detail, verified through primary research, and consolidated to obtain the final quantitative and qualitative data.

Occupancy Sensor Market : Top-Down and Bottom-Up Approach

Data Triangulation

Once the overall size of the occupancy sensor market was determined using the methods described above, it was divided into multiple segments and subsegments. Market engineering was performed for each segment and subsegment using market breakdown and data triangulation methods, as applicable, to obtain accurate statistics. To triangulate the data, various factors and trends from the demand and supply sides were studied. The market was validated using both top-down and bottom-up approaches.

Market Definition

Occupancy sensor a device that detects the presence of people in a given area and controls devices such as lighting, HVAC (heating, ventilation, and air conditioning), or security related to whether it is occupied or vacant. These sensors automatically perform certain functions to prevent energy wastage, increase safety, and increase efficiency. They work based on the use of technologies of passive infrared (PIR) and ultrasonic detection. Occupancy sensors are controlling devices on energy use for many applications such as lighting, HVAC, and security systems. They can be mounted in walls, such as corner post or as wall switches, or on ceilings in order to detect the occupancy of a space. It can be deployed in residential and commercial settings to save energy and enhance automation systems. The sensors, by adjusting parameters automatically based on real time detection of an individual's presence, save operational cost and promote user comfort and security.

Key Stakeholders

- Raw material & manufacturing equipment suppliers

- Property and building developers

- Original equipment manufacturers (end-user applications/electronic product manufacturers)

- Distributors and retailers

- Network providers

- Research organizations

- System integrators

- Technology investors

- Lighting companies

Report Objectives

- To describe and forecast the occupancy sensor market, by type, operation, installation type, coverage area, network connectivity, technology, application, end user and region, in terms of value

- To describe and forecast the market for various segments across four central regions, namely, North America, Europe, Asia Pacific, and Rest of the World (RoW), in terms of value

- To strategically analyze the micro markets with regard to the individual growth trends, prospects, and contribution to the market

- To provide detailed information regarding drivers, restraints, opportunities, and challenges influencing the growth of the market

- To analyze opportunities for stakeholders by identifying high-growth segments in the market

- To provide a detailed overview of the value chain

- To strategically analyze the ecosystem, regulatory landscape, patent landscape, Porter’s five forces, import and export scenarios trade landscape, and case studies pertaining to the market under study

- To strategically profile key players in the occupancy sensor market and comprehensively analyze their market shares and core competencies

- To strategically profile the key players and provide a detailed competitive landscape of the market

- To analyze competitive developments such as partnerships, acquisitions, expansions, collaborations, and product launches, along with research and development (R&D) in the occupancy sensor market

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

- Detailed analysis and profiling of additional market players (up to 5)

- Additional country-level analysis of the occupancy sensor market

Product Analysis

- Product matrix, which provides a detailed comparison of the product portfolio of each company in the occupancy sensor market.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Occupancy Sensor Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

- US Occupancy Sensor Market

- Canada Occupancy Sensor Market

- Mexico Occupancy Sensor Market

- Germany Occupancy Sensor Market

- UK Occupancy Sensor Market

- France Occupancy Sensor Market

- Rest Of Europe Occupancy Sensor Market

- China Occupancy Sensor Market

- Japan Occupancy Sensor Market

- South Korea Occupancy Sensor Market

- Australia Occupancy Sensor Market

- Rest Of Asia Pacific Occupancy Sensor Market

- GCC Occupancy Sensor Market

- South America Occupancy Sensor Market

Growth opportunities and latent adjacency in Occupancy Sensor Market

Gavin

Apr, 2026

Does the report profile key players based on product offerings, strategies, and future growth positioning?.

Terry

Apr, 2026

Does the report provide insights into demand drivers across offices, healthcare, education, and retail environments?.

Jan, 2015

Dear Ms./Sir, we are interested in Microwave sensor and Occupancy Sensor Market Technology. .

Ingar

Nov, 2015

Does this report tell me volume split of occupancy sensors for each technology? Does the report also split into technologies used for occupancy sensing vs application?.

Michael

Oct, 2016

I am interested to purchase only the market share for the occupancy sensors report. How much would be the cost?.