The Hidden Economics of AI in Healthcare: Who Actually Captures the Value?

The healthcare industry is standing at a fiscal crossroads. While much of the buzz surrounding Artificial Intelligence (AI) focuses on robotic surgeons and instant diagnoses, the real story is written in the balance sheets.

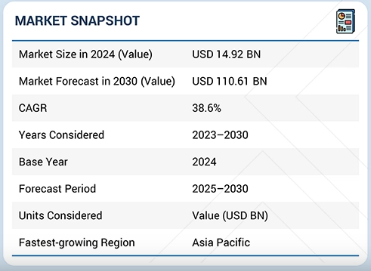

According to recent data from MarketsandMarkets, the AI in healthcare market is set to explode from USD 21.66 billion in 2025 to a staggering USD 110.61 billion by 2030. But in a landscape of 38.6% CAGR, a critical question remains: Who is actually pocketing the value?

1. The Tech Titans: Selling the "Picks and Shovels"

In every gold rush, the toolmakers win first. The "infrastructure layer" of healthcare AI is dominated by established giants.

-

Computing Power: Companies like NVIDIA provide the high-performance computing necessary for drug discovery and massive data processing.

-

The Cloud Gatekeepers:Microsoft Azure, Amazon Web Services (AWS), and Google capture value by hosting the "Cloud-Based Model," which is the fastest-growing deployment segment (41.7% CAGR) due to its scalability.

These players capture value regardless of whether a specific medical algorithm succeeds; they profit from the attempt to innovate.

2. Integrated Solution Providers: The Value of "One-Stop Shops"

The market is shifting away from fragmented tools toward Integrated Solutions. Segment leaders like Philips, Siemens Healthineers, and GE HealthCare capture value by embedding AI directly into the hardware and software hospitals already use.

By bundling AI with Electronic Health Records (EHR) and diagnostic imaging, these companies create "sticky" ecosystems. They don't just sell a tool; they sell a streamlined workflow that promises to solve the industry’s biggest bottleneck: doctor burnout and administrative bloat.

3. Healthcare Providers: Efficiency vs. Adoption Costs

Hospitals and clinics are the primary "End Users," and they capture value primarily through cost avoidance and early detection. * Early Diagnosis: The diagnosis and early detection segment is growing at nearly 40% because it improves survival rates and lowers long-term treatment expenses.

-

Administrative Relief: AI is being used to automate billing, scheduling, and documentation areas where hospitals historically lose billions to inefficiency.

However, the value capture here is dampened by reluctance among practitioners and a shortage of skilled AI professionals to manage these systems. For providers, the ROI is often a long game played against rising operational costs.

4. The Niche Disruptors: Precision and Specialization

While the titans handle the plumbing, startups like Qure.ai and Enlitic are carving out value in specialized niches. These companies capture value through unprecedented accuracy in specific functions like radiology, genomics, and immunotherapy. Their value proposition is clear: doing one thing significantly better than a human can, thereby reducing diagnostic errors a major liability and cost for the industry.

80% of the Forbes Global 2000 B2B companies rely on MarketsandMarkets to identify growth opportunities in emerging technologies and use cases that will have a positive revenue impact.

- Food Packaging Market Size Set for Strong Growth Through 2030 Amid Rising Demand for Convenience Foods

- Crop Protection Chemical Market Size, Share & Growth Forecast (2025�2030)

- Mulch Films Market: Driving Sustainable Agriculture Through Innovation

- Agricultural Adjuvants Market Analysis, Trends, and Growth Outlook (2026�2031)

- Japan Enterprise Asset Management Market Growth: AI and Smart Infrastructure Drive Demand

The Verdict: Where is the Value Flowing?

Currently, the value is heavily skewed toward integrated platform providers and cloud giants who control the data and the delivery systems. However, as the market matures toward 2030, the focus is shifting toward "Human-Aware AI." The ultimate winners will be those who can bridge the gap between "high-tech" and "high-touch" creating AI that doesn't just process data but actually collaborates with clinicians to deliver better patient outcomes at a lower price point.