Vetronics Market by Application (Defense and Homeland Security), Vehicle Type (Main Battle Tank, Light Protected Vehicle, Amphibious Armored Vehicle), Subsystem (Communication, Navigation, C3 Systems, Power Systems) - Global Forecast to 2035

Vetronics Market Summary

The Vetronics Market represents a critical component of modern military vehicle systems, integrating advanced electronics, communication networks, sensors, and computing platforms to enhance operational efficiency, situational awareness, and battlefield survivability. The market was valued at approximately USD 4.5–5.5 billion in 2025 and is projected to reach USD 9.5–11.5 billion by 2035, expanding at a CAGR of around 7%–9% during the forecast period. Growth in the Vetronics Market is driven by increasing defense modernization programs, the rising demand for connected and autonomous military vehicles, and the need for enhanced battlefield communication and intelligence systems. The integration of artificial intelligence, IoT-enabled battlefield networks, and automation technologies is transforming traditional vehicle electronics into intelligent, interconnected systems. As global defense forces shift toward digital warfare and multi-domain operations, vetronics solutions are becoming indispensable for achieving real-time data exchange, mission coordination, and operational superiority.

Key Market Trends & Insights

The Vetronics Market is undergoing rapid transformation due to advancements in defense technologies and increasing investments in vehicle modernization. North America leads the market owing to its strong defense infrastructure and early adoption of advanced technologies, while Asia Pacific is the fastest-growing region driven by rising defense budgets and regional security concerns.

Communication and navigation systems dominate the market, as they form the backbone of connected military vehicles. However, power systems and vehicle protection electronics are gaining traction with the increasing need for survivability and energy efficiency.

Emerging trends include the adoption of AI-driven decision support systems, enabling real-time data analysis and mission planning. IoT integration is enhancing connectivity across vehicles and command centers, while cloud-based platforms are enabling centralized data management.

Automation is playing a key role in enabling autonomous and semi-autonomous military vehicles, reducing human intervention and improving operational efficiency. Additionally, the integration of cybersecurity solutions is becoming critical to protect sensitive data and communication networks.

Market Size & Forecast

- Base year market size (2025): USD 4.5–5.5 billion

- Forecast value by 2035: USD 9.5–11.5 billion

- CAGR: 7%–9%

- Growth is driven by defense modernization, adoption of AI and IoT technologies, increasing demand for connected vehicles, and advancements in autonomous systems

Vetronics Market Top 10 key takeaway

- The market is expected to more than double by 2035 due to modernization programs.

- Communication systems dominate as the backbone of vetronics architecture.

- North America leads due to advanced defense capabilities.

- Asia Pacific is the fastest-growing region driven by rising defense budgets.

- AI enables real-time decision-making and predictive analytics.

- IoT enhances connectivity across battlefield platforms.

- Automation supports autonomous vehicle operations.

- Cybersecurity is becoming a critical component of vetronics systems.

- Integration of multi-domain systems is driving demand.

- Increasing focus on vehicle survivability boosts adoption.

Product Insights

The Vetronics Market is segmented into communication systems, navigation systems, power systems, vehicle protection systems, and weapon control systems. Among these, communication systems hold the largest market share due to their critical role in enabling seamless data exchange between vehicles and command centers. These systems support real-time coordination and situational awareness, which are essential for modern warfare.

The dominance of communication systems is reinforced by the growing adoption of network-centric warfare strategies and the need for interoperable platforms. Navigation systems are also gaining importance, particularly with the integration of GPS and advanced inertial navigation technologies to enhance accuracy and reliability.

Vehicle protection systems, including electronic countermeasures and threat detection systems, are witnessing increased demand as defense forces prioritize survivability. Emerging product categories include integrated vetronics architectures that combine multiple functionalities into a single platform, as well as modular systems that allow for easy upgrades and scalability. AI integration is enabling predictive maintenance and intelligent threat detection, while IoT connectivity is enhancing system interoperability.

Technology / Component Insights (Advanced Vehicle Electronics & Digital Combat Systems)

The Vetronics Market is driven by advancements in vehicle electronics, communication networks, and data processing technologies. Artificial intelligence is playing a transformative role by enabling real-time data analysis, predictive maintenance, and autonomous decision-making. AI-powered systems can process large volumes of data from sensors and provide actionable insights to operators.

IoT integration is facilitating seamless connectivity between vehicles, command centers, and other battlefield assets. Sensors embedded in vehicles collect data on performance, environmental conditions, and threats, enabling enhanced situational awareness.

Cloud computing is providing scalable infrastructure for data storage and analytics, allowing defense organizations to manage and analyze data more efficiently. Automation technologies are enabling autonomous and semi-autonomous vehicle operations, reducing reliance on human operators.

Future innovation trends include the integration of edge computing for real-time data processing, development of advanced cybersecurity solutions, and adoption of open architecture systems to improve interoperability and flexibility.

Application Insights

Military vehicles represent the largest application segment in the Vetronics Market, driven by the increasing demand for advanced electronics in armored vehicles, tanks, and infantry fighting vehicles. Vetronics systems enhance communication, navigation, and operational efficiency in these platforms.

Unmanned ground vehicles (UGVs) are also emerging as a significant application area, with vetronics systems enabling autonomous navigation and remote operation. The growing adoption of UGVs in reconnaissance and surveillance missions is driving demand for advanced vetronics solutions.

Homeland security and law enforcement applications are also contributing to market growth, with vetronics systems used in surveillance vehicles and emergency response units. Future opportunities are expected in autonomous and hybrid vehicle platforms, where advanced electronics will play a critical role.

Regional Insights

North America dominates the Vetronics Market due to its advanced defense infrastructure, strong presence of leading defense contractors, and significant investments in research and development. The region is at the forefront of adopting advanced vetronics technologies.

Europe is another key market, characterized by collaborative defense initiatives and increasing investments in vehicle modernization programs. The region is focusing on enhancing interoperability and integrating advanced technologies.

Asia Pacific is the fastest-growing region, driven by rising defense budgets, increasing geopolitical tensions, and rapid technological adoption. Countries in the region are investing heavily in modernizing their military vehicle fleets.

- North America leads due to strong defense infrastructure and innovation

- Europe focuses on modernization and interoperability

- Asia Pacific shows fastest growth due to rising investments

- Increasing geopolitical tensions drive demand globally

- Government initiatives support market expansion

Country Specific Market Trends

In Asia Pacific, China is experiencing strong growth with a CAGR of around 9%–11%, driven by significant investments in defense modernization and advanced vehicle systems. Japan is also witnessing steady growth, focusing on integrating AI and advanced electronics into its defense platforms.

In North America, the United States leads the market with a CAGR of approximately 7%–8%, supported by extensive R&D and advanced military programs. Canada and Mexico are contributing to growth through investments in defense infrastructure and modernization initiatives.

In Europe, Germany and France are key contributors, with a CAGR of 6%–8%. Germany is focusing on technological innovation and integration of advanced systems, while France is investing in modernizing its armored vehicle fleet.

- China leads APAC growth with strong defense investments

- Japan emphasizes AI-driven vehicle technologies

- United States dominates North America with advanced programs

- Canada and Mexico support infrastructure development

- Germany and France drive European market innovation

Key VETRONICS Company Insights

The Vetronics Market is highly competitive, with leading companies focusing on innovation, advanced technologies, and strategic partnerships. Key players include BAE Systems plc, General Dynamics Corporation, Rheinmetall AG, Thales Group, Leonardo S.p.A., Elbit Systems Ltd., L3Harris Technologies, Inc., Curtiss-Wright Corporation, and Saab AB.

These companies are investing heavily in research and development to develop advanced vetronics solutions that integrate AI, IoT, and automation technologies. The focus on modular and open architecture systems is enabling flexibility and scalability.

Strategic collaborations with defense organizations and technology providers are helping companies expand their market presence. The development of secure and interoperable systems is a key focus area for market players.

- Companies are investing in AI-driven vehicle electronics

- Focus on modular and open architecture systems is increasing

- Strategic partnerships are driving market growth

- IoT integration enhances connectivity and efficiency

- Continuous R&D ensures technological advancement

Recent Developments

Recent developments in the Vetronics Market highlight the growing emphasis on digital transformation and advanced technologies. Several companies have introduced next-generation vetronics systems with enhanced capabilities, including AI-driven analytics and autonomous operation features.

There has also been an increase in partnerships between defense organizations and technology providers to develop integrated vetronics solutions. Additionally, advancements in cybersecurity technologies are improving the resilience of vetronics systems.

Market Segmentation

The Vetronics Market is segmented based on product, technology/component, application, and region. By product, the market includes communication systems, navigation systems, power systems, vehicle protection systems, and weapon control systems. By technology, it encompasses AI-enabled platforms, IoT-integrated systems, cloud-based solutions, and automated vehicle systems.

In terms of application, the market serves military vehicles, unmanned ground vehicles, and homeland security applications. Regionally, the market is divided into North America, Europe, Asia Pacific, and the rest of the world, each contributing to overall growth with unique drivers and opportunities.

- Product segmentation includes communication, navigation, power, protection, and weapon systems

- Technology segmentation covers AI, IoT, cloud, and automation

- Applications include military vehicles, UGVs, and homeland security

- Regional segmentation includes North America, Europe, and Asia Pacific

- Each segment offers strong growth potential

Conclusion

The Vetronics Market is poised for substantial growth through 2035, driven by increasing defense modernization and the adoption of advanced digital technologies. The integration of AI, IoT, and automation is transforming vetronics systems into intelligent platforms capable of supporting complex battlefield operations.

As defense forces continue to prioritize connectivity, interoperability, and real-time decision-making, the demand for vetronics solutions will increase significantly. Companies that focus on innovation, cybersecurity, and advanced technologies will be well-positioned to capitalize on emerging opportunities and maintain a competitive edge in this evolving market.

FAQs

1. What is the market size of Vetronics?

The market was valued at approximately USD 4.5–5.5 billion in 2025.

2. What is the expected growth rate of the market?

The market is projected to grow at a CAGR of around 7%–9% during the forecast period.

3. What are the key drivers of market growth?

Key drivers include defense modernization, integration of AI and IoT, demand for connected vehicles, and advancements in autonomous systems.

4. Which region leads the market?

North America leads the market due to advanced defense infrastructure and technological capabilities.

5. Who are the key companies in the Market?

Key companies include BAE Systems plc, General Dynamics Corporation, Rheinmetall AG, Thales Group, Leonardo S.p.A., Elbit Systems Ltd., L3Harris Technologies, Inc., Curtiss-Wright Corporation, and Saab AB.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Table of Contents

1 Introduction (Page No. - 16)

1.1 Objectives of the Study

1.2 Market Definition

1.3 Study Scope

1.3.1 Markets Covered

1.3.2 Years Considered for the Study

1.4 Currency & Pricing

1.5 Limitations

1.6 Market Stakeholders

2 Research Methodology (Page No. - 19)

2.1 Research Data

2.1.1 Secondary Data

2.1.1.1 Key Data From Secondary Sources

2.1.2 Primary Data

2.1.2.1 Key Data From Primary Sources

2.1.2.2 Breakdown of Primaries

2.2 Factor Analysis

2.2.1 Demand Side Indicators

2.2.1.1 Rising Need for Accuracy in Navigation and Connectivity

2.2.1.2 Growing Regional Conflicts and Modernization of Militaries

2.2.2 Supply Side Indicators

2.2.2.1 High Availability of Small and Robust Electronic Components

2.3 Market Size Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.4 Market Breakdown & Data Triangulation

2.5 Assumptions

3 Executive Summary (Page No. - 28)

3.1 Market Drivers: Regional Mapping

3.2 Vetronics Market Share, By Region, 2016 & 2021

4 Premium Insights (Page No. - 32)

4.1 Attractive Market Opportunities in the Vetronics Market

4.2 Vetronics Market, By Application, 2014 -2021

4.3 Asia-Pacific Vetronics Market, 2015

4.4 North America Estimated to Capture the Largest Share in the Vetronics Market in 2016

4.5 Vetronics Market, By Subsystems

4.6 Life Cycle Analysis, By Geography

5 Market Overview (Page No. - 35)

5.1 Introduction

5.2 Market Segmentation

5.2.1 Vetronics Market, By Application

5.2.2 Vetronics Market, By Vehicle Type

5.2.3 Vetronics Market, By Subsystems

5.3 Market Dynamics

5.3.1 Drivers

5.3.1.1 Upgradation of Countries to Network-Centric Warfare

5.3.1.2 Situational Awareness

5.3.1.3 Embedded Technology System Commonality

5.3.1.4 Shift Towards Cots Enables Improved Swap Specification

5.3.2 Restraints

5.3.2.1 Defense Budget Cuts

5.3.3 Opportunities

5.3.3.1 Development of Vetronics Systems Which are Compatible With Hybrid Engines

5.3.3.2 Availability of New Energy Solutions

5.3.4 Challenges

5.3.4.1 Power Consumption

6 Industry Trends (Page No. - 42)

6.1 Introduction

6.2 Key Influencers

6.3 Key Trends in Vetronics Market

6.3.1 CS 13

6.3.2 Cots (Commercial Off-The-Shelf)

6.3.3 Victory

6.4 Vetronics Procurement for Armored Vehicles , By Regions

6.4.1 North America

6.4.2 Europe

6.4.3 Asia-Pacfic

6.4.4 The Middle East

6.4.5 Active Protection Systems

6.4.6 Interoperable Communication Systems

7 Vetronics Market, By Application (Page No. - 50)

7.1 Introduction

7.2 Defense

7.3 Homeland Security

8 Vetronics Market, By Vehicle Type (Page No. - 54)

8.1 Introduction

8.2 Main Battle Tanks

8.3 Light Protected Vehicles

8.4 Amphibious Armoured Vehicles

8.5 Mine Resistant Ambush Protected (MRAP) Vehicles

8.6 Infantry Fighting Vehicles

8.7 Armored Personnel Carriers

8.8 Others

9 Vetronics Market, By Subsystem (Page No. - 58)

9.1 Introduction

9.2 Navigation Systems

9.3 Observation & Display Systems

9.4 C3 Systems

9.5 Weapon Control Systems

9.6 Sensor & Control Systems

9.7 Vehicle Protection Systems

9.8 Power Systems

10 Geographic Analysis (Page No. - 61)

10.1 Introduction

10.2 North America

10.2.1 By Application

10.2.2 By Vehicle Type

10.2.3 By Subsystems

10.2.4 By Country

10.2.4.1 U.S.

10.2.4.2 Canada

10.3 Europe

10.3.1 By Application

10.3.2 By Vehicle Type

10.3.3 By Subsystems

10.3.4 By Country

10.3.4.1 U.K.

10.3.4.2 Germany

10.3.4.3 Russia

10.3.4.4 France

10.4 Asia-Pacific

10.4.1 By Application

10.4.2 By Vehicle Type

10.4.3 By Subsystems

10.4.4 By Country

10.4.4.1 China

10.4.4.2 India

10.4.4.3 Australia

10.5 The Middle East

10.5.1 By Application

10.5.2 By Vehicle Type

10.5.3 By Subsystems

10.5.4 By Country

10.5.4.1 UAE

10.5.4.2 Saudi Arabia

10.5.4.3 Israel

10.6 Rest of the World

10.6.1 By Application

10.6.2 By Vehicle Type

10.6.3 By Subsystems

10.6.4 By Region

10.6.4.1 Latin America

10.6.4.2 Africa

11 Competitive Landscape (Page No. - 103)

11.1 Introduction

11.2 Market Share Analysis

11.2.1 Brand Analysis

11.2.2 Competitive Situation and Trends

11.2.3 Contracts

11.2.4 New Product Launches

12 Company Profiles (Page No. - 113)

12.1 Introduction

(Overview, Financials, Products & Services, Strategy, and Developments)*

12.2 Thales Group

12.3 Saab Group

12.4 Lockheed Martin Corporation

12.5 General Dynamics Corporation

12.6 Raytheon Company

12.7 Curtiss-Wright Corporation

12.8 Leonardo-Finmeccanica S.P.A

12.9 Rheinmetall AG

12.10 BAE Systems PLC.

12.11 Harris Corporation

*Details on Overview, Financials, Product & Services, Strategy, and Developments Might Not Be Captured in Case of Unlisted Companies.

13 Appendix (Page No. - 143)

13.1 Discussion Guide

13.2 Knowledge Store: Marketsandmarkets Subscription Portal

13.3 Introducing RT: Real Time Market Intelligence

13.4 Available Customization

13.5 Related Reports

List of Tables (75 Tables)

Table 1 Major Conflicts Worldwide, 2002-2015

Table 2 Application Analysis: Vetronics Market

Table 3 Vehicle Type Analysis: Vetronics Market

Table 4 Subsystems Analysis: Vetronics Market

Table 5 Key Trend Analysis for CS 13

Table 6 Key Trend Analysis for Cots

Table 7 Key Trend Analysis for Victory

Table 8 North America: Current and Future Outlook for Vetronics Procurement in Armored Vehicles

Table 9 Europe: Current and Future Outlook for Vetronics Procurement in Armored Vehicles

Table 10 Asia-Pacfic: Current and Future Outlook for Vetronics Procurement in Armored Vehicles

Table 11 The Middle East: Current and Future Outlook for Vetronics Procurement in Armored Vehicles

Table 12 Market Size, By Application, 2014-2021 (USD Million)

Table 13 Market Size in Defense Application, By Region, 2014-2021 (USD Million)

Table 14 Market Size in Homeland Security Application, By Region, 2014-2021 (USD Million)

Table 15 Market Size, By Vehicle Type , 2015-2021 (USD Million)

Table 16 Market Size, By Subsystem, 2014-2021 (USD Million)

Table 17 North America: Market Size, By Application, 2015-2021 (USD Million)

Table 18 North America: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 19 North America: Market Size , By Subsystems, 2015-2021 (USD Million)

Table 20 U.S.: Market Size, By Application, 2015-2021 (USD Million)

Table 21 U.S.: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 22 U.S.: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 23 Canada: Market Size, By Application, 2015-2021 (USD Million)

Table 24 Canada: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 25 Canada: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 26 Europe: Market Size, By Application, 2015-2021 (USD Million)

Table 27 Europe: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 28 Europe: Market Size, By Subsystem, 2015-2021 (USD Million)

Table 29 U.K.: Market Size, By Application, 2015-2021 (USD Million)

Table 30 U.K.: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 31 U.K.: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 32 Germany: Market Size, By Application, 2015-2021 (USD Million)

Table 33 Germany: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 34 Germany: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 35 Russia: Market Size, By Application, 2015-2021 (USD Million)

Table 36 Russia: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 37 Russia: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 38 France: Market Size, By Application, 2015-2021 (USD Million)

Table 39 France: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 40 France: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 41 Asia-Pacific: Market Size, By Application, 2015-2021 (USD Million)

Table 42 Asia-Pacific: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 43 Asia-Pacific: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 44 China: Market Size, By Application, 2015-2021 (USD Million)

Table 45 China: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 46 China: Market Size, By Subsystems , 2015-2021 (USD Million)

Table 47 India: Market Size, By Application, 2015-2021 (USD Million)

Table 48 India: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 49 India: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 50 Australia: Vetronics Market Size, By Application, 2015-2021 (USD Million)

Table 51 Australia: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 52 Australia: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 53 Middle East: Market Size, By Application, 2015-2021 (USD Million)

Table 54 Middle East: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 55 Middle East: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 56 UAE: Market Size, By Application, 2015-2021 (USD Million)

Table 57 UAE: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 58 UAE: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 59 Saudi Arabia: Market Size, By Application, 2015-2021 (USD Million)

Table 60 Saudi Arabia: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 61 Saudi Arabia: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 62 Israel: Market Size, By Application, 2015-2021 (USD Million)

Table 63 Israel: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 64 Israel: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 65 RoW: Market Size, By Application, 2015-2021 (USD Million)

Table 66 RoW: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 67 RoW: Market Size, By Subsystems, 2015-2021 (USD Million)

Table 68 Latin America: Market Size, By Application, 2015-2021 (USD Million)

Table 69 Latin America: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 70 Latin America: Market Size, By Subsystem, 2015-2021 (USD Million)

Table 71 Africa: Market Size, By Application, 2015-2021 (USD Million)

Table 72 Africa: Market Size, By Vehicle Type, 2015-2021 (USD Million)

Table 73 Africa: Market Size, By Subsystem, 2015-2021 (USD Million)

Table 74 Contracts, April 2014 - July 2016

Table 75 New Product Launches, November 2013-June 2016

List of Figures (70 Figures)

Figure 1 Global Vetronics Market: Markets Covered

Figure 2 Study Years

Figure 3 Research Flow

Figure 4 Research Design

Figure 5 Breakdown of Primary Interviews: By Company, Designation & Region

Figure 6 Market Size Estimation Methodology: Bottom-Up Approach

Figure 7 Market Size Estimation Methodology: Top-Down Approach

Figure 8 Market Breakdown & Data Triangulation

Figure 9 Assumptions of the Research Study

Figure 10 Asia-Pacific Projected to Grow at the Highest Rate During the Forecast Period

Figure 11 Defense Application Projected to Lead the Vetronics Market in 2016

Figure 12 C3 Systems Segment Projected to Grow at the Fastest Rate During the Forecast Period

Figure 13 Contracts Was the Key Strategy Adopted By Companies in the Vetronics Market During 2014 to 2016

Figure 14 Increased Network Centric Warfare Playing the Major Role in Growth of Vetronics Market

Figure 15 Defense Segment Projected to Lead the Market Throughout the Forecast Period

Figure 16 China Accounted for the Largest Share in the Asia-Pacific Region

Figure 17 Asia-Pacific Projected to Grow at the Highest CAGR During the Forecast Period in Vetronics Market

Figure 18 Weapon Control Systems Segment Projected to Lead the Market During the Forecast Period

Figure 19 Asia-Pacific Projected to Be the Fastest-Growing Market During the Forecast Period

Figure 20 Vetronics Market, By Application

Figure 21 Market, By Vehicle Type

Figure 22 Market, By Subsystems

Figure 23 Network-Centric Warfare is A Major Driver for the Vetronics Market

Figure 24 Network Centric Warfare, Market Size, 2014 -2021 (USD Million)

Figure 25 Transition to Advanced Vetronics

Figure 26 Vetronics Market Size, By Application, 2014-2021 (USD Million)

Figure 27 Market in Defense Application, By Region, 2016 & 2021 (USD Million)

Figure 28 Market in Homeland Security Application, By Region, 2016 & 2021 (USD Million)

Figure 29 Regional Snapshot: Growth Rate Analysis, 2016-2021

Figure 30 North America Snapshot: the U.S. Projected to Dominate the Global Vetronics Market During the Forecast Period

Figure 31 North America: Vetronics Market, By Application, 2016 & 2021 (USD Million)

Figure 32 North America: Market, By Vehicle Type, 2016 & 2021 (USD Million)

Figure 33 North America: Market, By Subsystems, 2016 & 2021 (USD Million)

Figure 34 Europe Snapshot: Russia Projected to Dominate the Market During the Forecast Period

Figure 35 Europe: Vetronics Market, By Application, 2016 & 2021 (USD Million)

Figure 36 Europe: Market, By Vehicle Type, 2016 & 2021 (USD Million)

Figure 37 Europe: Market, By Subsystems, 2016 & 2021 (USD Million)

Figure 38 Asia-Pacific Snapshot: China to Projected Dominate Vetronics Market During the Forecast Period

Figure 39 Asia-Pacific: Vetronics Market, By Application, 2016 & 2021 (USD Million)

Figure 40 Asia-Pacific: Market, By Vehicle Type, 2016 & 2021 (USD Million)

Figure 41 Asia-Pacific: Market, By Subsystems, 2016 & 2021 (USD Million)

Figure 42 Middle East Snapshot: Saudi Arabia Projected to Dominate Vetronics Market During the Forecast Period

Figure 43 Middle East: Vetronics Market, By Application, 2016 & 2021 (USD Million)

Figure 44 Middle East: Market, By Vehicle Type, 2016 & 2021 (USD Million)

Figure 45 Middle East: Market, By Subsystems, 2016 & 2021 (USD Million)

Figure 46 RoW Snapshot: Latin America Projected to Dominate Vetronics Market During the Forecast Period

Figure 47 RoW: Vetronics Market, By Application, 2016 & 2021 (USD Million)

Figure 48 RoW: Market, By Vehicle Type, 2016 & 2021 (USD Million)

Figure 49 RoW: Market, By Subsystems, 2016 & 2021 (USD Million)

Figure 50 Companies Adopted Contracts as the Key Growth Strategy Between April 2014 and July 2016

Figure 51 Thales Group Dominated the Vetronics Market in 2015

Figure 52 Brand Analysis: Vetronics Market

Figure 53 Vetronics Market Witnessed Significant Growth Between April 2014 and July 2016

Figure 54 Contracts Was the Major Strategy Adopted By Players to Grow in the Market Between 2014 and 2016

Figure 55 Geographic Revenue Mix of Top 5 Market Players , 2015

Figure 56 Thales Group: Company Snapshot

Figure 57 Thales Group: SWOT Analysis

Figure 58 Saab Group: Company Snapshot

Figure 59 Saab AB: SWOT Analysis

Figure 60 Lockheed Martin Corporation: Company Snapshot

Figure 61 Lockheed Martin Corporation: SWOT Analysis

Figure 62 General Dynamics Corporation: Company Snapshot

Figure 63 General Dynamics Corporation: SWOT Analysis

Figure 64 The Raytheon Company: Company Snapshot

Figure 65 Raytheon Company: SWOT Analysis

Figure 66 Curtiss-Wright Corporation: Company Snapshot

Figure 67 Leonardo-Finmeccanica SPA: Company Snapshot

Figure 68 Rheinmetall AG: Company Snapshot

Figure 69 BAE Systems PLC.: Company Snapshot

Figure 70 Harris Corporation: Company Snapshot

Research Methodology:

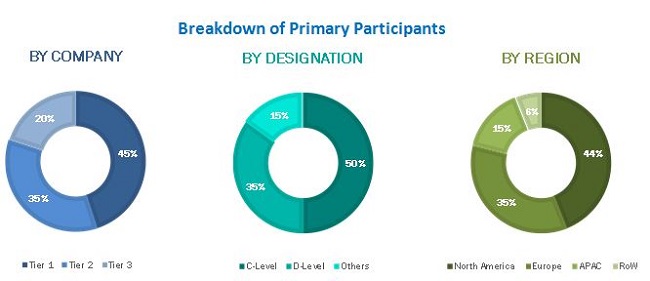

The research methodology used to estimate and forecast the vetronics market begins with obtaining data about key vendor revenues through secondary research, such as company websites, annual reports, press releases, investor presentations, SEC filings, secondary journals, industry news websites, and expert interviews. Vendor offerings are also taken into consideration to determine market segmentation. Bottom-up procedure was employed to arrive at the overall market size of the vetronics market from revenues of key market players. After arriving at the overall market size, the total market was split into several segments and subsegments, which were then verified through primary research by conducting extensive interviews with expects, such as CEOs, VPs, directors, and executives, among others. Data triangulation and market breakdown procedures have been employed to complete the overall market engineering process and arrive at the exact statistics for all segments and subsegments. Breakdown of profiles of primaries is depicted in the figure below:

To know about the assumptions considered for the study, download the pdf brochure

The ecosystem of the vetronics market comprises software/hardware/service, and solution providers, manufacturers, distributors, and end users. Some of the key players in the vetronics market are Thales Group (U.S.), Raytheon Company (U.S.), Lockheed Martin Corporation (U.S.), SAAB Group (Sweden), General Dynamics Corporation (U.S.), Curtiss Wright Corporation (U.S.), Elbit Systems (Israel), Leonardo-Finmeccanica SPA (Italy), Harris Corporation (U.S.), Rheinmetall AG (Germany), BAE Systems (U.K.), among others. These players are adopting various strategies, such as agreements and partnerships, new product developments, contracts, and expansion to strengthen their positions in the vetronics market. They are also focusing on the development of new products with higher accuracy and reduced weight, by investing considerable amount of their revenue on R&D.

Target Audience

- Software/Hardware/Service and Solution Providers

- Technology Support Providers

- Military Land Vehicles Manufacturers

- Subcomponent Manufacturers

Scope of the Report

By Application

- Defense

- Homeland Security

By Vehicle Type

- Main Battle Tank

- Light Protected Vehicles

- Amphibious Armored Vehicles

- Mine resistant ambush protected

- Infantry Fighting Vehicle

- Armored Personnel Carriers

- Others

By Subsystem

- Communication & Navigation

- Observation and Display Systems

- C3 Systems

- Weapon Control Systems

- Sensor & Control Systems

- Vehicle protection Systems

- Power Systems

By Region

- North America

- Europe

- Asia-Pacific

- Middle East

- Rest of the World

Available customization

- Detailed analysis and profiling of additional market players (up to five)

Growth opportunities and latent adjacency in Vetronics Market