TABLE OF CONTENTS

1 INTRODUCTION (Page No. - 26)

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION

1.3.2 INCLUSIONS & EXCLUSIONS

1.4 YEARS CONSIDERED

1.5 CURRENCY CONSIDERED

1.6 UNIT CONSIDERED

1.7 STAKEHOLDERS

2 RESEARCH METHODOLOGY (Page No. - 32)

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Primary interview participants

2.1.2.2 Key industry insights

2.1.2.3 Breakdown of primary interviews

2.1.2.4 List of primary participants

2.2 MARKET SIZE ESTIMATION METHODOLOGY

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

2.4 FACTOR ANALYSIS

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY (Page No. - 47)

4 PREMIUM INSIGHTS (Page No. - 52)

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HYDROGEN BUS & TRUCK MARKET

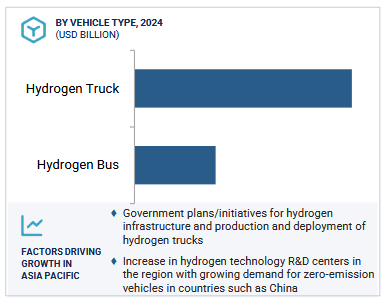

4.2 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE

4.3 HYDROGEN BUS & TRUCK MARKET, BY TYPE OF TANK

4.4 HYDROGEN BUS & TRUCK MARKET, BY HYDROGEN TANK SIZE

4.5 HYDROGEN BUS & TRUCK MARKET, BY RANGE

4.6 HYDROGEN BUS & TRUCK MARKET, BY MOTOR POWER

4.7 HYDROGEN BUS & TRUCK MARKET, BY REGION

5 MARKET OVERVIEW (Page No. - 56)

5.1 INTRODUCTION

5.2 IMPACT OF AI/GEN AI ON HYDROGEN BUS & TRUCK MARKET

5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

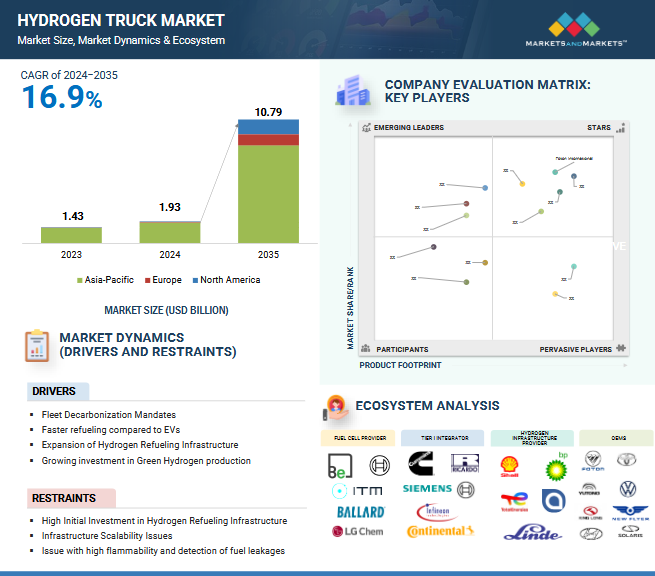

5.4 MARKET DYNAMICS

5.4.1 DRIVERS

5.4.1.1 Fleet decarbonization mandates

5.4.1.2 Faster refueling than EVs

5.4.1.3 Expansion of hydrogen refueling infrastructure

5.4.1.4 Growing investment in ‘Green Hydrogen’ production

5.4.1.5 Government initiatives promoting fuel cell vehicles

5.4.2 RESTRAINTS

5.4.2.1 High initial investments in hydrogen refueling infrastructure

5.4.2.2 Infrastructure scalability issues

5.4.2.3 High flammability and detection of fuel leakages

5.4.3 OPPORTUNITIES

5.4.3.1 Advancements in fuel cell technology

5.4.3.1.1 FCEV commercial freight truck developments

5.4.3.2 Development of mobile and community hydrogen fueling systems

5.4.3.3 Integration with renewable energy sources

5.4.3.4 Deployment of hydrogen corridors

5.4.4 CHALLENGES

5.4.4.1 High cost compared to gasoline/electric vehicles

5.4.4.2 Hydrogen storage and transportation challenges

5.4.4.3 Higher operating costs than EVs

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR HYDROGEN BUSES

5.5.2 AVERAGE SELLING PRICE TREND OF KEY OEMS FOR HYDROGEN TRUCKS

5.5.3 AVERAGE SELLING PRICE TREND, BY REGION

5.6 ECOSYSTEM ANALYSIS

5.7 VALUE CHAIN ANALYSIS

5.8 CASE STUDY ANALYSIS

5.8.1 BALLARD POWER SYSTEMS INTRODUCED ZERO-EMISSION HYDROGEN FUEL CELL BUSES TO REDUCE GREENHOUSE GAS EMISSIONS

5.8.2 BALLARD POWER SYSTEMS SUPPLIED FCVELOCITY-9SSL FUEL CELL STACKS TO SHANGHAI RE-FIRE TECHNOLOGY TO ESTABLISH FLEET OF 500 FUEL CELL TRUCKS

5.8.3 TRANSPORT FOR LONDON (TFL) INTRODUCED FUEL CELL BUSES TO REDUCE CARBON EMISSIONS BY 2025

5.8.4 BALLARD POWER SYSTEM AND VAN HOOL COLLABORATED TO ESTABLISH SUSTAINABLE TRANSPORTATION SOLUTION

5.8.5 HALL DECIDED TO INVEST IN NIKOLA TRE FCEVS (FUEL CELL ELECTRIC VEHICLES) TO ELIMINATE USE OF FOSSIL FUEL TRUCKS

5.9 KEY OEMS: MNM INSIGHTS

5.9.1 FOTON INTERNATIONAL: FCEV STRATEGIES

5.9.2 XIAMEN KING LONG INTERNATIONAL TRADING CO., LTD.: FCEV STRATEGIES

5.9.3 YUTONG BUS CO., LTD.: FCEV STRATEGIES

5.9.4 SOLARIS BUS & COACH SP. Z.O.O.: FCEV STRATEGIES

5.9.5 HYUNDAI MOTOR COMPANY: FCEV STRATEGIES

5.1 HYDROGEN BUS & TRUCK MARKET: BUSINESS MODELS

5.11 HYDROGEN REFUELING STATION SETUP TRENDS, BY REGION: MNM INSIGHTS

5.12 COUNTRY-LEVEL TARGETS OF HYDROGEN BUSES/TRUCKS AND REFUELLING STATIONS: MNM INSIGHTS

5.13 HYDROGEN COMMERCIAL VEHICLES’ FUEL CAPACITY AND RANGE: MNM INSIGHTS

5.14 EXISTING AND UPCOMING HYDROGEN COMMERCIAL VEHICLE MODELS: MNM INSIGHTS

5.15 H2ICE BUSES & TRUCKS: MNM INSIGHTS

5.16 TRADE ANALYSIS

5.16.1 EXPORT SCENARIO

5.16.2 IMPORT SCENARIO

5.17 TOTAL COST OF OWNERSHIP COMPARISON OF BEV AND FCEV BUSES AND TRUCKS

5.18 BILL OF MATERIALS

5.18.1 BILL OF MATERIAL COMPARISON BETWEEN FCEV, ICE, AND BEV BUSES

5.18.2 BILL OF MATERIAL COMPARISON BETWEEN FCEV, ICE, AND BEV TRUCKS

5.19 PATENT ANALYSIS

5.19.1 INTRODUCTION

5.2 REGULATORY LANDSCAPE

5.20.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS, BY REGION

5.21 TECHNOLOGY ANALYSIS

5.21.1 KEY TECHNOLOGIES

5.21.1.1 Solid Oxide Fuel Cell (SOFC)

5.21.1.2 Polymer Electrolyte Membrane Fuel Cell (PEMFC)

5.21.1.3 Direct Borohydride Fuel Cell (DBFC)

5.21.1.4 Packaged fuel cell system module

5.21.1.5 Fuel Cell Hybrid Electric Vehicle (FCHEV)

5.21.1.6 Hydrogen Internal Combustion Engine (H2ICE)

5.21.1.7 Non-precious metal catalyst-based fuel cell

5.21.1.8 Carbonate-Superstructured Solid Fuel Cell (CSSFC)

5.21.2 COMPLEMENTARY TECHNOLOGIES

5.21.2.1 Low carbon hydrogen

5.21.2.2 Hydrogenious LOHC (Liquid Organic Hydrogen Carrier)

5.21.2.3 Liquefied hydrogen technology

5.21.3 ADJACENT TECHNOLOGIES

5.21.3.1 Telematics and fleet management systems

5.21.3.2 Hydrogen sensor system

5.22 KEY CONFERENCES & EVENTS, 2024–2025

5.23 KEY STAKEHOLDERS & BUYING CRITERIA

5.23.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.23.2 BUYING CRITERIA

5.24 INVESTMENT & FUNDING SCENARIO

5.25 FUNDING, BY VEHICLE TYPE

6 HYDROGEN BUS & TRUCK MARKET, BY MOTOR POWER (Page No. - 133)

6.1 INTRODUCTION

6.2 UP TO 200 KW

6.2.1 LAST-MILE DELIVERY SERVICES TO BOOST DEMAND FOR ENGINES WITH POWER RANGE OF UP TO 200 KW

6.2.2 UP TO 200 KW: HYDROGEN BUS MODELS

6.2.3 UP TO 200 KW: HYDROGEN TRUCK MODELS

6.3 200–400 KW

6.3.1 GROWING DEMAND FOR TRANSIT BUSES TO DRIVE GROWTH OF 200–400 KW SEGMENT

6.3.2 200–400 KW: HYDROGEN BUS MODELS

6.3.3 200–400 KW: HYDROGEN TRUCK MODELS

6.4 ABOVE 400 KW

6.4.1 INCREASING DEMAND FOR HEAVY-DUTY TRANSPORTATION TO BOOST MARKET

6.4.2 ABOVE 400 KW: HYDROGEN BUS MODELS

6.4.3 ABOVE 400 KW: HYDROGEN TRUCK MODELS

6.5 KEY PRIMARY INSIGHTS

7 HYDROGEN BUS & TRUCK MARKET, BY RANGE (Page No. - 143)

7.1 INTRODUCTION

7.2 UP TO 300 MILES

7.2.1 DEMAND FOR EMISSION-FREE INTRACITY TRANSPORTATION AND LAST-MILE DELIVERY TO DRIVE SEGMENT GROWTH

7.2.2 UP TO 300 MILES: HYDROGEN BUS MODELS

7.2.3 UP TO 300 MILES: HYDROGEN TRUCK MODELS

7.3 300–500 MILES

7.3.1 DEMAND FOR FIELD SERVICES AND TRANSIT OPERATIONS TO DRIVE SEGMENT’S GROWTH

7.3.2 300–500 MILES: HYDROGEN BUS MODELS

7.3.3 300–500 MILES: HYDROGEN TRUCK MODELS

7.4 ABOVE 500 MILES

7.4.1 INCREASING NEED FOR LONG-HAUL, HEAVY-DUTY TRANSPORTATION TO DRIVE MARKET

7.4.2 ABOVE 500 MILES: HYDROGEN BUS MODELS

7.4.3 ABOVE 500 MILES: HYDROGEN TRUCK MODELS

7.5 KEY PRIMARY INSIGHTS

8 HYDROGEN BUS & TRUCK MARKET, BY HYDROGEN TANK SIZE (Page No. - 153)

8.1 INTRODUCTION

8.2 < 30 KG

8.2.1 DEMAND FOR LAST-MILE DELIVERY SERVICES AND SHORT-RANGE H2 BUSES TO BOOST MARKET

8.2.2 < 30 KG: HYDROGEN BUS AND TRUCK MODELS

8.3 30–60 KG

8.3.1 GROWING DEMAND FOR LONG-HAUL TRANSPORTATION TO SPUR MARKET GROWTH

8.3.2 30–60 KG: HYDROGEN BUS AND TRUCK MODELS

8.4 > 60 KG

8.4.1 INCREASING DEMAND FOR HEAVY-DUTY TRANSPORTATION TO BOOST GROWTH

8.4.2 > 60 KG: HYDROGEN BUS AND TRUCK MODELS

8.5 KEY PRIMARY INSIGHTS

9 HYDROGEN BUS & TRUCK MARKET, BY TYPE OF TANK (Page No. - 162)

9.1 INTRODUCTION

9.1.1 HYDROGEN TANK TYPE CLASSIFICATION FOR AUTOMOTIVE APPLICATION

9.2 TYPE III

9.2.1 TYPE III TANKS CAN WITHSTAND HIGHER INTERNAL PRESSURE THAN OTHER TANKS

9.2.2 HYDROGEN BUSES WITH TYPE III HYDROGEN TANKS

9.2.3 HYDROGEN TRUCKS WITH TYPE III HYDROGEN TANKS

9.3 TYPE IV

9.3.1 NEED FOR HIGH-PRESSURE STORAGE OF HYDROGEN TO BOOST DEMAND FOR TYPE IV TANKS

9.3.2 HYDROGEN BUSES WITH TYPE IV HYDROGEN TANKS

9.3.3 HYDROGEN TRUCKS WITH TYPE IV HYDROGEN TANKS

9.4 KEY PRIMARY INSIGHTS

10 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE (Page No. - 172)

10.1 INTRODUCTION

10.2 HYDROGEN BUSES

10.2.1 GOVERNMENT INITIATIVES TO BOOST DEMAND FOR HYDROGEN BUSES

10.2.2 MINIBUSES/SHUTTLES

10.2.2.1 HYDROGEN MINIBUS/SHUTTLE MODELS

10.2.3 CITY/TRANSIT BUSES

10.2.3.1 Hydrogen city/transit bus models

10.3 HYDROGEN TRUCKS

10.3.1 GROWING DEMAND FOR LONG-HAUL TRANSPORTATION TO DRIVE HYDROGEN TRUCKS MARKET

10.3.2 MEDIUM-DUTY TRUCKS

10.3.2.1 Hydrogen medium-duty truck models

10.3.3 HEAVY-DUTY TRUCKS

10.3.3.1 Hydrogen heavy-duty truck models

10.4 KEY PRIMARY INSIGHTS

11 HYDROGEN BUS & TRUCK MARKET, BY REGION (Page No. - 184)

11.1 INTRODUCTION

11.2 ASIA PACIFIC

11.2.1 MACROECONOMIC OUTLOOK

11.2.2 CHINA

11.2.2.1 Rising investments in clean and renewable energy to drive growth

11.2.3 JAPAN

11.2.3.1 Increasing demand for hydrogen infrastructure to boost market

11.2.4 SOUTH KOREA

11.2.4.1 Push by local OEMs like Hyundai to encourage market demand and expansion

11.2.5 INDIA

11.2.5.1 Initiatives by government to promote ‘Green Transportation’ to drive growth

11.3 EUROPE

11.3.1 MACROECONOMIC OUTLOOK

11.3.2 FRANCE

11.3.2.1 Presence of major hydrogen-powered fleets to spur demand

11.3.3 GERMANY

11.3.3.1 Developments in hydrogen infrastructure to boost growth

11.3.4 ITALY

11.3.4.1 Shift toward hydrogen-powered vehicles to drive market

11.3.5 SPAIN

11.3.5.1 Strategic partnerships and investments to drive production of hydrogen-powered vehicles

11.3.6 UK

11.3.6.1 Demand for zero-emission vehicles to drive market

11.4 NORTH AMERICA

11.4.1 MACROECONOMIC OUTLOOK

11.4.2 CANADA

11.4.2.1 Demand for fleet decarbonization to propel growth

11.4.3 US

11.4.3.1 Increasing deployment of hydrogen buses to spur popularity of hydrogen-powered vehicles

12 COMPETITIVE LANDSCAPE (Page No. - 232)

12.1 OVERVIEW

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

12.3 MARKET SHARE ANALYSIS, 2023

12.4 REVENUE ANALYSIS

12.5 COMPANY VALUATION AND FINANCIAL METRICS

12.6 BRAND/PRODUCT COMPARISON

12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

12.7.1 STARS

12.7.2 EMERGING LEADERS

12.7.3 PERVASIVE PLAYERS

12.7.4 PARTICIPANTS

12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

12.8.1 PROGRESSIVE COMPANIES

12.8.2 RESPONSIVE COMPANIES

12.8.3 DYNAMIC COMPANIES

12.8.4 STARTING BLOCKS

12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

12.9 COMPETITIVE SCENARIO

12.9.1 PRODUCT LAUNCHES

12.9.2 DEALS

12.9.3 EXPANSION

12.9.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES (Page No. - 257)

13.1 KEY PLAYERS

13.1.1 FOTON INTERNATIONAL

13.1.1.1 Business overview

13.1.1.2 Products/Solutions offered

13.1.1.3 Recent developments

13.1.1.4 MnM view

13.1.1.4.1 Right to win

13.1.1.4.2 Strategic choices

13.1.1.4.3 Weaknesses & competitive threats

13.1.2 YUTONG BUS CO., LTD.

13.1.2.1 Business overview

13.1.2.2 Products/Solutions offered

13.1.2.3 Recent developments

13.1.2.4 MnM view

13.1.2.4.1 Right to win

13.1.2.4.2 Strategic choices

13.1.2.4.3 Weaknesses & competitive threats

13.1.3 XIAMEN KING LONG INTERNATIONAL TRADING CO., LTD. (KING LONG)

13.1.3.1 Business overview

13.1.3.2 Products/Solutions offered

13.1.3.3 Recent developments

13.1.3.4 MnM view

13.1.3.4.1 Right to win

13.1.3.4.2 Strategic choices

13.1.3.4.3 Weaknesses & competitive threats

13.1.4 SOLARIS BUS & COACH SP. Z O.O.

13.1.4.1 Business overview

13.1.4.2 Products/Services offered

13.1.4.3 Recent developments

13.1.4.4 MnM view

13.1.4.4.1 Right to win

13.1.4.4.2 Strategic choices

13.1.4.4.3 Weaknesses & competitive threats

13.1.5 HYUNDAI MOTOR COMPANY

13.1.5.1 Business overview

13.1.5.2 Products/Solutions offered

13.1.5.3 Recent developments

13.1.5.4 MnM view

13.1.5.4.1 Right to win

13.1.5.4.2 Strategic choices

13.1.5.4.3 Weaknesses & competitive threats

13.1.6 ANHUI ANKAI AUTOMOBILE CO., LTD

13.1.6.1 Business overview

13.1.6.2 Products/Solutions offered

13.1.6.3 Recent developments

13.1.7 NIKOLA CORPORATION

13.1.7.1 Business overview

13.1.7.2 Products/Solutions offered

13.1.7.3 Recent developments

13.1.8 TOYOTA MOTOR CORPORATION

13.1.8.1 Business overview

13.1.8.2 Products/Solutions offered

13.1.8.3 Recent developments

13.1.9 VDL GROEP

13.1.9.1 Business overview

13.1.9.2 Products/Solutions offered

13.1.9.3 Recent developments

13.1.10 NFI GROUP

13.1.10.1 Business overview

13.1.10.2 Products/Solutions offered

13.1.10.3 Recent developments

13.1.11 ZHONGTONG BUS HOLDING CO., LTD.

13.1.11.1 Business overview

13.1.11.2 Products/Solutions offered

13.1.11.3 Recent developments

13.1.12 DAIMLER TRUCK AG

13.1.12.1 Business overview

13.1.12.2 Products/Solutions offered

13.1.12.3 Recent developments

13.1.13 IVECO S.P.A

13.1.13.1 Business overview

13.1.13.2 Products/Solutions offered

13.1.13.3 Recent developments

13.2 OTHER PLAYERS

13.2.1 SAIC-IVECO HONGYAN COMMERCIAL VEHICLE CO., LTD.

13.2.2 SINOTRUK (CNHTC)

13.2.3 DAYUN AUTO

13.2.4 DONGFENG MOTOR COMPANY

13.2.5 ZHEJIANG GEELY HOLDING GROUP

13.2.6 CHARIOT MOTORS

13.2.7 OTOKAR

13.2.8 KARSAN

13.2.9 RAMPINI CARLO S.P.A.

13.2.10 FIRST HYDROGEN

13.2.11 TEVVA

13.2.12 SANY GROUP

13.2.13 PACCAR INC.

13.2.14 WRIGHTBUS

13.2.15 HYZON

13.2.16 QINGLING ISUZU MOTORS IMPORT&EXPORT CO., LTD.

13.2.17 FAW JIEFANG AUTOMOTIVE CO., LTD.

13.2.18 AB VOLVO

14 RECOMMENDATIONS BY MARKETSANDMARKETS (Page No. - 333)

14.1 URBAN TRANSIT HYDROGEN BUSES TO GAIN TRACTION IN EUROPE

14.2 HYDROGEN TRUCKS FOR LONG-HAUL TRANSPORTATION

14.2.1 POTENTIAL OF HYDROGEN FUEL CELL TRUCKS IN NORTH AMERICA

14.3 CHINA TO BE MOST LUCRATIVE HYDROGEN BUS & TRUCK MARKET IN SHORT TERM

14.4 CONCLUSION

15 APPENDIX (Page No. - 335)

15.1 KEY INSIGHTS BY INDUSTRY EXPERTS

15.2 DISCUSSION GUIDE

15.3 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

15.4 CUSTOMIZATION OPTIONS

15.4.1 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE CLASS AT REGIONAL LEVEL

15.4.2 HYDROGEN BUS & TRUCK MARKET, ADDITIONAL COUNTRIES (UP TO THREE)

15.4.3 PROFILING OF ADDITIONAL MARKET PLAYERS (UP TO THREE)

15.5 RELATED REPORTS

15.6 AUTHOR DETAILS

LIST OF TABLES (267 TABLES)

TABLE 1 HYDROGEN BUS & TRUCK MARKET DEFINITION, BY MOTOR POWER

TABLE 2 HYDROGEN BUS & TRUCK MARKET DEFINITION, BY VEHICLE TYPE

TABLE 3 HYDROGEN BUS & TRUCK MARKET DEFINITION, BY RANGE

TABLE 4 HYDROGEN BUS & TRUCK MARKET DEFINITION, BY TYPE OF TANK

TABLE 5 HYDROGEN BUS & TRUCK MARKET DEFINITION, BY HYDROGEN TANK SIZE

TABLE 6 INCLUSIONS & EXCLUSIONS

TABLE 7 USD EXCHANGE RATES, 2019–2023

TABLE 8 FLEET PLANNING COMPARISON: ELECTRIC FLEET PLANNING VS. HYDROGEN FLEET PLANNING VS. ICE FLEET PLANNING

TABLE 9 COMPARISON OF TRUCKS: BEV, PHEV, FCEV, AND HEV CHARGING/REFUELING

TABLE 10 COMPARISON OF TRUCKS: FCEV HYDROGEN VS. BEV CHARGING/FUELING

TABLE 11 COMPARISON OF BUSES: FCEV HYDROGEN VS. BEV CHARGING/FUELING

TABLE 12 COMPARISON OF BUSES: FCEV HYDROGEN VS. BEV CHARGING/FUELING

TABLE 13 FCEV TRUCK COMPARISON

TABLE 14 FCEV BUS COMPARISON

TABLE 15 HYDROGEN BUS & TRUCK MARKET DYNAMICS: IMPACT ANALYSIS

TABLE 16 AVERAGE SELLING PRICES OF KEY PLAYERS FOR HYDROGEN BUSES, 2020–2023 (USD THOUSAND)

TABLE 17 AVERAGE SELLING PRICES OF KEY OEMS FOR HYDROGEN TRUCKS, 2020–2023 (USD THOUSAND)

TABLE 18 AVERAGE SELLING PRICES OF HYDROGEN BUSES, BY REGION, 2020–2023 (USD THOUSAND)

TABLE 19 AVERAGE SELLING PRICES OF HYDROGEN TRUCKS, BY REGION, 2020–2023 (USD THOUSAND)

TABLE 20 ROLE OF PLAYERS IN ECOSYSTEM

TABLE 21 FOTON INTERNATIONAL: FCEV STRATEGIES

TABLE 22 XIAMEN KING LONG INTERNATIONAL TRADING CO., LTD.: FCEV STRATEGIES

TABLE 23 YUTONG BUS CO., LTD.: FCEV STRATEGIES

TABLE 24 SOLARIS BUS & COACH SP. Z.O.O.: FCEV STRATEGIES

TABLE 25 HYUNDAI MOTOR COMPANY: FCEV STRATEGIES

TABLE 26 HYDROGEN BUS & TRUCK MARKET: BUSINESS MODELS

TABLE 27 US: FUEL CELL ELECTRIC BUS PROJECTS

TABLE 28 FUEL CELL BUS DEVELOPMENT AND DEPLOYMENT ANNOUNCEMENT

TABLE 29 HYDROGEN TRUCKS: EXISTING AND UPCOMING FCEV MODELS

TABLE 30 HYDROGEN BUSES: EXISTING AND UPCOMING FCEV MODELS

TABLE 31 EXISTING AND UPCOMING H2ICE MODELS

TABLE 32 EXPORT DATA FOR HS CODE: 8702, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 33 EXPORT DATA FOR HS CODE: 8703, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 34 IMPORT DATA FOR HS CODE: 8702, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 35 IMPORT DATA FOR HS CODE: 8703, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 36 BILL OF MATERIAL COMPARISON BETWEEN FCEV, ICE, AND BEV BUSES (USD THOUSAND)

TABLE 37 BILL OF MATERIAL COMPARISON BETWEEN FCEV, ICE, AND BEV TRUCKS (USD THOUSAND)

TABLE 38 LIST OF PATENTS GRANTED IN HYDROGEN BUS & TRUCK MARKET, 2021–2024

TABLE 39 NORTH AMERICA: POLICIES AND INITIATIVES SUPPORTING HYDROGEN-POWERED VEHICLES AND INFRASTRUCTURE

TABLE 40 EUROPE: POLICIES AND INITIATIVES SUPPORTING HYDROGEN-POWERED VEHICLES AND INFRASTRUCTURE

TABLE 41 ASIA PACIFIC: POLICIES AND INITIATIVES SUPPORTING HYDROGEN-POWERED VEHICLES AND INFRASTRUCTURE

TABLE 42 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 43 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 44 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 45 COMPARISON OF H2ICE AND FCEV

TABLE 46 LIST OF CONFERENCES & EVENTS, 2024–2025

TABLE 47 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF HYDROGEN BUSES AND TRUCKS (%)

TABLE 48 KEY BUYING CRITERIA FOR HYDROGEN BUSES AND TRUCKS, BY VEHICLE TYPE

TABLE 49 LIST OF FUNDING MADE BY PLAYERS, 2021−2022

TABLE 50 HYDROGEN BUS & TRUCK MARKET, BY MOTOR POWER, 2020–2023 (UNITS)

TABLE 51 HYDROGEN BUS & TRUCK MARKET, BY MOTOR POWER, 2024–2030 (UNITS)

TABLE 52 HYDROGEN BUS & TRUCK MARKET, BY MOTOR POWER, 2031–2035 (UNITS)

TABLE 53 UP TO 200 KW: HYDROGEN BUS MODELS

TABLE 54 UP TO 200 KW: HYDROGEN TRUCK MODELS

TABLE 55 UP TO 200 KW: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 56 UP TO 200 KW: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 57 UP TO 200 KW: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 58 200–400 KW: HYDROGEN BUS MODELS

TABLE 59 200–400 KW: HYDROGEN TRUCK MODELS

TABLE 60 200–400 KW: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 61 200–400 KW: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 62 200–400 KW: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 63 ABOVE 400 KW: HYDROGEN BUS MODELS

TABLE 64 ABOVE 400 KW: HYDROGEN TRUCK MODELS

TABLE 65 ABOVE 400 KW: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 66 ABOVE 400 KW: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 67 ABOVE 400 KW: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 68 HYDROGEN BUS & TRUCK MARKET, BY RANGE, 2020–2023 (UNITS)

TABLE 69 HYDROGEN BUS & TRUCK MARKET, BY RANGE, 2024–2030 (UNITS)

TABLE 70 HYDROGEN BUS & TRUCK MARKET, BY RANGE, 2031–2035 (UNITS)

TABLE 71 UP TO 300 MILES: HYDROGEN BUS MODELS

TABLE 72 UP TO 300 MILES: HYDROGEN TRUCK MODELS

TABLE 73 UP TO 300 MILES: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2020–2023 (UNITS)

TABLE 74 UP TO 300 MILES: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2024–2030 (UNITS)

TABLE 75 UP TO 300 MILES: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2031–2035 (UNITS)

TABLE 76 300–500 MILES: HYDROGEN BUS MODELS

TABLE 77 300–500 MILES: HYDROGEN TRUCK MODELS

TABLE 78 300–500 MILES: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2020–2023 (UNITS)

TABLE 79 300–500 MILES: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2024–2030 (UNITS)

TABLE 80 300–500 MILES: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2031–2035 (UNITS)

TABLE 81 ABOVE 500 MILES: HYDROGEN BUS MODELS

TABLE 82 ABOVE 500 MILES: HYDROGEN TRUCK MODELS

TABLE 83 ABOVE 500 MILES: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2020–2023 (UNITS)

TABLE 84 ABOVE 500 MILES: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2024–2030 (UNITS)

TABLE 85 ABOVE 500 MILES: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2031–2035 (UNITS)

TABLE 86 HYDROGEN BUS & TRUCK MARKET, BY HYDROGEN TANK SIZE, 2020–2023 (UNITS)

TABLE 87 HYDROGEN BUS & TRUCK MARKET, BY HYDROGEN TANK SIZE, 2024–2030 (UNITS)

TABLE 88 HYDROGEN BUS & TRUCK MARKET, BY HYDROGEN TANK SIZE, 2031–2035 (UNITS)

TABLE 89 < 30 KG: HYDROGEN BUS AND TRUCK MODELS

TABLE 90 < 30 KG: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 91 < 30 KG: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 92 < 30 KG: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 93 30–60 KG: HYDROGEN BUS AND TRUCK MODELS

TABLE 94 30–60 KG: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 95 30–60 KG: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 96 30–60 KG: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 97 > 60 KG: HYDROGEN BUS AND TRUCK MODELS

TABLE 98 > 60 KG: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 99 > 60 KG: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 100 > 60 KG: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 101 HYDROGEN TANK TYPE CLASSIFICATION FOR AUTOMOTIVE APPLICATION

TABLE 102 HYDROGEN BUS & TRUCK MARKET, BY TYPE OF TANK, 2020–2023 (UNITS)

TABLE 103 HYDROGEN BUS & TRUCK MARKET, BY TYPE OF TANK, 2024–2030 (UNITS)

TABLE 104 HYDROGEN BUS & TRUCK MARKET, BY TYPE OF TANK, 2031–2035 (UNITS)

TABLE 105 HYDROGEN BUSES WITH TYPE III HYDROGEN TANKS

TABLE 106 HYDROGEN TRUCKS WITH TYPE III HYDROGEN TANKS

TABLE 107 TYPE III: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 108 TYPE III: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 109 TYPE III: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 110 HYDROGEN BUSES WITH TYPE IV HYDROGEN TANKS

TABLE 111 HYDROGEN TRUCKS WITH TYPE IV HYDROGEN TANKS

TABLE 112 TYPE IV: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 113 TYPE IV: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 114 TYPE IV: HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 115 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (USD MILLION)

TABLE 116 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (USD MILLION)

TABLE 117 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (USD MILLION)

TABLE 118 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 119 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 120 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 121 HYDROGEN BUSES MARKET, BY REGION, 2020–2023 (USD MILLION)

TABLE 122 HYDROGEN BUSES MARKET, BY REGION, 2024–2030 (USD MILLION)

TABLE 123 HYDROGEN BUSES MARKET, BY REGION, 2031–2035 (USD MILLION)

TABLE 124 HYDROGEN BUSES MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 125 HYDROGEN BUSES MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 126 HYDROGEN BUSES MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 127 HYDROGEN MINIBUS/SHUTTLE MODELS

TABLE 128 HYDROGEN CITY/TRANSIT BUS MODELS

TABLE 129 CLASSIFICATION OF HYDROGEN TRUCKS BY GVW

TABLE 130 HYDROGEN TRUCKS MARKET, BY REGION, 2020–2023 (USD MILLION)

TABLE 131 HYDROGEN TRUCKS MARKET, BY REGION, 2024–2030 (USD MILLION)

TABLE 132 HYDROGEN TRUCKS MARKET, BY REGION, 2031–2035 (USD MILLION)

TABLE 133 HYDROGEN TRUCKS MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 134 HYDROGEN TRUCKS MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 135 HYDROGEN TRUCKS MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 136 HYDROGEN MEDIUM-DUTY TRUCK MODELS

TABLE 137 HYDROGEN HEAVY-DUTY TRUCK MODELS

TABLE 138 HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (USD MILLION)

TABLE 139 HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (USD MILLION)

TABLE 140 HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (USD MILLION)

TABLE 141 HYDROGEN BUS & TRUCK MARKET, BY REGION, 2020–2023 (UNITS)

TABLE 142 HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024–2030 (UNITS)

TABLE 143 HYDROGEN BUS & TRUCK MARKET, BY REGION, 2031–2035 (UNITS)

TABLE 144 INITIATIVES TAKEN BY MAJOR COUNTRIES TO PROMOTE USE OF HYDROGEN BUSES AND TRUCKS

TABLE 145 ASIA PACIFIC HYDROGEN BUS & TRUCK MARKET: UPCOMING PROJECTS

TABLE 146 ASIA PACIFIC: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2020–2023 (UNITS)

TABLE 147 ASIA PACIFIC: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2024–2030 (UNITS)

TABLE 148 ASIA PACIFIC: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2031–2035 (UNITS)

TABLE 149 CHINA: STRATEGIES TO PROMOTE PRODUCTION OF HYDROGEN-POWERED VEHICLES

TABLE 150 CHINA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 151 CHINA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 152 CHINA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 153 JAPAN: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 154 JAPAN: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 155 JAPAN: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 156 SOUTH KOREA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 157 SOUTH KOREA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 158 SOUTH KOREA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 159 INDIA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 160 INDIA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 161 INDIA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 162 EUROPE: TARGETS, VISIONS, AND PROJECTIONS

TABLE 163 EUROPE: HYDROGEN BUS & TRUCK MARKET: ONGOING PROJECTS

TABLE 164 EUROPE: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2020–2023 (UNITS)

TABLE 165 EUROPE: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2024–2030 (UNITS)

TABLE 166 EUROPE: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2031–2035 (UNITS)

TABLE 167 FRANCE: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 168 FRANCE: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 169 FRANCE: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 170 GERMANY: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 171 GERMANY: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 172 GERMANY: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 173 ITALY: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 174 ITALY: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 175 ITALY: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 176 SPAIN: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 177 SPAIN: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 178 SPAIN: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 179 UK: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 180 UK: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 181 UK: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 182 NORTH AMERICA: HYDROGEN BUS & TRUCK MARKET: UPCOMING PROJECTS

TABLE 183 NORTH AMERICA: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2020–2023 (UNITS)

TABLE 184 NORTH AMERICA: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2024–2030 (UNITS)

TABLE 185 NORTH AMERICA: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2031–2035 (UNITS)

TABLE 186 CANADA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 187 CANADA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 188 CANADA: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 189 US: TARGETS, VISIONS, AND PROJECTIONS

TABLE 190 US: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2020–2023 (UNITS)

TABLE 191 US: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2024–2030 (UNITS)

TABLE 192 US: HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE, 2031–2035 (UNITS)

TABLE 193 OVERVIEW OF STRATEGIES DEPLOYED BY KEY PLAYERS IN HYDROGEN BUS & TRUCK MARKET

TABLE 194 MARKET SHARE ANALYSIS, 2023

TABLE 195 COMPANY REGIONAL FOOTPRINT

TABLE 196 COMPANY VEHICLE TYPE FOOTPRINT

TABLE 197 DETAILED LIST OF KEY STARTUPS/SMES

TABLE 198 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 199 HYDROGEN BUS & TRUCK MARKET: PRODUCT LAUNCHES & DEVELOPMENTS, 2021–2024

TABLE 200 HYDROGEN BUS & TRUCK MARKET: DEALS, 2021–2024

TABLE 201 HYDROGEN BUS & TRUCK MARKET: EXPANSION, 2021–2024

TABLE 202 HYDROGEN BUS & TRUCK MARKET: OTHER DEVELOPMENTS, 2021–2024

TABLE 203 FOTON INTERNATIONAL: COMPANY OVERVIEW

TABLE 204 FOTON INTERNATIONAL: PRODUCTS/SOLUTIONS OFFERED

TABLE 205 FOTON INTERNATIONAL: PRODUCT LAUNCHES & ENHANCEMENTS

TABLE 206 FOTON INTERNATIONAL: DEALS

TABLE 207 FOTON INTERNATIONAL: EXPANSION

TABLE 208 FOTON INTERNATIONAL: OTHER DEVELOPMENTS

TABLE 209 YUTONG BUS CO., LTD.: COMPANY OVERVIEW

TABLE 210 YUTONG BUS CO., LTD.: PRODUCTS/SOLUTIONS OFFERED

TABLE 211 YUTONG BUS CO., LTD.: PRODUCT LAUNCHES & ENHANCEMENTS

TABLE 212 YUTONG BUS CO., LTD.: DEALS

TABLE 213 YUTONG BUS CO., LTD.: EXPANSION

TABLE 214 YUTONG BUS CO., LTD.: OTHER DEVELOPMENTS

TABLE 215 XIAMEN KING LONG INTERNATIONAL TRADING CO., LTD.: COMPANY OVERVIEW

TABLE 216 XIAMEN KING LONG INTERNATIONAL TRADING CO., LTD.: PRODUCTS/SOLUTIONS OFFERED

TABLE 217 XIAMEN KING LONG INTERNATIONAL TRADING CO., LTD.: DEALS

TABLE 218 XIAMEN KING LONG INTERNATIONAL TRADING CO., LTD.: OTHER DEVELOPMENTS

TABLE 219 SOLARIS BUS & COACH SP. Z O.O.: COMPANY OVERVIEW

TABLE 220 SOLARIS BUS & COACH SP. Z O.O.: PRODUCTS/SOLUTIONS OFFERED

TABLE 221 SOLARIS BUS & COACH SP. Z O.O.: PRODUCT LAUNCHES & ENHANCEMENTS

TABLE 222 SOLARIS BUS & COACH SP. Z O.O.: DEALS

TABLE 223 SOLARIS BUS & COACH SP. Z O.O.: OTHER DEVELOPMENTS

TABLE 224 HYUNDAI MOTOR CORPORATION: COMPANY OVERVIEW

TABLE 225 HYUNDAI MOTOR CORPORATION: PRODUCTS/SOLUTIONS OFFERED

TABLE 226 HYUNDAI MOTOR CORPORATION: DEALS

TABLE 227 HYUNDAI MOTOR CORPORATION: OTHER DEVELOPMENTS

TABLE 228 ANHUI ANKAI AUTOMOBILE CO., LTD: COMPANY OVERVIEW

TABLE 229 ANHUI ANKAI AUTOMOBILE CO., LTD: PRODUCTS/SOLUTIONS OFFERED

TABLE 230 ANHUI ANKAI AUTOMOBILE CO., LTD: PRODUCT LAUNCHES & ENHANCEMENTS

TABLE 231 ANHUI ANKAI AUTOMOBILE CO., LTD: OTHER DEVELOPMENTS

TABLE 232 NIKOLA CORPORATION: COMPANY OVERVIEW

TABLE 233 NIKOLA CORPORATION: PRODUCTS/SOLUTIONS OFFERED

TABLE 234 NIKOLA CORPORATION: PRODUCT LAUNCHES & ENHANCEMENTS

TABLE 235 NIKOLA CORPORATION: DEALS

TABLE 236 NIKOLA CORPORATION: EXPANSION

TABLE 237 NIKOLA CORPORATION: OTHER DEVELOPMENTS

TABLE 238 TOYOTA MOTOR CORPORATION: COMPANY OVERVIEW

TABLE 239 TOYOTA MOTOR CORPORATION: PRODUCTS/SOLUTIONS OFFERED

TABLE 240 TOYOTA MOTOR CORPORATION: DEALS

TABLE 241 TOYOTA MOTOR CORPORATION: OTHER DEVELOPMENTS

TABLE 242 VDL GROEP: COMPANY OVERVIEW

TABLE 243 VDL GROEP: PRODUCTS/SOLUTIONS OFFERED

TABLE 244 VDL GROEP: PRODUCT LAUNCHES & ENHANCEMENTS

TABLE 245 VDL GROEP: DEALS

TABLE 246 VDL GROEP: EXPANSION

TABLE 247 VDL GROEP: OTHER DEVELOPMENTS

TABLE 248 NFI GROUP: COMPANY OVERVIEW

TABLE 249 NFI GROUP: PRODUCTS/SOLUTIONS OFFERED

TABLE 250 NFI GROUP: PRODUCT LAUNCHES & DEVELOPMENTS

TABLE 251 NFI GROUP: DEALS

TABLE 252 NFI GROUP: OTHER DEVELOPMENTS

TABLE 253 ZHONGTONG BUS HOLDING CO., LTD.: COMPANY OVERVIEW

TABLE 254 ZHONGTONG BUS HOLDING CO., LTD.: PRODUCTS/SOLUTIONS OFFERED

TABLE 255 ZHONGTONG BUS HOLDING CO., LTD.: PRODUCT LAUNCHES & ENHANCEMENTS

TABLE 256 ZHONGTONG BUS HOLDING CO., LTD.: DEALS

TABLE 257 DAIMLER TRUCK AG: COMPANY OVERVIEW

TABLE 258 DAIMLER TRUCK AG: PRODUCTS/SOLUTIONS OFFERED

TABLE 259 DAIMLER TRUCK AG: PRODUCT LAUNCHES & ENHANCEMENTS

TABLE 260 DAIMLER TRUCK AG: DEALS

TABLE 261 DAIMLER TRUCK AG: EXPANSION

TABLE 262 DAIMLER TRUCK AG: OTHER DEVELOPMENTS

TABLE 263 IVECO S.P.A.: COMPANY OVERVIEW

TABLE 264 IVECO S.P.A.: PRODUCTS/SOLUTIONS OFFERED

TABLE 265 IVECO S.P.A.: DEALS

TABLE 266 IVECO S.P.A.: EXPANSION

TABLE 267 IVECO S.P.A.: OTHER DEVELOPMENTS

LIST OF FIGURES (106 FIGURES)

FIGURE 1 RESEARCH DESIGN

FIGURE 2 RESEARCH PROCESS FLOW

FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

FIGURE 4 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY FOR HYDROGEN BUS & TRUCK MARKET: BOTTOM-UP APPROACH

FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY FOR HYDROGEN BUS & TRUCK MARKET: TOP-DOWN APPROACH

FIGURE 7 HYDROGEN BUS & TRUCK MARKET: RESEARCH DESIGN & METHODOLOGY

FIGURE 8 DATA TRIANGULATION

FIGURE 9 MARKET GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS

FIGURE 10 DEMAND AND SUPPLY-SIDE FACTOR ANALYSIS

FIGURE 11 REPORT SUMMARY

FIGURE 12 HYDROGEN BUS & TRUCK MARKET, BY REGION

FIGURE 13 HYDROGEN BUS & TRUCK MARKET, BY VEHICLE TYPE

FIGURE 14 HYDROGEN BUS & TRUCK MARKET, BY TYPE OF TANK

FIGURE 15 KEY PLAYERS IN HYDROGEN BUS & TRUCK MARKET

FIGURE 16 RISING ENVIRONMENTAL CONCERNS AND EXPANSION OF HYDROGEN INFRASTRUCTURE TO DRIVE GROWTH

FIGURE 17 HYDROGEN TRUCKS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 18 TYPE IV SEGMENT TO ACCOUNT FOR SIGNIFICANT SHARE BY 2035

FIGURE 19 30–60 KG SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 20 300–500 MILES SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 21 200–400 KW SEGMENT TO ACCOUNT FOR LARGEST SHARE BY 2035

FIGURE 22 ASIA PACIFIC TO BE LARGEST MARKET IN 2024

FIGURE 23 WORKING PRINCIPLE OF HYDROGEN BUSES

FIGURE 24 COMPONENTS OF HYDROGEN TRUCKS

FIGURE 25 HYDROGEN BUS & TRUCK MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 26 FLEET DECARBONIZATION PROCESS

FIGURE 27 PACIFIC NORTHWEST HYDROGEN HUB LED BY GOVERNMENT INITIATIVES

FIGURE 28 DISPENSED COST BUILD-UP FOR FUTURE TRANSPORTATION FUEL TYPES

FIGURE 29 COMPARISON OF AUTOIGNITION TEMPERATURE OF VARIOUS FUEL TYPES

FIGURE 30 COMPARISON OF MINIMUM IGNITION ENERGY FOR VARIOUS FUEL TYPES

FIGURE 31 MOBILE HYDROGEN REFUELING STATION MODEL IN JAPAN

FIGURE 32 HYDROGEN PRODUCTION WITH INTEGRATION OF RENEWABLE ENERGY

FIGURE 33 HYDROGEN CORRIDORS PLANNED BY EHB

FIGURE 34 HYDROGEN CORRIDORS: INFRASTRUCTURE COMPANIES

FIGURE 35 HYDROGEN STORAGE AND TRANSPORTATION

FIGURE 36 AVERAGE SELLING PRICES OF KEY PLAYERS FOR HYDROGEN BUSES, 2020–2023 (USD THOUSAND)

FIGURE 37 AVERAGE SELLING PRICES OF KEY OEMS FOR HYDROGEN TRUCKS, 2020–2023 (USD THOUSAND)

FIGURE 38 HYDROGEN BUSES MARKET: AVERAGE SELLING PRICE TREND, BY REGION

FIGURE 39 HYDROGEN TRUCKS MARKET: AVERAGE SELLING PRICE TREND, BY REGION

FIGURE 40 ECOSYSTEM ANALYSIS

FIGURE 41 HYDROGEN BUS & TRUCK MARKET: VALUE CHAIN ANALYSIS

FIGURE 42 GLOBAL PUBLIC HYDROGEN REFUELING STATIONS: 2023

FIGURE 43 GLOBAL HYDROGEN PROJECTS: 2023

FIGURE 44 FUEL CELL BUSES IN OPERATION: 2023

FIGURE 45 HYDROGEN BUSES: FUEL CAPACITY VS. RANGE

FIGURE 46 HYDROGEN TRUCKS: FUEL CAPACITY VS. RANGE

FIGURE 47 TIMELINE OF H2ICE TECHNOLOGY, 2017−2030

FIGURE 48 BEV VS. FCEV TRUCKS: 10-YEAR TOTAL COST OF OWNERSHIP BREAKDOWN

FIGURE 49 BEV BUSES VS. FCEV BUSES: 10-YEAR TOTAL COST OF OWNERSHIP BREAKDOWN

FIGURE 50 BILL OF MATERIAL COMPARISON BETWEEN FCEV, ICE, AND BEV BUSES (USD THOUSAND)

FIGURE 51 BILL OF MATERIAL COMPARISON BETWEEN FCEV, ICE, AND BEV TRUCKS (USD THOUSAND)

FIGURE 52 NUMBER OF PATENTS GRANTED FOR HYDROGEN BUSES AND TRUCKS, 2013–2024

FIGURE 53 TECHNOLOGY ROADMAP FOR FCEVS

FIGURE 54 WORKING OF DIRECT BOROHYDRIDE FUEL CELLS

FIGURE 55 TOYOTA’S NEW PACKAGED FUEL CELL SYSTEM MODULE

FIGURE 56 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF HYDROGEN BUSES AND TRUCKS

FIGURE 57 KEY BUYING CRITERIA FOR HYDROGEN BUSES AND TRUCKS, BY VEHICLE TYPE

FIGURE 58 INVESTMENT & FUNDING SCENARIO, 2021−2024

FIGURE 59 200–400 KW SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 60 300–500 MILES SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 61 30–60 KG SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 62 TYPE IV SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 63 HYDROGEN TRUCKS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 64 HYDROGEN BUS & TRUCK MARKET, BY REGION, 2024 VS. 2035 (USD MILLION)

FIGURE 65 ASIA PACIFIC: HYDROGEN BUS & TRUCK MARKET SNAPSHOT

FIGURE 66 ASIA PACIFIC: REAL GDP GROWTH RATE, BY COUNTRY, 2023–2025

FIGURE 67 ASIA PACIFIC: GDP PER CAPITA, BY COUNTRY, 2023–2025

FIGURE 68 ASIA PACIFIC: INFLATION RATE (CONSUMER PRICE INDEX), BY COUNTRY, 2023–2025

FIGURE 69 ASIA PACIFIC: MANUFACTURING INDUSTRY’S CONTRIBUTION TO GDP, 2023 (USD TRILLION)

FIGURE 70 CHINA: ROADMAP AND STRATEGY FOR HYDROGEN-POWERED VEHICLES, 2020–2030

FIGURE 71 JAPAN: ROADMAP AND STRATEGY FOR HYDROGEN-POWERED VEHICLES, 2020–2030

FIGURE 72 SOUTH KOREA: ROADMAP AND STRATEGY FOR HYDROGEN GENERATION, 2020–2035

FIGURE 73 EUROPE: ROADMAP FOR HYDROGEN PRODUCTION

FIGURE 74 EUROPE: ROADMAP FOR HYDROGEN BUSES

FIGURE 75 EUROPE: HYDROGEN BUS & TRUCK MARKET, BY COUNTRY, 2024–2035 (UNITS)

FIGURE 76 EUROPE: REAL GDP GROWTH RATE, BY COUNTRY, 2023–2025

FIGURE 77 EUROPE: GDP PER CAPITA, BY COUNTRY, 2023–2025

FIGURE 78 EUROPE: INFLATION RATE (CONSUMER PRICE INDEX) BY COUNTRY, 2023–2025

FIGURE 79 EUROPE: MANUFACTURING INDUSTRY’S CONTRIBUTION TO GDP, 2023 (USD TRILLION)

FIGURE 80 UK: HYDROGEN NET ZERO INVESTMENT ROADMAP, 2021–2035

FIGURE 81 NORTH AMERICA: HYDROGEN BUS & TRUCK MARKET SNAPSHOT

FIGURE 82 NORTH AMERICA: REAL GDP GROWTH RATE, BY COUNTRY, 2023–2025

FIGURE 83 NORTH AMERICA: GDP PER CAPITA, BY COUNTRY, 2023–2025

FIGURE 84 NORTH AMERICA: INFLATION RATE (CONSUMER PRICE INDEX), BY COUNTRY, 2023–2025

FIGURE 85 NORTH AMERICA: MANUFACTURING INDUSTRY’S CONTRIBUTION TO GDP, 2023 (USD TRILLION)

FIGURE 86 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2022

FIGURE 87 REVENUE ANALYSIS OF KEY PLAYERS, 2019–2023

FIGURE 88 COMPANY VALUATION OF KEY PLAYERS

FIGURE 89 FINANCIAL METRICS OF KEY PLAYERS

FIGURE 90 BRAND/PRODUCT COMPARISON OF TOP FIVE PLAYERS

FIGURE 91 HYDROGEN BUS & TRUCK MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

FIGURE 92 HYDROGEN BUS & TRUCK MARKET: COMPANY FOOTPRINT, 2023

FIGURE 93 HYDROGEN BUS & TRUCK MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

FIGURE 94 FOTON INTERNATIONAL: COMPANY SNAPSHOT

FIGURE 95 YUTONG BUS CO., LTD.: COMPANY SNAPSHOT

FIGURE 96 XIAMEN KING LONG INTERNATIONAL TRADING CO., LTD.: COMPANY SNAPSHOT

FIGURE 97 SOLARIS BUS & COACH SP. Z O.O.: COMPANY SNAPSHOT

FIGURE 98 HYUNDAI MOTOR CORPORATION: COMPANY SNAPSHOT (2023)

FIGURE 99 ANHUI ANKAI AUTOMOBILE CO., LTD: COMPANY SNAPSHOT

FIGURE 100 NIKOLA CORPORATION: COMPANY SNAPSHOT

FIGURE 101 TOYOTA MOTOR CORPORATION: COMPANY SNAPSHOT

FIGURE 102 VDL GROEP: COMPANY SNAPSHOT

FIGURE 103 NFI GROUP: COMPANY SNAPSHOT

FIGURE 104 ZHONGTONG BUS HOLDING CO., LTD.: COMPANY SNAPSHOT

FIGURE 105 DAIMLER TRUCK AG: COMPANY SNAPSHOT

FIGURE 106 IVECO S.P.A.: COMPANY SNAPSHOT

HIGHEST CAGR MARKET IN 2024-35

HIGHEST CAGR MARKET IN 2024-35 CHINA: FASTEST GROWING MARKET IN THE REGION

CHINA: FASTEST GROWING MARKET IN THE REGION

Growth opportunities and latent adjacency in Hydrogen Truck Market