Download PDF

Download PDF Request Customisation

Request Customisation

Field-Programmable Gate Array (FPGA) Market Size, Share & Trends

Report Code

SE 3058

Published in

Oct, 2025, By MarketsandMarkets™

Field-Programmable Gate Array (FPGA) Market Size, Share & Trends by Configuration (Low-end FPGA, Mid-range FPGA, High-end FPGA), Technology (SRAM, Flash, Antifuse), Node Size (<16 nm, 20-90 nm, >90 nm), Vertical (Telecom, Data Center) and Region - Global Forecast to 2030

USD 19.34 BN

MARKET SIZE, 2030

CAGR 10.5%

(2025-2030)

300

REPORT PAGES

249

MARKET TABLES

FIELD-PROGRAMMABLE GATE ARRAY (FPGA) MARKET SIZE, SHARE & TRENDS

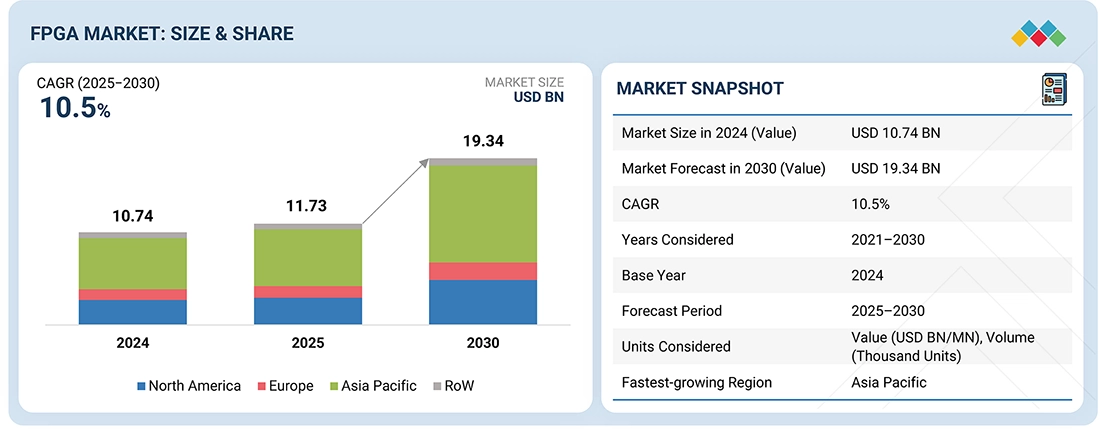

According to Marketsandmarkets, the Field-Programmable Gate Array (FPGA) market size was valued at USD 11.73 billion in 2025 and is projected to reach USD 19.34 billion in 2030 from , growing at a CAGR of 10.5% from 2025 to 2030. An FPGA is a reconfigurable semiconductor device that can be programmed after manufacturing to perform specific logic functions or digital processing tasks. The FPGA industry is driven by the rising demand for customizable and high-performance computing in data centers, telecommunications, and automotive applications, along with increasing adoption in AI acceleration, 5G infrastructure, and edge computing systems.

MARKET SNAPSHOT TABLE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2025 (Value) | USD 11.73 Billion |

| Market Forecast in 2030 (Value) | USD 19.34 Billion |

| Growth Rate | CAGR of 10.5% from 2025 to 2030 |

| Years Considered | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Thousand Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Top Companies |

|

| Growth Drivers |

|

| Segments Covered |

|

| Regional Scope | North America, Europe, Asia Pacific, and RoW |

The FPGA Market share has been expanding steadily due to the rising demand for high-performance and flexible semiconductor solutions across multiple industries. Field Programmable Gate Arrays are widely used in telecommunications, data centers, automotive electronics, and industrial automation, contributing significantly to overall FPGA Market growth. The increasing deployment of 5G infrastructure, artificial intelligence workloads, and edge computing devices is also strengthening the FPGA Market share of leading semiconductor companies. In addition, emerging FPGA Market trends such as heterogeneous computing, hardware acceleration, and low-power programmable chips are reshaping the global FPGA Industry, enabling organizations to build faster and more efficient processing systems.

Furthermore, the expansion of cloud computing and data center infrastructure is playing a crucial role in driving FPGA Market growth worldwide. Major technology companies are increasingly integrating FPGA-based accelerators to enhance computing performance, which is positively impacting the overall FPGA Market size. At the same time, evolving FPGA Market trends such as AI acceleration, automotive ADAS systems, and edge AI processing are opening new opportunities within the FPGA Industry. As innovation in programmable logic devices continues to advance, the FPGA Market share is expected to grow significantly, positioning the FPGA Industry as a key contributor to next-generation semiconductor technologies.

Market Size & Forecast

• 2025 Market Size: USD 11.73 billion

• 2030 Projected Market Size: USD 19.34 billion

• CAGR (2025-2030): 10.5%

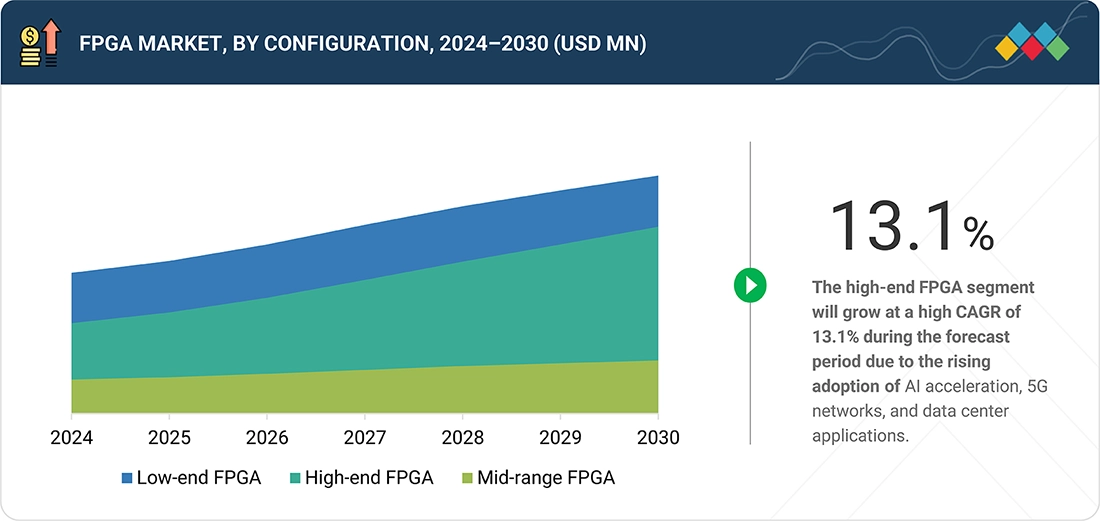

• High-end FPGA segment: Expected to register the highest CAGR of 13.1%

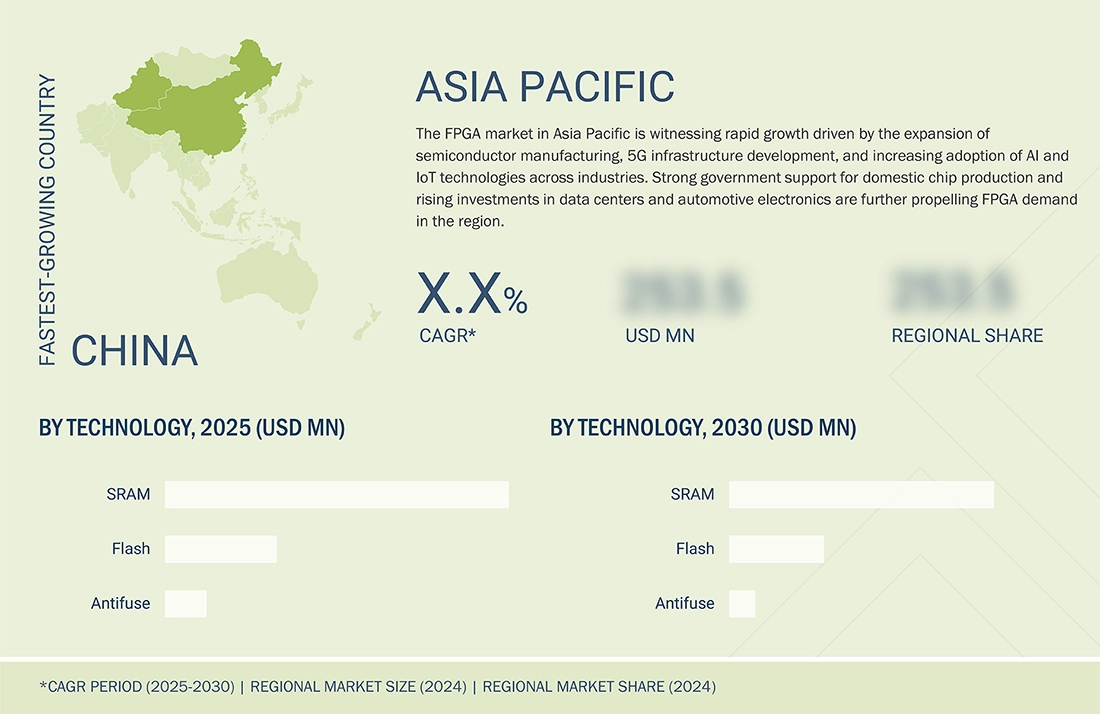

• Asia Pacific: Accounted for a 55.3% revenue share

FIELD-PROGRAMMABLE GATE ARRAY (FPGA) MARKET KEY TAKEAWAYS

- The Asia Pacific FPGA market accounted for a 55.3% revenue share in 2024.

- By configuration, the high-end FPGA segment is expected to register the highest CAGR of 13.1%.

- By node size, the 20-90 NM segment is expected to dominate the market.

- By technology, the flash segment is projected to grow at the fastest rate from 2025 to 2030.

- By FPGA and eFPGA, the eFPGA segment is expected to grow at the highest CAGR of 18.4%.

- By vertical, the data center and computing segment is expected to grow at highest CAGR.

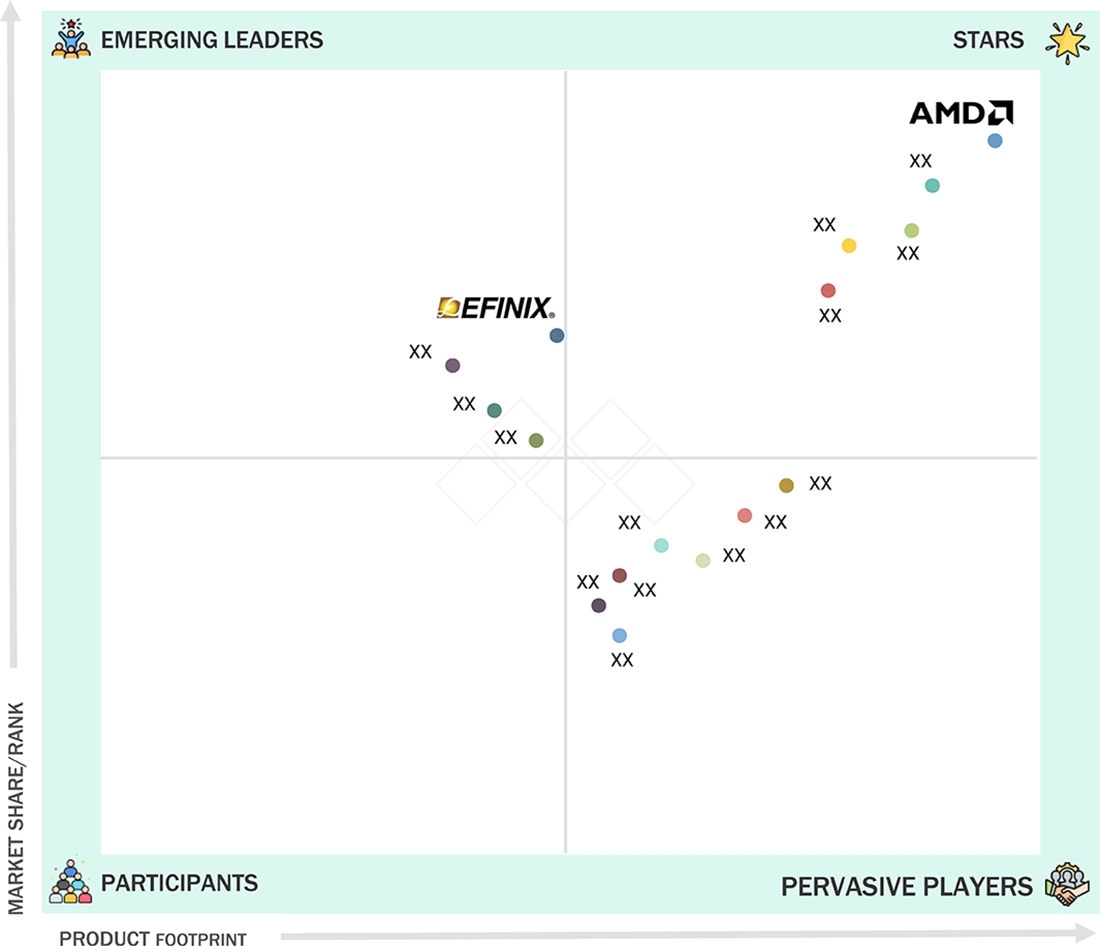

- Advanced Micro Devices, Inc., Altera Corporation, Lattice Semiconductor Corporation were identified as some of the star players in the FPGA market, given their strong market share and product footprint.

- QuickLogic Corporation, Efinix, Inc., GOWIN Semiconductor Corp., among others, have distinguished themselves among startups and SMEs by securing strong footholds in specialized niche areas, underscoring their potential as emerging market leaders

The FPGA market growth is experiencing strong growth driven by increasing demand for reconfigurable and high-performance computing across data centers, telecommunications, and automotive applications. The proliferation of AI and machine learning workloads, alongside rapid 5G network expansion, is accelerating FPGA adoption due to their parallel processing and low-latency capabilities. Additionally, advancements in system-on-chip (SoC) FPGAs and embedded FPGA (eFPGA) integration are broadening use cases in edge computing and IoT devices. As industries prioritize flexibility, energy efficiency, and faster prototyping, FPGAs are emerging as a cornerstone technology for next-generation intelligent hardware systems.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

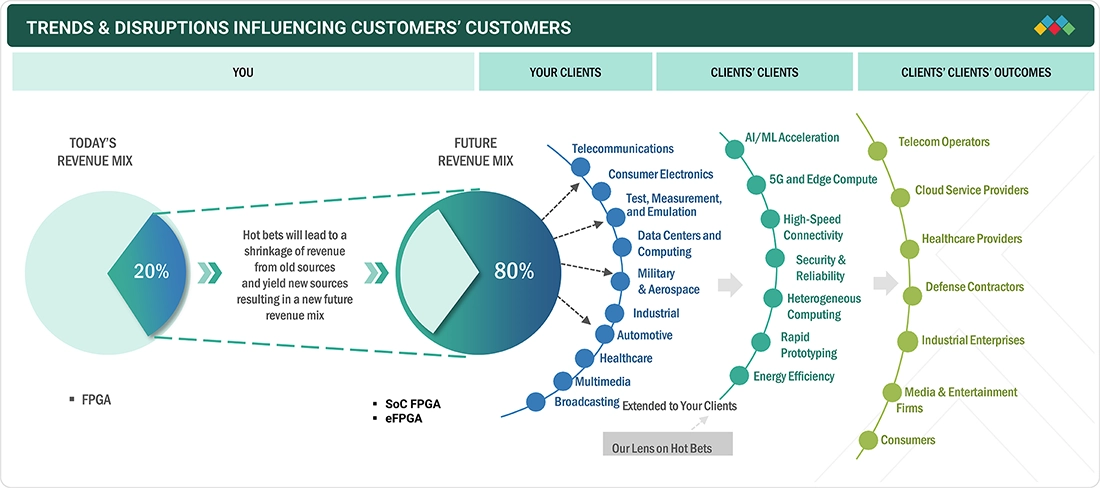

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

Customers across telecommunications, data centers, automotive, healthcare, and industrial sectors are navigating a landscape of rapid technological evolution and market disruption, driven by AI/ML adoption, 5G rollout, edge computing, and heterogeneous computing architectures. The shift from traditional FPGA market trends applications toward SoC FPGAs and eFPGAs is enabling businesses to accelerate real-time processing, optimize energy efficiency, and deploy flexible, reprogrammable platforms.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

FIELD-PROGRAMMABLE GATE ARRAY (FPGA) MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Wide adoption of AI and IoT technologies in aerospace & defense sector

-

Integration of FPGAs into advanced driver-assistance systems

RESTRAINTS

Impact

Level

Level

-

Limited availability of skilled FPGA developers

-

Risk of data security breaches arising from hidden bugs in FPGA chips

OPPORTUNITIES

Impact

Level

Level

-

Integration of FPGA technology into high-bandwidth devices

-

Rollout of 5G technology

CHALLENGES

Impact

Level

Level

-

Lack of standardized FPGA verification and validation techniques

-

Extended design cycles due to complexities associated with FPGA programming

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Wide adoption of AI and IoT technologies in aerospace & defense sector

The aerospace & defense sector is increasingly leveraging AI and IoT technologies for real-time data analysis, autonomous systems, and mission-critical applications. FPGAs play a key role in enabling high-speed processing, low-latency computations, and reconfigurable hardware for radar, avionics, and satellite systems. The growing need for adaptive and secure systems in defense operations is driving FPGA adoption, as they allow rapid customization and integration with AI-enabled sensors and communication networks. This trend is accelerating investments in FPGA-based solutions to meet the sector’s evolving technological demands.

Restraint: Limited availability of skilled FPGA developers

The FPGA market faces a shortage of skilled engineers who can effectively design, program, and optimize complex FPGA architectures. This talent gap slows down development cycles, increases project costs, and limits adoption among small and mid-sized enterprises. As FPGA applications become more sophisticated, especially in AI, 5G, and automotive sectors, the demand for specialized knowledge in hardware description languages (HDLs), high-level synthesis, and embedded system design grows.

Opportunity: Integration of FPGA technology into high-bandwidth devices

Integrating FPGAs into high-bandwidth devices such as 5G base stations, data center accelerators, and edge AI platforms presents significant growth potential. FPGAs can provide real-time processing, low latency, and adaptability to evolving communication protocols, making them ideal for bandwidth-intensive applications. This integration enables OEMs and system designers to deliver scalable and future-proof solutions while optimizing energy efficiency and performance. As device complexity increases, the role of FPGAs in enhancing throughput and flexibility becomes even more critical.

Challenge: Lack of standardized FPGA verification and validation techniques

FPGA development often geta affected from the absence of standardized verification and validation methodologies, leading to longer design cycles and a higher risk of functional errors. Different vendors and toolchains use varying simulation and testing protocols, making cross-platform integration and reliability assurance difficult. This challenge is particularly pronounced in safety-critical industries such as automotive, aerospace, and healthcare, where errors can have severe consequences. Addressing this requires the development of unified verification frameworks, the adoption of automated validation tools, and adherence to industry-wide best practices.

Field-Programmable Gate Array (FPGA) Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Magewell used AMD Artix UltraScale+ FPGAs to develop a 4K media capture device supporting 20 Gb/s USB 3.2 Gen 2x2 connectivity, ensuring high-speed data transmission and power efficiency. | Achieved stable 20 Gb/s USB performance, enhanced I/O efficiency, reduced development time, lower power consumption, and faster time-to-market |

|

DigiBird integrated Xilinx Kintex-7 and Kintex UltraScale+ FPGAs to build a lossless distributed audiovisual solution, replacing lossy H.264/H.265 compression for control room and conferencing systems. | Delivered ultra-low latency, lossless video streaming, faster product deployment, and high-quality visuals for mission-critical AV systems |

|

|

Newtouch Electronics employed Xilinx Virtex UltraScale+ VU19P FPGAs in its 4th-gen PHINEDesign platform for large-scale ASIC/SoC prototyping and verification in China’s semiconductors industry. | Improved verification efficiency by 30%, reduced workload by 50%, shortened verification cycles, and accelerated chip time-to-market |

|

TU Berlin researchers utilized Gidel’s ProcStar FPGA boards to develop a flexible Software-defined Radio (SDR) system for research, teaching, and real-time digital signal processing. | Enabled 250 MHz RF bandwidth, scalable SDR capabilities, real-time processing, and flexible system upgrades using advanced FPGA hardware |

|

|

Flex Ltd. partnered with Intel to integrate Cyclone IV FPGAs into its SMT production line for real-time analytics, predictive maintenance, and Industry 4.0 transformation. | Enhanced productivity, reduced downtime, enabled predictive maintenance, improved flexibility, and achieved intelligent, connected manufacturing |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

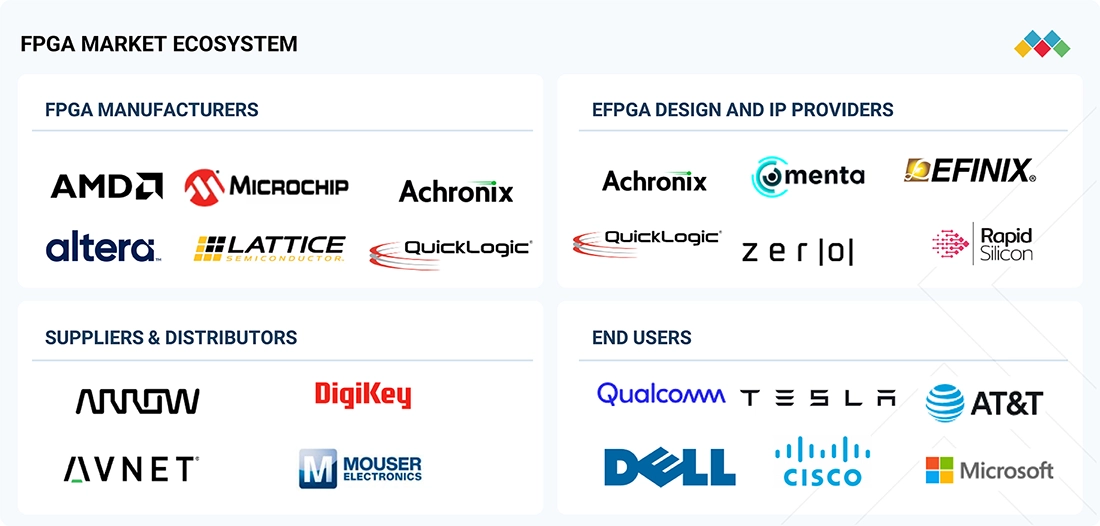

FIELD-PROGRAMMABLE GATE ARRAY (FPGA) MARKET ECOSYSTEM

The FPGA ecosystem is an interconnected network spanning device manufacturers, eFPGA design and IP providers, suppliers and distributors, and vertical end markets. FPGA manufacturers develop and produce programmable logic devices that serve as the foundation for diverse applications, while eFPGA IP providers and design partners enable the integration of customizable logic into SoCs and ASICs, accelerating time-to-market and supporting application-specific innovations.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

FIELD-PROGRAMMABLE GATE ARRAY (FPGA) MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

FPGA Market, By Configuration

The low-end FPGA segment is expected to dominate the market due to its widespread use in cost-sensitive and power-efficient applications such as industrial control systems, consumer electronics, and IoT devices. These FPGAs offer the right balance of flexibility, low power consumption, and affordability, making them ideal for edge and embedded systems. The growing miniaturization of electronics and demand for rapid product customization are further driving the adoption of low-end FPGAs across multiple industries.

FPGA Market, By Node Size

FPGAs built on ≤16 nm process nodes are expected to witness the highest growth rate as they deliver superior performance, lower power consumption, and higher logic density. The shift toward smaller nodes enables the integration of AI acceleration and advanced signal processing in compact form factors, ideal for data center, automotive, and 5G applications. As semiconductor manufacturers invest in next-generation fabrication technologies, sub-16 nm FPGAs are becoming central to high-speed computing and AI-driven workloads.

FPGA Market, By Technology

SRAM-based FPGAs hold the largest market share owing to their reprogrammability, high-speed operation, and adaptability for complex system architectures. They are widely deployed in networking, data center, and defense applications that demand frequent updates and configuration flexibility. The continuous evolution of SRAM architectures with enhanced security and power optimization features further reinforces their dominance in the FPGA landscape.

FPGA and eFPGA Market Size

The eFPGA segment is projected to grow at a rapid pace as more chipmakers integrate reconfigurable logic blocks directly into ASICs and SoCs for application-specific flexibility. This trend allows developers to achieve performance efficiency while maintaining adaptability for evolving workloads in AI, edge, and automotive systems. Increasing collaboration between eFPGA IP providers and semiconductor foundries is also driving faster adoption across custom silicon designs.

FPGA Market, By Vertical

The telecommunications vertical dominates the FPGA market, fueled by the expansion of 5G infrastructure, network virtualization, and high-speed data transmission requirements. FPGAs enable real-time signal processing, beamforming, and low-latency communication, making them critical for telecom base stations and edge networks. The transition toward open and software-defined network architectures further amplifies FPGA deployment across the telecom ecosystem.

FIELD-PROGRAMMABLE GATE ARRAY (FPGA) MARKET BY REGION

Asia Pacific to be fastest-growing region in global FPGA market during forecast period

The Asia Pacific is expected to register the fastest growth in the FPGA market, driven by strong semiconductor manufacturing bases in China, Japan, South Korea, and India. Rapid 5G deployment, industrial automation, and increasing adoption of AI-enabled devices are propelling regional demand. Furthermore, government initiatives supporting local chip production and R&D investments are positioning the Asia Pacific as a key hub for FPGA innovation and deployment.

Field-Programmable Gate Array (FPGA) Market: COMPANY EVALUATION MATRIX

The company evaluation matrix for the FPGA market highlights the positioning of key players based on their product capabilities, technological innovation, and market expansion strategies. In the FPGA market matrix, Advanced Micro Devices (AMD), Inc. leads with its broad portfolio of high-performance and adaptive FPGA solutions, advanced AI acceleration capabilities, and strong presence across data center, telecommunications, and automotive applications. Efinix, Inc. on the other hand, is rapidly gaining momentum with its innovative Trion FPGAs and low-power, cost-efficient solutions, targeting emerging applications in edge computing, IoT, and industrial automation.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

WHAT IS IN IT FOR YOU: Field-Programmable Gate Array (FPGA) Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Local Competitive Landscape | Profiles of key regional players in the FPGA market, including market share, revenue, product portfolios, and strategic initiatives in programmable logic devices and adaptive computing | Facilitated competitive benchmarking and informed strategy development |

| Regional Market Entry Strategy | Country- or region-specific go-to-market strategies, including barriers, regulations, and competitive landscape for FPGA technologies in semiconductors and electronics | Minimized entry risk and accelerated market adoption |

| Local Risk & Opportunity Assessment | Identification of regional risks, barriers, and untapped opportunities by market or sector in FPGA applications | Enabled proactive risk mitigation and strategic investments |

| Technology Adoption by Region | Insights on local adoption of key FPGA technologies (SRAM, Flash, Antifuse) and node sizes (≤16 nm, 20-90 nm, >90 nm) | Guided R&D, product positioning, and investment decisions |

| Vertical-specific Customization Strategies | Tailored analyses for sectors like telecommunications, data centers, automotive, and aerospace, covering FPGA use cases, integration challenges, and scalability | Enhanced sector-specific innovation and deployment efficiency |

RECENT DEVELOPMENTS IN FIELD-PROGRAMMABLE GATE ARRAY (FPGA)

- September 2025 : Altera Corporation completed the Silver Lake acquisition, finalizing its transition into the world’s largest independent FPGA solutions provider. The investment empowers Altera to enhance customer and partner support through a full-stack FPGA portfolio, robust software tools, and resilient supply chains, ensuring accessible, high-performance AI and programmable solutions across global markets.

- July 2024 : Microchip Technology Inc. introduced new milestones for its Radiation-Tolerant (RT) PolarFire family, including the availability of engineering samples for the RT PolarFire SoC FPGA. Leveraging nonvolatile technology for radiation immunity and up to 50% lower power consumption than SRAM-based devices, the RT PolarFire SoC FPGA ensures mission-critical reliability, reduced system complexity, and optimized SWaP for advanced space applications.

- January 2025 : QuickLogic Corporation and Honeywell International Inc. entered a strategic collaboration to develop Radiation-Hardened (SRH) FPGA technology for aerospace and Department of Defense applications. Valued at approximately USD 15 million over 4 years, the collaboration focuses on advanced FPGAs tailored for strategic space systems and defense needs.

- July 2025 : Lattice Semiconductor Corporation and Mitsubishi Electric collaborated to integrate Lattice’s low-power CertusPro-NX FPGAs into Mitsubishi Electric’s CNC solutions. This collaboration enables high-accuracy, adaptable, and energy-efficient factory automation, supporting industrial applications in machine building, automotive, and electronics.

- March 2024 : Advanced Micro Devices, Inc. launched the Spartan UltraScale+ FPGA family, expanding its portfolio of cost-optimized FPGAs for I/O-intensive edge applications. Built on a proven 16nm fabric, these devices offer the industry's highest I/O to logic cell ratio in their class, up to 30 percent lower total power than the previous generation, and robust security features. The Spartan UltraScale+ FPGAs enable seamless any-to-any connectivity for sensing and control with high I/O counts, flexible interfaces, and an ultra-compact footprint.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

35

2

RESEARCH METHODOLOGY

40

3

EXECUTIVE SUMMARY

53

4

PREMIUM INSIGHTS

58

5

MARKET OVERVIEW

AI and IoT drive FPGA demand, unlocking aerospace advancements and cross-sector growth opportunities.

61

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

WIDE ADOPTION OF AI AND IOT TECHNOLOGIES IN AEROSPACE & DEFENSE INDUSTRY

5.2.1.2

INTEGRATION OF FPGAS INTO ADVANCED DRIVER ASSISTANCE SYSTEMS

5.2.1.3

INCREASING DEPLOYMENT OF DATA CENTERS AND HIGH-PERFORMANCE COMPUTING FACILITIES

5.2.1.4

GROWING DEMAND FOR FPGA HARDWARE TESTING AND VERIFICATION SERVICES TO ENHANCE AVIONICS SYSTEM PERFORMANCE

5.2.1.5

GROWTH IN DEMAND FOR FPGAS TO HANDLE COMPLEX SENSOR DATA AND EXECUTE AI ALGORITHMS IN REAL TIME

5.2.2

RESTRAINTS

5.2.2.1

LIMITED AVAILABILITY OF SKILLED FPGA DEVELOPERS

5.2.2.2

RISK OF DATA SECURITY BREACHES ARISING FROM HIDDEN BUGS IN FPGA CHIPS

5.2.3

OPPORTUNITIES

5.2.3.1

INTEGRATION OF FPGA TECHNOLOGY INTO HIGH-BANDWIDTH DEVICES

5.2.3.2

ROLLOUT OF 5G TECHNOLOGY

5.2.3.3

UTILIZATION OF EFPGAS IN MILITARY AND AEROSPACE APPLICATIONS

5.2.4

CHALLENGES

5.2.4.1

LACK OF STANDARDIZED FPGA VERIFICATION AND VALIDATION TECHNIQUES

5.2.4.2

EXTENDED DESIGN CYCLES DUE TO COMPLEXITIES ASSOCIATED WITH FPGA PROGRAMMING

5.3

UNMET NEEDS AND WHITE SPACES

5.3.1

UNMET NEEDS IN FPGA MARKET

5.3.2

WHITE SPACE OPPORTUNITIES

5.4

INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

5.4.1

INTERCONNECTED MARKETS

5.4.2

CROSS-SECTOR OPPORTUNITIES

5.5

STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5.5.1

STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

6

INDUSTRY TRENDS

Uncover strategic shifts and pricing dynamics reshaping the competitive FPGA landscape.

76

6.1

INTRODUCTION

6.2

PORTER’S FIVE FORCES ANALYSIS

6.2.1

THREAT OF NEW ENTRANTS

6.2.2

THREAT OF SUBSTITUTES

6.2.3

BARGAINING POWER OF SUPPLIERS

6.2.4

BARGAINING POWER OF BUYERS

6.2.5

INTENSITY OF COMPETITIVE RIVALRY

6.3

MACROECONOMIC INDICATORS

6.3.1

INTRODUCTION

6.3.2

GDP TRENDS AND FORECAST

6.3.3

TRENDS IN LOGIC SEMICONDUCTORS INDUSTRY

6.3.4

TRENDS IN DATA CENTER INDUSTRY

6.4

VALUE CHAIN ANALYSIS

6.5

ECOSYSTEM ANALYSIS

6.6

PRICING ANALYSIS

6.6.1

AVERAGE SELLING PRICE OF FPGAS OFFERED BY TOP 3 KEY PLAYERS, BY VERTICAL, 2024

6.6.1.1

AVERAGE SELLING PRICE OF LOW-END FPGAS OFFERED BY TOP 3 KEY PLAYERS, BY VERTICAL, 2024

6.6.1.2

AVERAGE SELLING PRICE OF MID-RANGE FPGAS OFFERED BY TOP 3 KEY PLAYERS, BY VERTICAL, 2024

6.6.1.3

AVERAGE SELLING PRICE OF HIGH-END FPGAS OFFERED BY TOP 2 PLAYERS, BY VERTICAL, 2024

6.6.2

AVERAGE SELLING PRICE, BY REGION, 2021–2024

6.7

TRADE ANALYSIS

6.7.1

IMPORT DATA (HS CODE 854239)

6.7.2

EXPORT SCENARIO (HS CODE 854239)

6.8

KEY CONFERENCES AND EVENTS, 2025–2026

6.9

TRENDS/DISRUPTIONS IMPACTING CUSTOMERS’ BUSINESSES

6.10

INVESTMENT AND FUNDING SCENARIO, 2021–2025

6.11

CASE STUDY ANALYSIS

6.11.1

CANOGA PERKINS ACCELERATED AI-READY PRIVATE 5G NETWORKS WITH AMD VIRTEX ULTRASCALE+ FPGAS FOR DETERMINISTIC, ULTRA-LOW-LATENCY CONNECTIVITY

6.11.2

MAGEWELL ENHANCED 4K MEDIA CAPTURE PERFORMANCE USING AMD ARTIX ULTRASCALE+ FPGAS

6.11.3

DIGIBIRD’S AUDIOVISUAL SOLUTION EQUIPPED WITH XILINX’S KINTEX SERIES FPGA

6.11.4

NEWTOUCH’S FOURTH-GENERATION LARGE-SCALE PROTOTYPING SYSTEM EQUIPPED WITH XILINX’S FPGA

6.11.5

PERSEVERANCE ROVER EMPLOYED AMD’S FPGA-BASED HARDWARE ACCELERATION FOR IMAGE PROCESSING AND NAVIGATION TASKS

6.11.6

TECHNICAL UNIVERSITY OF BERLIN DEVELOPED SOFTWARE-DEFINED RADIO SYSTEM USING GIDEL’S FPGA PLATFORM

6.11.7

FLEX AND INTEL PARTNERED TO REVOLUTIONIZE SMT PRODUCTION WITH FPGA-BASED SOLUTIONS

6.12

IMPACT OF 2025 US TARIFFS

6.12.1

KEY TARIFF RATES

6.12.2

PRICE IMPACT ANALYSIS

6.12.3

IMPACT ON VARIOUS COUNTRIES/REGIONS

6.12.3.1

US

6.12.3.2

EUROPE

6.12.3.3

ASIA PACIFIC

6.12.4

IMPACT ON VERTICALS

7

CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

Unlock insights on stakeholder influence and unmet needs shaping FPGA market decisions.

109

7.1

DECISION-MAKING PROCESS

7.2

KEY STAKEHOLDERS AND BUYING CRITERIA

7.2.1

KEY STAKEHOLDERS IN BUYING PROCESS

7.2.2

BUYING CRITERIA

7.3

ADOPTION BARRIERS AND INTERNAL CHALLENGES

7.4

UNMET NEEDS FROM VARIOUS VERTICALS

8

REGULATORY LANDSCAPE

Navigate complex regulations with insights on global standards and key compliance bodies.

114

8.1

INTRODUCTION

8.1.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

8.1.2

STANDARDS

8.1.2.1

DO-254

8.1.2.2

ANSI/VITA STANDARDS

8.1.2.3

MOISTURE SENSITIVITY LEVEL

8.1.2.4

ISO 9001:2015

8.1.2.5

ISO 14001:2015

8.1.2.6

INTERNATIONAL AUTOMOTIVE TASK FORCE 16949

8.1.2.7

IEEE 1149.1

8.1.2.8

UL 60950-1

8.1.2.9

IEC 62368-1

8.1.2.10

IEC 62443

8.1.2.11

IEC 61508

8.1.2.12

JEDEC JESD47

8.1.2.13

ROHS (RESTRICTION OF HAZARDOUS SUBSTANCES) DIRECTIVE (EU 2011/65/EU)

8.1.3

GOVERNMENT REGULATIONS

8.1.3.1

US

8.1.3.2

EUROPE

8.1.3.3

CHINA

8.1.3.4

JAPAN

8.1.3.5

INDIA

9

STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

Harness AI and emerging tech for strategic disruption and competitive edge in FPGA market.

123

9.1

KEY EMERGING TECHNOLOGIES

9.1.1

EMBEDDED PROCESSORS

9.1.2

ON-CHIP MEMORY

9.1.3

HETEROGENEOUS INTEGRATION

9.2

COMPLEMENTARY TECHNOLOGIES

9.2.1

HIGH-SPEED INTERFACES AND PROTOCOLS

9.2.2

COOLING AND POWER MANAGEMENT SOLUTIONS

9.3

ADJACENT TECHNOLOGIES

9.3.1

APPLICATION-SPECIFIC INTEGRATED CIRCUIT (ASIC)

9.3.2

GRAPHICS PROCESSING UNIT (GPU)

9.3.3

SYSTEM-ON-CHIP (SOC)

9.4

TECHNOLOGY/PRODUCT ROADMAP

9.4.1

SHORT-TERM (2025–2027): ARCHITECTURE OPTIMIZATION AND AI INTEGRATION

9.4.2

MID-TERM (2027–2030): HETEROGENEOUS INTEGRATION & DESIGN ECOSYSTEM EXPANSION

9.4.3

LONG-TERM (2030–2035+): UNIVERSAL RECONFIGURABLE COMPUTING AND SYSTEM-LEVEL CONVERGENCE

9.5

PATENT ANALYSIS

9.6

IMPACT OF AI

9.6.1

TOP USE CASES AND MARKET POTENTIAL

9.6.2

BEST PRACTICES IN FPGA MARKET

9.6.3

CASE STUDIES OF AI IMPLEMENTATION IN FPGA MARKET

9.6.4

INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

9.6.5

CLIENTS’ READINESS TO ADOPT AI IN FPGA MARKET

10

MARKET SIZE FOR FPGA AND EFPGA

AI, edge applications, and customization fuel explosive growth in FPGA and eFPGA markets.

135

10.1

INTRODUCTION

10.2

FPGA

10.2.1

EMERGENCE OF AI/ML WORKLOADS, NETWORK VIRTUALIZATION, AND HIGH-PERFORMANCE EDGE APPLICATIONS TO DRIVE MARKET

10.3

EFPGA

10.3.1

INCREASING DEMAND FOR CUSTOMIZABLE HARDWARE ACCELERATORS, AI INFERENCE ENGINES, AND SECURE CRYPTOGRAPHIC APPLICATIONS TO DRIVE MARKET

11

FPGA MARKET, BY CONFIGURATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 5 Data Tables

139

11.1

INTRODUCTION

11.2

LOW-END FPGA

11.2.1

SURGE IN POWER-CONSCIOUS SOLUTIONS IN EMBEDDED AND INDUSTRIAL APPLICATIONS TO DRIVE DEMAND

11.3

MID-RANGE FPGA

11.3.1

ENTERPRISES SEEKING SCALABLE, HIGH-THROUGHPUT SOLUTIONS FOR DATA-CENTRIC AND NETWORKING WORKLOADS TO DRIVE DEMAND

11.4

HIGH-END FPGA

11.4.1

EXPONENTIAL GROWTH IN AI TRAINING, CLOUD COMPUTING, AND DATA CENTER WORKLOADS TO DRIVE DEMAND

12

FPGA MARKET, BY NODE SIZE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

145

12.1

INTRODUCTION

12.2

≤ 16 NM

12.2.1

DESIGNED FOR DATA-INTENSIVE, LATENCY-SENSITIVE WORKLOADS

12.3

20-90 NM

12.3.1

OFFERS MODERATE-TO-HIGH LOGIC DENSITY, MULTI-GBPS TRANSCEIVERS, AND EMBEDDED DSP AND MEMORY BLOCKS

12.4

>90 NM

12.4.1

MODERNIZATION OF DEFENSE AND SPACE INFRASTRUCTURE TO REINFORCE DEMAND FOR >90 NM RADIATION-HARDENED FPGAS

13

FPGA MARKET, BY TECHNOLOGY

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

150

13.1

INTRODUCTION

13.2

STATIC RANDOM-ACCESS MEMORY (SRAM)

13.2.1

RECONFIGURABLE, HIGH-PERFORMANCE LOGIC, AND AI/ML ACCELERATION TO DRIVE DEMAND

13.3

FLASH

13.3.1

LOW-POWER AND SECURE PROGRAMMABLE LOGIC TO DRIVE DEMAND

13.4

ANTIFUSE

13.4.1

EXTREME ENVIRONMENT TOLERANCE AND LONG-TERM SUPPORT TO STRENGTHEN ANTIFUSE FPGA MARKET

14

FPGA MARKET, BY VERTICAL

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 44 Data Tables

155

14.1

INTRODUCTION

14.2

TELECOMMUNICATIONS

14.2.1

WIRED COMMUNICATION

14.2.1.1

OPTICAL TRANSPORT NETWORK (OTN)

14.2.1.2

BACKHAUL & ACCESS NETWORK

14.2.1.3

NETWORK PROCESSING

14.2.1.4

WIRED CONNECTIVITY

14.2.1.5

PACKET-BASED PROCESSING & SWITCHING

14.2.2

WIRELESS COMMUNICATION

14.2.2.1

WIRELESS BASEBAND SOLUTIONS

14.2.2.2

WIRELESS BACKHAUL SOLUTIONS

14.2.2.3

RADIO SOLUTIONS

14.2.3

5G

14.2.3.1

GROWING 5G NETWORK CAPACITY DEMAND TO SPUR FPGA ADVANCEMENTS FOR HIGH-DENSITY LOGIC AND FAST MEMORY INTERFACES

14.3

CONSUMER ELECTRONICS

14.3.1

RISING DEMAND FOR SMART AND CONNECTED CONSUMER DEVICES TO DRIVE DEMAND

14.4

TESTING, MEASUREMENT, AND EMULATION

14.4.1

EXPANSION OF AUTOMATED TEST EQUIPMENT AND EMULATION PLATFORMS TO STRENGTHEN FPGA UTILIZATION

14.5

DATA CENTER & COMPUTING

14.5.1

STORAGE INTERFACE CONTROL

14.5.1.1

INCREASING NEED FOR ENERGY-EFFICIENT, FLEXIBLE, AND UPGRADEABLE STORAGE SYSTEMS TO DRIVE GROWTH

14.5.2

NETWORK INTERFACE CONTROL

14.5.2.1

INCREASING COMPLEXITY OF NETWORKING PROTOCOLS AND MULTI-TENANT ARCHITECTURES TO DRIVE GROWTH

14.5.3

HARDWARE ACCELERATOR

14.5.3.1

GROWTH IN REAL-TIME DATA ANALYTICS AND HIGH-PERFORMANCE COMPUTING TO DRIVE GROWTH

14.5.4

HIGH-PERFORMANCE COMPUTING

14.5.4.1

RISING DEMAND FOR EXASCALE COMPUTING, AI INTEGRATION, AND REAL-TIME SIMULATIONS TO DRIVE GROWTH

14.6

MILITARY & AEROSPACE

14.6.1

AVIONICS

14.6.1.1

GROWING USE OF PROGRAMMABLE FPGAS TO ENHANCE NEXT-GENERATION RADAR, COMMUNICATION, AND FLIGHT CONTROL CAPABILITIES

14.6.2

MISSILES AND MUNITIONS

14.6.2.1

GROWTH IN AUTONOMOUS AND SOFTWARE-DEFINED WEAPON SYSTEMS TO DRIVE GROWTH

14.6.3

RADARS AND SENSORS

14.6.3.1

ADVANCED SIGNAL PROCESSING FOR MULTI-FUNCTION RADARS TO DRIVE GROWTH

14.6.4

OTHERS

14.7

INDUSTRIAL

14.7.1

VIDEO SURVEILLANCE SYSTEMS

14.7.1.1

GROWING NEED FOR LOW-LATENCY IMAGE PROCESSING AND HARDWARE-LEVEL SECURITY TO DRIVE FPGA UTILIZATION IN SURVEILLANCE APPLICATIONS

14.7.2

MACHINE VISION SOLUTIONS

14.7.2.1

PROLIFERATION OF ROBOTICS AND AUTOMATED INSPECTION SYSTEMS TO ENHANCE DEMAND FOR FPGA-BASED MACHINE VISION ARCHITECTURE

14.7.3

INDUSTRIAL NETWORKING SOLUTIONS

14.7.3.1

EXPANDING USE OF TIME-SENSITIVE NETWORKING AND MULTI-PROTOCOL COMMUNICATION TO BOOST FPGA-BASED INDUSTRIAL CONNECTIVITY SOLUTIONS

14.7.4

INDUSTRIAL MOTOR CONTROL SOLUTIONS

14.7.4.1

INDUSTRIAL MOTOR CONTROL APPLICATIONS TO PROPEL FPGA ADOPTION FOR FASTER PROCESSING AND ADAPTIVE CONTROL

14.7.5

ROBOTICS

14.7.5.1

SURGE IN INTELLIGENT ROBOTICS AND MULTI-SENSOR SYSTEMS TO DRIVE GROWTH

14.7.6

INDUSTRIAL SENSORS

14.7.6.1

INTEGRATION OF FPGAS INTO INDUSTRIAL SYSTEMS TO ENABLE FASTER SIGNAL PROCESSING

14.7.7

OTHERS

14.8

AUTOMOTIVE

14.8.1

ADAS/SENSOR FUSION

14.8.1.1

FPGA GROWTH SUPPORTED BY INTEGRATION OF AI AND MACHINE LEARNING IN ADVANCED DRIVER ASSISTANCE SYSTEMS

14.8.2

AUTOMOTIVE INFOTAINMENT AND DRIVER INFORMATION SYSTEMS

14.8.2.1

GROWING COMPLEXITY IN AUTOMOTIVE DIGITAL COCKPITS TO DRIVE INCREASED FPGA INTEGRATION FOR INFOTAINMENT AND DRIVER INFORMATION APPLICATIONS

14.8.3

ELECTRIC VEHICLES

14.8.3.1

EV POWERTRAIN

14.8.3.2

EV CHARGING

14.8.3.3

VEHICLE-TO-GRID (V2G) COMMUNICATION

14.9

HEALTHCARE

14.9.1

IMAGE DIAGNOSTIC SYSTEMS

14.9.1.1

ULTRASOUND MACHINES

14.9.1.2

X-RAY MACHINES

14.9.1.3

CT SCANNERS

14.9.1.4

MRI MACHINES

14.9.2

WEARABLE DEVICES

14.9.2.1

GROWING INTEGRATION OF MULTI-SENSOR PLATFORMS TO SUPPORT GROWTH

14.9.3

OTHERS

14.10

MULTIMEDIA

14.10.1

AUDIO DEVICES

14.10.1.1

INCREASING CONSUMER DEMAND FOR HIGH-FIDELITY AUDIO TO DRIVE FPGA DEPLOYMENT ACROSS PROFESSIONAL AND CONSUMER ELECTRONICS

14.10.2

VIDEO PROCESSING

14.10.2.1

GROWING DEMAND FOR MULTI-FORMAT VIDEO PROCESSING TO DRIVE MARKET

14.11

BROADCASTING

14.11.1

BROADCASTING PLATFORM SYSTEMS

14.11.1.1

HIGH ADOPTION OF FPGAS DUE TO THEIR HARDWARE ACCELERATION ABILITY

14.11.2

HIGH-END BROADCASTING SYSTEMS

14.11.2.1

GROWING NEED FOR ADAPTIVE VIDEO PROCESSING AND MULTI-FORMAT COMPATIBILITY TO DRIVE DEMAND

15

FPGA MARKET, BY REGION

Comprehensive coverage of 11 Regions with country-level deep-dive of 11 Countries | 186 Data Tables.

206

15.1

INTRODUCTION

15.2

NORTH AMERICA

15.2.1

US

15.2.1.1

RISING DEFENSE MODERNIZATION AND STRATEGIC MILITARY SPENDING TO DRIVE MARKET

15.2.2

CANADA

15.2.2.1

STRATEGIC PARTNERSHIPS AND TELECOM EXPANSION TO DRIVE MARKET

15.2.3

MEXICO

15.2.3.1

EXPANSION OF HIGH-TECH MANUFACTURING AND LOCALIZED SUPPLY CHAINS TO DRIVE MARKET

15.3

EUROPE

15.3.1

GERMANY

15.3.1.1

ELECTRIC VEHICLE EXPANSION AND AUTOMOTIVE INNOVATION TO DRIVE MARKET

15.3.2

UK

15.3.2.1

GOVERNMENT-LED SEMICONDUCTOR INVESTMENTS AND DATA CENTER EXPANSION TO DRIVE MARKET

15.3.3

FRANCE

15.3.3.1

STRATEGIC EFPGA DEPLOYMENTS TO FUEL AEROSPACE AND DEFENSE TECHNOLOGY TO DRIVE MARKET

15.3.4

ITALY

15.3.4.1

STRATEGIC SEMICONDUCTOR INVESTMENTS TO DRIVE MARKET

15.3.5

REST OF EUROPE

15.4

ASIA PACIFIC

15.4.1

CHINA

15.4.1.1

LARGE-SCALE INVESTMENTS IN SEMICONDUCTOR MANUFACTURING TO DRIVE MARKET

15.4.2

JAPAN

15.4.2.1

SHIFT TOWARD SMART FACTORIES TO DRIVE MARKET

15.4.3

INDIA

15.4.3.1

DIGITAL TRANSFORMATION AND 5G ROLLOUT TO DRIVE MARKET

15.4.4

SOUTH KOREA

15.4.4.1

EXPANDING DIGITAL ECONOMY AND HIGH-PERFORMANCE COMPUTING NEEDS TO DRIVE MARKET

15.4.5

REST OF ASIA PACIFIC

15.5

REST OF THE WORLD (ROW)

15.5.1

SOUTH AMERICA

15.5.1.1

SURGING DEMAND FOR CLOUD COMPUTING AND EDGE AI APPLICATIONS TO DRIVE MARKET

15.5.2

GULF COOPERATION COUNCIL (GCC)

15.5.2.1

STRATEGIC PARTNERSHIPS IN SEMICONDUCTOR DESIGN TO DRIVE MARKET

15.5.3

REST OF MIDDLE EAST & AFRICA

16

COMPETITIVE LANDSCAPE

Gain insights into key players' strategies, market shares, and emerging leaders shaping the competitive landscape.

280

16.1

OVERVIEW

16.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021–2025

16.3

REVENUE ANALYSIS, 2021–2024

16.4

MARKET SHARE ANALYSIS, 2024

16.5

COMPANY VALUATION AND FINANCIAL METRICS

16.6

BRAND/PRODUCT COMPARISON

16.7

COMPANY EVALUATION MATRIX FOR FPGA: KEY PLAYERS, 2024

16.7.1

STARS

16.7.2

EMERGING LEADERS

16.7.3

PERVASIVE PLAYERS

16.7.4

PARTICIPANTS

16.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

16.7.5.1

COMPANY FOOTPRINT

16.7.5.2

REGIONAL FOOTPRINT

16.7.5.3

CONFIGURATION FOOTPRINT

16.7.5.4

NODE SIZE FOOTPRINT

16.7.5.5

TECHNOLOGY FOOTPRINT

16.7.5.6

VERTICAL FOOTPRINT

16.8

COMPANY EVALUATION MATRIX FOR FPGA: STARTUPS/SMES, 2024

16.8.1

PROGRESSIVE COMPANIES

16.8.2

RESPONSIVE COMPANIES

16.8.3

DYNAMIC COMPANIES

16.8.4

STARTING BLOCKS

16.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

16.8.5.1

LIST OF KEY STARTUPS/SMES

16.8.5.2

COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (1/2)

16.8.5.3

COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (2/2)

16.9

COMPETITIVE SCENARIO

16.9.1

PRODUCT LAUNCHES

16.9.2

DEALS

17

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

304

17.1

KEY PLAYERS

17.1.1

ADVANCED MICRO DEVICES, INC.

17.1.1.1

BUSINESS OVERVIEW

17.1.1.2

PRODUCTS OFFERED

17.1.1.3

RECENT DEVELOPMENTS

17.1.1.4

MNM VIEW

17.1.2

ALTERA CORPORATION

17.1.3

MICROCHIP TECHNOLOGY INC.

17.1.4

LATTICE SEMICONDUCTOR CORPORATION

17.1.5

ACHRONIX SEMICONDUCTOR CORPORATION

17.1.6

QUICKLOGIC CORPORATION

17.1.7

EFINIX, INC.

17.1.8

SHENZHEN PANGO MICROSYSTEMS CO., LTD.

17.1.9

GOWIN SEMICONDUCTOR CORP.

17.1.10

RENESAS ELECTRONICS CORPORATION

17.2

OTHER PLAYERS

17.2.1

AGM MICRO

17.2.2

SHANGHAI ANLOGIC INFOTECH CO., LTD.

17.2.3

HERCULES MICROELECTRONICS INC.

17.2.4

XI'AN ZHIDUOJING MICROELECTRONICS CO., LTD.

17.2.5

NANOXPLORE

17.2.6

COLOGNE CHIP AG

17.2.7

LEAFLABS, LLC

17.2.8

LOGIC FRUIT TECHNOLOGIES PRIVATE LIMITED

17.2.9

RAPID SILICON

17.2.10

ZERO ASIC

17.2.11

ADICSYS

17.2.12

RAPID FLEX

17.2.13

MENTA

17.2.14

SARACA SOLUTIONS PRIVATE LIMITED

17.2.15

BYTESNAP DESIGN

18

APPENDIX

381

18.1

DISCUSSION GUIDE

18.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

18.3

CUSTOMIZATION OPTIONS

18.4

RELATED REPORTS

18.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

FPGA MARKET: RISK ANALYSIS

TABLE 2

FPGA MARKET: IMPACT OF PORTER’S FIVE FORCES

TABLE 3

GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021–2029

TABLE 4

ROLE OF PLAYERS IN FPGA ECOSYSTEM

TABLE 5

AVERAGE SELLING PRICE OF LOW-END FPGAS OFFERED BY TOP 3 PLAYERS, BY VERTICAL (USD/UNIT), 2024

TABLE 6

AVERAGE SELLING PRICE OF MID-RANGE FPGAS OFFERED BY TOP 3 PLAYERS, BY VERTICAL (USD/UNIT), 2024

TABLE 7

AVERAGE SELLING PRICE OF HIGH-END FPGAS OFFERED BY TOP 2 PLAYERS, BY VERTICAL (USD/UNIT), 2024

TABLE 8

MAJOR PARAMETERS DIFFERENTIATING FPGAS BASED ON CONFIGURATION

TABLE 9

AVERAGE SELLING PRICE OF LOW-END FPGAS, BY REGION, 2021–2024 (USD/UNIT)

TABLE 10

AVERAGE SELLING PRICE OF MID-RANGE FPGAS, BY REGION, 2021–2024 (USD/UNIT)

TABLE 11

AVERAGE SELLING PRICE OF HIGH-END FPGAS, BY REGION, 2021–2024 (USD/UNIT)

TABLE 12

IMPORT DATA FOR HS CODE 854239-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 13

EXPORT DATA FOR HS CODE 854239-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 14

FPGA MARKET: KEY CONFERENCES AND EVENTS, 2025–2026

TABLE 15

US ADJUSTED RECIPROCAL TARIFF RATES

TABLE 16

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 VERTICALS (%)

TABLE 17

KEY BUYING CRITERIA FOR TOP THREE VERTICALS

TABLE 18

UNMET NEEDS IN FPGA MARKET BY VERTICAL

TABLE 19

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 20

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 21

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 22

REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 23

LIST OF APPLIED/GRANTED PATENTS RELATED TO FPGA MARKET, AUGUST 2023–JULY 2025

TABLE 24

TOP USE CASES AND MARKET POTENTIAL

TABLE 25

BEST PRACTICES: COMPANIES IMPLEMENTING USE CASES

TABLE 26

FPGA MARKET: CASE STUDIES RELATED TO AI IMPLEMENTATION

TABLE 27

INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

TABLE 28

COMPARISON OF MARKET SIZE OF FPGA AND EFPGA, 2021–2024 (USD MILLION)

TABLE 29

COMPARISON OF MARKET SIZE OF FPGA AND EFPGA, 2025–2030 (USD MILLION)

TABLE 30

MAJOR PARAMETERS CONSIDERED TO DIFFERENTIATE FPGA BASED ON CONFIGURATION

TABLE 31

FPGA MARKET, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 32

FPGA MARKET, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 33

FPGA MARKET, BY CONFIGURATION, 2021–2024 (THOUSAND UNITS)

TABLE 34

FPGA MARKET, BY CONFIGURATION, 2025–2030 (THOUSAND UNITS)

TABLE 35

FPGA MARKET, BY NODE SIZE, 2021–2024 (USD MILLION)

TABLE 36

FPGA MARKET, BY NODE SIZE, 2025–2030 (USD MILLION)

TABLE 37

FPGA MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 38

FPGA MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 39

FPGA MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 40

FPGA MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 41

FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 42

FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 43

FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 44

FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 45

FPGA MARKET FOR WIRED COMMUNICATION, BY TYPE, 2021–2024 (USD MILLION)

TABLE 46

FPGA MARKET FOR WIRED COMMUNICATION, BY TYPE, 2025–2030 (USD MILLION)

TABLE 47

FPGA MARKET FOR WIRELESS COMMUNICATION, BY TYPE, 2021–2024 (USD MILLION)

TABLE 48

FPGA MARKET FOR WIRELESS COMMUNICATION, BY TYPE, 2025–2030 (USD MILLION)

TABLE 49

FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 50

FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 51

FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 52

FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 53

FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 54

FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 55

FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 56

FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 57

FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 58

FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 59

FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 60

FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 61

FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 62

FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 63

FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2021–2024 (USD MILLION)

TABLE 64

FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2025–2030 (USD MILLION)

TABLE 65

FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 66

FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 67

FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 68

FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 69

FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 70

FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 71

FPGA MARKET FOR HEALTHCARE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 72

FPGA MARKET FOR HEALTHCARE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 73

FPGA MARKET FOR IMAGING DIAGNOSTIC SYSTEMS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 74

FPGA MARKET FOR IMAGING DIAGNOSTIC SYSTEMS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 75

FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 76

FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 77

FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2021–2024 (USD MILLION)

TABLE 78

FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2025–2030 (USD MILLION)

TABLE 79

FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 80

FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 81

FPGA MARKET FOR BROADCASTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 82

FPGA MARKET FOR BROADCASTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 83

FPGA MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 84

FPGA MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 85

NORTH AMERICA: FPGA MARKET, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 86

NORTH AMERICA: FPGA MARKET, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 87

NORTH AMERICA: FPGA MARKET, BY NODE SIZE, 2021–2024 (USD MILLION)

TABLE 88

NORTH AMERICA: FPGA MARKET, BY NODE SIZE, 2025–2030 (USD MILLION)

TABLE 89

NORTH AMERICA: FPGA MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 90

NORTH AMERICA: FPGA MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 91

NORTH AMERICA: FPGA MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 92

NORTH AMERICA: FPGA MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 93

NORTH AMERICA: FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 94

NORTH AMERICA: FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 95

NORTH AMERICA: FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 96

NORTH AMERICA: FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 97

NORTH AMERICA: FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 98

NORTH AMERICA: FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 99

NORTH AMERICA: FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2021–2024 (USD MILLION)

TABLE 100

NORTH AMERICA: FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2025–2030 (USD MILLION)

TABLE 101

NORTH AMERICA: FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 102

NORTH AMERICA: FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 103

NORTH AMERICA: FPGA MARKET FOR HEALTHCARE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 104

NORTH AMERICA: FPGA MARKET FOR HEALTHCARE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 105

NORTH AMERICA: FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2021–2024 (USD MILLION)

TABLE 106

NORTH AMERICA: FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2025–2030 (USD MILLION)

TABLE 107

NORTH AMERICA: FPGA MARKET FOR BROADCASTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 108

NORTH AMERICA: FPGA MARKET FOR BROADCASTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 109

NORTH AMERICA: FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 110

NORTH AMERICA: FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 111

NORTH AMERICA: FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 112

NORTH AMERICA: FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 113

NORTH AMERICA: FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 114

NORTH AMERICA: FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 115

NORTH AMERICA: FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 116

NORTH AMERICA: FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 117

NORTH AMERICA: FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 118

NORTH AMERICA: FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 119

NORTH AMERICA: FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 120

NORTH AMERICA: FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 121

NORTH AMERICA: FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 122

NORTH AMERICA: FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 123

NORTH AMERICA: FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 124

NORTH AMERICA: FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 125

NORTH AMERICA: FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 126

NORTH AMERICA: FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 127

NORTH AMERICA: FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 128

NORTH AMERICA: FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 129

NORTH AMERICA: FPGA MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 130

NORTH AMERICA: FPGA MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 131

EUROPE: FPGA MARKET, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 132

EUROPE: FPGA MARKET, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 133

EUROPE: FPGA MARKET, BY NODE SIZE, 2021–2024 (USD MILLION)

TABLE 134

EUROPE: FPGA MARKET, BY NODE SIZE, 2025–2030 (USD MILLION)

TABLE 135

EUROPE: FPGA MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 136

EUROPE: FPGA MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 137

EUROPE: FPGA MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 138

EUROPE: FPGA MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 139

EUROPE: FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 140

EUROPE: FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 141

EUROPE: FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 142

EUROPE: FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 143

EUROPE: FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 144

EUROPE: FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 145

EUROPE: FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2021–2024 (USD MILLION)

TABLE 146

EUROPE: FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2025–2030 (USD MILLION)

TABLE 147

EUROPE: FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 148

EUROPE: FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 149

EUROPE: FPGA MARKET FOR HEALTHCARE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 150

EUROPE: FPGA MARKET FOR HEALTHCARE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 151

EUROPE: FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2021–2024 (USD MILLION)

TABLE 152

EUROPE: FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2025–2030 (USD MILLION)

TABLE 153

EUROPE: FPGA MARKET FOR BROADCASTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 154

EUROPE: FPGA MARKET FOR BROADCASTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 155

EUROPE: FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 156

EUROPE: FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 157

EUROPE: FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 158

EUROPE: FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 159

EUROPE: FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 160

EUROPE: FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 161

EUROPE: FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 162

EUROPE: FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 163

EUROPE: FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 164

EUROPE: FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 165

EUROPE: FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 166

EUROPE: FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 167

EUROPE: FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 168

EUROPE: FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 169

EUROPE: FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 170

EUROPE: FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 171

EUROPE: FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 172

EUROPE: FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 173

EUROPE: FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 174

EUROPE: FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 175

EUROPE: FPGA MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 176

EUROPE: FPGA MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 177

ASIA PACIFIC: FPGA MARKET, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 178

ASIA PACIFIC: FPGA MARKET, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 179

ASIA PACIFIC: FPGA MARKET, BY NODE SIZE, 2021–2024 (USD MILLION)

TABLE 180

ASIA PACIFIC: FPGA MARKET, BY NODE SIZE, 2025–2030 (USD MILLION)

TABLE 181

ASIA PACIFIC: FPGA MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 182

ASIA PACIFIC: FPGA MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 183

ASIA PACIFIC: FPGA MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 184

ASIA PACIFIC: FPGA MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 185

ASIA PACIFIC: FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 186

ASIA PACIFIC: FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 187

ASIA PACIFIC: FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 188

ASIA PACIFIC: FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 189

ASIA PACIFIC: FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 190

ASIA PACIFIC: FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 191

ASIA PACIFIC: FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2021–2024 (USD MILLION)

TABLE 192

ASIA PACIFIC: FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2025–2030 (USD MILLION)

TABLE 193

ASIA PACIFIC: FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 194

ASIA PACIFIC: FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 195

ASIA PACIFIC: FPGA MARKET FOR HEALTHCARE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 196

ASIA PACIFIC: FPGA MARKET FOR HEALTHCARE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 197

ASIA PACIFIC: FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2021–2024 (USD MILLION)

TABLE 198

ASIA PACIFIC: FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2025–2030 (USD MILLION)

TABLE 199

ASIA PACIFIC: FPGA MARKET FOR BROADCASTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 200

ASIA PACIFIC: FPGA MARKET FOR BROADCASTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 201

ASIA PACIFIC: FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 202

ASIA PACIFIC: FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 203

ASIA PACIFIC: FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 204

ASIA PACIFIC: FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 205

ASIA PACIFIC: FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 206

ASIA PACIFIC: FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 207

ASIA PACIFIC: FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 208

ASIA PACIFIC: FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 209

ASIA PACIFIC: FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 210

ASIA PACIFIC: FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 211

ASIA PACIFIC: FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 212

ASIA PACIFIC: FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 213

ASIA PACIFIC: FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 214

ASIA PACIFIC: FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 215

ASIA PACIFIC: FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 216

ASIA PACIFIC: FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 217

ASIA PACIFIC: FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 218

ASIA PACIFIC: FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 219

ASIA PACIFIC: FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 220

ASIA PACIFIC: FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 221

ASIA PACIFIC: FPGA MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 222

ASIA PACIFIC: FPGA MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 223

ROW: FPGA MARKET, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 224

ROW: FPGA MARKET, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 225

ROW: FPGA MARKET, BY NODE SIZE, 2021–2024 (USD MILLION)

TABLE 226

ROW: FPGA MARKET, BY NODE SIZE, 2025–2030 (USD MILLION)

TABLE 227

ROW: FPGA MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 228

ROW: FPGA MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 229

ROW: FPGA MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 230

ROW: FPGA MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 231

ROW: FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 232

ROW: FPGA MARKET FOR TELECOMMUNICATIONS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 233

ROW: FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 234

ROW: FPGA MARKET FOR DATA CENTER & COMPUTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 235

ROW: FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 236

ROW: FPGA MARKET FOR MILITARY & AEROSPACE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 237

ROW: FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2021–2024 (USD MILLION)

TABLE 238

ROW: FPGA MARKET FOR INDUSTRIAL, BY TYPE, 2025–2030 (USD MILLION)

TABLE 239

ROW: FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 240

ROW: FPGA MARKET FOR AUTOMOTIVE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 241

ROW: FPGA MARKET FOR HEALTHCARE, BY TYPE, 2021–2024 (USD MILLION)

TABLE 242

ROW: FPGA MARKET FOR HEALTHCARE, BY TYPE, 2025–2030 (USD MILLION)

TABLE 243

ROW: FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2021–2024 (USD MILLION)

TABLE 244

ROW: FPGA MARKET FOR MULTIMEDIA, BY TYPE, 2025–2030 (USD MILLION)

TABLE 245

ROW: FPGA MARKET FOR BROADCASTING, BY TYPE, 2021–2024 (USD MILLION)

TABLE 246

ROW: FPGA MARKET FOR BROADCASTING, BY TYPE, 2025–2030 (USD MILLION)

TABLE 247

ROW: FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 248

ROW: FPGA MARKET FOR TELECOMMUNICATIONS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 249

ROW: FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 250

ROW: FPGA MARKET FOR CONSUMER ELECTRONICS, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 251

ROW: FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 252

ROW: FPGA MARKET FOR TESTING, MEASUREMENT, AND EMULATION, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 253

ROW: FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 254

ROW: FPGA MARKET FOR DATA CENTER & COMPUTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 255

ROW: FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 256

ROW: FPGA MARKET FOR MILITARY & AEROSPACE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 257

ROW: FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 258

ROW: FPGA MARKET FOR INDUSTRIAL, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 259

ROW: FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 260

ROW: FPGA MARKET FOR AUTOMOTIVE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 261

ROW: FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 262

ROW: FPGA MARKET FOR HEALTHCARE, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 263

ROW: FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 264

ROW: FPGA MARKET FOR MULTIMEDIA, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 265

ROW: FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2021–2024 (USD MILLION)

TABLE 266

ROW: FPGA MARKET FOR BROADCASTING, BY CONFIGURATION, 2025–2030 (USD MILLION)

TABLE 267

ROW: FPGA MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 268

ROW: FPGA MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 269

OVERVIEW OF STRATEGIES ADOPTED BY FPGA PROVIDERS

TABLE 270

DEGREE OF COMPETITION, 2024

TABLE 271

FPGA MARKET: REGIONAL FOOTPRINT, 2024

TABLE 272

FPGA MARKET: CONFIGURATION FOOTPRINT, 2024

TABLE 273

FPGA MARKET: NODE SIZE FOOTPRINT, 2024

TABLE 274

FPGA MARKET: TECHNOLOGY FOOTPRINT, 2024

TABLE 275

FPGA MARKET: VERTICAL FOOTPRINT, 2024

TABLE 276

FPGA MARKET: LIST OF KEY STARTUPS/SMES, 2024

TABLE 277

FPGA MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2024 (1/2)

TABLE 278

FPGA MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2024 (2/2)

TABLE 279

FPGA MARKET: PRODUCT LAUNCHES, JANUARY 2021−SEPTEMBER 2025

TABLE 280

FPGA MARKET: DEALS, JANUARY 2021−SEPTEMBER 2025

TABLE 281

ADVANCED MICRO DEVICES, INC.: COMPANY OVERVIEW

TABLE 282

ADVANCED MICRO DEVICES, INC.: PRODUCTS OFFERED

TABLE 283

ADVANCED MICRO DEVICES, INC.: PRODUCT LAUNCHES, JANUARY 2021–SEPTEMBER 2025

TABLE 284

ADVANCED MICRO DEVICES, INC.: DEALS, JANUARY 2021–SEPTEMBER 2025

TABLE 285

ALTERA CORPORATION: COMPANY OVERVIEW

TABLE 286

ALTERA CORPORATION: PRODUCTS OFFERED

TABLE 287

ALTERA CORPORATION: PRODUCT LAUNCHES, JANUARY 2021–SEPTEMBER 2025

TABLE 288

ALTERA CORPORATION: DEALS, JANUARY 2021–SEPTEMBER 2025

TABLE 289

ALTERA CORPORATION: EXPANSIONS, JANUARY 2021–SEPTEMBER 2025

TABLE 290

ALTERA CORPORATION: OTHER DEVELOPMENTS, JANUARY 2021–SEPTEMBER 2025

TABLE 291

MICROCHIP TECHNOLOGY INC.: COMPANY OVERVIEW

TABLE 292

MICROCHIP TECHNOLOGY INC.: PRODUCTS OFFERED

TABLE 293

MICROCHIP TECHNOLOGY INC.: PRODUCT LAUNCHES, JANUARY 2021–SEPTEMBER 2025

TABLE 294

MICROCHIP TECHNOLOGY INC.: DEALS, JANUARY 2021–SEPTEMBER 2025

TABLE 295

MICROCHIP TECHNOLOGY INC.: EXPANSIONS, JANUARY 2021–SEPTEMBER 2025

TABLE 296

MICROCHIP TECHNOLOGY INC.: OTHER DEVELOPMENTS, JANUARY 2021–SEPTEMBER 2025

TABLE 297

LATTICE SEMICONDUCTOR CORPORATION: COMPANY OVERVIEW

TABLE 298

LATTICE SEMICONDUCTOR CORPORATION: PRODUCTS OFFERED

TABLE 299

LATTICE SEMICONDUCTOR CORPORATION: PRODUCT LAUNCHES, JANUARY 2021–SEPTEMBER 2025

TABLE 300

LATTICE SEMICONDUCTOR CORPORATION: DEALS, JANUARY 2021–SEPTEMBER 2025

TABLE 301

LATTICE SEMICONDUCTOR CORPORATION: OTHER DEVELOPMENTS, JANUARY 2021–SEPTEMBER 2025

TABLE 302

ACHRONIX SEMICONDUCTOR CORPORATION: COMPANY OVERVIEW

TABLE 303

ACHRONIX SEMICONDUCTOR CORPORATION: PRODUCTS OFFERED

TABLE 304

ACHRONIX SEMICONDUCTOR CORPORATION: PRODUCT LAUNCHES, JANUARY 2021–SEPTEMBER 2025

TABLE 305

ACHRONIX SEMICONDUCTOR CORPORATION: DEALS, JANUARY 2021–SEPTEMBER 2025

TABLE 306

ACHRONIX SEMICONDUCTOR CORPORATION: OTHER DEVELOPMENTS, JANUARY 2021–SEPTEMBER 2025

TABLE 307

QUICKLOGIC CORPORATION: COMPANY OVERVIEW

TABLE 308

QUICKLOGIC CORPORATION: PRODUCTS OFFERED

TABLE 309

QUICKLOGIC CORPORATION: PRODUCT LAUNCHES, JANUARY 2021–SEPTEMBER 2025

TABLE 310

QUICKLOGIC CORPORATION: DEALS, JANUARY 2021–SEPTEMBER 2025

TABLE 311

QUICKLOGIC CORPORATION: OTHER DEVELOPMENTS, JANUARY 2021–SEPTEMBER 2025

TABLE 312

EFINIX, INC.: COMPANY OVERVIEW

TABLE 313

EFINIX, INC.: PRODUCTS OFFERED

TABLE 314

EFINIX, INC.: PRODUCT LAUNCHES, JANUARY 2021–SEPTEMBER 2025

TABLE 315

EFINIX, INC.: DEALS, JANUARY 2021–SEPTEMBER 2025

TABLE 316

SHENZHEN PANGO MICROSYSTEMS CO., LTD.: COMPANY OVERVIEW

TABLE 317

SHENZHEN PANGO MICROSYSTEMS CO., LTD.: PRODUCTS OFFERED

TABLE 318

GOWIN SEMICONDUCTOR CORP.: COMPANY OVERVIEW

TABLE 319

GOWIN SEMICONDUCTOR CORP.: PRODUCTS OFFERED

TABLE 320

GOWIN SEMICONDUCTOR CORP.: PRODUCT LAUNCHES, JANUARY 2021–SEPTEMBER 2025

TABLE 321

GOWIN SEMICONDUCTOR CORP.: DEALS, JANUARY 2021–SEPTEMBER 2025

TABLE 322

RENESAS ELECTRONICS CORPORATION: COMPANY OVERVIEW

TABLE 323

RENESAS ELECTRONICS CORPORATION: PRODUCTS OFFERED

TABLE 324

RENESAS ELECTRONICS CORPORATION: PRODUCT LAUNCHES, JANUARY 2021–SEPTEMBER 2025

TABLE 325

RENESAS ELECTRONICS CORPORATION: DEALS, JANUARY 2021–SEPTEMBER 2025

TABLE 326

AGM MICRO: COMPANY OVERVIEW

TABLE 327

SHANGHAI ANLOGIC INFOTECH CO., LTD.: COMPANY OVERVIEW

TABLE 328

HERCULES MICROELECTRONICS INC.: COMPANY OVERVIEW

TABLE 329

XI'AN ZHIDUOJING MICROELECTRONICS CO., LTD.: COMPANY OVERVIEW

TABLE 330

NANOXPLORE: COMPANY OVERVIEW

TABLE 331

COLOGNE CHIP AG: COMPANY OVERVIEW

TABLE 332

LEAFLABS, LLC: COMPANY OVERVIEW

TABLE 333

LOGIC FRUIT TECHNOLOGIES PRIVATE LIMITED: COMPANY OVERVIEW

TABLE 334

RAPID SILICON: COMPANY OVERVIEW

TABLE 335

ZERO ASIC: COMPANY OVERVIEW

TABLE 336

ADICSYS: COMPANY OVERVIEW

TABLE 337

RAPID FLEX: COMPANY OVERVIEW

TABLE 338

MENTA: COMPANY OVERVIEW

TABLE 339

SARACA SOLUTIONS PRIVATE LIMITED: COMPANY OVERVIEW

TABLE 340

BYTESNAP DESIGN: COMPANY OVERVIEW

LIST OF FIGURES

FIGURE 1

FIELD PROGRAMMABLE GATE ARRAY (FPGA) MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

FPGA MARKET: RESEARCH DESIGN

FIGURE 3

FPGA MARKET: RESEARCH FLOW OF MARKET SIZE ESTIMATION

FIGURE 4

FPGA MARKET: SUPPLY-SIDE ANALYSIS

FIGURE 5

FPGA MARKET: BOTTOM-UP APPROACH

FIGURE 6

FPGA MARKET: TOP-DOWN APPROACH

FIGURE 7

FPGA MARKET: DATA TRIANGULATION

FIGURE 8

KEY INSIGHTS AND MARKET HIGHLIGHTS

FIGURE 9

FPGA MARKET, BY CONFIGURATION, 2025–2030

FIGURE 10

MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN FPGA MARKET (JANUARY 2021–SEPTEMBER 2025)

FIGURE 11

DISRUPTIVE TRENDS IMPACTING GROWTH OF FPGA MARKET

FIGURE 12

HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS IN FPGA MARKET, 2024

FIGURE 13

ASIA PACIFIC TO BE LEADING MARKET DURING FORECAST PERIOD

FIGURE 14

RISE IN AI WORKLOADS AND TELECOM INFRASTRUCTURE MODERNIZATION TO DRIVE MARKET

FIGURE 15

LOW-END FPGA AND 20-90 NM SEGMENT TO LEAD MARKET IN 2025

FIGURE 16

FLASH TECHNOLOGY TO REGISTER FASTEST GROWTH DURING FORECAST PERIOD

FIGURE 17

TELECOMMUNICATIONS VERTICAL TO HOLD LARGEST MARKET SHARE BY 2030

FIGURE 18

CHINA TO WITNESS HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 19

DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN FPGA MARKET

FIGURE 20

ESTIMATED PERCENT OF REGISTERED VEHICLES EQUIPPED WITH ADAS, 2023 AND 2028

FIGURE 21

IMPACT ANALYSIS: DRIVERS

FIGURE 22

IMPACT ANALYSIS: RESTRAINTS

FIGURE 23

IMPACT ANALYSIS: OPPORTUNITIES

FIGURE 24

IMPACT ANALYSIS: CHALLENGES

FIGURE 25

FPGA MARKET: PORTER'S FIVE FORCES ANALYSIS

FIGURE 26

FPGA MARKET: VALUE CHAIN ANALYSIS

FIGURE 27

FPGA MARKET: ECOSYSTEM ANALYSIS

FIGURE 28

AVERAGE SELLING PRICE TREND OF LOW-END FPGAS OFFERED BY TOP 3 KEY PLAYERS, BY VERTICAL, 2024 (USD/UNIT)

FIGURE 29

AVERAGE SELLING PRICE TREND OF MID-RANGE FPGAS OFFERED BY TOP 3 KEY PLAYERS, BY VERTICAL, 2024 (USD/UNIT)

FIGURE 30

AVERAGE SELLING PRICE TREND OF HIGH-END FPGAS OFFERED BY TOP 2 PLAYERS, BY VERTICAL, 2024 (USD/UNIT)

FIGURE 31

AVERAGE SELLING PRICE TREND FOR LOW-END FPGAS, BY REGION, 2021–2024 (USD/UNIT)

FIGURE 32

AVERAGE SELLING PRICE TREND FOR MID-RANGE FPGAS, BY REGION, 2021–2024 (USD/UNIT)

FIGURE 33

AVERAGE SELLING PRICE TREND FOR HIGH-END FPGAS, BY REGION, 2021–2024 (USD/UNIT)

FIGURE 34

IMPORT SCENARIO FOR HS CODE 854239-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2020–2024

FIGURE 35

EXPORT SCENARIO FOR HS CODE 854239-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2020–2024

FIGURE 36

TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS’ BUSINESSES

FIGURE 37

INVESTMENT AND FUNDING SCENARIO, 2021–2025

FIGURE 38

DECISION-MAKING FACTORS IN FPGA MARKET

FIGURE 39

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 VERTICALS

FIGURE 40

KEY BUYING CRITERIA FOR TOP 3 VERTICALS

FIGURE 41

ADOPTION BARRIERS AND INTERNAL CHALLENGES

FIGURE 42

FPGA MARKET: PATENT ANALYSIS, 2014–2024

FIGURE 43

EFPGA SEGMENT TO GROW AT HIGHER CAGR THAN FPGA SEGMENT FROM 2025 TO 2030

FIGURE 44

LOW-END SEGMENT TO LEAD FPGA MARKET DURING FORECAST PERIOD

FIGURE 45

≤16 NM NODE SIZE TO REGISTER HIGHEST CAGR FROM 2025 TO 2030

FIGURE 46

SRAM TECHNOLOGY TO DOMINATE FPGA MARKET IN 2030

FIGURE 47

DATA CENTER & COMPUTING VERTICAL TO REGISTER HIGHEST CAGR FROM 2025 TO 2030

FIGURE 48

5G SEGMENT OF FPGA MARKET FOR TELECOMMUNICATIONS TO REGISTER HIGHEST CAGR FROM 2025 TO 2030

FIGURE 49

NETWORK INTERFACE CONTROL SEGMENT TO HOLD LARGEST MARKET SHARE FOR DATA CENTER & COMPUTING BY 2030

FIGURE 50

FPGA MARKET FOR AVIONICS SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 51

ROBOTICS SEGMENT TO LEAD INDUSTRIAL VERTICAL BY 2030

FIGURE 52

ADAS/SENSOR FUSION SEGMENT OF FPGA MARKET FOR AUTOMOTIVE TO HOLD HIGH MARKET SHARE IN 2030

FIGURE 53

WEARABLE DEVICES SEGMENT FOR HEALTHCARE TO RECORD HIGHEST CAGR FROM 2025 TO 2030

FIGURE 54

VIDEO PROCESSING SEGMENT TO GROW AT HIGHER CAGR THAN AUDIO DEVICES SEGMENT DURING FORECAST PERIOD

FIGURE 55

BROADCASTING PLATFORM DESIGNS TO HOLD DOMINANT MARKET SHARE FOR BROADCASTING SEGMENT IN 2030

FIGURE 56

ASIA PACIFIC TO LEAD FPGA MARKET 2025 TO 2030

FIGURE 57

NORTH AMERICA: FPGA MARKET SNAPSHOT

FIGURE 58

US TO GROW AT HIGHEST CAGR FOR FPGA MARKET FROM 2025 TO 2030

FIGURE 59

EUROPE: FPGA MARKET SNAPSHOT

FIGURE 60

GERMANY TO REGISTER HIGHEST CAGR IN EUROPEAN FPGA MARKET FROM 2025 TO 2030

FIGURE 61

ASIA PACIFIC: FPGA MARKET SNAPSHOT

FIGURE 62

CHINA TO LEAD FPGA MARKET IN ASIA PACIFIC BY 2030

FIGURE 63

ROW: FPGA MARKET SNAPSHOT

FIGURE 64

SOUTH AMERICA TO REGISTER HIGHEST CAGR FOR FPGA MARKET FROM 2025 TO 2030

FIGURE 65

REVENUE ANALYSIS OF KEY PLAYERS IN FPGA MARKET, 2021–2024 (USD MILLION)

FIGURE 66

FPGA MARKET SHARE OF KEY PLAYERS, 2024

FIGURE 67

COMPANY VALUATION, 2025 (USD BILLION)

FIGURE 68

FINANCIAL METRICS (EV/EBITDA), 2025

FIGURE 69

BRAND/PRODUCT COMPARISON

FIGURE 70

FPGA MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 71

FPGA MARKET: COMPANY FOOTPRINT, 2024

FIGURE 72

FPGA MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 73

ADVANCED MICRO DEVICES, INC.: COMPANY SNAPSHOT

FIGURE 74

MICROCHIP TECHNOLOGY INC.: COMPANY SNAPSHOT

FIGURE 75

LATTICE SEMICONDUCTOR CORPORATION: COMPANY SNAPSHOT

FIGURE 76

QUICKLOGIC CORPORATION: COMPANY SNAPSHOT

FIGURE 77

RENESAS ELECTRONICS CORPORATION: COMPANY SNAPSHOT

Methodology

The study involved four major activities in estimating the current size of the field programmable gate array (FPGA) market. Exhaustive secondary research collected information on the market, peer, and parent markets. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation techniques were used to estimate the market size of segments and subsegments.

Secondary Research