Proactive Security Market by Solution (Risk and Vulnerability Management, AMP, Security Analytics, Security Monitoring, Security Orchestration, and Attack Simulation), Service, Organization Size, Industry Vertical, and Region - Global Forecast to 2023

[174 Pages Report] The global proactive security market size was USD 16.01 billion in 2017 is projected to reach USD 41.77 billion by 2023, growing at a Compound Annual Growth Rate (CAGR) of 15.1% during the forecast period. The base year for the study is 2017 and the forecast period is 2018�2023.

The objective of the study is to define, describe, and forecast the proactive security market by solutions, services, organization size, verticals, and regions. It also analyzes recent developments, such as partnerships, strategic alliances, mergers and acquisitions, business expansions, new product developments, and research and development (R&D) in the global market.

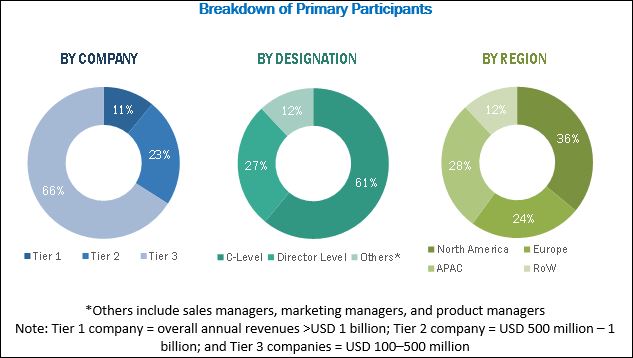

The research methodology used to estimate and forecast the proactive security market began with the collection and analysis of data on key vendors� revenues through secondary sources, such as company websites, press releases, annual reports, TechTarget reports, Cloud Security Alliance reports, SC magazine, and SANS Institute studies. Vendor offerings are taken into consideration to determine the market segmentation. The bottom-up procedure was employed to arrive at the total market size of the global market from the revenues of the key players. After arriving at the overall market size, the total market was split into several segments and subsegments, which were then verified through primary research by conducting extensive interviews with key people, such as Chief Executive Officers (CEOs), Vice Presidents (VPs), directors, and executives. The data triangulation and market breakdown procedures were employed to complete the overall proactive security market engineering process, and to arrive at the exact statistics for all the segments and subsegments. The breakdown of the profiles of the primary participants is depicted in the figure below:

To know about the assumptions considered for the study, download the pdf brochure

The proactive security market comprises key vendors, such as IBM (US), Symantec (US), McAfee (US), FireEye (US), Cisco (US), Palo Alto Networks (US), FireMon (US), LogRhythm (US), CyberSponse (US), RSA Security (US), Rapid7 (US), Demisto (US), ThreatConnect (US), Phantom (US), Securonix (US), Corvil (Ireland), Qualys (US), Siemplify (US), Skybox Security (US), Centrify (US), Oracle (US), Swimlane (US), AlienVault (US), Trustwave (US), and Aricent (US). These vendors provide proactive security solutions and services to end-users for catering to their unique business requirements, productivity, compliances, and security needs.

Key Target Audience

- Cybersecurity vendors

- Information security consultants

- Security system integrators

- Government agencies

- Managed Security Service Providers (MSSPs)

- Value-Added Resellers (VARs)

- Independent software vendors

�The study answers several questions for stakeholders, primarily which market segments to focus over the next 2�5 years for prioritizing their efforts and investments.�

Scope of the Proactive Security Market Report

|

Report Metrics |

Details |

|

Market size available for years |

2016-2023 |

|

Base year considered |

2017 |

|

Forecast period |

2018�2023 |

|

Forecast units |

Value (USD) |

|

Segments covered |

Solution, Service, Organization Size, Industry Vertical, and Region |

|

Geographies covered |

North America, Europe, Asia Pacific (APAC), Middle East and Africa (MEA), and Latin America |

|

Companies covered |

IBM (US), Symantec (US), McAfee (US), FireEye (US), Cisco (US), Palo Alto Networks (US), FireMon (US), LogRhythm (US), CyberSponse (US), RSA Security (US), Rapid7 (US), Demisto (US), ThreatConnect (US), Phantom (US), Securonix (US), Corvil (Ireland), Qualys (US), Siemplify (US), Skybox Security (US), Centrify (US), Oracle (US), Swimlane (US), AlienVault (US), Trustwave (US), and Aricent (US) |

The research report segments the proactive security market into the following submarkets:

By Component:

- Solution

- Security Analytics

- Advanced Malware Protection (AMP)

- Security Monitoring

- Attack Simulation

- Security Orchestration

- Risk and Vulnerability Management

- Services

- Professional Services

- Consulting Services

- Training and Education Services

- Support and Maintenance Services

- Design and Integration Services

- Managed Services

- Professional Services

Proactive Security Market By Organization Size:

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

By Vertical:

- Banking, Financial Services, and Insurance (BFSI)

- Government and Defense

- Retail and eCommerce

- IT and Telecom

- Healthcare and Life Sciences

- Manufacturing

- Energy and Utilities

- Others (Travel and Hospitality, Media and Entertainment, and Education)

Proactive Security Market By Region:

- North America

- Europe

- Asia Pacific (APAC)

- Middle East and Africa (MEA)

- Latin America

Available Customizations

With the given market data, MarketsandMarkets offers customizations as per the company�s specific needs. The following customization options are available for the report:

Product Analysis

- Product matrix which gives the detailed comparison of product portfolio of each company

Geographic Analysis

- Further breakdown of geographies into respective countries

Company Information

- Detailed analysis and profiling of additional proactive security market players

MarketsandMarkets forecasts the global proactive security market size to grow from USD 20.66 billion in 2018 to USD 41.77 billion by 2023, at a Compound Annual Growth Rate (CAGR) of 15.1% during the forecast period. Increasing sophistication of cyberattacks, along with the rising need to meet compliance requirements, are expected to drive the adoption of proactive security solutions for the protection of their sensitive information. Moreover, the SMEs segment is gaining a high traction in the market, as SMEs are more vulnerable to internal and external data breaches. With the adoption of proactive security solutions, organizations can effectively maintain and secure their critical information from data breaches. Proactive security solutions help organizations optimize their security infrastructure, easily manage security vulnerabilities, and control all their security products from a single platform.

Proactive security solutions include various solutions for prevention, such as security analytics, AMP, security monitoring, attack simulation, security orchestration, and risk and vulnerability management. The risk and vulnerability management solution is expected to dominate the proactive security market and is estimated to have the largest market size in 2018. The security analytics solution would play a key role in changing the market landscape and is expected to grow at the highest CAGR during the forecast period, as global organizations are highly proactive in improving their IT security and protecting sensitive information from data breaches and malware attacks.

The BFSI is the fastest-growing vertical in the proactive security market, as BFSI companies have stringent legal and regulatory compliances associated with information security. Small and Medium-sized Enterprises (SMEs) continue to deploy proactive security solutions, as SMEs are increasingly facing malware-based and DNS-based cyber-attacks.

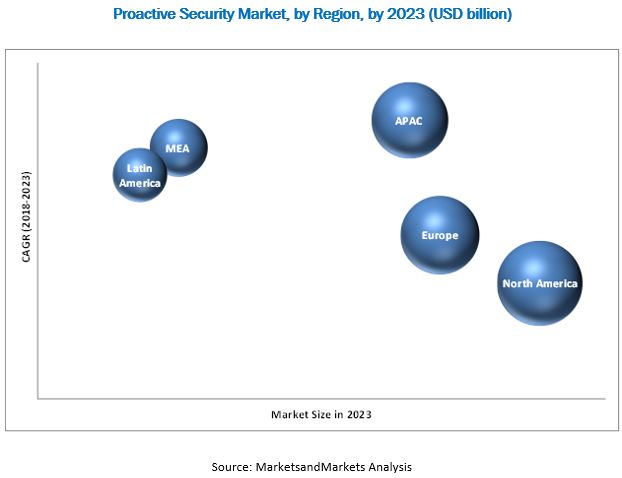

North America is estimated to hold the largest market size in 2018. The increasing need for organizations to protect their data from advanced cyber-attacks and addressing the stringent government regulations are expected to drive the proactive security market. Furthermore, rapid economic growth in the major countries, along with regulatory reforms and economic stability, is expected to drive the market in Asia Pacific (APAC). In Middle East and Africa (MEA), enterprises belonging to a range of verticals, such as BFSI, government, education, and manufacturing, are expected to increase their investments in proactive security solutions and services.

Security vendors are offering proactive security solutions via security analytics, AMP, security monitoring, attack simulation, security orchestration, and risk and vulnerability management. As the frequency of security breaches has increased over the past 5 years, organizations have increased their IT security investments to protect against advanced threats. However, for many enterprises, including SMEs, these investment costs are a matter of concern. Furthermore, for a strong and advanced security, the cost of innovation is still high, and thus many organizations view budgetary constraints as a barrier to the adoption of proactive security solutions and services.

The increasing adoption of cloud-based solutions and services among enterprises would provide significant growth opportunities to proactive security solution vendors. There are several established players, such as IBM (US), Symantec (US), McAfee (US), FireEye (US), Cisco (US), Palo Alto Networks (US), FireMon (US), LogRhythm (US), CyberSponse (US), RSA Security (US), Rapid7 (US), Demisto (US), ThreatConnect (US), Phantom (US), Securonix (US), Corvil (Ireland), Qualys (US), Siemplify (US), Skybox Security (US), Centrify (US), Oracle (US), Swimlane (US), AlienVault (US), Trustwave (US), and Aricent (US).

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 16)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Market Scope

1.4 Years Considered for the Study

1.5 Currency

1.6 Stakeholders

2 Research Methodology (Page No. - 19)

2.1 Research Data

2.1.1 Secondary Data

2.1.2 Primary Data

2.1.2.1 Breakdown of Primary Interviews

2.1.2.2 Key Industry Insights

2.2 Market Size Estimation

2.3 Research Assumptions

2.3.1 Assumptions

2.4 Limitations

3 Executive Summary (Page No. - 29)

4 Premium Insights (Page No. - 33)

4.1 Attractive Market Opportunities in the Proactive Security Market

4.2 Market By Component, 2018�2023

4.3 Market By Service, 2018�2023

4.4 Market Top 4 Industry Verticals and Regions

5 Proactive Security Market Overview (Page No. - 36)

5.1 Introduction

5.2 Market Dynamics

5.2.1 Drivers

5.2.1.1 Strategic Shift Toward Proactive Security Due to Increasing Sophistication in Attacking Techniques

5.2.1.2 Rising Need to Manage Stringent Regulations and Compliances

5.2.1.3 Rising Adoption of Iot, Smart Mobile Devices, and Byod Trends

5.2.2 Restraints

5.2.2.1 Budgetary Constraints to Deploy Proactive Cybersecurity Solutions

5.2.3 Opportunities

5.2.3.1 Proliferation of Cloud-Based Services Across Global Organizations

5.2.3.2 Rapidly Increasing Digital Transformation of Organizations in Major Economies

5.2.4 Challenges

5.2.4.1 Limited Skilled Cybersecurity Professionals

5.3 Standards and Regulations

5.3.1 General Data Protection Regulation (GDPR)

5.3.2 Health Insurance Portability and Accountability Act (HIPAA)

5.3.3 Federal Information Security Management Act (FISMA)

5.3.4 Sarbanes�Oxley Act (SOX)

5.3.5 Gramm�Leach�Bliley Act (GLBA)

5.3.6 Payment Card Industry Data Security Standard (PCI DSS)

5.3.7 Federal Information Processing Standard (FIPS)

5.4 Cyber Threat Landscape

5.4.1 Cyber-Attack Motives

5.4.2 Attacks Witnessed By Small and Medium-Sized Enterprises and Emergence of Insider Attacks

5.4.3 Key Targets of Cyber-Attackers During Data Breach

6 Proactive Security Market By Component (Page No. - 47)

6.1 Introduction

6.2 Solutions

6.2.1 Risk and Vulnerability Management

6.2.2 Advanced Malware Protection

6.2.3 Security Analytics

6.2.4 Security Monitoring

6.2.5 Security Orchestration

6.2.6 Attack Simulation

6.3 Services

6.3.1 Professional Services

6.3.1.1 Training and Education Services

6.3.1.2 Support and Maintenance Services

6.3.1.3 Consulting Services

6.3.1.4 Design and Integration Services

6.3.2 Managed Services

7 Proactive Security Market By Organization Size (Page No. - 63)

7.1 Introduction

7.2 Large Enterprises

7.3 Small and Medium-Sized Enterprises

8 Proactive Security Market By Industry Vertical (Page No. - 67)

8.1 Introduction

8.2 Banking, Financial Services, and Insurance

8.3 Government and Defense

8.4 Retail and Ecommerce

8.5 IT and Telecom

8.6 Healthcare and Life Sciences

8.7 Energy and Utilities

8.8 Manufacturing

8.9 Others

9 Proactive Security Market, By Region (Page No. - 80)

9.1 Introduction

9.2 North America

9.2.1 United States

9.2.2 Canada

9.3 Europe

9.3.1 United Kingdom

9.3.2 Germany

9.3.3 France

9.3.4 Rest of Europe

9.4 Asia Pacific

9.4.1 China

9.4.2 India

9.4.3 Australia

9.4.4 Japan

9.4.5 Rest of Asia Pacific

9.5 Middle East and Africa

9.5.1 Middle East

9.5.2 Africa

9.6 Latin America

9.6.1 Mexico

9.6.2 Brazil

9.6.3 Rest of Latin America

10 Competitive Landscape (Page No. - 109)

10.1 Overview

10.2 Competitive Scenario

10.2.1 Partnerships, Agreements, and Collaborations

10.2.2 New Product Launches/Product Enhancements

10.2.3 Mergers and Acquisitions

10.2.4 Business Expansions

11 Company Profiles (Page No. - 114)

(Business Overview, Products Offered, Recent Developments, SWOT Analysis, MnM View)*

11.1 IBM

11.2 Cisco

11.3 Symantec

11.4 Fireeye

11.5 Mcafee

11.6 Palo Alto Networks

11.7 Securonix

11.8 Logrhythm

11.9 Rapid7

11.10 Qualys

11.11 Alienvault

11.12 Trustwave

11.13 Cybersponse

11.14 Firemon

11.15 RSA Security

11.16 Demisto

11.17 Threatconnect

11.18 Centrify

11.19 Oracle

11.20 Swimlane

11.21 Aricent

11.22 Phantom

11.23 Skybox Security

11.24 Corvil

11.25 Siemplify

*Business Overview, Products Offered, Recent Developments, SWOT Analysis, MnM View Might Not Be Captured in Case of Unlisted Companies.

12 Appendix (Page No. - 167)

12.1 Discussion Guide

12.2 Knowledge Store: Marketsandmarkets� Subscription Portal

12.3 Introducing RT: Real-Time Market Intelligence

12.4 Available Customizations

12.5 Related Reports

12.6 Author Details

List of Tables (71 Tables)

Table 1 Proactive Security Market Size and Growth Rate, 2016�2023 (USD Million, Y-O-Y %)

Table 2 Market Size By Component, 2016�2023 (USD Million)

Table 3 Solutions: Market Size By Type, 2016�2023 (USD Million)

Table 4 Solutions: Market Size By Region, 2016�2023 (USD Million)

Table 5 Risk and Vulnerability Management Market Size, By Region, 2016�2023 (USD Million)

Table 6 Advanced Malware Protection Market Size, By Region, 2016�2023 (USD Million)

Table 7 Security Analytics Market Size, By Region, 2016�2023 (USD Million)

Table 8 Security Monitoring Market Size, By Region, 2016�2023 (USD Million)

Table 9 Security Orchestration Market Size, By Region, 2016�2023 (USD Million)

Table 10 Attack Simulation Market Size, By Region, 2016�2023 (USD Million)

Table 11 Services: Proactive Security Market Size By Type, 2016�2023 (USD Million)

Table 12 Services: Market Size By Region, 2016�2023 (USD Million)

Table 13 Professional Services Market Size, By Type, 2016�2023 (USD Million)

Table 14 Professional Services Market Size, By Region, 2016�2023 (USD Million)

Table 15 Training and Education Services Market Size, By Region, 2016�2023 (USD Million)

Table 16 Support and Maintenance Services Market Size, By Region, 2016�2023 (USD Million)

Table 17 Consulting Services Market Size, By Region, 2016�2023 (USD Million)

Table 18 Design and Integration Services Market Size, By Region, 2016�2023 (USD Million)

Table 19 Managed Services Market Size, By Region, 2016�2023 (USD Million)

Table 20 Proactive Security Market Size, By Organization Size, 2016�2023 (USD Million)

Table 21 Large Enterprises: Market Size By Region, 2016�2023 (USD Million)

Table 22 Small and Medium-Sized Enterprises: Market Size By Region, 2016�2023 (USD Million)

Table 23 Proactive Security Market Size, By Industry Vertical, 2016�2023 (USD Million)

Table 24 Banking, Financial Services, and Insurance: Market Size By Region, 2016�2023 (USD Million)

Table 25 Government and Defense: Market Size By Region, 2016�2023 (USD Million)

Table 26 Retail and Ecommerce: Market Size By Region, 2016�2023 (USD Million)

Table 27 IT and Telecom: Market Size By Region, 2016�2023 (USD Million)

Table 28 Healthcare and Life Sciences: Market Size By Region, 2016�2023 (USD Million)

Table 29 Energy and Utilities: Market Size By Region, 2016�2023 (USD Million)

Table 30 Manufacturing: Market Size By Region, 2016�2023 (USD Million)

Table 31 Others: Market Size By Region, 2016�2023 (USD Million)

Table 32 Proactive Security Market Size, By Region, 2016�2023 (USD Million)

Table 33 North America: Market Size By Country, 2016�2023 (USD Million)

Table 34 North America: Market Size By Component, 2016�2023 (USD Million)

Table 35 North America: Market Size By Solution, 2016�2023 (USD Million)

Table 36 North America: Market Size By Service, 2016�2023 (USD Million)

Table 37 North America: Market Size By Professional Service, 2016�2023 (USD Million)

Table 38 North America: Market Size By Organization Size, 2016�2023 (USD Million)

Table 39 North America: Market Size By Industry Vertical, 2016�2023 (USD Million)

Table 40 Europe: Proactive Security Market Size, By Country, 2016�2023 (USD Million)

Table 41 Europe: Market Size By Component, 2016�2023 (USD Million)

Table 42 Europe: Market Size By Solution, 2016�2023 (USD Million)

Table 43 Europe: Market Size By Service, 2016�2023 (USD Million)

Table 44 Europe: Market Size By Professional Service, 2016�2023 (USD Million)

Table 45 Europe: Market Size By Organization Size, 2016�2023 (USD Million)

Table 46 Europe: Market Size By Industry Vertical, 2016�2023 (USD Million)

Table 47 Asia Pacific: Proactive Security Market Size, By Country, 2016�2023 (USD Million)

Table 48 Asia Pacific: Market Size By Component, 2016�2023 (USD Million)

Table 49 Asia Pacific: Market Size By Solution, 2016�2023 (USD Million)

Table 50 Asia Pacific: Market Size By Service, 2016�2023 (USD Million)

Table 51 Asia Pacific: Market Size By Professional Service, 2016�2023 (USD Million)

Table 52 Asia Pacific: Market Size By Organization Size, 2016�2023 (USD Million)

Table 53 Asia Pacific: Market Size By Industry Vertical, 2016�2023 (USD Million)

Table 54 Middle East and Africa: Proactive Security Market Size, By Subregion, 2016�2023 (USD Million)

Table 55 Middle East and Africa: Market Size By Component, 2016�2023 (USD Million)

Table 56 Middle East and Africa: Market Size By Solution, 2016�2023 (USD Million)

Table 57 Middle East and Africa: Market Size By Service, 2016�2023 (USD Million)

Table 58 Middle East and Africa: Market Size By Professional Service, 2016�2023 (USD Million)

Table 59 Middle East and Africa: Market Size By Organization Size, 2016�2023 (USD Million)

Table 60 Middle East and Africa: Market Size By Industry Vertical, 2016�2023 (USD Million)

Table 61 Latin America: Proactive Security Market Size, By Country, 2016�2023 (USD Million)

Table 62 Latin America: Market Size By Component, 2016�2023 (USD Million)

Table 63 Latin America: Market Size By Solution, 2016�2023 (USD Million)

Table 64 Latin America: Market Size By Service, 2016�2023 (USD Million)

Table 65 Latin America: Market Size By Professional Service, 2016�2023 (USD Million)

Table 66 Latin America: Market Size By Organization Size, 2016�2023 (USD Million)

Table 67 Latin America: Market Size By Industry Vertical, 2016�2023 (USD Million)

Table 68 Partnerships, Agreements, and Collaborations, 2017�2018

Table 69 New Product Launches/Product Enhancements, 2017�2018

Table 70 Mergers and Acquisitions, 2016�2018

Table 71 Business Expansions, 2016�2017

List of Figures (44 Figures)

Figure 1 Global Proactive Security Market Segmentation

Figure 2 Market Research Design

Figure 3 Breakdown of Primary Interviews: By Company, Designation, and Region

Figure 4 Data Triangulation

Figure 5 Market Size Estimation Methodology: Bottom-Up Approach

Figure 6 Market Size Estimation Methodology: Top-Down Approach

Figure 7 Government and Defense Industry Vertical is Estimated to Contribute the Largest Market Share in the Proactive Security Market in 2018

Figure 8 North America is Estimated to Hold the Largest Market Share in 2018

Figure 9 Exponential Growth in the Volume of Enterprise Data and the High Demand for Proactive Security Solutions are Expected to Drive the Growth of Security Vendors in the Upcoming Years

Figure 10 Services Segment is Expected to Grow at A Higher CAGR During the Forecast Period

Figure 11 Professional Services Segment is Expected to Register A Higher CAGR During the Forecast Period

Figure 12 Government and Defense Industry Vertical, and North America are Expected to Hold the Largest Market Shares in 2018

Figure 13 Proactive Security Market: Drivers, Restraints, Opportunities, and Challenges

Figure 14 IT Security Guidelines Or Standards Organizations Comply With

Figure 15 Growth of Fileless and File-Based Attacks

Figure 16 Challenges Keeping IT Security Posture From Being Fully Effective

Figure 17 Major Reasons Behind Cyber-Attacks

Figure 18 Major Attacks Witnessed By Small and Medium-Sized Enterprises

Figure 19 Key Targets of Cyber-Attackers During Data Breach

Figure 20 Services Segment to Grow at A Higher CAGR During the Forecast Period

Figure 21 Small and Medium-Sized Enterprises Segment is Expected to Register A Higher CAGR During the Forecast Period

Figure 22 Industry Verticals Witnessing Security Incidents and Attacks

Figure 23 Average Annualized Cost of Cybercrime By Industry Vertical

Figure 24 Banking, Financial Services, and Insurance Industry Vertical is Expected to Grow at the Highest CAGR During the Forecast Period

Figure 25 Proactive Security Market: Top Malware By Region

Figure 26 Global Average Cost of Cybercrime (2013�2017)

Figure 27 North America is Expected to Account for the Largest Market Size During the Forecast Period

Figure 28 North America: Market Snapshot

Figure 29 Asia Pacific: Market Snapshot

Figure 30 Key Developments By the Leading Players in the Proactive Security Market for 2016�2018

Figure 31 Key Market Evaluation Framework

Figure 32 IBM: Company Snapshot

Figure 33 IBM: SWOT Analysis

Figure 34 Cisco: Company Snapshot

Figure 35 Cisco: SWOT Analysis

Figure 36 Symantec: Company Snapshot

Figure 37 Symantec: SWOT Analysis

Figure 38 Fireeye: Company Snapshot

Figure 39 Fireeye: SWOT Analysis

Figure 40 Mcafee: SWOT Analysis

Figure 41 Palo Alto Networks: Company Snapshot

Figure 42 Rapid7: Company Snapshot

Figure 43 Qualys: Company Snapshot

Figure 44 Oracle: Company Snapshot

Growth opportunities and latent adjacency in Proactive Security Market