Download PDF

Download PDF Request Customisation

Request Customisation

LiDAR Market Size, Share & Trends

Report Code

SE 3281

Published in

Aug, 2025, By MarketsandMarkets™

LiDAR Market Size, Share & Trends by Installation (Airborne, Ground-based), Type (Mechanical, Solid-state), Range (Short, Medium, Long), Service Aerial Surveying, Asset Management, GIS Services, Ground-based Surveying), Region - Global Forecast to 2030

USD 12.79 BN

MARKET SIZE, 2030

CAGR 31.3%

(2025-2030)

264

REPORT PAGES

250

MARKET TABLES

LIDAR MARKET SIZE, SHARE & TRENDS

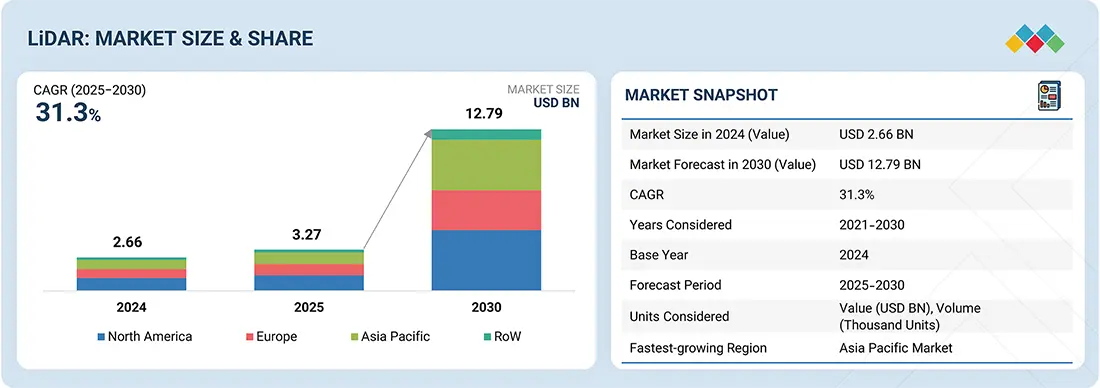

According to Marketsandmarkets, The global LiDAR market size was valued at USD 3.27 billion in 2025 and is projected to reach USD 12.79 billion by 2030, growing at a CAGR of 31.3%. from 2025 to 2030. . The LiDAR market is witnessing robust growth driven by rising adoption in autonomous vehicles, environmental mapping, and smart infrastructure projects. Segments such as automotive (ADAS), corridor mapping, and urban planning are positively influencing market expansion. Government initiatives supporting smart city development and investments in digital twin and 3D mapping technologies are fueling demand. Additionally, regulatory approvals for autonomous navigation and increased defense spending on surveillance systems are further accelerating LiDAR adoption.

MARKET SNAPSHOT TABLE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2025 (Value) | USD 3.27 Billion |

| Market Forecast in 2030 (Value) | USD 12.79 Billion |

| Growth Rate | CAGR of 31.3% from 2025–2030 |

| Years Considered | 2021–2030 |

| Base Year | 2024 |

| Forecast Period | 2025–2030 |

| Units Considered | Value (USD Billion), Volume (Thousand Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth |

| Top Companies |

|

| Growth Drivers |

|

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, and RoW |

Market Size & Forecast

• 2025 Market Size: USD 3.27 Billion

• 2030 Projected Market Size: USD 12.79 Billion

• CAGR (2025-2030): 31.3%

• Ground-based LiDAR : Larger Market Share

• Asia Pacific : Fastest growing market

LIDAR MARKET KEY TAKEAWAYS

-

BY INSTALLATIONGround-based LiDAR holds a larger market share and is expected to grow faster than airborne LiDAR due to its lower cost and simpler approval requirements for mapping and surveying. Its increasing use in applications such as meteorology, corridor mapping, ADAS, and autonomous vehicles is driving this growth.

-

BY TYPEThe mechanical LiDAR segment dominated the market in 2024, driven by its extensive use in applications like corridor mapping, military, and engineering. Its wide field of view and long-range capability make it ideal for large-scale mapping, contributing to its larger market share.

-

BY RANGEThe short-range LiDAR segment is projected to lead the market due to its adoption in applications such as automobiles, security, and robotics

-

BY SERVICEAerial surveying is projected to dominate the LiDAR market, as it enables precise inspection of roads, railways, highways, and bridges using manned or unmanned systems like drones and aircraft. Its accuracy and wide adoption by government bodies further drive its market share.

-

BY END USE APPLICATIONThe ADAS & driverless cars segment is expected to lead the LiDAR market, driven by the adoption of solid-state LiDAR to enhance safety in autonomous vehicles. With major automakers like Mercedes-Benz, Volvo, NIO, and others launching L2–L4 models, rising demand for intelligent vehicles is accelerating LiDAR adoption and market growth.

-

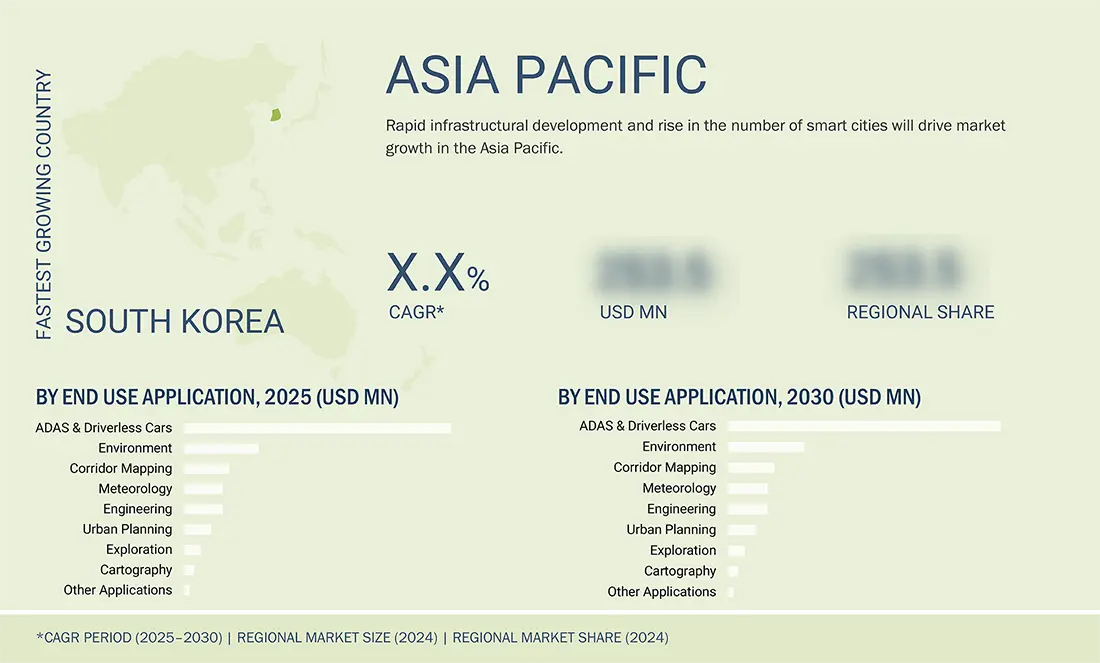

BY REGIONLiDAR market in the Asia Pacific is projected to grow at the highest CAGR during the forecast period. This market's growth can be attributed to the increase in surveying and mapping operations due to the increasing infrastructural development, focus on forest management, and an increase in mining activities.

-

COMPETITIVE LANDSCAPEMajor vendors in the LiDAR market includes Hesai Group (China), RoboSense Technology Co., Ltd. (China), Sick AG (Germany), Ouster, Inc. (US), Luminar Technologies (US), Leica Geosystems AG (Sweden), Trimble Inc. (US), Teledyne Optech (Canada), FARO Technologies, Inc. (US) and RIEGL Laser Measurement Systems GmbH (Austria). Key strategies adopted by the players in the LiDAR market ecosystem to enhance their product portfolios, increase their market share, and expand their presence in the market mainly include new product launches and partnerships, and acquisitions.

Key drivers of the LiDAR industry include the rising adoption of autonomous vehicles and advanced driver assistance systems (ADAS) for safety and navigation. Increasing use of LiDAR in surveying, mapping, and smart city applications is boosting demand. Additionally, technological advancements leading to cost reduction and improved accuracy are further propelling market growth The LiDAR Market is experiencing remarkable growth as industries increasingly adopt advanced sensing technologies for precision mapping, autonomous vehicles, and smart infrastructure projects.

The LiDAR Market size is expanding rapidly, driven by rising demand in urban planning, environmental monitoring, and transportation sectors. Recent studies show that the LiDAR Market share is being captured by key players investing in high-resolution sensors, UAV integration, and next-generation software solutions. Current LiDAR Market trends indicate a shift toward lightweight, high-speed scanning systems and cloud-enabled data processing, which are enabling faster deployments and more efficient operations. Overall, the LiDAR Market growth is being supported by technological innovation and expanding applications across multiple sectors.

The LiDAR Industry is also seeing significant opportunities in geospatial intelligence and mapping applications. The LiDAR in mapping Market is gaining momentum as surveyors, urban planners, and infrastructure developers adopt LiDAR for accurate topographical analysis and 3D modeling. Regionally, the Europe LiDAR Market is emerging as a major hub due to strong smart city initiatives, government support, and high adoption of autonomous vehicle technologies. These factors collectively enhance the LiDAR Market growth, while continued investment in AI integration and edge computing is expected to further boost the LiDAR Market size and strengthen the LiDAR Market share globally.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

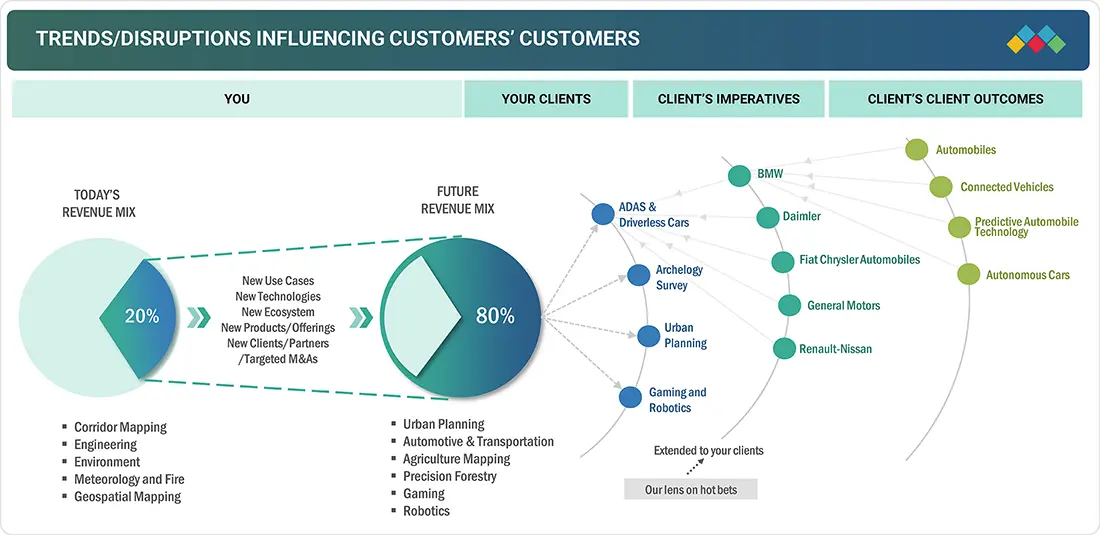

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The visual highlights how disruptive trends are reshaping customer business models, shifting revenue from traditional to emerging sources. Adopting mechanical LiDAR solutions in autonomous vehicles is expected to disrupt the LiDAR market in the coming years. LiDAR is currently being incorporated into advanced driver assistance systems to enhance the safety features of some semi-autonomous cars. Apart from this, the emergence of LiDAR technology has offered huge growth potential to a range of enterprises engaged in R&D and working toward introducing innovative solutions in the LiDAR market.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Rising adoption of UAV LiDAR systems to capture accurate evaluation data

-

Surging demand for 3D imaging solutions areas

RESTRAINTS

Impact

Level

Level

-

Availability of low-cost and lightweight alternatives

OPPORTUNITIES

Impact

Level

Level

-

Rising investments in ADAS systems by automotive giants

-

Increasing development of quantum dot detectors

CHALLENGES

Impact

Level

Level

-

High cost of post-processing LiDAR software

-

Complexities related to miniaturized LiDAR sensing

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Rising adoption of UAV LiDAR systems to capture accurate evaluation data

LiDAR-based UAVs are increasingly used in surveying and mapping as they offer cost-effective, portable, and versatile solutions compared to manual methods. Mounted on drones, LiDAR systems enable accurate data collection in inaccessible or hazardous terrains, supporting applications in infrastructure, environmental monitoring, and corridor mapping. Their ability to create digital elevation models and 3D representations makes them vital for complex engineering and remote area surveys.

Restraint: Availability of low-cost and lightweight alternatives

The growth of the LiDAR market size is restrained by the availability of low-cost and lightweight photogrammetry systems for mapping and surveying. While LiDAR drones offer higher accuracy and faster data acquisition, they are far more expensive due to costly sensors and hardware. In contrast, photogrammetry systems provide easily interpretable, colored 2D/3D models at significantly lower costs, making them a more accessible alternative.

Opportunity: Rising investments in ADAS systems by automotive giants

LiDAR technology is expanding its role in automobiles beyond ADAS to applications like self-driving taxis, shuttles, and mobility-on-demand fleets managed by companies such as Uber and Lyft. Automakers, including Volkswagen, which signed a USD 4 billion deal with Innoviz in 2022—are investing heavily in LiDAR for advanced driver assistance and autonomous driving. Major car manufacturers worldwide, from BMW and Toyota to GM and Hyundai, are partnering with LiDAR providers like Cepton, Innoviz, Ouster, and Waymo to advance Level 2 and Level 3 automation.

Challenge: High cost of post-processing LiDAR software

LiDAR surveying remains costly compared to traditional methods, with systems priced around USD 75,000 and post-processing software adding another USD 20,000–30,000 per license. While prices are expected to decline with market competition, high costs limit adoption in small-scale projects. Additionally, limited availability, uncertain accuracy, and privacy restrictions on geospatial data in many countries pose challenges to LiDAR market growth.

LiDAR Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

|

LiDAR sensors for autonomous vehicles to enable safe navigation and object detection | Enhanced accuracy in obstacle detection, improved safety, reliable performance in diverse environments |

|

|

Long-range LiDAR systems for ADAS and self-driving applications | 250m+ detection range, high-resolution mapping, better night and adverse weather visibility |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

LIDAR MARKET ECOSYSTEM

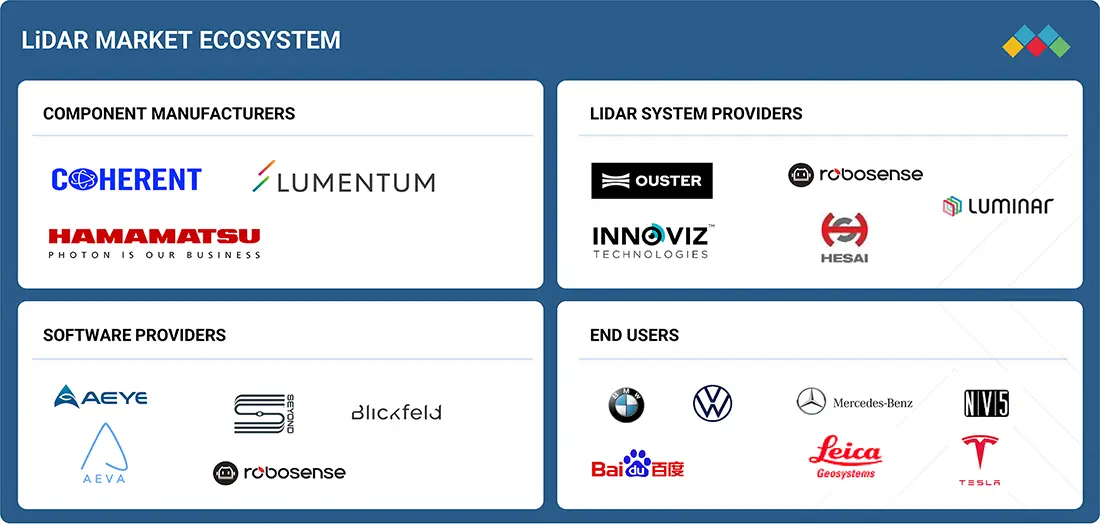

The LiDAR market ecosystem consists of several key players, including component manufacturers like Coherent, Hamamatsu, and Lumentum, system providers such as Ouster, Innoviz, and Hesai, and software providers such as AEye and Robosense. These companies collectively develop and deliver the essential hardware, complete LiDAR systems, and intelligent software solutions that enable diverse applications. End-users from automotive industrial, and technology sectors, like BMW, Tesla, and Mercedes-Benz, drive adoption and innovation within this interconnected ecosystem.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

LIDAR MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

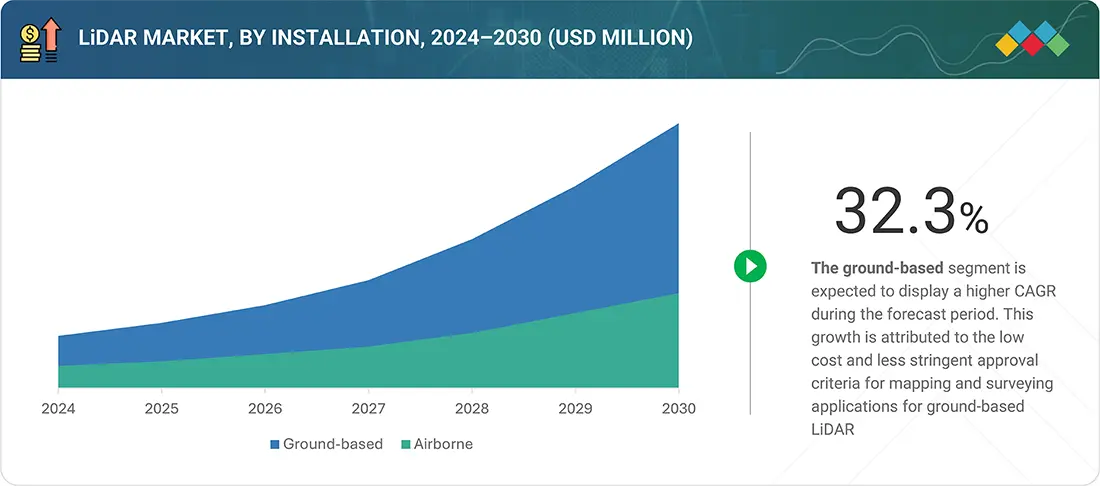

LiDAR Market, By Installation

The market for ground-based LiDAR accounted for a larger market share and is projected to grow at a higher CAGR than the airborne LiDAR segment during the forecast period. This growth is attributed to the low cost and less stringent approval criteria for mapping and surveying applications for ground-based LiDAR. Moreover, the high adoption of ground-based LiDAR in various applications, such as environment, meteorology, corridor mapping, advanced driver-assistance systems (ADAS), and driverless cars, is expected to drive the market soon.

LiDAR Market, By Type

The mechanical LiDAR segment accounted for a larger market share in 2024. By type, the LiDAR market is expected to be driven by the mechanical segment due to the widespread use of mechanical LiDAR in various applications, such as corridor mapping, military, volumetric mapping, and engineering. This leads to the larger size of the mechanical LiDAR market. The main advantage of mechanical Lidar is its ability to cover a wide field of view. A single sensor can cover an area of several square kilometers with a single scan, making it ideal for large-scale mapping applications. Mechanical LiDAR sensors can operate over long distances, with ranges of up to several kilometers.

LiDAR Market, By Range

The short-range LiDAR segment is projected to lead the market due to its adoption in applications such as automobiles, security, and robotics. The market for medium-range LiDAR is projected to grow at the highest rate, driven by its use in engineering and construction applications.

LiDAR Market, By Service

Aerial surveying is expected to hold the largest share of the LiDAR market during the forecast period. These services are widely deployed to monitor any mishaps in areas such as roads, railways, highways, and bridges. This surveying method can provide accurate results when inspecting the site and can be done using manned or unmanned aerial systems, such as drones and aircraft. Government bodies generally conduct these services.

LiDAR Market, By End Use Application

The market for ADAS & driverless cars is projected to have largest market share during the forecast period. The rising adoption of solid-state LiDAR in ADAS & driverless cars for assuring safety is expected to boost the market. Moreover, automotive giants are adopting LiDAR systems for their Level 3 automated vehicles, positively impacting the sales of these vehicle types. Mercedes-Benz, Volvo, NIO, and Xiaopeng have successfully released several models with L3-level autonomous driving capability since 2021. BYD also signed a strategic cooperation agreement with RoboSense, and BAIC ARCFOX and Huawei also jointly launched new models of the L2-L4 class. With the increased demand for intelligent autonomous vehicles, the advantages of LiDAR products are becoming more evident, and their market is undergoing massive development.

REGION

Asia Pacific to be the fastest-growing region in the global LiDAR market during the forecast period

The LiDAR market in the Asia Pacific is projected to grow at the highest CAGR during the forecast period. This market's growth can be attributed to the increase in surveying and mapping operations resulting from growing infrastructural development, a focus on forest management, and rising mining activities. The increasing applications of airborne and ground-based LiDAR systems, along with the growing number of surveying and mapping activities, are expected to drive demand for LiDAR in the region.

The Europe LiDAR market is projected to reach USD 3.16 billion by 2030 from USD 0.87 billion in 2025, at a CAGR of 29.6% during the period from 2025 to 2030. The proliferation of LiDAR technology in Europe is attributable to the robust adoption of autonomous driving, smart mobility solutions, and advanced mapping initiatives endorsed by European Union regulations. Furthermore, the expanding range of applications in environmental monitoring, agriculture, and infrastructure planning is fostering increased deployment throughout the region.

The LiDAR market in North America is projected to reach USD 4.8 billion by 2030 from USD 1.25 billion in 2025, growing at a CAGR of 30.9% from 2025 to 2030. The regional market is primarily driven by the rising deployment of autonomous and ADAS-enabled vehicles, as automotive OEMs and technology companies increasingly integrate LiDAR through supply agreements and partnerships. For instance, Luminar’s production contracts with global automakers and Ouster’s collaborations with robotics and mobility players play a major role in market expansion in the region.

The Asia Pacific LiDAR market is projected to reach USD 4.01 billion by 2030 from USD 0.92 billion in 2025, at a CAGR of 34.1% from 2025 to 2030. Segments, such as automotive (ADAS), corridor mapping, and urban planning, positively influence the market expansion. Growth is further supported by rising investments in autonomous and electric vehicles, large-scale smart city and infrastructure development programs across China, Japan, and Southeast Asia, and increasing adoption of LiDAR in industrial automation, robotics, and drone-based surveying applications across the region.

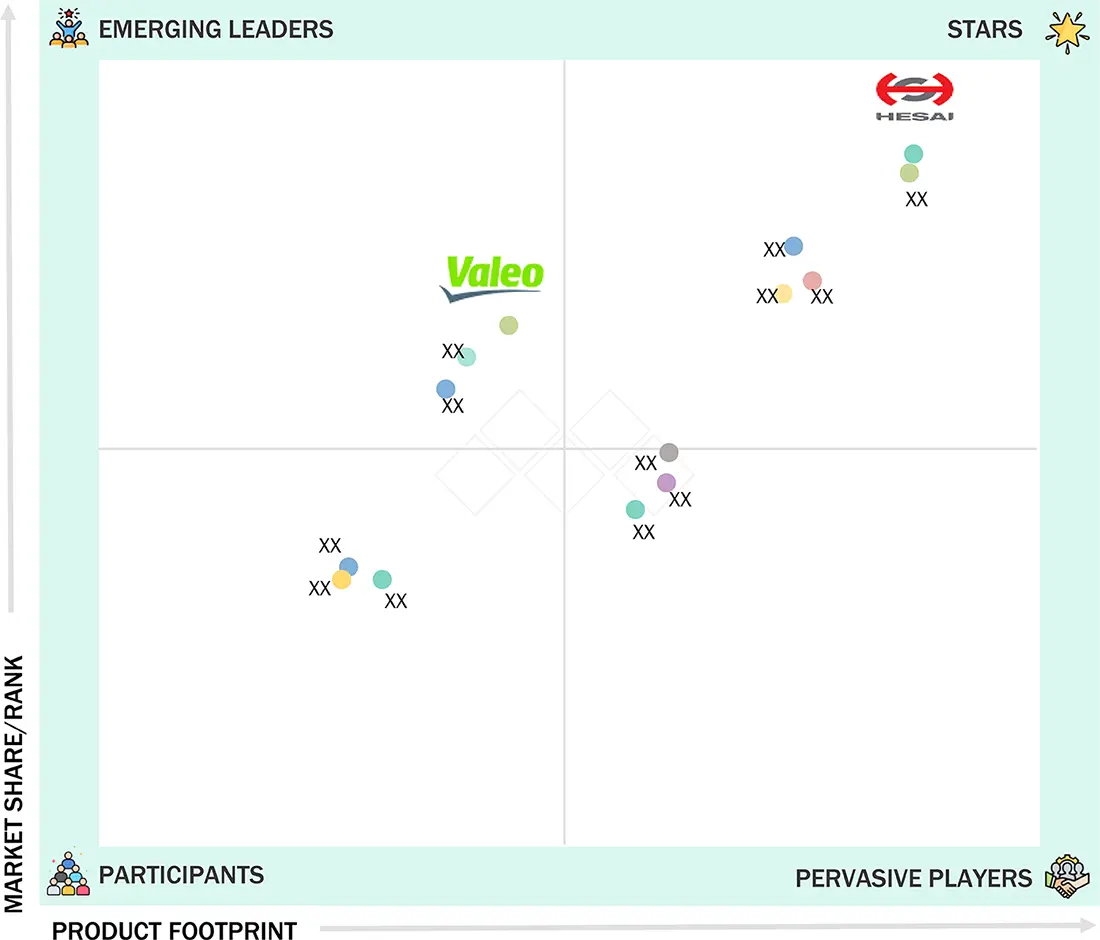

LiDAR Market: COMPANY EVALUATION MATRIX

Stars are the leading market players in new developments, such as product launches, innovative technologies, and the adoption of growth strategies. These players have a broad portfolio, innovative product offerings, and a global presence. They have well-established channels throughout the value chain. Hesai Group (China) comes under this category. Emerging Leaders demonstrate more substantial product innovations than their competitors. LiDAR Companies are investing more in R&D to launch several products in the market. A few players have a unique portfolio, while some have heavily invested in R&D or recently launched several products or innovative products. Valeo (France) comes under this category.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

- Hesai Group (China)

- RoboSense Technology Co., Ltd. (China)

- Sick AG (Germany)

- Ouster, Inc. (US)

- Luminar Technologies (US)

- Leica Geosystems AG (Sweden)

- Trimble Inc. (US)

- Teledyne Optech (Canada)

- FARO Technologies, Inc. (US)

- RIEGL Laser Measurement Systems GmbH(Austria)

- NV5 Geospatial (US)

- Beijing SureStar Technology Co., Ltd. (China)

- YellowScan (France)

WHAT IS IN IT FOR YOU: LiDAR Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Automotive OEM | Competitive benchmarking of LiDAR suppliers (cost, range, resolution), Assessment of LiDAR integration in ADAS & autonomous driving,Forecast of adoption levels across L2–L4 automation | Enable strategic sourcing for autonomous vehicle programs, Identify leading suppliers for long-term partnerships,Support technology roadmap for advanced mobility solutions |

| Defense & Security Contractor | Evaluation of LiDAR for surveillance, terrain mapping, and autonomous military vehicles,Adoption analysis in major defense programs | Strengthen positioning in defense modernization initiatives,Support entry into government-funded LiDAR programs |

RECENT DEVELOPMENTS

- March 2025 : Ouster introduced an important new feature called 3D Zone Monitoring for its REV7 digital LiDAR sensor lineup (including OS0, OS1, and OSDome models). This feature allows the sensor to detect objects within customized 3D zones on-sensor and trigger real-time alerts or actions, significantly enhancing collision avoidance capabilities in applications such as warehouse automation and industrial robotics. This update is delivered via firmware and represents a step towards Ouster's push to become an autonomy company by expanding sensor usability and simplifying development for customers.

- February 2025 : Leica Geosystems, part of Hexagon, introduced the Leica CoastalMapper, a next-generation airborne bathymetric LiDAR system. With a wider field of view and higher altitude operation, coastal and river survey efficiency is boosted by 250% compared to previous models. This advanced solution supports diverse applications, including infrastructure monitoring, flood assessment, and environmental studies in both shallow and deep waters.

- September 2023 : Trimble Inc. introduced the new Trimble R580 Global Navigation Satellite System (GNSS) receiver, the next generation in its Trimble ProPoint GNSS positioning engine-enabled receiver portfolio. The system’s survey-grade GNSS performance enables professionals in surveying, mapping, Geographic Information System (GIS), civil construction, and utilities to quickly and easily capture centimeter-level positioning and boost productivity in the field.

- February 2022 : Hexagon AB’s Geosystems division announced a strategic partnership with LocLab, a 3D digital content creator, to accelerate the adoption of smart digital realities in transportation, construction, and urban planning.

- June 2021 : Teledyne Optech and Teledyne CARIS launched the next-generation bathymetric lidar, the CZMIL SuperNova. The SuperNova provided a range of inputs for climate change modeling and was ideal for inland water environments and base mapping for coastal zones and shorelines.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

26

2

RESEARCH METHODOLOGY

31

3

EXECUTIVE SUMMARY

41

4

PREMIUM INSIGHTS

45

5

MARKET OVERVIEW

UAV LiDAR growth driven by 3D imaging demand, smart cities, and autonomous vehicle integration.

48

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

Rising adoption of UAV LiDAR systems to capture accurate evaluation data

5.2.1.2

Surging demand for 3D imaging solutions

5.2.1.3

Growing number of smart cities and infrastructure development projects

5.2.1.4

Rising deployment of 4D LiDAR technology in autonomous vehicles

5.2.1.5

Increasing enforcement of regulations related to commercial drone adoption in highway construction applications

5.2.2

RESTRAINTS

5.2.2.1

Safety threats associated with UAVs and autonomous vehicles

5.2.2.2

Availability of low-cost and lightweight alternatives

5.2.2.3

High testing, engineering, and calibration costs

5.2.3

OPPORTUNITIES

5.2.3.1

Growing investments in ADAS systems by automotive giants

5.2.3.2

Increasing development of quantum dot detectors

5.2.3.3

Rising popularity of compact and cost-effective flash LiDAR

5.2.3.4

Developing advanced geospatial solutions

5.2.3.5

Increasing reliance on drones to gather key analytic data

5.2.4

CHALLENGES

5.2.4.1

High cost of post-processing LiDAR software

5.2.4.2

Complexities related to miniaturized LiDAR sensing

5.3

VALUE CHAIN ANALYSIS

5.3.1

RESEARCH, DESIGN, AND DEVELOPMENT

5.3.2

RAW MATERIAL SUPPLY

5.3.3

LIDAR COMPONENT MANUFACTURING

5.3.4

SYSTEM INTEGRATION

5.3.5

SUPPLY AND DISTRIBUTION

5.3.6

END-USE APPLICATION

5.4

ECOSYSTEM/MARKET MAP

5.5

PRICING ANALYSIS

5.5.1

AVERAGE SELLING PRICE, BY KEY PLAYER, 2024

5.5.2

AVERAGE SELLING PRICE, BY REGION

5.6

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.7

TECHNOLOGY ANALYSIS

5.7.1

KEY TECHNOLOGY

5.7.1.1

Frequency-modulated continuous-wave LiDAR

5.7.1.2

Photon-counting LiDAR

5.7.1.3

Multi-wavelength LiDAR

5.7.2

ADJACENT TECHNOLOGY

5.7.2.1

Metamaterials

5.7.2.2

In-car LiDAR

5.7.2.3

Artificial intelligence (AI) and machine learning (ML)

5.7.3

COMPLEMENTARY TECHNOLOGIES

5.7.3.1

Sensor suite

5.7.3.2

Flash LiDAR technology

5.8

PORTER’S FIVE FORCES ANALYSIS

5.8.1

THREAT OF NEW ENTRANTS

5.8.2

THREAT OF SUBSTITUTES

5.8.3

BARGAINING POWER OF SUPPLIERS

5.8.4

BARGAINING POWER OF BUYERS

5.8.5

INTENSITY OF COMPETITIVE RIVALRY

5.9

CASE STUDY ANALYSIS

5.9.1

VISIMIND PARTNERS WITH VELODYNE LIDAR TO INCREASE SAFETY AND SECURE DATA RELATED TO ENERGY DISTRIBUTION

5.9.2

DRONE TECHNOLOGIES ADOPTS TRIMBLE INC.’S LIDAR SENSORS FOR TERRAIN MAPPING

5.9.3

TS ENGINEERING PERFORMS HIGHWAY AERIAL MAPPING WITH TRUEVIEW 535 AND LP360 PROCESSING SOFTWARE

5.9.4

CSX TRANSPORTATION UTILIZES PHOENIX LIDAR SCOUT SYSTEMS FOR RAILROAD SURVEYING

5.9.5

MEASUREMENT SCIENCES INC. IMPLEMENTS LIDAR IN PIPELINE SURVEYS TO MAP LARGE VEGETATED AREAS EFFICIENTLY

5.10

INVESTMENT AND FUNDING SCENARIO

5.11

TARIFF AND REGULATORY LANDSCAPE

5.11.1

REGULATIONS

5.11.1.1

Restriction of Hazardous Substances (RoHs) Directive

5.11.1.2

General Data Protection Regulation (GDPR)

5.11.1.3

Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH)

5.11.1.4

Import–export laws

5.11.2

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.12

TRADE ANALYSIS

5.12.1

IMPORT SCENARIO (HS CODE 901320)

5.12.2

EXPORT SCENARIO (HS CODE 901320)

5.13

PATENT ANALYSIS

5.14

KEY CONFERENCES AND EVENTS, 2025–2026

5.15

KEY STAKEHOLDERS AND BUYING PROCESS

5.15.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2

BUYING CRITERIA

5.16

IMPACT OF AI ON LIDAR MARKET

5.17

TRUMP TARIFF IMPACT ON LIDAR MARKET

5.17.1

INTRODUCTION

5.18

KEY TARIFF RATES

5.19

PRICE IMPACT ANALYSIS

5.20

IMPACT ON VARIOUS REGIONS

5.20.1

US

5.20.2

EUROPE

5.20.3

ASIA PACIFIC

5.21

END-USE INDUSTRY-LEVEL IMPACT

6

LIDAR MARKET, BY TECHNOLOGY

Market Size & Growth Rate Forecast Analysis

83

6.1

INTRODUCTION

6.2

2D

6.3

3D

6.4

4D

7

LIDAR MARKET, BY INSTALLATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 32 Data Tables

85

7.1

INTRODUCTION

7.2

AIRBORNE

7.2.1

TOPOGRAPHIC

7.2.1.1

Topographic LiDAR unlocks precision terrain intelligence, fueling market expansion

7.2.2

BATHYMETRIC LIDAR

7.2.2.1

Development of airborne bathymetric LiDAR systems to map coastal zones to contribute to market growth

7.3

GROUND-BASED

7.3.1

MOBILE

7.3.1.1

Deployment of mobile LiDAR technology in corridor mapping and meteorology applications to fuel segmental growth

7.3.2

STATIC

7.3.2.1

Utilization of static LiDAR in engineering and exploration to accelerate segmental growth

8

LIDAR MARKET, BY TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 6 Data Tables

101

8.1

INTRODUCTION

8.2

MECHANICAL

8.2.1

MECHANICAL LIDAR-ENABLED ENVIRONMENTAL MAPPING TO ACCELERATE MARKET EXPANSION

8.3

SOLID STATE

8.3.1

SOLID-STATE LIDAR GAINS TRACTION WITH SUPERIOR SHOCK AND VIBRATION RESISTANCE

9

LIDAR MARKET, BY RANGE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

106

9.1

INTRODUCTION

9.2

SHORT (0–200 M)

9.2.1

ADOPTION OF SHORT-RANGE LIDAR TO AUTOMATE INDUSTRIAL OBJECT PROXIMITY SENSING TO BOOST SEGMENTAL GROWTH

9.3

MEDIUM (200–500 M)

9.3.1

IMPLEMENTATION OF MEDIUM-RANGE LIDAR TO NAVIGATE AUTOMATED GUIDED VEHICLES TO ACCELERATE SEGMENTAL GROWTH

9.4

LONG (ABOVE 500 M)

9.4.1

EMPLOYMENT OF LONG-RANGE LIDAR COMPONENTS FOR WIDE-AREA MAPPING TO FOSTER SEGMENTAL GROWTH

10

LIDAR MARKET, BY SERVICE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

110

10.1

INTRODUCTION

10.2

AERIAL SURVEYING

10.2.1

RELIANCE ON AERIAL LIDAR SURVEYS TO PROVIDE ACCURATE 3D MAPPING OF TERRAINS AND LANDSCAPES TO PROPEL MARKET

10.3

ASSET MANAGEMENT

10.3.1

ADOPTION OF LIDAR IN TRANSMISSION LINE AND ROAD MAPPING PROJECTS TO FUEL SEGMENTAL GROWTH

10.4

GEOGRAPHIC INFORMATION SYSTEM (GIS) SERVICES

10.4.1

CAPABILITY TO INTEGRATE LIDAR WITH GEOSPATIAL DATA TO AUGMENT DEMAND

10.5

GROUND-BASED SURVEYING

10.5.1

USE OF GROUND-BASED MONITORING SYSTEMS IN HIGH-VOLUME TRAFFIC STUDIES TO DRIVE SEGMENTAL GROWTH

10.6

OTHER SERVICES

11

LIDAR MARKET, BY END-USE APPLICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 30 Data Tables

115

11.1

INTRODUCTION

11.2

CORRIDOR MAPPING

11.2.1

ROADWAYS

11.2.1.1

Reliance on LiDAR technology to determine length of roads and terrain structure to foster segmental growth

11.2.2

RAILWAYS

11.2.2.1

Use of LiDAR systems as cost-effective solution to map complete railway networks to propel market

11.2.3

OTHER CORRIDOR MAPPING TYPES

11.3

ENGINEERING

11.3.1

RELIANCE ON LIDAR-BASED SURVEY TO EXTRACT DATA RELATED TO GROUND ELEVATION TO CONTRIBUTE TO SEGMENTAL GROWTH

11.4

ENVIRONMENT

11.4.1

FOREST MANAGEMENT

11.4.1.1

Adoption of LiDAR technology to detect deforestation and forest loss to fuel segmental growth

11.4.2

COASTLINE MANAGEMENT

11.4.2.1

Utilization of LiDAR systems to create accurate topographic maps of coastal areas to accelerate segmental growth

11.4.3

POLLUTION MODELING

11.4.3.1

Implementation of LiDAR systems to determine carbon absorption in forests to drive market

11.4.4

AGRICULTURE MAPPING

11.4.4.1

Use of LiDAR systems to increase crop viability and mapping to fuel segmental growth

11.4.5

WIND FARM

11.4.5.1

Deployment of LiDAR technology to detect wind direction to accelerate segmental growth

11.4.6

PRECISION FORESTRY

11.4.6.1

Utilization of LiDAR systems to make data-driven decisions related to forest dynamics to boost segmental growth

11.5

ADAS & DRIVERLESS CARS

11.5.1

RELIANCE ON LIDAR TO ENSURE ACCURATE OBJECT DETECTION AND RECOGNITION BY ADAS & DRIVERLESS CARS TO PROPEL MARKET

11.6

EXPLORATION

11.6.1

OIL & GAS

11.6.1.1

Adoption of LiDAR photography solutions to identify threats along oil & gas pipelines to augment segmental growth

11.6.2

MINING

11.6.2.1

Utilization of LiDAR solutions to provide exact mining location to drive market

11.7

URBAN PLANNING

11.7.1

ADOPTION OF LIDAR TO OBTAIN DIGITAL MODELS OF CITIES AND DIGITAL SURFACE TO FUEL SEGMENTAL GROWTH

11.8

CARTOGRAPHY

11.8.1

UTILIZATION OF LIDAR COMPONENTS TO PRODUCE HIGH-RESOLUTION CONTOUR MAPS TO FOSTER SEGMENTAL GROWTH

11.9

METEOROLOGY

11.9.1

IMPLEMENTATION OF LIDAR TECHNOLOGY TO GAIN ACCURATE DATA ON ATMOSPHERIC GASES TO CONTRIBUTE TO SEGMENTAL GROWTH

11.10

OTHER END-USE APPLICATIONS

12

LIDAR MARKET, BY REGION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 80 Data Tables

136

12.1

INTRODUCTION

12.2

NORTH AMERICA

12.2.1

MACROECONOMIC OUTLOOK IN NORTH AMERICA

12.2.2

US

12.2.2.1

Surging demand for drones for corridor mapping applications to drive market

12.2.3

CANADA

12.2.3.1

Rising development of spatial data infrastructure to contribute to market growth

12.2.4

MEXICO

12.2.4.1

Increasing emphasis on examining ancient archeological sites to foster market growth

12.3

EUROPE

12.3.1

MACROECONOMIC OUTLOOK IN EUROPE

12.3.2

UK

12.3.2.1

Rising production of cost-effective terrain maps to assess flood risks to drive market

12.3.3

GERMANY

12.3.3.1

Increasing R&D of advanced automotive technologies to fuel market growth

12.3.4

FRANCE

12.3.4.1

Rising demand for innovative technologies for corridor mapping to boost market growth

12.3.5

ITALY

12.3.5.1

Growing need for infrastructure monitoring and coastline protection to augment demand for LiDAR components

12.3.6

SPAIN

12.3.6.1

Regulatory backing and cross-industry adoption to propel LiDAR market growth in Spain

12.3.7

POLAND

12.3.7.1

Government modernization initiatives and industrial automation to boost LiDAR market in Poland

12.3.8

NORDICS

12.3.8.1

Sustainability goals and advanced mobility projects fuel LiDAR growth in Nordic region

12.3.9

REST OF EUROPE

12.4

ASIA PACIFIC

12.4.1

MACROECONOMIC OUTLOOK IN ASIA PACIFIC

12.4.2

CHINA

12.4.2.1

Increasing development of advanced drone technologies to drive market

12.4.3

JAPAN

12.4.3.1

Growing demand for autonomous vehicles to fuel market

12.4.4

SOUTH KOREA

12.4.4.1

Rising emphasis on optimizing factory to accelerate market growth

12.4.5

INDIA

12.4.5.1

Increasing formulation of mandates on LiDAR adoption during highway construction to contribute to market growth

12.4.6

AUSTRALIA

12.4.6.1

Government-backed mapping and climate efforts to advance LiDAR adoption in Australia

12.4.7

INDONESIA

12.4.7.1

Infrastructure growth and urban planning to spur LiDAR demand in Indonesia

12.4.8

MALAYSIA

12.4.8.1

Smart nation ambitions and environmental policies to drive LiDAR growth in Malaysia

12.4.9

THAILAND

12.4.9.1

Tourism and urban expansion initiatives to encourage LiDAR usage in Thailand

12.4.10

VIETNAM

12.4.10.1

Disaster management and coastal planning to propel LiDAR market in Vietnam

12.4.11

REST OF ASIA PACIFIC

12.5

ROW

12.5.1

MACROECONOMIC OUTLOOK IN ROW

12.5.2

SOUTH AMERICA

12.5.2.1

Topographic mapping and environmental monitoring to accelerate LiDAR growth in South America

12.5.3

MIDDLE EAST

12.5.3.1

Smart infrastructure and sustainability goals to drive LiDAR demand in Middle East

12.5.3.2

Bahrain

12.5.3.3

Kuwait

12.5.3.4

Oman

12.5.3.5

Qatar

12.5.3.6

Saudi Arabia

12.5.3.7

United Arab Emirates (UAE)

12.5.3.8

Rest of Middle East

12.5.4

AFRICA

12.5.4.1

South Africa

12.5.4.2

Other African countries

13

COMPETITIVE LANDSCAPE

Discover top strategies and emerging leaders reshaping market share and valuations in 2024.

176

13.1

OVERVIEW

13.2

KEY PLAYER STRATEGIES/RIGHT TO WIN

13.3

REVENUE ANALYSIS, 2021–2024

13.4

MARKET SHARE ANALYSIS, 2024

13.5

COMPANY VALUATION AND FINANCIAL METRICS

13.6

BRAND/PRODUCT COMPARISON

13.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

13.7.1

STARS

13.7.2

EMERGING LEADERS

13.7.3

PERVASIVE PLAYERS

13.7.4

PARTICIPANTS

13.7.4.1

Company footprint

13.7.4.2

Company overall footprint

13.7.4.3

Company region footprint

13.7.4.4

Company end-use application footprint

13.7.4.5

Company installation footprint

13.8

START-UP/SME EVALUATION MATRIX, 2024

13.8.1

PROGRESSIVE COMPANIES

13.8.2

RESPONSIVE COMPANIES

13.8.3

DYNAMIC COMPANIES

13.8.4

STARTING BLOCKS

13.8.5

COMPETITIVE BENCHMARKING

13.8.5.1

Detailed list of key startups/SMEs

13.8.5.2

Competitive benchmarking of key startups/SMES

13.9

COMPETITIVE SCENARIO

13.9.1

PRODUCT LAUNCHES

13.9.2

DEALS

14

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

191

14.1

KEY PLAYERS

14.1.1

ROBOSENSE

14.1.1.1

Business overview

14.1.1.2

Products/Solutions/Services offered

14.1.1.3

Recent developments

14.1.1.4

Deals

14.1.1.5

MnM view

14.1.2

HESAI GROUP

14.1.3

LUMINAR TECHNOLOGIES, INC.

14.1.4

OUSTER, INC.

14.1.5

SICK AG

14.1.6

LEICA GEOSYSTEMS AG

14.1.7

TRIMBLE INC.

14.1.8

TELEDYNE OPTECH

14.1.9

FARO

14.1.10

RIEGL LASER MEASUREMENT SYSTEMS GMBH

14.1.11

NV5 GEOSPATIA

14.1.12

SURESTAR

14.1.13

YELLOWSCAN

14.2

OTHER PLAYERS

14.2.1

PREACT TECHNOLOGIES

14.2.2

OPSYS TECHNOLOGIES

14.2.3

GEOKNO

14.2.4

PHOENIX LIDAR SYSTEMS

14.2.5

QUANERGY SYSTEMS, INC.

14.2.6

INNOVIZ TECHNOLOGIES LTD

14.2.7

LEOSPHERE

14.2.8

WAYMO LLC

14.2.9

VALEO

14.2.10

NEPTEC TECHNOLOGIES CORP.

14.2.11

ZX LIDARS

14.2.12

LIVOX

14.2.13

ROUTESCENE

14.2.14

BLICKFELD GMBH

14.2.15

SABRE ADVANCED 3D SURVEYING SYSTEMS LTD

14.2.16

LEISHEN INTELLIGENT SYSTEM

15

APPENDIX

255

15.1

DISCUSSION GUIDE

15.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

15.3

CUSTOMIZATION OPTIONS

15.4

RELATED REPORTS

15.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

PARAMETERS INCLUDED AND EXCLUDED

TABLE 2

LIST OF INDUSTRY EXPERTS

TABLE 3

ASSUMPTIONS CONSIDERED DURING RESEARCH

TABLE 4

COMPANIES AND THEIR ROLES IN LIDAR ECOSYSTEM

TABLE 5

AVERAGE SELLING PRICE, BY KEY PLAYER, 2024 (USD)

TABLE 6

AVERAGE SELLING PRICE TREND, BY REGION, 2021–2024 (USD)

TABLE 7

PORTER’S FIVE FORCES: IMPACT ANALYSIS

TABLE 8

MFN TARIFFS FOR LIDAR COMPONENTS EXPORTED BY US

TABLE 9

MFN TARIFFS FOR LIDAR COMPONENTS EXPORTED BY CHINA

TABLE 10

NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 11

EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 12

ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 13

ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 14

IMPORT DATA FOR HS CODE 901320-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD THOUSAND)

TABLE 15

EXPORT DATA FOR HS CODE 901320-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD THOUSAND)

TABLE 16

PATENTS RELATED TO LIDAR

TABLE 17

LIDAR MARKET: LIST OF CONFERENCES AND EVENTS, 2025–2026

TABLE 18

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE APPLICATIONS (%)

TABLE 19

KEY BUYING CRITERIA FOR TOP THREE END-USE APPLICATIONS

TABLE 20

US ADJUSTED RECIPROCAL TARIFF RATES

TABLE 21

LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 22

LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 23

AIRBORNE: LIDAR MARKET, BY RANGE, 2021–2024 (USD MILLION)

TABLE 24

AIRBORNE: LIDAR MARKET, BY RANGE, 2025–2030 (USD MILLION)

TABLE 25

AIRBORNE: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 26

AIRBORNE: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 27

NORTH AMERICA: AIRBORNE LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 28

NORTH AMERICA: AIRBORNE LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 29

EUROPE: AIRBORNE LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 30

EUROPE: AIRBORNE LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 31

ASIA PACIFIC: AIRBORNE LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 32

ASIA PACIFIC: AIRBORNE LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 33

ROW: AIRBORNE LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 34

ROW: AIRBORNE LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 35

AIRBORNE: LIDAR MARKET, BY AIRCRAFT TYPE, 2021–2024 (USD MILLION)

TABLE 36

AIRBORNE: LIDAR MARKET, BY AIRCRAFT TYPE, 2025–2030 (USD MILLION)

TABLE 37

AIRBORNE: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 38

AIRBORNE: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 39

GROUND-BASED: LIDAR MARKET, BY RANGE, 2021–2024 (USD MILLION)

TABLE 40

GROUND-BASED: LIDAR MARKET, BY RANGE, 2025–2030 (USD MILLION)

TABLE 41

GROUND-BASED: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 42

GROUND-BASED: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 43

NORTH AMERICA: GROUND-BASED LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 44

NORTH AMERICA: GROUND-BASED LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 45

EUROPE: GROUND-BASED LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 46

EUROPE: GROUND-BASED LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 47

ASIA PACIFIC: GROUND-BASED LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 48

ASIA PACIFIC: GROUND-BASED LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 49

ROW: GROUND-BASED LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 50

ROW: GROUND-BASED LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 51

GROUND-BASED: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 52

GROUND-BASED: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 53

LIDAR MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 54

LIDAR MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 55

MECHANICAL LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 56

MECHANICAL LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 57

SOLID-STATE LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 58

SOLID-STATE LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 59

LIDAR MARKET, BY RANGE, 2021–2024 (USD MILLION)

TABLE 60

LIDAR MARKET, BY RANGE, 2025–2030 (USD MILLION)

TABLE 61

LIDAR MARKET, BY SERVICE, 2021–2024 (USD MILLION)

TABLE 62

LIDAR MARKET, BY SERVICE, 2025–2030 (USD MILLION)

TABLE 63

LIDAR MARKET: BY END-USE APPLICATION, 2021–2024 (USD MILLION)

TABLE 64

LIDAR MARKET: BY END-USE APPLICATION, 2025–2030 (USD MILLION)

TABLE 65

CORRIDOR MAPPING: LIDAR MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 66

CORRIDOR MAPPING: LIDAR MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 67

CORRIDOR MAPPING: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 68

CORRIDOR MAPPING: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 69

ENGINEERING: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 70

ENGINEERING: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 71

ENVIRONMENT: LIDAR MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 72

ENVIRONMENT: LIDAR MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 73

ENVIRONMENT: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 74

ENVIRONMENT: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 75

LIDAR MARKET FOR ADAS & DRIVERLESS CARS APPLICATION, BY TYPE, 2021–2024 (THOUSAND UNITS)

TABLE 76

LIDAR MARKET FOR ADAS & DRIVERLESS CARS APPLICATION, BY TYPE, 2025–2030 (THOUSAND UNITS)

TABLE 77

ADAS & DRIVERLESS CARS: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 78

ADAS & DRIVERLESS CARS: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 79

EXPLORATION: LIDAR MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 80

EXPLORATION: LIDAR MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 81

EXPLORATION: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 82

EXPLORATION: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 83

URBAN PLANNING: LIDAR MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 84

URBAN PLANNING: LIDAR MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 85

URBAN PLANNING: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 86

URBAN PLANNING: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 87

CARTOGRAPHY: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 88

CARTOGRAPHY: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 89

METEOROLOGY: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 90

METEOROLOGY: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 91

OTHER END-USE APPLICATIONS: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 92

OTHER END-USE APPLICATIONS: LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 93

LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 94

LIDAR MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 95

NORTH AMERICA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 96

NORTH AMERICA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 97

NORTH AMERICA: LIDAR MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 98

NORTH AMERICA: LIDAR MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 99

NORTH AMERICA: LIDAR MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 100

NORTH AMERICA: LIDAR MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 101

NORTH AMERICA: LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 102

NORTH AMERICA: LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 103

US: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 104

US: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 105

CANADA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 106

CANADA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 107

MEXICO: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 108

MEXICO: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 109

EUROPE: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 110

EUROPE: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 111

EUROPE: LIDAR MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 112

EUROPE: LIDAR MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 113

EUROPE: LIDAR MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 114

EUROPE: LIDAR MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 115

EUROPE: LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 116

EUROPE: LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 117

UK: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 118

UK: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 119

GERMANY: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 120

GERMANY: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 121

FRANCE: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 122

FRANCE: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 123

ITALY: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 124

ITALY: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 125

SPAIN: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 126

SPAIN: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 127

POLAND: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 128

POLAND: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 129

NORDICS: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 130

NORDICS: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 131

REST OF EUROPE: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 132

REST OF EUROPE: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 133

ASIA PACIFIC: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 134

ASIA PACIFIC: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 135

ASIA PACIFIC: LIDAR MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 136

ASIA PACIFIC: LIDAR MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 137

ASIA PACIFIC: LIDAR MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 138

ASIA PACIFIC: LIDAR MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 139

ASIA PACIFIC: LIDAR MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 140

ASIA PACIFIC: LIDAR MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 141

CHINA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 142

CHINA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 143

JAPAN: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 144

JAPAN: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 145

SOUTH KOREA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 146

SOUTH KOREA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 147

INDIA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 148

INDIA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 149

AUSTRALIA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 150

AUSTRALIA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 151

INDONESIA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 152

INDONESIA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 153

MALAYSIA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 154

MALAYSIA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 155

THAILAND: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 156

THAILAND: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 157

VIETNAM: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 158

VIETNAM: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 159

REST OF ASIA PACIFIC: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 160

REST OF ASIA PACIFIC: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 161

ROW: LIDAR MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 162

ROW: LIDAR MARKET, BY REGION 2025–2030 (USD MILLION)

TABLE 163

ROW: LIDAR MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 164

ROW: LIDAR MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 165

SOUTH AMERICA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 166

SOUTH AMERICA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 167

MIDDLE EAST: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 168

MIDDLE EAST: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 169

AFRICA: LIDAR MARKET, BY INSTALLATION, 2021–2024 (USD MILLION)

TABLE 170

AFRICA: LIDAR MARKET, BY INSTALLATION, 2025–2030 (USD MILLION)

TABLE 171

ROW: LIDAR MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 172

ROW: LIDAR MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 173

KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2021–JUNE 2025

TABLE 174

LIDAR MARKET: DEGREE OF COMPETITION, 2024

TABLE 175

OVERALL COMPANY FOOTPRINT

TABLE 176

COMPANY REGION FOOTPRINT

TABLE 177

COMPANY END-USE APPLICATION FOOTPRINT

TABLE 178

COMPANY INSTALLATION FOOTPRINT

TABLE 179

START-UP/SME MATRIX: LIST OF KEY START-UPS/SMES

TABLE 180

LIDAR MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

TABLE 181

LIDAR MARKET: PRODUCT LAUNCHES, JUNE 2021–MARCH 2025

TABLE 182

LIDAR MARKET: DEALS, APRIL 2022–JULY 2025

TABLE 183

ROBOSENSE: COMPANY OVERVIEW

TABLE 184

ROBOSENSE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 185

ROBOSENSE: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 186

ROBOSENSE: DEALS

TABLE 187

ROBOSENSE: OTHER DEVELOPMENTS

TABLE 188

HESAI GROUP: COMPANY OVERVIEW

TABLE 189

HESAI GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 190

HESAI GROUP: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 191

HESAI GROUP: DEALS

TABLE 192

HESAI GROUP: OTHER DEVELOPMENTS

TABLE 193

LUMINAR TECHNOLOGIES, INC.: COMPANY OVERVIEW

TABLE 194

LUMINAR TECHNOLOGIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 195

LUMINAR TECHNOLOGIES, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 196

LUMINAR TECHNOLOGIES, INC.: DEALS

TABLE 197

LUMINAR TECHNOLOGIES, INC.: EXPANSIONS

TABLE 198

OUSTER, INC.: COMPANY OVERVIEW

TABLE 199

OUSTER, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 200

OUSTER, INC.: PRODUCT LAUNCHES

TABLE 201

OUSTER, INC.: DEALS

TABLE 202

SICK AG: COMPANY OVERVIEW

TABLE 203

SICK AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 204

SICK AG: PRODUCT LAUNCHES

TABLE 205

SICK AG: DEALS

TABLE 206

LEICA GEOSYSTEMS AG: COMPANY OVERVIEW

TABLE 207

LEICA GEOSYSTEMS AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 208

LEICA GEOSYSTEMS AG: PRODUCT LAUNCHES

TABLE 209

LEICA GEOSYSTEMS AG: DEALS

TABLE 210

TRIMBLE INC.: COMPANY OVERVIEW

TABLE 211

TRIMBLE INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 212

TRIMBLE INC.: PRODUCT LAUNCHES

TABLE 213

TRIMBLE INC.: DEALS

TABLE 214

TELEDYNE OPTECH: COMPANY OVERVIEW

TABLE 215

TELEDYNE OPTECH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 216

TELEDYNE OPTECH: PRODUCT LAUNCHES

TABLE 217

FARO: COMPANY OVERVIEW

TABLE 218

FARO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 219

FARO: PRODUCT LAUNCHES

TABLE 220

FARO: DEALS

TABLE 221

RIEGL LASER MEASUREMENT SYSTEM GMBH: COMPANY OVERVIEW

TABLE 222

RIEGL LASER MEASUREMENT SYSTEM GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 223

RIEGL LASER MEASUREMENT SYSTEM GMBH: PRODUCT LAUNCHES

TABLE 224

RIEGL LASER MEASUREMENT SYSTEM GMBH: DEALS

TABLE 225

NV5 GEOSPATIAL: COMPANY OVERVIEW

TABLE 226

NV5 GEOSPATIAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 227

NV5 GEOSPATIAL: DEALS

TABLE 228

SURESTAR: COMPANY OVERVIEW

TABLE 229

SURESTAR: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 230

SURESTAR: PRODUCT LAUNCHES

TABLE 231

YELLOWSCAN: COMPANY OVERVIEW

TABLE 232

YELLOWSCAN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 233

YELLOWSCAN: PRODUCT LAUNCHES

TABLE 234

YELLOWSCAN: DEALS

TABLE 235

PREACT TECHNOLOGIES: COMPANY OVERVIEW

TABLE 236

OPSYS TECHNOLOGIES: COMPANY OVERVIEW

TABLE 237

GEOKNO: COMPANY OVERVIEW

TABLE 238

PHOENIX LIDAR SYSTEMS: COMPANY OVERVIEW

TABLE 239

QUANERGY SYSTEMS, INC.: COMPANY OVERVIEW

TABLE 240

INNOVIZ TECHNOLOGIES LTD: COMPANY OVERVIEW

TABLE 241

LEOSPHERE: COMPANY OVERVIEW

TABLE 242

WAYMO LLC: COMPANY OVERVIEW

TABLE 243

VALEO: COMPANY OVERVIEW

TABLE 244

NEPTEC TECHNOLOGIES CORP.: COMPANY OVERVIEW

TABLE 245

ZX LIDARS: COMPANY OVERVIEW

TABLE 246

LIVOX: BUSINESS OVERVIEW

TABLE 247

ROUTESCENE: COMPANY OVERVIEW

TABLE 248

BLICKFELD GMBH: COMPANY OVERVIEW

TABLE 249

SABRE ADVANCED 3D SURVEYING SYSTEMS: COMPANY OVERVIEW

TABLE 250

LEISHEN INTELLIGENT SYSTEM: COMPANY OVERVIEW

LIST OF FIGURES

FIGURE 1

LIDAR MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

LIDAR MARKET: RESEARCH DESIGN

FIGURE 3

DATA CAPTURED THROUGH SECONDARY SOURCES

FIGURE 4

INSIGHTS DERIVED FROM PRIMARY RESEARCH SOURCES

FIGURE 5

LIDAR MARKET SIZE ESTIMATION METHODOLOGY

FIGURE 6

LIDAR MARKET: BOTTOM-UP APPROACH

FIGURE 7

LIDAR MARKET: TOP-DOWN APPROACH

FIGURE 8

DATA TRIANGULATION

FIGURE 9

GROUND-BASED INSTALLATION TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

FIGURE 10

SOLID-STATE LIDAR TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

FIGURE 11

ADAS & DRIVERLESS CARS TO EXHIBIT HIGHEST CAGR BETWEEN 2025 AND 2030

FIGURE 12

NORTH AMERICA ACCOUNTED FOR LARGEST SHARE OF LIDAR MARKET IN 2024

FIGURE 13

INCREASE IN SMART CITY DEVELOPMENT AND INFRASTRUCTURE PROJECTS TO DRIVE LIDAR MARKET

FIGURE 14

MECHANICAL LIDAR TO ACCOUNT FOR LARGER MARKET SHARE IN 2030

FIGURE 15

ADAS & DRIVERLESS CARS APPLICATION TO HOLD LARGEST MARKET SHARE IN 2030

FIGURE 16

GROUND-BASED INSTALLATION AND CHINA HELD LARGEST SHARES OF ASIA PACIFIC LIDAR MARKET IN 2024

FIGURE 17

SOUTH KOREA TO REGISTER HIGHEST CAGR IN LIDAR MARKET DURING FORECAST PERIOD

FIGURE 18

LIDAR MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 19

LIDAR MARKET: DRIVERS AND THEIR IMPACT

FIGURE 20

LIDAR MARKET: RESTRAINTS AND THEIR IMPACT

FIGURE 21

LIDAR MARKET: OPPORTUNITIES AND THEIR IMPACT

FIGURE 22

LIDAR MARKET: CHALLENGES AND THEIR IMPACT

FIGURE 23

LIDAR MARKET: VALUE CHAIN ANALYSIS

FIGURE 24

LIDAR ECOSYSTEM

FIGURE 25

AVERAGE SELLING PRICE, BY KEY PLAYER, 2024 (USD)

FIGURE 26

AVERAGE SELLING PRICE TREND, BY REGION, 2021–2024 (USD)

FIGURE 27

LIDAR MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 28

LIDAR MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 29

INVESTMENT AND FUNDING SCENARIO FOR START-UP COMPANIES

FIGURE 30

IMPORT DATA FOR HS CODE 901320-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024

FIGURE 31

EXPORT DATA FOR HS CODE 901320-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024

FIGURE 32

PATENTS APPLIED AND GRANTED, 2014–2024

FIGURE 33

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE APPLICATIONS

FIGURE 34

KEY BUYING CRITERIA FOR TOP THREE END-USE APPLICATIONS

FIGURE 35

LIDAR MARKET: IMPACT OF AI

FIGURE 36

LIDAR MARKET, BY INSTALLATION

FIGURE 37

GROUND-BASED LIDAR TO HAVE LARGER MARKET SIZE DURING FORECAST PERIOD

FIGURE 38

LIDAR MARKET, BY TYPE

FIGURE 39

MECHANICAL LIDAR TO ACCOUNT FOR LARGER MARKET SHARE IN 2030

FIGURE 40

LIDAR MARKET, BY RANGE

FIGURE 41

SHORT-RANGE (0–200 M) LIDAR TO BE LARGEST SEGMENT OF LIDAR MARKET DURING FORECAST PERIOD

FIGURE 42

LIDAR MARKET, BY SERVICE

FIGURE 43

GEOGRAPHIC INFORMATION SYSTEM (GIS) SERVICES TO WITNESS HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 44

LIDAR MARKET, BY END-USE APPLICATION

FIGURE 45

ADAS & DRIVERLESS CARS APPLICATION TO BE LARGEST SEGMENT OF LIDAR MARKET DURING FORECAST PERIOD

FIGURE 46

LIDAR MARKET, BY REGION

FIGURE 47

NORTH AMERICA: LIDAR MARKET SNAPSHOT

FIGURE 48

EUROPE: LIDAR MARKET SNAPSHOT

FIGURE 49

ASIA PACIFIC: LIDAR MARKET SNAPSHOT

FIGURE 50

LIDRA MARKET: REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2021–2024

FIGURE 51

LIDAR MARKET SHARE ANALYSIS, 2024

FIGURE 52

VALUATION OF KEY PLAYERS IN LIDAR MARKET

FIGURE 53

EV/EBITDA OF KEY PLAYERS

FIGURE 54

BRAND/PRODUCT COMPARISON

FIGURE 55

LIDAR MARKET: COMPANY EVALUATION MATRIX, 2024

FIGURE 56

LIDAR MARKET: COMPANY FOOTPRINT

FIGURE 57

LIDAR MARKET: START-UP/SME EVALUATION MATRIX, 2024

FIGURE 58

ROBOSENSE: COMPANY SNAPSHOT

FIGURE 59

HESAI GROUP: COMPANY SNAPSHOT

FIGURE 60

LUMINAR TECHNOLOGIES, INC.: COMPANY SNAPSHOT

FIGURE 61

OUSTER, INC.: COMPANY SNAPSHOT

FIGURE 62

SICK AG: COMPANY SNAPSHOT

FIGURE 63

TRIMBLE INC.: COMPANY SNAPSHOT

Methodology

The study involved four major activities in estimating the size of the LiDAR market. Exhaustive secondary research was done to collect information on the market, peer market, and parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across value chains through primary research. The bottom-up approach was employed to estimate the overall market size. After that, market breakdown and data triangulation were used to estimate the market size of segments and subsegments.

Secondary Research

In the secondary research process, various sources were used to identify and collect information important for this study. These include annual reports, press releases & investor presentations of companies, white papers, technology journals, and certified publications, articles by recognized authors, directories, and databases.

Secondary research was mainly used to obtain key information about the supply chain of the industry, the total pool of market players, classification of the market according to industry trends to the bottom-most level, regional markets, and key developments from the market and technology-oriented perspectives.

Primary research was also conducted to identify the segmentation types, key players, competitive landscape, and key market dynamics such as drivers, restraints, opportunities, challenges, and industry trends, along with key strategies adopted by players operating in the LiDAR market. Extensive qualitative and quantitative analyses were performed on the complete market engineering process to list key information and insights throughout the report.

Primary Research

Extensive primary research has been conducted after acquiring knowledge about the LiDAR market scenario through secondary research. Several primary interviews have been conducted with experts from both the demand (end users) and supply (LiDAR solution providers) sides across four major geographic regions: North America, Europe, Asia Pacific, and RoW. Approximately 80% and 20% of the primary interviews have been conducted from the supply and demand sides, respectively. These primary data have been collected through questionnaires, emails, and telephone interviews.

Note: The 3 tiers of the companies have been defined based on their total/segmental revenue as of 2024; Tier 1 = >USD 1 billion, Tier 2 = USD 1 billion–USD 500 million, and Tier 3 = USD 500 million. Others includes sales, marketing, and product managers.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

In the complete market engineering process, both the top-down and bottom-up approaches were implemented, along with several data triangulation methods, to estimate and validate the size of the LiDAR market and various other dependent submarkets. Key players in the market were identified through secondary research, and their market share in the respective regions was determined through primary and secondary research. This entire research methodology included the study of annual and financial reports of the top players, as well as interviews with experts (such as CEOs, VPs, directors, and marketing executives) for key insights (quantitative and qualitative).

All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources. All the possible parameters that affect the markets covered in this research study were accounted for, viewed in detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data. This data was consolidated and supplemented with detailed inputs and analysis from MarketsandMarkets and presented in this report.

LiDAR Market : Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall market size from the market size estimation process as explained above, the total market has been split into several segments and subsegments. To complete the overall market engineering process and arrive at the exact statistics for all segments and subsegments, market breakdown and data triangulation procedures have been employed, wherever applicable. The data has been triangulated by studying various factors and trends from both demand and supply sides. Along with this, the market has been validated using top-down and bottom-up approaches.

Market Definition

LiDAR, or light detection and ranging, works on the time of flight principle. The system uses light waves or a light source as a pulsed laser to measure the distance between objects. Measuring distances helps create 3D maps of terrains or earth surfaces that are not visible to the human eye or cannot be created through photogrammetry. The light waves are combined with other data recorded by the system (airborne or ground-based) to generate precise 3D information about the shape and characteristics of the targeted object.

Key Stakeholders

- Senior Management

- End User

- Finance/Procurement Department

- R&D Department

Report Objectives

- To describe, segment, and forecast the overall size of the LiDAR market by type, installation, range, service, end-use application, and region, in terms of value

- To describe and forecast the market size for various segments with regard to four main regions—North America, Europe, Asia Pacific, and the Rest of the World (RoW), in terms of value

- To provide detailed information regarding major factors, such as drivers, restraints, opportunities, and challenges influencing the market growth

- To analyze the supply chain, trends/disruptions impacting customer business, market/ecosystem map, pricing analysis, and regulatory landscape pertaining to the LiDAR market

- To analyze opportunities in the market for stakeholders by identifying the high-growth segments of the market

- To briefly describe the value chain of light detection and ranging (LiDAR) solutions

- To strategically analyze micromarkets1 with respect to individual growth trends, prospects, and contributions to the overall market

- To profile key players and comprehensively analyze their market position in terms of their ranking and core competencies, along with the detailed competitive landscape of the market

- To analyze competitive developments, such as product launches and developments, partnerships, agreements, expansions, acquisitions, contracts, alliances, and research & development (R&D)undertaken in the LiDAR market

- To benchmark market players using the proprietary ‘Company Evaluation Matrix,’ which analyzes market players on various parameters within the broad categories of business strategy excellence and strength of product portfolio

- To analyze the probable impact of the recession on the market

Key Questions Addressed by the Report

What is the current size of the LiDAR Market?

The global LiDAR Market is estimated at around USD 3.27 billion in 2025 and is projected to reach USD 12.79 billion by 2030.

What is the expected growth rate of the LiDAR Market?

The LiDAR Market is expected to grow at a CAGR of 31.3% from 2025 to 2030 due to increasing demand for 3D sensing and mapping technologies.

What are the major growth drivers of the LiDAR Market?

Key drivers include adoption of autonomous vehicles, UAV LiDAR systems, smart infrastructure projects, 3D mapping demand, and environmental monitoring applications.

What are the key trends shaping the LiDAR Market?

Major trends include solid-state LiDAR adoption, AI-based data processing, LiDAR integration in autonomous vehicles, and growth of digital twins and smart cities.

Which region dominates the LiDAR Market?

Asia Pacific is expected to be the fastest-growing region due to infrastructure development, mapping activities, mining, and smart city initiatives.

Which LiDAR installation segment holds a major market share?

Ground-based LiDAR holds a significant market share due to increasing use in surveying, corridor mapping, and engineering applications.

Which application segment is driving LiDAR Market growth?

The ADAS and driverless cars segment is a major growth contributor due to increasing demand for accurate sensing and vehicle safety technologies.

Which industries are adopting LiDAR technology?

Major industries include automotive, construction, aerospace, defense, mining, agriculture, environmental monitoring, and surveying & mapping.

Who are the major companies in the LiDAR Market?

Leading companies include Hesai Group, RoboSense Technology Co., Ltd., SICK AG, Luminar Technologies, and Trimble Inc..

What does the LiDAR Market report analyze?

The report covers market size, forecast, installation type, technology, range, services, applications, end-use industries, regional analysis, competitive landscape, and growth opportunities through 2030.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the LiDAR Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

- US LiDAR Market

- Canada LiDAR Market

- Mexico LiDAR Market

- UK LiDAR Market

- Germany LiDAR Market

- France LiDAR Market

- Italy LiDAR Market

- Spain LiDAR Market

- Poland LiDAR Market

- China LiDAR Market

- Japan LiDAR Market

- South Korea LiDAR Market

- India LiDAR Market

- Australia LiDAR Market

- Indonesia LiDAR Market

- Malaysia LiDAR Market

- Thailand LiDAR Market

- Vietnam LiDAR Market

Growth opportunities and latent adjacency in LiDAR Market

Sunghun

Mar, 2016

Do you have technical report to focusing the components of 3D laser scanner for autonomous vehicle? If you have please send me the sample file. I'm little bit confusing with your reports. In your report contents, the meaning of LIDAR is little bit different as my understanding. Eventually the LIDAR components section, the components include GPS, Navigation. It's not only LIDAR sensor, kind of full system for autonomous vehicle. So, the other reports also mention the LIDAR components are same as yours. I think the 3D Laser scanner is mostly same as what I want to searching. So, I need not only market survey, but also technology reports..

Martin

Mar, 2019

We are looking to buy the LiDAR report and wanted to take a look at the sample to get a feeling on what we can expect..

Sanmeet

Nov, 2017

I am doing a school project on LIDAR and need a sample of the report to look at the potential market size..

Cameron

Apr, 2026

Which end-use industries are expected to dominate the LiDAR market by 2030, and how are applications such as urban planning, mining, agriculture, and infrastructure development evolving?.

Jason

Apr, 2026

What are the major factors driving the growth of the global LiDAR market, and how are advancements in 3D imaging, smart city projects, and autonomous vehicles contributing to this expansion?.

Alejandro

Apr, 2017

I am interested in the following topics Lidar bathymetry & topography services application mapping, cartography, exploration, urban planning..

Robbie

Feb, 2018

I am interested in knowing the key players in the LiDAR market specifically catering in the US..

Marcus

Aug, 2019

We are looking to quickly get smart on the LiDAR space to understand companies and their growth trajectory. .

Harris

Aug, 2015

I am interested to speak with the team that helped put together this report to explore the possibility to establish a relationship for future collaboration on such reports in the LiDAR market. It would be of mutual benefit to combine the views of the broader market with that of the leading 3-D real-time LiDAR manufacture..

Taylor

Nov, 2013

Hoping to see a bit more than what is on the website. Wanting to know if information has been gathered on LiDAR service providers, not just equipment. Also LiDAR systems now operate in the 500 kHz range (article says as high as 100 kHz)..

User

Sep, 2019

ADAS and Autonomus vehicles are expected to disrrupt the solid-state LiDAR market. What are the other applications that would impact our revenues? Who are the leading manufacturers for solid-state LiDAR? .

andy

Sep, 2019

I want the latest news about materials solutions to the new components on vehicles, such as ADAS sensors, integration of parts, HUD, future interior designs. .

Mateusz

Aug, 2015

I am interested in the following sections Market Analysis, By Application (Page No. - 79) Premium Insights (Page No. - 31) Market Overview (Page No. - 37) Industry Trends (Page No. - 46) Airborne LiDAR.

greg

May, 2015

We are interested only in the applications part of the LiDAR report. Do you provide it separately?.

Jake

Oct, 2017

Specifically interested in ADAS & Driverless car markets for LIDAR and its future growth. How is that market distinct from the other projected markets? .

Roberto

Dec, 2017

I am interested in offering my knowledge in the fields I have experience, such as Sales Manager, Trainer and Technology Transfer in Geomatics tools like Lidar. I am also interested in knowing about how does the Lidar Market work in some regions of the world and the latest updates on this interesting field..

User

Sep, 2019

Will government mandates really help in achieving a significant position in the market? What would be impact of government mandates in long term like after 3 years and 5 years and its impact on the use of drones in next 3-5 years? .

Zheenbek

Nov, 2013

We would like to conduct field surveys of mining areas, tailing sites and land use/cover analysis. We are interested in price of LIDAR's..

Zheenbek

Nov, 2013

We would like to conduct field surveys of mining areas, tailing sites and land use/cover analysis. We are interested in price of LIDAR's..

Tyson

Oct, 2014

Can you tell us the Lidar market size in 2014? We need to know if it's worth is to investigate this market more and purchase the full report..

User

Sep, 2019

Ground-based LiDAR being the dominant LiDAR type does airborne LiDAR have a significant penitration in LiDAR offerings? Do you have any estimations for use of airborne LiDAR in next 3 to 5 years? .

YSK

Jul, 2020