TABLE OF CONTENTS

1 INTRODUCTION

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS (Page No. - 46)

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CYANOACRYLATE ADHESIVES MARKET

4.2 CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY

4.3 ASIA PACIFIC CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY AND COUNTRY

4.4 CYANOACRYLATE ADHESIVES MARKET: DEVELOPED VS. DEVELOPING ECONOMIES

4.5 CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY

5 MARKET OVERVIEW (Page No. - 49)

5.1 INTRODUCTION

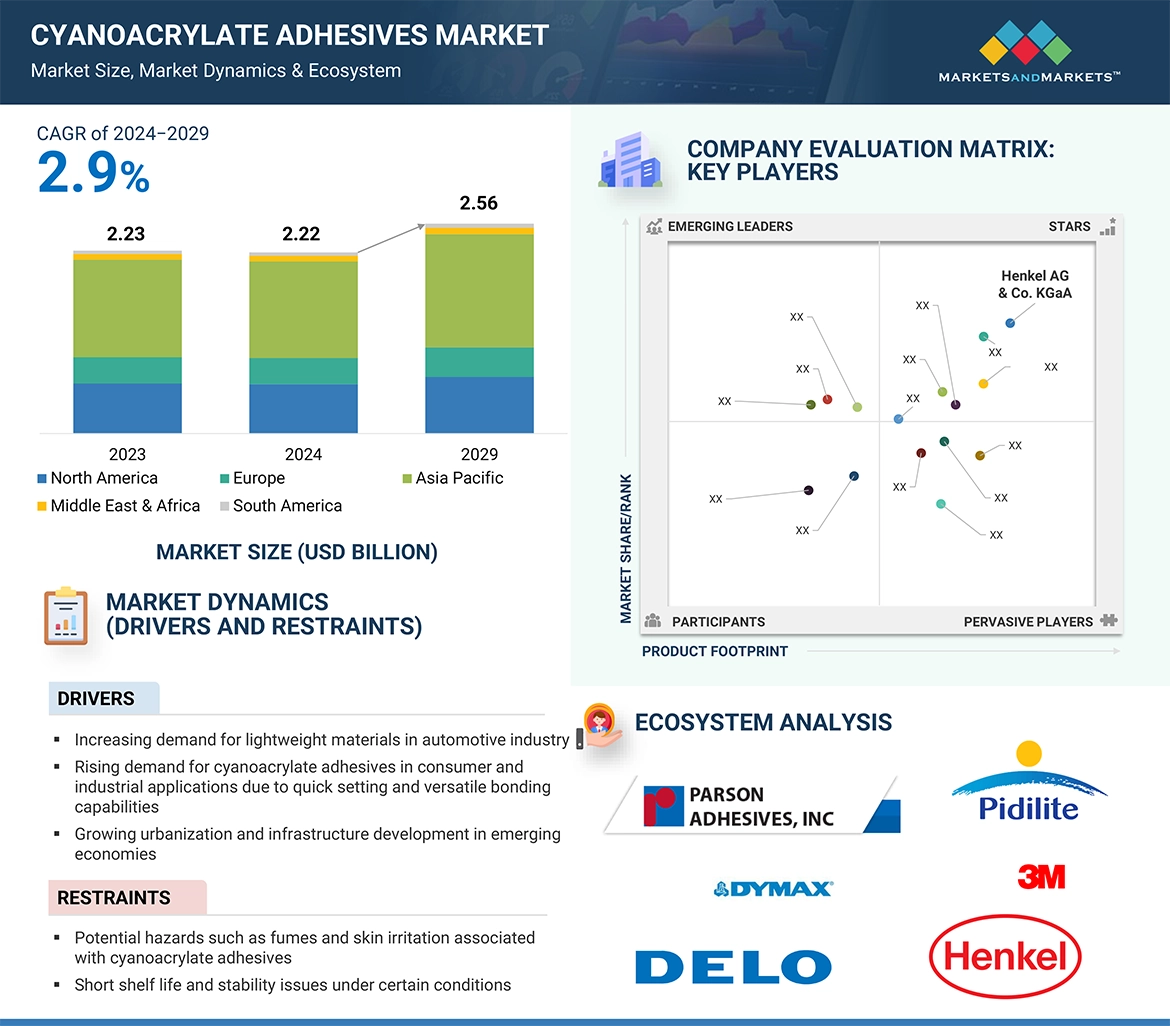

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Increasing demand for lightweight materials in automotive industry

5.2.1.2 Rising demand for cyanoacrylate adhesives in consumer and industrial applications due to quick setting and versatile bonding capabilities

5.2.1.3 Growing urbanization and infrastructure development in emerging economies

5.2.2 RESTRAINTS

5.2.2.1 Potential hazards such as fumes and skin irritation associated with cyanoacrylate adhesives

5.2.2.2 Short shelf life and stability issues under certain conditions

5.2.3 OPPORTUNITIES

5.2.3.1 Innovations in adhesive properties

5.2.3.2 Expanding medical and advanced electronics industries

5.2.4 CHALLENGES

5.2.4.1 Need to adhere to stringent safety and environmental regulations

5.3 PORTER’S FIVE FORCES ANALYSIS

5.3.1 THREAT OF NEW ENTRANTS

5.3.2 THREAT OF SUBSTITUTES

5.3.3 BARGAINING POWER OF BUYERS

5.3.4 BARGAINING POWER OF SUPPLIERS

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.4.2 BUYING CRITERIA

5.5 MACROECONOMIC INDICATORS

5.5.1 GDP TRENDS AND FORECAST

5.5.2 TRENDS IN CONSTRUCTION INDUSTRY

5.5.3 TRENDS IN AUTOMOTIVE INDUSTRY

5.6 SUPPLY CHAIN ANALYSIS

5.7 PRICING ANALYSIS

5.7.1 AVERAGE SELLING PRICE TREND, BY REGION

5.7.2 AVERAGE SELLING PRICE TREND, BY CHEMISTRY

5.7.3 AVERAGE SELLING PRICE TREND, BY CURING PROCESS

5.7.4 AVERAGE SELLING PRICE TREND, BY END-USE INDUSTRY

5.7.5 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY

5.8 TRADE ANALYSIS

5.8.1 EXPORT SCENARIO (HS CODE 350610)

5.8.2 IMPORT SCENARIO (HS CODE 350610)

5.9 REGULATORY LANDSCAPE

5.9.1 REGULATIONS IMPACTING CYANOACRYLATE ADHESIVES BUSINESS

5.9.1.1 Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) Regulation (European Union)

5.9.1.2 Globally Harmonized System (GHS) of Classification and Labelling of Chemicals

5.9.1.3 OSHA Regulations (US)

5.9.1.4 VOC Regulations (California Air Resources Board - CARB and EU Solvents Emissions Directive)

5.9.1.5 FDA Medical Device Regulations (US)

5.9.1.6 Food Contact Material Regulations (European Union)

5.9.1.7 Resource Conservation and Recovery Act (RCRA) and EU Waste Framework Directive

5.9.1.8 Consumer Product Safety Regulations (CPSA - US and EU General Product Safety Directive)

5.9.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.10 ECOSYSTEM ANALYSIS

5.11 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.12 INVESTMENT AND FUNDING SCENARIO

5.13 PATENT ANALYSIS

5.14 TECHNOLOGY ANALYSIS

5.14.1 KEY TECHNOLOGIES

5.14.1.1 Light-cured cyanoacrylates

5.14.1.2 Conventional cyanoacrylates

5.14.2 COMPLIMENTARY TECHNOLOGIES

5.14.2.1 Anaerobic adhesives

5.14.3 ADJACENT TECHNOLOGIES

5.14.3.1 Hybrid adhesives

5.14.3.2 Nanocomposites adhesives

5.15 IMPACT OF AI/GENERATIVE AI (GENAI) ON CYANOACRYLATE ADHESIVES MARKET

5.15.1 PRODUCT FORMULATION AND INNOVATION

5.15.2 PREDICTIVE MAINTENANCE AND PRODUCTION OPTIMIZATION

5.15.3 SUPPLY CHAIN OPTIMIZATION

5.15.4 SUSTAINABILITY AND ENVIRONMENTAL IMPACT REDUCTION

5.15.5 CUSTOMER-CENTRIC PRODUCT DESIGN

5.15.6 REGULATORY COMPLIANCE AND RISK MANAGEMENT

5.15.7 DIGITAL TWINS FOR PROCESS SIMULATION

5.16 MACROECONOMIC OUTLOOK IMPACTING MARKET GROWTH

5.16.1 RUSSIA–UKRAINE WAR

5.16.2 CHINA

5.16.2.1 Decreasing FDI conserving China’s growth trajectory

5.16.2.2 Environmental commitments

5.16.3 EUROPE

5.16.3.1 Energy crisis in Europe

5.16.4 CHOKEPOINTS THREATENING GLOBAL TRADE

5.16.5 OUTLOOK FOR CHEMICAL INDUSTRY

5.16.6 OPEC+ EXTENDS OIL OUTPUT CUTS INTO 2025

5.17 CASE STUDY ANALYSIS

5.17.1 CYANOACRYLATE GLUE EFFECTIVE FOR SMALL CORNEAL PERFORATION (<3 MM) IN CONNECTION WITH INFECTIOUS KERATITIS

5.17.2 CYANOACRYLATE ADHESIVES FOR SURGICAL APPLICATIONS

5.17.3 CYANOACRYLATE ADHESIVE AS ALTERNATIVE SOLUTION FOR MEMBRANE FIXATION IN GUIDED TISSUE REGENERATION

5.18 KEY CONFERENCES AND EVENTS, 2024–2025

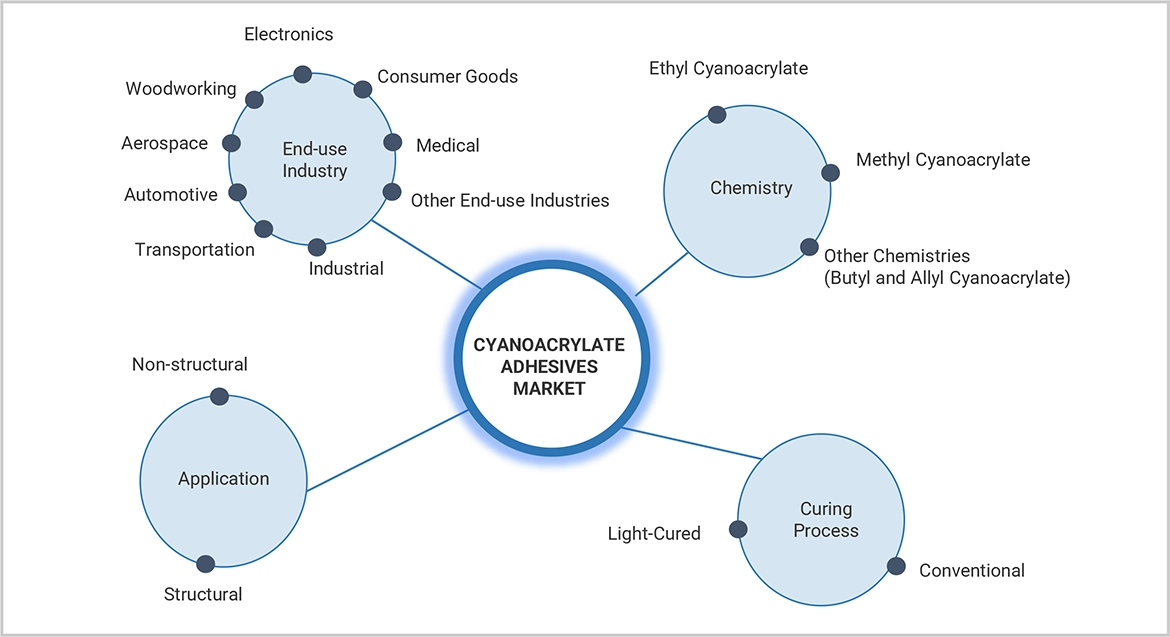

6 CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY (Page No. - 94)

6.1 INTRODUCTION

6.1.1 ETHYL CYANOACRYLATE (ECA)

6.1.1.1 Rising demand for rapid and efficient bonding solutions in various industries and sectors to propel market

6.1.2 METHYL CYANOACRYLATE (MCA)

6.1.2.1 Increasing applications in medical and industrial sectors to boost market growth

6.1.3 OTHER CHEMISTRIES

6.1.3.1 Allyl cyanoacrylate (ACA)

6.1.3.2 Butyl cyanoacrylate (BCA)

7 CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS (Page No. - 102)

7.1 INTRODUCTION

7.1.1 CONVENTIONAL

7.1.1.1 Fast curing time and strong initial adhesion to drive demand

7.1.2 LIGHT-CURED

7.1.2.1 Growing adoption of advanced cyanoacrylate adhesives in medical device industry to drive market

8 CYANOACRYLATE ADHESIVES MARKET, BY APPLICATION (Page No. - 107)

8.1 INTRODUCTION

8.2 STRUCTURAL

8.2.1 RISING DEMAND IN CONSTRUCTION AND MEDICAL INDUSTRIES TO BOOST MARKET GROWTH

8.3 NON-STRUCTURAL

8.3.1 RISING USE IN HOUSEHOLD AND MEDICAL APPLICATIONS TO DRIVE MARKET

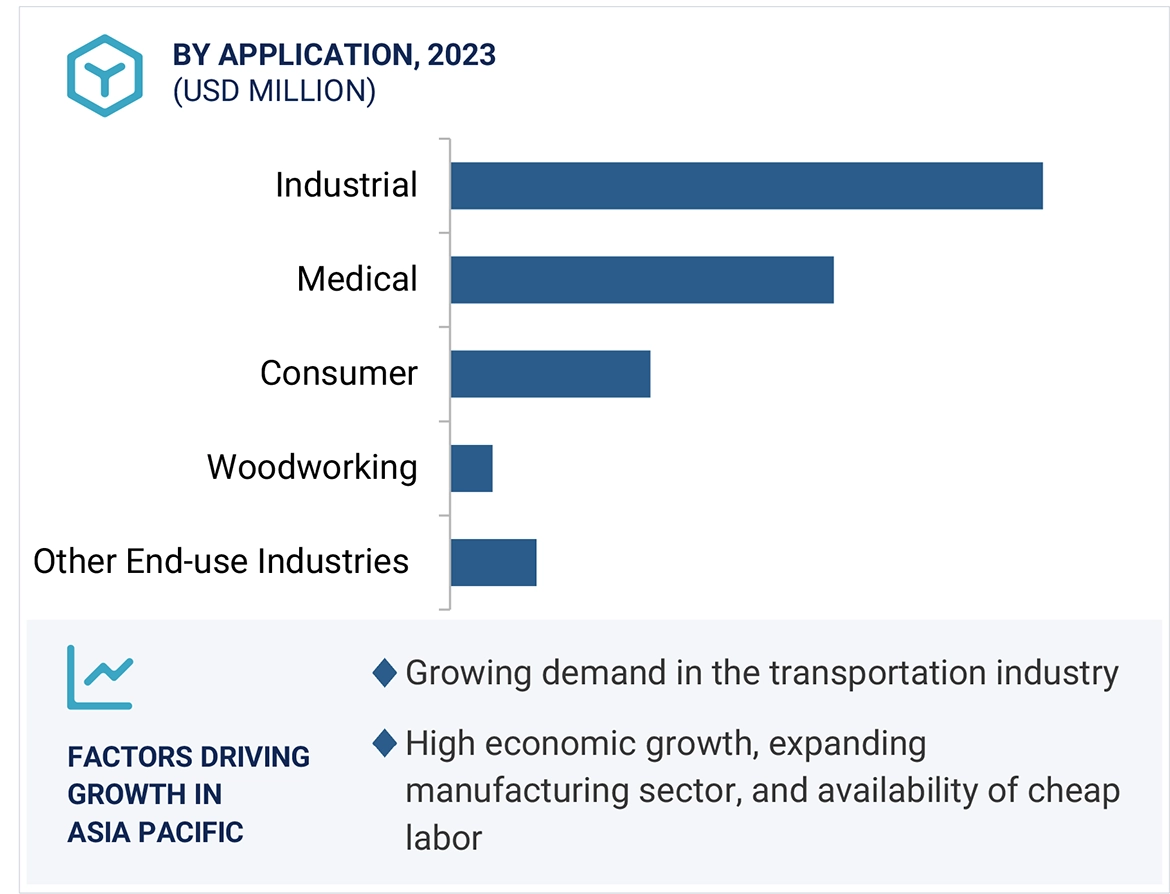

9 CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY (Page No. - 110)

9.1 INTRODUCTION

9.2 INDUSTRIAL

9.2.1 INCREASING DEMAND IN EMERGING ECONOMIES TO DRIVE MARKET

9.3 WOODWORKING

9.3.1 RISING CONSTRUCTION ACTIVITIES AND DEMAND FOR HIGH-PERFORMANCE ADHESIVES TO DRIVE MARKET

9.4 TRANSPORTATION

9.4.1 AUTOMOTIVE

9.4.1.1 Strategic advancements in automotive industry to fuel demand

9.4.2 AEROSPACE

9.4.2.1 Rise in maintenance, repair, and overhaul activities due to higher air travel and aircraft deliveries to propel demand

9.4.3 OTHER TRANSPORTATIONS

9.5 MEDICAL

9.5.1 ADVANCEMENTS IN MEDICAL SECTOR TO BOOST MARKET GROWTH

9.6 ELECTRONICS

9.6.1 INCREASING DEMAND FOR HIGH-PRECISION AND MINIATURIZED ELECTRONICS TO PROPEL MARKET

9.7 CONSUMER

9.7.1 RISING ADOPTION OF QUICK AND RELIABLE ADHESION SOLUTIONS TO FUEL MARKET GROWTH

9.8 OTHER END-USE INDUSTRIES

9.8.1 SIGNAGE & GRAPHICS

9.8.2 SPORTING GOODS

10 CYANOACRYLATE ADHESIVES MARKET, BY REGION (Page No. - 129)

10.1 INTRODUCTION

10.2 EUROPE

10.2.1 GERMANY

10.2.1.1 Rising innovations and digitalization in automotive sector to drive demand

10.2.2 UK

10.2.2.1 Rising demand for high-precision and durable wood products to fuel demand

10.2.3 FRANCE

10.2.3.1 High focus on innovation and research and development (R&D) in medical device industry to propel demand

10.2.4 ITALY

10.2.4.1 Expanding automotive sector to drive demand

10.2.5 TURKEY

10.2.5.1 Increasing domestic production of aircraft and defense systems to propel market

10.2.6 REST OF EUROPE

10.3 ASIA PACIFIC

10.3.1 CHINA

10.3.1.1 Technological advancements in manufacturing sector to propel market

10.3.2 INDIA

10.3.2.1 Booming electronics industry to fuel demand

10.3.3 JAPAN

10.3.3.1 Rising focus on sustainability and innovation in automotive industry to drive demand

10.3.4 SOUTH KOREA

10.3.4.1 Focus on enhancing domestic aircraft manufacturing and repair capabilities to drive market

10.3.5 INDONESIA

10.3.5.1 Surge in demand for advanced medical devices to boost market growth

10.3.6 VIETNAM

10.3.6.1 Booming manufacturing and consumer sectors to drive demand

10.3.7 REST OF ASIA PACIFIC

10.4 NORTH AMERICA

10.4.1 US

10.4.1.1 High economic growth to fuel demand

10.4.2 CANADA

10.4.2.1 Booming aerospace industry to drive market

10.4.3 MEXICO

10.4.3.1 Growing electric vehicle (EV) market to drive demand

10.5 MIDDLE EAST & AFRICA

10.5.1 GCC COUNTRIES

10.5.1.1 Saudi Arabia

10.5.1.1.1 Advancements in medical device industry to propel market

10.5.1.2 UAE

10.5.1.2.1 Rapid expansion and development of aerospace industry to fuel demand

10.5.1.3 Rest of GCC countries

10.5.2 SOUTH AFRICA

10.5.2.1 Rising production of new vehicles to propel market

10.5.3 REST OF MIDDLE EAST & AFRICA

10.6 SOUTH AMERICA

10.6.1 BRAZIL

10.6.1.1 Expansion of industrial sector to propel demand

10.6.2 ARGENTINA

10.6.2.1 Rising demand for EVs and HEVs to drive market

10.6.3 COLUMBIA

10.6.3.1 Heavy reliance on imported high-tech medical devices to create growth opportunities for market players

10.6.4 REST OF SOUTH AMERICA

11 COMPETITIVE LANDSCAPE (Page No. - 198)

11.1 OVERVIEW

11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2019–2024

11.3 MARKET SHARE ANALYSIS, 2023

11.3.1 MARKET RANKING ANALYSIS, 2023

11.4 REVENUE ANALYSIS, 2021–2023

11.5 COMPANY VALUATION AND FINANCIAL METRICS

11.6 BRAND/PRODUCT COMPARISON

11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

11.7.1 STARS

11.7.2 EMERGING LEADERS

11.7.3 PERVASIVE PLAYERS

11.7.4 PARTICIPANTS

11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

11.7.5.1 Company footprint

11.7.5.2 Chemistry footprint

11.7.5.3 Curing process footprint

11.7.5.4 End-use industry footprint

11.7.5.5 Region footprint

11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

11.8.1 PROGRESSIVE COMPANIES

11.8.2 RESPONSIVE COMPANIES

11.8.3 DYNAMIC COMPANIES

11.8.4 STARTING BLOCKS

11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

11.8.5.1 List of key startups/SMEs

11.8.5.2 Competitive benchmarking of key startups/SMEs

11.9 COMPETITIVE SCENARIO

11.9.1 PRODUCT LAUNCHES

11.9.2 DEALS

11.9.3 EXPANSIONS

12 COMPANY PROFILES (Page No. - 219)

12.1 KEY PLAYERS

12.1.1 HENKEL AG & CO. KGAA

12.1.1.1 Business overview

12.1.1.2 Products/Solutions/Services offered

12.1.1.3 Recent developments

12.1.1.3.1 Product launches

12.1.1.3.2 Expansions

12.1.1.4 MnM view

12.1.1.4.1 Key strengths/Right to win

12.1.1.4.2 Strategic choices

12.1.1.4.3 Weaknesses/Competitive threats

12.1.2 H.B. FULLER COMPANY

12.1.2.1 Business overview

12.1.2.2 Products/Solutions/Services offered

12.1.2.3 Recent developments

12.1.2.3.1 Product launches

12.1.2.3.2 Deals

12.1.2.4 MnM view

12.1.2.4.1 Key strengths/Right to win

12.1.2.4.2 Strategic choices

12.1.2.4.3 Weaknesses/Competitive threats

12.1.3 3M

12.1.3.1 Business overview

12.1.3.2 Products/Solutions/Services offered

12.1.3.3 Recent developments

12.1.3.3.1 Expansions

12.1.3.4 MnM view

12.1.3.4.1 Key strengths/Right to win

12.1.3.4.2 Strategic choices

12.1.3.4.3 Weaknesses/Competitive threats

12.1.4 SIKA AG

12.1.4.1 Business overview

12.1.4.2 Products/Solutions/Services offered

12.1.4.3 Recent developments

12.1.4.3.1 Deals

12.1.4.3.2 Expansions

12.1.4.4 MnM view

12.1.4.4.1 Key strengths/Right to win

12.1.4.4.2 Strategic choices

12.1.4.4.3 Weaknesses/Competitive threats

12.1.5 DYMAX

12.1.5.1 Business overview

12.1.5.2 Products/Solutions/Services offered

12.1.5.3 Recent developments

12.1.5.3.1 Deals

12.1.5.4 MnM view

12.1.5.4.1 Key strengths/Right to win

12.1.5.4.2 Strategic choices

12.1.5.4.3 Weaknesses/Competitive threats

12.1.6 ARKEMA

12.1.6.1 Business overview

12.1.6.2 Products/Solutions/Services offered

12.1.6.3 Recent developments

12.1.6.3.1 Deals

12.1.6.3.2 Others

12.1.6.3.3 Expansions

12.1.7 TOAGOSEI CO., LTD.

12.1.7.1 Business overview

12.1.7.2 Products/Solutions/Services offered

12.1.8 ILLINOIS TOOL WORKS INC.

12.1.8.1 Business overview

12.1.8.2 Products/Solutions/Services offered

12.1.9 PIDILITE INDUSTRIES LIMITED

12.1.9.1 Business overview

12.1.9.2 Products/Solutions/Services offered

12.1.9.3 Recent developments

12.1.9.3.1 Product launches

12.1.9.3.2 Deals

12.1.10 ASTRAL LTD.

12.1.10.1 Business overview

12.1.10.2 Products/Solutions/Services offered

12.1.10.3 Recent developments

12.1.10.3.1 Expansions

12.1.11 PARKER-HANNIFIN CORPORATION

12.1.11.1 Business overview

12.1.11.2 Products/Solutions/Services offered

12.1.11.3 Recent developments

12.1.11.3.1 Deals

12.1.12 PERMABOND

12.1.12.1 Business overview

12.1.12.2 Products/Solutions/Services offered

12.1.12.3 Recent developments

12.1.12.3.1 Product launches

12.1.13 FRANKLIN INTERNATIONAL

12.1.13.1 Business overview

12.1.13.2 Products/Solutions/Services offered

12.1.14 MASTERBOND

12.1.14.1 Business overview

12.1.14.2 Products/Solutions/Services offered

12.1.15 PARSON ADHESIVES, INC.

12.1.15.1 Business overview

12.1.15.2 Products/Solutions/Services offered

12.1.16 DELO INDUSTRIAL ADHESIVES LLC.

12.1.16.1 Business overview

12.1.16.2 Products/Solutions/Services offered

12.1.17 CHEMENCE

12.1.17.1 Business overview

12.1.17.2 Products/Solutions/Services offered

12.1.18 HERNON MANUFACTURING

12.1.18.1 Business overview

12.1.18.2 Products/Solutions/Services offered

12.1.19 NANPAO RESINS CHEMICAL GROUP

12.1.19.1 Business overview

12.1.19.2 Products/Solutions/Services offered

12.1.20 URJA SEALANTS PVT. LTD

12.1.20.1 Business overview

12.1.20.2 Products/Solutions/Services offered

12.1.21 J-B WELD

12.1.21.1 Business overview

12.1.21.2 Products/Solutions/Services offered

12.1.22 HYLOMAR PRODUCTS

12.1.22.1 Business overview

12.1.22.2 Products/Solutions/Services offered

12.1.23 PANACOL-ELOSOL GMBH

12.1.23.1 Business overview

12.1.23.2 Products/Solutions/Services offered

12.1.24 PLASTOCHEM

12.1.24.1 Business overview

12.1.24.2 Products/Solutions/Services offered

12.1.25 WEISS CHEMIE + TECHNIK GMBH & CO. KG

12.1.25.1 Business overview

12.1.25.2 Products/Solutions/Services offered

13 ADJACENT & RELATED MARKETS (Page No. - 270)

13.1 INTRODUCTION

13.2 INSTANT ADHESIVES MARKET

13.2.1 MARKET DEFINITION

13.2.2 MARKET OVERVIEW

13.3 INSTANT ADHESIVES MARKET, BY SUBSTRATE

13.4 INSTANT ADHESIVES MARKET, BY CURING PROCESS

13.5 INSTANT ADHESIVES MARKET, BY CHEMISTRY AND SUB-CHEMISTRY

13.6 INSTANT ADHESIVES MARKET, BY APPLICATION

13.7 INSTANT ADHESIVES MARKET, BY REGION

14 APPENDIX (Page No. - 276)

14.1 DISCUSSION GUIDE

14.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

14.3 CUSTOMIZATION OPTIONS

14.4 RELATED REPORTS

14.5 AUTHOR DETAILS

LIST OF TABLES (236 TABLES)

TABLE 1 DEFINITION AND INCLUSIONS, BY CHEMISTRY

TABLE 2 DEFINITION AND INCLUSIONS, BY CURING PROCESS

TABLE 3 DEFINITION AND INCLUSIONS, BY APPLICATION

TABLE 4 DEFINITION AND INCLUSIONS, BY END-USE INDUSTRY

TABLE 5 USD EXCHANGE RATE, 2020–2023

TABLE 6 CYANOACRYLATE ADHESIVES MARKET SNAPSHOT, 2024 VS. 2029

TABLE 7 CYANOACRYLATE ADHESIVES MARKET: PORTER’S FIVE FORCES ANALYSIS

TABLE 8 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE INDUSTRY (%)

TABLE 9 KEY BUYING CRITERIA, BY END-USE INDUSTRY

TABLE 10 GDP TRENDS AND FORECAST, BY COUNTRY, 2021–2029 (PERCENTAGE CHANGE)

TABLE 11 KEY TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

TABLE 12 AVERAGE SELLING PRICE TREND OF CYANOACRYLATE ADHESIVES, BY REGION, 2021–2023 (USD/KG)

TABLE 13 INDICATIVE PRICING TREND OF CYANOACRYLATE ADHESIVES OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2023 (USD/KG)

TABLE 14 EXPORT DATA RELATED TO HS CODE 350610-COMPLIANT PRODUCTS, BY COUNTRY, 2021–2023 (USD THOUSAND)

TABLE 15 IMPORT DATA RELATED TO HS CODE 350610-COMPLIANT PRODUCTS, BY COUNTRY, 2021–2023 (USD THOUSAND)

TABLE 16 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 17 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 18 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 19 ROLES OF COMPANIES IN CYANOACRYLATE ADHESIVES ECOSYSTEM

TABLE 20 CYANOACRYLATE ADHESIVES MARKET: INVESTMENT AND FUNDING SCENARIO

TABLE 21 CYANOACRYLATE ADHESIVES: LIST OF KEY CONFERENCES AND EVENTS, 2024–2025

TABLE 22 CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (USD MILLION)

TABLE 23 CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (TONS)

TABLE 24 ETHYL CYANOACRYLATE: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 25 ETHYL CYANOACRYLATE: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 26 METHYL CYANOACRYLATE: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 27 METHYL CYANOACRYLATE: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 28 OTHER CHEMISTRIES: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 29 OTHER CHEMISTRIES: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 30 CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (USD MILLION)

TABLE 31 CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (TONS)

TABLE 32 CONVENTIONAL: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 33 CONVENTIONAL: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 34 LIGHT-CURED: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 35 LIGHT-CURED: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 36 CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 37 CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 38 INDUSTRIAL: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 39 INDUSTRIAL: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 40 WOODWORKING: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 41 WOODWORKING: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 42 TRANSPORTATION: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 43 TRANSPORTATION: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 44 AUTOMOTIVE: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 45 AUTOMOTIVE: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 46 AEROSPACE: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 47 AEROSPACE: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 48 OTHER TRANSPORTATIONS: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 49 OTHER TRANSPORTATIONS: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 50 MEDICAL: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 51 MEDICAL: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 52 ELECTRONICS: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 53 ELECTRONICS: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 54 CONSUMER: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 55 CONSUMER: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 56 OTHER END-USE INDUSTRIES: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 57 OTHER END-USE INDUSTRIES: CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 58 CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (USD MILLION)

TABLE 59 CYANOACRYLATE ADHESIVES MARKET, BY REGION, 2021–2029 (TONS)

TABLE 60 EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (USD MILLION)

TABLE 61 EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (TONS)

TABLE 62 EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (USD MILLION)

TABLE 63 EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (TONS)

TABLE 64 EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (USD MILLION)

TABLE 65 EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (TONS)

TABLE 66 EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 67 EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 68 GERMANY: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 69 GERMANY: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 70 UK: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 71 UK: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 72 FRANCE: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 73 FRANCE: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 74 ITALY: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 75 ITALY: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 76 TURKEY: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 77 TURKEY: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 78 REST OF EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 79 REST OF EUROPE: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 80 ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (USD MILLION)

TABLE 81 ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (TONS)

TABLE 82 ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (USD MILLION)

TABLE 83 ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (TONS)

TABLE 84 ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (USD MILLION)

TABLE 85 ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (TONS)

TABLE 86 ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 87 ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 88 CHINA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 89 CHINA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 90 INDIA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 91 INDIA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 92 JAPAN: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 93 JAPAN: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 94 SOUTH KOREA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 95 SOUTH KOREA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 96 INDONESIA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 97 INDONESIA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 98 VIETNAM: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 99 VIETNAM: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 100 REST OF ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 101 REST OF ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 102 NORTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (USD MILLION)

TABLE 103 NORTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (TONS)

TABLE 104 NORTH AMERICA CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (USD MILLION)

TABLE 105 NORTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (TONS)

TABLE 106 NORTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (USD MILLION)

TABLE 107 NORTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (TONS)

TABLE 108 NORTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 109 NORTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 110 US: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 111 US: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 112 CANADA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 113 CANADA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 114 MEXICO: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 115 MEXICO: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 116 MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (USD MILLION)

TABLE 117 MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (TONS)

TABLE 118 GCC COUNTRIES: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (USD MILLION)

TABLE 119 GCC COUNTRIES: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (TONS)

TABLE 120 MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (USD MILLION)

TABLE 121 MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (TONS)

TABLE 122 MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (USD MILLION)

TABLE 123 MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (TONS)

TABLE 124 MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 125 MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 126 GCC COUNTRIES: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 127 GCC COUNTRIES: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 128 SOUTH AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 129 SOUTH AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 130 REST OF MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 131 REST OF MIDDLE EAST & AFRICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 132 SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (USD MILLION)

TABLE 133 SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY COUNTRY, 2021–2029 (TONS)

TABLE 134 SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (USD MILLION)

TABLE 135 SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY CHEMISTRY, 2021–2029 (TONS)

TABLE 136 SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (USD MILLION)

TABLE 137 SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY CURING PROCESS, 2021–2029 (TONS)

TABLE 138 SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 139 SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 140 BRAZIL: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 141 BRAZIL: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 142 ARGENTINA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 143 ARGENTINA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 144 COLUMBIA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 145 COLUMBIA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 146 REST OF SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (USD MILLION)

TABLE 147 REST OF SOUTH AMERICA: CYANOACRYLATE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021–2029 (TONS)

TABLE 148 CYANOACRYLATE ADHESIVES MARKET: OVERVIEW OF KEY STRATEGIES ADOPTED BY MAJOR MARKET PLAYERS, JANUARY 2019–JULY 2024

TABLE 149 CYANOACRYLATE ADHESIVES MARKET: DEGREE OF COMPETITION, 2023

TABLE 150 CYANOACRYLATE ADHESIVES MARKET: CHEMISTRY FOOTPRINT

TABLE 151 CYANOACRYLATE ADHESIVES MARKET: CURING PROCESS FOOTPRINT

TABLE 152 CYANOACRYLATE ADHESIVES MARKET: END-USE INDUSTRY FOOTPRINT

TABLE 153 CYANOACRYLATE ADHESIVES MARKET: REGION FOOTPRINT

TABLE 154 CYANOACRYLATE ADHESIVES MARKET: LIST OF KEY STARTUPS/SMES

TABLE 155 CYANOACRYLATE ADHESIVES MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 156 CYANOACRYLATE ADHESIVES MARKET: PRODUCT LAUNCHES, JANUARY 2019–JULY 2024

TABLE 157 CYANOACRYLATE ADHESIVES MARKET: DEALS, JANUARY 2019–JULY 2024

TABLE 158 CYANOACRYLATE ADHESIVES MARKET: EXPANSIONS, JANUARY 2019–JULY 2024

TABLE 159 HENKEL AG & CO. KGAA: COMPANY OVERVIEW

TABLE 160 HENKEL AG & CO. KGAA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 161 HENKEL AG & CO. KGAA: PRODUCT LAUNCHES

TABLE 162 HENKEL AG & CO. KGAA: EXPANSIONS

TABLE 163 H.B. FULLER COMPANY: COMPANY OVERVIEW

TABLE 164 H.B. FULLER COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 165 H.B. FULLER COMPANY: PRODUCT LAUNCHES

TABLE 166 H.B. FULLER COMPANY: DEALS

TABLE 167 3M: COMPANY OVERVIEW

TABLE 168 3M: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 169 3M: EXPANSIONS

TABLE 170 SIKA AG: COMPANY OVERVIEW

TABLE 171 SIKA AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 172 SIKA AG: DEALS

TABLE 173 SIKA AG: EXPANSIONS

TABLE 174 DYMAX: COMPANY OVERVIEW

TABLE 175 DYMAX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 176 DYMAX: DEALS

TABLE 177 ARKEMA: COMPANY OVERVIEW

TABLE 178 ARKEMA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 179 ARKEMA: DEALS

TABLE 180 ARKEMA: OTHERS

TABLE 181 ARKEMA: EXPANSIONS

TABLE 182 TOAGOSEI CO., LTD.: COMPANY OVERVIEW

TABLE 183 TOAGOSEI CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 184 ILLINOIS TOOL WORKS INC.: COMPANY OVERVIEW

TABLE 185 ILLINOIS TOOL WORKS INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 186 PIDILITE INDUSTRIES LIMITED: COMPANY OVERVIEW

TABLE 187 PIDILITE INDUSTRIES LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 188 PIDILITE INDUSTRIES LIMITED: PRODUCT LAUNCHES

TABLE 189 PIDILITE INDUSTRIES LIMITED: DEALS

TABLE 190 ASTRAL LTD.: COMPANY OVERVIEW

TABLE 191 ASTRAL LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 192 ASTRAL LTD.: EXPANSIONS

TABLE 193 PARKER-HANNIFIN CORPORATION: COMPANY OVERVIEW

TABLE 194 PARKER-HANNIFIN CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 195 PARKER-HANNIFIN CORPORATION: DEALS

TABLE 196 PERMABOND: COMPANY OVERVIEW

TABLE 197 PERMABOND: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 198 PERMABOND: PRODUCT LAUNCHES

TABLE 199 FRANKLIN INTERNATIONAL: COMPANY OVERVIEW

TABLE 200 FRANKLIN INTERNATIONAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 201 MASTERBOND: COMPANY OVERVIEW

TABLE 202 MASTERBOND: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 203 PARSON ADHESIVES, INC.: COMPANY OVERVIEW

TABLE 204 PARSON ADHESIVES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 205 DELO INDUSTRIAL ADHESIVES LLC.: COMPANY OVERVIEW

TABLE 206 DELO INDUSTRIAL ADHESIVES LLC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 207 CHEMENCE: COMPANY OVERVIEW

TABLE 208 CHEMENCE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 209 HERNON MANUFACTURING: COMPANY OVERVIEW

TABLE 210 HERNON MANUFACTURING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 211 NANPAO RESINS CHEMICAL GROUP: COMPANY OVERVIEW

TABLE 212 NANPAO RESINS CHEMICAL GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 213 URJA SEALANTS PVT. LTD: COMPANY OVERVIEW

TABLE 214 URJA SEALANTS PVT. LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 215 J-B WELD: COMPANY OVERVIEW

TABLE 216 J-B WELD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 217 HYLOMAR PRODUCTS: COMPANY OVERVIEW

TABLE 218 HYLOMAR PRODUCTS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 219 PANACOL-ELOSOL GMBH: COMPANY OVERVIEW

TABLE 220 PANACOL-ELOSOL GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 221 PLASTOCHEM: COMPANY OVERVIEW

TABLE 222 PLASTOCHEM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 223 WEISS CHEMIE + TECHNIK GMBH & CO. KG: COMPANY OVERVIEW

TABLE 224 WEISS CHEMIE + TECHNIK GMBH & CO. KG: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

TABLE 225 INSTANT ADHESIVES MARKET, BY CURING PROCESS, 2015–2022 (USD MILLION)

TABLE 226 INSTANT ADHESIVES MARKET, BY CURING PROCESS, 2015–2022 (TON)

TABLE 227 INSTANT ADHESIVES MARKET, BY CHEMISTRY, 2015–2022 (USD MILLION)

TABLE 228 INSTANT ADHESIVES MARKET, BY CHEMISTRY, 2015–2022 (TON)

TABLE 229 CYANOACRYLATE: INSTANT ADHESIVES MARKET, BY SUB-CHEMISTRY, 2015–2022 (USD MILLION)

TABLE 230 CYANOACRYLATE: INSTANT ADHESIVES MARKET, BY SUB-CHEMISTRY, 2015–2022 (TON)

TABLE 231 EPOXY-BASED: INSTANT ADHESIVES MARKET, BY SUB-CHEMISTRY, 2015–2022 (USD MILLION)

TABLE 232 EPOXY-BASED: INSTANT ADHESIVES MARKET, BY SUB-CHEMISTRY, 2015–2022 (TON)

TABLE 233 INSTANT ADHESIVES MARKET, BY APPLICATION, 2015–2022 (USD MILLION)

TABLE 234 INSTANT ADHESIVES MARKET, BY APPLICATION, 2015–2022 (TON)

TABLE 235 INSTANT ADHESIVES MARKET, BY REGION, 2015–2022 (USD MILLION)

TABLE 236 INSTANT ADHESIVES MARKET, BY REGION, 2015–2022 (TON)

LIST OF FIGURES (64 FIGURES)

FIGURE 1 CYANOACRYLATE ADHESIVES MARKET SEGMENTATION

FIGURE 2 CYANOACRYLATE ADHESIVES MARKET: RESEARCH DESIGN

FIGURE 3 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

FIGURE 4 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

FIGURE 5 CYANOACRYLATE ADHESIVES MARKET SIZE ESTIMATION, BY CHEMISTRY

FIGURE 6 CYANOACRYLATE ADHESIVES MARKET SIZE ESTIMATION, BY REGION

FIGURE 7 CYANOACRYLATE ADHESIVES MARKET: SUPPLY-SIDE FORECAST

FIGURE 8 CYANOACRYLATE ADHESIVES MARKET: DEMAND-SIDE FORECAST

FIGURE 9 METHODOLOGY FOR SUPPLY-SIDE SIZING OF CYANOACRYLATE ADHESIVES MARKET

FIGURE 10 MAJOR FACTORS RESPONSIBLE FOR GLOBAL RECESSION AND THEIR IMPACT ON MARKET

FIGURE 11 CYANOACRYLATE ADHESIVES MARKET: DATA TRIANGULATION

FIGURE 12 ETHYL CYANOACRYLATE SEGMENT TO DOMINATE CYANOACRYLATE ADHESIVES MARKET DURING FORECAST PERIOD

FIGURE 13 TRANSPORTATION SEGMENT TO HOLD LARGEST SHARE OF CYANOACRYLATE ADHESIVES MARKET IN 2029

FIGURE 14 ASIA PACIFIC TO DOMINATE CYANOACRYLATE ADHESIVES MARKET DURING FORECAST PERIOD

FIGURE 15 ONGOING R&D TO ENHANCE EFFICIENCIES AND FUNCTIONALITIES OF INDUSTRIAL MATERIALS TO CREATE LUCRATIVE OPPORTUNITIES FOR MARKET PLAYERS

FIGURE 16 ETHYL CYANOACRYLATE SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 17 INDUSTRIAL SEGMENT AND CHINA TO ACCOUNT FOR LARGEST SHARES OF ASIA PACIFIC CYANOACRYLATE ADHESIVES MARKET IN 2024

FIGURE 18 DEMAND FOR CYANOACRYLATE ADHESIVES TO GROW FASTER IN DEVELOPING COUNTRIES DURING FORECAST PERIOD

FIGURE 19 INDIA TO REGISTER HIGHEST CAGR IN CYANOACRYLATE ADHESIVES MARKET DURING FORECAST PERIOD

FIGURE 20 CYANOACRYLATE ADHESIVES MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 21 CYANOACRYLATE ADHESIVES MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END-USE INDUSTRY

FIGURE 23 KEY BUYING CRITERIA, BY END-USE INDUSTRY

FIGURE 24 CYANOACRYLATE ADHESIVES MARKET: SUPPLY CHAIN ANALYSIS

FIGURE 25 AVERAGE SELLING PRICE TREND OF CYANOACRYLATE ADHESIVES, BY REGION, 2021–2023 (USD/KG)

FIGURE 26 AVERAGE SELLING PRICE TREND OF CYANOACRYLATE ADHESIVES, BY CHEMISTRY, 2023 (USD/KG)

FIGURE 27 AVERAGE SELLING PRICE TREND OF CYANOACRYLATE ADHESIVES, BY CURING PROCESS, 2023 (USD/KG)

FIGURE 28 AVERAGE SELLING PRICE TREND OF CYANOACRYLATE ADHESIVES, BY END-USE INDUSTRY, 2023 (USD/KG)

FIGURE 29 AVERAGE SELLING PRICE TREND OF CYANOACRYLATE ADHESIVES OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2023 (USD/KG)

FIGURE 30 EXPORT DATA RELATED TO HS CODE 350610-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2019–2023 (USD THOUSAND)

FIGURE 31 IMPORT DATA RELATED TO HS CODE 350610-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2019–2023 (USD THOUSAND)

FIGURE 32 CYANOACRYLATE ADHESIVES MARKET: ECOSYSTEM ANALYSIS

FIGURE 33 STAKEHOLDERS IN CYANOACRYLATE ADHESIVES ECOSYSTEM

FIGURE 34 TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

FIGURE 35 LIST OF MAJOR PATENTS RELATED TO CYANOACRYLATE ADHESIVES, 2014–2024

FIGURE 36 ETHYL CYANOACRYLATE SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2024

FIGURE 37 CONVENTIONAL SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE IN 2024

FIGURE 38 TRANSPORTATION SEGMENT TO DOMINATE MARKET IN 2024

FIGURE 39 GLOBAL ANNUAL VEHICLE SALES, 2017−2025 (UNITS IN MILLIONS)

FIGURE 40 ASIA PACIFIC TO REGISTER HIGHEST CAGR IN CYANOACRYLATE ADHESIVES MARKET BETWEEN 2024 AND 2029

FIGURE 41 EUROPE: CYANOACRYLATE ADHESIVES MARKET SNAPSHOT

FIGURE 42 ASIA PACIFIC: CYANOACRYLATE ADHESIVES MARKET SNAPSHOT

FIGURE 43 NORTH AMERICA: CYANOACRYLATE ADHESIVES MARKET SNAPSHOT

FIGURE 44 SOUTH AFRICA TO REGISTER HIGHEST CAGR IN MIDDLE EAST & AFRICAN CYANOACRYLATE ADHESIVES MARKET BETWEEN 2024 AND 2029

FIGURE 45 BRAZIL TO REGISTER HIGHEST CAGR IN SOUTH AMERICAN CYANOACRYLATE ADHESIVES MARKET BETWEEN 2024 AND 2029

FIGURE 46 CYANOACRYLATE ADHESIVES MARKET SHARE ANALYSIS, 2023

FIGURE 47 CYANOACRYLATE ADHESIVES MARKET: RANKING OF LEADING PLAYERS, 2023

FIGURE 48 CYANOACRYLATE ADHESIVES MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2021–2023 (USD MILLION)

FIGURE 49 CYANOACRYLATE ADHESIVES MARKET: COMPANY VALUATION (USD BILLION)

FIGURE 50 CYANOACRYLATE ADHESIVES MARKET: FINANCIAL METRICS (EV/EBITDA)

FIGURE 51 CYANOACRYLATE ADHESIVES MARKET: BRAND/PRODUCT COMPARISON

FIGURE 52 CYANOACRYLATE ADHESIVES MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

FIGURE 53 CYANOACRYLATE ADHESIVES MARKET: COMPANY FOOTPRINT

FIGURE 54 CYANOACRYLATE ADHESIVES MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

FIGURE 55 HENKEL AG & CO. KGAA: COMPANY SNAPSHOT

FIGURE 56 H.B. FULLER COMPANY: COMPANY SNAPSHOT

FIGURE 57 3M: COMPANY SNAPSHOT`

FIGURE 58 SIKA AG: COMPANY SNAPSHOT

FIGURE 59 ARKEMA: COMPANY SNAPSHOT

FIGURE 60 TOAGOSEI CO., LTD.: COMPANY SNAPSHOT

FIGURE 61 ILLINOIS TOOL WORKS INC.: COMPANY SNAPSHOT

FIGURE 62 PIDILITE INDUSTRIES LIMITED: COMPANY SNAPSHOT

FIGURE 63 ASTRAL LTD.: COMPANY SNAPSHOT

FIGURE 64 PARKER-HANNIFIN CORPORATION: COMPANY SNAPSHOT

Growth opportunities and latent adjacency in Cyanoacrylate Adhesives Market