Download PDF

Download PDF Request Customisation

Request Customisation

Hydrogen Generation Market

Report Code

EP 2781

Published in

Jul, 2025, By MarketsandMarkets™

Hydrogen Generation Market by Technology (SMR, ATR, POX, Coal Gasification, Electrolysis), Application (Refinery, Ammonia, Methanol, Transportation, Power Generation), Source (Blue, Green, Gray), Generation & Delivery Mode, Region - Global Forecast to 2030

USD 226.37 BN

MARKET SIZE, 2030

CAGR 7.5%

(2025-2030)

300

REPORT PAGES

350

MARKET TABLES

OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

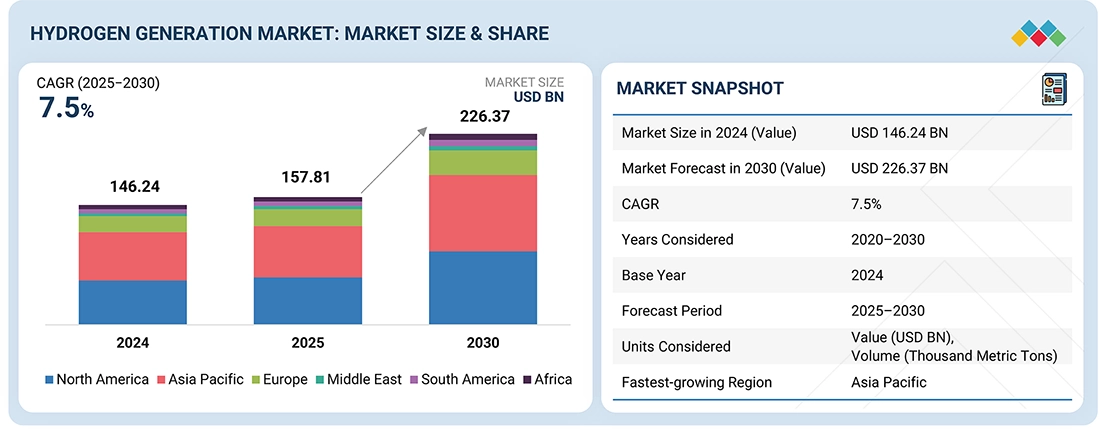

The hydrogen generation market size is projected to reach USD 226.37 billion by 2030, up from an estimated USD 157.81 billion in 2025, growing at a CAGR of 7.5% during the forecast period. The market growth is driven by increasing global efforts to decarbonize energy systems, growing demand for clean fuel alternatives, and the expanding use of hydrogen in industrial, transportation, and power generation sectors.

Market Size and Forecast:

- Market Size Value in 2024: USD 146.24 Billion

- Market Size Value in 2025: USD 157.81 Billion

- Revenue Forecast in 2030: USD 226.37 Billion

- Growth Rate: CAGR of 7.5% from 2025 to 2030

- Data available from 2020 to 2030

Key Market Trends and Insights

- Market Growth: Growth is driven by increasing global demand for low-carbon energy, government decarbonization initiatives, and rising hydrogen consumption across refining, ammonia production, transportation, and power generation sectors.

-

Green Hydrogen Impact: Advancements in electrolysis technologies and increasing investments in green hydrogen projects are accelerating the transition toward sustainable hydrogen production, supporting industrial decarbonization and energy security goals.

- Growing Trends: The market is witnessing increased adoption of green and blue hydrogen, expansion of hydrogen infrastructure, integration of carbon capture technologies, and growing use of hydrogen in transportation and power generation applications

-

Growth Opportunities: Opportunities include expanding green hydrogen production through electrolysis, increasing adoption of hydrogen fuel cells in transportation, investments in hydrogen infrastructure and storage networks, and integration of carbon capture technologies to support low-carbon hydrogen production.

-

North America Hydrogen Generation Market

- Market size USD 32.27 billion in 2025

- Market forecast USD 45.34 billion in 2030

- Market Growing at a CAGR of 7.0%

-

Europe Hydrogen Generation Market

- Market size USD 28.68 billion in 2025

- Market forecast USD 42.38 billion in 2030

- Market Growing at a CAGR of 8.1%

-

US Hydrogen Generation Market

- Market size USD 23.50 billion in 2025

- Market forecast USD 33.27 billion in 2030

- Market Growing at a CAGR of 7.2%

-

Captive Hydrogen Generation Market

- Market size USD 123.39 billion in 2022

- Market forecast USD 189.91 billion in 2030

- Market Growing at a CAGR of 7.4%

-

China Hydrogen Generation Market

- Market size USD 46.69 billion in 2024

- Market forecast USD 73.29 billion in 2030

- Market Growing at a CAGR of 7.8%

-

Asia Pacific Hydrogen Generation Market

- Market size USD 72.98 billion in 2025

- Market forecast USD 109.43 billion in 2030

- Market Growing at a CAGR of 8.4%

-

North America Hydrogen Generation Market

KEY TAKEAWAYS

-

BY TECHNOLOGYThe steam methane reforming segment holds the largest share in the hydrogen production market. This dominance is driven by SMR’s cost-effectiveness, technological maturity, and capacity to produce hydrogen at a large scale to meet industrial needs. SMR is widely used in the refinery, chemical, and fertilizer industries because of its reliable supply and integration with existing natural gas infrastructure. Additionally, advances in carbon capture and storage (CCS) improve the environmental performance of SMR, supporting its ongoing use. Government support and rising global hydrogen demand further solidify SMR’s leadership in the hydrogen production market.

-

BY APPLICATIONThe transportation segment is anticipated to be the most rapidly expanding application within the hydrogen generation market throughout the forecast period. This expansion is predominantly driven by the increasing adoption of hydrogen fuel cell technologies across diverse mobility sectors, including passenger vehicles, buses, trucks, trains, marine vessels, and aviation. Hydrogen fuel cells provide distinctive advantages such as high energy density, rapid refueling capabilities, and extended operational ranges relative to battery electric vehicles, thereby rendering them especially suitable for heavy-duty and long-distance applications where minimizing downtime remains a paramount concern.

-

BY SOURCEThe green hydrogen segment is anticipated to achieve the highest compound annual growth rate (CAGR) in the hydrogen generation market throughout the forecast period. This growth is propelled by the global shift toward carbon neutrality and the pressing necessity to decarbonize hard-to-abate sectors. Supportive policy frameworks expedite project development and commercialization, including tax incentives, subsidies, and national hydrogen strategies implemented worldwide. Moreover, the increasing demand for zero-emission fuels in applications such as fuel cell vehicles, power generation, and industrial feedstock establishes green hydrogen as a critical facilitator of the international transition to clean energy. Strategic collaborations, large-scale pilot initiatives, and comprehensive decarbonization roadmaps persistently contribute to the advancement of the green hydrogen sector globally.

-

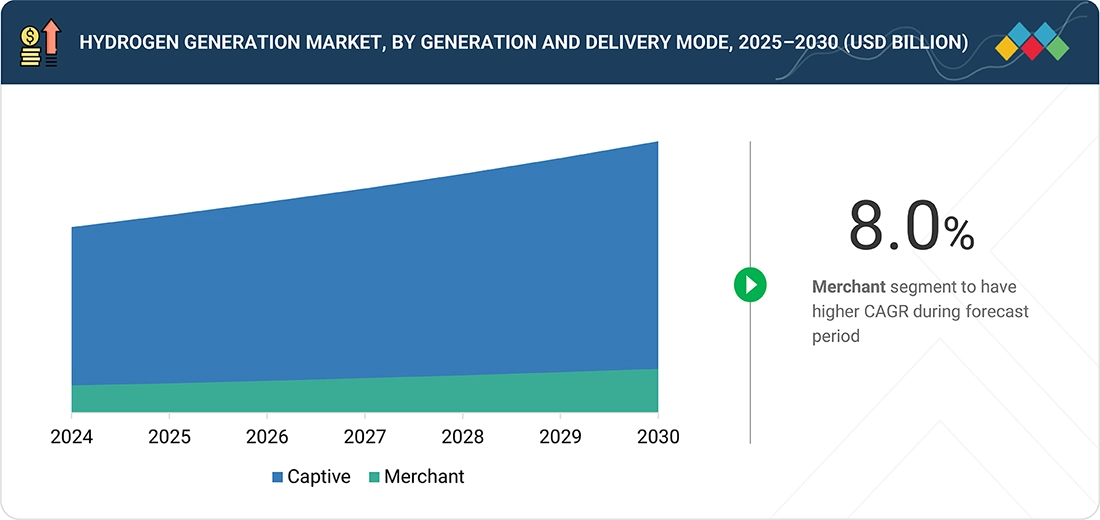

BY GENERATION & DELIVERY MODEThe captive segment is the leading method for hydrogen production, especially in refinery applications, because it can provide a reliable, continuous, and cost-effective hydrogen supply directly on-site. Unlike the merchant segment, which depends on external supply chains and adds transportation and storage costs, captive generation guarantees a steady supply tailored to specific operational needs. This approach is widely used in key sectors such as oil refining, food production, metals treatment, and fertilizer manufacturing, where reliability and seamless integration are essential.

-

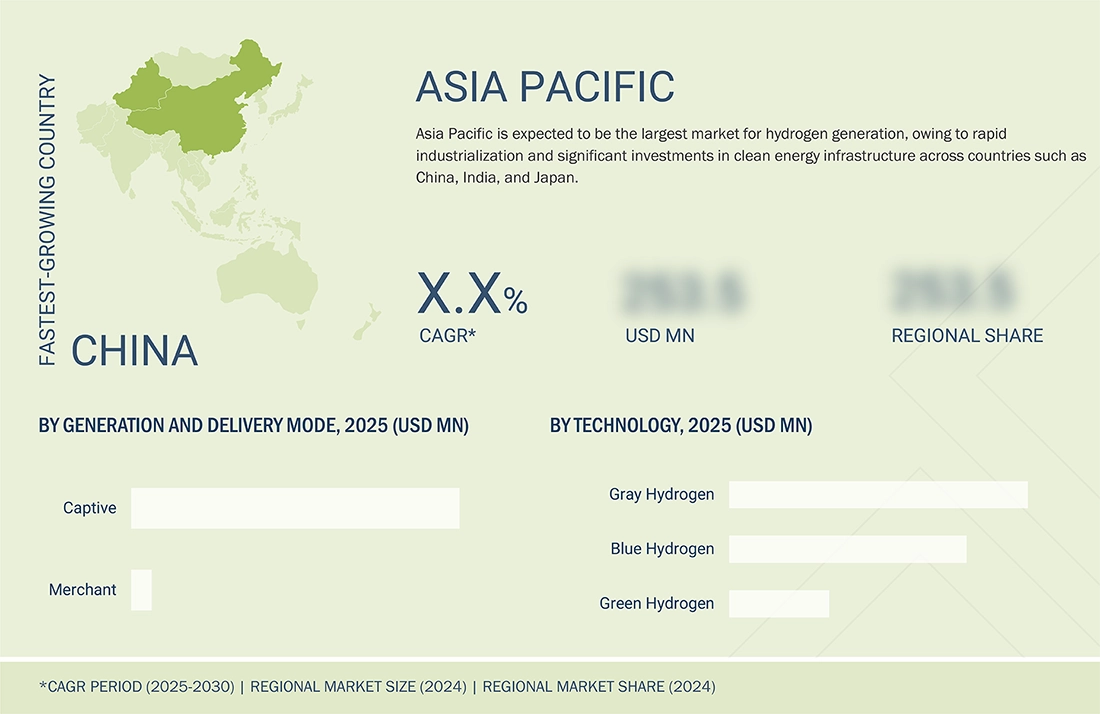

BY REGIONAsia Pacific holds the largest share in the hydrogen generation market, driven by rapid industrial growth, urbanization, and strong efforts to decarbonize energy systems. Countries such as China, Japan, South Korea, and India are making significant investments in hydrogen production infrastructure to support cleaner industrial processes and reduce reliance on fossil fuels. Supportive government policies, national hydrogen strategies, and substantial funding for renewable and low-carbon hydrogen projects speed up market growth. Additionally, increasing demand from refining, chemical, and mobility sectors further boosts the region’s leadership.

-

COMPETITIVE LANDSCAPEMajor market players have adopted both organic and inorganic strategies, such as forming partnerships and signing agreements. For example, Linde PLC, Saudi Arabian Oil Co., Uniper SE, and Orsted A/S have entered into several agreements and partnerships to meet the rising demand for hydrogen.

The hydrogen generation market is fueled by increasing global efforts to decarbonize energy systems, rising demand for clean fuel alternatives, and the expanding use of hydrogen in industrial, transportation, and power generation sectors. Supportive government policies, significant investments in renewable energy, and advances in electrolysis technology drive market growth. Additionally, the development of hydrogen infrastructure and a rising focus on energy security and emission reduction further boost the market’s growth across major global regions.

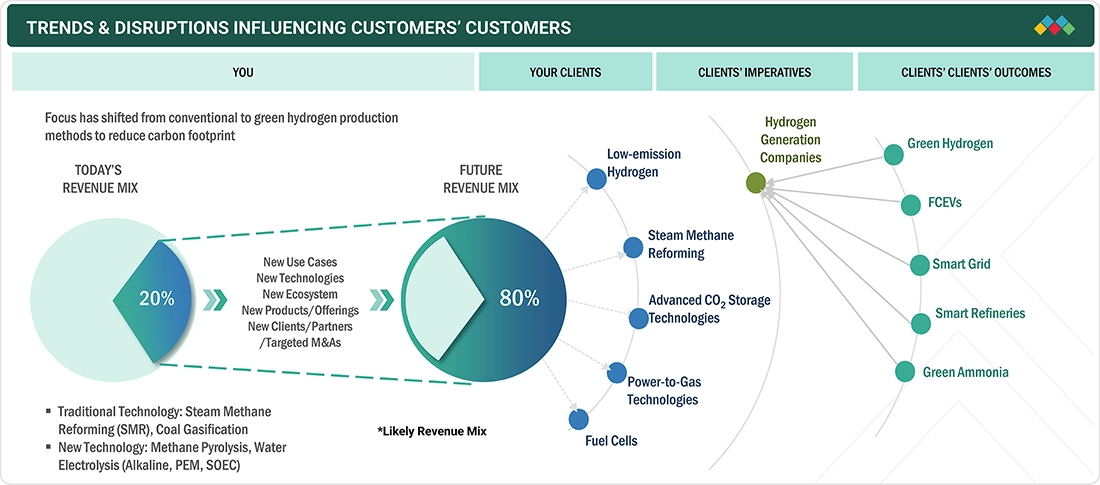

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The hydrogen generation market is undergoing transformative trends, with emerging technologies creating new growth opportunities. Moving from traditional fossil-based methods to low-carbon and renewable options, future revenue streams include green hydrogen from electrolysis, blue hydrogen with carbon capture, and integration with renewable energy sources. Major industries such as refining, chemicals, steel, and transportation are increasingly using hydrogen to reduce carbon emissions, supported by large-scale infrastructure investments. This shift aligns with global net-zero goals while maintaining energy security and efficiency, despite challenges in scaling up production, storage, and distribution infrastructure.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Enforcement of stringent regulations to curb greenhouse gas emissions

-

Government initiatives for developing hydrogen economy

RESTRAINTS

Impact

Level

Level

-

Limited hydrogen infrastructure

-

Energy loss during hydrogen production

OPPORTUNITIES

Impact

Level

Level

-

Rising emphasis on achieving net-zero carbon emission targets

-

Growing investment in low-emission fuels

CHALLENGES

Impact

Level

Level

-

High costs associated with renewable hydrogen production

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Growing emphasis on developing hydrogen economy

Countries around the world emphasize the development of a hydrogen economy as part of their comprehensive strategies to realize energy transition, achieve climate objectives, and strengthen economic resilience. Hydrogen, especially green hydrogen produced via renewable energy sources, is increasingly recognized as a pivotal solution to decarbonize sectors that are challenging to transform, such as steel, cement, chemicals, and heavy transportation. To expedite this transition, various governments have enacted detailed plans, policies, subsidies, and incentive schemes to promote hydrogen development. For example, the European Union unveiled its EU Hydrogen Strategy in 2020, concentrating on expanding hydrogen production and demand, supporting investments, developing infrastructure and markets, advancing research and innovation, and fostering international collaboration. This strategy is supported by an array of complementary policies and incentive mechanisms, including the European Green Deal, the Renewable Energy Directive III (RED III), and REPowerEU, all aimed at accelerating the deployment of clean hydrogen throughout the region. Canada introduced the Clean Hydrogen Investment Tax Credit (CHITC) in 2022, which became effective in 2023. This refundable tax credit applies to eligible clean hydrogen assets acquired and operational from March 28, 2023, through December 31, 2034, and is designed to stimulate investment in qualifying hydrogen projects..

Restraint: Energy loss during hydrogen production

Hydrogen is a synthetic energy carrier. It transports energy produced by various other processes. Water electrolysis converts electrical energy into hydrogen. However, in addition to producing hydrogen, high-grade electrical energy is also utilized to compress, liquefy, transport, transfer, or store the medium. Energy is needed for hydrogen production. The energy input should ideally match the energy level of the synthetic gas. Any method of producing hydrogen, such as electrolysis and reforming, involves energy transformation. The chemical energy of hydrogen is converted from electrical energy or the chemical energy of hydrocarbons. Unfortunately, energy losses are always a part of the creation of hydrogen. Energy loss occurs across every step of hydrogen production. In the production stage, the energy needed for electrolysis is lost by around 30%. An additional 10–25% of energy is lost during conversion to other forms. Energy input is required to deliver green hydrogen, either in the form of fuel for vehicles or energy from pipes. Utilizing hydrogen in fuel cells results in more energy loss.

Opportunity: Growing investment in low-emission fuels

Biofuels, hydrogen, and hydrogen-derived fuels are low-emission options essential for reducing carbon emissions in sectors with limited electrification, like heavy industry and long-distance transportation. These fuels constitute a small share of global final energy use. Hydrogen is a notably clean transportation fuel, emitting less carbon dioxide than other fossil fuels. Growth in hydrogen production has been driven by strict environmental regulations and rigorous engine manufacturer standards. For example, India adopted a Green Hydrogen Policy aiming to produce five million tons per year (MTPA) of green hydrogen by 2030. Similarly, China announced a long-term hydrogen development plan covering 2021–2035. According to this plan, China aims to produce 100,000 to 200,000 tons of renewable hydrogen annually by 2025 and expects to operate a fleet of 50,000 hydrogen-powered vehicles. The demand for cleaner fuels is expected to rise significantly in the future, fueled by a 10% growth in automotive sales in the Asia-Pacific region, increasing sales of premium cars, and shifting consumer fuel spending habits. The IEA reports that in 2023, global investment in clean energy surpassed USD 1.7 trillion, marking a major move toward sustainable energy systems. These investments include renewable power, nuclear energy, grid upgrades, energy storage, low-emission fuels, energy-efficiency upgrades, renewable end-use technologies, and electrification efforts. Such investments offer major opportunities for hydrogen as a fuel in the growing hydrogen market.

Challenge: High costs associated with renewable hydrogen production

Green hydrogen, produced using renewable energy sources such as wind, solar, or hydropower, or other low-carbon power, is increasingly recognized as a key element for achieving deep decarbonization across energy-intensive and hard-to-abate sectors. Industries like steel, cement, chemicals, heavy-duty transportation, shipping, and aviation can use green hydrogen to significantly cut carbon footprints and meet global net-zero targets. Besides lowering emissions, green hydrogen also provides strategic advantages such as improving energy security and aiding the integration of variable renewable energy into national grids. Despite its environmental benefits, the economic viability of green hydrogen remains a major obstacle. Its cost is roughly two to four times higher than that of grey hydrogen, which is made from fossil fuels without carbon capture. Several factors drive this gap, including the high capital costs of electrolyzer systems, limited and uneven access to affordable renewable electricity, and the underdeveloped infrastructure for hydrogen production, storage, and distribution. These economic and logistical challenges continue to slow the widespread adoption of green hydrogen and limit its role in the global energy transition.

Hydrogen Generation Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

SSAB, Sweden’s leading steelmaker, sought to decarbonize its operations by transitioning to hydrogen-based Direct Reduced Iron (DRI) technology. However, sourcing reliable, large-scale green hydrogen presented a significant challenge. To address this, SSAB partnered with Vattenfall and LKAB under the HYBRIT (Hydrogen Breakthrough Ironmaking Technology) initiative. The project deployed a 4.5 MW pilot electrolyzer powered by renewable electricity to produce fossil-free hydrogen for iron and steelmaking, demonstrating the feasibility of a sustainable production pathway. | The HYBRIT initiative proved that green hydrogen can replace coal in steelmaking, enabling fossil-free steel production. By integrating renewable electricity with electrolyzer technology, the project showcased a scalable solution for hydrogen generation at industrial levels. Upon full-scale commercialization, HYBRIT has the potential to reduce Sweden’s total CO2 emissions by nearly 10%, marking a major milestone in decarbonizing one of the most emission-intensive sectors. The project not only enhances hydrogen’s role as a clean industrial feedstock but also sets a blueprint for global steelmakers to adopt hydrogen-based pathways for sustainable operations. |

|

The National Renewable Energy Laboratory (NREL) and Electric Hydrogen have entered into a three-year, USD 3.6 million collaboration to advance the development of high-performance electrolyzer components. This partnership focuses on improving the durability and efficiency of electrolysis cells by identifying degradation mechanisms and validating next-generation designs capable of operating at higher stack currents. The collaboration leverages both organizations’ technical expertise in renewable energy innovation and builds upon their prior success—several team members from both sides were part of the long-term NREL–First Solar partnership that helped commercialize cadmium telluride (CdTe) solar photovoltaics. | This joint initiative is expected to accelerate the scalability and cost-effectiveness of clean hydrogen production, enabling broader deployment of renewable hydrogen across industries. By enhancing electrolyzer performance and lifespan, the project supports decarbonization of hard-to-abate sectors such as heavy industry, energy storage, and transportation. Additionally, the partnership strengthens the knowledge base in renewable hydrogen technologies, fostering innovation and driving progress toward a sustainable, low-carbon energy ecosystem |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The hydrogen generation market operates within a complex and interconnected ecosystem, facilitating the production, storage, and use of hydrogen in industrial and energy sectors. The supply chain starts with hydrogen technology providers, who supply the technologies needed to produce hydrogen. Notable providers include Linde PLC (Ireland), Nel ASA (Norway), and Cummins Inc. (US). EPC providers deliver engineering, procurement, and construction services for hydrogen plants, with some key companies being Technip Energies (France), Black & Veatch (US), and ANDRITZ (Austria). Hydrogen producers and suppliers acquire technology from these providers to generate hydrogen. Major component suppliers include Air Liquide (France), Air Products and Chemicals, Inc. (US), and ENGIE (France). Hydrogen is utilized in various end-use applications across mobility, industry, and power sectors. Some prominent end users are ElringKlinger AG (Germany), Doosan Fuel Cell Co., Ltd. (South Korea), and TotalEnergies (France).nce

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Hydrogen GenerationMarket, By Technology

The Steam Methane Reforming (SMR) accounted for the largest market revenue share in 2024. The SMR segment maintains its dominant share mainly due to its well-established infrastructure and cost-effective production, especially for grey hydrogen. In the short to medium term, the petroleum refining sector remains the top hydrogen consumer. In this industry, hydrogen is usually produced on-site via SMR, recovered as a by-product from petrochemical processes, or sourced externally as merchant hydrogen, depending on operational needs and cost considerations.

Hydrogen Generation Market, By Source

Green hydrogen is projected to have the highest CAGR in the hydrogen generation market. The global shift toward carbon neutrality and the urgent need to decarbonize hard-to-reach sectors fuel the demand for green hydrogen. Supportive policies, including tax incentives, subsidies, and national hydrogen strategies, help speed up project development and commercialization. Furthermore, the rising demand for zero-emission fuels in applications like fuel cell vehicles, power generation, and industrial feedstock makes green hydrogen a crucial part of the worldwide clean energy transition.

Hydrogen Generation Market, By Application

The transportation segment is expected to record the highest CAGR in the hydrogen generation market during the forecast period. This growth is primarily fueled by the rising adoption of hydrogen fuel cell technologies across various mobility segments, including passenger vehicles, buses, trucks, trains, marine vessels, and even aviation. Hydrogen fuel cells offer unique advantages such as high energy density, quick refueling times, and longer operational ranges compared to battery electric vehicles, making them particularly attractive for heavy-duty and long-distance applications where minimizing downtime is critical. Stringent global emission regulations, combined with ambitious climate targets set by governments and international organizations, are accelerating the transition toward zero-emission transportation solutions. National hydrogen roadmaps and supportive policy frameworks are encouraging large-scale investments in hydrogen infrastructure, including refueling networks and production facilities. These initiatives also provide financial incentives and subsidies to adopt hydrogen-powered solutions.

Hydrogen Generation Market, By Generation & Delivery Mode

The captive hydrogen generation segment hold the largest share in the generation & delivery mode in the hydrogen generation market due to its ability to provide a secure, continuous, and cost-effective hydrogen supply directly on-site. Unlike the merchant segment, which relies on external supply chains and incurs additional transportation and storage costs, captive generation ensures uninterrupted availability tailored to specific operational needs. This mode is extensively adopted in critical sectors, such as oil refining, food production, metals treatment, and fertilizer manufacturing, where reliability and process integration are crucial.

REGION

Asia Pacific is expected to witness the highest CAGR in global hydrogen generation market during forecast period

Asia Pacific is expected to see the highest CAGR in the hydrogen generation market during the forecast period, driven by rapid industrial growth, urbanization, and strong efforts to decarbonize energy systems. Countries like China, Japan, South Korea, and India are making significant investments in hydrogen production infrastructure to support cleaner industrial processes and reduce reliance on fossil fuels. Supportive government policies, national hydrogen strategies, and substantial funding for renewable and low-carbon hydrogen projects are boosting market growth. Additionally, increasing demand from the refining, chemical, and mobility sectors further solidifies the region’s leadership.

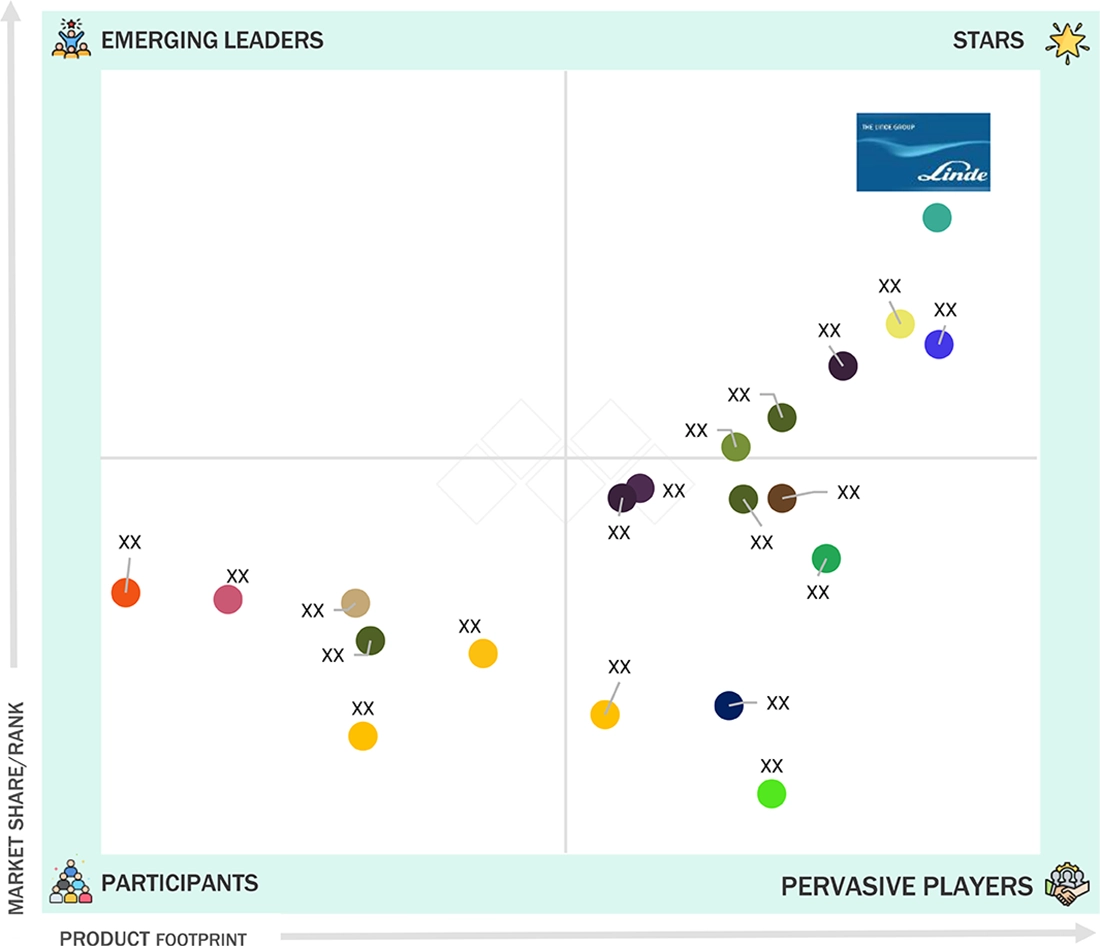

Hydrogen Generation Market: COMPANY EVALUATION MATRIX

Linde PLC (Star) leads the hydrogen generation market with significant investments in large-scale green and blue hydrogen projects, supported by its global infrastructure and extensive expertise in industrial gases. The company utilizes advanced electrolyzer technology, carbon capture solutions, and broad distribution networks to promote the adoption of clean hydrogen across mobility, refining, and heavy industry sectors. Its diversified portfolio and focus on decarbonization establish it as the leading player driving market growth, providing reliable hydrogen supply at scale and solidifying its leadership in the global energy transition.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2024 (Value) | USD 146.24 Billion |

| Market Forecast in 2030 (value) | USD 226.37 Billion |

| Growth Rate | CAGR of 7.5% from 2025-2030 |

| Years Considered | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2030 |

| Units Considered | Value (USD Million/Billion)/Volume (Thousand metric tons) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regions Covered | North America, Europe, Asia Pacific, Middle East & Africa, and South America |

WHAT IS IN IT FOR YOU: Hydrogen Generation Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Green Hydrogen Providers in the Europe Market | Detailed company profiles 10 green hydrogen generation & storage players in the Europe market | Identified and profiled 10-15 hydrogen generation & storage players in European market; Provided recent developments, financials, product portfolios, and business overviews |

RECENT DEVELOPMENTS

- June 2025 : Centrica entered an agreement with Equinor for a USD 25.6 billion natural gas supply deal spanning 10 years, from 2025 to 2035. Under this agreement, Equinor will deliver around 5 billion cubic metres of natural gas annually to the UK, enough to meet the heating needs of approximately 5 million homes or about 8–10% of the country’s total demand.

- May 2025 : Uniper SE entered a strategic partnership with thyssenkrupp Uhde to develop a cutting-edge ammonia cracker, designed to convert imported ammonia into hydrogen and nitrogen at its Gelsenkirchen-Scholven site. This cooperation will see the construction of one of the world’s first demonstration plants (processing around 28?t/day of ammonia) and serves as a critical first step toward a planned large-scale hydrogen import terminal in Wilhelmshaven.

- March 2025 : JERA Co., Inc. formed a collaboration with Exxon Mobil Corporation, to jointly explore the development of a large-scale low-carbon hydrogen and ammonia production facility at ExxonMobil’s Baytown Complex near Houston, Texas. Under this agreement, JERA Co., Inc. may take ownership of the project and intends to secure approximately 500,000?tonnes per year of low-carbon ammonia for supply to Japan.

- December 2024 : Saudi Arabian Oil Co. entered into a shareholders’ agreement with Linde plc and SLB to develop one of the world’s largest carbon capture and storage (CCS) hubs in Jubail, Saudi Arabia. In this deal, Aramco will hold a 60% stake, while Linde and SLB will each hold 20%. The project aims to capture and store up to 9 million tonnes of CO2 annually by 2027 through a network of pipelines and underground storage in a saline aquifer. This CCS hub is also designed to support Aramco’s blue hydrogen and ammonia programs by providing the carbon capture infrastructure needed to produce low-carbon fuels.

- November 2024 : ENGIE entered a strategic partnership with Morocco’s OCP Group to accelerate the production of green hydrogen and ammonia, alongside renewable energy, storage, electrical infrastructure, desalination, and R&D efforts. The deal commits parties to co-develop large-scale projects—feasibility studies for e-methanol and sustainable aviation fuel—supporting Morocco’s industrial decarbonization ambitions and clean energy transition.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

31

2

RESEARCH METHODOLOGY

37

3

EXECUTIVE SUMMARY

49

4

PREMIUM INSIGHTS

54

5

MARKET OVERVIEW

Seize hydrogen market growth through low-carbon fuel demand and government-backed initiatives.

58

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

Enforcement of stringent regulations to curb greenhouse gas emissions

5.2.1.2

Government initiatives for developing hydrogen economy

5.2.1.3

Growing demand for ammonia in agriculture sector

5.2.2

RESTRAINTS

5.2.2.1

Energy loss during hydrogen production

5.2.2.2

Limited hydrogen infrastructure

5.2.3

OPPORTUNITIES

5.2.3.1

Rising emphasis on achieving net-zero carbon emission targets

5.2.3.2

Increasing investment in low-emission fuels

5.2.3.3

Growing demand for low-carbon transportation fuels

5.2.4

CHALLENGES

5.2.4.1

High costs associated with renewable hydrogen production

5.3

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4

PRICING ANALYSIS

5.4.1

PRICING RANGE OF HYDROGEN, BY TECHNOLOGY, 2024

5.4.2

PRICING RANGE OF HYDROGEN, BY SOURCE, 2024

5.5

SUPPLY CHAIN ANALYSIS

5.6

ECOSYSTEM ANALYSIS

5.7

TRADE ANALYSIS

5.7.1

IMPORT SCENARIO (HS CODE 280410)

5.7.2

EXPORT SCENARIO (HS CODE 280410)

5.8

TECHNOLOGY ANALYSIS

5.8.1

KEY TECHNOLOGIES

5.8.1.1

Steam methane reforming (SMR)

5.8.1.2

Partial oxidation

5.8.1.3

Coal gasification

5.8.1.4

Electrolysis

5.8.2

COMPLEMENTARY TECHNOLOGIES

5.8.2.1

Carbon capture, utilization, and storage (CCUS)

5.9

CASE STUDY ANALYSIS

5.9.1

HYBRIT INITIATIVE HELPS TRANSFORM STEEL PRODUCTION WITH FOSSIL-FREE GREEN HYDROGEN IN SWEDEN

5.9.2

NATIONAL RENEWABLE ENERGY LABORATORY AND ELECTRIC HYDROGEN PARTNER TO DEVELOP HIGH-PERFORMANCE ELECTROLYZER COMPONENTS

5.9.3

RWE TESTS SUNFIRE’S ELECTROLYSIS TECHNOLOGIES TO GENERATE GREEN HYDROGEN

5.10

KEY CONFERENCES AND EVENTS, 2025–2026

5.11

PATENT ANALYSIS

5.12

REGULATORY LANDSCAPE

5.12.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.12.2

REGULATORY FRAMEWORKS/POLICIES

5.13

PORTER’S FIVE FORCES ANALYSIS

5.13.1

THREAT OF NEW ENTRANTS

5.13.2

BARGAINING POWER OF SUPPLIERS

5.13.3

BARGAINING POWER OF BUYERS

5.13.4

THREAT OF SUBSTITUTES

5.13.5

INTENSITY OF COMPETITIVE RIVALRY

5.14

KEY STAKEHOLDERS AND BUYING CRITERIA

5.14.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.14.2

BUYING CRITERIA

5.15

IMPACT OF AI/GEN AI ON HYDROGEN GENERATION MARKET

5.16

IMPACT OF 2025 US TARIFF ON HYDROGEN GENERATION MARKET

5.16.1

INTRODUCTION

5.16.2

KEY TARIFF RATES

5.16.3

PRICE IMPACT ANALYSIS

5.16.4

IMPACT ON COUNTRIES/REGIONS

5.16.4.1

US

5.16.4.2

Europe

5.16.4.3

Asia Pacific

5.16.5

IMPACT ON APPLICATIONS

6

HYDROGEN GENERATION MARKET, BY TECHNOLOGY

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Tons | 6 Data Tables

96

6.1

INTRODUCTION

6.2

STEAM METHANE REFORMING (SMR)

6.2.1

EMERGENCE AS COST-EFFECTIVE METHOD OF HYDROGEN PRODUCTION TO FOSTER SEGMENTAL GROWTH

6.3

PARTIAL OXIDATION (POX)

6.3.1

USE IN AUTOMOBILE FUEL CELLS AND OTHER COMMERCIAL APPLICATIONS TO BOOST SEGMENTAL GROWTH

6.4

AUTO THERMAL REFORMING (ATR)

6.4.1

STRONG FOCUS ON PRODUCING ADVANCED BIOFUELS TO CONTRIBUTE TO SEGMENTAL GROWTH

6.5

COAL GASIFICATION

6.5.1

NEED TO REDUCE RELIANCE ON IMPORTED NATURAL GAS TO FUEL SEGMENTAL GROWTH

6.6

ELECTROLYSIS

6.6.1

EMPHASIS ON INCREASING ENERGY EFFICIENCY OF HYDROGEN GENERATION PROCESS TO AUGMENT SEGMENTAL GROWTH

6.6.2

ALKALINE ELECTROLYSIS

6.6.3

PROTON-EXCHANGE MEMBRANE ELECTROLYSIS

6.6.4

SOLID OXIDE ELECTROLYSIS

6.6.5

ANION-EXCHANGE MEMBRANE ELECTROLYSIS

7

HYDROGEN GENERATION MARKET, BY SOURCE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Tons | 16 Data Tables

107

7.1

INTRODUCTION

7.2

BLUE HYDROGEN

7.2.1

LOW CARBON DIOXIDE PRODUCTION BENEFITS TO CONTRIBUTE TO SEGMENTAL GROWTH

7.3

GRAY HYDROGEN

7.3.1

IMPOSITION OF STRICT CARBON CAPS ON INDUSTRIES TO ACCELERATE SEGMENTAL GROWTH

7.4

GREEN HYDROGEN

7.4.1

DEPLOYMENT OF RENEWABLE POWER GENERATION TECHNOLOGIES TO DRIVE MARKET

8

HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Tons | 22 Data Tables

116

8.1

INTRODUCTION

8.2

CAPTIVE

8.2.1

NEED TO REDUCE DEPENDENCE ON EXTERNAL HYDROGEN SUPPLY CHAINS TO ACCELERATE SEGMENTAL GROWTH

8.3

MERCHANT

8.3.1

BY DELIVERY MODE

8.3.1.1

Liquid on-site plant & pipeline

8.3.1.2

Bulk & cylinder (gaseous form)

8.3.1.3

Bulk (liquid form)

8.3.1.4

Small on-site

8.3.2

BY STATE

8.3.2.1

Gas

8.3.2.2

Liquid

9

HYDROGEN GENERATION MARKET, BY APPLICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Tons | 28 Data Tables

130

9.1

INTRODUCTION

9.2

PETROLEUM REFINERY

9.2.1

INCREASING USE OF HYDROGEN TO REDUCE SULFUR CONTENT IN DIESEL FUEL TO BOOST SEGMENTAL GROWTH

9.3

AMMONIA PRODUCTION

9.3.1

RISING NEED FOR AMMONIA IN NITROGEN-BASED FERTILISERS TO FUEL SEGMENTAL GROWTH

9.4

METHANOL PRODUCTION

9.4.1

SURGING DEMAND FOR TRANSPORTATION FUEL AND ELECTRICITY TO AUGMENT SEGMENTAL GROWTH

9.5

TRANSPORTATION

9.5.1

GROWING CONSUMPTION OF FUEL-CELL ELECTRIC VEHICLES TO SUPPORT MARKET GROWTH

9.6

POWER GENERATION

9.6.1

INCREASING RELIANCE ON BACKUP POWER SOURCES TO CONTRIBUTE TO SEGMENTAL GROWTH

9.7

OTHER APPLICATIONS

10

HYDROGEN GENERATION MARKET, BY REGION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Tons | 195 Data Tables

146

10.1

INTRODUCTION

10.2

NORTH AMERICA

10.2.1

US

10.2.1.1

Increasing hydrogen use in petroleum refinery and chemical manufacturing to drive market

10.2.2

CANADA

10.2.2.1

Rising development of low-carbon hydrogen to support decarbonization strategies to fuel market growth

10.2.3

MEXICO

10.2.3.1

Increasing ammonia and green hydrogen Initiatives to accelerate market growth

10.3

ASIA PACIFIC

10.3.1

JAPAN

10.3.1.1

Strong ambitious targets and heavy infrastructure investment to accelerate market growth

10.3.2

CHINA

10.3.2.1

Increasing ammonia production to modernize agriculture to drive market

10.3.3

INDIA

10.3.3.1

Shifting focus toward renewable hydrogen to contribute to market growth

10.3.4

AUSTRALIA

10.3.4.1

Strong presence of renewable energy resources to bolster market growth

10.3.5

SOUTH KOREA

10.3.5.1

Ambitious carbon neutrality goals to contribute to market growth

10.3.6

REST OF ASIA PACIFIC

10.4

EUROPE

10.4.1

GERMANY

10.4.1.1

Strong focus on producing low-carbon green hydrogen to boost market growth

10.4.2

UK

10.4.2.1

Growing focus on supporting conventional hydrogen production to augment market growth

10.4.3

FRANCE

10.4.3.1

Rapid transition to low-carbon alternatives in industries to fuel market growth

10.4.4

RUSSIA

10.4.4.1

Increasing oil export and natural gas production to contribute to market growth

10.4.5

REST OF EUROPE

10.5

SOUTH AMERICA

10.5.1

BRAZIL

10.5.1.1

Increasing electricity generation using renewable energy to foster market growth

10.5.2

ARGENTINA

10.5.2.1

Rapid transition to low-carbon energy sources for industrial decarbonization to augment market growth

10.5.3

REST OF SOUTH AMERICA

10.6

MIDDLE EAST

10.6.1

GCC

10.6.1.1

Saudi Arabia

10.6.1.2

Qatar

10.6.1.3

UAE

10.6.2

IRAN

10.6.2.1

High demand for refined petroleum products to contribute to market growth

10.6.3

REST OF MIDDLE EAST

10.7

AFRICA

10.7.1

SOUTH AFRICA

10.7.1.1

Growing investment in hydrogen and green ammonia for energy transition to boost market growth

10.7.2

REST OF AFRICA

11

COMPETITIVE LANDSCAPE

Discover strategic moves and market dominance of key players shaping the competitive landscape.

233

11.1

OVERVIEW

11.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020–2025

11.3

MARKET SHARE ANALYSIS, 2024

11.4

REVENUE ANALYSIS, 2020–2024

11.5

COMPANY VALUATION AND FINANCIAL METRICS

11.6

PRODUCT COMPARISON

11.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

11.7.1

STARS

11.7.2

EMERGING LEADERS

11.7.3

PERVASIVE PLAYERS

11.7.4

PARTICIPANTS

11.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.7.5.1

Company footprint

11.7.5.2

Region footprint

11.7.5.3

Source footprint

11.7.5.4

Application footprint

11.7.5.5

Technology footprint

11.8

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

11.8.1

PROGRESSIVE COMPANIES

11.8.2

RESPONSIVE COMPANIES

11.8.3

DYNAMIC COMPANIES

11.8.4

STARTING BLOCKS

11.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

11.8.5.1

Detailed list of key startups/SMEs

11.8.5.2

Competitive benchmarking of key startups/SMEs

11.9

COMPETITIVE SCENARIO

11.9.1

PRODUCT LAUNCHES

11.9.2

DEALS

11.9.3

EXPANSIONS

11.9.4

OTHER DEVELOPMENTS

12

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

256

12.1

KEY PLAYERS

12.1.1

LINDE PLC

12.1.1.1

Business overview

12.1.1.2

Products/Solutions/Services offered

12.1.1.3

Recent developments

12.1.1.4

MnM view

12.1.2

AIR LIQUIDE

12.1.3

SAUDI ARABIAN OIL CO.

12.1.4

AIR PRODUCTS AND CHEMICALS, INC.

12.1.5

SHELL PLC

12.1.6

ENGIE

12.1.7

CHEVRON CORPORATION

12.1.8

ØRSTED A/S

12.1.9

MESSER SE & CO. KGAA

12.1.10

EQUINOR ASA

12.1.11

UNIPER SE

12.1.12

EXXON MOBIL CORPORATION

12.1.13

BP P.L.C.

12.1.14

IWATANI CORPORATION

12.1.15

PETROLIAM NASIONAL BERHAD (PETRONAS)

12.1.16

IBERDROLA, S.A.

12.2

OTHER PLAYERS

12.2.1

PLUG POWER INC.

12.2.2

REPSOL

12.2.3

AKER ASA

12.2.4

RELIANCE INDUSTRIES LIMITED

12.2.5

MATHESON TRI-GAS, INC.

12.2.6

LHYFE

12.2.7

HIRINGA ENERGY LTD

12.2.8

BAYOTECH

12.2.9

HYGEAR

13

APPENDIX

329

13.1

INSIGHTS OF INDUSTRY EXPERTS

13.2

DISCUSSION GUIDE

13.3

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

13.4

CUSTOMIZATION OPTIONS

13.5

RELATED REPORTS

13.6

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

INCLUSIONS AND EXCLUSIONS

TABLE 2

LIST OF KEY SECONDARY SOURCES

TABLE 3

LIST OF PRIMARY INTERVIEW PARTICIPANTS

TABLE 4

KEY DATA FROM PRIMARY SOURCES

TABLE 5

HYDROGEN GENERATION MARKET: RISKS ANALYSIS

TABLE 6

HYDROGEN GENERATION MARKET SNAPSHOT

TABLE 7

PRICING RANGE OF HYDROGEN, BY TECHNOLOGY, 2024 (USD/TON)

TABLE 8

PRICING RANGE OF HYDROGEN, BY SOURCE, 2024 (USD/KG)

TABLE 9

ROLE OF COMPANIES IN HYDROGEN GENERATION ECOSYSTEM

TABLE 10

IMPORT DATA FOR HS CODE 280410-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2022 (USD THOUSAND)

TABLE 11

EXPORT DATA FOR HS CODE 280410, BY COUNTRY, 2022–2024 (USD THOUSAND)

TABLE 12

LIST OF CONFERENCES AND EVENTS, 2025–2026

TABLE 13

LIST OF MAJOR PATENTS, 2019–2024

TABLE 14

NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 15

EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 16

ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 17

MIDDLE EAST: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 18

AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 19

SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 20

IMPACT OF PORTER’S FIVE FORCES ANALYSIS

TABLE 21

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS(%)

TABLE 22

KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

TABLE 23

US-ADJUSTED RECIPROCAL TARIFF RATES

TABLE 24

EXPECTED CHANGE IN PRICES AND LIKELY IMPACT ON END-USE MARKETS DUE TO TARIFF IMPACT

TABLE 25

HYDROGEN GENERATION MARKET, BY TECHNOLOGY, 2020–2024 (THOUSAND METRIC TONS)

TABLE 26

HYDROGEN GENERATION MARKET, BY TECHNOLOGY, 2025–2030 (THOUSAND METRIC TONS)

TABLE 27

HYDROGEN GENERATION MARKET, BY TECHNOLOGY, 2020–2024 (USD MILLION)

TABLE 28

HYDROGEN GENERATION MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 29

HYDROGEN GENERATION TECHNOLOGY COMPARISON

TABLE 30

ELECTROLYSIS TECHNOLOGY COMPARISON

TABLE 31

HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 32

HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 33

HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (USD MILLION)

TABLE 34

HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (USD MILLION)

TABLE 35

BLUE HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 36

BLUE HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 37

BLUE HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 38

BLUE HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 39

GRAY HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 40

GRAY HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 41

GRAY HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 42

GRAY HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 43

GREEN HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 44

GREEN HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 45

GREEN HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 46

GREEN HYDROGEN: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 47

HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 48

HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 49

HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (USD MILLION)

TABLE 50

HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (USD MILLION)

TABLE 51

CAPTIVE: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 52

CAPTIVE: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 53

CAPTIVE: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 54

CAPTIVE: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 55

MERCHANT: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 56

MERCHANT: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 57

MERCHANT: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 58

MERCHANT: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 59

MERCHANT: HYDROGEN GENERATION MARKET, BY DELIVERY MODE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 60

MERCHANT: HYDROGEN GENERATION MARKET, BY DELIVERY MODE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 61

MERCHANT: HYDROGEN GENERATION MARKET, BY DELIVERY MODE, 2020–2024 (USD MILLION)

TABLE 62

MERCHANT: HYDROGEN GENERATION MARKET, BY DELIVERY MODE, 2025–2030 (USD MILLION)

TABLE 63

MERCHANT: HYDROGEN GENERATION MARKET, BY STATE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 64

MERCHANT: HYDROGEN GENERATION MARKET, BY STATE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 65

MERCHANT: HYDROGEN GENERATION MARKET FOR GAS, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 66

MERCHANT: HYDROGEN GENERATION MARKET FOR GAS, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 67

MERSCHANT: HYDROGEN GENERATION MARKET FOR LIQUID, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 68

MERCHANT: HYDROGEN GENERATION MARKET FOR LIQUID, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 69

HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 70

HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 71

HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 72

HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 73

PETROLEUM REFINERY: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 74

PETROLEUM REFINERY: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 75

PETROLEUM REFINERY: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 76

PETROLEUM REFINERY: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 77

AMMONIA PRODUCTION: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 78

AMMONIA PRODUCTION: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 79

AMMONIA PRODUCTION: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 80

AMMONIA PRODUCTION: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 81

METHANOL PRODUCTION: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 82

METHANOL PRODUCTION: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 83

METHANOL PRODUCTION: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 84

METHANOL PRODUCTION: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 85

TRANSPORTATION: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 86

TRANSPORTATION: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 87

TRANSPORTATION: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 88

TRANSPORTATION: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 89

POWER GENERATION: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 90

POWER GENERATION: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 91

POWER GENERATION: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 92

POWER GENERATION: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 93

OTHER APPLICATIONS: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 94

OTHER APPLICATIONS: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 95

OTHER APPLICATIONS: HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 96

OTHER APPLICATIONS: HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 97

HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 98

HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 99

HYDROGEN GENERATION MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 100

HYDROGEN GENERATION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 101

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 102

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 103

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (USD MILLION)

TABLE 104

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (USD MILLION)

TABLE 105

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 106

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 107

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (USD MILLION)

TABLE 108

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (USD MILLION)

TABLE 109

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 110

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 111

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 112

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 113

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (THOUSAND METRIC TONS)

TABLE 114

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (THOUSAND METRIC TONS)

TABLE 115

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 116

NORTH AMERICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 117

US: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 118

US: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 119

US: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 120

US: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 121

CANADA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 122

CANADA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 123

CANADA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 124

CANADA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 125

MEXICO: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 126

MEXICO: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 127

MEXICO: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 128

MEXICO: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 129

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 130

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 131

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (USD MILLION)

TABLE 132

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (USD MILLION)

TABLE 133

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 134

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 135

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (USD MILLION)

TABLE 136

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (USD MILLION)

TABLE 137

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 138

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 139

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 140

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY APPLICATION,2025–2030 (USD MILLION)

TABLE 141

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (THOUSAND METRIC TONS)

TABLE 142

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (THOUSAND METRIC TONS)

TABLE 143

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 144

ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 145

JAPAN: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 146

JAPAN: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 147

JAPAN: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 148

JAPAN: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 149

CHINA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 150

CHINA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 151

CHINA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 152

CHINA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 153

INDIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 154

INDIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 155

INDIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 156

INDIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 157

AUSTRALIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 158

AUSTRALIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 159

AUSTRALIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 160

AUSTRALIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 161

SOUTH KOREA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 162

SOUTH KOREA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 163

SOUTH KOREA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 164

SOUTH KOREA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 165

REST OF ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 166

REST OF ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 167

REST OF ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 168

REST OF ASIA PACIFIC: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 169

EUROPE: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 170

EUROPE: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 171

EUROPE: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (USD MILLION)

TABLE 172

EUROPE: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (USD MILLION)

TABLE 173

EUROPE: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 174

EUROPE: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 175

EUROPE: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (USD MILLION)

TABLE 176

EUROPE: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (USD MILLION)

TABLE 177

EUROPE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 178

EUROPE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 179

EUROPE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 180

EUROPE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 181

EUROPE: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (THOUSAND METRIC TONS)

TABLE 182

EUROPE: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (THOUSAND METRIC TONS)

TABLE 183

EUROPE: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 184

EUROPE: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 185

GERMANY: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 186

GERMANY: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 187

GERMANY: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 188

GERMANY: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 189

UK: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 190

UK: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 191

UK: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 192

UK: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 193

FRANCE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 194

FRANCE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 195

FRANCE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 196

FRANCE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 197

RUSSIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 198

RUSSIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 199

RUSSIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 200

RUSSIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 201

REST OF EUROPE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 202

REST OF EUROPE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 203

REST OF EUROPE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 204

REST OF EUROPE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 205

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 206

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 207

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (USD MILLION)

TABLE 208

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (USD MILLION)

TABLE 209

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 210

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 211

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (USD MILLION)

TABLE 212

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (USD MILLION)

TABLE 213

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 214

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 215

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 216

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 217

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (THOUSAND METRIC TONS)

TABLE 218

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (THOUSAND METRIC TONS)

TABLE 219

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 220

SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 221

BRAZIL: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 222

BRAZIL: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 223

BRAZIL: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 224

BRAZIL: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 225

ARGENTINA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 226

ARGENTINA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 227

ARGENTINA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 228

ARGENTINA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 229

REST OF SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 230

REST OF SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 231

REST OF SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 232

REST OF SOUTH AMERICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 233

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 234

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 235

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (USD MILLION)

TABLE 236

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (USD MILLION)

TABLE 237

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 238

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 239

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (USD MILLION)

TABLE 240

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (USD MILLION)

TABLE 241

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 242

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 243

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 244

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 245

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (THOUSAND METRIC TONS)

TABLE 246

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (THOUSAND METRIC TONS)

TABLE 247

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 248

MIDDLE EAST: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 249

SAUDI ARABIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 250

SAUDI ARABIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 251

SAUDI ARABIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 252

SAUDI ARABIA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 253

QATAR: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 254

QATAR: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 255

QATAR: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 256

QATAR: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 257

UAE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 258

UAE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 259

UAE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 260

UAE: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 261

IRAN: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 262

IRAN: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 263

IRAN: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 264

IRAN: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 265

REST OF MIDDLE EAST: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 266

REST OF MIDDLE EAST: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 267

REST OF MIDDLE EAST: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 268

REST OF MIDDLE EAST: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 269

AFRICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 270

AFRICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2020–2024 (USD MILLION)

TABLE 271

AFRICA: HYDROGEN GENERATION MARKET, BY SOURCE, 2025–2030 (USD MILLION)

TABLE 272

AFRICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (THOUSAND METRIC TONS)

TABLE 273

AFRICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (THOUSAND METRIC TONS)

TABLE 274

AFRICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2020–2024 (USD MILLION)

TABLE 275

AFRICA: HYDROGEN GENERATION MARKET, BY GENERATION & DELIVERY MODE, 2025–2030 (USD MILLION)

TABLE 276

AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 277

AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 278

AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 279

AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 280

AFRICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (THOUSAND METRIC TONS)

TABLE 281

AFRICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (THOUSAND METRIC TONS)

TABLE 282

AFRICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 283

AFRICA: HYDROGEN GENERATION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 284

SOUTH AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 285

SOUTH AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 286

SOUTH AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 287

SOUTH AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 288

REST OF AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (THOUSAND METRIC TONS)

TABLE 289

REST OF AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (THOUSAND METRIC TONS)

TABLE 290

REST OF AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 291

REST OF AFRICA: HYDROGEN GENERATION MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 292

HYDROGEN GENERATION MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2020–JULY 2025

TABLE 293

HYDROGEN GENERATION MARKET: DEGREE OF COMPETITION, 2024

TABLE 294

HYDROGEN GENERATION MARKET: REGION FOOTPRINT

TABLE 295

HYDROGEN GENERATION MARKET: SOURCE FOOTPRINT

TABLE 296

HYDROGEN GENERATION MARKET: APPLICATION FOOTPRINT

TABLE 297

HYDROGEN GENERATION MARKET: TECHNOLOGY FOOTPRINT

TABLE 298

HYDROGEN GENERATION MARKET: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 299

HYDROGEN GENERATION MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 300

HYDROGEN GENERATION MARKET: PRODUCT LAUNCHES, JANUARY 2020–JULY 2025

TABLE 301

HYDROGEN GENERATION MARKET: DEALS, JANUARY 2020–JULY 2025

TABLE 302

HYDROGEN GENERATION MARKET: EXPANSIONS, JANUARY 2020–JULY 2025

TABLE 303

HYDROGEN GENERATION MARKET: OTHER DEVELOPMENTS, JANUARY 2020–JULY 2025

TABLE 304

LINDE PLC: COMPANY OVERVIEW

TABLE 305

LINDE PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 306

LINDE PLC: DEALS

TABLE 307

LINDE PLC: EXPANSIONS

TABLE 308

AIR LIQUIDE: COMPANY OVERVIEW

TABLE 309

AIR LIQUIDE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 310

AIR LIQUIDE: DEALS

TABLE 311

AIR LIQUIDE: EXPANSIONS

TABLE 312

AIR LIQUIDE: OTHER DEVELOPMENTS

TABLE 313

SAUDI ARABIAN OIL CO.: COMPANY OVERVIEW

TABLE 314

SAUDI ARABIAN OIL CO.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 315

SAUDI ARABIAN OIL CO.: DEALS

TABLE 316

SAUDI ARABIAN OIL CO.: EXPANSIONS

TABLE 317

AIR PRODUCTS AND CHEMICALS, INC.: COMPANY OVERVIEW

TABLE 318

AIR PRODUCTS AND CHEMICALS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 319

AIR PRODUCTS AND CHEMICALS, INC.: DEALS

TABLE 320

AIR PRODUCTS AND CHEMICALS, INC.: OTHER DEVELOPMENTS

TABLE 321

SHELL PLC: COMPANY OVERVIEW

TABLE 322

SHELL PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 323

SHELL PLC: DEALS

TABLE 324

SHELL PLC: EXPANSIONS

TABLE 325

SHELL PLC: OTHER DEVELOPMENTS

TABLE 326

ENGIE: COMPANY OVERVIEW

TABLE 327

ENGIE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 328

ENGIE: DEALS

TABLE 329

CHEVRON CORPORATION: COMPANY OVERVIEW

TABLE 330

CHEVRON CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 331

CHEVRON CORPORATION: DEALS

TABLE 332

ØRSTED A/S: COMPANY OVERVIEW

TABLE 333

ØRSTED A/S: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 334

ØRSTED A/S: DEALS

TABLE 335

ØRSTED A/S: EXPANSIONS

TABLE 336

MESSER SE & CO. KGAA: COMPANY OVERVIEW

TABLE 337

MESSER SE & CO. KGAA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 338

MESSER SE & CO. KGAA: DEALS

TABLE 339

EQUINOR ASA: COMPANY OVERVIEW

TABLE 340

EQUINOR ASA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 341

EQUINOR ASA: PRODUCT LAUNCHES

TABLE 342

EQUINOR ASA: DEALS

TABLE 343

UNIPER SE: COMPANY OVERVIEW

TABLE 344

UNIPER SE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 345

UNIPER SE: DEALS

TABLE 346

UNIPER SE: OTHER DEVELOPMENTS

TABLE 347

EXXON MOBIL CORPORATION: COMPANY OVERVIEW

TABLE 348

EXXON MOBIL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 349

EXXON MOBIL CORPORATION: DEALS

TABLE 350

BP P.L.C.: COMPANY OVERVIEW

TABLE 351

BP P.L.C.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 352

BP P.L.C.: DEALS

TABLE 353

BP P.L.C.: OTHERS DEVELOPMENTS

TABLE 354

IWATANI CORPORATION: COMPANY OVERVIEW

TABLE 355

IWATANI CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 356

IWATANI CORPORATION: DEALS

TABLE 357

IWATANI CORPORATION: EXPANSIONS

TABLE 358

PETROLIAM NASIONAL BERHAD (PETRONAS): COMPANY OVERVIEW

TABLE 359

PETROLIAM NASIONAL BERHAD (PETRONAS): PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 360

PETROLIAM NASIONAL BERHAD (PETRONAS): DEALS

TABLE 361

PETROLIAM NASIONAL BERHAD (PETRONAS): OTHER DEVELOPMENTS

TABLE 362

IBERDROLA, S.A.: COMPANY OVERVIEW

TABLE 363

IBERDROLA, S.A.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 364

IBERDROLA, S.A.: DEALS

TABLE 365

IBERDROLA, S.A.: OTHER DEVELOPMENTS

TABLE 366

PLUG POWER INC.: COMPANY OVERVIEW

TABLE 367

REPSOL: COMPANY OVERVIEW

TABLE 368

AKER ASA: COMPANY OVERVIEW

TABLE 369

RELIANCE INDUSTRIES LIMITED: COMPANY OVERVIEW

TABLE 370

MATHESON TRI-GAS, INC.: COMPANY OVERVIEW

TABLE 371

LHYFE: COMPANY OVERVIEW

TABLE 372

HIRINGA ENERGY LTD: COMPANY OVERVIEW

TABLE 373

BAYOTECH: COMPANY OVERVIEW

TABLE 374

HYGEAR: COMPANY OVERVIEW

LIST OF FIGURES

FIGURE 1

HYDROGEN GENERATION MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

HYDROGEN GENERATION MARKET: RESEARCH DESIGN

FIGURE 3

KEY DATA FROM SECONDARY SOURCES

FIGURE 4

KEY INDUSTRY INSIGHTS

FIGURE 5

BREAKDOWN OF PRIMARIES

FIGURE 6

HYDROGEN GENERATION MARKET: BOTTOM-UP APPROACH

FIGURE 7

HYDROGEN GENERATION MARKET: TOP-DOWN APPROACH

FIGURE 8

HYDROGEN GENERATION MARKET: DEMAND-SIDE ANALYSIS

FIGURE 9

KEY METRICS CONSIDERED TO ANALYZE DEMAND FOR HYDROGEN GENERATION SOLUTIONS

FIGURE 10

KEY METRICS CONSIDERED TO ANALYZE SUPPLY OF HYDROGEN GENERATION SOLUTIONS

FIGURE 11

HYDROGEN GENERATION MARKET: SUPPLY-SIDE ANALYSIS

FIGURE 12

HYDROGEN GENERATION MARKET: DATA TRIANGULATION

FIGURE 13

HYDROGEN GENERATION MARKET: RESEARCH LIMITATIONS

FIGURE 14

ASIA PACIFIC HELD LARGEST SHARE OF HYDROGEN GENERATION MARKET IN 2024

FIGURE 15

PETROLEUM REFINERY SEGMENT TO DOMINATE HYDROGEN GENERATION MARKET DURING FORECAST PERIOD

FIGURE 16

GRAY HYDROGEN SEGMENT TO ACCOUNT FOR LARGEST SHARE OF HYDROGEN GENERATION MARKET IN 2030

FIGURE 17

STEAM METHANE REFORMING (SMR) SEGMENT TO HOLD LARGEST SHARE OF HYDROGEN GENERATION MARKET IN 2030

FIGURE 18

MERCHANT SEGMENT TO EXHIBIT HIGHER CAGR BETWEEN 2025 AND 2030

FIGURE 19

RISING FOCUS ON CURBING GREENHOUSE GAS EMISSIONS FROM HYDROGEN PRODUCTION PROCESSES TO CONTRIBUTE TO MARKET GROWTH

FIGURE 20

ASIA PACIFIC HYDROGEN GENERATION MARKET TO RECORD HIGHEST CAGR FROM 2025 TO 2030

FIGURE 21

CAPTIVE SEGMENT AND CHINA HELD LARGEST SHARES OF ASIA PACIFIC HYDROGEN GENERATION MARKET IN 2024

FIGURE 22

STEAM METHANE REFORMING (SMR) SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2030

FIGURE 23

GRAY HYDROGEN SEGMENT HELD LARGEST SHARE OF HYDROGEN GENERATION MARKET IN 2030

FIGURE 24

CAPTIVE SEGMENT CAPTURED LARGEST SHARE OF HYDROGEN GENERATION MARKET IN 2030

FIGURE 25

PETROLEUM REFINERY SEGMENT HELD LARGEST MARKET SHARE IN 2030

FIGURE 26

MARKET DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 27

GLOBAL GREENHOUSE GAS EMISSIONS, BY SECTOR, 2023

FIGURE 28

AMMONIA DEMAND STRUCTURE, 2024

FIGURE 29

CUMULATIVE EMISSION REDUCTION, BY MITIGATION MEASURE, 2021–2050

FIGURE 30

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 31

SUPPLY CHAIN ANALYSIS

FIGURE 32

HYDROGEN GENERATION ECOSYSTEM

FIGURE 33

IMPORT DATA FOR HS CODE 280410-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2022–2024

FIGURE 34

EXPORT DATA FOR HS CODE 280410-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2022–2024

FIGURE 35

PATENTS APPLIED AND GRANTED, 2014–2024

FIGURE 36

PORTER’S FIVE FORCES ANALYSIS

FIGURE 37

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

FIGURE 38

BUYING CRITERIA FOR TOP THREE APPLICATIONS

FIGURE 39

IMPACT OF AI/GENERATIVE AI, BY APPLICATION

FIGURE 40

STEAM METHANE REFORMING (SMR) SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

FIGURE 41

GRAY HYDROGEN SEGMENT HELD LARGEST MARKET SHARE IN 2024

FIGURE 42

CAPTIVE SEGMENT HELD LARGER SHARE OF HYDROGEN GENERATION MARKET IN 2024

FIGURE 43

PETROLEUM REFINERY SEGMENT CAPTURED LARGEST MARKET SHARE IN 2024

FIGURE 44