The research study involved 4 major activities in estimating the size of the ALD equipment market. Exhaustive secondary research has been done to collect important information about the market and peer markets. The validation of these findings, assumptions, and sizing with the help of primary research with industry experts across the supply chain has been the next step. Both top-down and bottom-up approaches have been used to estimate the market size. Post which the market breakdown and data triangulation have been adopted to estimate the market sizes of segments and sub-segments.

Secondary Research:

In the secondary research process, various secondary sources have been referred to for identifying and collecting information required for this study. The secondary sources include annual reports, press releases, and investor presentations of companies, white papers, and articles from recognized authors. Secondary research has been mainly done to obtain key information about the market’s value chain, the pool of key market players, market segmentation according to industry trends, regional outlook and developments from both market and technology perspectives.

Primary Research:

In primary research, various primary sources from both supply and demand sides have been interviewed to obtain qualitative and quantitative insights required for this report. Primary sources from supply side include experts such as CEOs, vice presidents, marketing directors, manufacturers, technology and innovation directors, end users and related executives from multiple key companies and organizations operating in the ALD equipment market ecosystem.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

In the market engineering process, both top-down and bottom-up approaches have been used along with data triangulation methods to estimate and validate the size of the ALD equipment market and other dependent submarkets. The research methodology used to estimate the market sizes includes the following:

-

Identifying stakeholders in the ALD equipment market that influence the entire market, along with participants across the value chain.

-

Analyzing major manufacturers of ALD equipment and studying their product portfolios

-

Analyzing trends related to the adoption of ALD equipment

-

Tracking the recent and upcoming developments in the market that include investments, R&D activities, product launches, contracts, collaborations, acquisitions, agreements, and partnerships, as well as forecasting the market size based on these developments and other critical parameters

-

Carrying out multiple discussions with key opinion leaders to identify the adoption trends of ALD equipment

-

Segmenting the overall market into various other market segments

-

Validating the estimates at every level through discussions with key opinion leaders, such as chief executives (CXOs), directors, and operation managers, and finally with the domain experts at MarketsandMarkets

Market Size Estimation Methodology-Bottom-up Approach

Market Size Estimation Methodology-Top-down Approach

Data Triangulation

After arriving at the overall market size by the market size estimation process explained in the earlier section, the overall ALD equipment market has been divided into several segments and subsegments. To complete the overall market engineering process and arrive at the exact statistics for all segments, the data triangulation and market breakdown procedures have been used, wherever applicable. The data has been triangulated by studying various factors and trends from both the demand and supply side perspectives. Along with data triangulation and market breakdown, the market has been validated by top-down and bottom-up approaches.

Market Definition

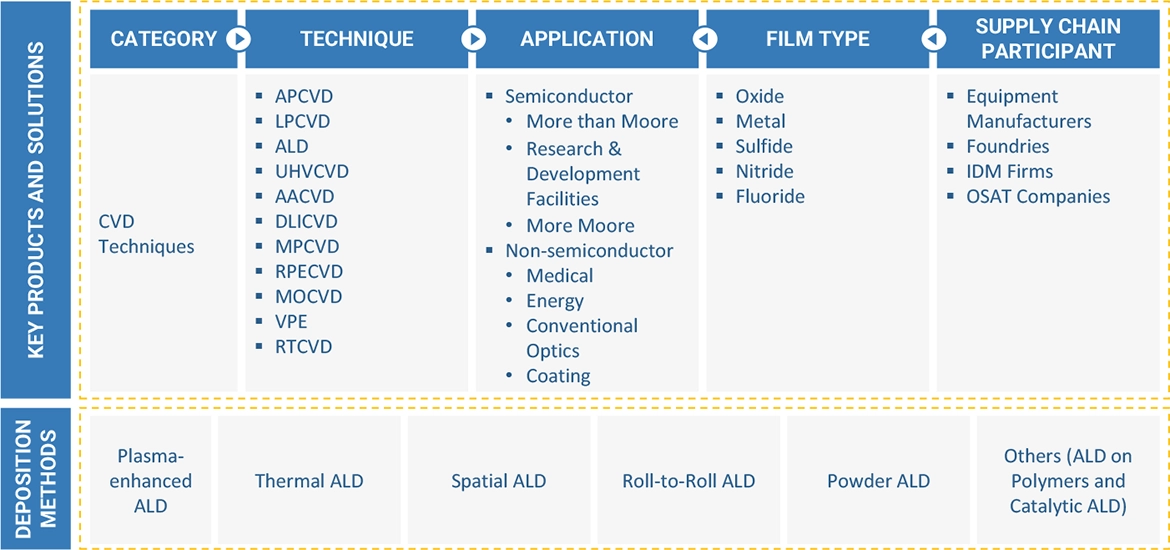

ALD equipment refers to a specialized set of machinery and components designed for executing the atomic layer deposition process. ALD is a thin-film deposition technique that enables precise and controlled growth of thin films at the atomic or molecular level. ALD equipment facilitates the sequential and self-limiting exposure of a substrate to precursor gases, resulting in the formation of thin, conformal, and uniform layers on the substrate surface.

Researchers, engineers, and manufacturers in various fields utilize ALD equipment to deposit thin films for a wide range of applications, such as more than Moore, R&D facilities, and more Moore applications. Additionally, ALD equipment is also used in the medical and energy industries, conventional optics, and coating applications. The precise and controlled nature of ALD makes it a fundamental tool for achieving desired material properties and functionalities in nanotechnology and advanced material sciences.

Stakeholders

-

Raw Material Suppliers

-

Technology Investors

-

Original Equipment Manufacturers (OEMs)

-

Device Suppliers and Distributors

-

Government Labs

-

In-house Testing Labs

-

System Integrators

-

Resellers and Traders

-

Research Institutes and Organizations

-

Semiconductor Manufacturing Equipment Forums, Alliances, Consortiums, and Associations

-

Governments, Financial Institutions, and Regulatory Bodies

-

Market Research and Consulting Firms

The main objectives of this study are as follows:

-

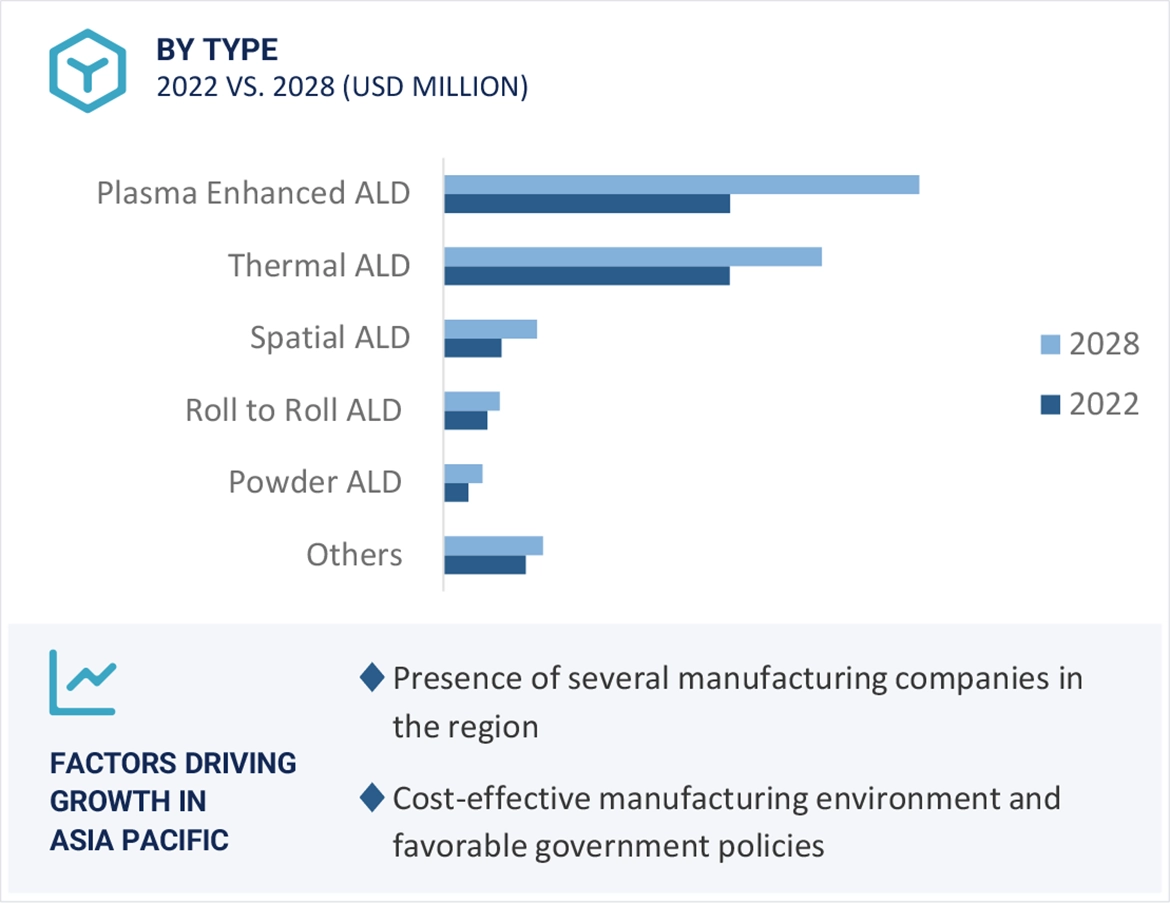

To analyze and forecast the ALD equipment market size by deposition method, film type, application (semiconductor and non-semiconductor), and region, in terms of value

-

To analyze and forecast the ALD equipment market size, in terms of volume

-

To forecast the market size for various segments with respect to four main regions, namely, North America, Europe, Asia Pacific, and Rest of the World (RoW)

-

To provide detailed information regarding the major drivers, restraints, opportunities, and challenges influencing the growth of the ALD equipment market

-

To study the complete supply chain and related industry segments for the ALD equipment market

-

To strategically analyze the micromarkets with respect to individual growth trends, prospects, and contributions to the total market

-

To analyze the supply chain, market ecosystem; trends/disruptions impacting customer business; technology analysis; pricing analysis; Porter’s five forces model; key stakeholders and buying criteria; case study analysis; trade analysis; patent analysis; key conferences and events, 2023–2024; and regulations related to the ALD equipment market

-

To analyze opportunities in the market for various stakeholders by identifying the high-growth segments

-

To strategically profile the key players and comprehensively analyze their market position in terms of ranking and core competencies, along with detailing the competitive landscape for the market leaders

-

To analyze competitive developments such as product launches, partnerships, collaborations, contracts, acquisitions, expansions, and research and development (R&D) activities carried out by players in the ALD equipment market.

Customizations Options:

With the given market data, MarketsandMarkets offers customizations according to the company’s specific needs. The following customization options are available for the report:

Company Information

-

Detailed analysis and profiling of additional market players (up to 5)

Geographic Information

-

Detailed analysis of additional countries (up to 5)

Growth opportunities and latent adjacency in ALD Equipment Market