Hi-Fi System Market by System (Product, Device), Connectivity Technology (Wired, Wireless (Bluetooth, Wi-Fi, Airplay, Others)), Application (Residential, Automotive, Commercial, Others), and Geography - Global Forecast to 2035

Hi-Fi System Market Summary

The global Hi-Fi System Market is experiencing steady growth, driven by increasing consumer demand for high-quality audio experiences, the proliferation of smart home ecosystems, and advancements in wireless and AI-enabled sound technologies. The market was valued at approximately USD 15.8 - 17.2 billion in 2024 and is projected to reach USD 32.6 - 34.8 billion by 2035, expanding at a CAGR of 6.8 - 7.6% during the forecast period (2025–2035). The integration of artificial intelligence, Internet of Things (IoT), and automation into home entertainment systems is reshaping the traditional Hi-Fi landscape. Consumers are increasingly adopting connected audio devices that offer seamless streaming, voice control, and personalized sound optimization. Additionally, the rise of digital content platforms and high-resolution audio formats is further accelerating market growth, making Hi-Fi systems a central component of modern digital lifestyles.

Key Market Trends & Insights

The Hi-Fi System Market is being redefined by evolving consumer preferences and rapid technological innovation. North America leads the market due to high consumer spending on premium audio equipment and early adoption of smart home technologies. Asia Pacific is emerging as the fastest-growing region, fueled by rising disposable incomes and expanding middle-class populations. Wireless and smart Hi-Fi systems dominate the product segment, as consumers shift away from traditional wired setups. AI-driven sound optimization and voice assistant integration are becoming standard features, enhancing user experience and convenience. Additionally, the growing popularity of home entertainment systems, especially post-pandemic, continues to drive demand. Automation and cloud connectivity are enabling multi-room audio control and personalized listening experiences, further boosting market adoption.

Market Size & Forecast

- Base year market size (2024): USD 15.8 - 17.2 billion

- Forecast value by 2035: USD 32.6 - 34.8 billion

- CAGR (2025–2035): 6.8% - 7.6%

- Growth is driven by increasing demand for premium audio experiences, integration of AI and IoT technologies, and the rising popularity of smart home entertainment systems.

Hi-Fi System Market Top 10 key takeaway

- The market is projected to grow at a CAGR of 6.8% through 2035.

- Wireless Hi-Fi systems are replacing traditional wired systems.

- North America remains the largest market.

- Asia Pacific is the fastest-growing region.

- AI-powered sound optimization is gaining traction.

- Integration with smart home ecosystems is increasing.

- Streaming services are driving demand for high-quality audio systems.

- Premium segment demand is rising among audiophiles.

- Multi-room and connected audio systems are trending.

- Technological innovation is a key competitive factor.

Product Insights

The wireless Hi-Fi system segment dominates the market due to its convenience, flexibility, and compatibility with modern digital lifestyles. Consumers increasingly prefer clutter-free setups that offer seamless connectivity through Bluetooth, Wi-Fi, and streaming platforms. These systems are particularly popular in urban households where space optimization and aesthetic appeal are important considerations.

Traditional component-based Hi-Fi systems, including amplifiers, speakers, and receivers, continue to hold relevance among audiophiles who prioritize sound quality and customization. However, emerging product categories such as smart speakers with Hi-Fi capabilities and integrated soundbars are rapidly gaining popularity. These advanced systems often include AI-based sound calibration, which adjusts audio output based on room acoustics and user preferences. The integration of voice assistants and mobile app controls further enhances user experience, making modern Hi-Fi systems more interactive and intelligent.

Technology / Component Insights

Technological advancements are at the core of the Hi-Fi System Market’s evolution. Wireless connectivity technologies such as Bluetooth Low Energy (BLE) and Wi-Fi streaming protocols are enabling seamless audio transmission across devices. IoT integration allows Hi-Fi systems to connect with other smart home devices, creating a unified entertainment ecosystem.

Artificial intelligence is playing a transformative role by enabling features such as adaptive sound tuning, voice recognition, and personalized playlists. AI algorithms analyze user behavior and environmental factors to deliver optimized audio experiences. Cloud-based platforms are also gaining importance, allowing users to access music libraries and streaming services effortlessly.

Automation is enhancing usability by enabling scheduled playback, multi-room synchronization, and remote system management. Looking ahead, advancements in spatial audio, immersive sound technologies, and integration with augmented and virtual reality platforms are expected to redefine the listening experience.

Application Insights

The residential segment dominates the Hi-Fi System Market, driven by increasing consumer investment in home entertainment systems. The growing popularity of streaming services, gaming, and home theaters has significantly boosted demand for high-quality audio solutions in households.

Commercial applications, including hospitality, retail, and event management, are also contributing to market growth. Businesses are leveraging Hi-Fi systems to enhance customer experiences through immersive audio environments. Additionally, the automotive sector is emerging as a promising application area, with premium in-car audio systems becoming a key differentiator for vehicle manufacturers.

Future opportunities lie in the integration of Hi-Fi systems with smart city infrastructure and public entertainment venues, as well as the expansion of high-resolution audio content.

Regional Insights

North America leads the Hi-Fi System Market due to high consumer awareness, strong purchasing power, and widespread adoption of advanced audio technologies. The presence of leading market players and a well-established distribution network further supports regional dominance. Europe follows closely, with strong demand for premium audio systems and a growing focus on sustainable and energy-efficient products.

Asia Pacific is the fastest-growing region, driven by rapid urbanization, increasing disposable incomes, and expanding consumer electronics markets in countries such as China, India, and Japan. The region is witnessing a surge in demand for smart and affordable Hi-Fi systems, supported by growing digitalization and e-commerce penetration.

- North America dominates due to high adoption of premium audio systems

- Europe shows strong demand for high-quality and sustainable products

- Asia Pacific is the fastest-growing region

- Rising disposable incomes drive growth in emerging markets

- Digitalization and e-commerce boost product accessibility

Country-Specific Market Trends

In Asia Pacific, China leads the market with a CAGR of approximately 8.2%, driven by strong manufacturing capabilities and growing consumer demand for smart electronics. Japan follows with steady growth, supported by technological innovation and a strong culture of high-fidelity audio appreciation.

In North America, the United States remains the largest market, with widespread adoption of smart home technologies and premium audio systems. Canada and Mexico are also experiencing growth due to increasing consumer spending on home entertainment.

In Europe, Germany leads with a focus on high-end audio engineering and innovation, while France is witnessing increased adoption of connected audio systems in both residential and commercial sectors.

- China dominates APAC with rapid market expansion

- Japan emphasizes innovation and premium audio quality

- United States leads in smart Hi-Fi adoption

- Canada and Mexico show steady growth trends

- Germany and France drive European market innovation

Key Hi-Fi System Market Company Insights

The Hi-Fi System Market is highly competitive, with key players focusing on innovation, product differentiation, and integration of advanced technologies. Companies are investing in AI-enabled audio solutions, wireless connectivity, and smart home compatibility to strengthen their market position.

Major players include Sony Corporation, Samsung Electronics, LG Electronics, Bose Corporation, Panasonic Corporation, Yamaha Corporation, Harman International, and Denon. These companies are leveraging strong brand recognition and extensive distribution networks to expand their global footprint. Their strategies include launching premium product lines, enhancing user experience through AI integration, and forming partnerships with streaming service providers.

- Companies focus on AI-driven audio enhancements

- Strong emphasis on wireless and smart connectivity

- Premium product innovation drives competition

- Strategic partnerships enhance market reach

- Investment in R&D supports technological advancements

Recent Developments

Recent developments in the Hi-Fi System Market highlight the increasing integration of advanced technologies. Several companies have launched AI-powered Hi-Fi systems with adaptive sound optimization and voice assistant capabilities.

There has also been a rise in partnerships between audio equipment manufacturers and streaming platforms to deliver seamless content access. Additionally, new product launches featuring spatial audio and immersive sound technologies are gaining traction among consumers seeking enhanced listening experiences.

Market Segmentation

The Hi-Fi System Market is segmented based on product, technology/component, application, and region. By product, the market includes wireless Hi-Fi systems, traditional component systems, and integrated smart audio devices. By technology, it encompasses Bluetooth, Wi-Fi, AI-driven sound processing, and IoT-enabled systems. Applications include residential, commercial, automotive, and entertainment sectors. Regionally, the market is divided into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Wireless systems dominate product segment

- AI and IoT are key technology drivers

- Residential segment leads application demand

- Commercial and automotive sectors show growth potential

- Asia Pacific emerges as a key growth region

The Hi-Fi System Market is set for substantial growth through 2035, driven by increasing demand for immersive audio experiences and rapid advancements in AI, IoT, and automation technologies. As consumers continue to embrace smart home ecosystems and digital entertainment, Hi-Fi systems are evolving into intelligent, connected devices. The integration of advanced features such as voice control, adaptive sound optimization, and multi-room audio will further enhance market appeal. Businesses investing in innovative audio solutions and strategic partnerships will be well-positioned to capitalize on emerging opportunities, making the Hi-Fi System Market a critical component of the future consumer electronics landscape.

FAQs on Hi-Fi System Market

-

What is the current size of the Hi-Fi System Market?

The market was valued at approximately USD 15.8 billion in 2024. -

What is the expected growth rate of the market?

The market is projected to grow at a CAGR of 6.8% from 2025 to 2035. -

What are the key drivers of the market?

Key drivers include AI integration, IoT connectivity, rising demand for premium audio, and smart home adoption. -

Which region leads the market?

North America currently leads the Hi-Fi System Market. -

Who are the key players in the market?

Major companies include Sony, Samsung, LG, Bose, Panasonic, Yamaha, Harman, and Denon.

To speak to our analyst for a discussion on the above findings, click Speak to Analyst

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TABLE OF CONTENTS

1 INTRODUCTION (Page No. - 17)

1.1 STUDY OBJECTIVES

1.2 DEFINITION AND SCOPE

1.2.1 INCLUSIONS AND EXCLUSIONS

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 YEARS CONSIDERED

1.4 CURRENCY

1.5 PACKAGE SIZE

1.6 MARKET STAKEHOLDERS

2 RESEARCH METHODOLOGY (Page No. - 20)

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Breakdown of primaries

2.1.2.2 Key data from primary sources

2.1.3 SECONDARY AND PRIMARY RESEARCH

2.1.3.1 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.1.1 Approach for estimating the market size by bottom-up analysis (demand side)

2.2.2 TOP-DOWN APPROACH

2.2.2.1 Approach for estimating the market size by top-down approach (supply side)

2.3 DATA TRIANGULATION

2.4 RESEARCH ASSUMPTIONS

3 EXECUTIVE SUMMARY (Page No. - 29)

4 PREMIUM INSIGHTS (Page No. - 33)

4.1 MAJOR OPPORTUNITIES IN HI-FI SYSTEM MARKET

4.2 MARKET, BY CONNECTIVITY TECHNOLOGY

4.3 MARKET IN APAC, BY SYSTEM AND COUNTRY

4.4 MARKET, BY COUNTRY

4.5 MARKET, BY APPLICATION

5 HI-FI SYSTEM MARKET OVERVIEW (Page No. - 36)

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rise in demand for infotainment services

5.2.1.2 High spending on R&D by OEMs

5.2.1.3 Innovations in wireless audio technology

5.2.1.4 Increasing adoption of portable devices

5.2.2 RESTRAINTS

5.2.2.1 Issues related to operating frequency compliance for wireless Hi-Fi systems

5.2.2.2 Health issues pertaining to prolonged use of audio devices

5.2.3 OPPORTUNITIES

5.2.3.1 Growth of speakers and soundbars market in emerging regions

5.2.3.2 Newer, nonconventional applications of headphones

5.2.4 CHALLENGES

5.2.4.1 Delivering high-quality and synchronized audio through wireless Hi-Fi systems

5.3 VALUE CHAIN ANALYSIS

5.4 IMPACT OF COVID-19 ON MARKET

6 HI-FI SYSTEM MARKET, BY SYSTEM (Page No. - 42)

6.1 INTRODUCTION

6.2 PRODUCT

6.2.1 SPEAKER & SOUNDBAR

6.2.1.1 Increasing popularity of wireless speakers and soundbars among consumers is expected to drive this segment

6.2.2 CD PLAYER

6.2.2.1 Hi-Fi CD player market is currently witnessing stagnant growth

6.2.3 DVD PLAYER

6.2.3.1 Hi-Fi DVD player market is expected to decline during forecast period

6.2.4 BLU-RAY PLAYER

6.2.4.1 Market for Blu-ray player is expected to witness sluggish growth

6.2.5 NETWORK MEDIA PLAYER

6.2.5.1 Market for network media players to witness significant growth during forecast period

6.2.6 TURNTABLE

6.2.6.1 Turntable is having negligible share in market

6.2.7 HEADPHONE & EARPHONE

6.2.7.1 Over-ear

6.2.7.1.1 Over-ear headphones are considered to be the best headphones among all categories

6.2.7.2 On-ear

6.2.7.2.1 On-ear headphones provide high portability

6.2.7.3 In-ear

6.2.7.3.1 In-ear headphones are generally tiny and provide high portability

6.2.8 MICROPHONE

6.2.8.1 Continuous technological advancements in output sound quality of wireless microphones are expected to fuel growth of this segment

6.3 DEVICE

6.3.1 DAC (DIGITAL-TO-ANALOG CONVERTER)

6.3.1.1 DAC converts digital data streams into analog audio signals

6.3.2 AMPLIFIER

6.3.2.1 Standalone amplifiers allow users to add more speakers to a Hi-Fi stereo system

6.3.3 PREAMPLIFIER

6.3.3.1 Preamps are used along with sound equipment to improve overall quality of sound

6.3.4 RECEIVER

6.3.4.1 Receiver is used to capture signal from different sources

7 HI-FI SYSTEM MARKET, BY CONNECTIVITY TECHNOLOGY (Page No. - 65)

7.1 INTRODUCTION

7.2 WIRED

7.2.1 ETHERNET CABLE

7.2.1.1 Ethernet cable is one of the popular forms of wired audio technology

7.2.2 AUDIO CABLE

7.2.2.1 Audio cables transfer analog or digital signals from an audio source to an amplifier or powered speaker

7.3 WIRELESS

7.3.1 BLUETOOTH

7.3.1.1 Cost-effectiveness and compatibility associated with this technology is driving market of audio devices equipped with Bluetooth

7.3.2 WI-FI

7.3.2.1 Secured operation carried out by Wi-Fi-enabled audio devices leading to growth of this technology

7.3.3 AIRPLAY

7.3.3.1 Increased use of AirPlay technology for wireless streaming on devices supported by Apple 7.3.4 OTHERS

7.3.4.1 SKAA

7.3.4.2 Sonos

7.3.4.3 Play-Fi

7.3.4.4 RF and IR

8 HI-FI SYSTEM MARKET, BY APPLICATION (Page No. - 76)

8.1 INTRODUCTION

8.2 RESIDENTIAL

8.2.1 INCREASED USE OF WIRELESS AUDIO SYSTEMS FOR IN-HOME APPLICATION IS FUELING GROWTH OF MARKET IN RESIDENTIAL APPLICATION

8.3 AUTOMOTIVE

8.3.1 RISING DEMAND FOR PREMIUM AUDIO SYSTEMS IN LUXURY AUTOMOBILES TO SPUR GROWTH MARKET

8.4 COMMERCIAL

8.4.1 PREFERENCE FOR HIGH-END AUDIO IN COMMERCIAL PLACES IS DRIVING GROWTH OF HI-FI SYSTEMS IN THIS APPLICATION

8.5 OTHERS

8.5.1 INCREASING DEMAND FOR HI-FI HEADPHONES AND MICROPHONES IN SECURITY AND MILITARY APPLICATIONS IS DRIVING GROWTH OF OTHERS SEGMENT

9 GEOGRAPHIC ANALYSIS (Page No. - 85)

9.1 INTRODUCTION

9.2 NORTH AMERICA

9.2.1 US

9.2.1.1 Presence of majority of wireless audio device manufacturers in the country is fueling growth of market in US

9.2.2 CANADA

9.2.2.1 Preference of Canadian population to adopt innovative products contributing to growth of market

9.2.3 MEXICO

9.2.3.1 Growing investments in consumer electronics industry of Mexico lead to growth of market

9.3 EUROPE

9.3.1 GERMANY

9.3.1.1 Popularity of wireless streaming speakers and premium soundbars to boost market in Germany

9.3.2 UK

9.3.2.1 Willingness of users to invest in wireless audio devices to fuel growth of market in UK

9.3.3 FRANCE

9.3.3.1 Rising demand for audio devices in home entertainment application to spur growth of market in France

9.3.4 SPAIN

9.3.4.1 Growing demand for Hi-Fi speakers will lead to growth of market in Spain

9.3.5 REST OF EUROPE

9.4 APAC

9.4.1 CHINA

9.4.1.1 Geographical expansion by international wireless audio device manufacturers is expected to lead to growth of market in China

9.4.2 JAPAN

9.4.2.1 Rise in demand for consumer electronics equipped with wireless audio technology to spur growth of market in Japan

9.4.3 AUSTRALIA

9.4.3.1 Adoption of innovative audio technologies among consumer groups to boost growth of market in Australia

9.4.4 INDIA

9.4.4.1 Government initiatives such as Make in India are fueling demand for consumer durables in India

9.4.5 REST OF APAC

9.5 REST OF THE WORLD (ROW)

9.5.1 SOUTH AMERICA

9.5.1.1 Brazil and Argentina are potential markets for Hi-Fi systems in

South America 104

9.5.2 MIDDLE EAST

9.5.2.1 Surge in demand for wireless speakers and wireless headphones to fuel growth of market in Middle East

9.5.3 AFRICA

9.5.3.1 South Africa holds significant share in market

10 COMPETITIVE LANDSCAPE (Page No. - 106)

10.1 INTRODUCTION

10.2 RANKING ANALYSIS OF KEY PLAYERS IN MARKET

10.3 COMPETITIVE SITUATIONS AND TRENDS

10.3.1 PRODUCT LAUNCHES

10.3.2 PARTNERSHIP

10.3.3 ACQUISITION

10.4 COMPETITIVE LEADERSHIP MAPPING, 2019

10.4.1 VISIONARY LEADERS

10.4.2 INNOVATORS

10.4.3 DYNAMIC DIFFERENTIATORS

10.4.4 EMERGING COMPANIES

11 COMPANY PROFILES (Page No. - 112)

11.1 KEY PLAYERS

(Business Overview, Products/Solutions/Services Offered, Recent Developments, SWOT Analysis, and MnM View)*

11.1.1 SAMSUNG ELECTRONICS CO., LTD.

11.1.2 SONY CORPORATION

11.1.3 APPLE INC.

11.1.4 BOSE CORPORATION

11.1.5 SENNHEISER ELECTRONIC GMBH & CO. KG

11.1.6 LG ELECTRONICS

11.1.7 PANASONIC CORPORATION

11.1.8 DEI HOLDINGS, INC.

11.1.9 YAMAHA CORPORATION

11.1.10 KONINKLIJKE PHILIPS N.V.

* Business Overview, Products/Solutions/Services Offered, Recent Developments, SWOT Analysis, and MnM View might not be captured in case of unlisted companies.

11.2 RIGHT TO WIN

11.3 OTHER IMPORTANT PLAYERS

11.3.1 BOWERS & WILKINS

11.3.2 TANNOY LTD.

11.3.3 VOXX INTERNATIONAL CORPORATION

11.3.4 SONOS, INC.

11.3.5 VIZIO INC.

11.3.6 ONKYO CORPORATION

11.3.7 BANG & OLUFSEN

11.3.8 PLANTRONICS, INC.

11.3.9 DALI A/S

11.3.10 HUMAN INC.

11.3.11 LINN PRODUCTS

11.3.12 CAMBRIDGE AUDIO

12 APPENDIX (Page No. - 145)

12.1 DISCUSSION GUIDE

12.2 KNOWLEDGE STORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

12.3 AVAILABLE CUSTOMIZATIONS

12.4 RELATED REPORTS

12.5 AUTHOR DETAILS

LIST OF TABLES (108 Tables)

TABLE 1 HI-FI SYSTEM MARKET, BY SYSTEM, 2017–2025 (USD BILLION)

TABLE 2 MARKET FOR PRODUCT, BY TYPE, 2017–2025 (USD MILLION)

TABLE 3 MARKET FOR PRODUCT, BY TYPE, 2017–2025 (MILLION UNITS)

TABLE 4 MARKET FOR PRODUCT, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 5 MARKET FOR PRODUCT, BY REGION, 2017–2025 (USD MILLION)

TABLE 6 MARKET FOR SPEAKER & SOUNDBAR, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 7 MARKET FOR SPEAKER & SOUNDBAR, BY REGION, 2017–2025 (USD MILLION)

TABLE 8 MARKET FOR SPEAKER & SOUNDBAR, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 9 MARKET FOR CD PLAYER, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 10 MARKET FOR CD PLAYER, BY REGION, 2017–2025 (USD MILLION)

TABLE 11 MARKET FOR CD PLAYER, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 12 MARKET FOR DVD PLAYER, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 13 MARKET FOR DVD PLAYER, BY REGION, 2017–2025 (USD MILLION)

TABLE 14 MARKET FOR DVD PLAYER, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 15 MARKET FOR BLU-RAY PLAYER, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 16 MARKET FOR BLU-RAY PLAYER, BY REGION, 2017–2025 (USD MILLION)

TABLE 17 MARKET FOR BLU-RAY PLAYER, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 18 MARKET FOR NETWORK MEDIA PLAYER, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 19 MARKET FOR NETWORK MEDIA PLAYER, BY REGION, 2017–2025 (USD MILLION)

TABLE 20 MARKET FOR NETWORK MEDIA PLAYER, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 21 MARKET FOR TURNTABLE, BY APPLICATION, 2017–2025 (USD THOUSAND)

TABLE 22 HI-FI SYSTEM MARKET FOR TURNTABLE, BY REGION, 2017–2025 (USD THOUSAND)

TABLE 23 MARKET FOR TURNTABLE, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD THOUSAND)

TABLE 24 MARKET FOR HEADPHONE & EARPHONE, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 25 MARKET FOR HEADPHONE & EARPHONE, BY REGION, 2017–2025 (USD MILLION)

TABLE 26 MARKET FOR HEADPHONE & EARPHONE, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 27 MARKET FOR MICROPHONE, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 28 MARKET FOR MICROPHONE, BY REGION, 2017–2025 (USD MILLION)

TABLE 29 MARKET FOR MICROPHONE, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 30 MARKET FOR DEVICE, BY TYPE, 2017–2025 (USD MILLION)

TABLE 31 MARKET FOR DEVICE, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 32 HI-FI SYSTEM MARKET FOR DEVICE, BY REGION, 2017–2025 (USD MILLION)

TABLE 33 MARKET FOR DAC, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 34 MARKET FOR DAC, BY REGION, 2017–2025 (USD MILLION)

TABLE 35 MARKET FOR DAC, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 36 MARKET FOR AMPLIFIER, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 37 MARKET FOR AMPLIFIER, BY REGION, 2017–2025 (USD MILLION)

TABLE 38 MARKET FOR AMPLIFIER, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 39 MARKET FOR PREAMPLIFIER, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 40 MARKET FOR PREAMPLIFIER, BY REGION, 2017–2025 (USD MILLION)

TABLE 41 MARKET FOR PREAMPLIFIER, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 42 MARKET FOR RECEIVER, BY APPLICATION, 2017–2025 (USD MILLION)

TABLE 43 MARKET FOR RECEIVER, BY REGION, 2017–2025 (USD MILLION)

TABLE 44 MARKET FOR RECEIVER, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 45 HI-FI SYSTEM MARKET, BY CONNECTIVITY TECHNOLOGY, 2017–2025 (USD BILLION)

TABLE 46 MARKET FOR WIRED CONNECTIVITY TECHNOLOGY FOR PRODUCT, BY TYPE, 2017–2025 (USD MILLION)

TABLE 47 MARKET FOR WIRED CONNECTIVITY TECHNOLOGY FOR DEVICE, BY TYPE, 2017–2025 (USD MILLION)

TABLE 48 MARKET FOR PRODUCT, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 49 MARKET FOR DEVICE, BY WIRELESS CONNECTIVITY TECHNOLOGY, 2017–2025 (USD MILLION)

TABLE 50 MARKET FOR WIRELESS CONNECTIVITY TECHNOLOGY FOR PRODUCT, BY TYPE, 2017–2025 (USD MILLION)

TABLE 51 MARKET FOR WIRELESS CONNECTIVITY TECHNOLOGY FOR DEVICE, BY TYPE, 2017–2025 (USD MILLION)

TABLE 52 MARKET FOR BLUETOOTH TECHNOLOGY, BY PRODUCT, 2017–2025 (USD MILLION)

TABLE 53 MARKET FOR BLUETOOTH TECHNOLOGY, BY DEVICE, 2017–2025 (USD MILLION)

TABLE 54 MARKET FOR WI-FI TECHNOLOGY, BY PRODUCT, 2017–2025 (USD MILLION)

TABLE 55 MARKET FOR WI-FI TECHNOLOGY, BY DEVICE, 2017–2025 (USD MILLION)

TABLE 56 MARKET FOR AIRPLAY TECHNOLOGY, BY PRODUCT, 2017–2025 (USD MILLION)

TABLE 57 MARKET FOR AIRPLAY TECHNOLOGY, BY DEVICE, 2017–2025 (USD MILLION)

TABLE 58 MARKET FOR OTHER TECHNOLOGIES, BY PRODUCT, 2017–2025 (USD MILLION)

TABLE 59 MARKET FOR OTHER TECHNOLOGIES, BY DEVICE, 2017–2025 (USD MILLION)

TABLE 60 HI-FI SYSTEM MARKET, BY APPLICATION, 2017–2025 (USD BILLION)

TABLE 61 MARKET IN RESIDENTIAL APPLICATION, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 62 MARKET FOR PRODUCT IN RESIDENTIAL APPLICATION, BY TYPE, 2017–2025 (USD MILLION)

TABLE 63 MARKET FOR DEVICE IN RESIDENTIAL APPLICATION, BY TYPE, 2017–2025 (USD MILLION)

TABLE 64 MARKET IN AUTOMOTIVE APPLICATION, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 65 MARKET FOR PRODUCT IN AUTOMOTIVE APPLICATION, BY TYPE, 2017–2025 (USD MILLION)

TABLE 66 MARKET FOR DEVICE IN AUTOMOTIVE APPLICATION, BY TYPE, 2017–2025 (USD MILLION)

TABLE 67 MARKET IN COMMERCIAL APPLICATION, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 68 MARKET FOR PRODUCT IN COMMERCIAL APPLICATION, BY TYPE, 2017–2025 (USD MILLION)

TABLE 69 MARKET FOR DEVICE IN COMMERCIAL APPLICATION, BY TYPE, 2017–2025 (USD MILLION)

TABLE 70 MARKET IN OTHER APPLICATIONS, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 71 MARKET FOR PRODUCT IN OTHER APPLICATIONS, BY TYPE, 2017–2025 (USD MILLION)

TABLE 72 MARKET FOR DEVICE IN OTHER APPLICATIONS, BY TYPE, 2017–2025 (USD MILLION)

TABLE 73 HI-FI SYSTEM MARKET, BY REGION, 2017–2025 (USD BILLION)

TABLE 74 MARKET IN NORTH AMERICA, BY COUNTRY, 2017–2025 (USD MILLION)

TABLE 75 MARKET IN NORTH AMERICA, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 76 MARKET FOR PRODUCT IN NORTH AMERICA, BY TYPE, 2017–2025 (USD MILLION)

TABLE 77 MARKET FOR DEVICE IN NORTH AMERICA, BY TYPE, 2017–2025 (USD MILLION)

TABLE 78 MARKET IN THE US, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 79 MARKET IN CANADA, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 80 MARKET IN MEXICO, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 81 MARKET IN EUROPE, BY COUNTRY, 2017–2025 (USD MILLION)

TABLE 82 MARKET IN EUROPE, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 83 MARKET FOR PRODUCT IN EUROPE, BY TYPE, 2017–2025 (USD MILLION)

TABLE 84 MARKET FOR DEVICE IN EUROPE, BY TYPE, 2017–2025 (USD MILLION)

TABLE 85 MARKET IN GERMANY, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 86 MARKET IN UK, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 87 MARKET IN FRANCE, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 88 MARKET IN SPAIN, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 89 MARKET IN REST OF EUROPE, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 90 MARKET IN APAC, BY COUNTRY, 2017–2025 (USD MILLION)

TABLE 91 MARKET IN APAC, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 92 HI-FI SYSTEM MARKET FOR PRODUCT IN APAC, BY TYPE, 2017–2025 (USD MILLION)

TABLE 93 MARKET FOR DEVICE IN APAC, BY TYPE, 2017–2025 (USD MILLION)

TABLE 94 MARKET IN CHINA, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 95 MARKET IN JAPAN, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 96 MARKET IN AUSTRALIA, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 97 MARKET IN INDIA, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 98 MARKET IN REST OF APAC, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 99 MARKET IN ROW, BY REGION, 2017–2025 (USD MILLION)

TABLE 100 MARKET IN ROW, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 101 MARKET FOR PRODUCT IN ROW, BY TYPE, 2017–2025 (USD MILLION)

TABLE 102 MARKET FOR DEVICE IN ROW, BY TYPE, 2017–2025 (USD MILLION)

TABLE 103 MARKET IN SOUTH AMERICA, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 104 HI-FI SYSTEM MARKET IN MIDDLE EAST, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 105 MARKET IN AFRICA, BY SYSTEM, 2017–2025 (USD MILLION)

TABLE 106 PRODUCT LAUNCHES, 2019

TABLE 107 PARTNERSHIP, 2018

TABLE 108 ACQUISITION, 2018

LIST OF FIGURES (55 Figures)

FIGURE 1 MARKET SEGMENTATION

FIGURE 2 HI-FI SYSTEM MARKET: RESEARCH DESIGN

FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY—APPROACH 1 (SUPPLY SIDE): REVENUE OF MARKET PLAYERS

FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY—APPROACH 2 (DEMAND SIZE): BOTTOM-UP MARKET ESTIMATION FOR HI-FI SYSTEMS

FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

FIGURE 7 DATA TRIANGULATION

FIGURE 8 ASSUMPTIONS FOR THE RESEARCH STUDY

FIGURE 9 HI-FI SYSTEM MARKET, 2017–2025

FIGURE 10 PRODUCT SEGMENT EXPECTED TO DOMINATE MARKET DURING FORECAST PERIOD

FIGURE 11 WIRELESS CONNECTIVITY TECHNOLOGY EXPECTED TO REGISTER HIGHER GROWTH RATE DURING FORECAST PERIOD

FIGURE 12 RESIDENTIAL APPLICATION EXPECTED TO HOLD LARGEST SHARE IN MARKET DURING FORECAST PERIOD

FIGURE 13 APAC HELD LARGEST SHARE OF MARKET IN 2019

FIGURE 14 MARKET EXPECTED TO REGISTER HIGHEST CAGR IN APAC DURING FORECAST PERIOD

FIGURE 15 MARKET FOR WIRELESS TECHNOLOGY EXPECTED TO WITNESS HIGHER GROWTH RATE DURING FORECAST PERIOD

FIGURE 16 PRODUCT SEGMENT HELD LARGER SHARE OF MARKET IN APAC IN 2019

FIGURE 17 US DOMINATED GLOBAL MARKET IN 2019

FIGURE 18 AUTOMOTIVE APPLICATION TO WITNESS HIGHEST GROWTH IN MARKET DURING FORECAST PERIOD

FIGURE 19 INNOVATIONS IN WIRELESS AUDIO TECHNOLOGIES BOOST GROWTH OF MARKET

FIGURE 20 IMPACT ANALYSIS: DRIVERS

FIGURE 21 IMPACT ANALYSIS: RESTRAINTS

FIGURE 22 IMPACT ANALYSIS: OPPORTUNITIES

FIGURE 23 IMPACT ANALYSIS: CHALLENGE

FIGURE 24 MAJOR VALUE IS ADDED DURING MANUFACTURING AND ASSEMBLY STAGES

FIGURE 25 MARKET, BY SYSTEM

FIGURE 26 PRODUCT SEGMENT EXPECTED TO DOMINATE MARKET DURING FORECAST PERIOD

FIGURE 27 MARKET, BY PRODUCT

FIGURE 28 HI-FI SYSTEM MARKET, BY DEVICE

FIGURE 29 MARKET, BY CONNECTIVITY TECHNOLOGY

FIGURE 30 WIRELESS TECHNOLOGY EXPECTED TO SURPASS WIRED TECHNOLOGY IN MARKET BY 2025

FIGURE 31 MARKET, BY WIRED TECHNOLOGY

FIGURE 32 MARKET, BY WIRELESS TECHNOLOGY

FIGURE 33 MARKET, BY APPLICATION

FIGURE 34 RESIDENTIAL APPLICATION EXPECTED TO HOLD LARGEST SIZE OF MARKET DURING FORECAST PERIOD

FIGURE 35 MARKET, BY REGION

FIGURE 36 MARKET IN NORTH AMERICA

FIGURE 37 HI-FI SYSTEM MARKET SNAPSHOT: NORTH AMERICA

FIGURE 38 MARKET IN EUROPE

FIGURE 39 MARKET SNAPSHOT: EUROPE

FIGURE 40 MARKET IN APAC

FIGURE 41 MARKET SNAPSHOT: APAC

FIGURE 42 MARKET IN ROW

FIGURE 43 MARKET SNAPSHOT: ROW

FIGURE 44 MARKET: KEY GROWTH STRATEGY ADOPTED BY COMPANIES FROM 2017 T0 2019

FIGURE 45 HI-FI SYSTEM MARKET: RANKING OF KEY COMPANIES

FIGURE 46 MARKET (GLOBAL) COMPETITIVE LEADERSHIP MAPPING, 2019

FIGURE 47 SAMSUNG ELECTRONICS CO., LTD.: COMPANY SNAPSHOT

FIGURE 48 SONY CORPORATION: COMPANY SNAPSHOT

FIGURE 49 APPLE INC.: COMPANY SNAPSHOT

FIGURE 50 BOSE CORPORATION: COMPANY SNAPSHOT

FIGURE 51 SENNHEISER ELECTRONIC GMBH & CO. KG: COMPANY SNAPSHOT

FIGURE 52 LG ELECTRONICS: COMPANY SNAPSHOT

FIGURE 53 PANASONIC CORPORATION: COMPANY SNAPSHOT

FIGURE 54 YAMAHA CORPORATION: COMPANY SNAPSHOT

FIGURE 55 KONINKLIJKE PHILIPS N.V.: COMPANY SNAPSHOT

The study involved four major activities in estimating the size of the Hi-Fi system market. Exhaustive secondary research was done to collect information on the market, peer market, and parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the total market’s size. After that, market breakdown and data triangulation were used to determine the market sizes of segments and sub-segments.

Secondary Research

In the Hi-Fi system market, both top-down and bottom-up approaches have been used to estimate and validate the size of the Hi-Fi system market, along with other dependent submarkets. Key players in the Hi-Fi system market have been identified through secondary research, and their revenue has been determined through primary and secondary research activities. This entire research methodology involved studying annual and financial reports of the top players and interviewing experts (such as CEOs, VPs, directors, and marketing executives) for key insights (both quantitative and qualitative). All percentage shares split, and breakdowns have been determined using secondary sources and verified through primary sources. All the possible parameters that may affect the markets covered in this research study have been accounted for, viewed in detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data. This data has been consolidated and supplemented with detailed inputs and analysis from MarketsandMarkets and presented in this report.

>

Primary Research

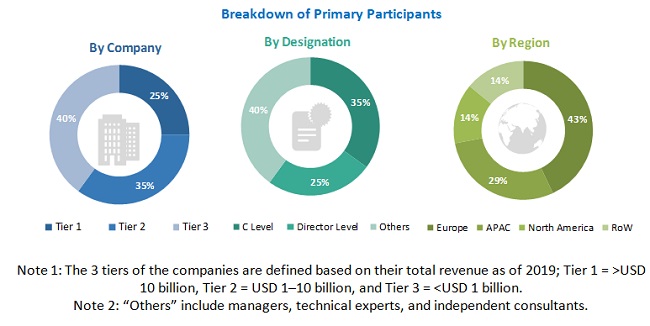

The Hi-Fi system market supply chain comprises several stakeholders, such as key technology providers, manufacturers, system integrators, distribution channels, marketing & sales, and end-users. The demand side of this market is characterized by applications such as residential, automotive, commercial, and others; the supply side is characterized by technology and product/associated device suppliers and software providers. Various primary sources from both the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information. The breakdown of the primary respondents is provided below:

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

Both top-down and bottom-up approaches were used to estimate and validate the total size of the Hi-Fi system market. These methods were also extensively used to estimate the sizes of various market sub-segments. The research methodology used to estimate the market sizes includes the following:

- The key players in the market were identified through extensive secondary research.

- The industry’s supply chain and market size, in terms of value, were determined through primary and secondary research.

All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources.

Data Triangulation

After arriving at the overall market size—using the market size estimation processes explained above—the market was split into several segments and sub-segments. To complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment, data triangulation, and market breakdown procedures were employed, wherever applicable. The data was triangulated by studying various factors and trends from both the demand and supply sides.

The main objectives of this study are:

- To define, describe, segment, and forecast the Hi-Fi system market, in terms of value, based on system, connectivity technology, and application

- To describe and forecast the size of the market, for four regions—North America, Europe, Asia Pacific (APAC), and the Rest of the World (RoW)—in terms of value

- To forecast the market size, in terms of volume, for the market segmented on the basis of product under system segment

- To strategically analyze micromarkets with respect to individual growth trends, prospects, and contributions to the total market

- To provide detailed information regarding the major factors such as drivers, restraints, opportunities, and challenges influencing the market growth

- To provide a detailed value chain for the Hi-Fi system market

- To analyze the opportunities in the market for stakeholders and details of the competitive landscape of the market

- To strategically profile the key players and comprehensively analyze their market shares and core competencies, along with the competitive leadership mapping chart

- To analyze the competitive developments such as partnerships, mergers and acquisitions, and product launches in the Hi-Fi system market

Available Customizations:

With the given market data, MarketsandMarkets offers customizations according to the company’s specific needs. The following customization options are available for the report:

Company Information

- Detailed analysis and profiling of additional market players (up to 5)

Growth opportunities and latent adjacency in Hi-Fi System Market