Download PDF

Download PDF Request Customisation

Request Customisation

Electric Ship Market Size, Size, Share & Trends 2032

Report Code

AS 7444

Published in

Sep, 2025, By MarketsandMarkets™

Electric Ship Market by Point of Sale (Newbuild & Line Fit vs. Retrofit), Technology (Fully Electric vs. Hybrid), Ship Type (Commercial, Defense), Solution (Storage, Conversion, Generation, Distribution, Drive) and Region - Global Forecast to 2032

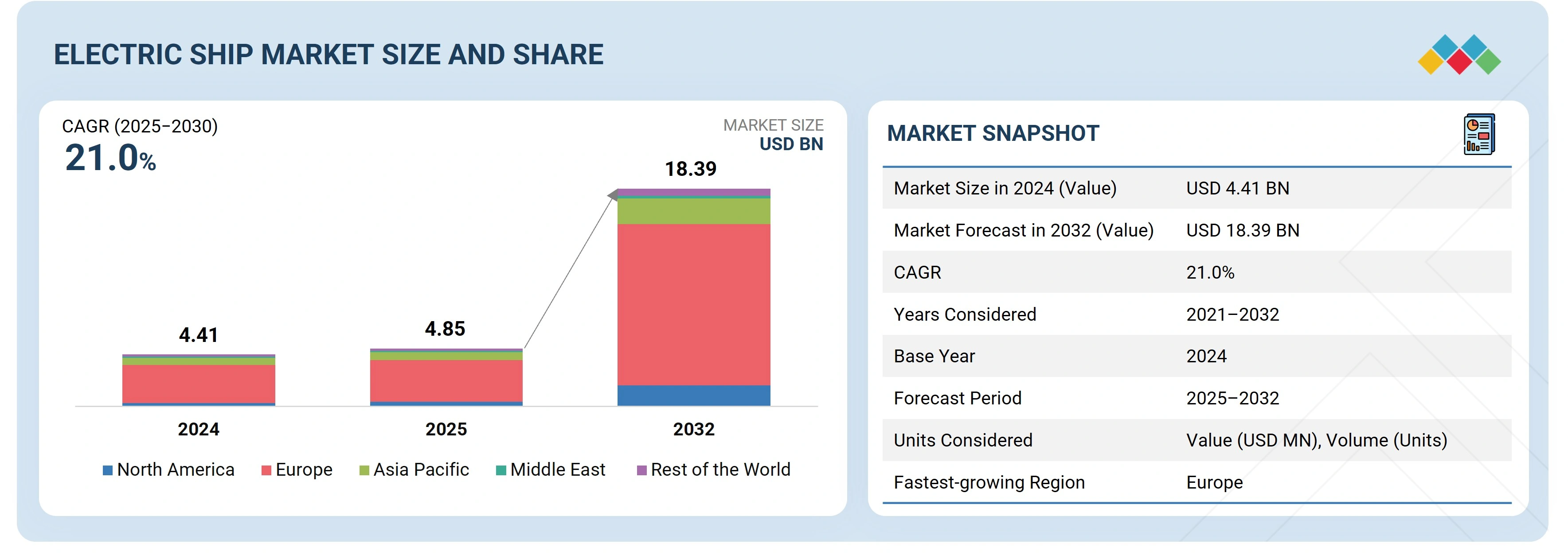

USD 18.39 BN

MARKET SIZE, 2030

CAGR 21.0%

(2025-2030)

357

REPORT PAGES

405

MARKET TABLES

ELECTRIC SHIP MARKET OVERVIEW

The Electric Ship Market Size is estimated at USD 4.85 billion in 2025 and is projected to reach USD 18.39 billion by 2032, at a CAGR of 21.0%. In terms of volume, the electric ship market is projected to grow from 553 units in 2024 to 2,958 units in 2032. Market growth is driven by the increasing demand for low-emission maritim

The Electric Ship Market is gaining strong momentum as maritime industries move toward cleaner propulsion technologies and lower emissions. The Electric Ship Market size is expanding steadily due to increasing investments in sustainable marine transport, battery powered vessels, and hybrid propulsion systems. Growing environmental regulations and decarbonization targets are influencing the Electric Ship Market share across commercial shipping, naval fleets, and passenger ferries. As governments and shipbuilders invest in electric propulsion infrastructure, the Electric Ship Market growth continues to accelerate globally. The power Ship Market is also evolving alongside the Electric and Ship Market, with advanced power management systems, lithium ion battery technologies, and integrated propulsion solutions driving innovation in vessel electrification.

Several emerging Electric Ship Market trends highlight the transition toward fully electric and hybrid vessels for short distance maritime operations. Increasing adoption of shore power systems, autonomous electric vessels, and smart grid integration is shaping the future of the Electric Ship Market. The US Electric ship Market is particularly witnessing strong development due to federal sustainability initiatives, modernization of naval fleets, and growing investments in electric ferries and commercial vessels. With technological advancements and rising environmental awareness, the Electric Ship Market size and Electric Ship Market share are expected to grow significantly over the coming years, strengthening the global Electric and Ship Market ecosystem and reinforcing the long term Electric Ship Market growth outlook.

ELECTRIC SHIP MARKET Size & Forecast

• 2025 Market Size: USD 4.85 Billion

• 2032 Projected Market Size: USD 18.39 Billion

• CAGR (2025-2030): 21.0%

• Power Drive: Highest CAGR

• Europe: Fastest growing region

KEY TAKEAWAYS

-

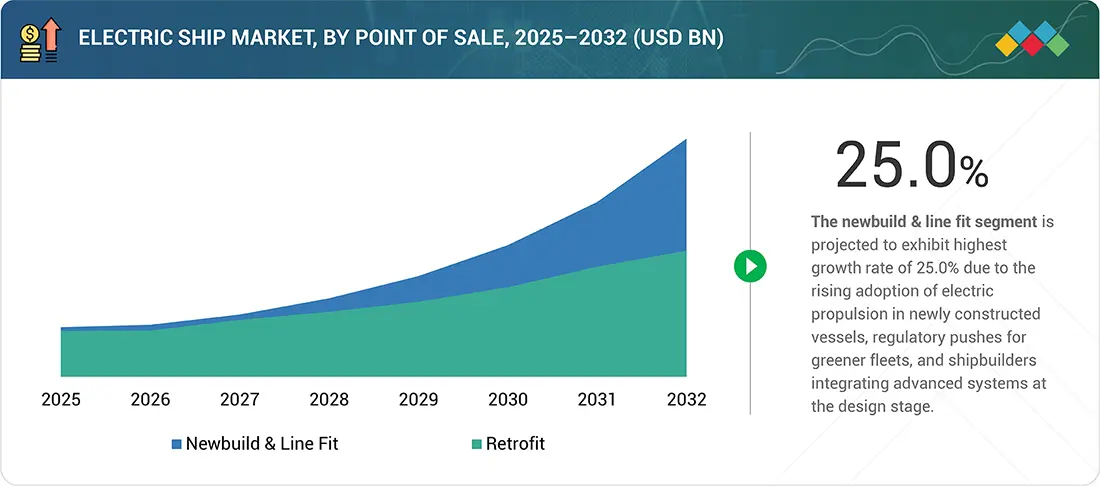

BY POINT OF SALEThe electric ship market by point of sale comprises newbuild & line fit and retrofit solutions. Newbuild & line fit dominate as shipyards integrate electric propulsion, battery storage, and hybrid systems directly during vessel construction, ensuring compliance with emission norms and reducing lifecycle costs. Retrofit solutions are gaining importance as existing fleets are upgraded with energy storage systems, shore power connectivity, and hybrid configurations to meet sustainability targets.

-

BY TONNAGEThe electric ship market by tonnage includes <500 DWT, 500–5,000 DWT, 5,001–15,000 DWT, and >15,000 DWT. The <500 DWT category leads adoption, covering ferries, harbor craft, and service vessels suited for full-electric operation.

-

BY SOLUTIONThe electric ship market by solution includes power storage, power conversion, power generation, power distribution, power drive, and system integration services.

-

BY RANGEThe electric ship market by range comprises <50 km, 50–100 km, 100–1,000 km, and >1,000 km. The 50–100 km range is the largest segment, driven by passenger ferries, inland waterway vessels, and short-sea cargo ships with frequent port calls and access to charging.

-

BY SHIP TYPEThe electric ship market by ship type comprises commercial and defense vessels. The commercial segment drives volume, whereas the defense segment advances high-performance, stealth-oriented solutions.

-

BY POWER CAPACITYThe electric ship market by power capacity includes <75 kW, 75–150 kW, 151–745 kW, 746–7,560 kW, and >7,560 kW. The 75–150 kW segment dominates due to widespread use in ferries, motorboats, and small cargo ships, while higher ranges support larger vessels with hybrid configurations.

-

BY AUTONOMYThe electric ship market by autonomy comprises manned, remotely operated, and autonomous vessels. Manned ships dominate current adoption, remotely operated vessels expand in offshore and defense use, while autonomous ships form the fastest-growing segment with advances in AI and automated navigation.

-

BY REGIONThe market has been segmented by region into North America, Europe, Asia Pacific, Middle East, and Rest of the World. Major ports across Scandinavia and Western Europe are investing heavily in shore power and charging infrastructure, enabling wider adoption of electric ferries and coastal vessels. Strong collaboration between governments, maritime clusters, and technology providers accelerates the commercialization of zero-emission vessels.

-

COMPETITIVE LANDSCAPEMajor players in the electric ship market have adopted both organic and inorganic strategies, including partnerships, joint ventures, and technology investments. For instance, ABB Marine & Ports, Wärtsilä, Kongsberg Maritime, Siemens Energy, and Yara Marine Technologies have entered into multiple collaborations and pilot projects to advance battery storage, hybrid propulsion, shore power connectivity, and autonomous navigation.

The future of the electric ship industry is expected to be driven by the increasing integration of electric and hybrid propulsion across passenger ferries, harbor crafts, short-sea cargo, and defense support vessels. This trend aligns with global decarbonization goals and government-led initiatives promoting maritime sustainability and green port infrastructure. Progress in battery technologies, energy management systems, and modular electric drivetrains is likely to reduce lifecycle costs and improve operational efficiency. As regulatory pressure grows through carbon pricing and zero-emission targets, electric ships are positioned as a critical enabler in the transformation of global maritime transport toward a cleaner and more resilient future.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

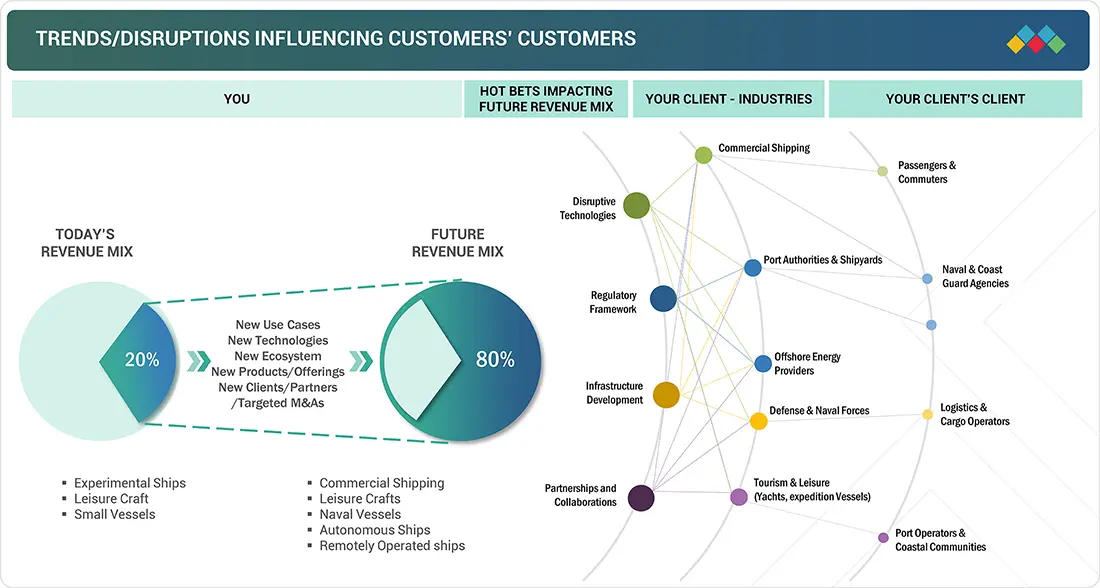

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The impact on maritime businesses is being shaped by emerging customer demands and sustainability-driven disruptions. Numerous electric ship startups and maritime OEMs are seeking venture capital funding, strategic partnerships, and joint ventures to accelerate innovation in electric propulsion and onboard power systems. These collaborations are helping develop critical charging infrastructure and high-performance battery technologies, expanding the adoption potential across commercial, defense, and logistics fleets.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

ELECTRIC SHIP MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Favorable regulatory frameworks and government initiatives

-

Rise in short-sea transport and coastal tourism

RESTRAINTS

Impact

Level

Level

-

High upfront investment and prolonged retrofit downtime

-

Technical limitations in range and power scalability

OPPORTUNITIES

Impact

Level

Level

-

Innovation in energy storage solutions

-

Scaling of battery and fuel cell technologies for long-range shipping

CHALLENGES

Impact

Level

Level

-

Supply chain issues for critical materials

-

Lack of adequate charging and port infrastructure

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Favorable regulatory frameworks and government initiatives

Favorable regulatory frameworks and government initiatives are creating strong momentum for the electric ship market. The International Maritime Organization’s decarbonization targets, coupled with regional emission norms in Europe, North America, and the Asia Pacific, are compelling operators to adopt greener propulsion systems. Governments are supporting this transition with grants, tax incentives, and port infrastructure upgrades to accommodate charging and hybrid operations. These initiatives reduce investment risks, encourage innovation, and accelerate the commercialization of hybrid and fully electric vessels.

Restraint: High upfront investment and prolonged retrofit downtime

One of the most significant barriers to electric ship adoption is the high initial cost associated with propulsion systems, battery packs, onboard power management units, and safety controls. These systems can increase vessel cost by 30–60% compared to conventional diesel propulsion, depending on the vessel type and operational profile. Additionally, retrofitting existing fleets for partial or full electrification involves structural redesign, removal of legacy systems, battery placement, and shore power interface installations all of which require the vessel to be out of service for extended periods.

Opportunity: Innovations in energy storage solutions

Energy storage is central to the operation of hybrid and electric ships. Battery-based propulsion is increasingly applied in smaller vessels, while engine manufacturers are developing hybrid battery solutions for larger vessels. Ongoing technological innovations are expanding the range of energy storage solutions relevant for maritime use. Beyond lithium-ion, there are efforts to develop alternatives such as silicon-based, sodium-sulfur, proton, graphite dual-ion, aluminum-ion, nickel-zinc, potassium-ion, salt-water, paper-polymer, and magnesium batteries.

Challenge: Supply chain issues of critical materials

The electric ship market depends heavily on critical raw materials such as lithium, cobalt, nickel, and rare earth elements for batteries, electric motors, and power electronics. These materials face growing global demand from EVs, grid storage, and industrial electrification creating intense supply pressure. Many of these resources are geographically concentrated, often in politically unstable regions, making prices volatile and access uncertain. Additionally, ethical concerns and ESG requirements related to mining practices are increasing scrutiny on sourcing.

Electric Ship Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Yara launched the Yara Birkeland, the world’s first fully electric and autonomous container vessel for short-sea logistics in 2021. | Reduced CO2 and NO? emissions, Cuts 1,000 tonnes of CO2 annually, eliminates 40,000 truck trips per year, and sets benchmarks for zero-emission autonomous shipping.. |

|

Wärtsilä deployed hybrid propulsion and advanced battery storage systems for the Aurora Botnia ferry, operating on the Kvarken route between Finland and Sweden. | Improved fuel efficiency by 50%, lowered emissions, and enabled flexible vessel operations in harsh Nordic conditions |

|

ABB equipped Grandi Navi Veloci ferries with shore-to-ship power connectivity and battery support to cut port emissions. | Reduced port CO2 emissions by 30–40%, cut particulate matter by up to 98%, and ensured compliance with EU port emission standards |

|

Kongsberg supplied propulsion and autonomous navigation systems for MS Ro Vision, the world’s first hybrid-electric live fish carrier. | Increased operational safety, supported semi-autonomous operations, and demonstrated scalable digital integration in maritime fleets. |

|

Siemens Energy delivered modular power distribution systems for Elektra, the world’s first hydrogen-electric push boat. | Achieved 100% CO2-free operations, optimized energy distribution efficiency by 15%, and enabled emission-free inland waterway transport. |

|

Corvus supplied battery systems for BC Ferries’ hybrid-electric vessels under its Island Class program. | Delivered high-capacity energy storage, reduced fuel costs by 25–30%, and enabled scalable electrification of short-haul routes. |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

ELECTRIC SHIP MARKET ECOSYSTEM

The key stakeholders in the market ecosystem are component manufacturers, system integrators, service providers, and ship builders. The following figure lists some key players working in the electric ship ecosystem. Major influencers in the market are investors, academic researchers, service providers, distributors, and companies producing components.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

ELECTRIC SHIP MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Electric Ship Market, By Range

The 50-100 km range vessels are expected to hold the largest share due to their alignment with short-sea and inland waterway operations. This range is optimal for passenger ferries, short-haul cargo carriers, and service vessels that have frequent access to charging infrastructure. The segment benefits from advancements in battery energy density and fast-charging systems, enabling reliable operations without compromising turnaround times.

Electric Ship Market, By Power Capacity

The 75–150 kW vessels are projected to dominate the electric ship market during the forecast period, driven by their suitability for small ferries, motorboats, and harbor craft that operate on short to medium ranges. These vessels typically require moderate propulsion power, making this category cost-effective and technologically viable with current battery capabilities. Growing investments in coastal transport electrification, particularly in Europe and the Asia Pacific, are further supporting this segment’s expansion.

Electric Ship Market, By Tonnage

The <500 DWT segment is projected to lead adoption in the early phase of the electric ship market, as smaller vessels are ideally suited for full-electric propulsion. The segment benefits from the availability of compact battery packs, rapid charging infrastructure, and strong regulatory support for the electrification of inland waterways and coastal transport.

Electric Ship Market, By Autonomy

The manned segment currently represents the largest share of the electric ships market, reflecting the widespread adoption of electric and hybrid propulsion in traditional vessel operations. Manned electric vessels are particularly prevalent in short-sea routes and inland waterways, where predictable operations and access to charging infrastructure make battery integration practical.

Electric Ship Market, By Ship Type

The commercial segment accounts for the largest share of the electric ship market and is expected to remain the dominant category throughout the forecast period. This segment includes ferries, cargo carriers, cruise ships, yachts, and motorboats, where electrification is being driven by rising regulatory pressure to reduce maritime emissions and growing investments in sustainable transport infrastructure.

Electric Ship Market, By Point of Sale

The newbuild & line fit segment is projected to lead the electric ship market, supported by strong demand for newly constructed vessels designed with integrated electric and hybrid propulsion systems. Shipbuilders are increasingly incorporating battery storage, power distribution, and digital control solutions during the construction phase, ensuring compliance with evolving emission regulations and future-proofing fleets.

Electric Ship Market, By Solution

The power distribution segment is expected to dominate the electric ship market. This segment is a critical enabler of electric ship operations, ensuring the efficient transfer of electricity from onboard storage systems to propulsion drives and auxiliary loads. Modern electric ships increasingly rely on integrated distribution networks that manage energy flows across propulsion, navigation, and hoteling functions, particularly in ferries, cruise ships, and offshore support vessels.

ELECTRIC SHIP MARKET REGION

Europe to be fastest-growing region in global electric ship market during forecast period

Europe is projected to be the fastest-growing region in the global electric ship market due to stringent decarbonization policies, strong government funding, and early adoption of green maritime technologies. The International Maritime Organization’s emission targets, alongside the EU’s Fit for 55 package, are driving investments in electrification, shore charging networks, and hybrid propulsion solutions.

Electric Ship Market: COMPANY EVALUATION MATRIX

The company evaluation matrix for the electric ship market evaluates players based on product footprint and market share. It highlights their competitive positioning and ranks them according to market strength and growth strategies. ABB is positioned as a leading player with a strong focus on advanced technologies, while Yara is recognized as an emerging leader in this market.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

ELECTRIC SHIP MARKET KEY PLAYERS

List of Top Electric Ship Market Companies

ELECTRIC SHIP MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2024 (Value) | USD 4.41 Billion |

| Market Forecast in 2032 (value) | USD 18.39 Billion |

| Growth Rate | CAGR of 21.0% from 2025–2032 |

| Years Considered | 2021–2032 |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Units Considered | Value (USD Billion), Volume (Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regions Covered | North America, Europe, Asia Pacific, Middle East, and Rest of the World |

WHAT IS IN IT FOR YOU: Electric Ship Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Comprehensive Electric Ships Market Analysis with Focus on Market Players and Ecosystem | This is a dedicated electric ship market study focusing on the ecosystem of solution providers, component suppliers, and OEMs. It also provides lifespan analysis of vessels by type and pricing benchmarks across key regions. The study also provides supply chain mapping of components, system integrators, and end users, alongside a comparative assessment of thermal management pricing structures by ship category and region. |

|

RECENT DEVELOPMENTS

- August 2025 : GE Vernova Naval Systems was awarded a USD 10.4 million contract by the US Navy to prototype a megawatt-scale hybrid modular multi-level converter (HMMC) for naval propulsion and power distribution.

- August 2025 : Corvus Energy was selected to supply the energy storage system powering the world’s first fully electric offshore construction vessel. The vessel will rely entirely on the ESS for main propulsion rather than hybrid assistance.

- July 2025 : SCHOTTEL was awarded a contract by French maritime service provider Louis Dreyfus Armateurs (LDA) to supply eight SRP 430 D RudderPropeller Dynamic units for two service operation vessels being built for Vattenfall.

- July 2025 : Kongsberg was contracted to upgrade the Norwegian Coastal Administration’s hybrid vessel, OV Bøkfjord, by installing electric Rim-Drive azimuth thrusters and enhancing its hybrid propulsion system.

- June 2025 : Wärtsilä secured a contract from Vertom Group to supply hybrid propulsion systems for four 10,700 DWT tween-decker vessels under construction at Chowgule Shipyards in India. The solution integrates Wärtsilä 25 engines, electric drive systems, CPP, thrusters, and EcoControl, enabling battery-only sailing in specific conditions.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

35

2

RESEARCH METHODOLOGY

40

3

EXECUTIVE SUMMARY

51

4

PREMIUM INSIGHTS

55

5

MARKET OVERVIEW

Decarbonization drives maritime innovation amid regulatory, investment, and infrastructure challenges.

58

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

IMPLEMENTATION OF NET-ZERO FRAMEWORK WITH GHG PRICING

5.2.1.2

RISE IN SHORT-SEA TRANSPORT AND COASTAL TOURISM

5.2.1.3

ADVANCES IN ENERGY STORAGE AND POWER SYSTEMS

5.2.1.4

DECARBONIZATION AND SUSTAINABILITY GOALS

5.2.2

RESTRAINTS

5.2.2.1

HIGH UPFRONT INVESTMENT AND PROLONGED RETROFIT DOWNTIME

5.2.2.2

TECHNICAL LIMITATIONS IN RANGE AND POWER SCALABILITY

5.2.2.3

FRAGMENTED REGULATORY STANDARDS AND COMPLIANCE BURDEN

5.2.3

OPPORTUNITIES

5.2.3.1

INNOVATIONS IN ENERGY STORAGE SOLUTIONS

5.2.3.2

SCALING OF BATTERY AND FUEL CELL TECHNOLOGIES FOR LONG-RANGE SHIPPING

5.2.3.3

GOVERNMENT INCENTIVES FOR CLEAN SHIPBUILDING PROGRAMS

5.2.4

CHALLENGES

5.2.4.1

SUPPLY CHAIN CONSTRAINTS FOR CRITICAL MATERIALS

5.2.4.2

LACK OF ADEQUATE CHARGING AND PORT INFRASTRUCTURE

5.3

TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4

ECOSYSTEM ANALYSIS

5.4.1

SHIP BUILDERS

5.4.2

SYSTEM INTEGRATORS

5.4.3

END USERS

5.5

CASE STUDY ANALYSIS

5.5.1

CHINA STATE SHIPBUILDING CORPORATION’S FULLY ELECTRIC CONTAINER SHIP

5.5.2

INCAT TASMANIA’S HULL 096 FERRY

5.5.3

WÄRTSILÄ AND WETA’S FULLY ELECTRIC HIGH-SPEED FERRY

5.5.4

HD HYUNDAI’S MMC HIGH-PRESSURE ELECTRIC PROPULSION DRIVE

5.5.5

ABB AZIPOD XO2100 / XO2300 BY ABB

5.5.6

ABILITY MARINE PILOT CONTROL BY ABB

5.5.7

KONGSBERG SYSTEMS ON YARA BIRKELAND BY YARA

5.5.8

NAVALT MAKO ELECTRIC MOTOR BY NAVALT

5.5.9

ABB AMXE MARINE MOTOR BY ABB

5.5.10

SAFT SEAENERGY 2.0 BY SAFT

5.5.11

ABB DYNAFIN BY ABB

5.5.12

GE NAVAL ELECTRIC POWER & PROPULSION BY GE VERNOVA

5.5.13

ELLEN BY SØBY SHIPYARD

5.5.14

AZIPULL THRUSTER BY KONGSBERG

5.5.15

FERRY 30 CAT ELECTRIC BY BALTIC WORKBOATS AS

5.5.16

CORVUS DOLPHIN NXTGEN ESS – ENERGY BY CORVUS ENERGY

5.5.17

FERRY 27 PAX HYBRID BY BALTIC WORKBOATS AS

5.5.18

DIRECT ELECTRIC-DRIVE THRUSTERS BY KONGSBERG

5.5.19

UNDERWATER MOUNTABLE AZIMUTHING BY KONGSBERG

5.5.20

GE SEAJET POD BY GE VERNOVA

5.5.21

GE SEAPULSE MV3000 AFE NAVAL MARINE DRIVE BY GE VERNOVA

5.6

KEY STAKEHOLDERS AND BUYING CRITERIA

5.6.1

KEY STAKEHOLDERS IN BUYING PROCES, BY SHIP TYPE

5.6.2

BUYING CRITERIA

5.7

KEY CONFERENCES AND EVENTS (2025-2026)

5.8

REGULATORY LANDSCAPE

5.9

TECHNOLOGY ANALYSIS

5.9.1

KEY TECHNOLOGIES

5.9.1.1

ENERGY STORAGE SYSTEMS

5.9.1.2

ELECTRIC PROPULSION AND MOTORS

5.9.1.3

SMART POWER DISTRIBUTION AND ENERGY MANAGEMENT

5.9.2

COMPLEMENTARY TECHNOLOGIES

5.9.2.1

HVDC SHIPBOARD GRIDS

5.9.2.2

FUEL CELLS

5.9.2.3

PERMANENT MAGNET PROPULSION RODS

5.9.3

ADJACENT TECHNOLOGIES

5.9.3.1

RENEWABLE ENERGY INTEGRATION

5.9.3.2

DIGITAL TWINS AND SIMULATION PLATFORMS

5.9.3.3

CHARGING AND SHORE POWER INFRASTRUCTURE

5.10

OPERATIONAL DATA

5.10.1

NEWBUILD VS. RETROFIT VESSELS

5.10.2

NEWBUILD VS. RETROFIT VESSELS, VOLUME ESTIMATES, 2021-2024 (UNITS)

5.10.3

NEWBUILD VS. RETROFIT VESSELS, VOLUME FORECASTS, 2025-2032 (UNITS)

5.11

VOLUME DATA

5.11.1

LINE FIT VS. RETROFIT PROPULSION

5.11.2

LINE FIT VS. RETROFIT PROPULSION, VOLUME ESTIMATES, 2021-2024 (UNITS)

5.11.3

LINE FIT VS. RETROFIT PROPULSION, VOLUME FORECASTS, 2025-2032 (UNITS)

5.12

TRADE DATA

5.12.1

IMPORT SCENARIO (HS CODE 8901) - COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD THOUSAND)

5.12.2

EXPORT SCENARIO (HS CODE 8901) - COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD THOUSAND)

5.13

PATENT ANALYSIS

5.14

MACROECONOMIC OUTLOOK

5.14.1

NORTH AMERICA

5.14.2

EUROPE

5.14.3

ASIA PACIFIC

5.14.4

MIDDLE EAST

5.14.5

REST OF THE WORLD

5.15

PRICING ANALYSIS

5.15.1

AVERAGE SELLING PRICE TREND OF SHIP TYPE OFFERED BY KEY PLAYERS (USD MILLION), 2019 TO 2024

5.15.2

AVERAGE SELLING PRICE TREND, BY REGION, (USD MILLION), 2020 TO 2024

5.16

INVESTMENT AND FUNDING SCENARIO

5.17

BUSINESS MODELS

5.17.1

DIRECT SALES MODEL

5.17.2

LEASING & CHARTER MODEL

5.17.3

PAY-PER-USE/TRANSPORT-AS-A-SERVICE MODEL

5.17.4

RETROFIT & LIFECYCLE SERVICE MODEL

5.18

VALUE CHAIN ANALYSIS

5.18.1

RESEARCH AND DEVELOPMENT (UP TO 30%)

5.18.2

RAW MATERIAL & COMPONENTS (30-40%)

5.18.3

SUBSYSTEM /PRODUCT MANUFACTURING (40-60%)

5.18.4

SYSTEM INTEGRATION & TESTING (60-80%)

5.18.5

POST-SALES SERVICE (80-100%)

5.19

BILL OF MATERIALS

5.19.1

POWER STORAGE BOM (%) FOR HYBRIDIZATION

5.19.1

POWER CONVERSION BOM (%) FOR HYBRIDIZATION

5.19.2

POWER GENERATION BOM (%) FOR HYBRIDIZATION

5.19.3

POWER DISTRIBUTION BOM (%) FOR HYBRIDIZATION

5.19.4

POWER DRIVE BOM (%) FOR HYBRIDIZATION

5.20

TOTAL COST OF OWNERSHIP

5.20.1

FUEL COST ESTIMATES AND PROJECTION (USD/KWH)

5.20.2

CHARGING COST ESTIMATES AND PROJECTION (USD/KWH)

5.20.3

CHARGING INFRASTRUCTURE COST ESTIMATES AND PROJECTION (USD/KWH)

5.20.4

BATTERY SYSTEM COST ESTIMATES AND PROJECTION (USD/KWH)

5.20.5

CO2E SOCIAL COST ESTIMATES AND PROJECTION (USD/CO2E TONNES)

5.21

TECHNOLOGY ROADMAP

5.22

IMPACT OF AI

5.22.1

INTRODUCTION

5.22.2

ADOPTION OF AI IN MARINE BY TOP COUNTRIES

5.22.3

IMPACT OF AI ON MARINE USE CASES

5.22.4

IMPACT OF AI ON ELECTRIC SHIP MARKET

5.23

US 2025 TARIFF – ELECTRIC SHIP MARKET

5.23.1

INTRODUCTION

5.23.2

KEY TARIFF RATES

5.23.3

PRICE IMPACT ANALYSIS

5.23.4

IMPACT ON COUNTRY/REGION

5.23.4.1

US

5.23.4.2

EUROPE

5.23.4.3

ASIA PACIFIC

5.23.5

IMPACT ON END-USE INDUSTRIES

6

ELECTRIC SHIP MARKET, BY POINT OF SALE (MARKET SIZE & FORECAST TO 2032 – USD MILLION)

Market Size & Growth Rate Forecast Analysis to 2032 in USD Million | 8 Data Tables

113

6.1

INTRODUCTION

6.1.1

NEWBUILD & LINEFIT VESSELS VS. RETROFIT

6.2

FULLY ELECTRIC, BY PROPULSION

6.2.1

PREVALENCE OF BATTERY-POWERED VESSELS TO DRIVE DEMAND FOR FULLY ELECTRIC VESSELS

6.2.2

BATTERY-POWERED

6.2.2.1

USE CASE: NYK E-CREA EMPLOYS FULLY BATTERY-POWERED VESSEL FOR SHORT-RANGE MARITIME SUPPORT ACTIVITIES

6.2.3

ELECTRO-SOLAR & BATTERY-POWERED

6.2.3.1

USE CASE: HGK “BLUE MARLIN” INCORPORATED ELECTRO-SOLAR & BATTERY-POWERED CONFIGURATION TO IMPROVE OPERATIONAL PERFORMANCE

6.2.4

FUEL CELL & BATTERY-POWERED

6.2.4.1

USE CASE: CMB.TECH “HYDROVILLE” APPLIES FUEL CELL BATTERY-DRIVEN SYSTEMS FOR POWER DELIVERY

6.3

HYBRID, BY PROPULSION

6.3.1

EXTENSIVE USE IN VESSELS WITH VARIABLE DUTY CYCLES TO DRIVE THE ADOPTION OF HYBRID PROPULSION

6.3.2

DIESEL & BATTERY-POWERED

6.3.2.1

USE CASE: SIEMENS BLUEDRIVE SYSTEM USES LITHIUM-ION BATTERIES FOR ENERGY STORAGE & DIESEL ENGINE FOR POWER GENERATION

6.3.3

LPG/LNG & BATTERY-POWERED

6.3.3.1

USE CASE: KAWASAKI HYBRID PROPULSION & POWER SUPPLY SYSTEM COMBINES LNG ENGINE WITH BATTERY ENERGY STORAGE SYSTEM

7

ELECTRIC SHIP MARKET, BY SOLUTION (MARKET SIZE & FORECAST TO 2032 – USD MILLION)

Market Size & Growth Rate Forecast Analysis to 2032 in USD Million | 6 Data Tables

121

7.1

INTRODUCTION

7.1.1

LINE FIT VS. RETROFIT PROPULSION

7.2

POWER STORAGE

7.2.1

RIGOROUS PUSH FOR DECARBONIZATION TO DRIVE THE MARKET

7.2.2

BATTERIES

7.2.2.1

USE CASE: CORVUS ORCA ENERGY STORAGE SYSTEM (ESS) USES LITHIOUM-ION BATTERY TECHNOLOGY

7.2.2.2

LITHIUM-ION

7.2.2.3

LEAD ACID

7.2.2.4

NICKEL CADMIUM

7.2.2.5

SODIUM-ION

7.2.3

SUPERCAPACITORS/ULTRACAPACITORS

7.2.3.1

USE CASE: LECLANCHÉ MARINE RACK SYSTEM (MRS) INCORPORATES SUPERCAPACITOR MODULES TO MANAGE POWER DEMANDS

7.2.4

HYBRID ENERGY STORAGE SYSTEMS

7.2.4.1

USE CASE: SAFT SEANERGY 2.0 SYSTEM USES HYBRID ENERGY STORAGE SYSTEM COMBINING LI-ION WITH POWER GENERATORS

7.3

POWER CONVERSION

7.3.1

INCREASING COMPLEXITY OF ELECTRIC AND HYBRID SHIP DESIGNS TO DRIVE THE MARKET

7.3.2

CONVERTERS

7.3.2.1

USE CASE: GE VERNOVA MV7000 MEDIUM VOLTAGE DRIVE USES VARIABLE FREQUENCY CONVERSION TO ALLOW MOTORS TO OPERATE EFFICIENTLY

7.3.3

TRANSFORMERS

7.3.3.1

USE CASE: SCHNEIDER ELECTRIC ECOSTRUXURE MARINE MEDIUM-VOLTAGE DRY-TYPE TRANSFORMER TO PROVIDE CONSISTENT VOLTAGE CONVERSION

7.4

POWER GENERATION

7.4.1

SHIFT FROM CONVENTIONAL FUELS TO EMERGING TECHNOLOGIES TO DRIVE THE MARKET

7.4.2

AC VS. DC GENERATORS

7.4.2.1

USE CASE: WÄRTSILÄ HY ELECTRIC PROPULSION SYSTEM APPLIES DC GENERATOR CONFIGURATION

7.4.3

LPG/LNG VS. DIESEL ENGINES

7.4.3.1

USE CASE: MAN 51/60DF DUAL-FUEL ENGINE ENABLES LNG/LPG AS PRIMARY FUEL WITH DIESEL AS SECONDARY FUEL

7.4.4

SOLAR CELLS

7.4.4.1

USE CASE: NAVALT “INDRA” APPLIES ONBOARD SOLAR POWER GENERATION SYSTEM WITH 25 KWP SOLAR PANELS TO GENERATE POWER

7.4.5

FUEL CELLS

7.4.5.1

USE CASE: MV SEA CHANGE OPERATES ON A HYDROGEN FUEL CELL SYSTEM FOR ELECTROCHEMICAL POWER GENERATION

7.5

POWER DISTRIBUTION

7.5.1

EXPANSION OF MARITIME ELECTRIFICATION TO LARGER COMMERCIAL AND DEFENSE PLATFORMS TO DRIVE THE MARKET

7.5.2

INTERCONNECTORS

7.5.2.1

USE CASE: SCHNEIDER ELECTRIC ECOSTRUXURE MARINE MICROGRID POWER DISTRIBUTION SYSTEM ENABLES CONNECTION & MANAGEMENT OF MULTIPLE ENERGY SOURCES

7.5.3

SWITCHBOARDS

7.5.3.1

USE CASE: WÄRTSILÄ LOW- AND MEDIUM-VOLTAGE MARINE SWITCHBOARD SYSTEM DESIGNED FOR POWER DISTRIBUTION

7.6

POWER DRIVE

7.6.1

RAPID ADOPTION DUE TO ADVANCES IN ELECTRIFICATION TO DRIVE THE MARKET

7.6.2

VARIABLE FREQUENCY DRIVES

7.6.2.1

USE CASE: SIEMENS SINAMICS PERFECT HARMONY GH180 MARINE DRIVE REGULATES THE ELECTRICAL SUPPLY TO PROPULSION MOTORS

7.6.3

MOTORS

7.6.3.1

USE CASE: SIEMENS PERMASYN SYNCHRONOUS PROPULSION MOTOR USES PERMANENT-MAGNET SYNCHRONOUS OPERATION TO MAINTAIN CONSTANT TORQUE

7.6.3.2

SYNCHRONOUS MOTORS

7.6.3.3

INDUCTION MOTORS

7.6.4

GEARBOXES

7.6.4.1

USE CASE: TWIN DISC MGE-5126SC HYBRID-READY MARINE TRANSMISSION ALLOWS POWER TRANSFER FROM DIESEL ENGINES & ELECTRIC MOTORS

7.6.5

PROPELLERS

7.6.5.1

USE CASE: ROLLS-ROYCE KAMEWA TYPE A CONTROLLABLE PITCH PROPELLER (CPP) TO MANAGE OPERATIONAL VARIATIONS

7.6.6

THRUSTERS

7.6.6.1

USE CASE: BRUNVOLL FU SERIES AZIMUTH TUNNEL THRUSTER PROVIDES A ROTATIONAL PROPULSION SYSTEM FOR POWER DRIVE

7.7

SYSTEM INTEGRATION

7.7.1

USE CASE: CROWLEY EWOLF SHOWS HOW SMART INTEGRATION TURNS ELECTRIC PROPULSION INTO DAY-ONE RELIABILITY

8

ELECTRIC SHIP MARKET, BY AUTONOMY (MARKET SIZE & FORECAST TO 2032 – USD MILLION)

Market Size & Growth Rate Forecast Analysis to 2032 in USD Million | 2 Data Tables

139

8.1

INTRODUCTION

8.2

MANNED

8.2.1

ALIGNMENT WITH EXISTING MARITIME PRACTICES TO DRIVE MARKET

8.3

REMOTELY OPERATED

8.3.1

IMPROVED OPERATIONAL FEASIBILITY TO DRIVE MARKET

8.4

AUTONOMOUS

8.4.1

FAVORABLE REGULATORY FRAMEWORKS AND SUPPORTING INFRASTRUCTURE AT PORTS TO DRIVE MARKET

9

ELECTRIC SHIP MARKET, BY POWER CAPACITY (MARKET SIZE & FORECAST TO 2032 – USD MILLION)

Market Size & Growth Rate Forecast Analysis to 2032 in USD Million | 2 Data Tables

143

9.1

INTRODUCTION

9.2

<75 KW

9.2.1

LARGE-SCALE ADOPTION IN SMALLER VESSELS TO DRIVE MARKET

9.3

75–150 KW

9.3.1

NEED FOR LONGER OPERATING HOURS AND HIGHER SERVICE SPEEDS TO DRIVE MARKET

9.4

151–745 KW

9.4.1

FERRY ELECTRIFICATION PROGRAMS AND DECARBONIZATION POLICIES TO DRIVE MARKET

9.5

746–7,560 KW

9.5.1

EMPHASIS ON SYSTEM RELIABILITY AND ENDURANCE TO DRIVE MARKET

9.6

>7,560 KW

9.6.1

INTRODUCTION OF ALTERNATIVE ENERGY SOURCES INTO OCEANGOING SHIPPING TO DRIVE MARKET

10

ELECTRIC SHIP MARKET, BY RANGE (MARKET SIZE & FORECAST TO 2032 – USD MILLION)

Market Size & Growth Rate Forecast Analysis to 2032 in USD Million | 2 Data Tables

148

10.1

INTRODUCTION

10.2

<50 KM

10.2.1

COMMERCIAL VIABILITY FOR ELECTRIC PROPULSION ADOPTION TO DRIVE MARKET

10.3

50–100 KM

10.3.1

REGIONAL CONNECTIVITY NEEDS TO DRIVE MARKET

10.4

101–1,000 KM

10.4.1

VESSEL OPERATIONS REQUIRING EXTENDED ENDURANCE AND CONSISTENT PERFORMANCE TO DRIVE MARKET

10.5

>1,000 KM

10.5.1

CONTINUOUS HIGH-POWER OUTPUT REQUIREMENT FOR PROLONGED PERIOD TO DRIVE MARKET

11

ELECTRIC SHIP MARKET, BY TONNAGE (MARKET SIZE & FORECAST TO 2032 – USD MILLION)

Market Size & Growth Rate Forecast Analysis to 2032 in USD Million | 2 Data Tables

152

11.1

INTRODUCTION

11.2

<500 DWT

11.2.1

REDUCED PROPULSION DEMAND DUE TO LIMITED CARGO AND PASSENGER CAPACITY TO DRIVE MARKET

11.3

500–5,000 DWT

11.3.1

OPERATIONAL DEMANDS FOR SCALABLE AND MODULAR PROPULSION SOLUTIONS TO DRIVE MARKET

11.4

5,001–15,000 DWT

11.4.1

NEED FOR HIGHER PROPULSION CAPACITY AND ENDURANCE TO DRIVE MARKET

11.5

>15,000 DWT

11.5.1

EXTENSIVE USE OF HYBRID CONFIGURATIONS TO DRIVE MARKET

12

ELECTRIC SHIP MARKET, BY SHIP TYPE (MARKET SIZE & FORECAST TO 2032 – USD MILLION)

Market Size & Growth Rate Forecast Analysis to 2032 in USD Million | 12 Data Tables

156

12.1

INTRODUCTION

12.2

COMMERCIAL

12.2.1

STRINGENT ENVIRONMENTAL REGULATIONS AND EXPANSION OF CHARGING INFRASTRUCTURE TO DRIVE MARKET

12.2.2

PASSENGER VESSELS

12.2.2.1

YACHTS

12.2.2.2

FERRIES

12.2.2.3

CRUISE SHIPS

12.2.2.4

MOTORBOATS

12.2.3

CARGO VESSELS

12.2.3.1

CONTAINER VESSELS

12.2.3.2

BULK CARRIERS

12.2.3.3

TANKERS

12.2.3.4

GENERAL CARGO SHIPS

12.2.4

OTHERS

12.2.4.1

FISHING VESSELS

12.2.4.2

TUGS & WORKBOATS

12.2.4.3

RESEARCH VESSELS

12.2.4.4

DREDGERS

12.2.4.5

SUBMARINES

12.3

DEFENSE

12.3.1

NAVAL MODERNIZATION PROGRAMS TO DRIVE MARKET

12.3.2

DESTROYERS

12.3.3

FRIGATES

12.3.4

CORVETTES

12.3.5

OFFSHORE SUPPORT VESSELS

12.3.6

AIRCRAFT CARRIERS

12.3.7

SUBMARINES

13

ELECTRIC SHIP MARKET, BY REGION (MARKET SIZE & FORECAST TO 2032 – USD MILLION)

Comprehensive coverage of 8 Regions with country-level deep-dive of 16 Countries | 236 Data Tables.

167

13.1

INTRODUCTION

13.2

NORTH AMERICA

13.2.1

PESTLE ANALYSIS

13.2.2

US

13.2.2.1

RISE OF MARITIME ELECTRIFICATION TO DRIVE MARKET

13.2.3

CANADA

13.2.3.1

ADVANCES IN ELECTRIC SHIPPING THROUGH FLEET RENEWAL AND INTEGRATED INFRASTRUCTURE PROGRAMS TO DRIVE MARKET

13.3

EUROPE

13.3.1

PESTLE ANALYSIS

13.3.2

NORWAY

13.3.2.1

SHIFT FROM TRADITIONAL FOSSIL-FUEL-POWERED VESSELS TO ELECTRIC ALTERNATIVES TO DRIVE MARKET

13.3.3

SWEDEN

13.3.3.1

ROBUST NATIONAL SUSTAINABILITY AGENDA TO DRIVE MARKET

13.3.4

NETHERLANDS

13.3.4.1

TRANSITION TO ZERO-EMISSION SHIPPING TO DRIVE MARKET

13.3.5

FINLAND

13.3.5.1

ADVANCED SHIPBUILDING EXPERTISE TO DRIVE MARKET

13.3.6

DENMARK

13.3.6.1

FAVORABLE ENVIRONMENTAL REGULATIONS TO DRIVE MARKET

13.3.7

UK

13.3.7.1

REGULATORY PUSH FOR ZERO-EMISSION SHIPPING TO DRIVE MARKET

13.3.8

REST OF EUROPE

13.4

ASIA PACIFIC

13.4.1

PESTLE ANALYSIS

13.4.2

CHINA

13.4.2.1

DOMESTIC BATTERY AND POWER ELECTRONICS LEADERSHIP TO DRIVE MARKET

13.4.3

JAPAN

13.4.3.1

GOVERNMENT-LED AUTONOMY INITIATIVES TO DRIVE MARKET

13.4.4

AUSTRALIA

13.4.4.1

INFRASTRUCTURE MODERNIZATION AND INNOVATION AGILITY TO DRIVE MARKET

13.4.5

SOUTH KOREA

13.4.5.1

POLICY-BACKED FLEETS, GREEN POWER SUPPLY, AND SHIPYARD DOMINANCE TO DRIVE MARKET

13.4.6

INDIA

13.4.6.1

INFRASTRUCTURE MODERNIZATION AND SOLAR INNOVATION TO DRIVE MARKET

13.4.7

REST OF ASIA PACIFIC

13.5

MIDDLE EAST

13.5.1

PESTLE ANALYSIS

13.5.2

GCC

13.5.2.1

SAUDI ARABIA

13.5.2.2

UAE

13.5.3

ISRAEL

13.5.3.1

TECHNOLOGY INTEGRATION AND NAVAL MODERNIZATION TO DRIVE MARKET

13.5.4

TURKEY

13.5.4.1

COMPLIANCE WITH INTERNATIONAL TRADE AND SHIPPING REGULATIONS TO DRIVE MARKET

13.6

REST OF THE WORLD

13.6.1

PESTLE ANALYSIS

13.6.2

AFRICA

13.6.2.1

URBAN TRANSIT MODERNIZATION AND TOURISM-LED INITIATIVES TO DRIVE MARKET

13.6.3

LATIN AMERICA

13.6.3.1

INLAND WATERWAY SCALE AND ECO-TOURISM TO DRIVE MARKET

14

COMPETITIVE LANDSCAPE

Uncover strategic market shifts and dominant players shaping competitive dynamics through 2025.

240

14.1

INTRODUCTION

14.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022–2025

14.3

MARKET SHARE ANALYSIS, 2024

14.3.1

SHARE ANALYSIS OF ABB, WÄRTSILÄ, SCHOTTEL GROUP, CORVUS ENERGY & GE VERNOVA

14.3.2

DEGREE OF COMPETITION

14.4

REVENUE ANALYSIS, 2021–2024

14.4.1

REVENUE OF ABB, WÄRTSILÄ, SCHOTTEL GROUP, CORVUS ENERGY & GE VERNOVA

14.5

BRAND/PRODUCT COMPARISON

14.6

COMPANY VALUATION AND FINANCIAL METRICS

14.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

14.7.1

STARS

14.7.2

EMERGING LEADERS

14.7.3

PERVASIVE PLAYERS

14.7.4

PARTICIPANTS

14.7.5

COMPANY FOOTPRINT

14.7.5.1

COMPANY FOOTPRINT

14.7.5.2

REGION FOOTPRINT

14.7.5.3

POINT OF SALE FOOTPRINT

14.7.5.4

SHIP TYPE FOOTPRINT

14.8

COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

14.8.1

PROGRESSIVE COMPANIES

14.8.2

RESPONSIVE COMPANIES

14.8.3

DYNAMIC COMPANIES

14.8.4

STARTING BLOCKS

14.8.5

COMPETITIVE BENCHMARKING

14.8.5.1

LIST OF START-UPS/SMES

14.8.5.2

COMPETITIVE BENCHMARKING OF START-UPS/SMES

14.9

COMPETITIVE SCENARIO

14.9.1

PRODUCT LAUNCHES/DEVELOPMENTS

14.9.2

DEALS

14.9.3

OTHERS

15

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

278

15.1

KEY PLAYERS

15.1.1

ABB

15.1.1.1

BUSINESS OVERVIEW

15.1.1.2

PRODUCTS OFFERED

15.1.1.3

RECENT DEVELOPMENTS

15.1.1.4

MNM VIEW

15.1.2

WÄRTSILÄ

15.1.3

SCHOTTEL GROUP

15.1.4

CORVUS ENERGY

15.1.5

GE VERNOVA

15.1.6

KONGSBERG

15.1.7

VARD AS

15.1.8

SIEMENS

15.1.9

LECLANCHÉ SA

15.1.10

BAE SYSTEMS

15.1.11

SAFT

15.1.12

NORWEGIAN ELECTRIC SYSTEMS

15.1.13

EVERLLENCE

15.1.14

ECHANDIA AB

15.1.15

ANGLO BELGIAN CORPORATION NV

15.1.16

DANFOSS

15.1.17

FJELLSTRAND AS

15.1.18

SØBY SHIPYARD

15.1.19

MITSUBISHI SHIPBUILDING CO., LTD.

15.1.20

DAMEN SHIPYARDS GROUP

15.1.21

BALTIC WORKBOATS AS

15.1.22

COCHIN SHIPYARD LIMITED

15.2

OTHER PLAYERS

15.2.1

ECO MARINE POWER CO., LTD.

15.2.2

EST FLOATTECH

15.2.3

SHIFT

15.2.4

INCAT CROWTHER

15.2.5

INGETEAM, S.A.

15.2.6

VOITH TURBO MARINE

15.2.7

YARA

16

APPENDIX

352

16.1

DISCUSSION GUIDE

16.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

16.3

CUSTOMIZATION OPTIONS

16.4

RELATED REPORTS

16.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

USD EXCHANGE RATE

TABLE 2

BATTERY CAPACITY/POWER REQUIREMENTS OF SHIPS

TABLE 3

ROLE OF COMPANIES IN ECOSYSTEM

TABLE 4

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY SHIP TYPE (%)

TABLE 5

KEY BUYING CRITERIA, BY SHIP TYPE

TABLE 6

KEY CONFERENCES AND EVENTS, 2025–2026

TABLE 7

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 8

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 9

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 10

REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 11

NEWBUILD VS. RETROFIT VESSELS, 2021–2024 (UNITS)

TABLE 12

NEWBUILD VS. RETROFIT VESSELS, 2025–2032 (UNITS)

TABLE 13

LINE FIT VS. RETROFIT PROPULSION, 2021–2024 (UNITS)

TABLE 14

LINE FIT VS. RETROFIT PROPULSION, 2025–2032 (UNITS)

TABLE 15

IMPORT DATA FOR HS CODE 8901-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD THOUSAND)

TABLE 16

EXPORT DATA FOR HS CODE 8901-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD THOUSAND)

TABLE 17

PATENT ANALYSIS

TABLE 18

AVERAGE SELLING PRICE TREND OF ELECTRIC SHIPS OFFERED BY KEY PLAYERS, 2021–2024 (USD MILLION)

TABLE 19

AVERAGE SELLING PRICE TREND, BY REGION, 2020–2024 (USD MILLION)

TABLE 20

BUSINESS MODELS IN ELECTRIC SHIP MARKET

TABLE 21

KEY OBSERVATIONS BY SUBSYSTEM & COMPONENTS OF ELECTRIC SHIPS

TABLE 22

RETROFIT PROPLULSION BILL OF MATERIALS FOR POWER STORAGE BY SHIP TYPE (%)

TABLE 23

RETROFIT PROPLULSION BILL OF MATERIALS FOR POWER CONVERSION BY SHIP TYPE (%)

TABLE 24

RETROFIT PROPLULSION BILL OF MATERIALS FOR POWER GENERATION BY SHIP TYPE (%)

TABLE 25

RETROFIT PROPLULSION BILL OF MATERIALS FOR POWER DISTRIBUTION BY SHIP TYPE (%)

TABLE 26

RETROFIT PROPLULSION BILL OF MATERIALS FOR POWER DRIVE BY SHIP TYPE (%)

TABLE 27

COST ELEMENTS & IMPACT OF COMPONENT ON TCO

TABLE 28

FUEL COST ESTIMATES 2022 TO 2050, (USD/KWH)

TABLE 29

CHARGING COST ESTIMATES 2022 TO 2050, (USD/KWH)

TABLE 30

CHARGING INFRASTRUCTURE COST ESTIMATES 2022 TO 2024, (USD/KWH)

TABLE 31

BATTERY SYSTEM COST ESTIMATES 2022 TO 2050, (USD/KWH)

TABLE 32

CO2E SOCIAL COST ESTIMATES 2022 TO 2050, (USD/CO2E TONNES)

TABLE 33

US-ADJUSTED RECIPROCAL TARIFF RATES

TABLE 34

KEY PRODUCT-RELATED TARIFF FOR ELECTRIC SHIPS

TABLE 35

ANTICIPATED CHANGES IN PRICES AND POTENTIAL IMPACT ON END-USE MARKETS

TABLE 36

NEWBUILD & LINE FIT VESSELS VS. RETROFIT, 2021–2024 (USD MILLION)

TABLE 37

NEWBUILD & LINE FIT VESSELS VS. RETROFIT, 2025–2032 (USD MILLION)

TABLE 38

ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 39

ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 40

FULLY ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 41

FULLY ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 42

HYBRID ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 43

HYBRID ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 44

LINE FIT VS. RETROFIT PROPULSION, 2021–2024 (USD MILLION)

TABLE 45

LINE FIT VS. RETROFIT PROPULSION, 2025–2032 (USD MILLION)

TABLE 46

ELECTRIC SHIP MARKET, BY SOLUTION, 2021–2024 (USD MILLION)

TABLE 47

ELECTRIC SHIP MARKET, BY SOLUTION, 2025–2032 (USD MILLION)

TABLE 48

ELECTRIC SHIP SOLUTION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 49

ELECTRIC SHIP SOLUTION MARKET, BY REGION, 2025–2032 (USD MILLION)

TABLE 50

ELECTRIC SHIP MARKET, BY AUTONOMY, 2021–2024 (USD MILLION)

TABLE 51

ELECTRIC SHIP MARKET, BY AUTONOMY, 2025–2032 (USD MILLION)

TABLE 52

ELECTRIC SHIP MARKET, BY POWER CAPACITY, 2021–2024 (USD MILLION)

TABLE 53

ELECTRIC SHIP MARKET, BY POWER CAPACITY, 2025–2032 (USD MILLION)

TABLE 54

ELECTRIC SHIP MARKET, BY RANGE, 2021–2024 (USD MILLION)

TABLE 55

ELECTRIC SHIP MARKET, BY RANGE, 2025–2032 (USD MILLION)

TABLE 56

ELECTRIC SHIP MARKET, BY TONNAGE, 2021–2024 (USD MILLION)

TABLE 57

ELECTRIC SHIP MARKET, BY TONNAGE, 2025–2032 (USD MILLION)

TABLE 58

ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 59

ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 60

COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 61

COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 62

PASSENGER VESSELS: COMMERCIAL ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 63

PASSENGER VESSELS: COMMERCIAL ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 64

CARGO VESSELS: COMMERCIAL ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 65

CARGO VESSELS: COMMERCIAL ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 66

OTHERS: COMMERCIAL ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 67

OTHERS: COMMERCIAL ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 68

DEFENSE ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 69

DEFENSE ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 70

ELECTRIC SHIP MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 71

ELECTRIC SHIP MARKET, BY REGION, 2025–2032 (USD MILLION)

TABLE 72

NORTH AMERICA: ELECTRIC SHIP MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 73

NORTH AMERICA: ELECTRIC SHIP MARKET, BY COUNTRY, 2025–2032 (USD MILLION)

TABLE 74

NORTH AMERICA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 75

NORTH AMERICA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 76

NORTH AMERICA: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 77

NORTH AMERICA: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 78

NORTH AMERICA: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 79

NORTH AMERICA: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 80

NORTH AMERICA: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 81

NORTH AMERICA: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 82

NORTH AMERICA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 83

NORTH AMERICA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 84

NORTH AMERICA: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 85

NORTH AMERICA: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 86

NORTH AMERICA: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 87

NORTH AMERICA: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 88

NORTH AMERICA: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 89

NORTH AMERICA: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 90

NORTH AMERICA: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 91

NORTH AMERICA: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 92

US: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 93

US: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 94

US: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 95

US: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 96

US: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 97

US: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 98

CANADA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 99

CANADA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 100

CANADA: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 101

CANADA: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 102

CANADA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 103

CANADA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 104

EUROPE: ELECTRIC SHIP MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 105

EUROPE: ELECTRIC SHIP MARKET, BY COUNTRY, 2025–2032 (USD MILLION)

TABLE 106

EUROPE: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 107

EUROPE: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 108

EUROPE: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 109

EUROPE: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 110

EUROPE: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 111

EUROPE: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 112

EUROPE: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 113

EUROPE: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 114

EUROPE: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 115

EUROPE: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 116

EUROPE: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 117

EUROPE: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 118

EUROPE: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 119

EUROPE: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 120

EUROPE: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 121

EUROPE: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 122

EUROPE: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 123

EUROPE: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 124

NORWAY: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 125

NORWAY: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 126

NORWAY: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 127

NORWAY: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 128

NORWAY: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 129

NORWAY: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 130

SWEDEN: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 131

SWEDEN: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 132

SWEDEN: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 133

SWEDEN: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 134

SWEDEN: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 135

SWEDEN: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 136

NETHERLANDS: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 137

NETHERLANDS: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 138

NETHERLANDS: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 139

NETHERLANDS: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 140

NETHERLANDS: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 141

NETHERLANDS: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 142

FINLAND: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 143

FINLAND: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 144

FINLAND: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 145

FINLAND: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 146

FINLAND: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 147

FINLAND: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 148

DENMARK: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 149

DENMARK: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 150

DENMARK: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 151

DENMARK: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 152

DENMARK: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 153

DENMARK: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 154

UK: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 155

UK: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 156

UK: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 157

UK: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 158

UK: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 159

UK: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 160

REST OF EUROPE: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 161

REST OF EUROPE: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 162

REST OF EUROPE: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 163

REST OF EUROPE: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 164

REST OF EUROPE: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 165

REST OF EUROPE: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 166

ASIA PACIFIC: ELECTRIC SHIP MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 167

ASIA PACIFIC: ELECTRIC SHIP MARKET, BY COUNTRY, 2025–2032 (USD MILLION)

TABLE 168

ASIA PACIFIC: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 169

ASIA PACIFIC: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 170

ASIA PACIFIC: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 171

ASIA PACIFIC: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 172

ASIA PACIFIC: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 173

ASIA PACIFIC: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 174

ASIA PACIFIC: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 175

ASIA PACIFIC: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 176

ASIA PACIFIC: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 177

ASIA PACIFIC: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 178

ASIA PACIFIC: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 179

ASIA PACIFIC: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 180

ASIA PACIFIC: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 181

ASIA PACIFIC: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 182

ASIA PACIFIC: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 183

ASIA PACIFIC: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 184

ASIA PACIFIC: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 185

ASIA PACIFIC: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 186

CHINA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 187

CHINA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 188

CHINA: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 189

CHINA: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 190

CHINA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 191

CHINA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 192

JAPAN: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 193

JAPAN: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 194

JAPAN: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 195

JAPAN: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 196

JAPAN: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 197

JAPAN: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 198

AUSTRALIA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 199

AUSTRALIA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 200

AUSTRALIA: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 201

AUSTRALIA: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 202

AUSTRALIA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 203

AUSTRALIA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 204

SOUTH KOREA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 205

SOUTH KOREA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 206

SOUTH KOREA: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 207

SOUTH KOREA: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 208

SOUTH KOREA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 209

SOUTH KOREA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 210

INDIA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 211

INDIA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 212

INDIA: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 213

INDIA: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 214

INDIA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 215

INDIA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 216

REST OF ASIA PACIFIC: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 217

REST OF ASIA PACIFIC: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 218

REST OF ASIA PACIFIC: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 219

REST OF ASIA PACIFIC: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 220

REST OF ASIA PACIFIC: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 221

REST OF ASIA PACIFIC: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 222

MIDDLE EAST: ELECTRIC SHIP MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 223

MIDDLE EAST: ELECTRIC SHIP MARKET, BY COUNTRY, 2025–2032 (USD MILLION)

TABLE 224

MIDDLE EAST: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 225

MIDDLE EAST: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 226

MIDDLE EAST: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 227

MIDDLE EAST: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 228

MIDDLE EAST: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 229

MIDDLE EAST: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 230

MIDDLE EAST: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 231

MIDDLE EAST: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 232

MIDDLE EAST: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 233

MIDDLE EAST: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 234

MIDDLE EAST: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 235

MIDDLE EAST: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 236

MIDDLE EAST: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 237

MIDDLE EAST: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 238

MIDDLE EAST: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 239

MIDDLE EAST: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 240

MIDDLE EAST: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 241

MIDDLE EAST: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 242

GCC: ELECTRIC SHIP MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 243

GCC: ELECTRIC SHIP MARKET, BY COUNTRY, 2025–2032 (USD MILLION)

TABLE 244

GCC: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 245

GCC: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 246

GCC: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 247

GCC: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 248

GCC: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 249

GCC: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 250

SAUDI ARABIA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 251

SAUDI ARABIA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 252

SAUDI ARABIA: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 253

SAUDI ARABIA: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 254

SAUDI ARABIA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 255

SAUDI ARABIA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 256

UAE: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 257

UAE: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 258

UAE: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 259

UAE: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 260

UAE: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 261

UAE: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 262

ISRAEL: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 263

ISRAEL: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 264

ISRAEL: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 265

ISRAEL: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 266

ISRAEL: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 267

ISRAEL: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 268

TURKEY: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 269

TURKEY: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 270

TURKEY: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 271

TURKEY: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 272

TURKEY: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 273

TURKEY: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 274

REST OF THE WORLD: ELECTRIC SHIP MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 275

REST OF THE WORLD: ELECTRIC SHIP MARKET, BY REGION, 2025–2032 (USD MILLION)

TABLE 276

REST OF THE WORLD: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 277

REST OF THE WORLD: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 278

REST OF THE WORLD: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 279

REST OF THE WORLD: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 280

REST OF THE WORLD: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 281

REST OF THE WORLD: FULLY ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 282

REST OF THE WORLD: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 283

REST OF THE WORLD: HYBRID ELECTRIC SHIP MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 284

REST OF THE WORLD: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 285

REST OF THE WORLD: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 286

REST OF THE WORLD: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 287

REST OF THE WORLD: COMMERCIAL ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 288

REST OF THE WORLD: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 289

REST OF THE WORLD: ELECTRIC PASSENGER VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 290

REST OF THE WORLD: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 291

REST OF THE WORLD: ELECTRIC CARGO VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 292

REST OF THE WORLD: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 293

REST OF THE WORLD: OTHER COMMERCIAL VESSEL MARKET, BY TYPE, 2025–2032 (USD MILLION)

TABLE 294

AFRICA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 295

AFRICA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 296

AFRICA: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 297

AFRICA: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 298

AFRICA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 299

AFRICA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 300

LATIN AMERICA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2021–2024 (USD MILLION)

TABLE 301

LATIN AMERICA: ELECTRIC SHIP MARKET, BY POINT OF SALE, 2025–2032 (USD MILLION)

TABLE 302

LATIN AMERICA: ELECTRIC SHIP MARKET, BY PROPULSION, 2021–2024 (USD MILLION)

TABLE 303

LATIN AMERICA: ELECTRIC SHIP MARKET, BY PROPULSION, 2025–2032 (USD MILLION)

TABLE 304

LATIN AMERICA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2021–2024 (USD MILLION)

TABLE 305

LATIN AMERICA: ELECTRIC SHIP MARKET, BY SHIP TYPE, 2025–2032 (USD MILLION)

TABLE 306

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022–2025

TABLE 307

ELECTRIC SHIP MARKET: DEGREE OF COMPETITION

TABLE 308

REGION FOOTPRINT

TABLE 309

POINT OF SALE FOOTPRINT

TABLE 310

SHIP TYPE FOOTPRINT

TABLE 311

LIST OF START-UPS/SMES

TABLE 312

COMPETITIVE BENCHMARKING OF START-UPS/SMES

TABLE 313

ELECTRIC SHIP MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, 2021–2025

TABLE 314

ELECTRIC SHIP MARKET: DEALS, 2021–2025

TABLE 315

ELECTRIC SHIP MARKET: OTHERS, 2021–2025

TABLE 316

ABB: COMPANY OVERVIEW

TABLE 317

ABB: PRODUCTS OFFERED

TABLE 318

ABB: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 319

ABB: DEALS

TABLE 320

ABB: OTHERS

TABLE 321

WÄRTSILÄ: COMPANY OVERVIEW

TABLE 322

WÄRTSILÄ: PRODUCTS OFFERED

TABLE 323

WÄRTSILÄ: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 324

WÄRTSILÄ: DEALS

TABLE 325

WÄRTSILÄ: OTHERS

TABLE 326

SCHOTTEL GROUP: COMPANY OVERVIEW

TABLE 327

SCHOTTEL GROUP: PRODUCTS OFFERED

TABLE 328

SCHOTTEL GROUP: DEALS

TABLE 329

SCHOTTEL GROUP: OTHERS

TABLE 330

CORVUS ENERGY: COMPANY OVERVIEW

TABLE 331

CORVUS ENERGY: PRODUCTS OFFERED

TABLE 332

CORVUS ENERGY: DEALS

TABLE 333

CORVUS ENERGY: OTHERS

TABLE 334

GE VERNOVA: COMPANY OVERVIEW

TABLE 335

GE VERNOVA: PRODUCTS OFFERED

TABLE 336

GE VERNOVA: DEALS

TABLE 337

GE VERNOVA: OTHERS

TABLE 338

KONGSBERG: COMPANY OVERVIEW

TABLE 339

KONGSBERG: PRODUCTS OFFERED

TABLE 340

KONGSBERG: OTHERS

TABLE 341

VARD AS: COMPANY OVERVIEW

TABLE 342

VARD AS: PRODUCTS OFFERED

TABLE 343

VARD AS: OTHERS

TABLE 344

SIEMENS: COMPANY OVERVIEW

TABLE 345

SIEMENS: PRODUCTS OFFERED

TABLE 346

LECLANCHÉ SA: COMPANY OVERVIEW

TABLE 347

LECLANCHÉ SA: PRODUCTS OFFERED

TABLE 348

LECLANCHÉ SA: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 349

LECLANCHÉ SA: DEALS

TABLE 350

LECLANCHÉ SA: OTHERS

TABLE 351

BAE SYSTEMS: COMPANY OVERVIEW

TABLE 352

BAE SYSTEMS: PRODUCTS OFFERED

TABLE 353

BAE SYSTEMS: OTHERS

TABLE 354

SAFT: COMPANY OVERVIEW

TABLE 355

SAFT: PRODUCTS OFFERED

TABLE 356

NORWEGIAN ELECTRIC SYSTEMS: COMPANY OVERVIEW

TABLE 357

NORWEGIAN ELECTRIC SYSTEMS: PRODUCTS OFFERED

TABLE 358

NORWEGIAN ELECTRIC SYSTEMS: DEALS

TABLE 359

NORWEGIAN ELECTRIC SYSTEMS: OTHERS

TABLE 360

EVERLLENCE: COMPANY OVERVIEW

TABLE 361

EVERLLENCE: PRODUCTS OFFERED

TABLE 362

EVERLLENCE: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 363

EVERLLENCE: DEALS

TABLE 364

EVERLLENCE: OTHERS

TABLE 365

ECHANDIA AB: COMPANY OVERVIEW

TABLE 366

ECHANDIA AB: PRODUCTS OFFERED

TABLE 367

ECHANDIA AB: DEALS

TABLE 368

ECHANDIA AB: OTHERS

TABLE 369

ANGLO BELGIAN CORPORATION NV: COMPANY OVERVIEW

TABLE 370

ANGLO BELGIAN CORPORATION NV: PRODUCTS OFFERED

TABLE 371

ANGLO BELGIAN CORPORATION NV: DEALS

TABLE 372

ANGLO BELGIAN CORPORATION NV: OTHERS

TABLE 373

DANFOSS: COMPANY OVERVIEW

TABLE 374

DANFOSS: PRODUCTS OFFERED

TABLE 375

DANFOSS: DEALS

TABLE 376

DANFOSS: OTHERS

TABLE 377

FJELLSTRAND AS: COMPANY OVERVIEW

TABLE 378

FJELLSTRAND AS: PRODUCTS OFFERED

TABLE 379

FJELLSTRAND AS: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 380

FJELLSTRAND AS: OTHERS

TABLE 381

SØBY SHIPYARD: COMPANY OVERVIEW

TABLE 382

SØBY SHIPYARD: PRODUCTS OFFERED

TABLE 383

MITSUBISHI SHIPBUILDING CO., LTD.: COMPANY OVERVIEW

TABLE 384

MITSUBISHI SHIPBUILDING CO., LTD.: PRODUCTS OFFERED

TABLE 385

DAMEN SHIPYARDS GROUP: COMPANY OVERVIEW

TABLE 386

DAMEN SHIPYARDS GROUP: PRODUCTS OFFERED

TABLE 387

DAMEN SHIPYARDS GROUP: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 388

DAMEN SHIPYARDS GROUP: DEALS

TABLE 389

DAMEN SHIPYARDS GROUP: OTHERS

TABLE 390

BALTIC WORKBOATS AS: COMPANY OVERVIEW

TABLE 391

BALTIC WORKBOATS AS: PRODUCTS OFFERED

TABLE 392

BALTIC WORKBOATS AS: DEALS

TABLE 393

BALTIC WORKBOATS AS: OTHERS

TABLE 394

COCHIN SHIPYARD LIMITED: COMPANY OVERVIEW

TABLE 395

COCHIN SHIPYARD LIMITED: PRODUCTS OFFERED

TABLE 396

COCHIN SHIPYARD LIMITED: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 397

COCHIN SHIPYARD LIMITED: DEALS

TABLE 398

COCHIN SHIPYARD LIMITED: OTHERS

TABLE 399

ECO MARINE POWER CO., LTD.: COMPANY OVERVIEW

TABLE 400

EST FLOATTECH: COMPANY OVERVIEW

TABLE 401

SHIFT: COMPANY OVERVIEW

TABLE 402

INCAT CROWTHER: COMPANY OVERVIEW

TABLE 403

INGETEAM, S.A.: COMPANY OVERVIEW

TABLE 404

VOITH TURBO MARINE: COMPANY OVERVIEW

TABLE 405

YARA: COMPANY OVERVIEW

LIST OF FIGURES

FIGURE 1

ELECTRIC SHIP MARKET SEGMENTATION

FIGURE 2

RESEARCH DESIGN MODEL

FIGURE 3

RESEARCH DESIGN

FIGURE 4

BOTTOM-UP APPROACH

FIGURE 5

TOP-DOWN APPROACH

FIGURE 6

DATA TRIANGULATION

FIGURE 7

COMMERCIAL TO BE LARGER THAN DEFENSE DURING FORECAST PERIOD

FIGURE 8

MANNED SEGMENT TO BE DOMINANT DURING FORECAST PERIOD

FIGURE 9

NEWBUILD & LINE FIT SEGMENT TO ACQUIRE HIGHER SHARE DURING FORECAST PERIOD

FIGURE 10

POWER DRIVE TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 11

<500 DWT SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 12

EUROPE TO EXHIBIT FASTEST GROWTH DURING FORECAST PERIOD

FIGURE 13

RISING ADOPTION OF ELECTRIC PROPULSION TO DRIVE MARKET

FIGURE 14

FULLY ELECTRIC TO HOLD HIGHER SHARE THAN HYBRID IN 2025

FIGURE 15

DIESEL & BATTERY-POWERED TO BE LARGEST SEGMENT DURING FORECAST PERIOD

FIGURE 16

PASSENGER VESSELS TO SURPASS OTHER SEGMENTS DURING FORECAST PERIOD

FIGURE 17

FERRIES TO SECURE LEADING POSITION DURING FORECAST PERIOD

FIGURE 18

ELECTRIC SHIP MARKET DYNAMICS

FIGURE 19

COMMON LITHIUM-ION BATTERIES

FIGURE 20

RELATIVE FEASIBILITY OF ENERGY STORAGE TECHNOLOGIES

FIGURE 21

TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 22

ECOSYSTEM ANALYSIS

FIGURE 23

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY SHIP TYPE

FIGURE 24

KEY BUYING CRITERIA, BY SHIP TYPE

FIGURE 25

IMPORT DATA FOR HS CODE 8901-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD THOUSAND)

FIGURE 26

EXPORT DATA FOR HS CODE 8901-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD THOUSAND)

FIGURE 27

PATENT ANALYSIS

FIGURE 28

AVERAGE SELLING PRICING TREND ELECTRIC SHIPS OFFERED BY KEY PLAYERS, 2021–2024 (USD MILLION)

FIGURE 29

AVERAGE SELLING PRICING TREND, BY REGION, 2020–2024 (USD MILLION)

FIGURE 30

INVESTMENT AND FUNDING SCENARIO, 2020–2024

FIGURE 31

BUSINESS MODELS IN ELECTRIC SHIP MARKET

FIGURE 32

VALUE CHAIN ANALYSIS

FIGURE 33

TECHNOLOGY ROADMAP OF ELECTRIC SHIP MARKET

FIGURE 34

EVOLUTION OF ELECTRIC SHIP TECHNOLOGIES

FIGURE 35

AI IN MARINE INDUSTRY

FIGURE 36