Download PDF

Download PDF Request Customisation

Request Customisation

Heat Transfer Fluids Market

Report Code

CH 2592

Published in

Sep, 2025, By MarketsandMarkets™

Heat Transfer Fluids Market by Product Type (Mineral Oils, Synthetic Fluids, Glycol-Based Fluids, Other Product Types), Temperature (Low, Medium, High, Ultra-High), Application (Industrial Process Heating, Thermal Energy Storage, Chilled/Hot Water Loops, Pharmaceutical & Biotech, Power Generation & Waste Heat Recovery, Thermal Management, Other Applications), End-Use Industry (Chemical & Petrochemicals, Oil & Gas, Automotive, Food & Beverage, Pharmaceuticals, Hvac, Renewable Energy, Other End-Use Industries), and Region - Global Forecast to 2030

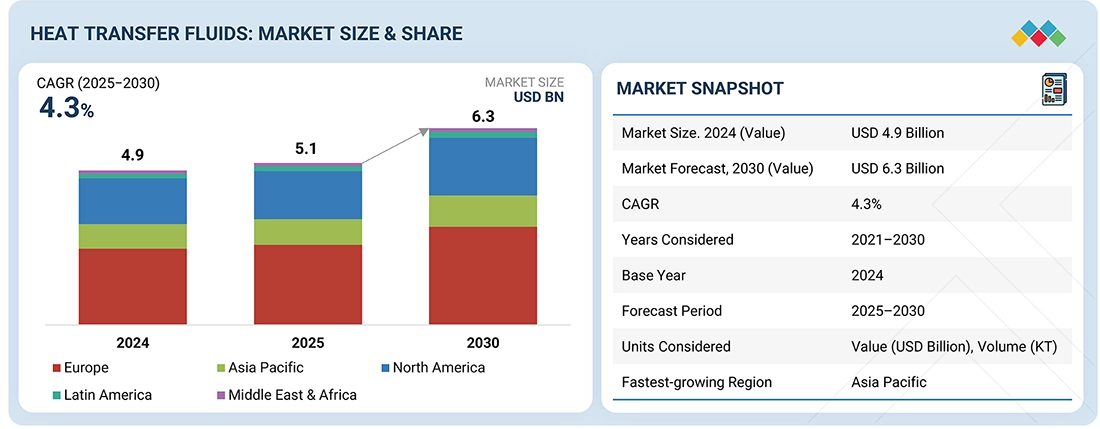

USD 6.3 BN

MARKET SIZE, 2030

CAGR 4.3%

(2025-2030)

250

REPORT PAGES

68

MARKET TABLES

HEAT TRANSFER FLUIDS MARKET SIZE

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis | Updated on : April 28, 2026

The global heat transfer fluids market size is projected to grow from USD 5.1 billion in 2025 to USD 6.3 billion by 2030, registering a CAGR of 4.3% from 2025 to 2030. This expansion is supported by the increasing importance of efficient thermal management across a broad spectrum of industries.

KEY TAKEAWAYS

-

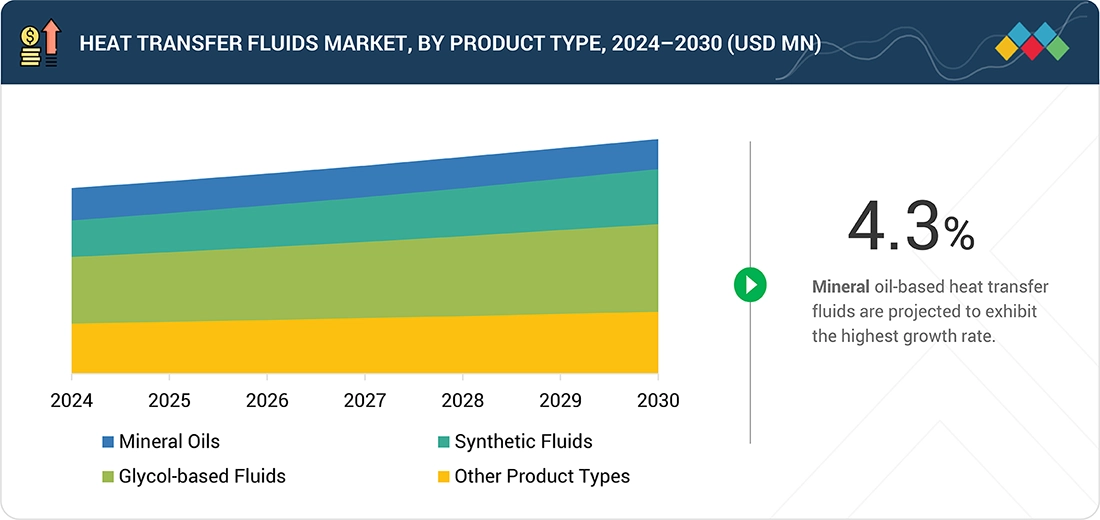

BY Product typeMineral oils are estimated to be the largest subsegment in the heat transfer fluids (HTF) market due to several key advantages that make them a preferred choice across various industries. Mineral oils are significantly cheaper compared to synthetic fluids and glycol-based fluids, making them an economical option for companies looking to optimize their operational budgets without compromising performance.

-

By temperatureThe growth of low-temperature heat transfer fluids (HTFs) is the highest in recent years, primarily due to the rapid expansion of industries that require reliable performance in sub-zero and cryogenic environments. The global cold chain sector, driven by rising demand for frozen food, pharmaceuticals, and vaccine storage, has significantly boosted the adoption of HTFs capable of operating efficiently at very low temperatures. Similarly, the surge in liquefied natural gas (LNG) projects, including regasification and liquefaction plants, has created strong demand for these fluids, as they are essential for handling extreme thermal conditions.

-

By End-use industryThe chemicals and petrochemicals industry is estimated to be the largest end-use segment for the heat transfer fluids (HTF) market due to its extensive and continuous demand for precise thermal management solutions. This sector encompasses a wide range of processes, such as distillation, polymerization, and chemical synthesis, which require accurate temperature control to maintain product quality and process efficiency. Heat transfer fluids are essential in these processes for maintaining optimal reaction conditions, ensuring process safety, and enhancing energy efficiency.

-

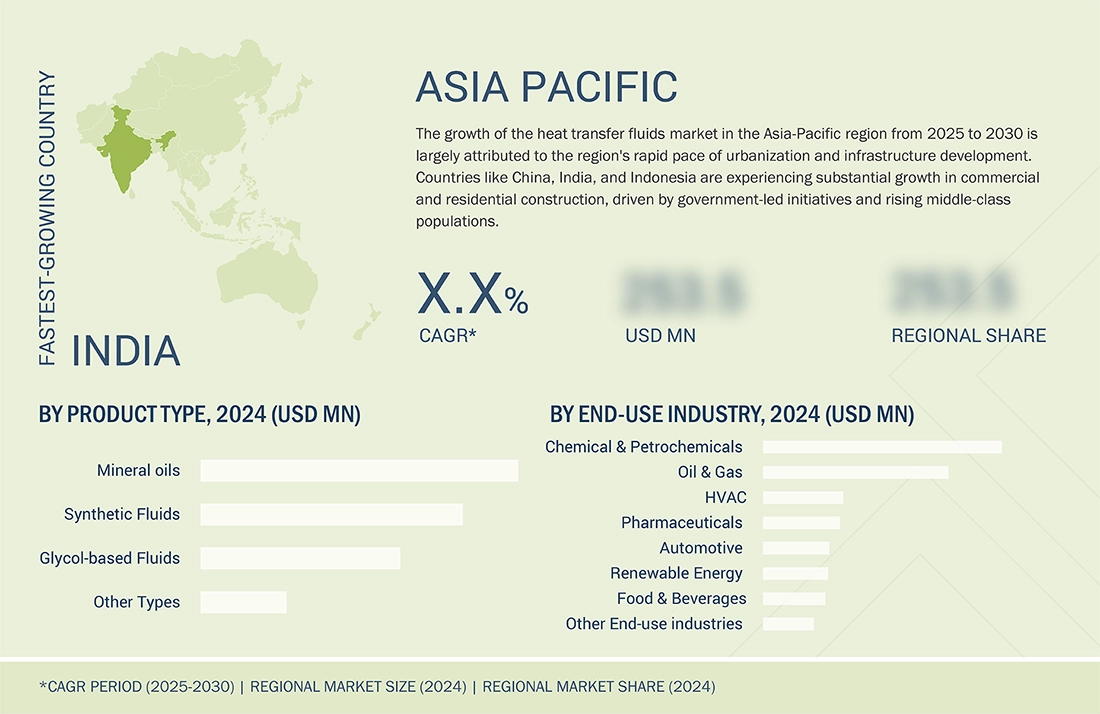

By regionAsia Pacific is estimated to be the largest market for heat transfer fluids (HTFs) due to a confluence of several key factors, including rapid industrialization, robust economic growth, and the presence of significant end-use industries. This region's dynamic economic landscape and ongoing industrial expansion have created substantial demand for efficient thermal management solutions across various sectors. Rapid industrialization in countries like China, India, and Japan has driven the demand for HTFs.

-

COMPETITIVE LANDSCAPEThe heat transfer fluids market is driven by product innovation, capacity expansions, and strategic collaborations among global leaders such as Dow (US), Eastman Chemical Company (US), ExxonMobil (US), Chevron Corporation (US), Huntsman Corporation (US), Shell plc (UK), Lanxess (Germany), Clariant (Switzerland), Wacker Chemie AG (Germany), Indian Oil Corporation Ltd. (India), and Schultz Canada Chemicals Ltd. (Canada). These companies are focusing on developing advanced fluids with improved acoustic, safety, and thermal properties to cater to the growing demand from petrochemical industries.

The heat transfer fluids market is growing steadily, driven by industrial processes becoming more advanced and energy-intensive. The need for reliable systems to regulate temperature has grown substantially. Traditional methods of cooling and heating are proving inadequate in many cases, creating strong demand for HTFs that provide greater efficiency, stability, and safety. These fluids are no longer viewed as auxiliary materials but as critical enablers of operational performance, energy savings, and compliance with modern industrial standards.

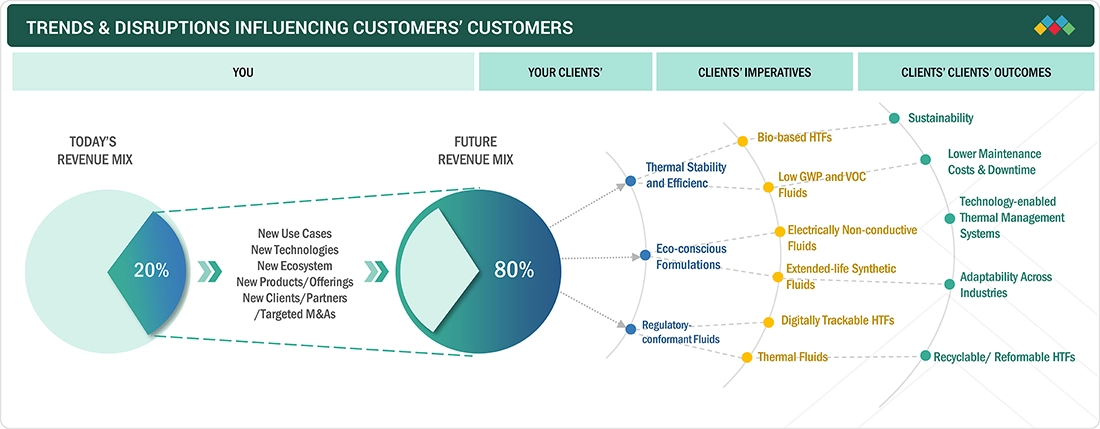

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The heat transfer fluid industry is undergoing a significant transformation, shifting from 80% revenue reliance on existing products to an expected 80% from new technologies within 4–5 years. Key sectors driving this change include data center cooling, electric vehicle thermal management, and chemical & pharmaceutical processing. These sectors prioritize sustainability, energy efficiency, and safety, aiming for outcomes like enhanced energy capture, lightweight vehicles with better fuel efficiency, and reduced environmental impact. This trend reflects the industry’s strategic focus on innovation and diversification, meeting evolving client needs with advanced solutions that optimize performance and environmental sustainability.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

HEAT TRANSFER FLUIDS MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Increasing expansion in renewable and industrial heat applications

-

Rising adoption of immersion cooling in EVs and electronics

RESTRAINTS

Impact

Level

Level

-

Absence of standardized testing and performance criteria for EV cooling fluids

OPPORTUNITIES

Impact

Level

Level

-

250

-

Technological innovation in immersion and direct cooling

CHALLENGES

Impact

Level

Level

-

68

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Increasing expansion in renewable and industrial heat applications

Expansion in renewable and industrial heat applications is one of the most important drivers for the growth of the heat transfer fluids (HTFs) industry. On the renewable side, the increasing global shift toward clean energy has amplified investments in technologies such as concentrated solar power (CSP), solar thermal systems, and other renewable energy projects that require reliable heat storage and transfer solutions. HTFs play a critical role in these systems by enabling efficient capture, storage, and distribution of thermal energy, which helps maximize output and improve overall energy conversion efficiency. The growing emphasis on reducing carbon emissions and meeting sustainability goals has further accelerated the adoption of advanced HTFs, particularly synthetic and molten salt-based fluids, capable of withstanding extreme temperatures in renewable energy applications.

Restraint: absence of standardized testing and performance criteria for EV cooling fluids

The absence of standardized testing and performance criteria for EV cooling fluids is emerging as a key restraint for the heat transfer fluids (HTFs) market. As electric vehicles (EVs) continue to expand rapidly, the demand for efficient thermal management systems has become critical to ensure battery safety, performance, and longevity. EV cooling fluids, a specialized class of HTFs, are designed to regulate battery pack temperatures, maintain optimal operating conditions, and prevent overheating or thermal runaway. However, unlike traditional automotive coolants or industrial HTFs, there is no universally accepted standard or benchmark to evaluate the performance, safety, or compatibility of these fluids across different vehicle platforms and chemistries. This lack of harmonization creates uncertainty for both manufacturers and end users, making it difficult to compare products, validate long-term reliability, and ensure consistent quality across the market.

Opportunity: Customized, application-specific formulations in the HTF industry

The trend of customized, application-specific formulations represents a significant opportunity for the heat transfer fluids (HTFs) market because it allows manufacturers to move beyond standard offerings and create value-added, high-margin products tailored to niche requirements. As industries diversify and technologies evolve, one-size-fits-all HTFs are increasingly insufficient to meet the unique performance, safety, and regulatory needs of different applications. This creates room for HTF producers to collaborate directly with end-users—such as solar plant developers, EV manufacturers, chemical processors, and data center operators—to develop fluids optimized for their exact operating conditions.

Challenge: Balancing performance with environmental compliance

Balancing performance with environmental compliance poses a major challenge in the heat transfer fluids (HTFs) industry because high thermal stability and efficiency often conflict with sustainability requirements. Traditional HTFs, such as mineral oils and synthetic aromatics, are widely used due to their excellent heat transfer efficiency, high temperature resistance, and cost-effectiveness. However, many of these fluids are toxic, non-biodegradable, or environmentally persistent, making them increasingly difficult to use under today’s strict regulations on emissions, waste management, and chemical safety.

Heat Transfer Fluids Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Use of HTFs in concentrated solar power (CSP) plants | Efficient thermal energy storage, improved solar plant output, contribution to renewable energy adoption, reduced carbon footprint |

|

Application in oil & gas processing (refineries, LNG, petrochemicals) | Reliable high-temperature performance, enhanced process efficiency, safe handling of extreme conditions, reduced operational downtime |

|

HTFs in chemical and industrial manufacturing (plastics, polymers, pharmaceuticals) | Precise temperature control, consistent product quality, reduced energy consumption, improved process safety |

|

Use of HTFs in food & beverage processing (cold storage, refrigeration, beverage cooling) | Compliance with food safety standards, stable low-temperature performance, improved product shelf life, energy-efficient cooling |

|

Adoption in data centers and electronics cooling | Advanced thermal management, prevention of overheating, extended equipment lifespan, improved energy efficiency and cost savings |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

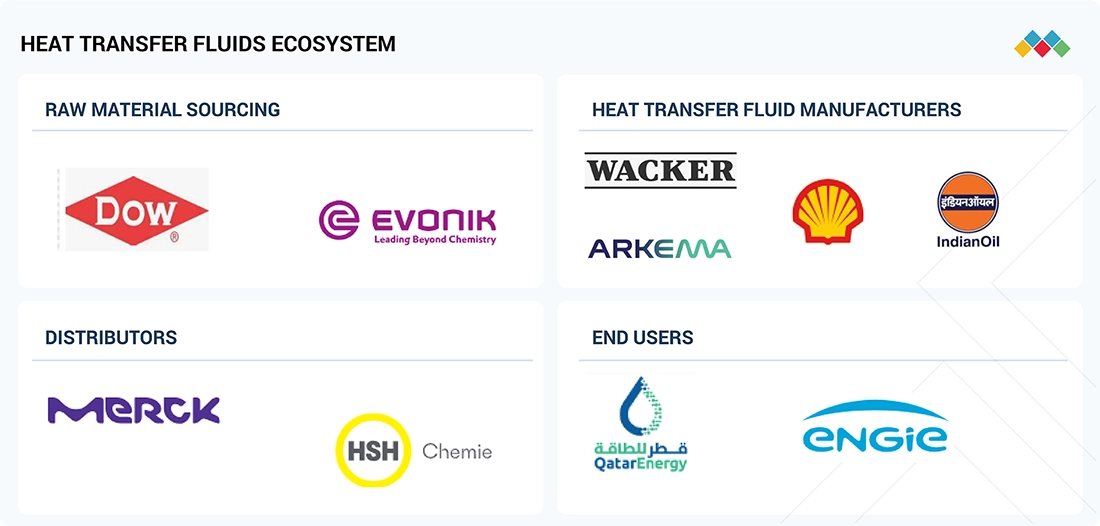

HEAT TRANSFER FLUIDS MARKET ECOSYSTEM

The heat transfer fluids ecosystem analysis involves identifying and analyzing interconnected relationships among various stakeholders, including raw material suppliers, manufacturers, distributors, and end users. The raw material suppliers provide synthetic fluids and mineral oil to manufacturers. The distributors and suppliers establish contact between the manufacturing companies and end users to streamline the supply chain, increasing operational efficiency and profitability.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Heat transfer fluids Market, By temperature Type

Low-temperature heat transfer fluids (HTFs) have emerged as the fastest-growing segment in recent years, largely driven by the increasing demand from industries that operate in sub-zero and cryogenic conditions. The rapid expansion of the global cold chain—fueled by the rising need for frozen food, pharmaceutical products, and vaccine storage—has significantly accelerated the adoption of HTFs designed for efficient low-temperature performance. At the same time, the growth of liquefied natural gas (LNG) infrastructure, particularly in regasification and liquefaction facilities, has boosted the need for these fluids to ensure safe and reliable operation under extreme thermal environments.

Polyvinyl butyral market, By End use industry

The chemical and petrochemical sector is the largest and fastest-growing segment in the heat transfer fluids (HTFs) market because it relies heavily on precise thermal management for a wide range of processes. In this industry, operations such as distillation, polymerization, condensation, refining, and cracking require stable, high-performance fluids that can withstand extreme temperatures while ensuring safety and efficiency. The rapid expansion of the global chemical industry, particularly in Asia-Pacific countries like China and India, has amplified demand for HTFs to support rising production capacities in plastics, fertilizers, and specialty chemicals.

REGION

Asia Pacific to be fastest-growing region in global heat transfer fluids market during forecast period

Heat Transfer Fluids Market: COMPANY EVALUATION MATRIX

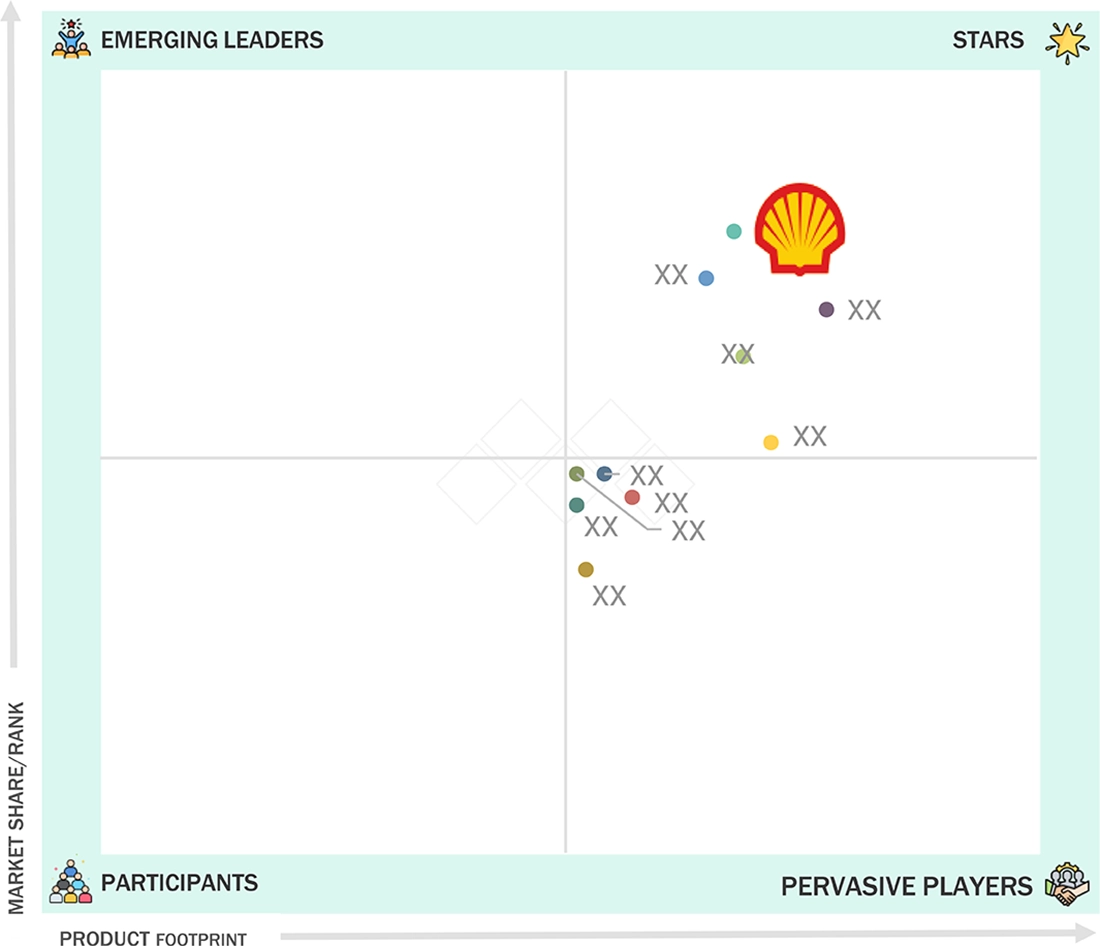

In the heat transfer fluids (HTFs) market matrix, Shell plc (Star) leads with its strong global presence, diversified product portfolio, and well-established supply chain, catering to a wide spectrum of industrial applications including petrochemicals, oil & gas, and renewable energy. Eastman Chemical Company (Strong Performer) continues to expand its footprint through innovative HTF formulations designed for efficiency and environmental compliance, making it a preferred choice in chemical processing and solar energy systems. Meanwhile, Dow Inc. (Emerging Leader) is gaining visibility with advanced synthetic fluids that deliver superior thermal stability and energy efficiency, strengthening its position across high-growth segments such as electronics cooling and concentrated solar power. While Shell dominates with scale and global reach, Eastman and Dow showcase strong potential to move further up the leadership quadrant as demand for energy-efficient and sustainable thermal management solutions accelerates worldwide.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size, 2024 (Value) | USD 4.9 Billion |

| Market Forecast, 2030 (Value) | USD 6.3 Billion |

| Growth Rate | CAGR of 4.3% from 2025 to 2030 |

| Study Period | 2021–2030 |

| Base Year | 2024 |

| Forecast Period | 2025–2030 |

| Units Considered | Value (USD Billion), Volume (Kilotons) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, South America, Middle East & Africa |

WHAT IS IN IT FOR YOU: Heat Transfer Fluids Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Country-Level Breakdown | • Instead of just regional coverage, the report can provide country-specific market data (e.g., China, India, the US, and Germany). This includes demand drivers, production capacities, import/export trends, and regulatory outlooks. | 250 |

| Application-Specific Deep Dive | • It can offer a customized focus on specific HTF applications such as solar thermal systems, data center cooling, or industrial heat exchangers, including end-user adoption rates, OEM partnerships, and future demand projections for each application. | • Supports clients targeting niche segments, enabling them to design product portfolios or allocate R&D spending more effectively |

| Fluid Type Customization | • Comparative analysis of synthetic, glycol-based, and mineral oil HTFs, as well as modified grades was offered. This covered performance benchmarks, technical advantages, pricing, and suitability for different industries. | • Enables manufacturers and buyers to optimize fluid selection, align pricing with performance, and explore premium-grade opportunities |

| Competitive Benchmarking | • It can offer extended profiling of regional and niche players alongside global leaders (e.g., Dow, Chevron, Therminol), including SWOT analysis, product differentiation, technology focuses, and market positioning. | • Provides a clear competitive landscape, helping clients identify potential partners, acquisition targets, or competitive threats |

RECENT DEVELOPMENTS

- December 2022 : Eastman Chemical Company (US) and Krahn Chemie GmbH (KRAHN), (Greece) revised their distribution agreement to extend the market reach for Eastman’s heat transfer fluids (HTF) in southeastern Europe. Under the revised agreement, KRAHN was authorized to distribute Eastman’s Therminol® and Marlotherm® product lines throughout Greece. These fluids were designed for the indirect transfer of process heat in a variety of single- or multiple-use heat systems. They are known for their outstanding thermal stability, precise temperature control, and minimal maintenance requirements.

- December 2022 : Chevron completed the acquisition of the Renewable Energy Group. This acquisition would help company leverage its strengths to deliver lower carbon energy.

- July 2022 : Eastman Chemical Company announced a planned expansion of its manufacturing capacity for Eastman Therminol® 66 heat transfer fluid in Anniston, Alabama. The expansion, slated for completion in 2024, boosted US-based capacity for this product by 50%.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

25

2

RESEARCH METHODOLOGY

29

3

EXECUTIVE SUMMARY

40

4

PREMIUM INSIGHTS

44

5

MARKET OVERVIEW

Renewable expansion and AI-driven innovation propel heat transfer fluids market amid regulatory shifts.

47

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

Expansion in renewable and industrial heat applications

5.2.1.2

Regulatory incentives and energy efficiency legislation

5.2.1.3

Lifecycle services and analytical programs by major suppliers

5.2.1.4

Rising adoption of immersion cooling in EVs and electronics

5.2.2

RESTRAINTS

5.2.2.1

Absence of standardized testing and performance criteria for EV cooling fluids

5.2.3

OPPORTUNITIES

5.2.3.1

Customized, application-specific formulations

5.2.3.2

Technological innovation in immersion and direct cooling

5.2.4

CHALLENGES

5.2.4.1

Balancing performance with environmental compliance

5.3

IMPACT OF GENERATIVE AI

5.3.1

INTRODUCTION

5.3.2

IMPACT OF GENERATIVE AI ON HEAT TRANSFER FLUIDS MARKET

6

INDUSTRY TRENDS

Discover how emerging technologies and pricing shifts redefine competitive dynamics across global markets.

55

6.1

INTRODUCTION

6.2

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.3

SUPPLY CHAIN ANALYSIS

6.4

PRICING ANALYSIS

6.4.1

AVERAGE SELLING PRICE TREND, BY REGION, 2021–2024

6.4.2

AVERAGE SELLING PRICE TREND, BY PRODUCT TYPE, 2021–2024

6.4.3

AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PRODUCT TYPE, 2021–2024

6.5

INVESTMENT LANDSCAPE AND FUNDING SCENARIO

6.6

ECOSYSTEM ANALYSIS

6.7

TECHNOLOGY ANALYSIS

6.7.1

KEY TECHNOLOGIES

6.7.2

COMPLEMENTARY TECHNOLOGIES

6.7.3

ADJACENT TECHNOLOGIES

6.8

PATENT ANALYSIS

6.8.1

METHODOLOGY

6.8.2

PATENTS GRANTED WORLDWIDE, 2014–2024

6.8.3

PATENT PUBLICATION TRENDS

6.8.4

INSIGHTS

6.8.5

LEGAL STATUS OF PATENTS

6.8.6

JURISDICTION ANALYSIS

6.8.7

TOP APPLICANTS

6.8.8

LIST OF MAJOR PATENTS

6.9

TRADE ANALYSIS

6.9.1

IMPORT SCENARIO (HS CODE 841950)

6.9.2

EXPORT SCENARIO (HS CODE 841950)

6.10

KEY CONFERENCES AND EVENTS, 2025–2026

6.11

TARIFF AND REGULATORY LANDSCAPE

6.11.1

TARIFF AND REGULATORY REGULATIONS RELATED TO HEAT TRANSFER FLUIDS MARKET

6.11.2

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.11.3

REGULATIONS RELATED TO HEAT TRANSFER FLUIDS MARKET

6.12

PORTER’S FIVE FORCES ANALYSIS

6.12.1

THREAT OF NEW ENTRANTS

6.12.2

THREAT OF SUBSTITUTES

6.12.3

BARGAINING POWER OF SUPPLIERS

6.12.4

BARGAINING POWER OF BUYERS

6.12.5

INTENSITY OF COMPETITIVE RIVALRY

6.13

KEY STAKEHOLDERS AND BUYING CRITERIA

6.13.1

KEY STAKEHOLDERS IN BUYING PROCESS

6.13.2

BUYING CRITERIA

6.14

MACROECONOMIC OUTLOOK

6.14.1

GDP TRENDS AND FORECASTS, BY COUNTRY

6.15

CASE STUDY ANALYSIS

6.15.1

ITC MAURYA ENHANCED HEAT PUMP EFFICIENCY WITH NANO-ENHANCED HEAT TRANSFER FLUIDS

6.15.2

ENHANCING SOLAR POWER PLANT EFFICIENCY THROUGH ADVANCED HEAT TRANSFER FLUID PERFORMANCE

6.15.3

EXTENDING THERMAL LIMITS AND RELIABILITY: VERSALIS’ TRANSITION TO THERMINOL FOR HIGH-TEMPERATURE DISTILLATION

6.16

IMPACT OF 2025 US TARIFF – HEAT TRANSFER FLUIDS MARKET

6.16.1

INTRODUCTION

6.16.2

KEY TARIFF RATES

6.16.3

PRICE IMPACT ANALYSIS

6.16.4

IMPACT ON COUNTRY/REGION

6.16.4.1

US

6.16.4.2

Europe

6.16.4.3

Asia Pacific

6.16.5

IMPACT ON END-USE INDUSTRIES

7

HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Kilotons | 4 Data Tables

85

7.1

INTRODUCTION

7.2

MINERAL OILS

7.2.1

COST-EFFECTIVE COMPARED TO GLYCOL-BASED AND SYNTHETIC FLUIDS—KEY FACTOR DRIVING MARKET GROWTH

7.3

SYNTHETIC FLUIDS

7.3.1

ENVIRONMENTALLY FRIENDLY NATURE TO SUPPORT ADOPTION

7.4

GLYCOL-BASED FLUIDS

7.4.1

OFFER EXCELLENT CORROSION INHIBITION PROPERTIES—KEY FACTOR PROPELLING MARKET GROWTH

7.5

OTHER PRODUCT TYPES

7.5.1

NANOFLUIDS

7.5.2

IONIC LIQUIDS

7.5.3

BIO-BASED HTF

7.5.4

MOLTEN SALTS

8

HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Kilotons | 4 Data Tables

91

8.1

INTRODUCTION

8.2

LOW TEMPERATURE

8.2.1

NEED TO ENHANCE EFFICIENCY IN COOLING & CRYOGENICS SYSTEMS TO DRIVE MARKET

8.3

MEDIUM TEMPERATURE

8.3.1

RISING INDUSTRIALIZATION AND URBANIZATION TO SUPPORTMARKET GROWTH

8.4

HIGH TEMPERATURE

8.4.1

VITAL ROLE IN ENERGY-INTENSIVE INDUSTRIES TO DRIVE MARKET

8.5

ULTRA-HIGH TEMPERATURE

8.5.1

USE IN HIGHLY SPECIALIZED APPLICATIONS TO DRIVE ADOPTION

9

HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Kilotons | 4 Data Tables

97

9.1

INTRODUCTION

9.2

CHEMICAL & PETROCHEMICAL

9.2.1

IMPLEMENTATION IN CHEMICAL PLANTS OWING TO LOW VOLATILITY PROPERTIES TO PROPEL MARKET

9.3

OIL & GAS

9.3.1

ADOPTION IN OIL & GAS PLANTS TO REDUCE VIBRATIONS IN TRANSDUCERS, CABLES, AND CONTROL VALVES TO PROPEL MARKET

9.4

AUTOMOTIVE

9.4.1

USE IN AUTOMOBILE BATTERIES, COMPRESSORS, AND MOTORS FOR EFFICIENT HEAT TRANSFER TO PROPEL MARKET

9.5

RENEWABLE ENERGY

9.5.1

DEPLOYMENT IN CSP PLANTS DUE TO HIGH OXIDATION RESISTANCE AND THERMAL STABILITY TO PROPEL MARKET

9.6

PHARMACEUTICALS

9.6.1

IMPLEMENTATION OF FOOD-GRADE HEAT TRANSFER FLUIDS IN PHARMACEUTICAL APPLICATIONS TO PROPEL MARKET

9.7

FOOD & BEVERAGES

9.7.1

UTILIZATION OF HEAT TRANSFER FLUIDS AS SUBSTITUTE FOR STEAM IN FOOD PROCESSING PLANTS TO PROPEL MARKET

9.8

HVAC

9.8.1

CORROSION RESISTANCE AND LONG-TERM STABILITY OF HEAT TRANSFER FLUIDS TO INCREASE DEMAND FOR HVAC APPLICATIONS

9.9

OTHER END-USE INDUSTRIES

9.9.1

ELECTRICAL & ELECTRONICS

9.9.2

AEROSPACE

10

HEAT TRANSFER FLUIDS MARKET, BY REGION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Kilotons | 172 Data Tables

107

10.1

INTRODUCTION

10.2

ASIA PACIFIC

10.2.1

CHINA

10.2.1.1

Thriving chemical and automotive sectors to propel market

10.2.2

JAPAN

10.2.2.1

Automotive sector to drive demand

10.2.3

INDIA

10.2.3.1

Government initiatives for renewable energy to support market growth

10.2.4

SOUTH KOREA

10.2.4.1

Thriving automotive & chemical industry to drive market

10.2.5

REST OF ASIA PACIFIC

10.3

NORTH AMERICA

10.3.1

US

10.3.1.1

Increasing demand for renewable energy to drive market

10.3.2

CANADA

10.3.2.1

Focus on renewable energy sector to drive demand

10.3.3

MEXICO

10.3.3.1

Thriving petrochemical and automotive manufacturing sectors to propel market

10.4

EUROPE

10.4.1

GERMANY

10.4.1.1

Strong manufacturing sector to drive growth

10.4.2

ITALY

10.4.2.1

Established manufacturing and food & beverages sectors to drive market

10.4.3

FRANCE

10.4.3.1

Technological & sustainability initiatives to drive market

10.4.4

UK

10.4.4.1

Focus on renewable energy sector and commitment to circular economy to drive market

10.4.5

SPAIN

10.4.5.1

Government initiatives for renewable energy sector to drive demand

10.4.6

REST OF EUROPE

10.5

MIDDLE EAST & AFRICA

10.5.1

GCC COUNTRIES

10.5.1.1

UAE

10.5.1.2

Saudi Arabia

10.5.1.3

Rest of GCC countries

10.5.2

SOUTH AFRICA

10.5.2.1

Burgeoning industrial sector, coupled with government schemes, to drive market

10.5.3

REST OF MIDDLE EAST & AFRICA

10.6

SOUTH AMERICA

10.6.1

ARGENTINA

10.6.1.1

Government initiatives to drive demand

10.6.2

BRAZIL

10.6.2.1

Diverse industrial landscape to drive market

10.6.3

REST OF SOUTH AMERICA

11

COMPETITIVE LANDSCAPE

Discover leading strategies and emerging players reshaping the competitive landscape in 2024.

189

11.1

INTRODUCTION

11.2

KEY PLAYER STRATEGIES/RIGHT TO WIN

11.3

MARKET SHARE ANALYSIS

11.4

REVENUE ANALYSIS

11.5

BRAND/PRODUCT COMPARATIVE ANALYSIS

11.6

COMPANY EVALUATION MATRIX, 2024

11.6.1

STARS

11.6.2

EMERGING LEADERS

11.6.3

PERVASIVE PLAYERS

11.6.4

PARTICIPANTS

11.6.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.6.5.1

Product type footprint

11.6.5.2

End-use industry footprint

11.6.5.3

Region footprint

11.7

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

11.7.1

PROGRESSIVE COMPANIES

11.7.2

RESPONSIVE COMPANIES

11.7.3

DYNAMIC COMPANIES

11.7.4

STARTING BLOCKS

11.7.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES

11.7.5.1

Detailed list of key startups/SMEs

11.7.5.2

Competitive benchmarking of key startups/SMEs

11.8

COMPANY VALUATION AND FINANCIAL METRICS

11.9

COMPETITIVE SCENARIO

11.9.1

PRODUCT LAUNCHES

11.9.2

DEALS

11.9.3

EXPANSIONS

12

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

209

12.1

KEY PLAYERS

12.1.1

DOW

12.1.1.1

Business overview

12.1.1.2

Products/Solutions/Services offered

12.1.1.3

Recent developments

12.1.1.4

MnM view

12.1.2

EASTMAN CHEMICAL COMPANY

12.1.3

EXXON MOBIL CORPORATION

12.1.4

CHEVRON CORPORATION

12.1.5

HUNTSMAN CORPORATION

12.1.6

SHELL PLC

12.1.7

LANXESS

12.1.8

CLARIANT

12.1.9

WACKER CHEMIE AG

12.1.10

INDIAN OIL CORPORATION LTD.

12.1.11

SCHULTZ CANADA CHEMICALS LTD.

12.2

OTHER PLAYERS

12.2.1

PARATHERM

12.2.2

ARKEMA

12.2.3

BASF SE

12.2.4

DALIAN RICHFORTUNE CHEMICALS CO., LTD.

12.2.5

BRITISH PETROLEUM

12.2.6

DUPONT TATE & LYLE BIOPRODUCTS COMPANY LLC

12.2.7

DYNALENE

12.2.8

HINDUSTAN PETROLEUM CORPORATION LIMITED

12.2.9

GLOBAL HEAT TRANSFER LTD.

12.2.10

ISEL

12.2.11

PARAS LUBRICANTS LTD.

12.2.12

PETRO-CANADA LUBRICANTS, INC.

12.2.13

PHILLIPS 66 COMPANY

12.2.14

RADCO INDUSTRIES, INC.

12.2.15

SCHAEFFER MANUFACTURING CO.

13

APPENDIX

253

13.1

DISCUSSION GUIDE

13.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

13.3

CUSTOMIZATION OPTIONS

13.4

RELATED REPORTS

13.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

AVERAGE SELLING PRICE TREND OF HEAT TRANSFER FLUIDS, BY REGION, 2021–2024 (USD/KILOTON)

TABLE 2

AVERAGE SELLING PRICE TREND, BY PRODUCT TYPE, 2021–2024 (USD/KILOTON)

TABLE 3

AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PRODUCT TYPE, 2021–2024 (USD/KILOTON)

TABLE 4

HEAT TRANSFER FLUIDS MARKET: ROLE OF PLAYERS IN ECOSYSTEM

TABLE 5

KEY TECHNOLOGIES IN HEAT TRANSFER FLUIDS MARKET

TABLE 6

COMPLEMENTARY TECHNOLOGIES IN HEAT TRANSFER FLUIDS MARKET

TABLE 7

ADJACENT TECHNOLOGIES IN HEAT TRANSFER FLUIDS MARKET

TABLE 8

HEAT TRANSFER FLUIDS MARKET: TOTAL NUMBER OF PATENTS

TABLE 9

HEAT TRANSFER FLUIDS MARKET: LIST OF MAJOR PATENT OWNERS

TABLE 10

HEAT TRANSFER FLUIDS MARKET: LIST OF MAJOR PATENTS, 2018–2024

TABLE 11

HEAT TRANSFER FLUIDS MARKET: LIST OF KEY CONFERENCES & EVENTS, 2025–2026

TABLE 12

TARIFF RATES ASSOCIATED WITH HEAT TRANSFER FLUIDS MARKET

TABLE 13

NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 14

ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 15

EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 16

MIDDLE EAST AND AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 17

SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 18

LIST OF REGULATIONS FOR HEAT TRANSFER FLUIDS MARKET

TABLE 19

HEAT TRANSFER FLUIDS MARKET: PORTER’S FIVE FORCES ANALYSIS

TABLE 20

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

TABLE 21

KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

TABLE 22

GDP TRENDS AND FORECASTS, BY COUNTRY, 2023–2025 (USD MILLION)

TABLE 23

HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 24

HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 25

HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (KILOTON)

TABLE 26

HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (KILOTON)

TABLE 27

HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (USD MILLION)

TABLE 28

HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (USD MILLION)

TABLE 29

HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (KILOTON)

TABLE 30

HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (KILOTON)

TABLE 31

HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 32

HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 33

HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 34

HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 35

HEAT TRANSFER FLUIDS MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 36

HEAT TRANSFER FLUIDS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 37

HEAT TRANSFER FLUIDS MARKET, BY REGION, 2021–2024 (KILOTON)

TABLE 38

HEAT TRANSFER FLUIDS MARKET, BY REGION, 2025–2030 (KILOTON)

TABLE 39

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 40

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 41

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (KILOTON)

TABLE 42

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (KILOTON)

TABLE 43

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 44

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 45

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (KILOTON)

TABLE 46

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (KILOTON)

TABLE 47

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (USD MILLION)

TABLE 48

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (USD MILLION)

TABLE 49

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (KILOTON)

TABLE 50

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (KILOTON)

TABLE 51

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 52

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 53

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 54

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 55

CHINA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 56

CHINA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 57

CHINA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 58

CHINA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 59

JAPAN: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 60

JAPAN: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 61

JAPAN: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 62

JAPAN: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 63

INDIA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 64

INDIA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 65

INDIA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 66

INDIA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 67

SOUTH KOREA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 68

SOUTH KOREA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 69

SOUTH KOREA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 70

SOUTH KOREA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 71

REST OF ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 72

REST OF ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 73

REST OF ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 74

REST OF ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 75

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 76

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 77

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (KILOTON)

TABLE 78

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (KILOTON)

TABLE 79

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 80

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 81

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (KILOTON)

TABLE 82

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (KILOTON)

TABLE 83

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (USD MILLION)

TABLE 84

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (USD MILLION)

TABLE 85

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (KILOTON)

TABLE 86

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (KILOTON)

TABLE 87

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 88

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 89

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 90

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 91

US: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 92

US: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 93

US: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 94

US: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 95

CANADA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 96

CANADA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 97

CANADA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 98

CANADA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 99

MEXICO: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 100

MEXICO: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 101

MEXICO: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 102

MEXICO: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 103

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 104

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 105

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (KILOTON)

TABLE 106

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (KILOTON)

TABLE 107

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 108

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 109

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (KILOTON)

TABLE 110

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (KILOTON)

TABLE 111

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (USD MILLION)

TABLE 112

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (USD MILLION)

TABLE 113

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (KILOTON)

TABLE 114

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (KILOTON)

TABLE 115

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 116

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 117

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 118

EUROPE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 119

GERMANY: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 120

GERMANY: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 121

GERMANY: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 122

GERMANY: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 123

ITALY: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 124

ITALY: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 125

ITALY: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 126

ITALY: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 127

FRANCE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 128

FRANCE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 129

FRANCE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 130

FRANCE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 131

UK: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 132

UK: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 133

UK: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 134

UK: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 135

SPAIN: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 136

SPAIN: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 137

SPAIN: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 138

SPAIN: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 139

REST OF EUROPE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 140

REST OF EUROPE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 141

REST OF EUROPE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 142

REST OF EUROPE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 143

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 144

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 145

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (KILOTON)

TABLE 146

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (KILOTON)

TABLE 147

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 148

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 149

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (KILOTON)

TABLE 150

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (KILOTON)

TABLE 151

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (USD MILLION)

TABLE 152

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (USD MILLION)

TABLE 153

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (KILOTON)

TABLE 154

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (KILOTON)

TABLE 155

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 156

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 157

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 158

MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 159

UAE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 160

UAE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 161

UAE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 162

UAE: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 163

SAUDI ARABIA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 164

SAUDI ARABIA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY,2025–2030 (USD MILLION)

TABLE 165

SAUDI ARABIA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 166

SAUDI ARABIA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 167

REST OF GCC COUNTRIES: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 168

REST OF GCC COUNTRIES: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 169

REST OF GCC COUNTRIES: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 170

REST OF GCC COUNTRIES: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 171

SOUTH AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 172

SOUTH AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 173

SOUTH AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 174

SOUTH AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 175

REST OF MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 176

REST OF MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 177

REST OF MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 178

REST OF MIDDLE EAST & AFRICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 179

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 180

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 181

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2021–2024 (KILOTON)

TABLE 182

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY COUNTRY, 2025–2030 (KILOTON)

TABLE 183

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 184

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 185

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2021–2024 (KILOTON)

TABLE 186

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY PRODUCT TYPE, 2025–2030 (KILOTON)

TABLE 187

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (USD MILLION)

TABLE 188

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (USD MILLION)

TABLE 189

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2021–2024 (KILOTON)

TABLE 190

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY TEMPERATURE, 2025–2030 (KILOTON)

TABLE 191

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 192

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 193

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 194

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 195

ARGENTINA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 196

ARGENTINA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 197

ARGENTINA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 198

ARGENTINA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 199

BRAZIL: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 200

BRAZIL: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 201

BRAZIL: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 202

BRAZIL: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 203

REST OF SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (USD MILLION)

TABLE 204

REST OF SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (USD MILLION)

TABLE 205

REST OF SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2021–2024 (KILOTON)

TABLE 206

REST OF SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET, BY END-USE INDUSTRY, 2025–2030 (KILOTON)

TABLE 207

OVERVIEW OF STRATEGIES ADOPTED BY KEY HEAT TRANSFER FLUID MANUFACTURERS

TABLE 208

HEAT TRANSFER FLUIDS MARKET: DEGREE OF COMPETITION

TABLE 209

HEAT TRANSFER FLUIDS MARKET: PRODUCT TYPE FOOTPRINT

TABLE 210

HEAT TRANSFER FLUIDS MARKET: END-USE INDUSTRY FOOTPRINT

TABLE 211

HEAT TRANSFER FLUIDS MARKET: REGION FOOTPRINT

TABLE 212

HEAT TRANSFER FLUIDS MARKET: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 213

HEAT TRANSFER FLUIDS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (1/2)

TABLE 214

HEAT TRANSFER FLUIDS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (2/2)

TABLE 215

HEAT TRANSFER FLUIDS MARKET: PRODUCT LAUNCHES, JANUARY 2020–JULY 2025

TABLE 216

HEAT TRANSFER FLUIDS MARKET: DEALS, JANUARY 2020–JULY 2025

TABLE 217

HEAT TRANSFER FLUIDS MARKET: EXPANSIONS, JANUARY 2020–JULY 2025

TABLE 218

DOW: COMPANY OVERVIEW

TABLE 219

DOW: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 220

DOW: DEALS

TABLE 221

EASTMAN CHEMICAL COMPANY: COMPANY OVERVIEW

TABLE 222

EASTMAN CHEMICAL COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 223

EASTMAN CHEMICAL COMPANY: PRODUCT LAUNCHES

TABLE 224

EASTMAN CHEMICAL COMPANY: DEALS

TABLE 225

EASTMAN CHEMICAL COMPANY: EXPANSIONS

TABLE 226

EXXON MOBIL CORPORATION: COMPANY OVERVIEW

TABLE 227

EXXON MOBIL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 228

CHEVRON CORPORATION: COMPANY OVERVIEW

TABLE 229

CHEVRON CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 230

CHEVRON CORPORATION: DEALS

TABLE 231

HUNTSMAN CORPORATION: COMPANY OVERVIEW

TABLE 232

HUNTSMAN CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 233

SHELL PLC: COMPANY OVERVIEW

TABLE 234

SHELL PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 235

SHELL PLC: DEALS

TABLE 236

LANXESS: COMPANY OVERVIEW

TABLE 237

LANXESS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 238

CLARIANT: COMPANY OVERVIEW

TABLE 239

CLARIANT: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 240

WACKER CHEMIE AG: COMPANY OVERVIEW

TABLE 241

WACKER CHEMIE AG: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 242

INDIAN OIL CORPORATION LTD.: COMPANY OVERVIEW

TABLE 243

INDIAN OIL CORPORATION LTD.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 244

SCHULTZ CANADA CHEMICALS LTD.: COMPANY OVERVIEW

TABLE 245

SCHULTZ CANADA CHEMICALS LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 246

PARATHERM: COMPANY OVERVIEW

TABLE 247

ARKEMA: COMPANY OVERVIEW

TABLE 248

BASF SE: COMPANY OVERVIEW

TABLE 249

DALIAN RICHFORTUNE CHEMICALS CO., LTD.: COMPANY OVERVIEW

TABLE 250

BRITISH PETROLEUM: COMPANY OVERVIEW

TABLE 251

DUPONT TATE & LYLE BIOPRODUCTS COMPANY LLC: COMPANY OVERVIEW

TABLE 252

DYNALENE: COMPANY OVERVIEW

TABLE 253

HINDUSTAN PETROLEUM CORPORATION LIMITED: COMPANY OVERVIEW

TABLE 254

GLOBAL HEAT TRANSFER LTD.: COMPANY OVERVIEW

TABLE 255

ISEL: COMPANY OVERVIEW

TABLE 256

PARAS LUBRICANTS LTD.: COMPANY OVERVIEW

TABLE 257

PETRO-CANADA LUBRICANTS, INC.: COMPANY OVERVIEW

TABLE 258

PHILLIPS 66 COMPANY: COMPANY OVERVIEW

TABLE 259

RADCO INDUSTRIES, INC.: COMPANY OVERVIEW

TABLE 260

SCHAEFFER MANUFACTURING CO.: COMPANY OVERVIEW

LIST OF FIGURES

FIGURE 1

HEAT TRANSFER FLUIDS MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

HEAT TRANSFER FLUIDS MARKET: RESEARCH DESIGN

FIGURE 3

MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE APPROACH

FIGURE 4

MARKET SIZE ESTIMATION METHODOLOGY: DEMAND-SIDE APPROACH

FIGURE 5

MARKET SIZE ESTIMATION METHODOLOGY: REVENUE OF MARKET PLAYERS

FIGURE 6

MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

FIGURE 7

MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

FIGURE 8

HEAT TRANSFER FLUIDS MARKET: DATA TRIANGULATION

FIGURE 9

MINERAL OILS SEGMENT TO DOMINATE MARKET IN 2025

FIGURE 10

LOW-TEMPERATURE SEGMENT WILL DOMINATE MARKET DURING STUDY PERIOD

FIGURE 11

CHEMICAL & PETROCHEMICAL INDUSTRY SEGMENT TO LEAD MARKET IN 2025

FIGURE 12

ASIA PACIFIC TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 13

EXPANSION IN RENEWABLE AND INDUSTRIAL HEAT APPLICATIONS TO DRIVE MARKET

FIGURE 14

SYNTHETIC FLUIDS TO REGISTER FASTEST GROWTH DURING FORECAST PERIOD

FIGURE 15

LOW TEMPERATURE TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

FIGURE 16

RENEWABLE ENERGY SEGMENT TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

FIGURE 17

CHINA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 18

HEAT TRANSFER FLUIDS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 19

USE OF GENERATIVE AI IN HEAT TRANSFER FLUIDS MARKET

FIGURE 20

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 21

HEAT TRANSFER FLUIDS MARKET: SUPPLY CHAIN ANALYSIS

FIGURE 22

AVERAGE SELLING PRICE TREND OF HEAT TRANSFER FLUIDS, BY REGION, 2021–2024 (USD/KILOTON)

FIGURE 23

AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PRODUCT TYPE, 2021–2024

FIGURE 24

HEAT TRANSFER FLUIDS MARKET: INVESTMENT AND FUNDING SCENARIO

FIGURE 25

HEAT TRANSFER FLUIDS MARKET: ECOSYSTEM

FIGURE 26

NUMBER OF PATENTS GRANTED, 2015−2024

FIGURE 27

HEAT TRANSFER FLUIDS MARKET: LEGAL STATUS OF PATENTS

FIGURE 28

PATENT ANALYSIS FOR HEAT TRANSFER FLUIDS, BY JURISDICTION, 2015−2024

FIGURE 29

TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENTS IN LAST 10 YEARS

FIGURE 30

IMPORT OF HS CODE 841950-COMPLIANT PRODUCTS, BY COUNTRY, 2021–2024 (USD THOUSAND)

FIGURE 31

EXPORT OF HS CODE 841950-COMPLIANT PRODUCTS, BY COUNTRY, 2021–2024 (USD THOUSAND)

FIGURE 32

PORTER’S FIVE FORCES ANALYSIS: HEAT TRANSFER FLUIDS MARKET

FIGURE 33

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

FIGURE 34

KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

FIGURE 35

MINERAL OILS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 36

LOW TEMPERATURE SEGMENT TO LEAD HEAT TRANSFER FLUIDS MARKET IN 2024

FIGURE 37

CHEMICAL & PETROCHEMICALS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

FIGURE 38

ASIA PACIFIC TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

FIGURE 39

ASIA PACIFIC: HEAT TRANSFER FLUIDS MARKET SNAPSHOT

FIGURE 40

NORTH AMERICA: HEAT TRANSFER FLUIDS MARKET SNAPSHOT

FIGURE 41

EUROPE: HEAT TRANSFER FLUIDS MARKET SNAPSHOT

FIGURE 42

MIDDLE EAST AND AFRICA: HEAT TRANSFER FLUIDS MARKET SNAPSHOT

FIGURE 43

SOUTH AMERICA: HEAT TRANSFER FLUIDS MARKET SNAPSHOT

FIGURE 44

HEAT TRANSFER FLUIDS MARKET SHARE OF KEY PLAYERS, 2024

FIGURE 45

HEAT TRANSFER FLUIDS MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2021–2025 (USD BILLION)

FIGURE 46

HEAT TRANSFER FLUIDS MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS

FIGURE 47

HEAT TRANSFER FLUIDS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 48

HEAT TRANSFER FLUIDS MARKET: COMPANY FOOTPRINT

FIGURE 49

HEAT TRANSFER FLUIDS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 50

EV/EBITDA OF KEY VENDORS

FIGURE 51

YEAR-TO-DATE (YTD) PRICE TOTAL RETURN

FIGURE 52

DOW: COMPANY SNAPSHOT

FIGURE 53

EASTMAN CHEMICAL COMPANY: COMPANY SNAPSHOT

FIGURE 54

EXXON MOBIL CORPORATION: COMPANY SNAPSHOT

FIGURE 55

CHEVRON CORPORATION: COMPANY SNAPSHOT

FIGURE 56

HUNTSMAN CORPORATION: COMPANY SNAPSHOT

FIGURE 57

SHELL PLC: COMPANY SNAPSHOT

FIGURE 58

LANXESS: COMPANY SNAPSHOT

FIGURE 59

CLARIANT: COMPANY SNAPSHOT

Methodology

The study involved four main activities to estimate the market size of the heat transfer fluids market. Extensive secondary research was conducted to gather information on the market, peer, and parent markets. The next step was to validate these findings, assumptions, and estimates with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were used to determine the overall market size. Subsequently, market breakdown and data triangulation methods were applied to estimate the sizes of segments and subsegments.

Secondary Research

In the secondary research process, various sources were referenced to identify and gather information for this study. These sources include annual reports, press releases, investor presentations, white papers, verified publications, trade directories, articles from reputable authors, trusted websites, and databases. Secondary research was used to gather essential details about the industry’s value chain, the market’s monetary chain, the overall market for key heat transfer fluids, their classification, and segmentation based on industry trends down to the regional level. It also provided insights into major developments from a market-oriented perspective.

Primary Research

The heat transfer fluids market involves several stakeholders in the value chain, including raw material suppliers, manufacturers, and end users. Various primary sources from both the supply and demand sides of the heat transfer fluids market have been interviewed to gather both qualitative and quantitative information. Key opinion leaders in end-use sectors serve as primary demand-side interviewees. On the supply side, primary sources include manufacturers, associations, and institutions involved in the heat transfer fluids industry.

Primary interviews were conducted to gather insights such as market statistics, data on revenue generated from products and services, market breakdowns, market size estimates, market forecasting, and data triangulation. Primary research also helped in understanding various trends related to product type, temperature, end-use industry, application, and region. Stakeholders from the demand side, such as CIOs, CTOs, and CSOs, were interviewed to understand the buyer’s perspective on suppliers, products, component providers, and their current and future use of the heat transfer fluids market, which will influence the overall market.

The breakdown of profiles of the primary interviewees is illustrated in the figure below:

Note: Tier 1, Tier 2, and Tier 3 companies are classified based on their market revenue in 2024 available in the public domain, product portfolios, and geographical presence.

Other designations include sales representatives, production heads, and technicians.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

The top-down approach was used to estimate and validate the size of various submarkets for the heat transfer fluids market. The research methodology used to estimate the market size included the following steps:

- The key players in the industry have been identified through extensive secondary research.

- The supply chain of the industry has been mapped through both primary and secondary research.

- All percentage shares, splits, and breakdowns based on product type, temperature, application, end-use industry, and region were determined using secondary sources and verified through primary sources.

- All potential parameters influencing the markets covered in this study were thoroughly examined, validated through primary research, and analyzed to obtain final quantitative and qualitative data. This data was compiled, enriched with detailed inputs and analysis, and presented in this report.

Data Triangulation

After estimating the total market size for heat transfer fluids, the overall market has been divided into several segments and sub-segments. Data triangulation and market breakdown methods have been used where applicable to complete the market analysis and obtain accurate data for all parts. The data was triangulated by examining various factors and trends from both demand and supply sides. Additionally, the market size was validated using both top-down and bottom-up approaches, along with primary interviews. For each data segment, three sources were used—top-down approach, bottom-up approach, and expert interviews. The data was considered accurate when the values from these three sources matched.

Market Definition

Heat transfer fluids (HTFs) are specialized liquids or gases designed to transfer thermal energy efficiently between systems, components, or processes. They ensure precise heating, cooling, or temperature regulation in applications where direct heat exchange is impractical or unsafe. Built to operate across a wide temperature range from cryogenic to extremely high temperatures, they maintain stability, safety, and efficiency. This makes them essential in industries such as chemicals, oil and gas, food and beverage, pharmaceuticals, automotive, HVAC, and renewable energy.

The heat transfer fluids market has a wide global reach, with Asia Pacific leading due to high automotive production and significant construction activity in countries like China, India, Japan, and South Korea. North America and Europe are the next largest markets, driven by technological advancements, infrastructure investments, and essential environmental and safety regulations. Additionally, some emerging markets in South America and the Middle East & Africa are experiencing moderate growth due to urbanization and increased industrial uses.

Stakeholders

- Heat transfer fluid manufacturers

- Heat transfer fluid traders, distributors, and suppliers

- Raw material suppliers

- Government and private research organizations

- Associations and industrial bodies

- R&D institutions

- Environmental support agencies

Report Objectives

- To define, describe, and forecast the size of the heat transfer fluids market, in terms of value and volume

- To provide detailed information regarding the major factors (drivers, opportunities, restraints, and challenges) influencing the growth of the market

- To estimate and forecast the market size based on product type, temperature, application, end-use industry, and region

- To forecast the size of the market with respect to major regions, namely, North America, Europe, the Middle East & Africa, and South America, along with their key countries

- To strategically analyze micromarkets with respect to individual growth trends, prospects, and their contribution to the overall market

- To analyze opportunities in the market for stakeholders and provide a competitive landscape of market leaders

- To track and analyze recent developments such as partnerships, agreements, joint ventures, collaborations, announcements, awards, and expansions in the market

- To strategically profile key market players and comprehensively analyze their core competencies

Key Questions Addressed by the Report

What is the expected growth rate of the heat transfer fluids market?

The market is expected to grow at a CAGR of 4.3% in terms of value during the forecast period.

Who are the key players in the heat transfer fluids market?

Leading players include Dow (US), Eastman Chemical Company (US), ExxonMobil (US), Chevron Corporation (US), Huntsman Corporation (US), Shell PLC (UK), Lanxess (Germany), Clariant (Switzerland), Wacker Chemie AG (Germany), Indian Oil Corporation Ltd. (India), and Schultz Canada Chemicals Ltd. (Canada).

What are the emerging trends in the heat transfer fluids market?

Key trends include the development of high-performance synthetic fluids, increased adoption of bio-based and environmentally friendly fluids, integration of advanced monitoring systems for real-time performance tracking, and growing use of HTFs in renewable energy applications such as solar and wind power.

What are the drivers and opportunities for the heat transfer fluids market?

The market is driven by global industrialization and urbanization, demand for energy-efficient solutions, and advancements in HTF technologies. Opportunities arise from the growing renewable energy sector and supportive government initiatives.

What are the restraining factors in the heat transfer fluids market?

Stringent regulatory requirements and volatility in raw material prices are key factors restraining market growth.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Heat Transfer Fluids Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

We at Nissan Chemicals Corporation have been clients of MarketsandMarkets for more than a year now. We recently consulted MarketsandMarkets for a study, the team at MarketsandMarkets was extremely professional and organized. The business insights were very detailed and aligned well with our expectations that really helped us formulate the Business Plans and device new strategies for development themes. MarketsandMarkets offers a unique combination of expertise and dedicated engagement model. Their research findings have helped us in designing our Pricing Strategy which will make it easier for us to predict the future sales and profits for the next ten years. We look forward to working with MarketsandMarkets in the future.

VP of Strategy & New Business Development

Leading Specialty Chemical Company

The MarketsandMarkets Engagement Model, composed of both the Knowledge Store and advisory custom research, has greatly helped us in understanding our markets and making strategic decisions. The Knowledge Store is a fast way to allow everyone in our organization to understand more about most any market they are interested in. The ability to then get custom research done and get answers to specific strategic questions and market insight has been spectacular. The Markets and Markets team feel more like colleagues than vendors and their services have helped us change our culture where statements of things like growth opportunities and competitive position are always backed by industry research.

Rich Gibson,

Director, Corporate Strategy

Milliken & Company,

Leading Industrial Manufacturer of specialty chemical, floor covering, performance and protective textile materials, and healthcaremilliken.com

MarketsandMarkets is a trusted resource that helps us to better understand markets that are near-adjacencies-whether its technology, value chain or geography. Their Knowledge Store platform provides a dashboard of markets and their characteristics which is easy to use and saves us time.

Adam Shaw,

Market Development and Strategy Manager

AdvanSix Inc. USA,

An American Leader in Chemicalswww.advansix.com

The Knowledge Store from MarketsandMarkets is a valuable tool which has helped my team acquire greater insight in to the end markets that our business serves. This has enabled us to help our company build stronger strategies throughout our planning process.

TOSHIO KINOSHITA

Senior Chif Consultion Research & Consulting Division

Mitsubishi Chemical Research Corporation,

Leading Manufacturer of Chemical Productswww.mitsubishichem-res.co.jp/en/

We recently engaged with MarketsandMarkets for a study, the team not only clearly understood our business objectives but was also extremely professional in the way they handled the entire project. The study was efficiently conducted in a phase-wise manner, and the engagement model furnished us with high-quality business insights that far exceeded our expectations at each phase. We were especially happy that MarketsandMarkets could provide us with both, an English as well as a Japanese version of the study. A special thanks to the Analyst Team and Client Services Team, whose fluency in Japanese enhanced our comfort level, as we could converse with them in our preferred language.

Independent entrepreneurs

Arrow Precision

We approached MarketsandMarkets for study on Proppants Market, and their work exceeded our expectations. The study conducted was comprehensive and enabled us to view the market through the various dimensions. In addition, the team was extraordinarily responsive throughout the process and resolved our queries on time. I strongly recommend MarketsandMarkets and will certainly consider them for additional market assessments we will need in the future.

Global engineering company, Japan

Deputy Manager,

Strategic Planning OfficeThe high-quality insights shared by the MarketsandMarkets team helped us understand the pharmaceutical plant designers in a specific geography. It also captured the risks that we may likely face in communicating with our potential partners. The study would enable us identify partners, which would impact our future growth.

- China Heat Transfer Fluids Market

- Japan Heat Transfer Fluids Market

- India Heat Transfer Fluids Market

- South Korea Heat Transfer Fluids Market

- Canada Heat Transfer Fluids Market

- Mexico Heat Transfer Fluids Market

- US Heat Transfer Fluids Market

- Germany Heat Transfer Fluids Market

- Italy Heat Transfer Fluids Market

- France Heat Transfer Fluids Market

- UK Heat Transfer Fluids Market

- Spain Heat Transfer Fluids Market

- UAE Heat Transfer Fluids Market

- Saudi Arabia Heat Transfer Fluids Market

- South Africa Heat Transfer Fluids Market

- Argentina Heat Transfer Fluids Market

- Brazil Heat Transfer Fluids Market

- South America Heat Transfer Fluids Market

- Rest Of Europe Heat Transfer Fluids Market

- Rest Of Asia Pacific Heat Transfer Fluids Market

- GCC Countries Heat Transfer Fluids Market

- �Rest Of GCC Countries Heat Transfer Fluids Market

- Rest Of South America Heat Transfer Fluids Market

Growth opportunities and latent adjacency in Heat Transfer Fluids Market

Caroline

Nov, 2017

Market overview and dynamics.

Seungyoon

Jun, 2019

General information on Heat Transfer Fluid and Synthetic market .

Caroline

Feb, 2016

General information on Heat Transfer Fluids Market.

Gabriella

Aug, 2019

General information on Heat Transfer Fluids.

Gabriella

Aug, 2019

Market growth trends and major company profiles along with the strategies adopted by key players present in the market.

Kevin

Dec, 2014

Heat transfer fluids by application segment, i.e. HVAC, Oil and Gas, Automotive, etc..

Roshan

Feb, 2019

General information on Heat Transfer Fluids in auomotive and power generation.

Levent

May, 2019

Detailed information of Heat Transfer Fluids Market.

Bruno

Apr, 2014

Glycol based thermal Fluids market.

Todd

Oct, 2014

General information on Heat Transfer Fluids in North America.

Miyuki

Jun, 2018

Interested in the report.

Ranjit

May, 2013

Interested in Heat (Cold) transfer fluids Market for low temp..