Download PDF

Download PDF Request Customisation

Request Customisation

Armored Vehicles Market Size, Share & Trends, 2025 To 2030

Report Code

AS 2369

Published in

Jun, 2025, By MarketsandMarkets™

Armored Vehicles Market by Platform (Combat Vehicles, Combat Support Vehicles, Unmanned Ground Vehicles), Mobility (Wheeled, Tracked), Propulsion (Conventional, Electric), System, Operation Mode, Point of Sale and Region - Global Forecast to 2030

USD 49.90 BN

MARKET SIZE, 2030

CAGR 3.5%

(2025-2030)

338

REPORT PAGES

327

MARKET TABLES

ARMORED VEHICLES MARKET OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

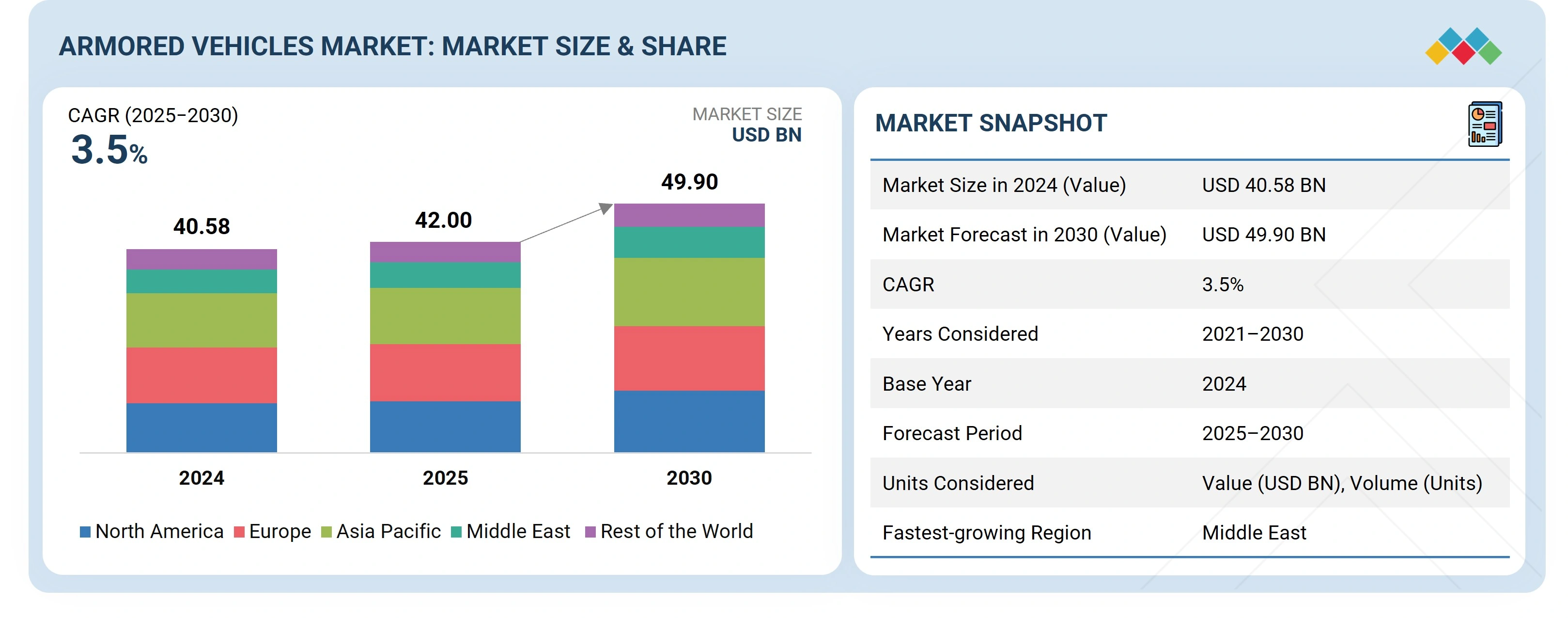

The Armored Vehicles Market is projected to grow from USD 42.0 billion in 2025 to USD 49.9 billion by 2030, at a CAGR of 3.5%. The volume of armored vehicles is projected to grow from 14,393 (units) in 2025 to 16,536 (units) by 2030. Growth is driven by rising defense spending, geopolitical tensions, and the need for enhanced border security. Continuous technological advancements in protection and mobility are enhancing vehicle capabilities. These improvements are also attracting investments and supporting sustained long-term growth in the market.

The Armored Vehicle Market Size is witnessing steady expansion as global defense forces continue to invest in advanced land combat systems to strengthen battlefield mobility, survivability, and protection capabilities. Rising geopolitical tensions, border security concerns, and modernization programs across several countries are contributing significantly to Armored Vehicle Market Growth. Governments are increasingly allocating defense budgets toward the procurement of next generation armored platforms equipped with enhanced ballistic protection, active protection systems, and advanced communication technologies. These developments are shaping the Armored Vehicle Market Industry, where manufacturers are focusing on improving vehicle performance, mobility, and mission adaptability for modern warfare environments.

At the same time, the Armored Vehicle Market Share is becoming more competitive as major defense contractors expand their production capabilities and introduce technologically advanced armored platforms to meet evolving military requirements. Emerging Armored Vehicle Market Trends include the integration of autonomous technologies, hybrid propulsion systems, and digital battlefield management solutions that enhance operational efficiency and situational awareness. In addition, the increasing demand for multi role combat vehicles and troop transport systems is further supporting Armored Vehicle Market Growth across both developed and emerging defense markets. With continuous innovation and increasing defense procurement programs worldwide, the Armored Vehicle Market Industry is expected to experience sustained expansion in the coming years.

ARMORED VEHICLES MARKET Size & Forecast

• 2024 Market Size (Value): USD 40.58 Billion

• 2030 Market Forecast (Value): USD 49.90 Billion

• CAGR: 3.5% from 2025–2030

• Middle East: Fastest-Growing Region

• Driver: Rising Military Modernization Programs

KEY TAKEAWAYS

-

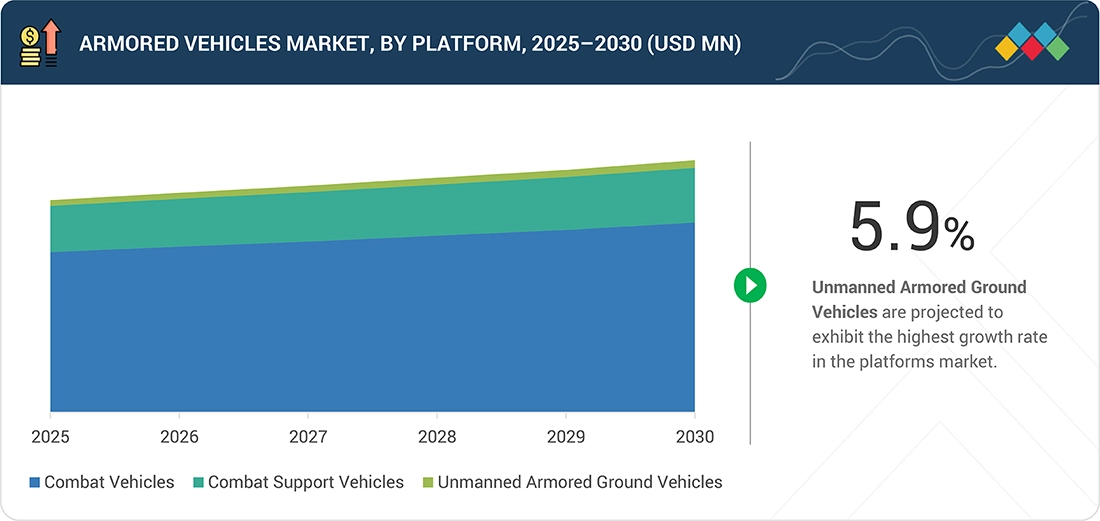

BY PLATFORMArmored vehicle demand is shaped by the balance between combat, support, and unmanned systems, with modernization programs and evolving mission profiles such as urban warfare and counter-insurgency driving diversification.

-

BY SYSTEMAdvancements in subsystems, including C4ISR, armaments, and countermeasure technologies, are enhancing lethality, survivability, and interoperability, positioning integrated systems as key value creators.

-

BY MODE OF OPERATIONManned platforms continue to provide assured control in complex combat environments, while unmanned solutions are increasingly deployed for reconnaissance, surveillance, and autonomous missions as force multipliers.

-

BY MOBILITYWheeled vehicles offer strategic speed and cost advantages for rapid deployments, while tracked platforms deliver superior performance in high-intensity and off-road operations, making both essential for mission flexibility.

-

BY POINT OF SALEOEM procurement supports new platform acquisition and fleet modernization, while the aftermarket ensures lifecycle support, upgrades, and sustainment, creating dual revenue streams for industry stakeholders.

-

BY TYPEConventional vehicles dominate current fleets due to their established infrastructure, while electric and hybrid platforms are emerging as future-ready alternatives that align with efficiency and sustainability goals.

-

BY REGIONRegional growth drivers differ across markets. North America focuses on advanced R&D, Europe on joint defense programs, and Asia-Pacific on accelerating indigenous production. The Middle East is boosting procurement due to security threats, while other regions prioritize cost-efficient modernization of existing fleets.

-

COMPETITIVE LANDSCAPEMajor players are pursuing organic and inorganic strategies, including partnerships and investments. Rheinmetall received a multimillion-dollar contract from the Japanese Ministry of Defence to supply Mission Master SP unmanned ground vehicles (UGVs) for surveillance, logistics, and autonomous support operations.

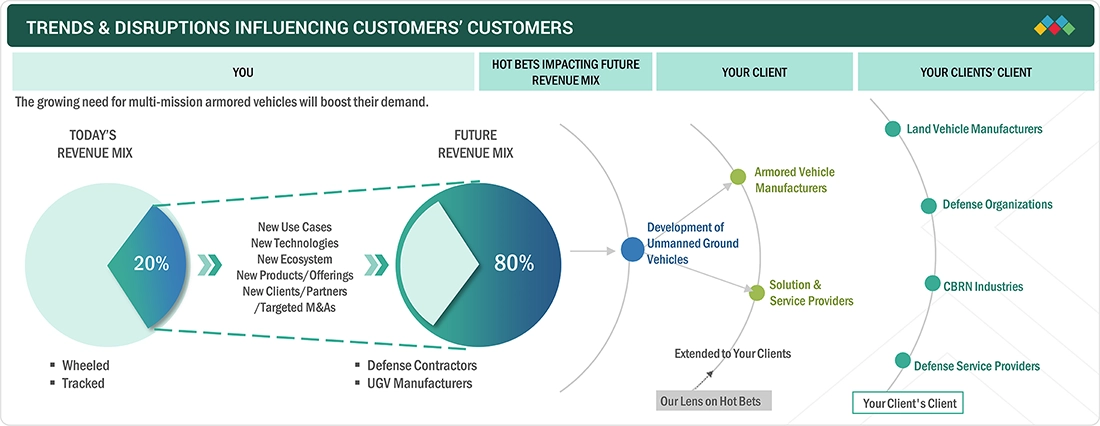

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The future outlook for the Armored Vehicles Industry indicates strong growth, supported by sustained expansion as governments focus on fleet modernization to address evolving security challenges. The integration of advanced technologies, including AI, unmanned systems, and next-generation armor, will enhance operational effectiveness and survivability. Ongoing defense investments and replacement cycles are expected to generate long-term growth opportunities for industry stakeholders.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

ARMORED VEHICLES MARKET DYNAMICS

![]()

Drivers

Impact

Level

Level

-

Rising military modernization programs

-

Growing demand for armored vehicles to tackle cross-border conflicts

![]()

RESTRAINTS

Impact

Level

Level

-

Susceptibility to mechanical and electrical failures

-

Survivability risks for personnel onboard armored vehicles

![]()

OPPORTUNITIES

Impact

Level

Level

-

Rising technology integration and upgrades in military vehicles

-

Adoption of lifecycle optimization strategies for sustainment

![]()

CHALLENGES

Impact

Level

Level

-

High costs of main battle tanks

-

Hardware and software malfunction

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Rising military modernization programs

Military modernization is a key growth driver, with over USD 50 billion allocated globally to replace aging fleets and adopt next-generation platforms. Major programs in the US, Europe, India, and Asia focus on AI-enabled systems, digital integration, and survivability, while countries such as the UK, Australia, and Saudi Arabia link modernization to industrial capability development. These initiatives ensure sustained demand and long-term investment opportunities worldwide.

Restraint:Survivability risks for personnel onboard armored vehicles

Despite significant advancements in armor systems, countermeasures, and protection technologies, armored vehicles remain vulnerable to evolving threats, including improvised explosive devices, mines, and advanced enemy weaponry. Enhancing crew protection often adds weight, which drives up operational costs and reduces mobility and efficiency. These ongoing vulnerabilities directly affect procurement priorities and continue to constrain the overall effectiveness of armored platforms.

Opportunity: Rising technology integration and upgrades in military vehicles

Technology integration presents a significant opportunity as armored vehicles adopt C4ISR suites, AI-enabled navigation, precision-guided munitions, and automated loading systems. These upgrades enhance situational awareness, accuracy, and survivability, driving demand for compatible solutions and reshaping procurement priorities.

Challenge: High costs of main battle tanks

The development and acquisition of main battle tanks demand substantial investment, with advanced configurations further driving costs. This financial burden limits large-scale procurement, especially in emerging economies, and pushes manufacturers and governments to prioritize prototyping, lighter vehicles, or fleet modernization over new MBT acquisitions.

Armored Vehicles Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Open-architecture integration of C4ISR and electronic warfare systems into tactical wheeled and ground combat vehicles | Enhances interoperability, optimizes space and power use, improves situational awareness, and supports future upgrades without major redesign |

|

Electric armor system that neutralizes anti-tank grenades and shells on impact | Strengthens crew protection, reduces vehicle vulnerability to shaped charges, lowers weight compared to conventional armor, and improves battlefield resilience |

|

See-through Armor (STA) using high-resolution imaging and integration with vehicle systems | Delivers 360° situational awareness, improves threat detection in low-visibility conditions, and enhances crew safety through real-time transparent vision capability |

|

ProPulse hybrid diesel-electric propulsion for heavy-duty armored vehicles | Improves fuel efficiency, reduces lifecycle costs, provides onboard power generation, and increases operational flexibility through modular hybrid design |

|

ADAPTIV adaptive camouflage using thermal pixel technology | Enhances stealth by making vehicles less visible to infrared and surveillance systems, improves survivability, and allows rapid replacement of damaged modules |

|

Advanced SATCOM and VSAT solutions for defense and mobility | Provides secure, resilient, and low-latency communications, ensuring operational connectivity for defense, mobility, and government missions |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

ARMORED VEHICLES MARKET ECOSYSTEM

The armored vehicles market ecosystem is shaped by major defense firms, specialized SMEs, and end users. Large companies drive technological innovation through R&D, while SMEs provide niche capabilities and tailored solutions. End users, including military forces, governments, and law enforcement agencies, are the primary demand drivers influencing procurement priorities and market growth.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

ARMORED VEHICLES MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Armored Vehicles Market, By Platform

Combat vehicles command the largest share, driven by their critical role in modern warfare, which involves delivering mobility, protection, and firepower. Ongoing fleet modernization and procurement of main battle tanks and infantry fighting vehicles continue to sustain demand in this segment.

Armored Vehicles Market, By Mobility

Wheeled armored vehicles lead the market due to their operational flexibility, cost efficiency, and suitability for urban and cross-border missions. Their growing use in peacekeeping and rapid-deployment operations reinforces their dominance.

Armored Vehicles Market, By System

Armaments represent the most significant system segment as defense forces prioritize upgrading offensive and defensive capabilities. Investments in precision-guided munitions, remote weapon stations, and fire-control technologies are key drivers of growth.

Armored Vehicles Market, By Mode of Operation

Manned armored vehicles hold the largest share, supported by their proven battlefield reliability and direct operator control. Their established role in complex combat environments ensures continued preference over unmanned alternatives.

Armored Vehicles Market, By Type

Conventional vehicles dominate the market, backed by mature production infrastructure and widespread deployment. Their cost-effectiveness and alignment with large-scale modernization programs strengthen their position.

Armored Vehicles Market, By Point of Sale

OEM sales account for the largest share as defense agencies procure directly from manufacturers under long-term modernization initiatives. Demand for next-generation platforms continues to drive OEM-led growth.

ARMORED VEHICLES MARKET REGION

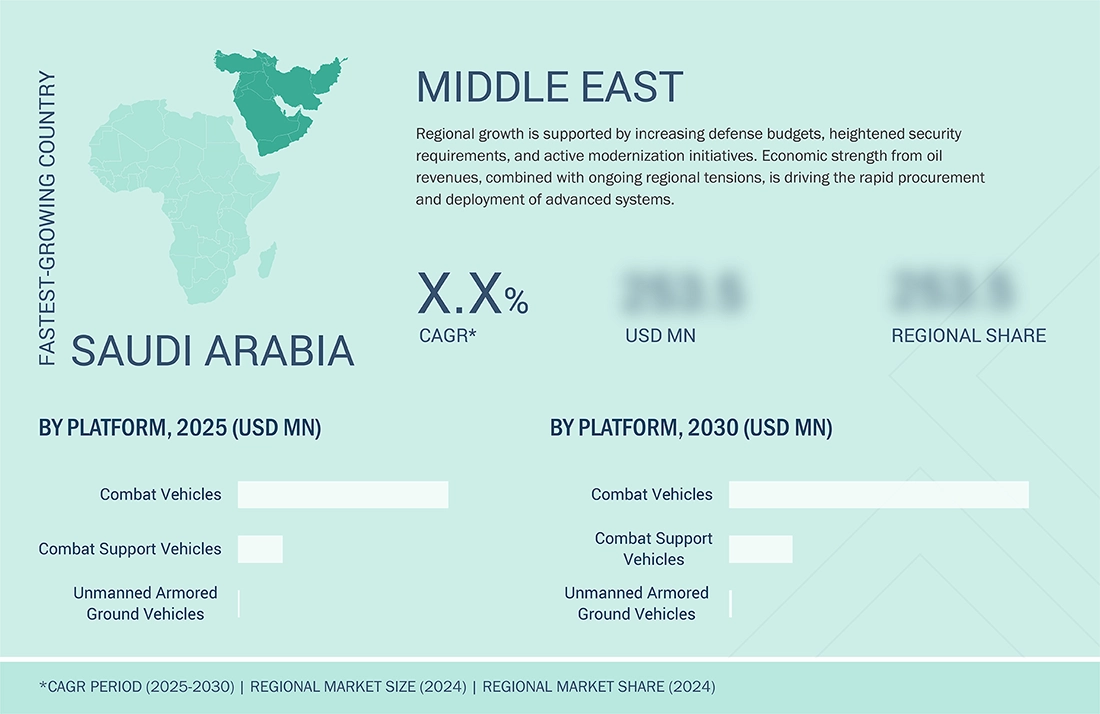

Middle East to be fastest-growing region in global armored vehicles market during forecast period

The Middle East is the fastest-growing region in the armored vehicles market, driven by rising defense spending, border security needs, and ongoing modernization programs. Strong economic capacity from oil revenues and persistent regional tensions are accelerating procurement and development of advanced platforms.

Armored Vehicles Market: COMPANY EVALUATION MATRIX

The company evaluation matrix for the armored vehicles market evaluates players based on product footprint and market share. It highlights their competitive positioning and ranks them according to market strength and growth strategies. Rheinmetall AG (Star) is positioned as a leading defense player, with a strong focus on advanced combat vehicles, protection systems, and integrated weapon solutions. Hyundai Rotem (Emerging Leader) is recognized as a leading innovator in this market.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

ARMORED VEHICLES MARKET KEY PLAYERS

List of Top Armored Vehicles Market Companies

ARMORED VEHICLES MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2024 (Value) | USD 40.58 Billion |

| Market Forecast in 2030 (Value) | USD 49.90 Billion |

| Growth Rate | CAGR of 3.5% from 2025–2030 |

| Years Considered | 2021–2030 |

| Base Year | 2024 |

| Forecast Period | 2025–2030 |

| Units Considered | Value (USD Million/Billion), Volume (Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regions Covered | North America, Europe, Asia Pacific, Middle East, and Rest of the World |

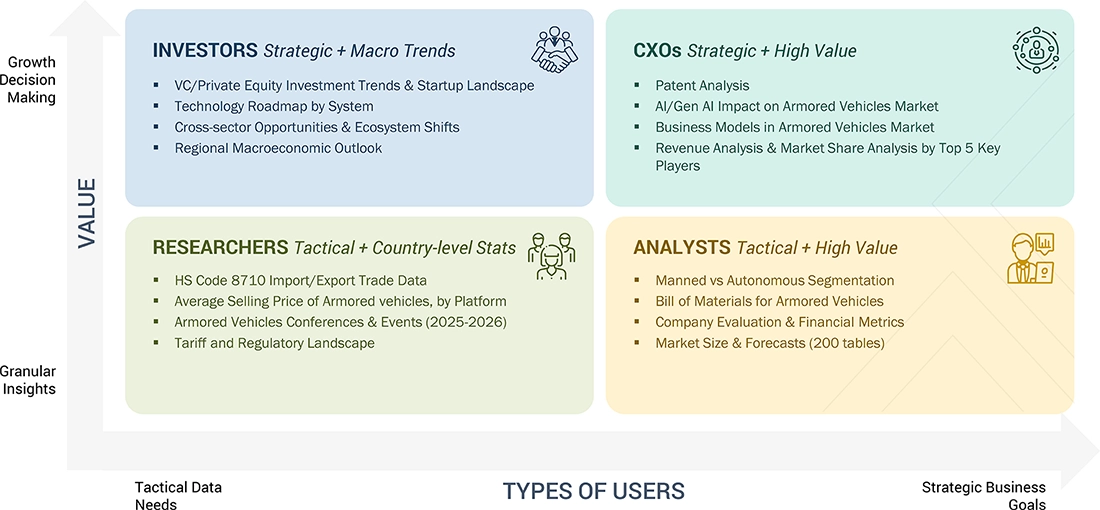

WHAT IS IN IT FOR YOU: Armored Vehicles Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Civil Armored Vehicles Market Customization (Global – Historic & Forecast Market Numbers) | A dedicated civil armored vehicles (non-military) market study providing an in-depth assessment of the market in terms of value and volume. The analysis covers vehicle categories and regional distribution, highlighting comparative benchmarks across different types of civil armored platforms. It delivers quantitative insights into the number of units deployed and the corresponding market valuation, offering a clear view of demand dynamics. |

|

| Geopolitical Situation & Impact on Armored Vehicles Market |

|

|

| Detailed segmentation of the armored vehicles market by platform and sub-categories with regional and country-level breakdown (Value and Volume) |

|

|

RECENT DEVELOPMENTS

- May 2025 : Oshkosh Defense secured a contract for USD 34 million to manufacture wheel and tire assemblies for the US Army. This four-year contract ensures the timely availability of essential components that support routine maintenance and sustainment of the Army’s tactical vehicle fleet

- May 2025 : IDV was awarded a contract to supply 785 military logistic vehicles to the Dutch Armed Forces. The contract includes 8×8 and 4×4 military trucks in three versions: semitrailer tractor, recovery, and hook-lift. Deliveries are scheduled between 2027 and 2029, with an option for an additional 785 vehicles.

- April 2025 : The Netherlands Marine Corps awarded Oshkosh Defense a contract to deliver 150 JLTV-based Dutch Expeditionary Patrol Vehicles (DXPV).

- April 2025 : The US Army placed a USD 95 million order under the Family of Heavy Tactical Vehicles (FHTV) V contract. The order includes autonomy-ready PLS A2 vehicles, supporting logistics modernization efforts with enhanced powertrains, armor, and digital readiness for future autonomy integration.

- April 2025 : Hanwha Aerospace signed a contract with Poland's Huta Stalowa Wola (HSW) to supply chassis and power packs for 87 Krab self-propelled howitzers (SPHs). The contract, valued at approximately USD 280 million, includes deliveries between 2026 and 2028, enhancing Poland's artillery capabilities.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

33

2

RESEARCH METHODOLOGY

39

3

EXECUTIVE SUMMARY

48

4

PREMIUM INSIGHTS

52

5

MARKET OVERVIEW

Rising defense budgets and tech upgrades drive demand for advanced, resilient armored vehicles.

55

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

RISING MILITARY MODERNIZATION PROGRAMS

5.2.1.2

GROWING DEMAND FOR ARMORED VEHICLES TO TACKLE CROSS-BORDER CONFLICTS

5.2.1.3

RISING INCIDENCES OF ASYMMETRIC WARFARE

5.2.1.4

INCREASED GLOBAL DEFENSE SPENDING

5.2.2

RESTRAINTS

5.2.2.1

SUSCEPTIBILITY TO MECHANICAL AND ELECTRICAL FAILURES

5.2.2.2

SURVIVABILITY RISKS FOR PERSONNEL ONBOARD ARMORED VEHICLES

5.2.3

OPPORTUNITIES

5.2.3.1

RISING TECHNOLOGY INTEGRATION AND UPGRADES IN MILITARY VEHICLES

5.2.3.2

ADOPTION OF LIFECYCLE OPTIMIZATION STRATEGIES FOR SUSTAINMENT

5.2.3.3

SURGE IN DEMAND FOR LIGHT ARMORED VEHICLES IN ASYMMETRIC WARFARE

5.2.3.4

INCREASING PROCUREMENT OF UNMANNED SYSTEMS BY DEFENSE FORCES

5.2.3.5

RISE OF NEXT-GEN AMPHIBIOUS AND ARCTIC-CAPABLE PLATFORMS

5.2.4

CHALLENGES

5.2.4.1

HARDWARE AND SOFTWARE MALFUNCTIONS

5.2.4.2

HIGH COSTS OF MAIN BATTLE TANKS

5.3

TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS’ BUSINESSES

5.4

ECOSYSTEM ANALYSIS

5.4.1

PROMINENT COMPANIES

5.4.2

PRIVATE AND SMALL ENTERPRISES

5.4.3

END USERS

5.5

VOLUME DATA

5.6

PRICING ANALYSIS

5.7

VALUE CHAIN ANALYSIS

5.8

TECHNOLOGY ROADMAP

5.9

KEY STAKEHOLDERS AND BUYING CRITERIA

5.9.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.9.2

BUYING CRITERIA

5.10

USE CASE ANALYSIS

5.10.1

VEHICLE INTEGRATION FOR C4ISR/EW INTEROPERABILITY (VICTORY) INITIATIVE

5.10.2

ELECTRIC FORCE FIELD FOR ARMORED VEHICLES

5.10.3

SEE-THROUGH ARMOR

5.10.4

OSHKOSH PROPULSION HYBRID DIESEL-ELECTRIC SYSTEM

5.10.5

ADAPTIVE CAMOUFLAGE SYSTEM

5.11

KEY CONFERENCES AND EVENTS, 2024–2025

5.12

TRADE ANALYSIS

5.12.1

EXPORT DATA

5.12.2

IMPORT DATA

5.13

TECHNOLOGY ANALYSIS

5.13.1

KEY TECHNOLOGY

5.13.1.1

DESIGN AND IMPLEMENTATION OF SOLAR-POWERED ARMORED VEHICLES

5.13.1.2

DEVELOPMENT OF MULTI-PAYLOAD UNMANNED ARMORED VEHICLES

5.13.2

COMPLEMENTARY TECHNOLOGY

5.13.2.1

ELECTRO-OPTICAL AND RADAR SENSOR PAYLOADS FOR UNMANNED ARMORED VEHICLES

5.14

BILL OF MATERIALS

5.15

TOTAL COST OF OWNERSHIP

5.16

BUSINESS MODELS

5.17

REGULATORY LANDSCAPE

5.18

INVESTMENT AND FUNDING SCENARIO

5.19

IMPACT OF 2025 US TARIFFS – OVERVIEW

5.19.1

INTRODUCTION

5.19.2

KEY TARIFF RATES

5.19.3

PRICE IMPACT ANALYSIS

5.19.4

IMPACT ON COUNTRY/REGION

5.19.4.1

US

5.19.4.2

EUROPE

5.19.4.3

ASIA PACIFIC

5.19.4.4

IMPACT ON END USERS

5.20

IMPACT OF AI

5.20.1

INTRODUCTION

5.20.2

IMPACT OF AI ON DEFENSE INDUSTRY

5.20.3

ADOPTION OF AI IN MILITARY BY TOP COUNTRIES

5.20.4

IMPACT OF AI ON ARMORED VEHICLES MARKET

5.21

MACROECONOMIC OUTLOOK

5.21.1

INTRODUCTION

5.21.2

NORTH AMERICA

5.21.3

EUROPE

5.21.4

ASIA PACIFIC

5.21.5

MIDDLE EAST

5.21.6

REST OF THE WORLD

6

INDUSTRY TRENDS

Discover cutting-edge advancements reshaping defense with tech-driven innovations and strategic supply chain insights.

104

6.1

INTRODUCTION

6.2

TECHNOLOGY TRENDS

6.2.1

ACTIVE PROTECTION SYSTEM

6.2.1.1

SOFT-KILL TECHNOLOGY

6.2.1.2

ELECTRO-OPTICAL JAMMER

6.2.1.3

HARD-KILL TECHNOLOGY

6.2.2

REACTIVE ARMOR TECHNOLOGY

6.2.3

PROGRAMMABLE AMMUNITION

6.2.4

LINKLESS FEED SYSTEM

6.2.5

AMMUNITION FEED CHUTE

6.2.6

SENSOR FUSION TECHNOLOGY

6.3

IMPACT OF MEGATRENDS

6.3.1

IMPROVED AMMUNITION CARRYING CAPABILITY

6.3.2

INNOVATIONS IN MICRO-ELECTROMECHANICAL SYSTEM AND NANOTECHNOLOGY

6.3.3

INTEROPERABLE COMMUNICATION SYSTEM

6.3.4

ADVANCED AUTOLOADER

6.4

SUPPLY CHAIN ANALYSIS

6.5

PATENT ANALYSIS

7

ARMORED VEHICLES MARKET, BY PLATFORM

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

112

7.1

INTRODUCTION

7.2

COMBAT VEHICLES

7.2.1

MAIN BATTLE TANKS

7.2.1.1

SURGE IN UPGRADE AND PROCUREMENT PROGRAMS TO DRIVE GROWTH

7.2.1.2

USE CASE: LEOPARD 2A7 IN NATO FORWARD PRESENCE OPERATIONS IN LITHUANIA BY KRAUSS-MAFFEI WEGMANN

7.2.2

INFANTRY FIGHTING VEHICLES

7.2.2.1

ONGOING DEVELOPMENTS BY PROMINENT DEFENSE COMPANIES AND GOVERNMENTS TO DRIVE GROWTH

7.2.2.2

USE CASE: BMP-2 IFV USED BY INDIAN ARMY IN EASTERN LADAKH PATROLS BY ORDNANCE FACTORY BOARD

7.2.3

ARMORED PERSONNEL CARRIERS

7.2.3.1

SIGNIFICANT INVESTMENTS IN DEFENSE ARMORED VEHICLES TO DRIVE GROWTH

7.2.3.2

USE CASE: STRYKER APC IN NATO PEACEKEEPING MISSIONS IN EASTERN EUROPE BY GENERAL DYNAMICS LAND SYSTEMS

7.2.4

ARMORED AMPHIBIOUS VEHICLES

7.2.4.1

INNOVATIONS IN PROPULSION TECHNOLOGY AND HULL DESIGN TO DRIVE GROWTH

7.2.4.2

USE CASE: USMC AAV-7 DEPLOYMENT IN PACIFIC AMPHIBIOUS ASSAULT DRILLS BY BAE SYSTEMS

7.2.5

MINE-RESISTANT AMBUSH-PROTECTED VEHICLES

7.2.5.1

NEED FOR PROTECTION AGAINST ROCKET-PROPELLED GRENADES AND SMALL ARMS TO DRIVE GROWTH

7.2.5.2

USE CASE: OSHKOSH M-ATV IN US SPECIAL FORCES OPERATIONS IN AFRICA BY OSHKOSH DEFENSE

7.2.6

LIGHT ARMORED VEHICLES

7.2.6.1

NEED FOR RAPID RESPONSE IN FLUID COMBAT SITUATIONS TO DRIVE GROWTH

7.2.6.2

USE CASE: CANADIAN LAV III IN UN PEACEKEEPING OPERATIONS IN MALI BY GENERAL DYNAMICS LAND SYSTEMS – CANADA

7.2.7

SELF-PROPELLED HOWITZERS

7.2.7.1

ADVANCED TARGETING TECHNOLOGIES AND POWERFUL MUNITIONS TO DRIVE GROWTH

7.2.7.2

USE CASE: K9 THUNDER SELF-PROPELLED HOWITZER IN SOUTH KOREAN ARTILLERY DETERRENCE ALONG DMZ BY HANWHA AEROSPACE

7.2.8

AIR DEFENSE VEHICLES

7.2.8.1

TREND TOWARD FULLY AUTOMATED AIR DEFENSE SYSTEMS TO DRIVE GROWTH

7.2.8.2

USE CASE: PANTSIR-S1 AIR DEFENSE VEHICLE IN SYRIAN THEATER BY KBP INSTRUMENT DESIGN BUREAU

7.2.9

ARMORED MORTAR CARRIERS

7.2.9.1

ABILITY TO PROVIDE INCREASED FIREPOWER AND MOBILITY TO DRIVE GROWTH

7.2.9.2

USE CASE: M1129 STRYKER MORTAR CARRIER IN US MECHANIZED INFANTRY UNITS BY GENERAL DYNAMICS LAND SYSTEMS

7.3

COMBAT SUPPORT VEHICLES

7.3.1

ARMORED SUPPLY TRUCKS

7.3.1.1

FOCUS ON ENSURING SECURE DELIVERY OF VITAL SUPPLIES TO FRONTLINE UNITS TO DRIVE GROWTH

7.3.1.2

ARMORED FUEL TRUCKS

7.3.1.3

ARMORED AMMUNITION REPLENISHMENT VEHICLES

7.3.1.4

ARMORED AMBULANCES

7.3.2

ARMORED COMMAND & CONTROL VEHICLES

7.3.2.1

SEAMLESS INTEGRATION WITH EXISTING MILITARY SYSTEMS TO DRIVE GROWTH

7.3.2.2

USE CASE: BOXER COMMAND VARIANT USED BY UKRAINIAN FORCES FOR TACTICAL CONTROL NEAR BAKHMUT BY ARTEC

7.3.3

REPAIR & RECOVERY VEHICLES

7.3.3.1

NEED FOR TOWING OR REPAIRING COMBAT VEHICLES ON BATTLEFIELDS TO DRIVE GROWTH

7.3.3.2

USE CASE: M88A2 HERCULES DEPLOYED BY US FORCES IN IRAQ FOR ARMORED VEHICLE RECOVERY BY BAE SYSTEMS

7.3.4

BRIDGE-LAYING TANKS

7.3.4.1

OPERATIONAL READINESS TO DRIVE GROWTH

7.3.4.2

USE CASE: RUSSIAN MTU-90 BRIDGE-LAYING TANK USED IN RIVER CROSSINGS DURING DONBAS OFFENSIVE BY URALVAGONZAVOD

7.3.5

MINE CLEARANCE VEHICLES

7.3.5.1

HIGH DEMAND FOR PREVENTION OF MINE BLASTS AND OTHER BATTLEFIELD HAZARDS TO DRIVE GROWTH

7.3.5.2

USE CASE: FRENCH ARAVIS SOUVIM 2 USED IN SAHEL REGION FOR IED & MINE CLEARANCE DURING OPERATION BARKHANE BY NEXTER SYSTEMS

7.4

UNMANNED ARMORED GROUND VEHICLES

7.4.1

INCREASING DEMAND FOR AUTONOMIC DECISION-MAKING CAPABILITIES IN COMPLEX REMOTE OPERATIONS TO DRIVE GROWTH

7.4.1.1

USE CASE: MILREM THEMIS USED FOR UNMANNED CASEVAC, ISR PATROLS, AND REMOTE WEAPON FIRING SUPPORT BY MILREM ROBOTICS

8

ARMORED VEHICLES MARKET, BY TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

125

8.1

INTRODUCTION

8.2

ELECTRIC ARMORED VEHICLES

8.2.1

EMPHASIS ON REDUCING DEPENDENCE ON FOSSIL FUELS TO DRIVE GROWTH

8.3

CONVENTIONAL ARMORED VEHICLES

8.3.1

HIGHER POWER OUTPUT AND PERFORMANCE TO DRIVE GROWTH

9

ARMORED VEHICLES MARKET, BY MOBILITY

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 4 Data Tables

128

9.1

INTRODUCTION

9.2

WHEELED

9.2.1

NEED FOR IMPROVED MOBILITY DURING CRITICAL COMBAT OPERATIONS TO DRIVE GROWTH

9.2.2

4X4

9.2.3

6X6

9.2.4

8X8

9.2.5

10X10

9.2.6

12X12

9.3

TRACKED

9.3.1

ONGOING MILITARY MODERNIZATION EFFORTS TO DRIVE GROWTH

10

ARMORED VEHICLES MARKET, BY MODE OF OPERATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 3 Data Tables

133

10.1

INTRODUCTION

10.2

MANNED

10.2.1

NEED FOR ROBUST LAND COMBAT PLATFORMS TO DRIVE GROWTH

10.3

UNMANNED

10.3.1

DEVELOPMENT OF AUTONOMOUS TRUCKS FOR COMBAT SUPPORT TO DRIVE GROWTH

11

ARMORED VEHICLES MARKET, BY SYSTEM

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

137

11.1

INTRODUCTION

11.2

ENGINES

11.2.1

USE CASE: MTU 883 DIESEL ENGINE POWERING LEOPARD 2A7+ MBTS FOR ENHANCED POWER-TO-WEIGHT IN URBAN WARFARE

11.2.2

DIESEL ENGINES

11.2.3

TURBINE ENGINES

11.3

DRIVE SYSTEMS

11.3.1

USE CASE: HYBRID-ELECTRIC DRIVE IN RCV-LIGHT PROTOTYPE BY US ARMY FOR REDUCED THERMAL SIGNATURE AND SILENT MOBILITY

11.3.2

POWER TRANSMISSION DRIVES

11.3.3

SUSPENSION & BRAKING SYSTEMS

11.3.4

TRACKS & WHEELS

11.4

BALLISTIC ARMORS

11.4.1

USE CASE: COMPOSITE MODULAR ARMOR IN CV90 MKIV PROVIDING ADAPTIVE PROTECTION IN NATO OPERATIONS IN ESTONIA

11.4.2

COMPOSITE ARMORS

11.4.3

EXPLOSIVE REACTIVE ARMORS

11.4.4

ELECTRIC ARMORS

11.4.5

HOMOGENOUS ARMORS

11.4.6

DEPLETED URANIUM ARMORS

11.4.7

ADD-ON ARMORS

11.5

TURRET DRIVES

11.5.1

USE CASE: ALL-ELECTRIC TURRET DRIVE BY CURTISS-WRIGHT ON BOXER RCT 30 BY CURTISS-WRIGHT

11.6

AMMUNITION HANDLING SYSTEMS

11.7

FIRE CONTROL SYSTEMS

11.7.1

USE CASE: IRON VISION FCS ON MERKAVA MK4 BARAK FOR 360° SITUATIONAL AWARENESS IN CLOSED-HATCH MODE BY ELBIT SYSTEMS

11.8

ARMAMENTS

11.8.1

USE CASE: 30MM XM813 CHAIN GUN ON STRYKER DRAGOON FOR RAPID ENGAGEMENT BY NORTHROP GRUMMAN

11.9

COUNTERMEASURE SYSTEMS

11.9.1

USE CASE: TROPHY ACTIVE PROTECTION SYSTEM (APS) ON ISRAELI AND US ABRAMS TANKS TO INTERCEPT RPGS AND ATGMS IN GAZA BY RAFAEL ADVANCED DEFENSE SYSTEMS

11.10

COMMAND & CONTROL SYSTEMS

11.10.1

USE CASE: TACTICAL COMMAND SOFTWARE BY THALES ON ITS SCORPION VEHICLES

11.11

POWER SYSTEMS

11.11.1

USE CASE: AUXILIARY POWER UNITS (APUS) IN CHALLENGER 3 MBT ENABLING SILENT WATCH OPERATIONS AND ELECTRONIC SUB-SYSTEM SUPPORT

11.12

NAVIGATION SYSTEMS

11.12.1

USE CASE: INERTIAL NAVIGATION SYSTEM WITH GPS-DENIED CAPABILITY IN RHEINMETALL’S LYNX KF41 FOR MANEUVERING IN JAMMING ENVIRONMENTS BY RHEINMETALL AG

11.13

OBSERVATION & DISPLAY SYSTEMS

11.13.1

USE CASE: PANORAMIC DISPLAY AND SENSOR FUSION SUITE IN RHEINMETALL’S LYNX KF41 FOR ENHANCED CREW AWARENESS

11.14

HULLS/FRAMES

11.14.1

USE CASE: MODULAR HULL DESIGN IN PATRIA AMV XP ALLOWING MISSION-SPECIFIC CONFIGURATIONS BY PATRIA GROUP

12

ARMORED VEHICLES MARKET, BY POINT OF SALE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

149

12.1

INTRODUCTION

12.2

OEM

12.3

RETROFIT

13

ARMORED VEHICLES MARKET, BY REGION

Comprehensive coverage of 8 Regions with country-level deep-dive of 11 Countries | 188 Data Tables.

152

13.1

INTRODUCTION

13.2

NORTH AMERICA

13.2.1

PESTLE ANALYSIS

13.2.2

DEFENSE PROGRAMS: NORTH AMERICA

13.2.3

US

13.2.3.1

COLLABORATIONS AND JOINT VENTURES BETWEEN KEY PLAYERS TO DRIVE GROWTH

13.2.4

CANADA

13.2.4.1

MILITARY MODERNIZATION PROGRAMS TO DRIVE GROWTH

13.3

EUROPE

13.3.1

PESTLE ANALYSIS

13.3.2

DEFENSE PROGRAMS: EUROPE

13.3.3

UK

13.3.3.1

SURGE IN ARMORED VEHICLE UPGRADE PROGRAMS TO DRIVE GROWTH

13.3.4

GERMANY

13.3.4.1

FOCUS ON MODERNIZING DOMESTIC ARMORED PERSONNEL CARRIER FLEETS TO DRIVE GROWTH

13.3.5

FRANCE

13.3.5.1

PROCUREMENT OF NEW-GENERATION COMBAT VEHICLES TO DRIVE GROWTH

13.3.6

POLAND

13.3.6.1

INCREASE IN DOMESTIC DEFENSE SPENDING TO DRIVE GROWTH

13.3.7

REST OF EUROPE

13.4

ASIA PACIFIC

13.4.1

PESTLE ANALYSIS

13.4.2

DEFENSE PROGRAMS: ASIA PACIFIC

13.4.3

INDIA

13.4.3.1

INDIGENOUS MANUFACTURING AND CROSS-BORDER PROCUREMENT TO DRIVE GROWTH

13.4.4

JAPAN

13.4.4.1

DEVELOPMENT OF HIGH-END MILITARY TECHNOLOGIES TO DRIVE GROWTH

13.4.5

AUSTRALIA

13.4.5.1

RISE IN MANUFACTURING OF COMBAT FLEETS TO DRIVE GROWTH

13.4.6

SOUTH KOREA

13.4.6.1

RISING MILITARY EXPORTS DRIVE MARKET

13.4.7

REST OF ASIA PACIFIC

13.5

MIDDLE EAST

13.5.1

PESTLE ANALYSIS

13.5.2

DEFENSE PROGRAMS: MIDDLE EAST

13.5.3

GULF COOPERATION COUNCIL (GCC)

13.5.3.1

SAUDI ARABIA

13.5.3.2

UAE

13.5.4

REST OF MIDDLE EAST

13.6

REST OF THE WORLD

13.6.1

LATIN AMERICA

13.6.1.1

INCREASING ACQUISITION OF MODERN ARMORED VEHICLES TO DRIVE GROWTH

13.6.2

AFRICA

13.6.2.1

RISING DEMAND FOR UNMANNED MILITARY GROUND VEHICLES TO DRIVE GROWTH

14

COMPETITIVE LANDSCAPE

Uncover key players' strategies and market rankings shaping the competitive landscape.

217

14.1

INTRODUCTION

14.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021–2024

14.3

MARKET RANKING ANALYSIS, 2024

14.4

MARKET SHARE ANALYSIS, 2024

14.5

REVENUE ANALYSIS, 2021–2024

14.6

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

14.6.1

STARS

14.6.2

EMERGING LEADERS

14.6.3

PERVASIVE PLAYERS

14.6.4

PARTICIPANTS

14.6.5

COMPANY FOOTPRINT

14.6.5.1

COMPANY FOOTPRINT

14.6.5.2

MOBILITY FOOTPRINT

14.6.5.3

PLATFORM FOOTPRINT

14.6.5.4

REGION FOOTPRINT

14.7

COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

14.7.1

PROGRESSIVE COMPANIES

14.7.2

RESPONSIVE COMPANIES

14.7.3

DYNAMIC COMPANIES

14.7.4

STARTING BLOCKS

14.7.5

COMPETITIVE BENCHMARKING

14.7.5.1

KEY START-UPS/SMES

14.7.5.2

COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

14.8

COMPANY VALUATION AND FINANCIAL METRICS

14.9

BRAND/PRODUCT COMPARISON

14.10

COMPETITIVE SCENARIO

14.10.1

MARKET EVALUATION FRAMEWORK

14.10.2

PRODUCT LAUNCHES

14.10.3

DEALS

14.10.4

OTHERS

15

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

248

15.1

KEY PLAYERS

15.1.1

RHEINMETALL AG

15.1.1.1

BUSINESS OVERVIEW

15.1.1.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

15.1.1.3

RECENT DEVELOPMENTS

15.1.1.4

MNM VIEW

15.1.2

GENERAL DYNAMICS CORPORATION

15.1.3

OSHKOSH CORPORATION

15.1.4

BAE SYSTEMS

15.1.5

HANWHA GROUP

15.1.6

NORTHROP GRUMMAN

15.1.7

LOCKHEED MARTIN CORPORATION

15.1.8

THALES

15.1.9

L3HARRIS TECHNOLOGIES, INC.

15.1.10

ST ENGINEERING

15.1.11

ELBIT SYSTEMS LTD.

15.1.12

MITSUBISHI HEAVY INDUSTRIES, LTD.

15.1.13

HYUNDAI ROTEM COMPANY

15.1.14

TEXTRON INC.

15.1.15

OTOKAR OTOMOTIV VE SAVUNMA SANAYI

15.1.16

DENEL SOC LTD.

15.1.17

KNDS

15.1.18

FNSS

15.1.19

CHINA NORTH INDUSTRIES CORPORATION (NORINCO)

15.1.20

RTX

15.1.21

IVECO DEFENCE VEHICLES

15.1.22

PARAMOUNT GROUP

15.2

OTHER PLAYERS

15.2.1

ARQUUS

15.2.2

TATRA TRUCKS A.S.

15.2.3

KALYANI STRATEGIC SYSTEMS LTD.

15.2.4

AM GENERAL

15.2.5

MAHINDRA EMIRATES VEHICLE ARMOURING FZ LLC

15.2.6

TATA ADVANCED SYSTEMS LIMITED

15.2.7

INKAS ARMORED VEHICLE MANUFACTURING

15.2.8

STREIT GROUP

16

APPENDIX

328

16.1

DISCUSSION GUIDE

16.2

ANNEXURE A: DEFENSE PROGRAM MAPPING

16.3

ANNEXURE B: COMPANY LISTED

16.4

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

16.5

CUSTOMIZATION OPTIONS

16.6

RELATED REPORTS

16.7

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

INCLUSIONS AND EXCLUSIONS

TABLE 2

USD EXCHANGE RATES

TABLE 3

ROLE OF COMPANIES IN ECOSYSTEM

TABLE 4

ACTIVE FLEET VOLUME OF MAIN BATTLE TANKS, BY COUNTRY, 2020–2030 (UNITS)

TABLE 5

ACTIVE FLEET VOLUME OF COMBAT SUPPORT VEHICLES, BY COUNTRY, 2020–2030 (UNITS)

TABLE 6

ACTIVE FLEET VOLUME OF COMBAT VEHICLES, BY COUNTRY, 2020–2030 (UNITS)

TABLE 7

INDICATIVE PRICING ANALYSIS OF ARMORED VEHICLES, BY PLATFORM, 2024

TABLE 8

AVERAGE SELLING PRICE RANGE OF MAIN BATTLE TANKS, 2024 (USD MILLION)

TABLE 9

AVERAGE SELLING PRICE RANGE OF INFANTRY FIGHTING VEHICLES, 2024 (USD MILLION)

TABLE 10

AVERAGE SELLING PRICE RANGE OF ARMORED PERSONNEL CARRIERS, 2024 (USD MILLION)

TABLE 11

AVERAGE SELLING PRICE RANGE OF MINE-RESISTANT AMBUSH- PROTECTED VEHICLES, 2024 (USD MILLION)

TABLE 12

AVERAGE SELLING PRICE RANGE OF LIGHT-PROTECTED VEHICLES, 2024 (USD MILLION)

TABLE 13

AVERAGE SELLING PRICE RANGE OF SELF-PROPELLED HOWITZERS, 2024 (USD MILLION)

TABLE 14

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF ARMORED VEHICLES, BY MODE OF OPERATION (%)

TABLE 15

KEY BUYING CRITERIA FOR ARMORED VEHICLES, BY PLATFORM

TABLE 16

KEY CONFERENCES AND EVENTS, 2024–2025

TABLE 17

EXPORT DATA, BY REGION, 2021–2024

TABLE 18

IMPORT DATA, BY REGION, 2021–2024

TABLE 19

TOTAL COST OF OWNERSHIP OF MAIN BATTLE TANKS

TABLE 20

BUSINESS MODELS OF ARMORED VEHICLES MARKET

TABLE 21

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 22

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 23

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 24

MIDDLE EAST: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 25

REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 26

VENTURE CAPITAL FOR UNMANNED GROUND VEHICLES, 2021–2023 (USD MILLION)

TABLE 27

US ADJUSTED RECIPROCAL TARIFF RATES

TABLE 28

KEY PRODUCT-RELATED TARIFF EFFECTIVE FOR ARMORED VEHICLES MARKET

TABLE 29

EXPECTED CHANGE IN PRICES AND LIKELY IMPACT ON END-USE MARKETS DUE TO TARIFF IMPACT

TABLE 30

PATENT ANALYSIS

TABLE 31

ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 32

ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 33

ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 34

ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 35

ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 36

ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 37

ARMORED VEHICLES MARKET, BY WHEELED MOBILITY, 2021–2024 (USD MILLION)

TABLE 38

ARMORED VEHICLES MARKET, BY WHEELED MOBILITY, 2025–2030 (USD MILLION)

TABLE 39

ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 40

ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 41

TYPES OF UNMANNED ARMORED VEHICLES

TABLE 42

ARMORED VEHICLES MARKET, BY SYSTEM, 2021–2024 (USD MILLION)

TABLE 43

ARMORED VEHICLES MARKET, BY SYSTEM, 2025–2030 (USD MILLION)

TABLE 44

ARMORED VEHICLES MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 45

ARMORED VEHICLES MARKET, BY POINT OF SALE, 2025–2030 (USD MILLION)

TABLE 46

ARMORED VEHICLES MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 47

ARMORED VEHICLES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 48

NORTH AMERICA: ARMORED VEHICLES MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 49

NORTH AMERICA: ARMORED VEHICLES MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 50

NORTH AMERICA: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 51

NORTH AMERICA: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 52

NORTH AMERICA: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 53

NORTH AMERICA: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 54

NORTH AMERICA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 55

NORTH AMERICA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 56

NORTH AMERICA: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 57

NORTH AMERICA: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 58

US: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 59

US: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 60

US: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 61

US: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 62

US: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 63

US: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 64

US: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 65

US: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 66

CANADA: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 67

CANADA: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 68

CANADA: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 69

CANADA: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 70

CANADA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 71

CANADA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 72

CANADA: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 73

CANADA: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 74

EUROPE: ARMORED VEHICLES MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 75

EUROPE: ARMORED VEHICLES MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 76

EUROPE: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 77

EUROPE: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 78

EUROPE: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 79

EUROPE: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 80

EUROPE: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 81

EUROPE: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 82

EUROPE: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 83

EUROPE: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 84

UK: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 85

UK: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 86

UK: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 87

UK: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 88

UK: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 89

UK: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 90

UK: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 91

UK: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 92

GERMANY: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 93

GERMANY: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 94

GERMANY: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 95

GERMANY: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 96

GERMANY: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 97

GERMANY: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 98

GERMANY: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 99

GERMANY: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 100

FRANCE: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 101

FRANCE: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 102

FRANCE: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 103

FRANCE: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 104

FRANCE: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 105

FRANCE: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 106

FRANCE: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 107

FRANCE: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 108

POLAND: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 109

POLAND: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 110

POLAND: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 111

POLAND: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 112

POLAND: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 113

POLAND: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 114

POLAND: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 115

POLAND: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 116

REST OF EUROPE: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 117

REST OF EUROPE: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 118

REST OF EUROPE: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 119

REST OF EUROPE: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 120

REST OF EUROPE: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 121

REST OF EUROPE: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 122

REST OF EUROPE: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 123

REST OF EUROPE: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 124

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 125

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 126

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 127

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 128

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 129

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 130

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 131

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 132

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 133

ASIA PACIFIC: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 134

INDIA: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 135

INDIA: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 136

INDIA: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 137

INDIA: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 138

INDIA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 139

INDIA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 140

INDIA: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 141

INDIA: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 142

JAPAN: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 143

JAPAN: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 144

JAPAN: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 145

JAPAN: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 146

JAPAN: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 147

JAPAN: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 148

JAPAN: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 149

JAPAN: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 150

AUSTRALIA: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 151

AUSTRALIA: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 152

AUSTRALIA: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 153

AUSTRALIA: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 154

AUSTRALIA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 155

AUSTRALIA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 156

AUSTRALIA: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 157

AUSTRALIA: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 158

SOUTH KOREA: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 159

SOUTH KOREA: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 160

SOUTH KOREA: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 161

SOUTH KOREA: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 162

SOUTH KOREA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 163

SOUTH KOREA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 164

SOUTH KOREA: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 165

SOUTH KOREA: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 166

REST OF ASIA PACIFIC: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 167

REST OF ASIA PACIFIC: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 168

REST OF ASIA PACIFIC: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 169

REST OF ASIA PACIFIC: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 170

REST OF ASIA PACIFIC: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 171

REST OF ASIA PACIFIC: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 172

REST OF ASIA PACIFIC: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 173

REST OF ASIA PACIFIC: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 174

MIDDLE EAST: ARMORED VEHICLES MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 175

MIDDLE EAST: ARMORED VEHICLES MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 176

MIDDLE EAST: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 177

MIDDLE EAST: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 178

MIDDLE EAST: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 179

MIDDLE EAST: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 180

MIDDLE EAST: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 181

MIDDLE EAST: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 182

MIDDLE EAST: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 183

MIDDLE EAST: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 184

SAUDI ARABIA: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 185

SAUDI ARABIA: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 186

SAUDI ARABIA: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 187

SAUDI ARABIA: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 188

SAUDI ARABIA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 189

SAUDI ARABIA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 190

SAUDI ARABIA: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 191

SAUDI ARABIA: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 192

UAE: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 193

UAE: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 194

UAE: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 195

UAE: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 196

UAE: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 197

UAE: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 198

UAE: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 199

UAE: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 200

REST OF MIDDLE EAST: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 201

REST OF MIDDLE EAST: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 202

REST OF MIDDLE EAST: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 203

REST OF MIDDLE EAST: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 204

REST OF MIDDLE EAST: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 205

REST OF MIDDLE EAST: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 206

REST OF MIDDLE EAST: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 207

REST OF MIDDLE EAST: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 208

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 209

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 210

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 211

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 212

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 213

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 214

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 215

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 216

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 217

REST OF THE WORLD: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 218

LATIN AMERICA: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 219

LATIN AMERICA: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 220

LATIN AMERICA: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 221

LATIN AMERICA: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 222

LATIN AMERICA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 223

LATIN AMERICA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 224

LATIN AMERICA: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 225

LATIN AMERICA: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 226

AFRICA: ARMORED VEHICLES MARKET, BY PLATFORM, 2021–2024 (USD MILLION)

TABLE 227

AFRICA: ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030 (USD MILLION)

TABLE 228

AFRICA: ARMORED VEHICLES MARKET, BY MOBILITY, 2021–2024 (USD MILLION)

TABLE 229

AFRICA: ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030 (USD MILLION)

TABLE 230

AFRICA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2021–2024 (USD MILLION)

TABLE 231

AFRICA: ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030 (USD MILLION)

TABLE 232

AFRICA: ARMORED VEHICLES MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 233

AFRICA: ARMORED VEHICLES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 234

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021–2024

TABLE 235

ARMORED VEHICLES MARKET: DEGREE OF COMPETITION

TABLE 236

ARMORED VEHICLES MARKET: MOBILITY FOOTPRINT

TABLE 237

ARMORED VEHICLES MARKET: PLATFORM FOOTPRINT

TABLE 238

ARMORED VEHICLES MARKET: REGION FOOTPRINT

TABLE 239

ARMORED VEHICLES MARKET: KEY START-UPS/SMES

TABLE 240

ARMORED VEHICLES MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

TABLE 241

ARMORED VEHICLES MARKET: PRODUCT LAUNCHES, JANUARY 2020–MAY 2025

TABLE 242

ARMORED VEHICLES MARKET: DEALS, JANUARY 2020–MAY 2025

TABLE 243

ARMORED VEHICLES MARKET: OTHERS, JANUARY 2020–MAY 2025

TABLE 244

RHEINMETALL AG: COMPANY OVERVIEW

TABLE 245

RHEINMETALL AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 246

RHEINMETALL AG: PRODUCT LAUNCHES

TABLE 247

RHEINMETALL AG: DEALS

TABLE 248

RHEINMETALL AG: OTHERS

TABLE 249

GENERAL DYNAMICS CORPORATION: COMPANY OVERVIEW

TABLE 250

GENERAL DYNAMICS CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 251

GENERAL DYNAMICS CORPORATION: OTHERS

TABLE 252

OSHKOSH CORPORATION: COMPANY OVERVIEW

TABLE 253

OSHKOSH CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 254

OSHKOSH CORPORATION: OTHERS

TABLE 255

BAE SYSTEMS: COMPANY OVERVIEW

TABLE 256

BAE SYSTEMS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 257

BAE SYSTEMS: OTHERS

TABLE 258

HANWHA GROUP: COMPANY OVERVIEW

TABLE 259

HANWHA GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 260

HANWHA GROUP: OTHERS

TABLE 261

NORTHROP GRUMMAN: COMPANY OVERVIEW

TABLE 262

NORTHROP GRUMMAN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 263

NORTHROP GRUMMAN: OTHERS

TABLE 264

LOCKHEED MARTIN CORPORATION: COMPANY OVERVIEW

TABLE 265

LOCKHEED MARTIN CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 266

LOCKHEED MARTIN CORPORATION: OTHERS

TABLE 267

THALES: COMPANY OVERVIEW

TABLE 268

THALES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 269

THALES: OTHERS

TABLE 270

L3HARRIS TECHNOLOGIES, INC.: COMPANY OVERVIEW

TABLE 271

L3HARRIS TECHNOLOGIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 272

L3HARRIS TECHNOLOGIES, INC.: DEALS

TABLE 273

L3HARRIS TECHNOLOGIES, INC.: OTHERS

TABLE 274

ST ENGINEERING: COMPANY OVERVIEW

TABLE 275

ST ENGINEERING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 276

ST ENGINEERING: PRODUCT LAUNCHES

TABLE 277

ST ENGINEERING: DEALS

TABLE 278

ELBIT SYSTEMS LTD.: COMPANY OVERVIEW

TABLE 279

ELBIT SYSTEMS LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 280

ELBIT SYSTEMS LTD.: OTHERS

TABLE 281

MITSUBISHI HEAVY INDUSTRIES, LTD.: COMPANY OVERVIEW

TABLE 282

MITSUBISHI HEAVY INDUSTRIES, LTD.: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

TABLE 283

MITSUBISHI HEAVY INDUSTRIES, LTD.: OTHERS

TABLE 284

HYUNDAI ROTEM COMPANY: COMPANY OVERVIEW

TABLE 285

HYUNDAI ROTEM COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 286

HYUNDAI ROTEM COMPANY: PRODUCT LAUNCHES

TABLE 287

HYUNDAI ROTEM COMPANY: OTHERS

TABLE 288

TEXTRON INC.: COMPANY OVERVIEW

TABLE 289

TEXTRON INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 290

OTOKAR OTOMOTIV VE SAVUNMA SANAYI: COMPANY OVERVIEW

TABLE 291

OTOKAR OTOMOTIV VE SAVUNMA SANAYI: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

TABLE 292

OTOKAR OTOMOTIV VE SAVUNMA SANAYI: OTHERS

TABLE 293

DENEL SOC LTD.: COMPANY OVERVIEW

TABLE 294

DENEL SOC LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 295

DENEL SOC LTD.: DEALS

TABLE 296

KNDS: COMPANY OVERVIEW

TABLE 297

KNDS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 298

KNDS: DEALS

TABLE 299

KNDS: OTHERS

TABLE 300

FNSS: COMPANY OVERVIEW

TABLE 301

FNSS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 302

FNSS: PRODUCT LAUNCHES

TABLE 303

FNSS: OTHERS

TABLE 304

CHINA NORTH INDUSTRIES CORPORATION (NORINCO): COMPANY OVERVIEW

TABLE 305

CHINA NORTH INDUSTRIES CORPORATION (NORINCO): PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 306

CHINA NORTH INDUSTRIES CORPORATION (NORINCO): PRODUCT LAUNCHES

TABLE 307

RTX: COMPANY OVERVIEW

TABLE 308

RTX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 309

RTX: OTHERS

TABLE 310

IVECO DEFENCE VEHICLES: COMPANY OVERVIEW

TABLE 311

IVECO DEFENCE VEHICLES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 312

IVECO DEFENCE VEHICLES: PRODUCT LAUNCHES

TABLE 313

IVECO DEFENCE VEHICLES: DEALS

TABLE 314

IVECO DEFENCE VEHICLES: OTHERS

TABLE 315

PARAMOUNT GROUP: COMPANY OVERVIEW

TABLE 316

PARAMOUNT GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 317

PARAMOUNT GROUP: PRODUCT LAUNCHES

TABLE 318

PARAMOUNT GROUP: DEALS

TABLE 319

PARAMOUNT GROUP: OTHERS

TABLE 320

ARQUUS: COMPANY OVERVIEW

TABLE 321

TATRA TRUCKS A.S.: COMPANY OVERVIEW

TABLE 322

KALYANI STRATEGIC SYSTEMS LTD.: COMPANY OVERVIEW

TABLE 323

AM GENERAL: COMPANY OVERVIEW

TABLE 324

MAHINDRA EMIRATES VEHICLE ARMOURING FZ LLC: COMPANY OVERVIEW

TABLE 325

TATA ADVANCED SYSTEMS LIMITED: COMPANY OVERVIEW

TABLE 326

INKAS ARMORED VEHICLE MANUFACTURING: COMPANY OVERVIEW

TABLE 327

STREIT GROUP: COMPANY OVERVIEW

LIST OF FIGURES

FIGURE 1

ARMORED VEHICLES MARKET SEGMENTATION

FIGURE 2

REPORT PROCESS FLOW

FIGURE 3

RESEARCH DESIGN

FIGURE 4

BOTTOM-UP APPROACH

FIGURE 5

TOP-DOWN APPROACH

FIGURE 6

DATA TRIANGULATION

FIGURE 7

COMBAT VEHICLES TO BE LARGEST SEGMENT DURING FORECAST PERIOD

FIGURE 8

WHEELED SEGMENT TO HOLD LARGER MARKET SHARE DURING FORECAST PERIOD

FIGURE 9

UNMANNED TO BE FASTER-GROWING SEGMENT DURING FORECAST PERIOD

FIGURE 10

ELECTRIC ARMORED VEHICLES TO EXHIBIT FASTER GROWTH DURING FORECAST PERIOD

FIGURE 11

EUROPE TO BE LARGEST MARKET FOR ARMORED VEHICLES DURING FORECAST PERIOD

FIGURE 12

NEED FOR BORDER SECURITY AND MARITIME PATROLLING TO DRIVE GROWTH

FIGURE 13

COMBAT VEHICLES TO SECURE LEADING MARKET SHARE DURING FORECAST PERIOD

FIGURE 14

WHEELED SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 15

MANNED SEGMENT TO ACQUIRE MAXIMUM MARKET SHARE IN 2030

FIGURE 16

CONVENTIONAL ARMORED VEHICLES TO SURPASS ELECTRIC ARMORED VEHICLES DURING FORECAST PERIOD

FIGURE 17

ARMORED VEHICLES MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 18

TOP 10 DEFENSE SPENDERS, 2020–2030

FIGURE 19

TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS’ BUSINESSES

FIGURE 20

ECOSYSTEM ANALYSIS

FIGURE 21

INDICATIVE PRICING ANALYSIS OF ARMORED VEHICLES, BY PLATFORM, 2024

FIGURE 22

VALUE CHAIN ANALYSIS

FIGURE 23

EVOLUTION OF KEY TECHNOLOGIES

FIGURE 24

EMERGING TRENDS RELATED TO ARMORED VEHICLES

FIGURE 25

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF ARMORED VEHICLES, BY MODE OF OPERATION

FIGURE 26

KEY BUYING CRITERIA FOR ARMORED VEHICLES, BY PLATFORM

FIGURE 27

EXPORT DATA, BY COUNTRY, 2021–2024

FIGURE 28

IMPORT DATA, BY REGION, 2020–2022

FIGURE 29

BILL OF MATERIALS FOR ARMORED VEHICLES

FIGURE 30

BILL OF MATERIALS FOR MAIN BATTLE TANKS

FIGURE 31

BILL OF MATERIALS FOR ARMORED PERSONNEL CARRIERS

FIGURE 32

BILL OF MATERIALS FOR INFANTRY FIGHTING VEHICLES

FIGURE 33

TOTAL COST OF OWNERSHIP OF ARMORED VEHICLES

FIGURE 34

PERCENTAGE BREAKDOWN OF TOTAL COST OF OWNERSHIP

FIGURE 35

BUSINESS MODELS IN ARMORED VEHICLES MARKET

FIGURE 36

VENTURE CAPITAL FOR UNMANNED GROUND VEHICLES

FIGURE 37

AI LANDSCAPE

FIGURE 38

IMPACT OF AI ON DEFENSE INDUSTRY

FIGURE 39

ADOPTION OF AI IN MILITARY BY TOP COUNTRIES

FIGURE 40

IMPACT OF AI ON ARMORED VEHICLES MARKET

FIGURE 41

MACROECONOMIC OUTLOOK FOR NORTH AMERICA, EUROPE, ASIA PACIFIC, AND MIDDLE EAST

FIGURE 42

MACROECONOMIC OUTLOOK FOR REST OF THE WORLD

FIGURE 43

TECHNOLOGY TRENDS

FIGURE 44

SUPPLY CHAIN ANALYSIS

FIGURE 45

PATENT ANALYSIS, 2014–2024

FIGURE 46

ARMORED VEHICLES MARKET, BY PLATFORM, 2025–2030

FIGURE 47

ARMORED VEHICLES MARKET, BY TYPE, 2025–2030

FIGURE 48

ARMORED VEHICLES MARKET, BY MOBILITY, 2025–2030

FIGURE 49

ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030

FIGURE 50

ARMORED VEHICLES MARKET, BY SYSTEM, 2025–2030

FIGURE 51

ARMORED VEHICLES MARKET, BY MODE OF OPERATION, 2025–2030

FIGURE 52

ARMORED VEHICLES MARKET, BY REGION, 2025–2030

FIGURE 53

NORTH AMERICA: ARMORED VEHICLES MARKET SNAPSHOT

FIGURE 54

EUROPE: ARMORED VEHICLES MARKET SNAPSHOT

FIGURE 55

ASIA PACIFIC: ARMORED VEHICLES MARKET SNAPSHOT

FIGURE 56

MIDDLE EAST: ARMORED VEHICLES MARKET SNAPSHOT

FIGURE 57

REST OF THE WORLD: ARMORED VEHICLES MARKET SNAPSHOT

FIGURE 58

MARKET SHARE ANALYSIS OF KEY PLAYERS, 2024

FIGURE 59

REVENUE ANALYSIS OF TOP 5 PLAYERS, 2021–2024

FIGURE 60

COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 61

ARMORED VEHICLES MARKET: COMPANY FOOTPRINT

FIGURE 62

COMPANY EVALUATION MATRIX (START-UPS/SMES), 2023

FIGURE 63

FINANCIAL METRICS OF PROMINENT PLAYERS, 2024

FIGURE 64

COMPANY VALUATION OF PROMINENT PLAYERS, 2024

FIGURE 65

BRAND/PRODUCT COMPARISON

FIGURE 66

RHEINMETALL AG: COMPANY SNAPSHOT

FIGURE 67

GENERAL DYNAMICS CORPORATION: COMPANY SNAPSHOT

FIGURE 68

OSHKOSH CORPORATION: COMPANY SNAPSHOT

FIGURE 69

BAE SYSTEMS: COMPANY SNAPSHOT

FIGURE 70

HANWHA GROUP: COMPANY SNAPSHOT

FIGURE 71

NORTHROP GRUMMAN: COMPANY SNAPSHOT

FIGURE 72

LOCKHEED MARTIN CORPORATION: COMPANY SNAPSHOT

FIGURE 73

THALES: COMPANY SNAPSHOT

FIGURE 74

L3HARRIS TECHNOLOGIES, INC.: COMPANY SNAPSHOT

FIGURE 75

ST ENGINEERING: COMPANY SNAPSHOT

FIGURE 76

ELBIT SYSTEMS LTD.: COMPANY SNAPSHOT

FIGURE 77

MITSUBISHI HEAVY INDUSTRIES, LTD.: COMPANY SNAPSHOT

FIGURE 78

HYUNDAI ROTEM COMPANY: COMPANY SNAPSHOT

FIGURE 79

TEXTRON INC.: COMPANY SNAPSHOT

FIGURE 80

OTOKAR OTOMOTIV VE SAVUNMA SANAYI: COMPANY SNAPSHOT

FIGURE 81

RTX: COMPANY SNAPSHOT

Methodology

The study involved four major activities in estimating the current size of the armored vehicles market. Exhaustive secondary research was done to collect information on the armored vehicles market, its adjacent markets, and its parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Demand-side analyses were carried out to estimate the overall size of the market. After that, market breakdown and data triangulation procedures were used to estimate the sizes of different segments and subsegments of the armored vehicles market.

Secondary Research

In the secondary research process, various sources were referred to for identifying and collecting information for this study. The secondary sources included government sources, such as SIPRI; corporate filings, such as annual reports, press releases, and investor presentations of companies; white papers, journals, and certified publications; and articles from recognized authors, directories, and databases.

Primary Research

Extensive primary research was conducted after acquiring information regarding the armored vehicles market scenario through secondary research. Several primary interviews were conducted with market experts from both the demand and supply sides across major countries of North America, Europe, Asia Pacific, the Middle East, and the Rest of the World, which includes Africa and Latin America. Primary data was collected through questionnaires, emails, and telephonic interviews.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

The top-down and bottom-up approaches were used to estimate and validate the size of the armored vehicles market. The research methodology used to estimate the size of the market includes the following details.

Key players in the Armored vehicles market were identified through secondary research, and their market share was determined through primary and secondary research. This included a study of the annual and financial reports of the top market players and extensive interviews with leaders such as directors, engineers, marketing executives, and other stakeholders of leading companies operating in the armored vehicles market.

All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources. All possible parameters that affect the markets covered in this research study were accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data on the armored vehicles market. This data was consolidated, enhanced with detailed input, analyzed by MarketsandMarkets, and presented in this report.

Armored Vehicles Market : Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall market size, the total market was split into several segments and subsegments. The data triangulation and market breakdown procedures explained below were implemented, wherever applicable, to complete the overall market engineering process and arrive at the estimated market numbers for the market segments and subsegments. The data was triangulated by studying various factors and trends from the demand and supply sides. Along with this, the market size was validated using the top-down and bottom-up approaches.

Market Definition

Armored vehicles are designed to carry combat infantry squads to battlefields and provide them with direct fire support. They offer a high level of protection to defense personnel against Improvised Explosive Devices (IEDs), land mines, and indirect enemy fire. These vehicles may be equipped with weapons of different types, calibers, and ranges.

Key Stakeholders

- Armored Vehicle Manufacturers

- Ministries of Defense

- Regulatory Bodies

- R&D Companies

- Manufacturers of Ballistic Armor

- Providers of Weapons and Remote Weapon Stations

- Providers of Active Protection Systems

- Manufacturers of Armored Vehicles

- Providers of Armored Vehicle Components and Sub-components

- Armed Forces

Report Objectives

- To define, describe, and forecast the armored vehicles market size based on platform, type, mobility, mode of operation, and point of sale

- To forecast the size of different segments of the market with respect to five major regions: North America, Europe, Asia Pacific, the Middle East, and the Rest of the World, along with their respective key countries

- To identify and analyze key drivers, restraints, opportunities, and challenges influencing market growth

- To identify industry trends and technology trends currently prevailing in the market

- To analyze micromarkets1 with respect to their individual growth trends, prospects, and contribution to the overall market

- To profile companies operating in the market based on their product portfolios, market shares, and key growth strategies

- To analyze the degree of competition among players in the market by identifying and analyzing their business revenues, products offered, and recent developments and ranking them based on these parameters

- To analyze competitive developments such as deals, product launches/developments, and partnerships/acquisitions undertaken by key market players

- To strategically profile key players and comprehensively analyze their share and core competencies in the market

Available Customizations

MarketsandMarkets offers the following customizations for this market report:

- Additional country-level analysis of the armored vehicles market

- Profiling of other market players (up to 5)

Product Analysis

- Product matrix, which provides a detailed comparison of the product portfolio of each company in the armored vehicles market

Key Questions Addressed by the Report

What is the current and projected market value of the armored vehicle market?

The armored vehicle market is estimated at USD 42.0 billion in 2025 and is projected to reach USD 49.9 billion by 2030, growing at a CAGR of 3.5% during the forecast period.

Which region is expected to grow the fastest in the armored vehicle market?

The Middle East is expected to be the fastest growing region in the armored vehicle market due to rising defense spending, border security needs, and ongoing military modernization programs.

Which segment dominates the armored vehicle market by type?

Conventional armored vehicles dominate the market due to their cost effectiveness, established production infrastructure, and widespread adoption in military modernization programs.

How is the armored vehicle market segmented?

The armored vehicle market is segmented by platform into combat vehicles, combat support vehicles, and unmanned ground vehicles, along with segmentation by mobility, propulsion, system, operation mode, point of sale, and region.

Who are the key players in the armored vehicle market?

Key players in the armored vehicle market include Rheinmetall AG, General Dynamics Corporation, Oshkosh Corporation, BAE Systems, and Hanwha Defense, which are leading innovation and global market competition.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Armored Vehicles Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

- Canada Armored Vehicles Market

- US Armored Vehicles Market

- UK Armored Vehicles Market

- Germany Armored Vehicles Market

- France Armored Vehicles Market

- Poland Armored Vehicles Market

- India Armored Vehicles Market

- Japan Armored Vehicles Market

- Australia Armored Vehicles Market

- South Korea Armored Vehicles Market

- Saudi Arabia Armored Vehicles Market

- UAE Armored Vehicles Market

- Middle East Armored Vehicles Market

- Rest Of Europe Armored Vehicles Market

- Rest Of Asia Pacific Armored Vehicles Market

- Rest Of Middle East Armored Vehicles Market

Growth opportunities and latent adjacency in Armored Vehicles Market

Emmanuel

Apr, 2026

Can I understand how emerging battlefield requirements like asymmetric warfare and cross border conflicts are shaping demand across different vehicle categories?.

Henry

Apr, 2026

Can I see insights into procurement trends and defense programs across regions like India, Europe, and North America?.

Chayan

Jun, 2019

We are trying to understand the armored vehicles requirement, subsegment categorization, and the Indian customers for such products..

Adam

May, 2019