TABLE OF CONTENTS

1 INTRODUCTION (Page No. - 26)

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.2.1 CERAMIC SUBSTRATES MARKET: INCLUSIONS AND EXCLUSIONS

1.2.2 CERAMIC SUBSTRATES: MARKET DEFINITION AND INCLUSIONS, BY PRODUCT TYPE

1.2.3 CERAMIC SUBSTRATES: MARKET DEFINITION AND INCLUSIONS, BY END-USE INDUSTRY

1.3 MARKET SCOPE

1.3.1 REGIONS COVERED

1.3.2 YEARS CONSIDERED

1.4 CURRENCY

1.5 UNITS CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

1.7.1 IMPACT OF RECESSION

2 RESEARCH METHODOLOGY (Page No. - 32)

2.1 RESEARCH DATA

FIGURE 1 CERAMIC SUBSTRATES MARKET: RESEARCH DESIGN

2.1.1 SECONDARY DATA

2.1.2 PRIMARY DATA

2.1.2.1 Primary interviews–Demand and supply sides

2.1.2.2 Key industry insights

2.1.2.3 Breakdown of primary interviews

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

FIGURE 2 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 (SUPPLY SIDE)-COLLECTIVE SHARE OF MAJOR PLAYERS

FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 2 (SUPPLY SIDE) - COLLECTIVE REVENUE OF ALL PRODUCTS (BOTTOM-UP)

FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 3 (DEMAND SIDE): PRODUCTS SOLD (BOTTOM-UP)

2.2.2 TOP-DOWN APPROACH

FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 4 (TOP-DOWN)

2.3 DATA TRIANGULATION

FIGURE 6 CERAMIC SUBSTRATES MARKET: DATA TRIANGULATION

2.4 GROWTH RATE ASSUMPTIONS/GROWTH FORECAST

2.4.1 SUPPLY SIDE

FIGURE 7 MARKET GROWTH PROJECTIONS FROM SUPPLY SIDE

2.4.2 DEMAND SIDE

FIGURE 8 MARKET GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS AND OPPORTUNITIES

2.5 IMPACT OF RECESSION

2.6 FACTOR ANALYSIS

2.7 ASSUMPTIONS

2.8 LIMITATIONS

2.9 RISK ASSESSMENT

3 EXECUTIVE SUMMARY (Page No. - 43)

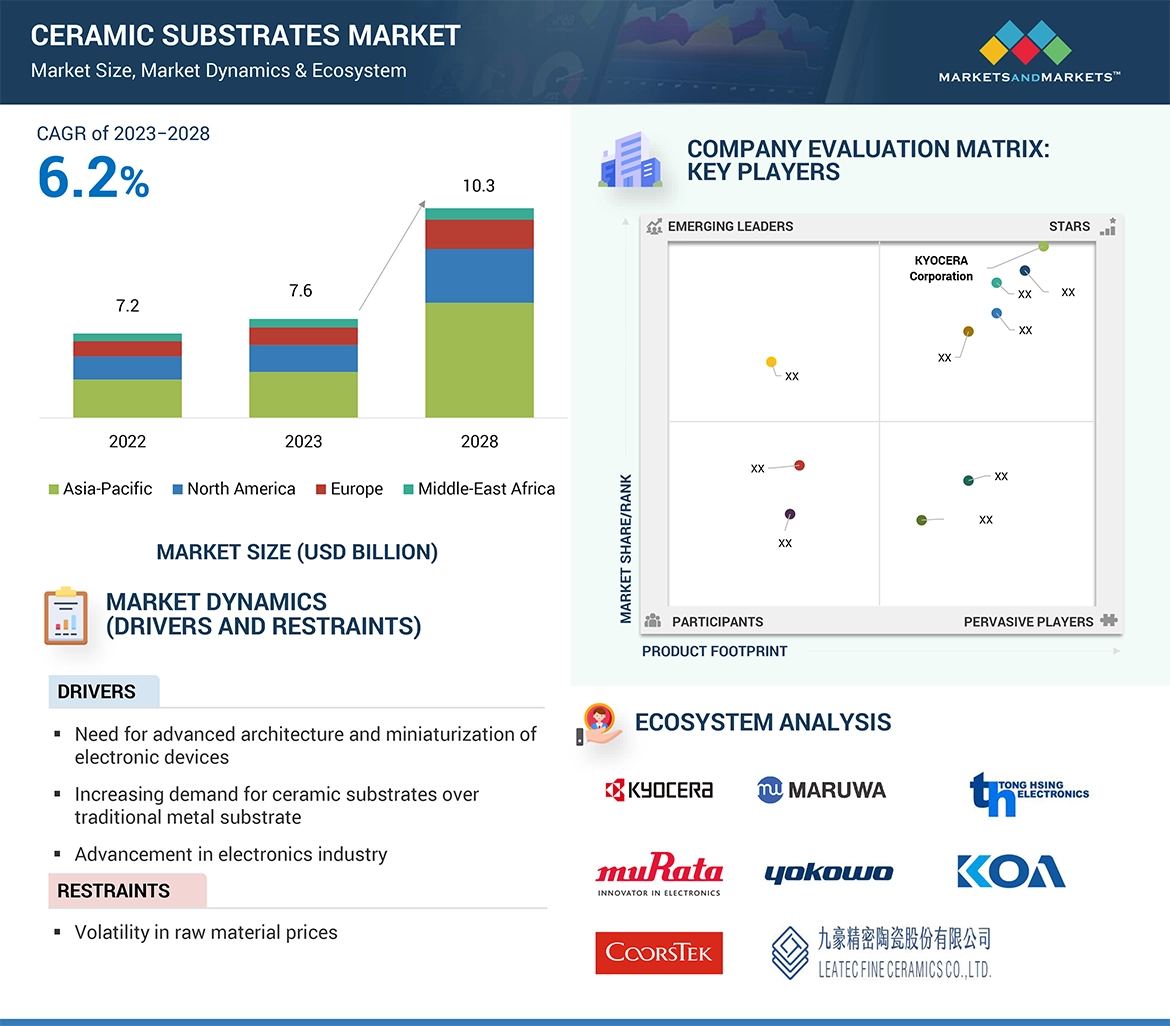

FIGURE 9 ALUMINA ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

FIGURE 10 CONSUMER ELECTRONICS TO BE LARGEST END-USE INDUSTRY OF CERAMIC SUBSTRATES DURING FORECAST PERIOD

FIGURE 11 ASIA PACIFIC ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

4 PREMIUM INSIGHTS (Page No. - 46)

4.1 ATTRACTIVE OPPORTUNITIES IN CERAMIC SUBSTRATES MARKET

FIGURE 12 INCREASING NEED FOR ADVANCED ARCHITECTURE AND MINIATURIZATION OF ELECTRONIC DEVICES TO DRIVE MARKET

4.2 CERAMIC SUBSTRATES MARKET, BY REGION

FIGURE 13 ASIA PACIFIC TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

4.3 ASIA PACIFIC CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE & COUNTRY

FIGURE 14 ALUMINA DOMINATED OVERALL CERAMIC SUBSTRATES MARKET IN 2022

4.4 CERAMIC SUBSTRATES MARKET, END-USE INDUSTRY VS. REGION

FIGURE 15 CONSUMER ELECTRONICS END-USE INDUSTRY LED THE OVERALL CERAMIC SUBSTRATES MARKET

4.5 CERAMIC SUBSTRATES MARKET, BY MAJOR COUNTRIES

FIGURE 16 INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

5 MARKET OVERVIEW (Page No. - 49)

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

FIGURE 17 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN CERAMIC SUBSTRATES MARKET

5.2.1 DRIVERS

5.2.1.1 Need for advanced architecture and miniaturization of electronic devices

5.2.1.2 Increasing demand for ceramic substrates over traditional metal substrates

5.2.1.3 Advancements in electronics industry

TABLE 1 GLOBAL ELECTRICAL & ELECTRONICS INDUSTRY PRODUCTION

5.2.1.4 Global expansion of 5G technology

5.2.2 RESTRAINTS

5.2.2.1 Volatility in raw material prices

5.2.3 OPPORTUNITIES

5.2.3.1 Growing demand for nanotechnology and high-end computing systems

5.2.3.2 Increasing demand from medical industry

5.2.4 CHALLENGES

5.2.4.1 Issues related to recyclability and reparability

5.2.4.2 High price of ceramic substrates

5.3 PORTER’S FIVE FORCES ANALYSIS

FIGURE 18 CERAMIC SUBSTRATES MARKET: PORTER’S FIVE FORCES ANALYSIS

5.3.1 THREAT OF SUBSTITUTES

5.3.2 THREAT OF NEW ENTRANTS

5.3.3 BARGAINING POWER OF SUPPLIERS

5.3.4 BARGAINING POWER OF BUYERS

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

TABLE 2 CERAMIC SUBSTRATES MARKET: PORTER’S FIVE FORCES ANALYSIS

5.4 MACROECONOMIC INDICATORS

TABLE 3 GDP TRENDS AND FORECAST OF MAJOR ECONOMIES, 2020–2028 (USD BILLION)

6 INDUSTRY TRENDS (Page No. - 57)

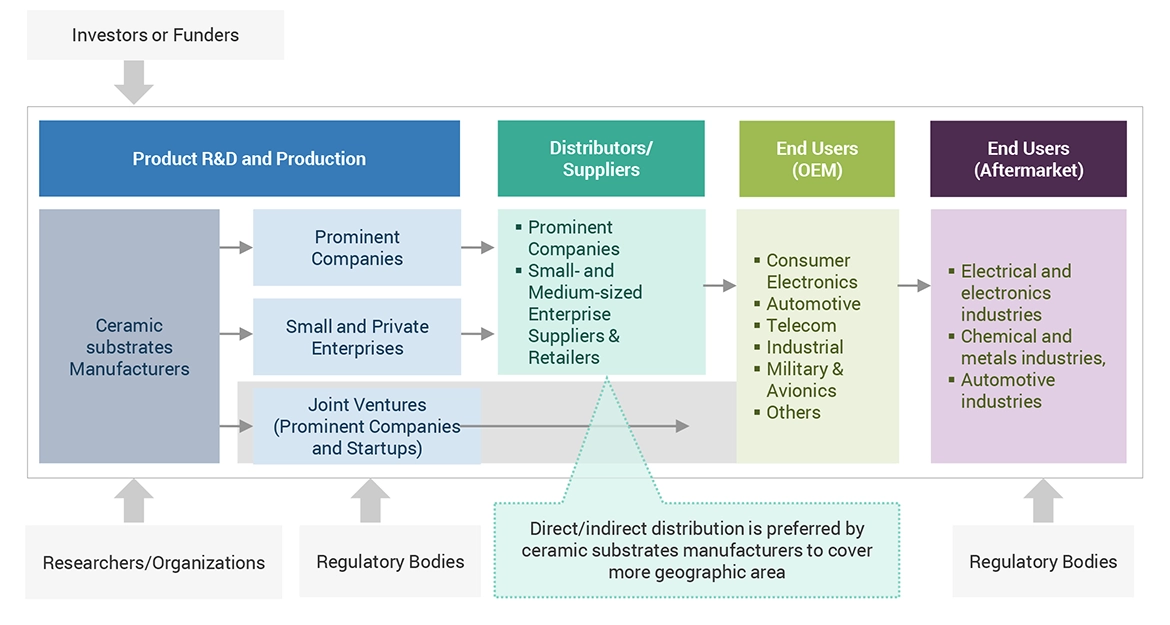

6.1 SUPPLY CHAIN ANALYSIS

FIGURE 19 CERAMIC SUBSTRATES MARKET SUPPLY CHAIN

6.1.1 RAW MATERIALS

6.1.2 INTERMEDIATE MATERIAL

6.1.3 MANUFACTURING PROCESS

6.1.4 DISTRIBUTION

6.1.5 END-USE INDUSTRY

6.2 LIST OF COMPANIES OFFERING BOTH RAW MATERIALS AND CERAMIC SUBSTRATES

6.3 CERAMIC SUBSTRATE MANUFACTURING PROCESS

6.3.1 HIGH-TEMPERATURE CO-FIRED CERAMIC (HTCC)

6.3.2 LOW-TEMPERATURE CO-FIRED CERAMIC (LTCC)

6.3.3 DIRECT BONDED COPPER (DBC)

6.3.4 DIRECT PLATED COPPER (DPC)

6.3.5 LASER-ASSISTED MILLING (LAM)

6.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMER’S BUSINESS

6.4.1 REVENUE SHIFTS AND REVENUE POCKETS FOR CERAMIC SUBSTRATE MANUFACTURERS

FIGURE 20 REVENUE SHIFT IN CERAMIC SUBSTRATES MARKET

6.5 ECOSYSTEM/MARKET MAP

FIGURE 21 CERAMIC SUBSTRATES MARKET: ECOSYSTEM MAPPING

TABLE 4 CERAMIC SUBSTRATES MARKET: ROLE IN ECOSYSTEM

6.6 KEY STAKEHOLDERS & BUYING CRITERIA

6.6.1 KEY STAKEHOLDERS IN BUYING PROCESS

FIGURE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 END-USE INDUSTRIES

TABLE 5 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 END-USE INDUSTRIES

6.6.2 BUYING CRITERIA

FIGURE 23 KEY BUYING CRITERIA FOR TOP 3 END-USE INDUSTRIES

TABLE 6 KEY BUYING CRITERIA FOR TOP 3 END-USE INDUSTRIES

6.7 PRICING ANALYSIS

6.7.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRIES

FIGURE 24 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRIES

TABLE 7 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRIES (USD/KG)

6.7.2 AVERAGE SELLING PRICE TREND, BY REGION

FIGURE 25 AVERAGE SELLING PRICE TREND OF CERAMIC SUBSTRATES, BY REGION

TABLE 8 AVERAGE SELLING PRICE TREND OF CERAMIC SUBSTRATES, BY REGION (USD/KG)

6.8 CASE STUDIES

6.8.1 CASE STUDY ON QUALITY IMPROVEMENT FOR LIQUID COMPOSITION ANALYSIS DEVICE

6.8.2 CASE STUDY ON ALUMINUM CASTING PART REPLACEMENT WITH FINE CERAMICS TO IMPROVE PRODUCTIVITY AND QUALITY

6.8.3 CASE STUDY ON SAMSUNG ELECTRONICS (TELECOMMUNICATION)

6.9 TECHNOLOGY ANALYSIS

6.9.1 LIST OF NEW TECHNOLOGIES FOR CERAMIC SUBSTRATES

6.10 TARIFF AND REGULATORY LANDSCAPE

6.10.1 REGULATIONS RELATED TO CERAMIC SUBSTRATES MARKET

6.10.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.11 KEY CONFERENCES & EVENTS IN 2023–2024

TABLE 9 CERAMIC SUBSTRATES MARKET: DETAILED LIST OF CONFERENCES & EVENTS

6.12 TRADE DATA

6.12.1 IMPORT SCENARIO OF CERAMIC SUBSTRATES

FIGURE 26 IMPORT OF CERAMIC SUBSTRATES, BY KEY COUNTRIES (2017–2022)

TABLE 10 IMPORT OF CERAMIC SUBSTRATES, BY REGION, 2017–2022 (USD MILLION)

6.12.2 EXPORT SCENARIO OF CERAMIC SUBSTRATES

FIGURE 27 EXPORT OF CERAMIC SUBSTRATES, BY KEY COUNTRIES (2017–2022)

TABLE 11 EXPORT OF CERAMIC SUBSTRATES, BY REGION, 2017–2022 (USD MILLION)

6.13 PATENT ANALYSIS

6.13.1 METHODOLOGY

6.13.2 DOCUMENT TYPE

FIGURE 28 PATENTS REGISTERED FOR CERAMIC SUBSTRATES, 2012–2022

FIGURE 29 PATENT PUBLICATION TRENDS FOR CERAMIC SUBSTRATES, 2012–2022

6.13.3 LEGAL STATUS OF PATENTS

FIGURE 30 LEGAL STATUS OF PATENTS FILED FOR CERAMIC SUBSTRATES

6.13.4 JURISDICTION ANALYSIS

FIGURE 31 MAXIMUM PATENTS FILED BY COMPANIES IN US

6.13.5 TOP APPLICANTS

FIGURE 32 INTERNATIONAL BUSINESS MACHINES CORPORATION REGISTERED MAXIMUM NUMBER OF PATENTS BETWEEN 2012 AND 2022

TABLE 12 LIST OF PATENTS BY MURATA MANUFACTURING CO., LTD.

TABLE 13 LIST OF PATENTS BY INTERNATIONAL BUSINESS MACHINES CORPORATION

TABLE 14 LIST OF PATENTS BY SAMSUNG ELECTRONICS CO., LTD.

TABLE 15 LIST OF PATENTS BY KYOCERA CORPORATION

TABLE 16 TOP 10 PATENT OWNERS (US) IN LAST 10 YEARS

7 CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE (Page No. - 88)

7.1 INTRODUCTION

FIGURE 33 CERAMIC SUBSTRATE FABRICATION PROCESS

TABLE 17 CERAMIC SUBSTRATE FABRICATION TECHNOLOGY

TABLE 18 THERMAL CONDUCTIVITY OF VARIOUS CERAMICS

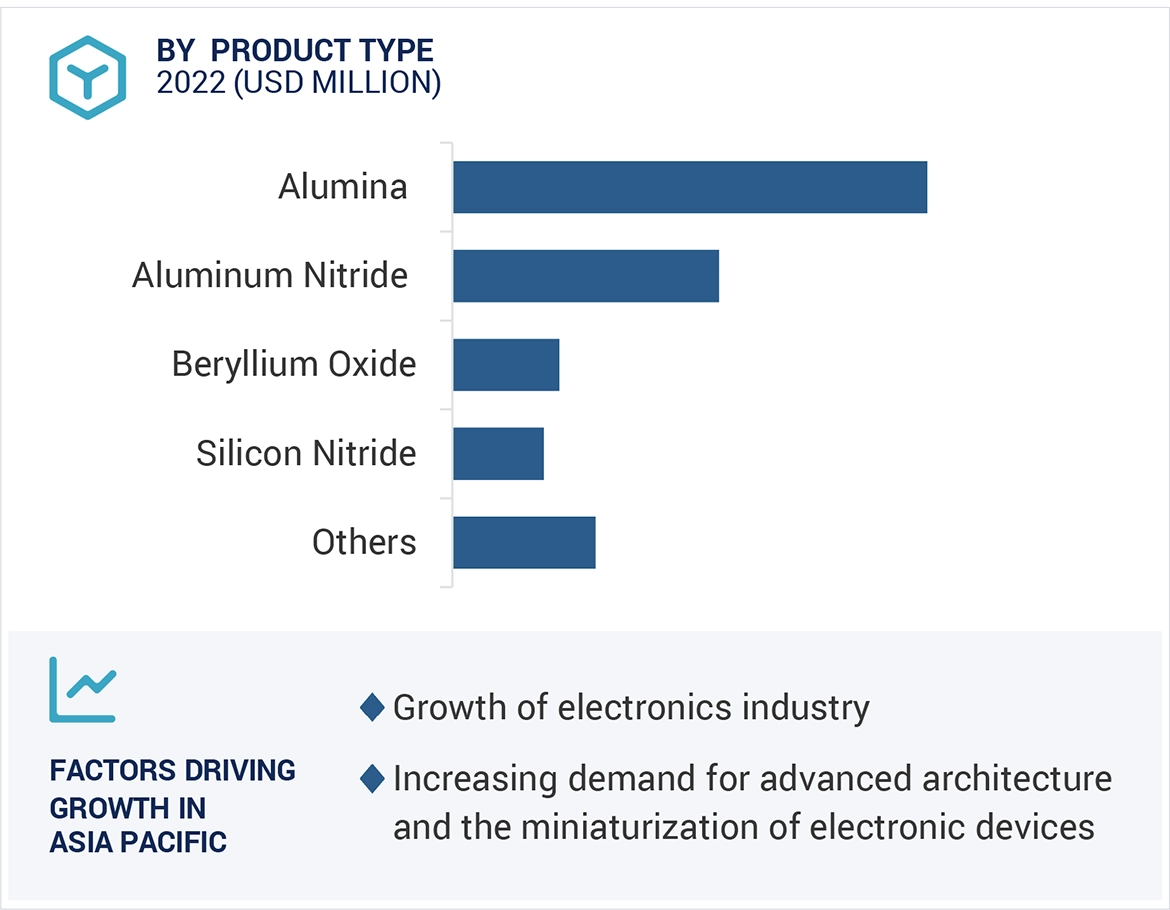

FIGURE 34 ALUMINUM NITRIDE TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

TABLE 19 CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (USD MILLION)

TABLE 20 CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (USD MILLION)

TABLE 21 CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (TON)

TABLE 22 CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (TON)

7.2 ALUMINA

7.2.1 MOST WIDELY USED ADVANCED OXIDE CERAMIC MATERIAL

TABLE 23 ALUMINA: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (USD MILLION)

TABLE 24 ALUMINA: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (USD MILLION)

TABLE 25 ALUMINA: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (TON)

TABLE 26 ALUMINA: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (TON)

7.3 ALUMINUM NITRIDE

7.3.1 ASIA PACIFIC TO BE LARGEST MARKET DURING FORECAST PERIOD

TABLE 27 ALUMINUM NITRIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (USD MILLION)

TABLE 28 ALUMINUM NITRIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (USD MILLION)

TABLE 29 ALUMINUM NITRIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (TON)

TABLE 30 ALUMINUM NITRIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (TON)

7.4 BERYLLIUM OXIDE

7.4.1 HIGH COST RESTRICTING WIDESPREAD APPLICATION IN MANY END-USE SEGMENTS

TABLE 31 BERYLLIUM OXIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (USD MILLION)

TABLE 32 BERYLLIUM OXIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (USD MILLION)

TABLE 33 BERYLLIUM OXIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (TON)

TABLE 34 BERYLLIUM OXIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (TON)

7.5 SILICON NITRIDE

7.5.1 SIGNIFICANT USE IN HIGH-POWER ELECTRONIC APPLICATIONS TO DRIVE MARKET

TABLE 35 SILICON NITRIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (USD MILLION)

TABLE 36 SILICON NITRIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (USD MILLION)

TABLE 37 SILICON NITRIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (TON)

TABLE 38 SILICON NITRIDE: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (TON)

7.6 OTHERS

TABLE 39 OTHERS: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (USD MILLION)

TABLE 40 OTHERS: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (USD MILLION)

TABLE 41 OTHERS: CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (TON)

TABLE 42 OTHERS: CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (TON)

8 CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY (Page No. - 102)

8.1 INTRODUCTION

FIGURE 35 AUTOMOTIVE TO BE FASTEST-GROWING END-USE INDUSTRY OF CERAMIC SUBSTRATES DURING FORECAST PERIOD

TABLE 43 CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 44 CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 45 CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 46 CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

8.2 CONSUMER ELECTRONICS

8.2.1 CERAMIC SUBSTRATES WIDELY USED AS VERSATILE AND COST-EFFECTIVE THICK FILM TECHNOLOGY IN CONSUMER ELECTRONICS

TABLE 47 CERAMIC SUBSTRATES MARKET IN CONSUMER ELECTRONICS, BY REGION, 2017–2021 (USD MILLION)

TABLE 48 CERAMIC SUBSTRATES MARKET IN CONSUMER ELECTRONICS, BY REGION, 2022–2028 (USD MILLION)

TABLE 49 CERAMIC SUBSTRATES MARKET IN CONSUMER ELECTRONICS, BY REGION, 2017–2021 (TON)

TABLE 50 CERAMIC SUBSTRATES MARKET IN CONSUMER ELECTRONICS, BY REGION, 2022–2028 (TON)

8.3 AUTOMOTIVE

8.3.1 HIGH THERMAL CONDUCTIVITY OF CERAMIC SUBSTRATES DRIVING DEMAND IN AUTOMOBILE MANUFACTURING

TABLE 51 CERAMIC SUBSTRATES MARKET IN AUTOMOTIVE, BY REGION, 2017–2021 (USD MILLION)

TABLE 52 CERAMIC SUBSTRATES MARKET IN AUTOMOTIVE, BY REGION, 2022–2028 (USD MILLION)

TABLE 53 CERAMIC SUBSTRATES MARKET IN AUTOMOTIVE, BY REGION, 2017–2021 (TON)

TABLE 54 CERAMIC SUBSTRATES MARKET IN AUTOMOTIVE, BY REGION, 2022–2028 (TON)

8.4 TELECOM

8.4.1 CERAMIC SUBSTRATES ENABLE MINIATURIZATION OF CIRCUITS

TABLE 55 CERAMIC SUBSTRATES MARKET IN TELECOM, BY REGION, 2017–2021 (USD MILLION)

TABLE 56 CERAMIC SUBSTRATES MARKET IN TELECOM, BY REGION, 2022–2028 (USD MILLION)

TABLE 57 CERAMIC SUBSTRATES MARKET IN TELECOM, BY REGION, 2017–2021 (TON)

TABLE 58 CERAMIC SUBSTRATES MARKET IN TELECOM, BY REGION, 2022–2028 (TON)

8.5 INDUSTRIAL

8.5.1 ADVANCED MANUFACTURING TECHNOLOGIES DRIVING DEMAND IN DIFFERENT INDUSTRIAL APPLICATIONS

TABLE 59 CERAMIC SUBSTRATES MARKET IN INDUSTRIAL, BY REGION, 2017–2021 (USD MILLION)

TABLE 60 CERAMIC SUBSTRATES MARKET IN INDUSTRIAL, BY REGION, 2022–2028 (USD MILLION)

TABLE 61 CERAMIC SUBSTRATES MARKET IN INDUSTRIAL, BY REGION, 2017–2021 (TON)

TABLE 62 CERAMIC SUBSTRATES MARKET IN INDUSTRIAL, BY REGION, 2022–2028 (TON)

8.6 MILITARY & AVIONICS

8.6.1 GROWING MINIATURIZATION AND DEMAND FOR LIGHTWEIGHT EQUIPMENT TO DRIVE MARKET

TABLE 63 CERAMIC SUBSTRATES MARKET IN MILITARY & AVIONICS, BY REGION, 2017–2021 (USD MILLION)

TABLE 64 CERAMIC SUBSTRATES MARKET IN MILITARY & AVIONICS, BY REGION, 2022–2028 (USD MILLION)

TABLE 65 CERAMIC SUBSTRATES MARKET IN MILITARY & AVIONICS, BY REGION, 2017–2021 (TON)

TABLE 66 CERAMIC SUBSTRATES MARKET IN MILITARY & AVIONICS, BY REGION, 2022–2028 (TON)

8.7 OTHERS

TABLE 67 CERAMIC SUBSTRATES MARKET IN OTHER END-USE INDUSTRIES, BY REGION, 2017–2021 (USD MILLION)

TABLE 68 CERAMIC SUBSTRATES MARKET IN OTHER END-USE INDUSTRIES, BY REGION, 2022–2028 (USD MILLION)

TABLE 69 CERAMIC SUBSTRATES MARKET IN OTHER END-USE INDUSTRIES, BY REGION, 2017–2021 (TON)

TABLE 70 CERAMIC SUBSTRATES MARKET IN OTHER END-USE INDUSTRIES, BY REGION, 2022–2028 (TON)

9 CERAMIC SUBSTRATES MARKET, BY REGION (Page No. - 116)

9.1 INTRODUCTION

FIGURE 36 ASIA PACIFIC TO BE LARGEST AND FASTEST-GROWING MARKET FOR CERAMIC SUBSTRATES

TABLE 71 CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (USD MILLION)

TABLE 72 CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (USD MILLION)

TABLE 73 CERAMIC SUBSTRATES MARKET, BY REGION, 2017–2021 (TON)

TABLE 74 CERAMIC SUBSTRATES MARKET, BY REGION, 2022–2028 (TON)

9.2 ASIA PACIFIC

9.2.1 IMPACT OF RECESSION

FIGURE 37 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET SNAPSHOT

9.2.2 ASIA PACIFIC CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE

TABLE 75 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (USD MILLION)

TABLE 76 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (USD MILLION)

TABLE 77 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (TON)

TABLE 78 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (TON)

9.2.3 ASIA PACIFIC CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY

TABLE 79 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 80 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 81 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 82 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.2.4 ASIA PACIFIC CERAMIC SUBSTRATES MARKET, BY COUNTRY

TABLE 83 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (USD MILLION)

TABLE 84 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (USD MILLION)

TABLE 85 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (TON)

TABLE 86 ASIA PACIFIC: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (TON)

9.2.4.1 China

9.2.4.1.1 Presence of manufacturing hub of major consumer electronics companies to drive demand

TABLE 87 CHINA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 88 CHINA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 89 CHINA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 90 CHINA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.2.4.2 Japan

9.2.4.2.1 Strong electronics and automotive sectors to fuel demand

TABLE 91 JAPAN: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 92 JAPAN: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 93 JAPAN: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 94 JAPAN: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.2.4.3 South Korea

9.2.4.3.1 Increasing infrastructural developments driving ceramic substrates market

TABLE 95 SOUTH KOREA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 96 SOUTH KOREA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 97 SOUTH KOREA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 98 SOUTH KOREA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.2.4.4 Taiwan

9.2.4.4.1 Presence of major players in advanced microelectronics packaging services to support market growth

TABLE 99 TAIWAN: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 100 TAIWAN: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 101 TAIWAN: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 102 TAIWAN: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.2.4.5 Malaysia

9.2.4.5.1 Electrical & electronics sector to drive market

TABLE 103 MALAYSIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 104 MALAYSIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 105 MALAYSIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 106 MALAYSIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.2.4.6 Singapore

9.2.4.6.1 Presence of leading aviation hub for maintenance, repair, and overhaul (MRO) activities to drive market

TABLE 107 SINGAPORE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 108 SINGAPORE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 109 SINGAPORE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 110 SINGAPORE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.2.4.7 India

9.2.4.7.1 Fastest-growing ceramic substrates market globally

TABLE 111 INDIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 112 INDIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 113 INDIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 114 INDIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.2.4.8 Australia

9.2.4.8.1 Advancements in electronics, aviation, and telecom sectors to increase consumption

TABLE 115 AUSTRALIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 116 AUSTRALIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 117 AUSTRALIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 118 AUSTRALIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.3 EUROPE

9.3.1 IMPACT OF RECESSION

FIGURE 38 EUROPE: CERAMIC SUBSTRATES MARKET SNAPSHOT

9.3.2 EUROPE CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE

TABLE 119 EUROPE: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (USD MILLION)

TABLE 120 EUROPE: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (USD MILLION)

TABLE 121 EUROPE: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (TON)

TABLE 122 EUROPE: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (TON)

9.3.3 EUROPE CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY

TABLE 123 EUROPE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 124 EUROPE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 125 EUROPE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 126 EUROPE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.3.4 EUROPE CERAMIC SUBSTRATES MARKET, BY COUNTRY

TABLE 127 EUROPE: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (USD MILLION)

TABLE 128 EUROPE: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (USD MILLION)

TABLE 129 EUROPE: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (TON)

TABLE 130 EUROPE: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (TON)

9.3.4.1 Germany

9.3.4.1.1 Aerospace and automotive industries boosting demand for ceramic substrates

TABLE 131 GERMANY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 132 GERMANY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 133 GERMANY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 134 GERMANY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.3.4.2 France

9.3.4.2.1 Presence of major players in key sectors influencing market growth

TABLE 135 FRANCE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 136 FRANCE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 137 FRANCE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 138 FRANCE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.3.4.3 UK

9.3.4.3.1 Growth of automotive sector to propel market

TABLE 139 UK: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 140 UK: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 141 UK: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 142 UK: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.3.4.4 Italy

9.3.4.4.1 Aerospace and telecommunications industries influencing demand for ceramic substrates

TABLE 143 ITALY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 144 ITALY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 145 ITALY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 146 ITALY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.3.4.5 Poland

9.3.4.5.1 High economic growth to support market growth

TABLE 147 POLAND: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 148 POLAND: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 149 POLAND: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 150 POLAND: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.3.4.6 Netherlands

9.3.4.6.1 Expanding manufacturing base for various end-use segments driving market

TABLE 151 NETHERLANDS: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 152 NETHERLANDS: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 153 NETHERLANDS: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 154 NETHERLANDS: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.3.4.7 Russia

9.3.4.7.1 Electronics & appliances and automotive industries to propel demand

TABLE 155 RUSSIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 156 RUSSIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 157 RUSSIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 158 RUSSIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.4 NORTH AMERICA

9.4.1 IMPACT OF RECESSION

FIGURE 39 NORTH AMERICA: CERAMIC SUBSTRATES MARKET SNAPSHOT

9.4.2 NORTH AMERICA CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE

TABLE 159 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (USD MILLION)

TABLE 160 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (USD MILLION)

TABLE 161 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (TON)

TABLE 162 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (TON)

9.4.3 NORTH AMERICA CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY

TABLE 163 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 164 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 165 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 166 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.4.4 NORTH AMERICA CERAMIC SUBSTRATES MARKET, BY COUNTRY

TABLE 167 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (USD MILLION)

TABLE 168 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (USD MILLION)

TABLE 169 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (TON)

TABLE 170 NORTH AMERICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (TON)

9.4.4.1 US

9.4.4.1.1 Increasing demand from automotive, military, and electronics sectors to boosts market growth

TABLE 171 US: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 172 US: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 173 US: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 174 US: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.4.4.2 Canada

9.4.4.2.1 Increasing trend of miniaturization in telecom industry to fuel growth

TABLE 175 CANADA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 176 CANADA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 177 CANADA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 178 CANADA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.4.4.3 Mexico

9.4.4.3.1 Growing manufacturing industries and technological advancements to drive market

TABLE 179 MEXICO: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 180 MEXICO: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 181 MEXICO: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 182 MEXICO: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.5 MIDDLE EAST & AFRICA

9.5.1 IMPACT OF RECESSION

9.5.2 MIDDLE EAST & AFRICA CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE

TABLE 183 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (USD MILLION)

TABLE 184 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (USD MILLION)

TABLE 185 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (TON)

TABLE 186 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (TON)

9.5.3 MIDDLE EAST & AFRICA CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY

TABLE 187 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 188 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 189 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 190 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.5.4 MIDDLE EAST & AFRICA CERAMIC SUBSTRATES MARKET, BY COUNTRY

TABLE 191 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (USD MILLION)

TABLE 192 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (USD MILLION)

TABLE 193 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (TON)

TABLE 194 MIDDLE EAST & AFRICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (TON)

9.5.4.1 GCC

9.5.4.1.1 UAE

9.5.4.1.1.1 Largest market for ceramic substrates in Middle East & Africa

TABLE 195 UAE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 196 UAE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 197 UAE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 198 UAE: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.5.4.1.2 Saudi Arabia

9.5.4.1.2.1 High military spending to positively influence market

TABLE 199 SAUDI ARABIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 200 SAUDI ARABIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 201 SAUDI ARABIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 202 SAUDI ARABIA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.5.4.2 Turkey

9.5.4.2.1 Increase in production of consumer electronics to propel market

TABLE 203 TURKEY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 204 TURKEY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 205 TURKEY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 206 TURKEY: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.5.4.3 South Africa

9.5.4.3.1 Increasing demand from automotive sector to support market growth

TABLE 207 SOUTH AFRICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 208 SOUTH AFRICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 209 SOUTH AFRICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 210 SOUTH AFRICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.6 SOUTH AMERICA

9.6.1 IMPACT OF RECESSION

9.6.2 SOUTH AMERICA CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE

TABLE 211 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (USD MILLION)

TABLE 212 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (USD MILLION)

TABLE 213 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2017–2021 (TON)

TABLE 214 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY PRODUCT TYPE, 2022–2028 (TON)

9.6.3 SOUTH AMERICA CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY

TABLE 215 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 216 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 217 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 218 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

9.6.4 SOUTH AMERICA CERAMIC SUBSTRATES MARKET, BY COUNTRY

TABLE 219 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (USD MILLION)

TABLE 220 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (USD MILLION)

TABLE 221 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2017–2021 (TON)

TABLE 222 SOUTH AMERICA: CERAMIC SUBSTRATES MARKET, BY COUNTRY, 2022–2028 (TON)

9.6.4.1 Brazil

9.6.4.1.1 Growing aviation industry to drive demand for ceramic substrates

TABLE 223 BRAZIL: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (USD MILLION)

TABLE 224 BRAZIL: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (USD MILLION)

TABLE 225 BRAZIL: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2017–2021 (TON)

TABLE 226 BRAZIL: CERAMIC SUBSTRATES MARKET, BY END-USE INDUSTRY, 2022–2028 (TON)

10 COMPETITIVE LANDSCAPE (Page No. - 198)

10.1 INTRODUCTION

10.2 KEY PLAYER STRATEGIES

TABLE 227 OVERVIEW OF STRATEGIES ADOPTED BY KEY CERAMIC SUBSTRATE MANUFACTURERS

10.3 COMPARATIVE ANALYSIS OF MAJOR PLAYERS

TABLE 228 COMPARATIVE ANALYSIS OF MAJOR CERAMIC SUBSTRATE MANUFACTURERS

10.4 RANKING OF KEY MARKET PLAYERS, 2022

FIGURE 40 RANKING OF TOP 5 PLAYERS IN CERAMIC SUBSTRATES MARKET, 2022

10.5 MARKET SHARE ANALYSIS

TABLE 229 CERAMIC SUBSTRATES MARKET: DEGREE OF COMPETITION

FIGURE 41 KYOCERA CORPORATION LED CERAMIC SUBSTRATES MARKET IN 2022

10.6 REVENUE ANALYSIS OF TOP 5 PLAYERS

FIGURE 42 REVENUE ANALYSIS OF KEY COMPANIES IN LAST 5 YEARS

10.7 COMPANY EVALUATION MATRIX (TIER 1)

10.7.1 STARS

10.7.2 EMERGING LEADERS

10.7.3 PERVASIVE PLAYERS

10.7.4 PARTICIPANTS

FIGURE 43 COMPANY EVALUATION MATRIX, 2022

10.7.5 COMPANY FOOTPRINT

FIGURE 44 CERAMIC SUBSTRATES MARKET: COMPANY FOOTPRINT

TABLE 230 CERAMIC SUBSTRATES MARKET: PRODUCT TYPE FOOTPRINT

TABLE 231 CERAMIC SUBSTRATES MARKET: END-USE INDUSTRY FOOTPRINT

TABLE 232 CERAMIC SUBSTRATES MARKET: COMPANY REGION FOOTPRINT

10.8 START-UP/SME EVALUATION MATRIX

10.8.1 PROGRESSIVE COMPANIES

10.8.2 RESPONSIVE COMPANIES

10.8.3 DYNAMIC COMPANIES

10.8.4 STARTING BLOCKS

FIGURE 45 START-UP/SME EVALUATION MATRIX, 2022

10.8.5 COMPETITIVE BENCHMARKING

TABLE 233 CERAMIC SUBSTRATES MARKET: DETAILED LIST OF KEY START-UPS/SMES

TABLE 234 CERAMIC SUBSTRATES MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

10.9 COMPETITIVE SITUATION AND TRENDS

10.9.1 PRODUCT LAUNCHES

TABLE 235 CERAMIC SUBSTRATES MARKET: PRODUCT LAUNCHES (2018–2023)

10.9.2 OTHER DEVELOPMENTS

TABLE 236 CERAMIC SUBSTRATES MARKET: EXPANSIONS, INVESTMENTS, AND INNOVATIONS (2018–2023)

11 COMPANY PROFILES (Page No. - 221)

(Business overview, Products offered, Recent developments & MnM View)*

11.1 KEY PLAYERS

11.1.1 KYOCERA CORPORATION

TABLE 237 KYOCERA CORPORATION: COMPANY OVERVIEW

FIGURE 46 KYOCERA CORPORATION: COMPANY SNAPSHOT

11.1.2 MURATA MANUFACTURING CO., LTD.

TABLE 238 MURATA MANUFACTURING CO., LTD.: COMPANY OVERVIEW

FIGURE 47 MURATA MANUFACTURING CO., LTD.: COMPANY SNAPSHOT

11.1.3 COORSTEK INC.

TABLE 239 COORSTEK INC.: COMPANY OVERVIEW

11.1.4 CERAMTEC GMBH

TABLE 240 CERAMTEC GMBH: COMPANY OVERVIEW

FIGURE 48 CERAMTEC GMBH: COMPANY SNAPSHOT

11.1.5 MARUWA CO., LTD.

TABLE 241 MARUWA CO., LTD.: COMPANY OVERVIEW

FIGURE 49 MARUWA CO., LTD.: COMPANY SNAPSHOT

11.1.6 KOA CORPORATION

TABLE 242 KOA CORPORATION: COMPANY OVERVIEW

FIGURE 50 KOA CORPORATION: COMPANY SNAPSHOT

11.1.7 YOKOWO CO., LTD.

TABLE 243 YOKOWO CO., LTD.: COMPANY OVERVIEW

FIGURE 51 YOKOWO CO., LTD.: COMPANY SNAPSHOT

11.1.8 TONG HSING ELECTRONIC INDUSTRIES, LTD.

TABLE 244 TONG HSING ELECTRONIC INDUSTRIES, LTD.: COMPANY OVERVIEW

FIGURE 52 TONG HSING ELECTRONIC INDUSTRIES, LTD.: COMPANY SNAPSHOT

11.1.9 LEATEC FINE CERAMICS CO., LTD.

TABLE 245 LEATEC FINE CERAMICS CO., LTD.: COMPANY OVERVIEW

FIGURE 53 LEATEC FINE CERAMICS CO., LTD.: COMPANY SNAPSHOT

11.1.10 NIKKO COMPANY

TABLE 246 NIKKO COMPANY: COMPANY OVERVIEW

FIGURE 54 NIKKO COMPANY: COMPANY SNAPSHOT

*Details on Business overview, Products offered, Recent developments & MnM View might not be captured in case of unlisted companies.

11.2 OTHER PLAYERS

11.2.1 NITERRA CO., LTD.

TABLE 247 NITERRA CO., LTD.: COMPANY OVERVIEW

11.2.2 ENRG INC.

TABLE 248 ENRG INC.: COMPANY OVERVIEW

11.2.3 NIPPON CARBIDE INDUSTRIES CO., INC.

TABLE 249 NIPPON CARBIDE INDUSTRIES CO., INC.: COMPANY OVERVIEW

11.2.4 TA-I TECHNOLOGY CO., LTD.

TABLE 250 TA-I TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

11.2.5 ECOCERA OPTRONICS CO., LTD.

TABLE 251 ECOCERA OPTRONICS CO., LTD.: COMPANY OVERVIEW

11.2.6 TOSHIBA MATERIALS CO., LTD.

TABLE 252 TOSHIBA MATERIALS CO., LTD.: COMPANY OVERVIEW

11.2.7 ICP TECHNOLOGY CO., LTD.

TABLE 253 ICP TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

11.2.8 ADVANCED SUBSTRATE MICROTECHNOLOGY CORPORATION

TABLE 254 ADVANCED SUBSTRATE MICROTECHNOLOGY CORPORATION: COMPANY OVERVIEW

11.2.9 ANAREN

TABLE 255 ANAREN: COMPANY OVERVIEW

11.2.10 CHAOZHOU THREE-CIRCLE (GROUP) CO., LTD.

TABLE 256 CHAOZHOU THREE-CIRCLE (GROUP) CO., LTD.: COMPANY OVERVIEW

11.2.11 AGC INC.

TABLE 257 AGC INC.: COMPANY OVERVIEW

11.2.12 HITECH CERAMICS

TABLE 258 HITECH CERAMICS: COMPANY OVERVIEW

11.2.13 ORTECH ADVANCED CERAMICS

TABLE 259 ORTECH ADVANCED CERAMICS: COMPANY OVERVIEW

11.2.14 STANFORD ADVANCED MATERIALS

TABLE 260 STANFORD ADVANCED MATERIALS: COMPANY OVERVIEW

11.2.15 ANTS CERAMICS

TABLE 261 ANTS CERAMICS: COMPANY OVERVIEW

12 ADJACENT MARKETS (Page No. - 256)

12.1 INTRODUCTION

12.2 LIMITATION

12.3 HERMETIC PACKAGING MARKET

12.3.1 MARKET DEFINITION

12.3.2 MARKET OVERVIEW

12.4 HERMETIC PACKAGING MARKET, BY REGION

TABLE 262 HERMETIC PACKAGING MARKET, BY REGION, 2018–2025 (USD MILLION)

12.4.1 ASIA PACIFIC

TABLE 263 HERMETIC PACKAGING MARKET IN ASIA PACIFIC, BY COUNTRY, 2018–2025 (USD MILLION)

12.4.2 EUROPE

TABLE 264 HERMETIC PACKAGING MARKET IN EUROPE, BY COUNTRY, 2018–2025 (USD MILLION)

12.4.3 NORTH AMERICA

TABLE 265 HERMETIC PACKAGING MARKET IN NORTH AMERICA, BY COUNTRY, 2018–2025 (USD MILLION)

12.4.4 REST OF WORLD

TABLE 266 HERMETIC PACKAGING MARKET IN REST OF WORLD, BY REGION, 2018–2025 (USD MILLION)

13 APPENDIX (Page No. - 260)

13.1 DISCUSSION GUIDE

13.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

13.3 CUSTOMIZATION OPTIONS

13.4 RELATED REPORTS

13.5 AUTHOR DETAILS

Growth opportunities and latent adjacency in Ceramic Substrates Market