The research process for this study included systematic gathering, recording, and analysis of data about customers and companies operating in the millimeter wave technology market. This process involved the extensive use of secondary sources, directories, and databases (Factiva, Oanda, and OneSource) for identifying and collecting valuable information for the comprehensive, technical, market-oriented, and commercial study of the millimeter wave technology market. In-depth interviews were conducted with primary respondents, including experts from core and related industries and preferred manufacturers, to obtain and verify critical qualitative and quantitative information as well as to assess growth prospects. Key players in the mm wave technology market were identified through secondary research, and their market rankings were determined through primary and secondary research. This research included studying annual reports of top players and interviewing key industry experts such as CEOs, directors, and marketing executives.

Secondary Research

In the secondary research process, various secondary sources were referred to for identifying and collecting information important for this study. Secondary sources included corporate filings, such as annual reports, investor presentations, and financial statements; trade, business, and professional associations; white papers; millimeter wave technology products-related journals; certified publications; articles by recognized authors; directories; and databases.

Secondary research was conducted to obtain key information about the industry supply chain, market value chain, key players, market classification and segmentation as per industry trends to the bottom-most level, geographic markets, and key developments from both market- and technology-oriented perspectives. Data from secondary research was collected and analyzed to determine the overall market size, which was further validated by primary research.

Primary Research

In the primary research process, various primary sources from the supply and demand sides were interviewed to obtain qualitative and quantitative information for this report. Primary sources from the supply side included industry experts such as CEOs, VPs, marketing directors, technology & innovation directors, and key executives from major companies in the millimeter wave technology market.

After going through market engineering (which includes calculations for market statistics, market breakdown, market size estimations, market forecasting, and data triangulation), extensive primary research was conducted to gather information and verify and validate the critical numbers obtained. Primary research was conducted to identify segmentation types, industry trends, key players, competitive landscape, and key market dynamics such as drivers, restraints, opportunities, and challenges, along with the key strategies adopted by players operating in the market.

To know about the assumptions considered for the study, download the pdf brochure

Market size Estimation

In the complete market engineering process, both top-down and bottom-up approaches were used, along with several data triangulation methods, to estimate and forecast the size of the market and its segments and subsegments listed in the report. Extensive qualitative and quantitative analyses were carried out on the complete market engineering process to list the key information/insights pertaining to the millimeter wave technology market.

The key players in the market were identified through secondary research, and their rankings in the respective regions were determined through primary and secondary research. This entire procedure involved the study of the annual and financial reports of top players, as well as interviews with industry experts such as chief executive officers, vice presidents, directors, and marketing executives for quantitative and qualitative key insights. All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources. All parameters that affect the markets covered in this research study were accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data. This data was consolidated and enhanced with detailed inputs and analysis from MarketsandMarkets and presented in this report.

Millimeter wave technology market: Bottom-Up Approach.

Millimeter wave technology market: Top-Down Approach.

Data Triangulation

After arriving at the overall size of the millimeter wave technology market from the market size estimation process explained above, the total market was split into several segments and subsegments. Where applicable, the market breakdown and data triangulation procedures were employed to complete the overall market engineering process and arrive at the exact statistics for all segments and subsegments. The data was triangulated by studying various factors and trends from both the demand and supply sides. Along with this, the market size was validated using top-down and bottom-up approaches.

Market Definition

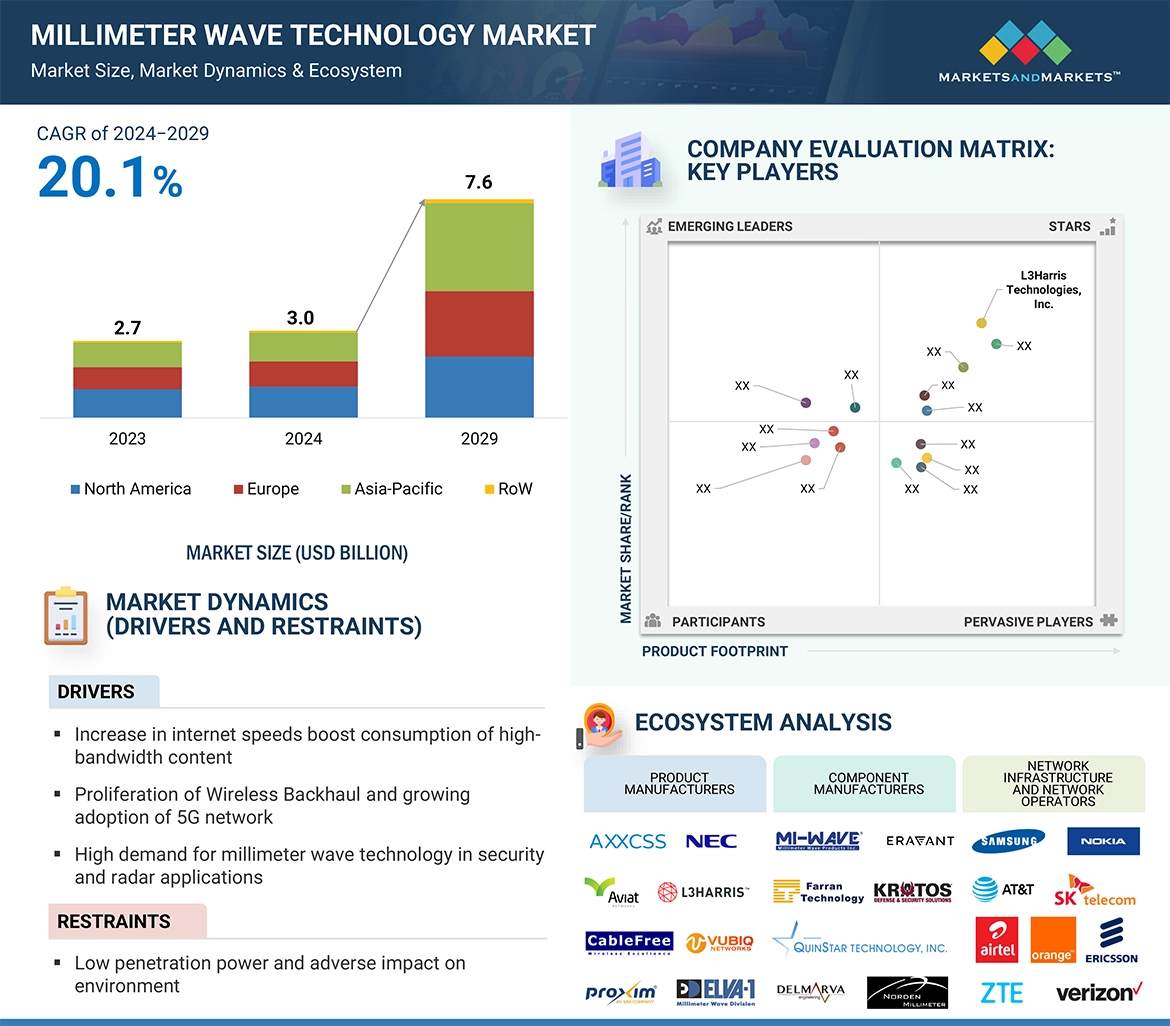

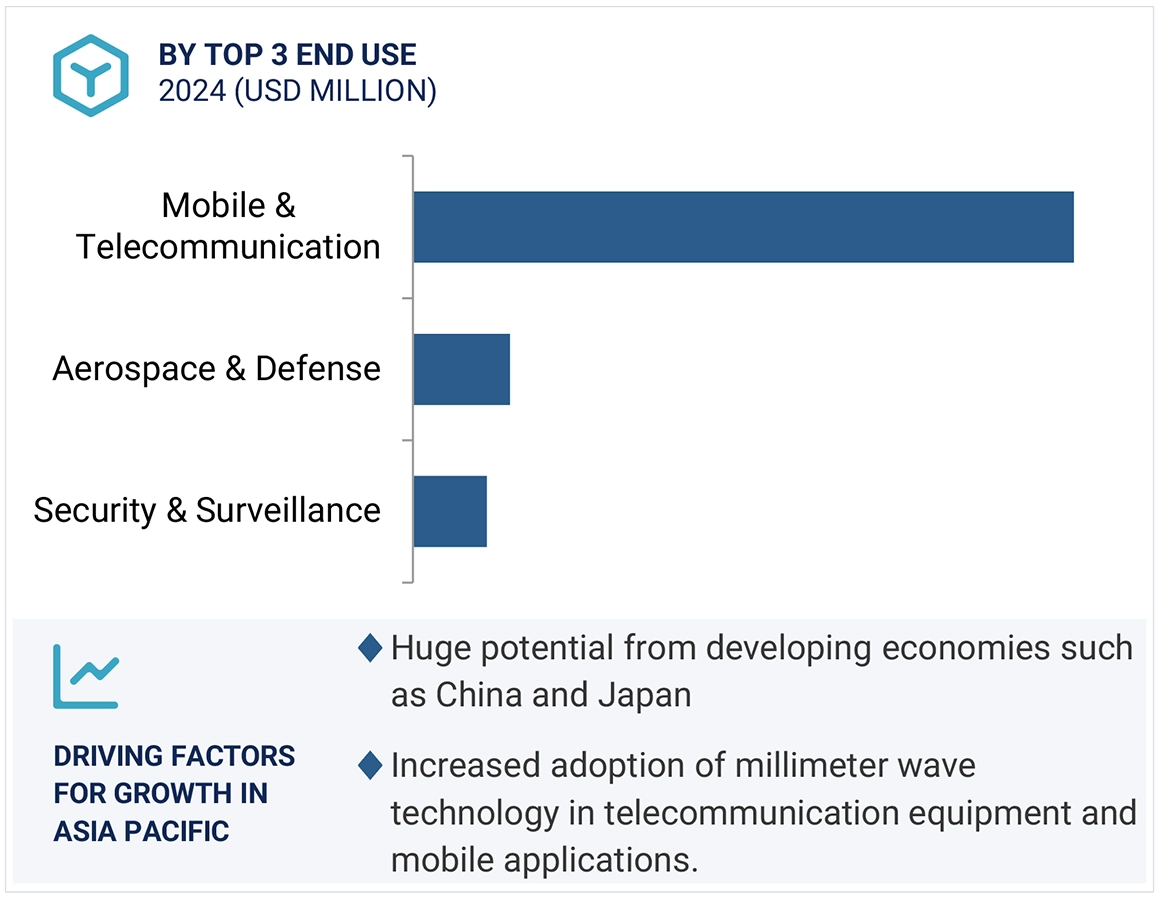

Millimeter wave, also known as extremely high frequency (EHF) or very high frequency (VHF), is the band of spectrum between 30 gigahertz (GHz) and 300 GHz. These waves are named so because their wavelengths range from 1 millimeter to 10 millimeters. Previously, millimeter waves were mainly used in military and satellite communication applications. However, this technology has been gaining traction in mobile and telecom applications, mainly for 5G. In the context of wireless communication, millimeter waves generally refer to bands of the spectrum of around 38 GHz, 60 GHz, and 94 GHz.

Key Stakeholders

-

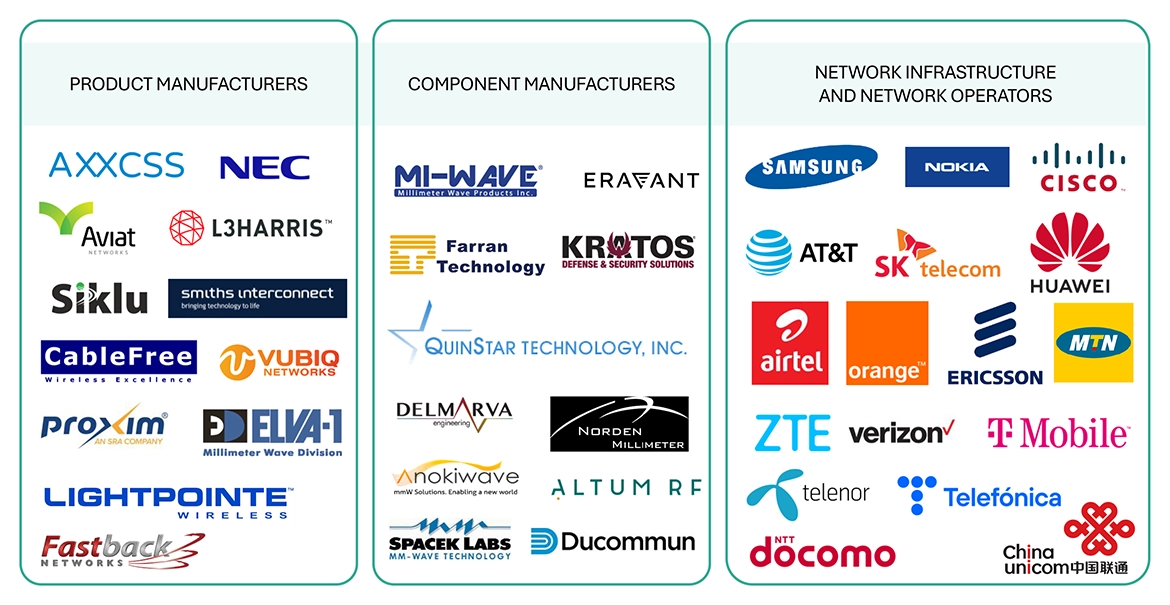

Companies in the millimeter wave technology market

-

Providers of millimeter wave components

-

Technical standards organizations

-

Research institutes and organizations

-

Government and financial institutions

-

Venture capitalists

-

Private equity firms

Report Objectives

-

To define, describe, and forecast the millimeter wave technology market based on product, frequency band, license type, end use, component, and region.

-

To forecast the sizes of various segments with respect to four major regions—

North America, Europe, Asia Pacific, and Rest of the World (RoW)

-

To provide a detailed analysis of the millimeter wave technology supply chain.

-

To analyze the impact of the recession on mm wave technology market

-

To strategically analyze the micromarkets1 with respect to individual growth trends and prospects and their contributions to the total market

-

To analyze competitive developments such as expansions, agreements, partnerships, acquisitions, product developments, and research and development (R&D) in the millimeter wave technology market

-

To analyze the opportunities for market players and provide details of the competitive landscape of the market.

-

To benchmark the market players using the proprietary company evaluation matrix framework, which analyzes the market players on various parameters within the broad categories of business strategy excellence and strength of product portfolios.

-

To strategically profile the key players and comprehensively analyze their market positions in terms of ranking and core competencies2, along with a detailed competitive landscape of the market.

Available customizations

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies.

Product analysis

-

Detailed analysis and profiling of additional market players

The following customization options are available for the report:

-

Market sizing and forecast for additional countries

-

Additional five companies profiling

Jacob

Apr, 2026

Which product or component segment (radar systems, scanners, antennas, telecom equipment) offers the highest revenue opportunity for new entrants or existing companies?.

Billy

Apr, 2026

What is the ROI outlook for companies investing in millimeter wave technology over the next 5�7 years?.