Download PDF

Download PDF Request Customisation

Request Customisation

Head-up Display (HUD) Market Size, Share & Growth

Report Code

SE 2330

Published in

Sep, 2025, By MarketsandMarkets™

Head-up Display (HUD) Market Size, Share, Growth & Trends by Combiner HUD, Windshield HUD, Wearable HUD, Augmented Reality (AR) HUD, Conventional HUD, Display Unit, Video Generator/Processing Unit, and Projector/ Projection Unit - Global Forecast to 2030

USD 7.34 BN

MARKET SIZE, 2030

CAGR 11.8%

(2025-2030)

250

REPORT PAGES

175

MARKET TABLES

HEAD-UP DISPLAY MARKET SIZE, SHARE & TRENDS

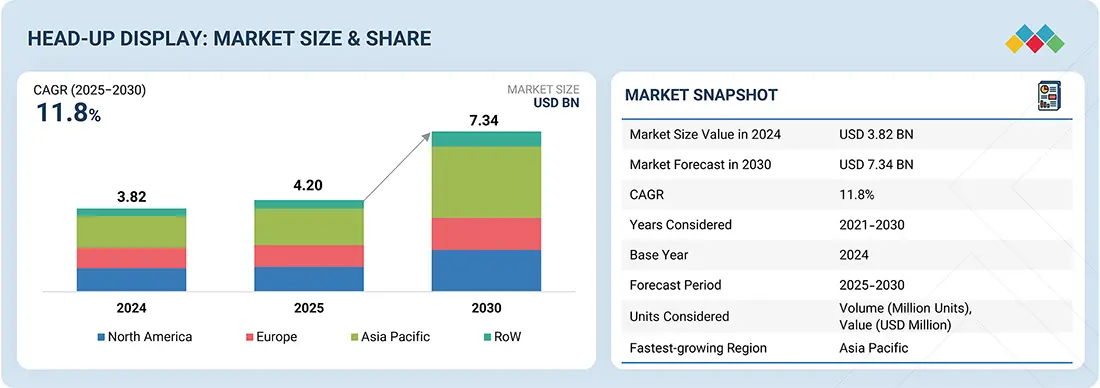

According to Marketsandmarkets, the global head-up display market size was valued at USD 4.20 billion in 2025 and is projected to reach USD 7.34 billion by 2030, growing at a CAGR of 11.8% from 2025 to 2030. The market is being driven by the rising demand for advanced driver-assistance systems (ADAS) and enhanced in-vehicle safety features. Increasing consumer preference for connected and immersive driving experiences has further accelerated adoption, especially with the integration of augmented reality (AR) HUDs. Automakers are also focusing on minimizing driver distraction by projecting critical information such as navigation, speed, and alerts directly onto the windshield.

MARKET SNAPSHOT TABLE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2025 (Value) | USD 4.20 Billion |

| Market Forecast in 2030 (Value) | USD 7.34 Billion |

| Growth Rate | CAGR of 11.8% from 2025-2030 |

| Years Considered | 2021–2030 |

| Base Year | 2024 |

| Forecast Period | 2025–2030 |

| Units Considered | Value (USD Million), Volume (Million Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regional Scope | North America, Europe, Asia Pacific, and RoW |

| Top Companies |

|

| Growth Drivers |

|

Market Size & Forecast

• 2025 Market Size: USD 4.20 Billion

• 2030 Projected Market Size: USD 7.34 Billion

• CAGR (2025-2030): 11.8%

• Video generators/processing: Fastest Growing Market

• Asia Pacific: Fastest CAGR

HEAD-UP DISPLAY MARKET GROWTH KEY TAKEAWAYS

-

BY COMPONENTThe component segment is evolving rapidly, with video processors and projection units driving innovation as they enable high-performance AR overlays and real-time rendering. Display units are benefiting from advances in OLED and microLED technologies, while supporting components like optics, sensors, and software are creating new value pools through enhanced safety and personalized experiences.

-

BY FORM FACTORWindshield HUDs dominate the market due to their wide field of view and seamless integration into driver sightlines, while combiners continue to serve cost-sensitive and retrofit applications. Wearable and helmet-mounted HUDs are emerging as high-growth niches, particularly in defense, industrial, and two-wheeler segments, where mobility and adaptability are critical.

-

BY TYPEConventional HUDs remain the most widely adopted due to proven reliability and affordability, especially across mid-range vehicles. However, AR HUDs represent the fastest-growing type, as demand rises for contextual navigation, lane-level guidance, and immersive ADAS displays, supported by advancements in optics and computational imaging.

-

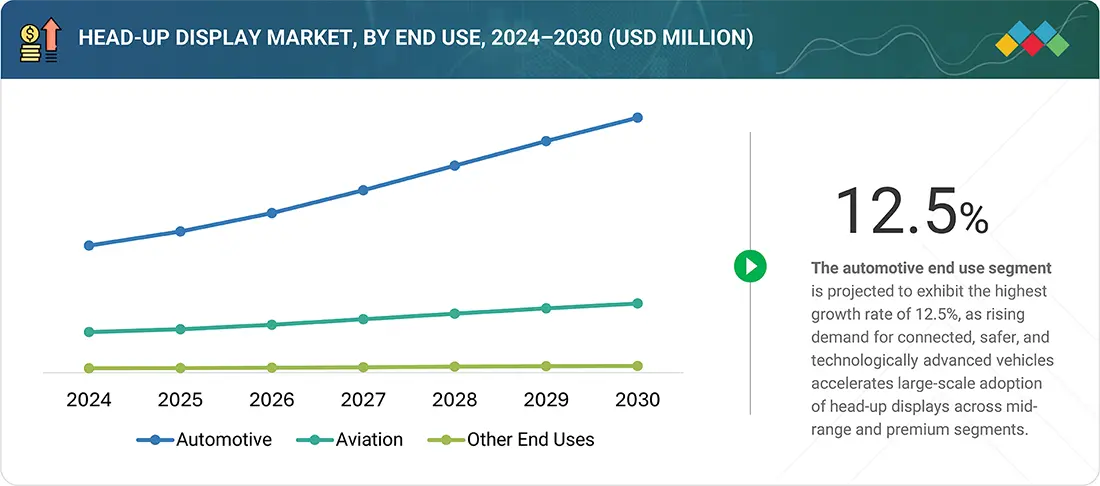

BY END USEAutomotive dominates the HUD market, as rising demand for advanced driver assistance, navigation overlays, and enhanced safety features makes HUDs a mainstream offering in mid-range and premium vehicles. Industrial applications are gaining traction, particularly in sectors requiring hands-free data visualization for operational efficiency.

-

BY REGIONAsia Pacific is expected to exhibit the fastest CAGR of 14.3%, driven by strong adoption in the automotive sector, rapid technological advancements, and increasing integration of HUDs by regional automobile manufacturers.

-

COMPETITIVE LANDSCAPEThe major market players have adopted both organic and inorganic strategies, including partnerships and agreements. For instance, Nippon Seiki Co., Ltd. entered a joint venture agreement in India with Emerging Display Technologies Corporation (Taiwan), a manufacturer of high-definition TFT LCD modules.

The head-up display industry is gaining momentum due to increasing demand for enhanced driver safety and convenience, as HUDs reduce driver distraction by projecting critical information within the line of sight. Growing adoption of advanced driver assistance systems (ADAS), coupled with the rising integration of augmented reality (AR) technologies, is further driving market expansion. Automakers are incorporating HUDs as a key differentiator in premium and mid-segment vehicles, reflecting a trend toward mass adoption. In addition, continuous improvements in projection technologies, miniaturization of components, and integration with connected and autonomous vehicle systems are shaping the evolution of HUDs.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

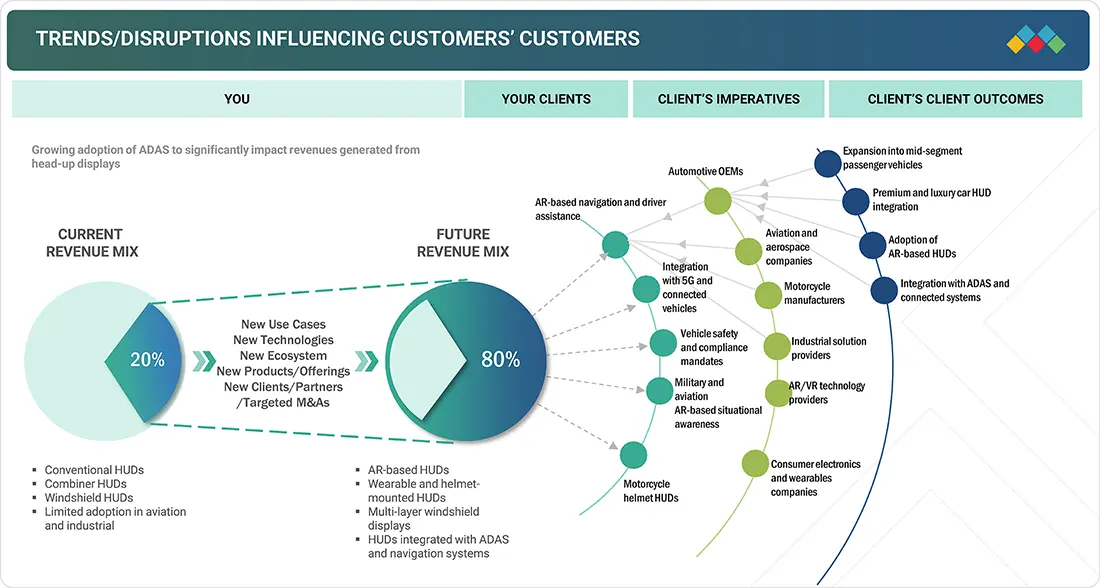

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The disruptions and emerging trends impacting customers’ businesses in the head-up display market size include moving from a luxury-focused HUD adoption base toward wider integration in mid-segment vehicles, with AR-based HUDs and ADAS connectivity emerging as key growth enablers.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

HEAD-UP DISPLAY MARKET GROWTH DYNAMICS

Drivers

Impact

Level

Level

-

Rising integration of HUDs with ADAS and real-time data

-

Growing emphasis on vehicle and passenger safety

RESTRAINTS

Impact

Level

Level

-

Issues related to retrofitting and standardization

-

Display visibility issues in bright sunlight or adverse conditions

OPPORTUNITIES

Impact

Level

Level

-

Increasing interest in HUDs for electric and software-defined vehicles

-

Rising application in two-wheeler and commercial vehicles

CHALLENGES

Impact

Level

Level

-

Regulatory challenges

-

High-expenses linked to advanced HUDs

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Rising integration of HUDs with ADAS and real-time data

The integration of HUDs with advanced driver assistance systems (ADAS) and real-time data is reshaping the driving experience by enhancing safety, awareness, and operational efficiency. By projecting critical information, such as ADAS alerts, navigation details, and traffic insights, directly onto the windshield, HUDs allow drivers to stay focused on the road rather than glancing at dashboards or infotainment screens. This seamless display reduces cognitive load, enabling safer and more intuitive vehicle operation.

Restraint: Complex installation and maintenance

The head-up display market is significantly restrained by the complex installation and maintenance requirements of HUD systems. Installing a HUD system, whether during vehicle manufacturing or as an aftermarket addition, demands specialized expertise to align it with the driver’s line of sight and calibrate it correctly. This specialized skill set may not be readily available in all repair shops or regions, limiting the widespread adoption of HUD technology and potentially raising installation costs.

Opportunity: Increasing interest in HUDs for electric and software-defined vehicles

As the automotive landscape shifts toward electric vehicles (EVs) and software-defined vehicles (SDVs), HUDs emerge as a natural interface for communicating real-time, software-driven insights to the driver. EVs, by nature, depend heavily on digital interfaces to convey battery levels, charging status, regenerative braking intensity, and range estimations. HUDs allow such data to be displayed in the driver’s field of view, reducing cognitive load and enhancing situational awareness. The silent operation of EVs also increases the need for visual cues, especially for pedestrians and low-speed manoeuvring, which HUDs can facilitate through AR overlays and dynamic alerts.

Challenge: Limited field of view (FOV)

One of the major limitations of the head-up display market is the restricted field of view (FOV) that HUDs can offer. HUDs generally project information onto a small part of the windshield or a dedicated display screen, which can limit the amount of data displayed. The FOV constraint means that critical data may not be displayed simultaneously, which could cause drivers to switch their attention between the HUD and the road.

Head-up Display (HUD) Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Automotive HUDs integrated into premium and mid-segment passenger vehicles, focusing on compact windshield and combiner HUDs | Enhanced driver visibility |Reduced distraction| Safer navigation| Growing a+C5+C2 |

|

AR-based HUD systems designed for connected and autonomous vehicles, providing large-field projections and ADAS integration | Improved situational awareness| Seamless ADAS alerts| Enhanced road safety| Immersive driver experience |

|

HUD solutions integrated with vehicle infotainment and safety systems, emphasizing energy-efficient and compact designs | Lower power consumption| Optimized in-cabin space usage| Improved safety alerts| Better driver convenience |

|

Advanced windshield HUDs and AR HUDs targeted for electric and autonomous vehicle platforms | Clearer projection in varied lighting| Improved driver–vehicle interaction|Stronger EV compatibility |

|

Multi-layered AR HUDs combining navigation, driver assistance data, and infotainment for high-end vehicles | Immersive AR visualization|Reduced cognitive load| Enhanced driving comfort |Premium user experience |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

HEAD-UP DISPLAY MARKET SHARE ECOSYSTEM

The head-up display ecosystem involves component suppliers, HUD manufacturers, software developers, distributors, and end users. Each collaborates to advance the market by sharing knowledge, resources, and expertise to attain end innovation in this field. Head-up display companies, such as Nippon Seiki Co., Ltd. (Japan), Continental AG (Germany), DENSO CORPORATION (Japan), E-LEAD ELECTRONIC CO. LTD (Taiwan), BAE Systems (UK), Yazaki Corporation (Japan), HARMAN International (US), Valeo (France), Panasonic Holdings Corporation (Japan), and Garmin Ltd. (US), are at the core of the market and are responsible for developing head-up display solutions for various end users.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

HEAD-UP DISPLAY MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Head-up Display Market, by Type

Conventional HUDs continue to dominate due to their cost-effectiveness, simpler integration, and proven reliability in mass-market vehicles. Their widespread use in mid-segment passenger cars makes them more scalable compared to advanced AR-based HUDs, which are still limited to premium models. Additionally, their lower production and maintenance costs appeal to OEMs targeting volume sales.

Head-up Display Market, by Component

Video generators/processing units are projected to grow fastest as they are the core enablers of AR-based HUDs, supporting real-time rendering of navigation, ADAS alerts, and immersive displays. Increasing demand for advanced visualization and seamless driver information systems is driving their rapid adoption. With the rise of complex driving data and 3D projections, these units are becoming indispensable to next-gen HUDs.

Head-up Display Market, by Form Factor

Windshield HUDs are expected to lead the market as they offer a wider field of view, seamless integration with the driver’s line of sight, and improved safety by minimizing distractions. Their growing adoption in premium and mid-segment vehicles, supported by advancements in projection technology, makes them the preferred choice over combiner HUDs.

Head-up Display Market, by End Use

Automotive end use is expected to grow at the fastest rate due to rising integration of HUDs in both premium and mid-segment passenger vehicles. Safety regulations, growing ADAS adoption, and consumer demand for enhanced driving experiences are fueling rapid expansion in this sector. Continuous OEM investments in connected and semi-autonomous vehicles further amplify HUD adoption in the automotive industry.

HEAD-UP DISPLAY MARKET TRENDS BY REGION

Asia Pacific to exhibit the fastest CAGR in the global head-up display market during the forecast period

Asia Pacific is expected to exhibit the highest CAGR in the head-up display market owing to rapid growth in automobile production, rising consumer preference for advanced safety and comfort features, and strong adoption of connected technologies in countries such as China, Japan, and South Korea. Expanding premium and mid-segment passenger vehicle sales, coupled with government support for road safety and technology-driven automotive innovations, further accelerate HUD penetration in the region. Additionally, increasing investments from global and regional OEMs in AR-based HUDs strengthens the region’s growth outlook.

The Asia-Pacific head-up display market is projected to reach USD 3.26 billion by 2030, growing from USD 1.67 billion in 2025, at a CAGR of around 14.3%. The market is driven by rising vehicle production, rapid adoption of advanced driver-assistance systems, and increasing penetration of premium and electric vehicles across key automotive markets such as China, Japan, South Korea, and India. Demand for enhanced vehicle safety, improved driver awareness, and digitally advanced in-vehicle user experiences is also growing. Automakers across the region are increasingly integrating windshield-based and augmented reality head-up displays to support real-time navigation, hazard alerts, and vehicle status visualization.

The European head-up display market is projected to reach USD 1.48 billion by 2030, growing from USD 0.99 billion in 2025, at a CAGR of around 8.4% from 2025 to 2030. The market is driven by the increasing integration of advanced driver-assistance systems, stringent vehicle safety regulations, and high penetration of premium and technologically advanced vehicles across the region. European automakers are actively adopting windshield-based and augmented reality head-up displays to enhance driver safety, reduce distractions, and support real-time navigation, hazard warnings, and vehicle status visualization.

The North America head-up display market is projected to reach USD 1.90 billion by 2030 from USD 1.15 billion in 2025, at a CAGR of 10.7%. Growth is driven by rising integration of advanced driver-assistance systems, increasing demand for enhanced driver safety and situational awareness, and the strong presence of OEMs offering premium and mid-range vehicles in the region. Automakers are increasingly adopting windshield-based and AR head-up displays to reduce driver distraction and support real-time navigation, hazard alerts, and vehicle status visualization.

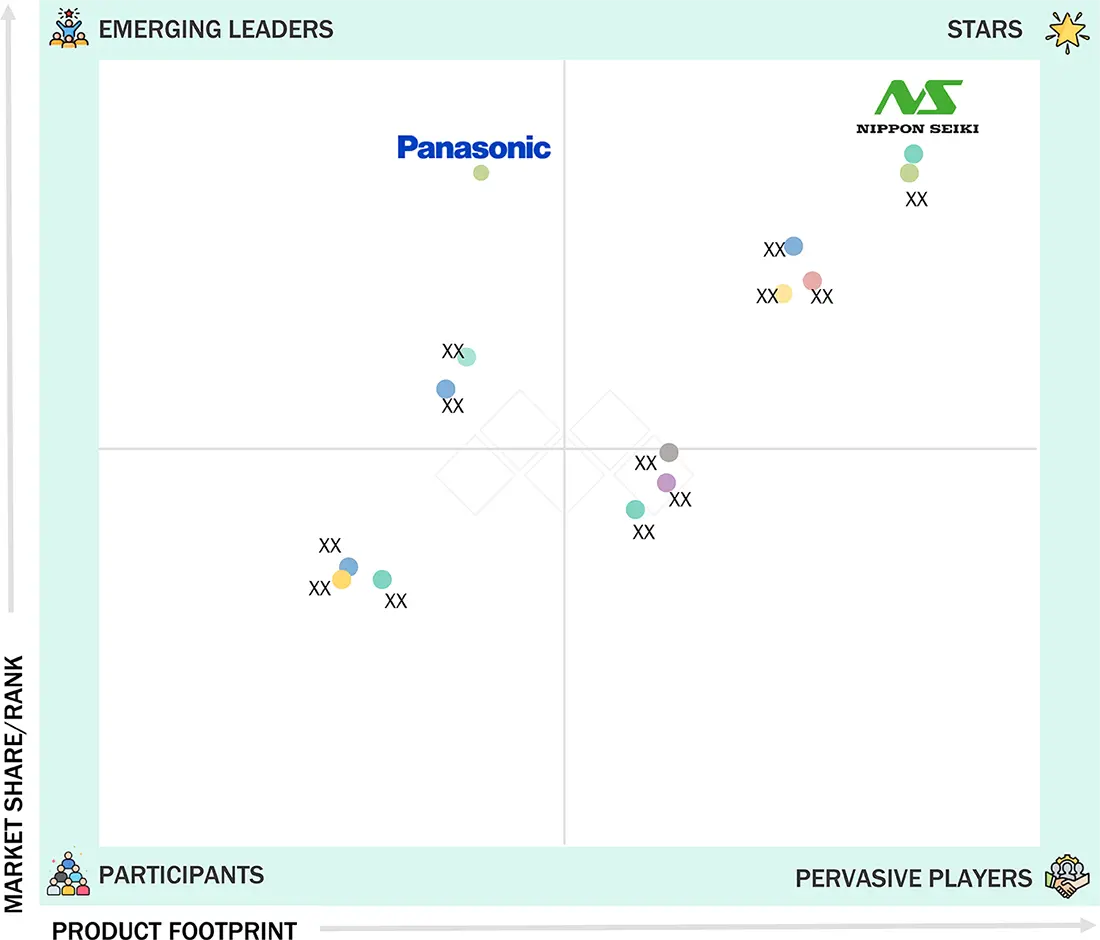

Head-up Display (HUD) Market: COMPANY EVALUATION MATRIX

In the head-up display market share matrix, Nippon Seiki is positioned as a star due to its strong product footprint and dominant market share, reflecting its leadership in both innovation and adoption across OEMs. Panasonic Holdings Corporation, on the other hand, is seen as an emerging leader, holding a significant market share but with a comparatively smaller product footprint, indicating strong growth potential as it expands its HUD offerings.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

HEAD-UP DISPLAY MARKET KEY PLAYERS

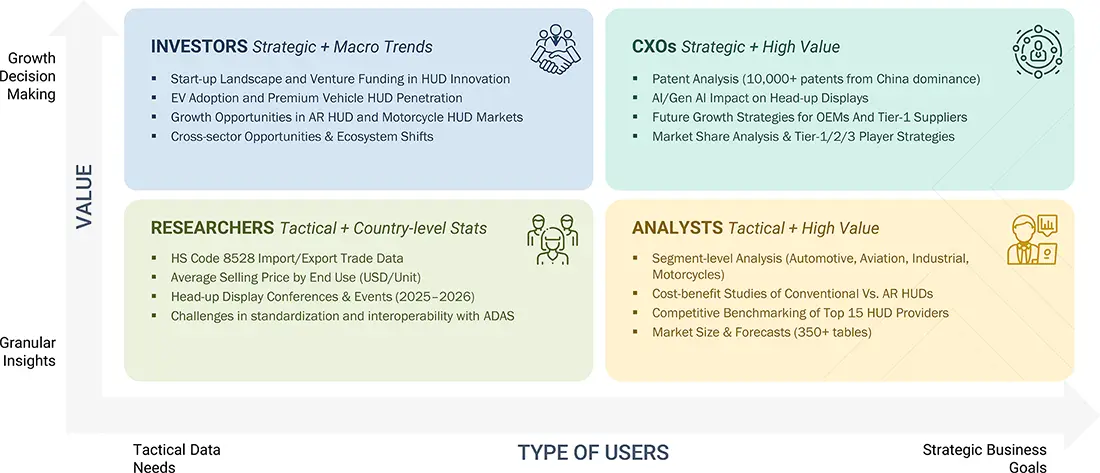

WHAT IS IN IT FOR YOU: Head-up Display (HUD) Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| European Automotive OEM | • Competitive benchmarking of conventional vs. AR HUD integration in premium and mid-segment vehicles | • Helped refine product positioning for next-gen HUD rollouts • Identified adoption roadmap across vehicle classes |

| North American Defense Contractor | • Technology road mapping for advanced AR HUD adoption in military aviation and tactical vehicles | • Reduced program risks with clear adoption timelines • Supported procurement strategies for mission-critical systems |

| Global Tier-1 Supplier | • Cost-performance trade-off analysis for video generators and projection units | • Optimized sourcing strategy • Identified opportunities for localization and reduced supply chain risks |

| European Aviation Manufacturer | • Regulatory and certification benchmarking for HUD use in cockpits | • Accelerated certification process • Highlighted compliance risks and streamlined approval strategy |

| Asian Motorcycle Manufacturer | • Market feasibility study on wearable HUDs for motorcycle helmets | • Informed new product development strategy • Supported diversification into mobility and safety wearables |

RECENT DEVELOPMENTS

- July 2025 : Valeo was chosen by a leading Chinese OEM to equip upcoming vehicle models with its advanced pillar-to-pillar head-up display. This panoramic system transforms the windshield into an interactive interface by projecting essential information directly into the driver’s field of vision. Utilizing high-efficiency displays embedded within the dashboard, the system reflects data onto a specially treated lower windshield section. In line with China’s rapid innovation cycle, Valeo supports its customers with production slated to begin in 2026.

- June 2025 : Xpeng, in collaboration with Huawei, developed an augmented reality head-up display (AR-HUD) system called “Chasing Light Panorama” for its upcoming mid-size electric SUV, the G7. The system combines Huawei’s hardware expertise with Xpeng’s software capabilities to deliver advanced navigation and enhanced driving assistance features.

- April 2025 : Nippon Seiki Co., Ltd. entered a joint venture agreement in India with Emerging Display Technologies Corporation (Taiwan), a manufacturer of high-definition TFT LCD modules. Under this partnership, the two companies will establish a new jointly funded entity, EDT-India Private Limited, focused on manufacturing TFT LCD modules in India. The newly planned facility aims to massively produce automotive TFT LCD modules by 2027.

- January 2023 : HARMAN introduced Ready Vision, an integrated suite of AR head-up display (HUD) hardware and software solutions to enhance driver safety and situational awareness. The Ready Vision AR software synchronizes with vehicle sensors to provide immersive audio and visual alerts, delivering critical information to drivers in a timely, precise, and non-intrusive manner.

- January 2022 : Panasonic Holdings Corporation unveiled the AR-HUD 2.0, the first product to include a new patented eye-tracking system, ETS, enhancing the AR experience. This HUD also includes AI-powered navigation software with 3D AR overlays, icons, and mappings.

FAQ

1: What is the current size of the Head-Up Display (HUD) market and how fast is it growing?

The Head-Up Display (HUD) market is witnessing strong growth, driven by rising adoption across automotive, aerospace & defense, and commercial aviation sectors. The market is expected to grow steadily through the forecast period, supported by increasing demand for advanced visualization systems, safety features, and digital cockpit technologies.

2: What are the key trends shaping the HUD market?

Major trends in the HUD market include the adoption of augmented reality (AR)-based HUDs, wider field-of-view displays, high-resolution digital optics, and seamless integration with AI, sensors, and connected vehicle or aircraft systems. Lightweight and energy-efficient HUD devices are also gaining traction.

3: Which devices and applications drive demand in the HUD industry?

HUD devices are widely used in automotive dashboards, aircraft cockpits, military platforms, and helicopters. Key applications include navigation guidance, safety alerts, flight and vehicle status monitoring, weapon targeting (defense), and enhanced situational awareness.

4: How is the HUD market segmented by industry and share?

The HUD market is segmented by industry into automotive, aerospace & defense, and commercial aviation, with automotive and aerospace segments holding significant market share. Aerospace & defense HUDs dominate in terms of technology value, while automotive HUDs lead in volume deployment.

5: What is the forecast and future growth outlook for the HUD market?

The HUD market is forecast to grow at a healthy CAGR over the coming years, supported by advancements in AR, smart mobility, aviation modernization, and rising safety regulations. Increasing investments in autonomous vehicles, smart cockpits, and next-generation aircraft will further drive market expansion.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

24

2

RESEARCH METHODOLOGY

29

3

EXECUTIVE SUMMARY

41

4

PREMIUM INSIGHTS

46

5

MARKET OVERVIEW

Rising demand for connected, AR-enhanced HUDs reshapes vehicle safety and user experience in evolving markets.

49

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

Growing emphasis on vehicle and passenger safety

5.2.1.2

Rising integration of HUDs with ADAS and real-time data

5.2.1.3

Proliferating adoption of AR-based HUDs in premium and mid-segment vehicles

5.2.1.4

Rapid advances in microdisplay and projection technologies

5.2.1.5

Growing focus on enhanced in-vehicle user experience

5.2.1.6

Mounting global demand for connected vehicles

5.2.2

RESTRAINTS

5.2.2.1

Spatial limitations in vehicle cockpits

5.2.2.2

Display visibility issues in bright sunlight or adverse conditions

5.2.2.3

Issues related to retrofitting and standardization

5.2.2.4

Complex installation and maintenance

5.2.3

OPPORTUNITIES

5.2.3.1

Increasing interest in HUDs for electric and software-defined vehicles

5.2.3.2

Rising application in two-wheeler and commercial vehicles

5.2.4

CHALLENGES

5.2.4.1

Regulatory challenges

5.2.4.2

Limited field of view (FOV)

5.2.4.3

High expenses linked to advanced HUDs

5.3

VALUE CHAIN ANALYSIS

5.4

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.5

ECOSYSTEM ANALYSIS

5.6

INVESTMENT AND FUNDING SCENARIO

5.7

TECHNOLOGY ANALYSIS

5.7.1

KEY TECHNOLOGIES

5.7.1.1

Waveguide optics

5.7.1.2

Micro-LED and OLED displays

5.7.1.3

Digital light processing (DLP)

5.7.2

ADJACENT TECHNOLOGIES

5.7.2.1

Advanced driver assistance systems (ADAS)

5.7.2.2

Augmented reality mapping engines

5.7.3

COMPLEMENTARY TECHNOLOGIES

5.7.3.1

Holographic optical elements (HOEs)

5.8

PRICING ANALYSIS

5.8.1

AVERAGE SELLING PRICE OF AUTOMOTIVE HUDS, BY KEY PLAYER, 2024

5.8.2

AVERAGE SELLING PRICE OF AUTOMOTIVE HUDS, BY REGION, 2024

5.9

CASE STUDY ANALYSIS

5.9.1

BOYD CORPORATION HELPED NAVDY DEVELOP THERMAL SOLUTION FOR HEAD-UP DISPLAYS

5.9.2

GX GROUP ASSISTED VISTEON IN DESIGNING COMPACT HEAD-UP DISPLAY UNIT

5.9.3

MITSUBISHI ELECTRIC RESEARCH LABORATORIES EVALUATED PERFORMANCE AND USER PREFERENCE OF HEAD-UP DISPLAYS

5.10

TRADE ANALYSIS

5.10.1

IMPORT SCENARIO (HS CODE 8528)

5.10.2

EXPORT SCENARIO (HS CODE 8528)

5.11

PATENT ANALYSIS

5.12

PORTER’S FIVE FORCES ANALYSIS

5.12.1

BARGAINING POWER OF SUPPLIERS

5.12.2

BARGAINING POWER OF BUYERS

5.12.3

THREAT OF NEW ENTRANTS

5.12.4

THREAT OF SUBSTITUTES

5.12.5

INTENSITY OF COMPETITIVE RIVALRY

5.13

KEY STAKEHOLDERS AND BUYING CRITERIA

5.13.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.13.2

BUYING CRITERIA

5.14

REGULATORY LANDSCAPE

5.14.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.14.2

STANDARDS AND REGULATIONS

5.15

KEY CONFERENCES AND EVENTS, 2025–2026

5.16

IMPACT OF AI/GEN AI ON HEAD-UP DISPLAY MARKET

5.16.1

INTRODUCTION

5.16.2

USE CASES AND IMPACT OF AI/GEN AI ON HEAD-UP DISPLAY MARKET

5.17

IMPACT OF 2025 US TARIFF ON HEAD-UP DISPLAY MARKET

5.17.1

INTRODUCTION

5.17.2

KEY TARIFF RATES

5.17.3

PRICE IMPACT ANALYSIS

5.17.4

IMPACT ON COUNTRIES/REGIONS

5.17.4.1

US

5.17.4.2

Europe

5.17.4.3

Asia Pacific

5.17.5

IMPACT ON END USES

6

HEAD-UP DISPLAY TECHNOLOGIES

Explore cutting-edge HUD advancements, from digital displays to innovative laser and waveguide systems.

87

6.1

INTRODUCTION

6.2

DIGITAL HUD (LCD/LED/OLED)

6.3

DLP-BASED HUD

6.4

WAVEGUIDE-BASED HUD

6.5

LASER-BASED HUD

7

HEAD-UP DISPLAY FEATURES

Maximize driving efficiency with enhanced HUD clarity and precise visual accuracy.

90

7.1

INTRODUCTION

7.2

FIELD OF VIEW

7.3

RESOLUTION

7.4

BRIGHTNESS

7.5

ACCURACY

7.6

COMBINER TRANSMITTANCE

8

HEAD-UP DISPLAY MARKET, BY COMPONENT

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

92

8.1

INTRODUCTION

8.2

VIDEO GENERATORS/PROCESSING UNITS

8.2.1

RELIANCE ON ADVANCED PROCESSING POWER FOR AR INTEGRATION TO BOOST SEGMENTAL GROWTH

8.2.2

GRAPHICS PROCESSING UNIT (GPU)

8.2.3

EMBEDDED SYSTEM CONTROLLER

8.2.4

SIGNAL PROCESSING UNIT

8.2.5

AUGMENTED REALITY ENGINE

8.3

PROJECTORS/PROJECTION UNITS

8.3.1

ADVANCES IN LIQUID CRYSTAL, LASER BEAM, AND DIGITAL LIGHT PROCESSING TECHNOLOGIES TO FUEL SEGMENTAL GROWTH

8.4

DISPLAY UNITS

8.4.1

EVOLVING DISPLAY ARCHITECTURES TO ENHANCE VISUAL CLARITY TO FACILITATE SEGMENTAL GROWTH

8.4.2

LCD/TFT DISPLAY

8.4.3

OLED

8.4.4

DLP

8.4.5

LCOS

8.5

OTHER COMPONENTS

9

HEAD-UP DISPLAY MARKET, BY TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

98

9.1

INTRODUCTION

9.2

CONVENTIONAL HUDS

9.2.1

RISING INTEGRATION INTO MID-RANGE AND MASS-MARKET VEHICLES TO CONTRIBUTE TO SEGMENTAL GROWTH

9.3

AR HUDS

9.3.1

INCREASING ADOPTION IN LUXURY CARS TO BOLSTER SEGMENTAL GROWTH

10

HEAD-UP DISPLAY MARKET, BY FORM FACTOR

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 8 Data Tables

102

10.1

INTRODUCTION

10.2

WINDSHIELD HUDS

10.2.1

GROWING POPULARITY AMONG MANUFACTURERS OF LUXURY AND UPPER MID-RANGE VEHICLES TO ACCELERATE SEGMENTAL GROWTH

10.3

COMBINER HUDS

10.3.1

RELIABILITY, EASE OF INTEGRATION, AND LOW COST ATTRIBUTES TO CONTRIBUTE TO SEGMENTAL GROWTH

10.4

WEARABLE HUDS

10.4.1

APPLICATION SCOPE IN HIGH-PERFORMANCE, MOBILITY-INTENSIVE ENVIRONMENTS TO FUEL SEGMENTAL GROWTH

11

HEAD-UP DISPLAY MARKET, BY END USE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 38 Data Tables

107

11.1

INTRODUCTION

11.2

AVIATION

11.2.1

CIVIL AVIATION

11.2.1.1

Ability to provide flight path guidance, airspeed notifications, and other information to boost HUD demand

11.2.1.2

Civil aircraft

11.2.1.3

Civil helicopters

11.2.2

MILITARY AVIATION

11.2.2.1

Reliance on HUDs to support search and rescue operations and provide pilots with vital flight-related information to drive market

11.2.2.2

Military aircraft

11.2.2.3

Military helicopters

11.3

AUTOMOTIVE

11.3.1

MID-RANGE VEHICLES

11.3.1.1

Strong focus on improving safety, efficiency, and affordability to foster segmental growth

11.3.2

LUXURY VEHICLES

11.3.2.1

Growing emphasis on personalization, immersive user experiences, and seamless integration of advanced electronics to drive market

11.4

OTHER END USES

12

HEAD-UP DISPLAY MARKET, BY REGION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 126 Data Tables

126

12.1

INTRODUCTION

12.2

NORTH AMERICA

12.2.1

MACROECONOMIC OUTLOOK FOR NORTH AMERICA

12.2.2

US

12.2.2.1

Increasing consumption of luxury, sports, and mid-tier vehicles to boost market growth

12.2.3

CANADA

12.2.3.1

Growing concern about passenger and vehicle safety to drive market

12.2.4

MEXICO

12.2.4.1

Dynamic evolution of automotive industry to fuel market growth

12.3

EUROPE

12.3.1

MACROECONOMIC OUTLOOK FOR EUROPE

12.3.2

GERMANY

12.3.2.1

Increasing reliance on advanced in-vehicle electronics to accelerate market growth

12.3.3

UK

12.3.3.1

Mounting luxury car demand to augment market expansion

12.3.4

FRANCE

12.3.4.1

Growing popularity of displays offering advanced technological capabilities to drive market

12.3.5

ITALY

12.3.5.1

Strong focus on enhancing safety and user experience to foster market growth

12.3.6

SPAIN

12.3.6.1

Rising emphasis on connected mobility and safety features to boost market growth

12.3.7

POLAND

12.3.7.1

Rising automotive manufacturing and defense modernization to expedite market growth

12.3.8

NORDICS

12.3.8.1

High inclination toward safety, EV adoption, and technological innovation to fuel market growth

12.3.9

REST OF EUROPE

12.4

ASIA PACIFIC

12.4.1

MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

12.4.2

CHINA

12.4.2.1

Rising vehicle production to contribute to market growth

12.4.3

JAPAN

12.4.3.1

Continuous mass production of automotive components to drive market

12.4.4

SOUTH KOREA

12.4.4.1

Mounting demand for semi-autonomous and autonomous vehicle technologies to expedite market growth

12.4.5

INDIA

12.4.5.1

Growing automobile innovation and consumer demand to augment HUD adoption

12.4.6

AUSTRALIA

12.4.6.1

Burgeoning adoption of mid-sized and luxury vehicles to bolster market growth

12.4.7

INDONESIA

12.4.7.1

Rapid urbanization and surge in vehicle ownership to support market growth

12.4.8

MALAYSIA

12.4.8.1

Rising enforcement of road safety regulations to boost market growth

12.4.9

THAILAND

12.4.9.1

Government EV push and emergence as automotive hub to accelerate market growth

12.4.10

VIETNAM

12.4.10.1

Rapid economic growth and preference for smart features among middle class population to foster market growth

12.4.11

REST OF ASIA PACIFIC

12.5

ROW

12.5.1

MACROECONOMIC OUTLOOK FOR ROW

12.5.2

MIDDLE EAST

12.5.2.1

Bahrain

12.5.2.2

Kuwait

12.5.2.3

Oman

12.5.2.4

Qatar

12.5.2.5

Saudi Arabia

12.5.2.6

UAE

12.5.2.7

Rest of Middle East

12.5.3

AFRICA

12.5.3.1

South Africa

12.5.3.2

Other African countries

12.5.4

SOUTH AMERICA

12.5.4.1

Strong presence of automobile assembly facilities to foster market growth

13

COMPETITIVE LANDSCAPE

Uncover market dominance tactics and financial prowess shaping competitive dynamics through 2024's key players.

175

13.1

OVERVIEW

13.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020–2025

13.3

MARKET SHARE ANALYSIS, 2024

13.4

REVENUE ANALYSIS, 2020–2024

13.5

COMPANY VALUATION AND FINANCIAL METRICS

13.6

PRODUCT COMPARISON

13.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

13.7.1

STARS

13.7.2

EMERGING LEADERS

13.7.3

PERVASIVE PLAYERS

13.7.4

PARTICIPANTS

13.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

13.7.5.1

Company footprint

13.7.5.2

Region footprint

13.7.5.3

Form factor footprint

13.7.5.4

End use footprint

13.7.5.5

Type footprint

13.8

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

13.8.1

PROGRESSIVE COMPANIES

13.8.2

RESPONSIVE COMPANIES

13.8.3

DYNAMIC COMPANIES

13.8.4

STARTING BLOCKS

13.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

13.8.5.1

Detailed list of key startups/SMEs

13.8.5.2

Competitive benchmarking of key startups/SMEs

13.9

COMPETITIVE SCENARIO

13.9.1

PRODUCT LAUNCHES/DEVELOPMENTS

13.9.2

DEALS

14

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

190

14.1

INTRODUCTION

14.2

KEY PLAYERS

14.2.1

NIPPON SEIKI CO., LTD.

14.2.1.1

Business overview

14.2.1.2

Products/Solutions/Services offered

14.2.1.3

Recent developments

14.2.1.4

MnM view

14.2.2

CONTINENTAL AG

14.2.3

DENSO CORPORATION

14.2.4

PANASONIC HOLDINGS CORPORATION

14.2.5

VALEO

14.2.6

HARMAN INTERNATIONAL

14.2.7

E-LEAD ELECTRONICS CO., LTD

14.2.8

BAE SYSTEMS

14.2.9

YAZAKI CORPORATION

14.2.10

GARMIN LTD.

14.3

OTHER PLAYERS

14.3.1

THALES

14.3.2

HONEYWELL INTERNATIONAL INC.

14.3.3

CMC ELECTRONICS

14.3.4

COLLINS AEROSPACE

14.3.5

RENESAS ELECTRONICS CORPORATION

14.3.6

STMICROELECTRONICS

14.3.7

EXCELITAS TECHNOLOGIES CORP.

14.3.8

ELBIT SYSTEMS LTD.

14.3.9

VUZIX CORPORATION

14.3.10

FORYOU CORPORATION

14.3.11

HUDWAY, LLC

14.3.12

WAYRAY AG

14.3.13

ENVISICS

14.3.14

TEXAS INSTRUMENTS INCORPORATED

14.3.15

SAMTEL AVIONICS

15

APPENDIX

233

15.1

INSIGHTS FROM INDUSTRY EXPERTS

15.2

DISCUSSION GUIDE

15.3

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

15.4

CUSTOMIZATION OPTIONS

15.5

RELATED REPORTS

15.6

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

HEAD-UP DISPLAY MARKET: INCLUSIONS AND EXCLUSIONS

TABLE 2

MAJOR SECONDARY SOURCES

TABLE 3

DATA CAPTURED FROM PRIMARY SOURCES

TABLE 4

PRIMARY INTERVIEW PARTICIPANTS

TABLE 5

HEAD-UP DISPLAY MARKET: RISK ANALYSIS

TABLE 6

APPLICATIONS THAT BENEFIT FROM HUDS

TABLE 7

ROLE OF COMPANIES IN HEAD-UP DISPLAY ECOSYSTEM

TABLE 8

AVERAGE SELLING PRICE OF AUTOMOTIVE HUDS PROVIDED BY KEY PLAYERS, 2024 (USD)

TABLE 9

AVERAGE SELLING PRICE OF AUTOMOTIVE HUDS, BY REGION, 2024 (USD)

TABLE 10

IMPORT DATA FOR HS CODE 8528-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 11

EXPORT ATA FOR HS CODE 8528-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 12

LIST OF KEY PATENTS, 2021–2024

TABLE 13

HEAD-UP DISPLAY MARKET: PORTER’S FIVE FORCES ANALYSIS

TABLE 14

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP TWO END USES (%)

TABLE 15

KEY BUYING CRITERIA FOR TOP TWO END USES

TABLE 16

NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 17

EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 18

ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 19

ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 20

BASE STANDARDS OF C-ITS

TABLE 21

EUROPEAN TELECOMMUNICATIONS STANDARDS INSTITUTE

TABLE 22

SECURITY AND PRIVACY STANDARDS DEVELOPED BY ETSI

TABLE 23

LIST OF CONFERENCES AND EVENTS, 2025–2026

TABLE 24

US-ADJUSTED RECIPROCAL TARIFF RATES

TABLE 25

HEAD-UP DISPLAY MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 26

HEAD-UP DISPLAY MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 27

HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 28

HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 29

HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2021–2024 (USD MILLION)

TABLE 30

HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2025–2030 (USD MILLION)

TABLE 31

WINDSHIELD HUDS: HEAD-UP DISPLAY MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 32

WINDSHIELD HUDS: HEAD-UP DISPLAY MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 33

COMBINER HUDS: HEAD-UP DISPLAY MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 34

COMBINER HUDS: HEAD-UP DISPLAY MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 35

WEARABLE HUDS: HEAD-UP DISPLAY MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 36

WEARABLE HUDS: HEAD-UP DISPLAY MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 37

HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 38

HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 39

HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (MILLION UNITS)

TABLE 40

HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (MILLION UNITS)

TABLE 41

AVIATION: HEAD-UP DISPLAY MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 42

AVIATION: HEAD-UP DISPLAY MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 43

AVIATION: HEAD-UP DISPLAY MARKET IN NORTH AMERICA, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 44

AVIATION: HEAD-UP DISPLAY MARKET IN NORTH AMERICA, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 45

AVIATION: HEAD-UP DISPLAY MARKET IN EUROPE, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 46

AVIATION: HEAD-UP DISPLAY MARKET IN EUROPE, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 47

AVIATION: HEAD-UP DISPLAY MARKET IN ASIA PACIFIC, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 48

AVIATION: HEAD-UP DISPLAY MARKET IN ASIA PACIFIC, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 49

AVIATION: HEAD-UP DISPLAY MARKET IN ROW, BY REGION, 2021–2024 (USD MILLION)

TABLE 50

AVIATION: HEAD-UP DISPLAY MARKET IN ROW, BY REGION, 2025–2030 (USD MILLION)

TABLE 51

AVIATION: HEAD-UP DISPLAY MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 52

AVIATION: HEAD-UP DISPLAY MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 53

AUTOMOTIVE: HEAD-UP DISPLAY MARKET, BY VEHICLE TYPE, 2021–2024 (USD MILLION)

TABLE 54

AUTOMOTIVE: HEAD-UP DISPLAY MARKET, BY VEHICLE TYPE, 2025–2030 (USD MILLION)

TABLE 55

AUTOMOTIVE: HEAD-UP DISPLAY MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 56

AUTOMOTIVE: HEAD-UP DISPLAY MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 57

AUTOMOTIVE: HEAD-UP DISPLAY MARKET IN NORTH AMERICA, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 58

AUTOMOTIVE: HEAD-UP DISPLAY MARKET IN NORTH AMERICA, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 59

AUTOMOTIVE: HEAD-UP DISPLAY MARKET IN EUROPE, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 60

AUTOMOTIVE: HEAD-UP DISPLAY MARKET IN EUROPE, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 61

AUTOMOTIVE: HEAD-UP DISPLAY MARKET IN ASIA PACIFIC, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 62

AUTOMOTIVE: HEAD-UP DISPLAY MARKET IN ASIA PACIFIC, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 63

AUTOMOTIVE: HEAD-UP DISPLAY MARKET IN ROW, BY REGION, 2021–2024 (USD MILLION)

TABLE 64

AUTOMOTIVE: HEAD-UP DISPLAY MARKET IN ROW, BY REGION, 2025–2030 (USD MILLION)

TABLE 65

OTHER END USES: HEAD-UP DISPLAY MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 66

OTHER END USES: HEAD-UP DISPLAY MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 67

OTHER END USES: HEAD-UP DISPLAY MARKET IN NORTH AMERICA, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 68

OTHER END USES: HEAD-UP DISPLAY MARKET IN NORTH AMERICA, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 69

OTHER END USES: HEAD-UP DISPLAY MARKET IN EUROPE, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 70

OTHER END USES: HEAD-UP DISPLAY MARKET IN EUROPE, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 71

OTHER END USES: HEAD-UP DISPLAY MARKET IN ASIA PACIFIC, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 72

OTHER END USES: HEAD-UP DISPLAY MARKET IN ASIA PACIFIC, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 73

OTHER END USES: HEAD-UP DISPLAY MARKET IN ROW, BY REGION, 2021–2024 (USD MILLION)

TABLE 74

OTHER END USES: HEAD-UP DISPLAY MARKET IN ROW, BY REGION, 2025–2030 (USD MILLION)

TABLE 75

HEAD-UP DISPLAY MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 76

HEAD-UP DISPLAY MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 77

NORTH AMERICA: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 78

NORTH AMERICA: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 79

NORTH AMERICA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 80

NORTH AMERICA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 81

NORTH AMERICA: HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2021–2024 (USD MILLION)

TABLE 82

NORTH AMERICA: HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2025–2030 (USD MILLION)

TABLE 83

US: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 84

US: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 85

US: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 86

US: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 87

CANADA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 88

CANADA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 89

CANADA: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 90

CANADA: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 91

MEXICO: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 92

MEXICO: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 93

MEXICO: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 94

MEXICO: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 95

EUROPE: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 96

EUROPE: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 97

EUROPE: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 98

EUROPE: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 99

EUROPE: HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2021–2024 (USD MILLION)

TABLE 100

EUROPE: HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2025–2030 (USD MILLION)

TABLE 101

GERMANY: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 102

GERMANY: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 103

GERMANY: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 104

GERMANY: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 105

UK: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 106

UK: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 107

UK: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 108

UK: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 109

FRANCE: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 110

FRANCE: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 111

FRANCE: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 112

FRANCE: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 113

ITALY: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 114

ITALY: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 115

ITALY: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 116

ITALY: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 117

SPAIN: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 118

SPAIN: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 119

SPAIN: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 120

SPAIN: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 121

POLAND: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 122

POLAND: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 123

POLAND: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 124

POLAND: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 125

NORDICS: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 126

NORDICS: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 127

NORDICS: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 128

NORDICS: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 129

REST OF EUROPE: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 130

REST OF EUROPE: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 131

REST OF EUROPE: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 132

REST OF EUROPE: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 133

ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 134

ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 135

ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 136

ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 137

ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2021–2024 (USD MILLION)

TABLE 138

ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2025–2030 (USD MILLION)

TABLE 139

CHINA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 140

CHINA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 141

CHINA: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 142

CHINA: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 143

JAPAN: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 144

JAPAN: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 145

JAPAN: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 146

JAPAN: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 147

SOUTH KOREA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 148

SOUTH KOREA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 149

SOUTH KOREA: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 150

SOUTH KOREA: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 151

INDIA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 152

INDIA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 153

INDIA: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 154

INDIA: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 155

AUSTRALIA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 156

AUSTRALIA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 157

AUSTRALIA: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 158

AUSTRALIA: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 159

INDONESIA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 160

INDONESIA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 161

INDONESIA: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 162

INDONESIA: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 163

MALAYSIA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 164

MALAYSIA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 165

MALAYSIA: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 166

MALAYSIA: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 167

THAILAND: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 168

THAILAND: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 169

THAILAND: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 170

THAILAND: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 171

VIETNAM: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 172

VIETNAM: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 173

VIETNAM: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 174

VIETNAM: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 175

REST OF ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 176

REST OF ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 177

REST OF ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 178

REST OF ASIA PACIFIC: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 179

ROW: HEAD-UP DISPLAY MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 180

ROW: HEAD-UP DISPLAY MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 181

ROW: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 182

ROW: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 183

ROW: HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2021–2024 (USD MILLION)

TABLE 184

ROW: HEAD-UP DISPLAY MARKET, BY FORM FACTOR, 2025–2030 (USD MILLION)

TABLE 185

MIDDLE EAST: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 186

MIDDLE EAST: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 187

MIDDLE EAST: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 188

MIDDLE EAST: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 189

MIDDLE EAST: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 190

MIDDLE EAST: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 191

AFRICA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 192

AFRICA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 193

AFRICA: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 194

AFRICA: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 195

AFRICA: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 196

AFRICA: HEAD-UP DISPLAY MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 197

SOUTH AMERICA: HEAD-UP DISPLAY MARKET, BY END USE, 2021–2024 (USD MILLION)

TABLE 198

SOUTH AMERICA: HEAD-UP DISPLAY MARKET, BY END USE, 2025–2030 (USD MILLION)

TABLE 199

SOUTH AMERICA: HEAD-UP DISPLAY MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 200

SOUTH AMERICA: HEAD-UP DISPLAY MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 201

HEAD-UP DISPLAY MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2020–JULY 2025

TABLE 202

HEAD-UP DISPLAY MARKET: DEGREE OF COMPETITION, 2024

TABLE 203

HEAD-UP DISPLAY MARKET: REGION FOOTPRINT

TABLE 204

HEAD-UP DISPLAY MARKET: FORM FACTOR FOOTPRINT

TABLE 205

HEAD-UP DISPLAY MARKET: END USE FOOTPRINT

TABLE 206

HEAD-UP DISPLAY MARKET: TYPE FOOTPRINT

TABLE 207

HEAD-UP DISPLAY MARKET: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 208

HEAD-UP DISPLAY MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 209

HEAD-UP DISPLAY MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, JANUARY 2020–JULY 2025

TABLE 210

HEAD-UP DISPLAY MARKET: DEALS, JANUARY 2020–JULY 2025

TABLE 211

NIPPON SEIKI CO., LTD.: COMPANY OVERVIEW

TABLE 212

NIPPON SEIKI CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 213

NIPPON SEIKI CO., LTD.: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 214

NIPPON SEIKI CO., LTD.: DEALS

TABLE 215

NIPPON SEIKI CO., LTD.: EXPANSIONS

TABLE 216

CONTINENTAL AG: COMPANY OVERVIEW

TABLE 217

CONTINENTAL AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 218

CONTINENTAL AG: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 219

CONTINENTAL AG: DEALS

TABLE 220

DENSO CORPORATION: COMPANY OVERVIEW

TABLE 221

DENSO CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 222

DENSO CORPORATION: DEALS

TABLE 223

PANASONIC HOLDINGS CORPORATION: COMPANY OVERVIEW

TABLE 224

PANASONIC HOLDINGS CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 225

PANASONIC HOLDINGS CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 226

PANASONIC HOLDINGS CORPORATION: DEALS

TABLE 227

VALEO: COMPANY OVERVIEW

TABLE 228

VALEO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 229

VALEO: DEALS

TABLE 230

HARMAN INTERNATIONAL: COMPANY OVERVIEW

TABLE 231

HARMAN INTERNATIONAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 232

HARMAN INTERNATIONAL: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 233

HARMAN INTERNATIONAL: OTHER DEVELOPMENTS

TABLE 234

E-LEAD ELECTRONIC CO. LTD: COMPANY OVERVIEW

TABLE 235

E-LEAD ELECTRONIC CO. LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 236

BAE SYSTEMS: COMPANY OVERVIEW

TABLE 237

BAE SYSTEMS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 238

BAE SYSTEMS: PRODUCT LAUNCHES/DEVELOPMENTS

TABLE 239

YAZAKI CORPORATION: COMPANY OVERVIEW

TABLE 240

YAZAKI CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 241

GARMIN LTD.: COMPANY OVERVIEW

TABLE 242

GARMIN LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

LIST OF FIGURES

FIGURE 1

HEAD-UP DISPLAY MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

HEAD-UP DISPLAY MARKET: DURATION CONSIDERED

FIGURE 3

HEAD-UP DISPLAY MARKET: RESEARCH DESIGN

FIGURE 4

DATA CAPTURED FROM SECONDARY SOURCES

FIGURE 5

BREAKDOWN OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

FIGURE 6

CORE FINDINGS FROM INDUSTRY EXPERTS

FIGURE 7

HEAD-UP DISPLAY MARKET: RESEARCH APPROACH

FIGURE 8

HEAD-UP DISPLAY MARKET SIZE ESTIMATION - APPROACH 1 (SUPPLY SIDE)

FIGURE 9

HEAD-UP DISPLAY MARKET SIZE ESTIMATION - APPROACH 2 (SUPPLY SIDE)

FIGURE 10

HEAD-UP DISPLAY MARKET SIZE ESTIMATION - APPROACH 3 (DEMAND SIDE)

FIGURE 11

HEAD-UP DISPLAY MARKET: BOTTOM-UP APPROACH

FIGURE 12

HEAD-UP DISPLAY MARKET: TOP-DOWN APPROACH

FIGURE 13

HEAD-UP DISPLAY MARKET: DATA TRIANGULATION

FIGURE 14

HEAD-UP DISPLAY MARKET: RESEARCH ASSUMPTIONS

FIGURE 15

HEAD-UP DISPLAY MARKET: RESEARCH LIMITATIONS

FIGURE 16

GLOBAL HEAD-UP DISPLAY MARKET SIZE, 2021–2030

FIGURE 17

CONVENTIONAL HUDS SEGMENT TO HOLD LARGER MARKET SHARE IN 2030

FIGURE 18

WINDSHIELD HUDS SEGMENT TO DOMINATE MARKET FROM 2025 TO 2030

FIGURE 19

PROJECTORS/PROJECTION UNITS SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2030

FIGURE 20

AUTOMOTIVE SEGMENT TO RECORD HIGHEST CAGR FROM 2025 TO 2030

FIGURE 21

ASIA PACIFIC TO EXHIBIT HIGHEST CAGR IN HEAD-UP DISPLAY MARKET DURING FORECAST PERIOD

FIGURE 22

RISING GLOBAL DEMAND FOR SEMI-AUTONOMOUS AND ELECTRIC VEHICLES TO DRIVE HEAD-UP DISPLAY MARKET

FIGURE 23

AUTOMOTIVE SEGMENT TO CAPTURE LARGEST MARKET SHARE IN 2025

FIGURE 24

WINDSHIELD HUDS TO DOMINATE HEAD-UP DISPLAY MARKET DURING FORECAST PERIOD

FIGURE 25

CONVENTIONAL HUDS TO HOLD LARGER SHARE OF HEAD-UP DISPLAY MARKET IN 2030

FIGURE 26

ASIA PACIFIC TO DOMINATE HEAD-UP DISPLAY MARKET BETWEEN 2025 AND 2030

FIGURE 27

DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 28

DRIVERS: IMPACT ANALYSIS

FIGURE 29

NUMBER OF ROAD ACCIDENT DEATHS, BY COUNTRY, H1 2024

FIGURE 30

PROJECTED ANNUAL COUNT OF FATALITIES POTENTIALLY AVOIDED BY ADAS TECHNOLOGIES

FIGURE 31

BENEFITS OF HUD FOR END USERS

FIGURE 32

CATEGORIES OF HUD DESIGNS

FIGURE 33

RESTRAINTS: IMPACT ANALYSIS

FIGURE 34

OPPORTUNITIES: IMPACT ANALYSIS

FIGURE 35

CHALLENGES: IMPACT ANALYSIS

FIGURE 36

VALUE CHAIN ANALYSIS

FIGURE 37

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 38

HEAD-UP DISPLAY ECOSYSTEM

FIGURE 39

INVESTMENT AND FUNDING SCENARIO

FIGURE 40

AVERAGE SELLING PRICE OF AUTOMOTIVE HUDS OFFERED BY KEY PLAYERS, 2024

FIGURE 41

IMPORT DATA FOR HS CODE 8528-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2020–2024

FIGURE 42

EXPORT DATA FOR HS CODE 8528-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2020–2024

FIGURE 43

PATENTS APPLIED AND GRANTED, 2015–2024

FIGURE 44

PORTER’S FIVE FORCES ANALYSIS

FIGURE 45

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP TWO END USES

FIGURE 46

KEY BUYING CRITERIA FOR TOP TWO END USES

FIGURE 47

USE CASES AND IMPACT OF AI/GEN AI ON HEAD-UP DISPLAY MARKET

FIGURE 48

PROJECTORS/PROJECTION UNITS SEGMENT TO HOLD LARGEST MARKET SHARE IN 2030

FIGURE 49

CONVENTIONAL HUDS SEGMENT TO DOMINATE HEAD-UP DISPLAY MARKET FROM 2025 TO 2030

FIGURE 50

WINDSHIELD HUDS SEGMENT TO CAPTURE LARGEST SHARE OF HEAD-UP DISPLAY MARKET IN 2030

FIGURE 51

AUTOMOTIVE SEGMENT TO EXHIBIT HIGHEST CAGR FROM 2025 TO 2030

FIGURE 52

ASIA PACIFIC TO RECORD HIGHEST CAGR IN HEAD-UP DISPLAY MARKET DURING FORECAST PERIOD

FIGURE 53

NORTH AMERICA: HEAD-UP DISPLAY MARKET SNAPSHOT

FIGURE 54

EUROPE: HEAD-UP DISPLAY MARKET SNAPSHOT

FIGURE 55

ASIA PACIFIC: HEAD-UP DISPLAY MARKET SNAPSHOT

FIGURE 56

ROW: HEAD-UP DISPLAY MARKET SNAPSHOT

FIGURE 57

MARKET SHARE ANALYSIS OF COMPANIES OFFERING HEAD-UP DISPLAYS, 2024

FIGURE 58

HEAD-UP DISPLAY MARKET: REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2020–2024

FIGURE 59

COMPANY VALUATION

FIGURE 60

FINANCIAL METRICS (EV/EBITDA)

FIGURE 61

PRODUCT COMPARISON

FIGURE 62

HEAD-UP DISPLAY MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 63

HEAD-UP DISPLAY MARKET: COMPANY FOOTPRINT

FIGURE 64

HEAD-UP DISPLAY MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 65

NIPPON SEIKI CO., LTD.: COMPANY SNAPSHOT

FIGURE 66

CONTINENTAL AG: COMPANY SNAPSHOT

FIGURE 67

DENSO CORPORATION: COMPANY SNAPSHOT

FIGURE 68

PANASONIC HOLDINGS CORPORATION: COMPANY SNAPSHOT

FIGURE 69

VALEO: COMPANY SNAPSHOT

FIGURE 70

HARMAN INTERNATIONAL: COMPANY SNAPSHOT

FIGURE 71

E-LEAD ELECTRONIC CO. LTD: COMPANY SNAPSHOT

FIGURE 72

BAE SYSTEMS: COMPANY SNAPSHOT

FIGURE 73

YAZAKI CORPORATION: COMPANY SNAPSHOT

FIGURE 74

GARMIN LTD.: COMPANY SNAPSHOT

Methodology

The study involved major activities in estimating the current market size for the global Head-Up Display market. Exhaustive secondary research was done to collect information on the market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain using primary research. Different approaches, such as top-down and bottom-up, were employed to estimate the total market size. After that, the market breakup and data triangulation procedures were used to estimate the market size of the segments and subsegments of the head-up display market.

Secondary Research

The secondary research for this study involved gathering information from a range of credible sources. These included company annual reports, investor presentations, press releases, whitepapers, certified publications, and articles from reputable associations and government publications. Additional data was obtained from corporate filings, professional and trade associations, journals, and industry-recognized authors. Research from consortia, councils, and gold- and silver-standard websites, directories, and databases also contributed to the qualitative framework. Key global sources, such as the International Trade Centre (ITC) and the International Monetary Fund (IMF), were consulted to support and validate the market analysis.

Primary Research

Extensive primary research was conducted after understanding and analyzing the head-up display market scenario through secondary research. Several primary interviews were conducted with key opinion leaders from demand- and supply-side vendors across four major regions—North America, Europe, Asia Pacific, and RoW. Approximately 20% of the primary interviews were conducted with the demand side and 80% with the supply side. Primary data was collected through questionnaires, e-mails, and telephonic interviews. Various departments within organizations, such as sales, operations, and administration, were contacted to provide a holistic viewpoint in the report.

Market Size, and Share")

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

Both top-down and bottom-up approaches were used to estimate and validate the total size of the head-up display market. These methods were also used extensively to estimate the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

Head-up Display (HUD) Market : Top-Down and Bottom-Up Approach

Market Top Down and Bottom Up Approach")

Data Triangulation

After arriving at the overall size of the head-up display market through the process explained above, the overall market has been split into several segments. Data triangulation procedures have been employed to complete the overall market engineering process and arrive at the exact statistics for all the segments, wherever applicable. The data has been triangulated by studying various factors and trends from the demand and supply sides. The market has also been validated using top-down and bottom-up approaches.

Market Definition

A head-up display (HUD) is a visual system that projects key information, such as speed, navigation cues, or safety alerts, directly into the user’s line of sight, typically onto a windshield, combiner, or wearable device. Its purpose is to provide critical data without requiring the driver or pilot to look away from their primary viewpoint, thereby enhancing safety, reducing distractions, and improving situational awareness.

Key Stakeholders

- Raw material suppliers

- Original equipment manufacturers (OEMs)

- Original design manufacturers (ODM)

- Research institutes

- Head-up display solution providers

- Forums, alliances, and associations

- Governments and financial institutions

- Analysts and strategic business planners

- Distributors

- End users

Report Objectives

- To describe and forecast the size of the global Head-Up Display market, by type, component, form factor, and end user, in terms of value

- To describe and forecast the global Head-Up Display market size of various segments across four key regions—North America, Europe, Asia Pacific, and the Rest of the World (RoW), in terms of value

- To describe and forecast the size of the global Head-Up Display market, by end user, in terms of volume

- To provide detailed information regarding the drivers, restraints, opportunities, and challenges influencing the growth of the global Head-Up Display market

- To provide an overview of the value chain pertaining to the global Head-Up Display ecosystem and the average selling prices of head-up displays

- To provide a detailed overview of the impact of AI/Gen AI and the US 2025 tariff on the global Head-Up Display market

- To provide information about key technological trends, trade analysis, and patents related to head-up displays

- To benchmark the market players using the proprietary company evaluation matrix framework, which analyzes them on various parameters within the broad categories of market ranking/share and product portfolio in the global Head-Up Display

- To analyze competitive developments, such as partnerships, acquisitions, agreements, collaborations, and product launches in the global Head-Up Display market

- To strategically profile key players and analyze their market share, ranking, and core competencies in the global Head-Up Display market

Customization Options

With the market data given, MarketsandMarkets offers customizations according to the company’s specific needs. The following customization options are available for the report:

Company Information:

- Detailed analysis and profiling of additional market players (up to 7)

Key Questions Addressed by the Report

What is the current size of the Head-Up Display (HUD) market?

The global Head-Up Display (HUD) market is valued at USD 4.20 billion in 2025 and is projected to reach USD 7.34 billion by 2030. (MarketsandMarkets)

What is the expected growth rate of the HUD market?

The market is expected to grow at a CAGR of 11.8% during the forecast period from 2025 to 2030. (MarketsandMarkets)

What are the major growth drivers for the HUD industry?

Growth is driven by increasing adoption of Advanced Driver Assistance Systems (ADAS), demand for enhanced road safety, connected vehicles, electric vehicles, and augmented reality (AR) technologies in automotive applications. (MarketsandMarkets)

What are the key technology trends in the HUD market?

Major trends include AR-based HUDs, high-resolution display technologies, waveguide optics, real-time navigation overlays, and integration with autonomous and connected vehicle systems. (MarketsandMarkets)

Which segment dominates the HUD market by end user?

The automotive segment is expected to account for the largest market share due to rising demand for navigation assistance, safety alerts, and immersive driving experiences. (MarketsandMarkets)

Which HUD type is witnessing the fastest growth?

Augmented Reality (AR) HUDs are expected to be the fastest-growing segment because they provide contextual navigation, lane guidance, and enhanced driver awareness. (MarketsandMarkets)

Which region is expected to grow the fastest in the HUD market?

Asia Pacific is projected to record the highest growth, with a CAGR of approximately 14.3% from 2025 to 2030, driven by strong automotive production and adoption of advanced vehicle technologies. (MarketsandMarkets)

Who are the leading companies operating in the HUD market?

Key players include Nippon Seiki Co., Ltd., Continental AG, Panasonic Holdings Corporation, Valeo, and DENSO CORPORATION. (MarketsandMarkets)

What opportunities exist in the HUD market?

Opportunities include expansion of HUDs into mid-range vehicles, wearable HUD applications, electric and autonomous vehicles, aviation systems, and industrial hands-free visualization solutions. (MarketsandMarkets)

How is the HUD market analyzed in the report?

The report uses top-down and bottom-up market sizing methodologies, data triangulation, competitive benchmarking, company analysis, regional assessments, and forecast modeling to estimate market size and growth. (MarketsandMarkets)

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Head-up Display (HUD) Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

- Canada Head-up Display (HUD) Market

- Mexico Head-up Display (HUD) Market

- US Head-up Display (HUD) Market

- Germany Head-up Display (HUD) Market

- UK Head-up Display (HUD) Market

- France Head-up Display (HUD) Market

- Italy Head-up Display (HUD) Market

- Spain Head-up Display (HUD) Market

- Poland Head-up Display (HUD) Market

- China Head-up Display (HUD) Market

- Japan Head-up Display (HUD) Market

- South Korea Head-up Display (HUD) Market

- India Head-up Display (HUD) Market

- Australia Head-up Display (HUD) Market

- Indonesia Head-up Display (HUD) Market

- Malaysia Head-up Display (HUD) Market

- Thailand Head-up Display (HUD) Market

- Vietnam Head-up Display (HUD) Market

- Nordics Head-up Display (HUD) Market

- Rest Of Europe Head-up Display (HUD) Market

- Rest Of Asia Pacific Head-up Display (HUD) Market

Growth opportunities and latent adjacency in Head-up Display (HUD) Market

Arthur

Apr, 2026

I�m considering purchasing this Head-up Display Market report�does it analyze long-term growth opportunities across automotive and aviation applications?.

User

Sep, 2019

The demand for HUDs is high in automotive as well as in aerospace sector. I would like to know in detail, which of these sectors would grow at a high rate and where would the return on investment (RoI) be high? Is this aspect of comparative analysis between these two applications been covered in detail in your report?.

User

Sep, 2019

What would be the major differentiating factors between AR HUD and conventional HUDs? Which would be the one preferred by the car makers considering their features, avaialability, as well as pricing? Would you be able to provide the major players producing both these HUDs and their product features?.

User

Sep, 2019

The European region leads in production of high-end cars. Will this also be in line with the demand of HUDs? I would like to know the regionwise demand of HUDs and the key reasons behind the analysis. Does your report cover the regionwise data of HUDs and analysis?.