The study involves four major activities that estimate the size of the in-plant logistics market. Exhaustive secondary research was conducted to collect information related to the market. Following this was validating these findings, assumptions, and sizing with the industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the overall size of the in-plant logistics market. Subsequently, market breakdown and data triangulation procedures were used to determine the extent of different segments and subsegments of the market.

Secondary Research

Secondary sources in this research study include corporate filings (such as annual reports, investor presentations, and financial statements); trade, business, and professional associations; white papers, certified publications, articles from recognized authors; directories; and databases. The secondary data were collected and analyzed to estimate the overall market size, further validated by primary research.

Primary Research

In the primary research process, numerous sources from both the supply and demand sides were interviewed to obtain qualitative and quantitative information about this report. The primary sources from the supply side included various industry experts such as Chief X Officers (CXOs), Vice Presidents (VPs), and Directors from business development, marketing, product development/innovation teams, and related key executives from in-plant logistics providers, such as Daifuku Co., Ltd. (Japan), JBT (US), KION GROUP AG (Germany), KUKA AG (Germany), and Toyota Industries Corporation (Japan); research organizations, distributors, professional and managed service providers, industry associations, and key opinion leaders. Approximately 25% of the primary interviews were conducted with the demand side and 75% with the supply side. These data were collected mainly through questionnaires, emails, and telephonic interviews, accounting for 80% of the primary interviews.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

In the market engineering process, both top-down and bottom-up approaches were implemented, along with several data triangulation methods, to estimate and validate the size of the market and other dependent submarkets listed in this report.

-

The key players in the industry and markets were identified through extensive secondary research.

-

Both the supply chain of the industry and the market size, in terms of value, were determined through primary and secondary research.

-

All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources.

-

Market Size Estimation Methodology-Bottom-up Approach and Top-down Approach

Data Triangulation

After estimating the overall market size, the total market was split into several segments. The market breakdown and data triangulation procedures were employed wherever applicable to complete the overall market engineering process and gauge exact statistics for all segments. The data were triangulated by studying various factors and trends from both the demand and supply sides. The market was also validated using both top-down and bottom-up approaches.

Market Definition

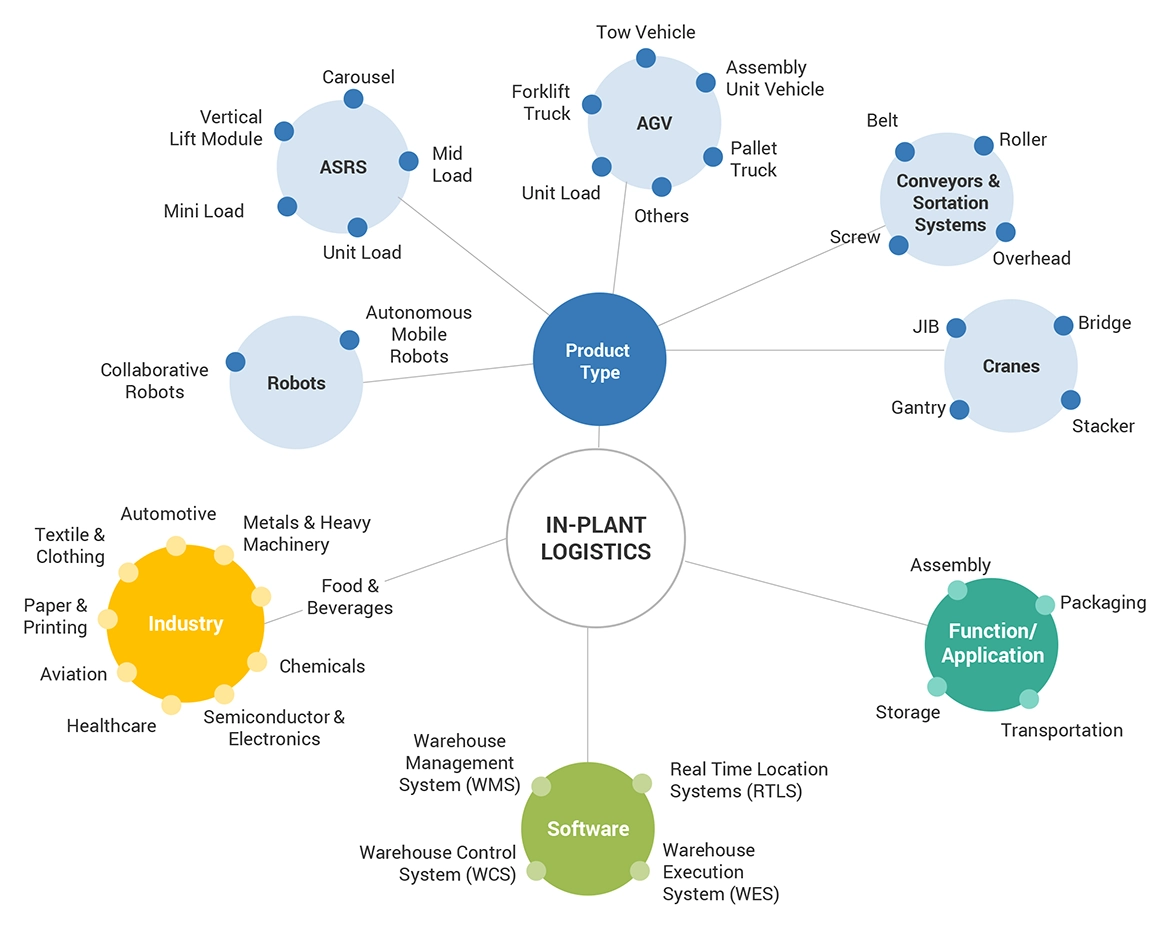

In-plant logistics refers to the management and coordination of material flow, storage, and distribution within a manufacturing or production facility. It involves optimizing the movement of raw materials, components, and finished products within the confines of the plant, aiming to enhance efficiency and reduce operational costs. This specialized branch of logistics focuses on streamlining processes such as inventory management, order fulfillment, and transportation within the facility to ensure a smooth and timely production cycle. In-plant logistics plays a crucial role in minimizing lead times, preventing bottlenecks, and maximizing the utilization of resources within the manufacturing environment.

The key objectives of in-plant logistics include minimizing idle time for both labor and equipment, optimizing storage space, and ensuring that the right materials are available at the right place and time for the production process. This involves the use of advanced technologies, such as warehouse management systems (WMS) and automated guided vehicles (AGVs), to facilitate efficient material handling and tracking. By focusing on the internal movements of goods within a facility, in-plant logistics contributes to overall supply chain effectiveness, enhancing the competitiveness of the manufacturing operation in terms of cost, speed, and responsiveness to market demands. We are considering only the products used for logistics activities related to manufacturing plant plants for production and storage.

Stakeholders

-

Integrators of material handling systems

-

Warehousing companies

-

Government bodies, venture capitalists, and private equity firms

-

Original device manufacturers (ODMs)

-

Original equipment manufacturers (OEMs)

-

Manufacturers of automated material handling equipment

-

Research organizations, forums, alliances, and associations

-

Software and service providers

The main objectives of this study are as follows:

-

To describe and forecast the in-plant logistics market, by product, location, and industry, in terms of value

-

To forecast the market size, in terms of value, for four main regions, namely, North America, Europe, Asia Pacific, and Rest of the World (RoW)

-

To provide information on the services involved in in-plant logistics system

-

To provide detailed information regarding the drivers, restraints, opportunities, and challenges influencing the growth of the market

-

To analyze the probable impact of the recession on the market in the future

-

To provide a comprehensive overview of the value chain of the in-plant logistics ecosystem

-

To analyze competitive developments, such as product launches, acquisitions, collaborations, agreements, and partnerships, in the in-plant logistics market

-

To strategically analyze micromarkets1 with respect to individual growth trends, prospects, and contributions to the total market

-

To strategically profile key players and comprehensively analyze their market positions in terms of ranking and core competencies2, and provide a detailed competitive landscape of the market

Available Customizations:

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

Country-wise Information:

-

Analysis for additional countries (up to five)

Company Information:

-

Detailed analysis and profiling of different market players (up to five)

Growth opportunities and latent adjacency in In-Plant Logistics Market