The study involved four major activities in estimating the market size of the Satellite solar cell materials market. Exhaustive secondary research was done to collect information on the market, the peer market, and the parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. Thereafter, the market breakdown and data triangulation procedures were used to estimate the market size of the segments and subsegments.

Secondary Research

In the secondary research process, various secondary sources have been referred to for identifying and collecting information for this study. These secondary sources include annual reports, press releases, investor presentations of companies, white papers, certified publications, trade directories, articles from recognized authors, the gold standard and silver standard websites, and databases.

Secondary research has been used to obtain key information about the value chain of the industry, the monetary chain of the market, the total pool of key players, market classification, and segmentation according to industry trends to the bottom-most level and regional markets. It was also used to obtain information about the key developments from a market-oriented perspective.

Primary Research

The satellite solar cell materials market comprises several stakeholders in the value chain, which include raw material suppliers, research & development, fabricators/applicators, distribution and logistics, and end users. Various primary sources from the supply and demand sides of the satellite solar cell materials market have been interviewed to obtain qualitative and quantitative information. The primary interviewees from the demand side include key opinion leaders in end-use sectors. The primary sources from the supply side include manufacturers, associations, and institutions involved in the satellite solar cell materials industry.

Primary interviews were conducted to gather insights such as market statistics, data on revenue collected from the products and services, market breakdowns, market size estimations, market forecasting, and data triangulation. Primary research also helped in understanding the various trends related to form, type, application, end-use industry and region. Stakeholders from the demand side, such as CIOs, CTOs, and CSOs, were interviewed to understand the buyer’s perspective on the suppliers, products, fabricators, and their current usage of satellite solar cells materials and the outlook of their business, which will affect the overall market.

The breakdown of profiles of the primary interviewees is illustrated in the figure below:

Note: Tier 1, Tier 2, and Tier 3 companies are classified based on their market revenue in 2022, available in the public domain, product portfolios, and geographical presence.

Other designations include consultants and sales, marketing, and procurement managers.

To know about the assumptions considered for the study, download the pdf brochure

|

Company name

|

Designation

|

|

Spectrolab (US)

|

Individual Industry Expert

|

|

AZUR SPACE Solar Power GmbH (Germany)

|

Director Sales and Marketing

|

|

ROCKET LAB USA (US)

|

Manager

|

|

Sharp Corporation (Japan)

|

Marketing Manager

|

|

CESI S.p.A (Italy)

|

Senior Scientist

|

Market Size Estimation

The top-down and bottom-up approaches have been used to estimate and validate the size of the Satellite solar cell materials market.

-

The key players in the industry have been identified through extensive secondary research.

-

The industry's supply chain has been determined through primary and secondary research.

-

All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

-

All possible parameters that affect the markets covered in this research study have been accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data.

-

The research includes the study of reports, reviews, and newsletters of the key market players, along with extensive interviews for opinions with leaders such as directors and marketing executives.

Note: All the shares are based on the global market size.

Source: Secondary Research, Interviews with Experts, and MarketsandMarkets Analysis

To know about the assumptions considered for the study, Request for Free Sample Report

Satellite Solar Cells Materials Market: Top-Down Approach

Data Triangulation

After arriving at the total market size from the estimation process explained above, the overall market has been split into several segments and sub-segments. To complete the overall market engineering process and arrive at the exact statistics for all the segments and sub-segments, the data triangulation and market breakdown procedures have been employed, wherever applicable. The data has been triangulated by studying various factors and trends from both the demand and supply sides. Along with this, the market size has been validated by using both the top-down and bottom-up approaches and primary interviews. Hence, for every data segment, there have been three sources—top-down approach, bottom-up approach, and expert interviews. The data was assumed correct when the values arrived from the three sources matched.

Market Definition

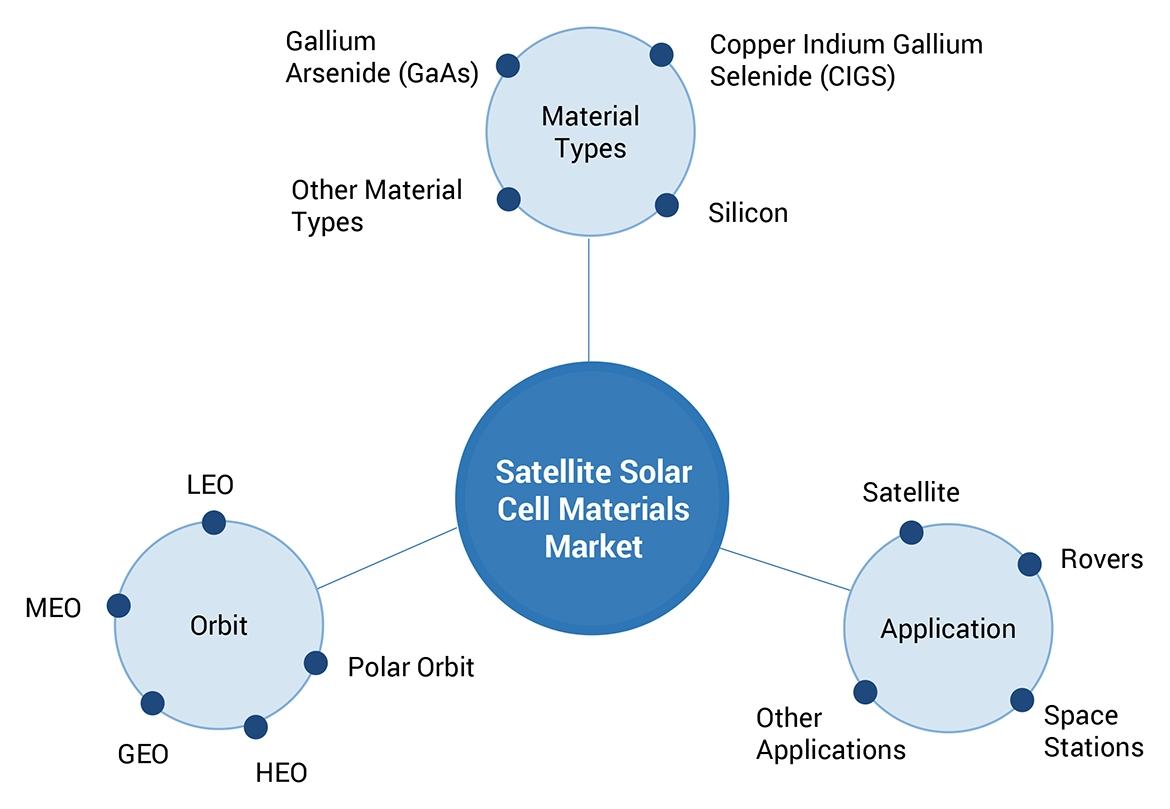

The satellite solar cell materials market pertains to the array of materials involved in the production of solar cells specifically designed for use in satellites. These materials play a pivotal role in constructing solar cells capable of harnessing solar energy in the harsh and demanding conditions of outer space. The market encompasses a range of advanced materials, including materials like silicon and GaAs, which are carefully selected for their ability to withstand extreme temperatures, radiation, and vacuum conditions prevalent in space environments. Key components such as coverglass and interconnected cells contribute to the durability and efficiency of these solar cells. The market is characterized by the stringent requirements of the space industry, demanding materials that ensure reliability, longevity, and optimal energy conversion in space applications. As space exploration, satellite deployment, and communication activities continue to rise, the demand for high-performance satellite solar cell materials is expected to grow, making this market integral to the success of various space missions and satellite technologies. Companies operating in this market focus on developing cutting-edge materials to meet the rigorous standards of the space industry, catering to the evolving needs of satellite manufacturers and space agencies worldwide.

Key Stakeholders

-

Satellite solar cells materials manufacturers

-

Satellite solar cells materials traders, distributors, and suppliers

-

End-use industry participants of different segments of the satellite solar cells materials market

-

Government and research organizations

-

Associations and industrial bodies

-

Research and consulting firms.

-

Research & development (R&D) institutions.

-

Environmental support agencies.

Report Objectives

-

To define, describe, and forecast the size of the satellite solar cell materials market, in terms of value and volume.

-

To provide detailed information regarding the major factors (drivers, opportunities, restraints, and challenges) influencing the growth of the market

-

To estimate and forecast the market size based on material types, application, orbit and region.

-

To forecast the size of the market with respect to major regions, namely, Europe, North America, Asia Pacific, Rest of the world, along with their key countries.

-

To strategically analyze micromarkets1 with respect to individual growth trends, prospects, and their contribution to the overall market.

-

To analyze opportunities in the market for stakeholders and provide a competitive landscape of market leaders.

-

To track and analyze recent developments such as expansions, new product launches, partnerships & agreements, and acquisitions in the market.

-

To strategically profile key market players and comprehensively analyze their core competencies.

Available Customizations

Along with the given market data, MarketsandMarkets offers customizations according to the company’s specific needs. The following customization options are available for the report:

Regional Analysis

-

Further breakdown of a region with respect to a particular country or additional application

Company Information

-

Detailed analysis and profiles of additional market players

Growth opportunities and latent adjacency in Satellite Solar Cell Materials Market