OTA Testing Market Size, Share & Growth Analysis, 2029

Download PDF

Download PDF Request Customisation

Request CustomisationOTA Testing Market by Test Chambers, Antenna Testing Solutions, Software, Services, 5G, LTE, UMTS, GSM, CDMA, Wi-Fi, Bluetooth, Smartphones, Laptops, Notebooks & Tablets, Wearables, Automotive & Transportation and Smart Cities - Global Forecast to 2029

OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

The OTA testing market is projected to grow from USD 2.23 billion in 2024 to USD 3.17 billion by 2029, registering a CAGR of 7.3% during the forecast period (2024–2029). Growth is driven by increasing adoption of 5G and advanced wireless technologies, rising complexity of antenna and RF designs, and expanding use of connected devices across automotive, consumer electronics, and industrial IoT applications.

KEY TAKEAWAYS

-

BY REGIONBy region, the market accounted for a share of 39.7% in 2024.

-

BY OFFERINGBy offering, the services segment is expected to dominate the OTA testing market.

-

BY TECHNOLOGYBy technology, the cellular network segment is projected to register the fastest growth during the forecast period.

-

BY END USERSBy end user, the consumer devices segment is expected to dominate the OTA testing market.

-

COMPETITIVE LANDSCAPERohde & Schwarz, Keysight Technologies, Anritsu, SGS SA, Intertek Group plc, and UL LLC, among others, were identified as star players in the OTA testing market, supported by their strong financial capabilities, well-established brand equity, comprehensive service portfolios, and global operational presence.

-

COMPETITIVE LANDSCAPEOrbis Systems Oy, Copper Mountain Technologies, and Millibox have distinguished themselves as progressive companies in the OTA testing market due to their expanding solution offerings, agile business models, and increasing focus on niche and high-growth OTA testing applications.

The OTA testing market is witnessing steady growth, driven by increasing adoption of 5G and advanced wireless technologies, rising antenna and RF design complexity, and the proliferation of connected devices. Growing demand for multi-antenna, multi-band, and mmWave validation is improving test accuracy, real-world performance assessment, and certification efficiency. Advancements in automated OTA platforms, AI-driven analytics, and compact antenna test environments are further reshaping the market landscape.

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The OTA testing industry is undergoing a structural shift as customers move from legacy, instrument-based RF validation toward advanced, real-world wireless performance testing solutions. While past revenues were driven by vector network analyzers, spectrum analyzers, and basic anechoic chambers, future growth is increasingly supported by compact antenna test ranges (CATR), massive MIMO OTA systems, 5G NR signal analyzers, and AI-powered automated test platforms. Rising adoption of 5G NR (FR1 and FR2), Wi-Fi 6/6E/7, Bluetooth Low Energy, NB-IoT, and V2X technologies is reshaping client imperatives across consumer devices, automotive and transportation, industrial, and smart city applications. This transition reflects a broader industry shift toward multi-technology, software-enabled, and high-throughput OTA testing platforms that support faster validation cycles, improved wireless reliability, and scalable deployment, creating new revenue opportunities across developed and emerging markets.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Level

-

Rising Demand for Wireless Consumer Device

-

Growing adoption of 5G technology

Level

-

High cost of OTA testing equipment

-

Complexity of OTA testing procedures

Level

-

Advancements in autonomous vehicles

-

Growth in smart city initiatives and infrastructures

Level

-

Rapidly Evolving Wireless Standards and Technologies

-

Simulating Real-World Conditions in Laboratory Environments

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Rising Demand for Wireless Consumer Device

The increasing adoption of wireless consumer devices such as smartphones, wearables, smart home products, and AR/VR headsets is a key driver of the OTA testing market. These devices integrate multiple antennas and support advanced standards including 5G, Wi-Fi 6/7, and Bluetooth. OTA testing is essential to validate real-world antenna performance, ensure regulatory compliance, minimize connectivity issues, and deliver consistent user experience across compact and complex device form factors.

Restraint: High cost of OTA testing equipment

OTA testing equipment, including anechoic chambers, compact antenna test ranges, and mmWave measurement systems, involves high upfront capital expenditure. Additional costs related to installation, calibration, skilled labor, and system upgrades further increase the financial burden. These high costs restrict adoption among small and mid-sized manufacturers and testing labs, particularly in emerging markets, thereby limiting broader market penetration and slowing overall growth.

Opportunity: Advancements in autonomous vehicles

Rapid advancements in autonomous and connected vehicle technologies are creating significant growth opportunities for the OTA testing market. Modern vehicles rely on multiple wireless systems such as 5G, V2X, GNSS, Wi-Fi, and Bluetooth for communication and safety functions. OTA testing enables accurate evaluation of complex antenna placements and real-world signal behavior, supporting reliable connectivity and regulatory compliance in next-generation autonomous mobility solutions.

Challenge: Rapidly Evolving Wireless Standards and Technologies

The fast pace of innovation in wireless standards, including 5G-Advanced, Wi-Fi 7, and emerging V2X protocols, presents a major challenge for OTA testing providers. Test systems must be frequently upgraded to support new frequency bands, modulation schemes, and performance metrics. Maintaining compatibility, measurement accuracy, and interoperability across evolving standards increases development complexity and operational costs for market participants.

OTA TESTING MARKET SIZE, SHARE & GROWTH ANALYSIS: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Implementation of OTA testing during smartphone and wearable device development to evaluate antenna efficiency, radiated performance, and multi-band 4G/5G, Wi-Fi, and Bluetooth connectivity. | Ensures regulatory compliance, enhances device connectivity, reduces post-launch performance issues, and accelerates product commercialization. |

|

Adoption of OTA testing solutions for connected and autonomous vehicles to validate telematics, V2X, GNSS, infotainment, and in-vehicle wireless systems. | Improves vehicle connectivity reliability, supports advanced driver-assistance systems, enhances passenger safety, and meets automotive certification standards. |

|

Use of OTA testing chambers to assess wireless performance of smartphones, tablets, wearables, and AR devices across multiple frequency bands and form factors. | Delivers consistent user experience, minimizes RF-related field issues, improves device interoperability, and reduces return rates. |

|

Application of OTA testing for 5G base stations, small cells, and customer premise equipment to validate massive MIMO, beamforming, and mmWave performance. | Optimizes network performance, ensures compliance with global standards, and supports deployment of advanced 5G infrastructure. |

|

Deployment of OTA testing for industrial IoT and automation devices to evaluate wireless reliability, coexistence, and performance in complex industrial environments. | Enhances device reliability, reduces connectivity-related downtime, and supports large-scale industrial digitalization initiatives. |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The OTA testing companies ecosystem consists of component and chipset providers (Intel, NXP, Panasonic, STMicroelectronics, Infineon, TDK), OTA testing equipment manufacturers (Keysight Technologies, Rohde & Schwarz, Teradyne, Anritsu, Spirent), OTA testing and certification service providers (UL Solutions, SGS, TÜV SÜD, TÜV Rheinland, Intertek, DEKRA), and end users (Apple, Tesla, Samsung, Sony, BMW Group, HP, Dell). Component and chipset providers supply advanced RF, antenna, and connectivity technologies, while equipment manufacturers deliver anechoic chambers, signal generators, and automated OTA test systems. Service providers support compliance and performance validation, and end users drive demand through growing adoption of 5G, Wi-Fi, Bluetooth, and multi-radio connectivity across consumer, automotive, and enterprise devices.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

OTA Testing Market, By Offering

As of 2024, the services segment held the largest share of the OTA testing market and is expected to maintain its dominance throughout the forecast period. This growth is driven by increasing reliance on third-party testing, certification, and validation services as device complexity rises. Service-based models help manufacturers reduce capital expenditure, access advanced test infrastructure, and ensure compliance with evolving wireless standards, including 5G, Wi-Fi, and Bluetooth, across global regulatory environments.

OTA Testing Market, By Technology

As of 2024, the cellular network segment accounted for the largest share of the OTA testing market and is projected to remain dominant during the forecast period. Widespread adoption of 4G LTE and rapid deployment of 5G technologies have significantly increased antenna complexity and testing requirements. Cellular OTA testing is essential for validating multi-band, multi-antenna, and massive MIMO configurations across FR1 and FR2 bands, ensuring reliable connectivity and regulatory compliance.

OTA Testing Market, By End-user

As of 2024, consumer devices represented the leading end-user segment in the OTA testing market and are expected to sustain their dominance over the forecast period. High production volumes of smartphones, wearables, tablets, and smart home devices drive continuous demand for OTA testing. The integration of cellular, Wi-Fi, and Bluetooth technologies, along with frequent product refresh cycles, further reinforces the need for comprehensive over-the-air performance validation.

REGION

The Asia Pacific OTA testing market is expected to register the highest growth during the forecast period, driven by rapid expansion of electronics manufacturing, large-scale deployment of 5G networks, and increasing production of wireless consumer devices. Countries such as China, South Korea, Japan, Taiwan, and India are key contributors, supported by strong investments in device R&D, automotive connectivity, and testing infrastructure. Rising adoption of smartphones, connected vehicles, IoT devices, and advanced wireless standards further accelerates demand for OTA testing solutions across the region.

OTA TESTING MARKET SIZE, SHARE & GROWTH ANALYSIS: COMPANY EVALUATION MATRIX

In the OTA testing market matrix, Rohde & Schwarz (Star) leads with a strong market position supported by a comprehensive portfolio of OTA chambers, compact antenna test ranges, signal analyzers, and automated validation platforms. Its strong global presence, deep RF expertise, and continuous innovation in 5G, massive MIMO, and mmWave testing position it as a dominant force in the market. National Instruments Corporation (Emerging Leader) is steadily expanding its influence through software-centric test platforms, flexible system architectures, and growing adoption in advanced wireless and automotive OTA applications, indicating strong potential to move toward the leaders quadrant.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

- Rohde & Schwarz (Germany)

- Keysight Technologies (US)

- Anritsu (Japan)

- SGS SA (Switzerland)

- Intertek Group plc (UK)

- National Instruments (US)

- UL LLC (US)

- Spirent (UK)

- Bureau Veritas (France)

- Eurofins Scientific (Luxembourg)

- DEKRA (Germany)

- TÜV Rheinland (Germany)

- Element Materials Technology (UK)

- TÜV SÜD (Germany)

- Teradyne (US)

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2023 (Value) | USD 2.03 Billion |

| Market Forecast in 2029 (Value) | USD 3.17 Billion |

| Growth Rate | CAGR of 7.3% from 2023-2029 |

| Years Considered | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Million), Volume (Thousand Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, Rest of the World |

WHAT IS IN IT FOR YOU: OTA TESTING MARKET SIZE, SHARE & GROWTH ANALYSIS REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Consumer Device Manufacturer |

|

|

| Automotive OEM / Tier-1 Supplier |

|

|

| Telecom Equipment Manufacturer |

|

|

| IoT & Industrial Device Provider |

|

|

| Test & Certification Service Provider |

|

|

RECENT DEVELOPMENTS

- February 2024 : Keysight Technologies launched the E7515W UXM Wireless Connectivity Test Platform for Wi-Fi, enabling advanced network emulation for Wi-Fi 7 devices with comprehensive signaling, RF, and throughput testing, supporting 4×4 MIMO and 320 MHz bandwidth.

- January 2024 : Keysight Technologies launched the SSA-X Signal Source Analyzer, expanding its portfolio with high-frequency models up to 54 GHz and providing integrated phase noise and signal source analysis for advanced wireless, radar, and high-speed digital applications.

- December 2023 : Rohde & Schwarz launched the R&S TS8991 OTA Test System, the first CTIA-certified solution for 5G A-GNSS antenna testing, enabling accurate GNSS performance evaluation for E911 emergency call support over 5G networks.

- COLUMN 'A' SHOULD BE IN TEXT FORMAT AND NOT DATE FORMAT :

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Methodology

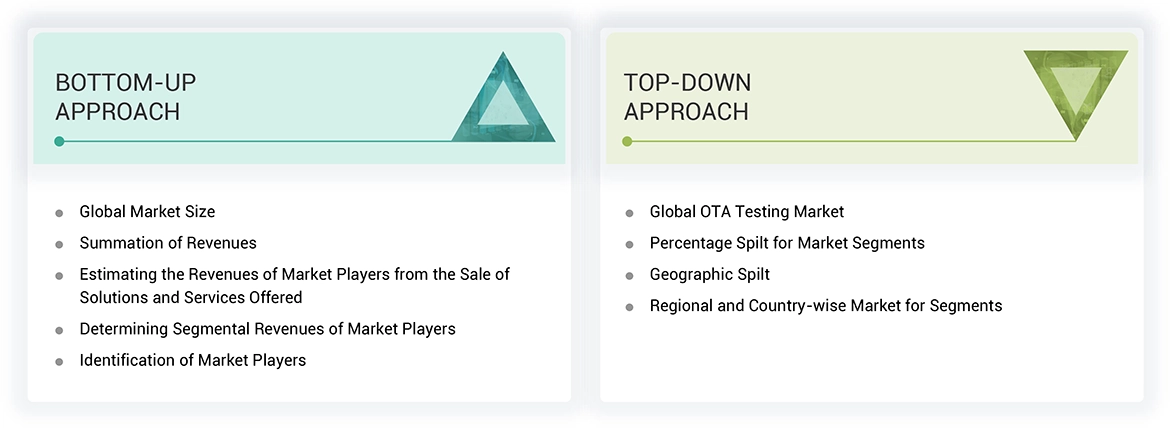

The research study involved 4 major activities in estimating the size of the OTA testing market. Exhaustive secondary research has been done to collect important information about the market and peer markets. The validation of these findings, assumptions, and sizing with the help of primary research with industry experts across the value chain has been the next step. Both top-down and bottom-up approaches have been used to estimate the market size. Post which the market breakdown and data triangulation have been adopted to estimate the market sizes of segments and sub-segments.

Secondary Research

In the secondary research process, various secondary sources have been referred to for identifying and collecting information required for this study. The secondary sources include annual reports, press releases, investor presentations of companies, white papers, and articles from recognized authors. Secondary research has been mainly done to obtain key information about the market’s value chain, the pool of key market players, market segmentation according to industry trends, regional outlook, and developments from both market and technology perspectives.

In the OTA testing market report, the global market size has been estimated using both the top-down and bottom-up approaches, along with several other dependent submarkets. The major players in the market were identified using extensive secondary research, and their presence in the market was determined using secondary and primary research. All the percentage shares splits, and breakdowns have been determined using secondary sources and verified through primary sources.

Primary Research

Extensive primary research has been conducted after understanding the OTA testing market scenario through secondary research. Several primary interviews have been conducted with key opinion leaders from both demand- and supply-side vendors across 4 major regions— North America, Europe, Asia Pacific, and the Rest of the World. Approximately 25% of the primary interviews have been conducted with the demand-side vendors and 75% with the supply-side vendors. Primary data has been collected mainly through telephonic interviews, which consist of 80% of the total primary interviews; questionnaires and emails have also been used to collect the data.

After successful interaction with industry experts, brief sessions were conducted with highly experienced independent consultants to reinforce the findings of our primary research. This, along with the in-house subject matter experts’ opinions, has led us to the findings as described in the report.

Note: “Others” includes sales, marketing, and product managers

About the assumptions considered for the study, To know download the pdf brochure

Market Size Estimation

In the market engineering process, both top-down and bottom-up approaches, along with data triangulation methods, have been used to estimate and validate the size of the OTA testing and other dependent submarkets. The research methodology used to estimate the market sizes includes the following:

- Identifying top-line investments and spending in the ecosystem and considering segment-level splits and major market developments

- Identifying different stakeholders in the OTA testing market that influence the entire market, along with participants across the supply chain

- Analyzing major manufacturers and service providers in the OTA testing market and studying their solutions and service portfolios

- Analyzing trends related to the adoption of OTA testing solutions and services

- Tracking recent and upcoming market developments, including investments, R&D activities, solution and service launches, collaborations, mergers and acquisitions, and partnerships, as well as forecasting the market size based on these developments and other critical parameters

- Carrying out multiple discussions with key opinion leaders to identify the adoption trends of OTA testing solutions and services

- Segmenting the overall market into various other market segments

- Validating the estimates at every level through discussions with key opinion leaders, such as chief executives (CXOs), directors, and operation managers, and finally with the domain experts at MarketsandMarkets

Data Triangulation

After arriving at the overall market size by the market size estimation process explained in the earlier section, the overall OTA testing market has been divided into several segments and subsegments. To complete the overall market engineering process and arrive at the exact statistics for all segments, the data triangulation and market breakdown procedures have been used, wherever applicable. The data has been triangulated by studying various factors and trends from both the demand and supply side perspectives. Along with data triangulation and market breakdown, the market has been validated by top-down and bottom-up approaches.

Market Definition

OTA testing is basically a methodology that considers the performance of a wireless device about the performance of its antenna transmitting and receiving signals in the air. The main parameters for this test include Total Isotropic Sensitivity and Total Radiated Power. The TIS refers to the total sensitivity of an antenna to receive signals from every direction so that it can ensure that communication is okay in different scenarios, and it is tested inside anechoic chambers under different environmental conditions. Total Radiated Power-TRP measures antenna performance with regard to sending out signals, ensuring that the antenna does not exceed the maximum radiated power limits and works well in real-life environments.

The segments of the OTA Testing market based on offerings include test chambers (anechoic chambers), antenna testing solutions, and software, along with comprehensive testing and certification services. The technology segment includes cellular networks, inclusive of 5G, LTE, UMTS, GSM, CDMA, WiFi, and Bluetooth. The end-user segment is quite diversified and includes applications such as consumer smartphones, laptops, tablets, wearables, others, automotive & transportation systems, industrial applications, smart cities infrastructure, and emerging use cases. Each of these segments requires precise OTA testing against performance standards and regulations.

Key Stakeholders

- Raw Material Suppliers

- Test Equipment Manufacturers

- Service Providers

- Device Manufacturers

- Network Operators

- Research and Development Organizations

- Government and Regulatory Bodies

- Industry Associations

- System Integrators

- Component Suppliers

- Certification Bodies

Report Objectives

- To define, describe, and forecast the OTA testing market in terms of value on the basis of offering, technology, end users, and region.

- To forecast the market size for various segments with respect to four main regions, namely, North America, Europe, Asia Pacific, and Rest of the World

- To define, describe, and forecast test chamber and antenna testing solutions in OTA testing market in terms of volume

- To provide detailed information regarding the major drivers, restraints, opportunities, and challenges influencing the growth of the OTA testing market

- To study the complete value chain and related industry segments for the OTA testing market

- To strategically analyze the micro markets with respect to individual growth trends, prospects, and contributions to the total market

- To analyze trends and disruptions; pricing trends; investment and funding scenario; patents and innovations; trade data (export and import data); regulatory environment; Porter's five forces analysis; case studies; key stakeholders & buying criteria; technology trends; the market ecosystem; and key conferences and events related to the OTA testing market.

- To analyze opportunities in the market for various stakeholders by identifying the high-growth segments of the market

- To strategically profile the key players and comprehensively analyze their market position in terms of ranking and core competencies, along with detailing the competitive landscape for the market leaders.

- To analyze competitive developments such as solution and service launches/developments, expansions, acquisitions, partnerships, collaborations, agreements, and research and development (R&D) activities carried out by players in the OTA testing market

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

- Country-wise Information:

- Country-wise breakdown for North America, Europe, Asia Pacific, and Rest of the World

- Company Information:

- Detailed analysis and profiling of additional market players (up to five)

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This ReportPersonalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the OTA Testing Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

Growth opportunities and latent adjacency in OTA Testing Market

Jerry

Apr, 2026

What is the long-term growth potential of OTA testing driven by 5G, IoT, and wireless device expansion?.

Randy

Apr, 2026

Which industries (consumer electronics, automotive, telecom, defense) will drive the most stable demand for OTA testing solutions?.

thesmaz

Apr, 2021

Need details about companies using OTA Testing (5G & 4G).