Aerospace Materials Market

Download PDF

Download PDF Request Customisation

Request CustomisationAerospace Materials Market by Type (Aluminum Alloys, Steel Alloys, Titanium Alloys, Super Alloys, Composite Materials), Aircraft Type (Commercial Aircraft, Business & General Aviation, Helicopters), and Region - Global Forecast to 2030

OVERVIEW

Source: Secondary Research, Interview with Experts, MarketsandMarkets Analysis

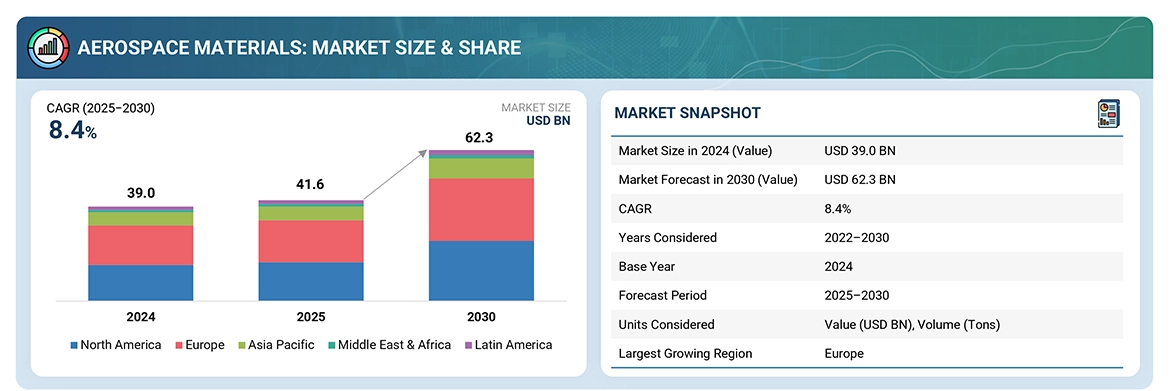

The aerospace materials market is projected to reach USD 62.3 billion by 2030 from USD 41.6 billion in 2025, at a CAGR of 8.4% from 2025 to 2030. The growth of the aerospace materials market is driven by the rising demand for advanced materials that deliver superior performance, efficiency, and sustainability in modern aircraft.

KEY TAKEAWAYS

-

BY TYPEThe aerospace materials market comprises aluminum alloys, steel alloys, titanium alloys, super alloys, and composite materials.

-

BY AIRCRAFT TYPEKey aircraft types include commercial aircraft, business and general aviation aircraft, civil helicopters, military aircraft, and others (UAVs and spacecraft).

-

BY APPLICATIONKey applications of aerospace materials span the interior and exterior segments.

-

BY REGIONThe aerospace materials market covers Europe, North America, Asia Pacific, South America, the Middle East, and Africa. Europe is the largest market for aerospace materials and is home to several prominent aerospace companies. It is also witnessing new aircraft projects that are contributing to the increasing adoption of aerospace materials products.

-

COMPETITIVE LANDSCAPEMajor market players have adopted both organic and inorganic strategies, including partnerships and investments. For instance, Syensqo (Belgium), Toray Industries, Inc. (Japan), and Mitsubishi Chemical Group Corporation (Japan)have entered into a number of agreements and partnerships to cater to the growing demand for aerospace materials across innovative applications.

The aerospace materials market is witnessing steady growth, driven by the rising demand for lightweight, high-performance materials such as aluminum alloys, titanium, and advanced composites to enhance fuel efficiency, reduce emissions, and meet stringent safety standards. New deals and developments, including strategic partnerships between OEMs and material suppliers, investments in recycling technologies, and innovations in high-strength alloys and sustainable composites, are reshaping the industry landscape.

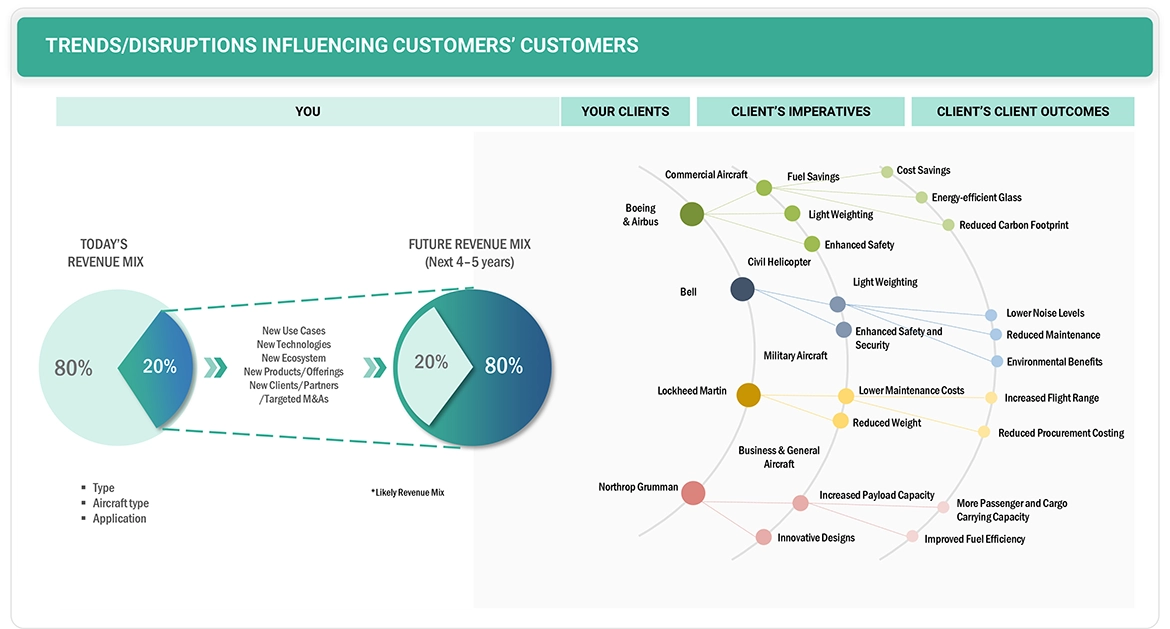

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMER'S BUSINESS

The impact on consumers' business emerges from customer trends or disruptions. Hotbets are clients of aerospace materials manufacturers, and target applications are clients of aerospace materials manufacturers. Shifts, which are changing trends or disruptions, will impact the revenues of end users. The revenue impact on end users will affect the revenue of hotbets, which will further affect the revenues of aerospace materials manufacturers.

Source: Secondary Research, Interview with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Level

-

Increasing demand for lightweight and fuel-efficient aircraft.

-

Rising adoption of composite materials for enhanced performance and durability.

Level

-

High cost of advanced aerospace materials such as composites and titanium.

-

Stringent regulations and certification requirements for material approval.

Level

-

Expanding aircraft fleet to meet rising passenger traffic.

-

Growing investments in next-generation aircraft and space exploration programs.

Level

-

Volatility in raw material prices.

-

Supply chain disruptions affecting material availability and costs.

Source: Secondary Research, Interview with Experts, MarketsandMarkets Analysis

Driver: Increasing demand for lightweight and fuel-efficient aircraft.

The aerospace industry is under constant pressure to reduce emissions and operating costs. Lightweight materials such as advanced composites, titanium alloys, and aluminum-lithium alloys enable significant weight savings, leading to improved fuel efficiency and lower maintenance costs. Airlines and OEMs are increasingly prioritizing these materials in both commercial and military aircraft to meet stringent environmental regulations and enhance performance.

Restraint: High cost of advanced aerospace materials.

Despite their advantages, aerospace-grade composites, titanium alloys, and ceramic matrix composites come with high production and processing costs. These costs are further escalated by complex manufacturing requirements, limited suppliers, and lengthy certification processes. As a result, widespread adoption is restricted, particularly among regional aircraft manufacturers and low-budget airlines, creating a barrier to mass market penetration.

Opportunity: Expanding aircraft fleet to meet rising air passenger traffic.

Global air passenger traffic continues to surge, especially in emerging economies such as India, China, and Southeast Asia, prompting record aircraft orders from Boeing, Airbus, and other OEMs. This expansion fuels demand for advanced aerospace materials that can support next-generation aircraft design, improve durability, and reduce lifecycle costs. Moreover, rising investments in space exploration, UAVs, and sustainable aviation open new avenues for aerospace material applications.

Challenge: Volatility in raw material prices and supply chain disruptions.

The aerospace sector is highly vulnerable to fluctuations in raw material prices, particularly titanium, carbon fiber, and specialty alloys. Global trade tensions and geopolitical risks have exposed weaknesses in supply chains, leading to delays and cost overruns. Ensuring a stable supply of high-quality materials while managing cost pressures remains a critical challenge for OEMs and suppliers alike.

Aerospace Materials Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | BENEFITS USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Use of advanced carbon fiber composites in 787 Dreamliner fuselage and wings. | 20% weight reduction compared to traditional aluminum, improved fuel efficiency, and reduced maintenance cost. |

|

Titanium alloys in A350 aircraft structures and landing gears. | High strength-to-weight ratio, superior corrosion resistance, extended service life. |

|

Ceramic matrix composites (CMCs) in jet engine components. | Withstands higher operating temperatures, improves engine efficiency by 10–15%, reduces fuel burn. |

|

Advanced aluminum-lithium alloys in military aircraft structures. | Enhanced durability, lower structural weight, and improved payload capacity. |

|

Composite materials in unmanned aerial vehicles (UAVs). | Lightweight design, higher endurance, and improved stealth capabilities. |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The aerospace materials market ecosystem consists of raw material suppliers (Toray, Teijin), part manufacturers (3M, Lee Aerospace), and end users (Boeing, Airbus). Raw materials like composites and metal alloys are processed into lightweight, high-performance components for use in aircraft. End users drive demand for fuel efficiency and sustainability, while manufacturers deliver precision-engineered parts. Collaboration across the value chain is key to innovation and market growth.

Source: Secondary Research, Interview with Experts, MarketsandMarkets Analysis

MARKET SEGMENTS

Source: Secondary Research, Interview with Experts, MarketsandMarkets Analysis

Aerospace Materials Market, By Type

As of 2024, aluminum alloys held the largest share of the aerospace materials market and will continue leading the market through 2025 due to their light weight, high strength-to-weight ratio, corrosion resistance, and cost-effectiveness. Widely used in fuselage skins, wings, and bulkheads of aircraft like the Airbus A320 and Boeing 737, aluminum alloys offer proven performance, repairability, and a strong supply chain. Advancements in Al-Li alloys further enhance fatigue resistance and reduce weight, reinforcing the role of aluminum alongside composites in next-generation aircraft.

Aerospace Materials Market, By Aircraft Type

In 2024, commercial aircraft dominated the aerospace materials market, driven by demand for lightweight, fuel-efficient, and sustainable jets like the Airbus A350 and Boeing 737 MAX, which heavily rely on composites. Aluminum alloys remain key for cost-effective structural applications, while titanium alloys support engines, landing gear, and joints due to their high strength and heat resistance. Additionally, steel alloys and nickel-based superalloys are essential in load-bearing parts and turbine blades, ensuring durability and performance.

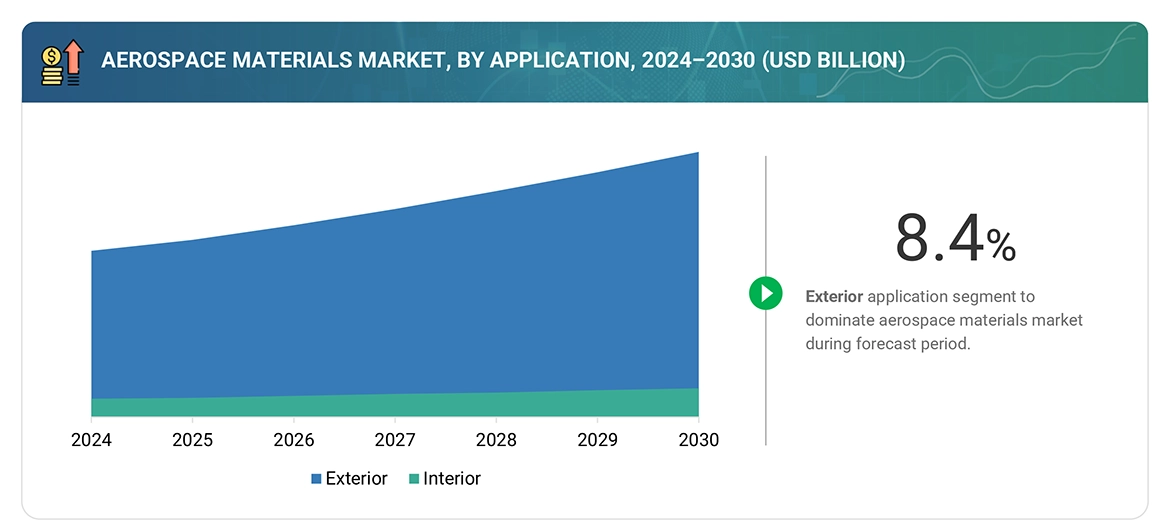

Aerospace Materials Market, By Application

The exterior segment is expected to dominate the aerospace materials market, as aircraft structures require lightweight yet durable materials to ensure strength, aerodynamics, and fuel efficiency under extreme conditions. Advanced composites like CFRPs, used extensively in the Airbus A350 and Boeing 787, deliver up to 20% fuel savings while enhancing durability. Aluminum alloys such as 7075 and Al-Li remain critical for fuselage skins and wing ribs due to their toughness, repairability, and cost-effectiveness in large-scale production.

REGION

North America to be fastest-growing region in global aerospace materials market during forecast period

The North American aerospace materials market is expected to register the highest CAGR during the forecast period, driven by strong demand for next-generation commercial aircraft, defense modernization programs, and increasing investments in space exploration. Leading OEMs and suppliers in the US and Canada are adopting advanced composites, titanium, and aluminum-lithium alloys to enhance fuel efficiency, reduce emissions, and improve aircraft performance. Rising air passenger traffic and R&D initiatives in sustainable aviation and electric aircraft are further accelerating the adoption of aerospace materials in the region.

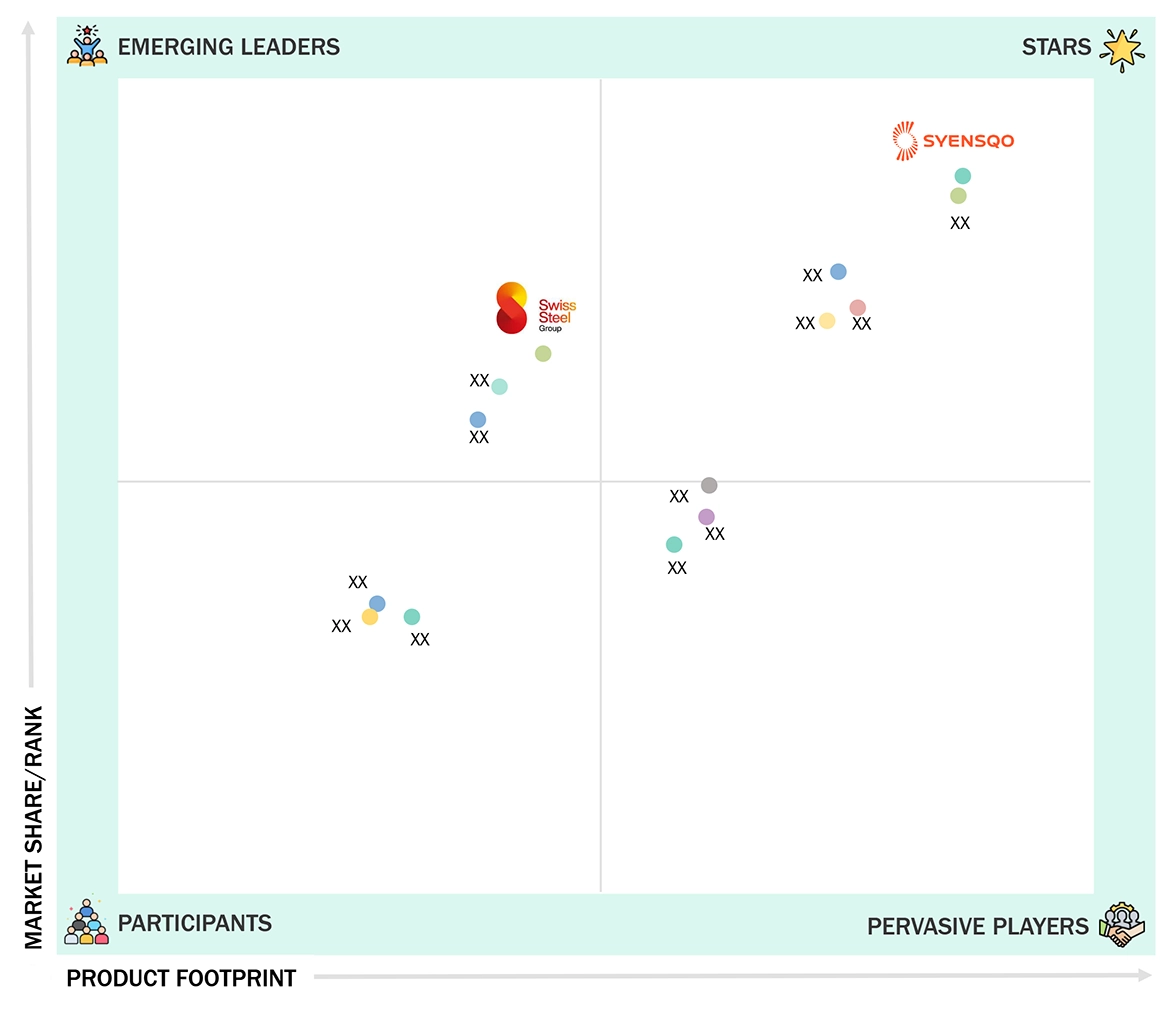

Aerospace Materials Market: COMPANY EVALUATION MATRIX

In the aerospace materials market matrix, Syensqo (Star) leads with a strong market share and extensive product footprint, driven by its advanced composites and high-performance materials widely adopted in commercial and Defense aviation. Swiss Steel Group (Emerging Leader) is gaining visibility with its specialized alloys and tailored solutions for aerospace applications, strengthening its position through innovation and niche product offerings. While Syensqo dominates through scale and a diverse portfolio, Swiss Steel Group shows significant potential to move toward the leaders’ quadrant as demand for high-strength alloys continues to rise.

Source: Secondary Research, Interview with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2024 (Value) | USD 39.0 Billion |

| Market Forecast in 2030 (value) | USD 62.3 Billion |

| Growth Rate | CAGR of 8.4% from 2025-2030 |

| Years Considered | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Kiloton) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends. |

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, South America, Middle East & Africa |

WHAT IS IN IT FOR YOU: Aerospace Materials Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the deep dive customization for players like you-

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Leading Aircraft OEM |

|

|

| Composite Material Manufacturer |

|

|

| Engine Manufacturer |

|

|

| Raw Material Supplier |

|

|

| Defense Contractor |

|

|

RECENT DEVELOPMENTS

- May 2025 : Syensqo demonstrated the replacement of titanium with CYCOM 5250-4HT prepreg in Boeing’s MQ-25 Stingray UAV exhaust nozzle, showcasing high-temperature composite innovation.

- March 2024 : Hexcel Corporation and Arkema entered into a strategic partnership to develop high-performance thermoplastic composite structures. These structures were successfully designed and manufactured using HexPly thermoplastic tapes within the HAICoPAS (Highly Automatized Integrated Composites for Performing Adaptable Structures) collaborative project, which was led by Hexcel and Arkema.

- January 2024 : Materion Beryllium & Composites (subsidiary of Materion Corporation) partnered with Liquidmetal Technologies Inc. and other Certified Liquidmetal Partners to use their alloy production technologies to provide high-quality products and support services to their customers.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Methodology

The study to estimate the current size of the aerospace materials market involved two key steps. First, comprehensive secondary research was conducted to gather data on the market itself, as well as related and parent markets. This was followed by primary research, where insights, assumptions, and market estimates were validated through interviews with industry experts across the value chain. Both top-down and bottom-up methodologies were applied to determine the overall market size. Finally, the market was segmented, and data triangulation techniques were used to refine and validate the estimates for each segment and subsegment.

Secondary Research

Secondary sources consulted for this research included financial reports of aerospace materials manufacturers, along with data from trade organizations, business publications, and professional associations. This secondary research provided essential insights into the industry's value chain, identified key players, and helped classify and segment the market based on prevailing industry trends down to the regional and sub-regional levels. The information gathered was thoroughly analyzed to estimate the overall size of the aerospace materials market, which was then validated through primary research with industry experts.

Primary Research

Extensive primary research was carried out following the collection of market insights through secondary research to validate the aerospace materials market scenario. Numerous interviews were conducted with industry experts from both the demand and supply sides across key regions, including North America, Europe, Asia Pacific, the Middle East & Africa, and South America. Primary data was gathered through structured questionnaires, emails, and telephonic interviews. On the supply side, respondents included industry professionals such as CXOs, Vice Presidents, Directors of business development, marketing, product innovation teams, system integrators, component suppliers, distributors, and key opinion leaders in the aerospace materials space. These interviews provided valuable insights into market statistics, revenue data, segmentation, size estimations, forecasts, and enabled data triangulation. On the demand side, stakeholders such as CIOs, CTOs, CSOs, and installation teams from end-user organizations were consulted to gain a better understanding of customer perspectives, current usage patterns, supplier evaluations, and the future outlook for aerospace materials, all of which influence the overall market dynamics.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

The research methodology used to estimate the size of the aerospace materials market primarily focused on a demand-side approach. Market sizing was conducted by analyzing procurement activities and modernization efforts involving aerospace composite products across various applications at the regional level. These procurement trends offered valuable insights into the demand patterns within the aerospace materials industry for each application segment. All relevant segments were thoroughly mapped and integrated to provide a comprehensive view of the market structure and size across different end-use applications.

Data Triangulation

After estimating the overall market size through the process described above, the total market was further segmented into various segments and subsegments. To ensure accuracy, data triangulation and market breakdown techniques were applied wherever relevant, forming a key part of the overall market engineering process. This involved analyzing multiple factors and trends from both the demand and supply sides. Additionally, the final market size and segment-level figures were validated using a combination of top-down and bottom-up approaches to ensure precision and reliability of the statistical estimates.

Market Definition

Aerospace materials are specialized materials engineered to deliver high performance under the extreme operating conditions of aircraft and spacecraft, characterized by their lightweight properties, high strength-to-weight ratio, and resistance to fatigue, creep, and corrosion. These include composites, which combine carbon, glass, or aramid fibers in a resin matrix to provide lightweight strength for fuselage, wings, and interiors; titanium alloys, valued for their high strength, corrosion resistance, and temperature endurance; aluminum alloys, widely used for their light weight, corrosion resistance, and machinability in fuselage and wing structures; steel alloys, offering exceptional strength and durability for landing gear, fasteners, and load-bearing components; and super alloys (nickel-, cobalt-, and iron-based), critical in jet engines and turbines for their ability to withstand extreme heat. Other advanced materials include GLARE (Glass Laminate Aluminum Reinforced Epoxy), which combines aluminum and glass fibers to offer fatigue resistance and damage tolerance, ceramics for thermal protection systems, and magnesium alloys for lightweight structural and interior applications. Collectively, these materials enable the aerospace industry to achieve greater efficiency, durability, safety, and innovation in modern aircraft and space vehicles.

Stakeholders

- Aerospace materials manufacturers

- Aircraft manufacturers

- Universities, governments, and research organizations

- Aerospace composites and composite associations and industrial bodies

- Research and consulting firms

- R&D institutions

- Environmental support agencies

- Investment banks and private equity firms

Report Objectives

- To define, describe, and forecast the aerospace materials market size in terms of volume and value

- To provide detailed information regarding the key factors, such as drivers, restraints, opportunities, and challenges influencing market growth

- To analyze and project the global aerospace materials market by type, aircraft type, application, and region

- To forecast the market size concerning five main regions (along with country-level data), namely, North America, Europe, Asia Pacific, South America, and the Middle East & Africa, and analyze the significant region-specific trends

- To strategically analyze micromarkets with respect to individual growth trends, prospects, and contributions of the submarkets to the overall market

- To analyze the market opportunities and the competitive landscape for stakeholders and market leaders

- To assess recent market developments and competitive strategies, such as agreements, contracts, acquisitions, and new product developments/new product launches, to draw the competitive landscape

- To strategically profile the key market players and comprehensively analyze their core competencies

Key Questions Addressed by the Report

Who are the major companies in the aerospace materials market? What strategies do they adopt?

Major companies include Syensqo (Belgium), Toray Industries (Japan), Hexcel Corporation (US), Teijin Limited (Japan), Huntsman (US), VSMPO-AVISMA (Russia), SGL Carbon (Germany), Mitsubishi Chemical Advanced Materials (Japan), DuPont (US), SABIC (Saudi Arabia), Swiss Steel Group (Switzerland), ATI (US), Alcoa (US), China Ansteel (China), Precision Castparts Corp. (US). Other notable players include Arris Composites, Victrex, Albany International, Carpenter Technology, Voestalpine Böhler Edelstahl, Outokumpu, Western Superconducting Technologies, Baoji Titanium (Baoti), Kaiser Aluminum, and Novelis. The key strategy used by these companies is partnerships and deals to strengthen market presence.

What are the drivers and opportunities for the aerospace materials market?

Rising air traffic, demand for greater fuel efficiency, and rapid technological advancements that support next-generation aircraft are the main drivers. These trends create opportunities for advanced aerospace materials that improve efficiency, performance, and sustainability.

Which region is expected to hold the largest market share?

Europe, due to its strong aerospace ecosystem, presence of leading manufacturers, and new aircraft development programs.

What is the projected CAGR of the aerospace materials market during 2025–2030?

The market is expected to grow at a CAGR of 7.7% (value-based) from 2025 to 2030.

How is the aerospace materials market structured in terms of technology, applications, and trends?

The market centers on advanced composites and metal alloys such as carbon-fiber composites, aluminum alloys, steel alloys, and titanium alloys. Key trends include lightweighting, fuel efficiency, and adoption of AFP/ATL (automated fiber placement / automated tape laying), digital twin technology, and robotics in aerospace manufacturing.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This ReportPersonalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Aerospace Materials Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

We at Nissan Chemicals Corporation have been clients of MarketsandMarkets for more than a year now. We recently consulted MarketsandMarkets for a study, the team at MarketsandMarkets was extremely professional and organized. The business insights were very detailed and aligned well with our expectations that really helped us formulate the Business Plans and device new strategies for development themes. MarketsandMarkets offers a unique combination of expertise and dedicated engagement model. Their research findings have helped us in designing our Pricing Strategy which will make it easier for us to predict the future sales and profits for the next ten years. We look forward to working with MarketsandMarkets in the future.

VP of Strategy & New Business Development

Leading Specialty Chemical Company

The MarketsandMarkets Engagement Model, composed of both the Knowledge Store and advisory custom research, has greatly helped us in understanding our markets and making strategic decisions. The Knowledge Store is a fast way to allow everyone in our organization to understand more about most any market they are interested in. The ability to then get custom research done and get answers to specific strategic questions and market insight has been spectacular. The Markets and Markets team feel more like colleagues than vendors and their services have helped us change our culture where statements of things like growth opportunities and competitive position are always backed by industry research.

Rich Gibson,

Director, Corporate Strategy

Milliken & Company,

Leading Industrial Manufacturer of specialty chemical, floor covering, performance and protective textile materials, and healthcaremilliken.com

MarketsandMarkets is a trusted resource that helps us to better understand markets that are near-adjacencies-whether its technology, value chain or geography. Their Knowledge Store platform provides a dashboard of markets and their characteristics which is easy to use and saves us time.

Adam Shaw,

Market Development and Strategy Manager

AdvanSix Inc. USA,

An American Leader in Chemicalswww.advansix.com

The Knowledge Store from MarketsandMarkets is a valuable tool which has helped my team acquire greater insight in to the end markets that our business serves. This has enabled us to help our company build stronger strategies throughout our planning process.

TOSHIO KINOSHITA

Senior Chif Consultion Research & Consulting Division

Mitsubishi Chemical Research Corporation,

Leading Manufacturer of Chemical Productswww.mitsubishichem-res.co.jp/en/

We recently engaged with MarketsandMarkets for a study, the team not only clearly understood our business objectives but was also extremely professional in the way they handled the entire project. The study was efficiently conducted in a phase-wise manner, and the engagement model furnished us with high-quality business insights that far exceeded our expectations at each phase. We were especially happy that MarketsandMarkets could provide us with both, an English as well as a Japanese version of the study. A special thanks to the Analyst Team and Client Services Team, whose fluency in Japanese enhanced our comfort level, as we could converse with them in our preferred language.

Independent entrepreneurs

Arrow Precision

We approached MarketsandMarkets for study on Proppants Market, and their work exceeded our expectations. The study conducted was comprehensive and enabled us to view the market through the various dimensions. In addition, the team was extraordinarily responsive throughout the process and resolved our queries on time. I strongly recommend MarketsandMarkets and will certainly consider them for additional market assessments we will need in the future.

Global engineering company, Japan

Deputy Manager,

Strategic Planning OfficeThe high-quality insights shared by the MarketsandMarkets team helped us understand the pharmaceutical plant designers in a specific geography. It also captured the risks that we may likely face in communicating with our potential partners. The study would enable us identify partners, which would impact our future growth.

Growth opportunities and latent adjacency in Aerospace Materials Market

J.H.Kim

Nov, 2018

Aerospace Materials Market insights.

Elizabeth

Aug, 2019

More insights on Foam Steel market.

Elizabeth

Aug, 2019

Foam steel market by application .

Tanguy

Nov, 2015

Incomplete query.

pascal

Nov, 2017

Information about the aluminium material in aerospace.

Fernando

Sep, 2018

General information on Aluminum Alloys Market.

Rifat

May, 2019

Information on global trends on aerospace materials along with their market estimation .

Rifat

May, 2019

Interested in aerospace materials markets with the segment parts by material used.

Kumar

Apr, 2018

Aerospace 3D Printing Market .