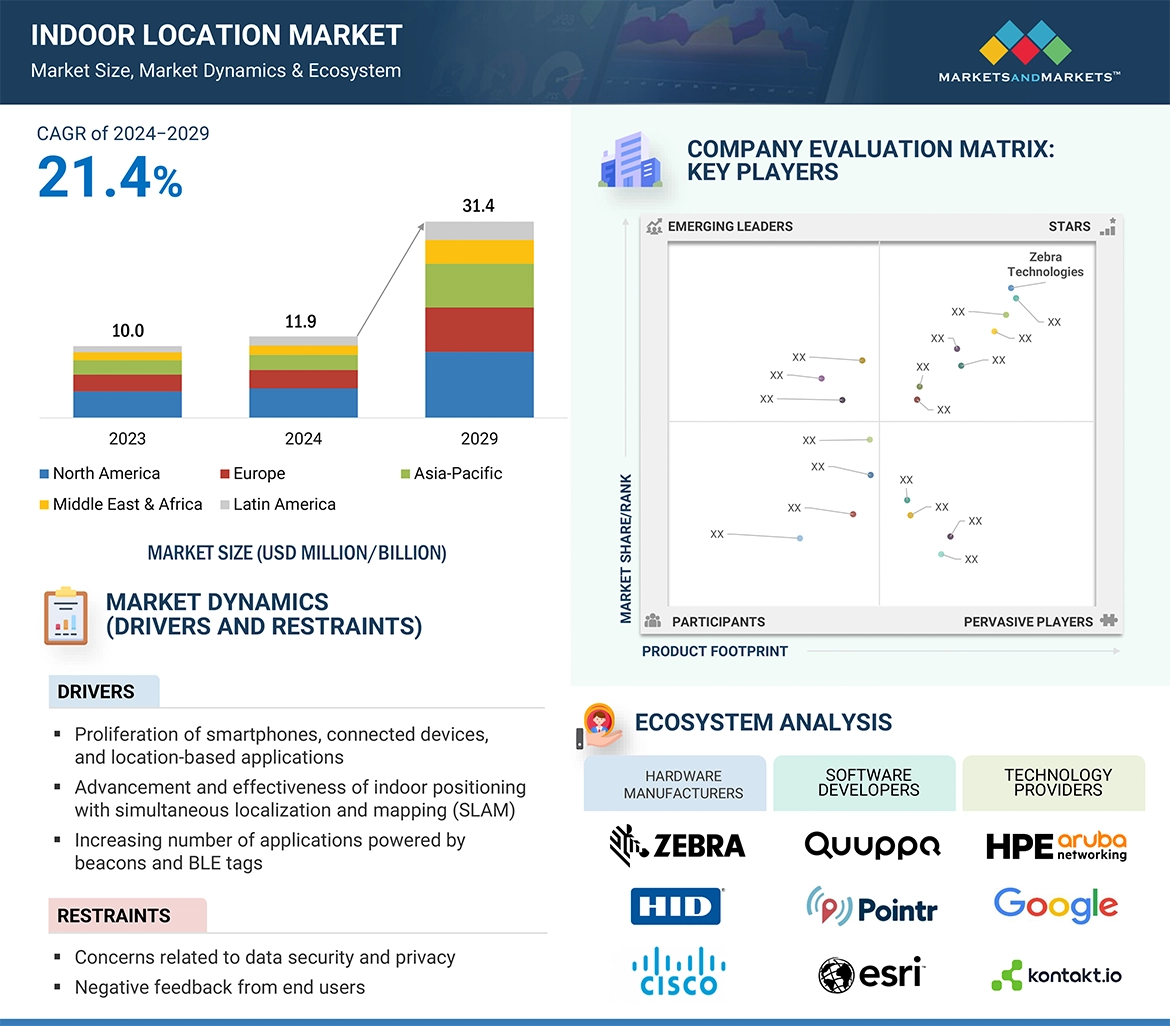

5.2 MARKET DYNAMICS

DRIVERS

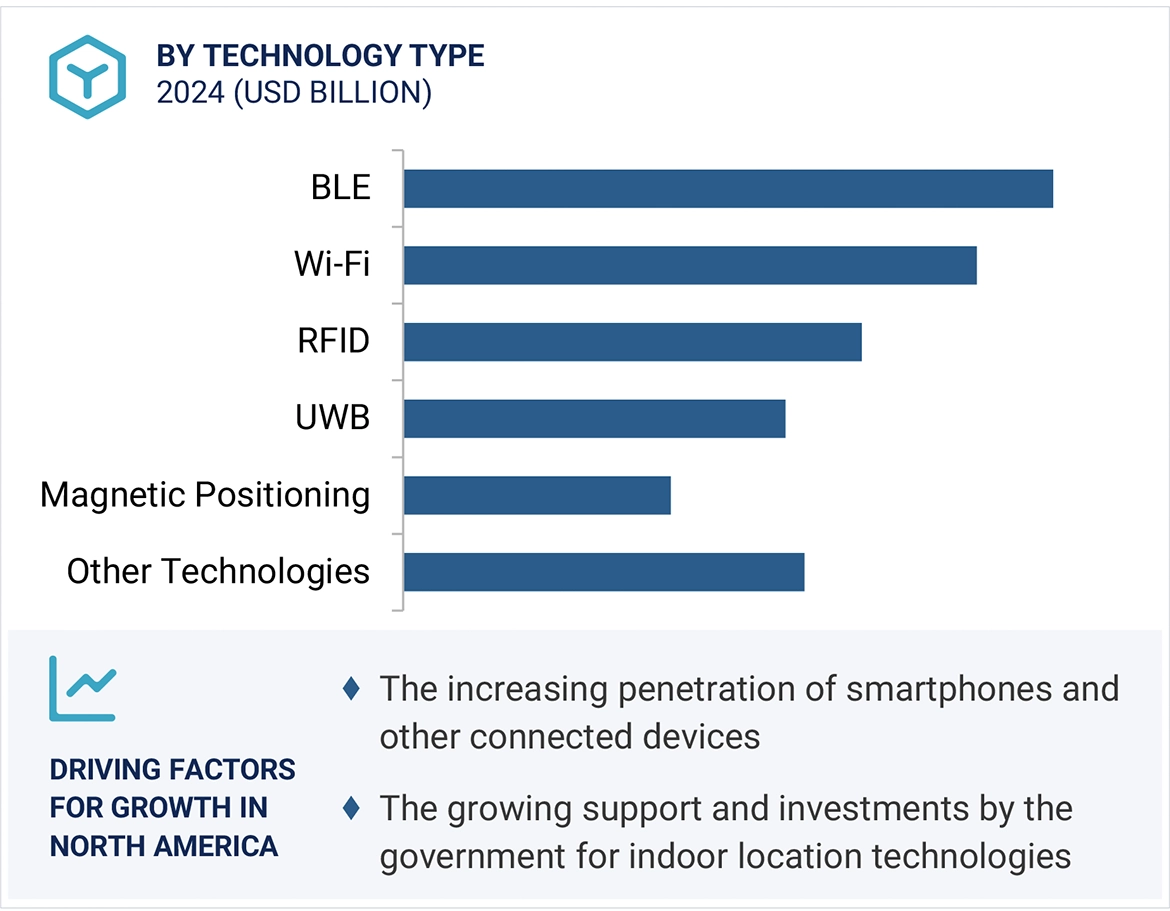

- Proliferation of smartphones, connected devices, and location-based applications

- Advancement and effectiveness of indoor positioning with SLAM

- Increasing number of applications powered by beacons and BLE tags

- Growing integration of beacons in cameras, LED lighting, PoS devices, and digital signage

- Inefficiency of GPS in indoor environments

RESTRAINTS

- Concerns related to data security and privacy

- Negative feedback from end users

- Stringent government regulations

- High installation and maintenance costs

OPPORTUNITIES

- Increasing demand for RFID tags across retail industry

- Growing use of 5G for location-based services

- Growing demand for indoor location technologies to support lean automation and robotic processes

- Focus on Industry 4.0 smart cities and smart manufacturing

CHALLENGES

- Lack of skills and awareness related to indoor location technologies

- Dearth of uniform standards and interoperability coupled with system incompatibility

5.3 INDUSTRY TRENDS

BRIEF HISTORY OF INDOOR LOCATION MARKET

- 2000–2010

- 2011–2020

- 2021–present

TRENDS/DISRUPTIONS IMPACTING BUYERS/CUSTOMERS IN INDOOR LOCATION MARKET

PRICING ANALYSIS

- Average selling price trend of key players, by offering

- Indicative pricing analysis

SUPPLY CHAIN ANALYSIS

ECOSYSTEM/MARKET MAP

TECHNOLOGY ANALYSIS

- Key technologies

- Adjacent technologies

- Complementary technologies

PATENT ANALYSIS

- Methodology

HS CODE: CARDS INCORPORATING ONE OR MORE ELECTRONIC INTEGRATED CIRCUITS "SMART CARDS" (854381)

- Export scenario

- Import scenario

USE CASES

- Las Vegas Convention Center helped visitors navigate efficiently with indoor Google Maps

- OSRAM Malaysia deployed Blueiot RTLS to track assets accurately and protect them

- Kesko increased average check by 6% using Navigine’s personal purchasing assistant

- Senion StepInside Indoor Positioning System helped Ericsson enhance workplace employee performance

- Transports Publics Fribourgeois (TPF) adopted Ubisense RTLS solution for efficient business operations

- TOSHIN Industry Co. Ltd improved its production quality by deploying Quuppa’s new plating methods

KEY CONFERENCES & EVENTS, 2024–2025

CURRENT AND EMERGING BUSINESS MODELS

BEST PRACTICES OF INDOOR LOCATION MARKET

FUTURE LANDSCAPE OF INDOOR LOCATION MARKET

- Indoor location technology roadmap till 2030

- Short-term roadmap (2024–2025)

- Mid-term roadmap (2026–2028)

- Long-term roadmap (2029–2030)

REGULATORY LANDSCAPE

- Regulatory bodies, government agencies, and other organizations

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

PORTER’S FIVE FORCES MODEL

- Threat of new entrants

- Threat of substitutes

- Bargaining power of suppliers

- Bargaining power of buyers

- Intensity of competitive rivalry

KEY STAKEHOLDERS AND BUYING CRITERIA

- Key stakeholders in buying process

- Buying criteria

COMPANY VALUATION, INVESTMENT, AND FUNDING SCENARIO

INTRODUCTION TO ARTIFICIAL INTELLIGENCE AND GENERATIVE AI

- Impact of AI/generative AI on indoor location market

- Use cases of generative AI in indoor location market

- Future of generative AI in indoor location market

ARCHITECTURE

- Magnetic field approach

- Fingerprinting

- Smartphone data

INDOOR LOCATION IMPACT ON ADJACENT NICHE TECHNOLOGIES

- Internet of Things (IoT)

- Augmented reality (AR) and virtual reality (VR)

- Mobile applications and app development

- Indoor mapping and geographic information system (GIS)

- Asset tracking and inventory management

- Smart buildings and facilities management

- Data analytics and business intelligence

Growth opportunities and latent adjacency in Indoor Location Market