The study involved two major segments in estimating the current size of the savory ingredients market. Exhaustive secondary research was done to collect information on the market, peer, and parent markets. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation were used to estimate the market size of segments and subsegments.

Secondary Research

This research study involved the extensive use of secondary sources—directories and databases such as Bloomberg Businessweek and Factiva—to identify and collect information useful for a technical, market-oriented, and commercial study of the savory ingredients market.

In the secondary research process, various sources such as annual reports, press releases & investor presentations of companies, white papers, food journals, certified publications, articles from recognized authors, directories, and databases, were referred to identify and collect information.

Secondary research was mainly used to obtain key information about the industry’s supply chain, the total pool of key players, and market classification and segmentation as per the industry trends to the bottom-most level, regional markets, and key developments from both market- and technology-oriented perspectives.

Primary Research

Extensive primary research was conducted after obtaining information regarding the savory ingredients market scenario through secondary research. Several primary interviews were conducted with market experts from both the demand and supply sides across major countries of North America, Europe, Asia Pacific, South America, and the Rest of the World. Primary data was collected through questionnaires, emails, and telephonic interviews. The primary sources from the supply side included various industry experts, such as Chief X Officers (CXOs), Vice Presidents (VPs), Directors, from business development, marketing, research, and development teams, and related key executives from distributors, and key opinion leaders. Primary interviews were conducted to gather insights such as market statistics, data on revenue collected from the products, market breakdowns, market size estimations, market forecasting, and data triangulation. Primary research also helped in understanding the various trends related to savory ingredients type, form, origin, application, and region. Stakeholders from the demand side, such as meat products manufacturers who use the savory ingredients were interviewed to understand the buyer’s perspective on the suppliers, products, and their current usage of savory ingredients and the outlook of their business which will affect the overall market.

To know about the assumptions considered for the study, download the pdf brochure

|

COMPANY NAME

|

designation

|

|

Ajinomoto Co., Inc. (Japan)

|

Regional Sales Manager

|

|

Kerry Group plc. (Ireland)

|

Marketing Manager

|

|

ADM (US)

|

General Manager

|

|

Tate & Lyle (UK)

|

Head of Export Department

|

|

AngelYeast Co., Ltd. (China)

|

Sales Manager

|

|

Cargill, Incorporated (US)

|

Sales Executive

|

Market Size Estimation

Both the top-down and bottom-up approaches were used to estimate and validate the total market size. These approaches were also used to estimate the size of various dependent submarkets. The research methodology used to estimate the market size includes the following:

-

The key players in the industry and markets were identified through extensive secondary research.

-

All shares, splits, and breakdowns were determined using secondary sources and verified through primary sources.

-

All possible parameters that affect the markets covered in this research study were accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data.

-

The research included the study of reports, reviews, and newsletters of top market players, along with extensive interviews for opinions from leaders, such as CEOs, directors, and marketing executives.

Global Savory Ingredients Market: Bottom-Up Approach.

To know about the assumptions considered for the study, Request for Free Sample Report

Global Savory Ingredients Market: Top-Down Approach.

Data Triangulation

After arriving at the overall market size from the estimation process explained above, the total market was split into several segments and subsegments. To estimate the overall savory ingredients market and arrive at the exact statistics for all segments and subsegments, data triangulation and market breakdown procedures were employed, wherever applicable. The data was triangulated by studying various factors and trends from the demand and supply sides. Along with this, the market size was validated using both the top-down and bottom-up approaches.

Market Definition

Savory ingredients are flavoring agents that do not have an individual flavor of their own but enhance the overall taste of food or feed products. Savory, also known as umami flavor, ingredients used in the form of powders, liquids, pastes, or sprays, are neither sour, bitter, sweet, or salty. Still, they have a significant impact on improving the flavor and aroma of the food products.

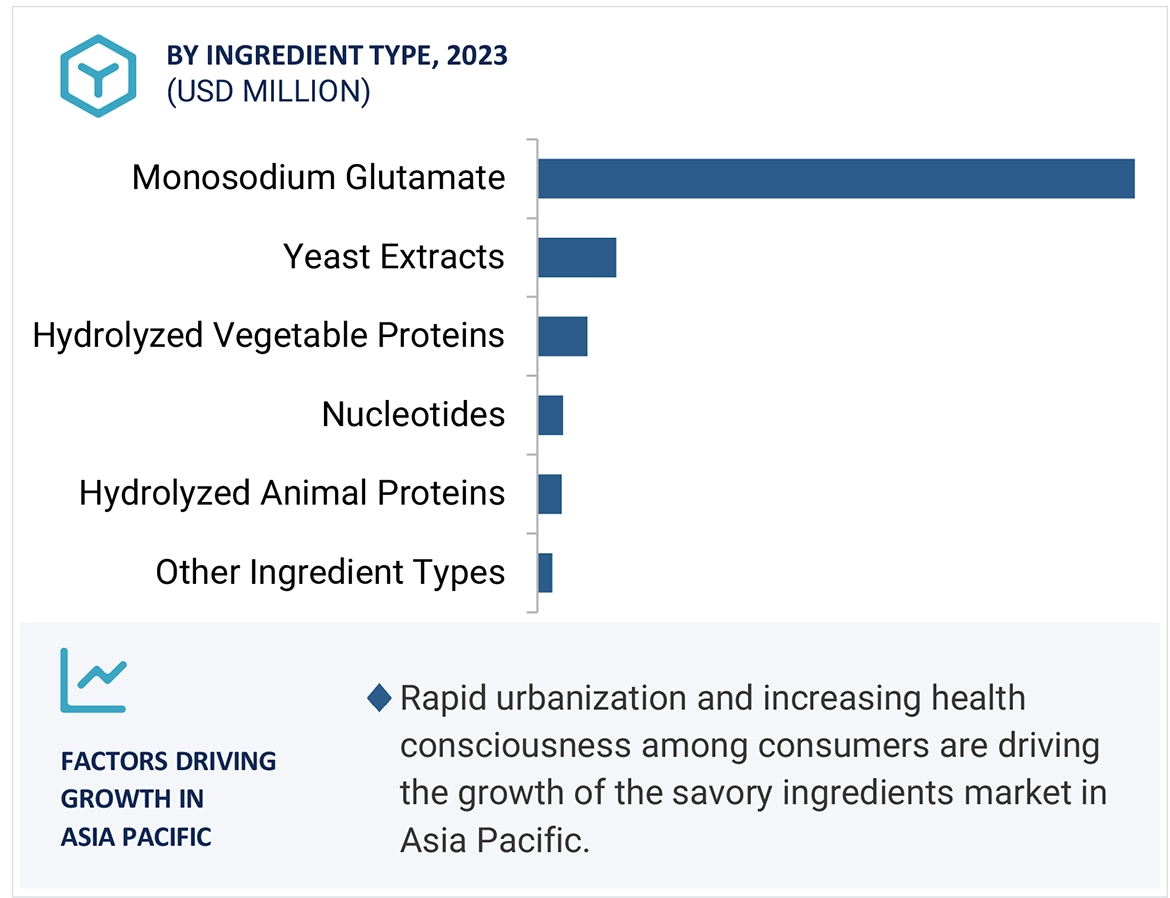

Savory ingredients are derived from natural or synthetic sources, which provide taste and appetizing fragrances to food or other food products influenced by aromatic spices, which enhance the flavor. Some major types of savory ingredients that find applications in food and feed sectors include monosodium glutamate, yeast extracts, nucleotides, hydrolyzed vegetable proteins, and hydrolyzed animal proteins.

Key Stakeholders

-

Raw material suppliers

-

Savory ingredients manufacturers and suppliers

-

Foodservice and restaurant operators

-

Retailers & Distributors

-

Commercial research & development (R&D) institutions and financial institutions

-

Importers and exporters of savory ingredients

-

Food & beverage traders, distributors, and suppliers

-

Government organizations, research organizations, consulting firms, trade associations, and industry bodies

-

Associations, regulatory bodies, and other industry-related bodies:

-

United States Department of Agriculture (USDA)

-

The European Food Information Council (EUFIC)

-

International Association of Food Industry Suppliers

-

International Foodservice Manufacturers Association

-

European Food Safety Authority (EFSA)

-

Food and Drug Administration (FDA)

-

American Spice Trade Association (ASTA)

-

European Spice Association (ESA)

-

Flavor and Extract Manufacturers Association (FEMA)

-

Intermediary suppliers such as traders, distributors, and suppliers of ingredients and end products

Report Objectives

-

To define, segment, and forecast the global savory ingredients market based on ingredient type, origin, form, application, and region over a historical period ranging from 2019 to 2023 and a forecast period ranging from 2024 to 2029.

-

To provide detailed information about the key factors influencing the growth of the market (drivers, restraints, opportunities, and challenges).

-

Identifying attractive opportunities in the market by determining the largest and fastest-growing segments across the regions.

-

Analyzing the demand-side factors based on the following:

-

Impact of macro and microeconomic factors on the market.

-

Shifts in demand patterns across different subsegments and regions.

-

To strategically profile the key players and comprehensively analyze their core competencies.

-

To analyze competitive developments, such as partnerships, mergers & acquisitions, product developments, and expansions & investments in the savory ingredients market.

Available Customizations:

With the given market data, MarketsandMarkets offers customizations according to company-specific scientific needs.

The following customization options are available for the report:

Product Analysis

-

Product Matrix, which gives a detailed comparison of the product portfolio of each company.

Geographic Analysis

With the given market data, MarketsandMarkets offers customizations according to company-specific scientific needs.

-

Further breakdown of the Rest of European market for savory ingredients into Denmark, Poland, and Norway.

-

Further breakdown of the Rest of Asia Pacific market for savory ingredients into Singapore, Indonesia, Thailand, Vietnam, Malaysia, and the Philippines.

-

Further breakdown of the Rest of South American market for savory ingredients into Chile, Peru, and Colombia.

Company Information

-

Detailed analyses and profiling of additional market players (up to five)

Growth opportunities and latent adjacency in Savory Ingredients Market