TABLE OF CONTENTS

1 INTRODUCTION

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS (Page No. - 44)

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AMPHOTERIC SURFACTANTS MARKET

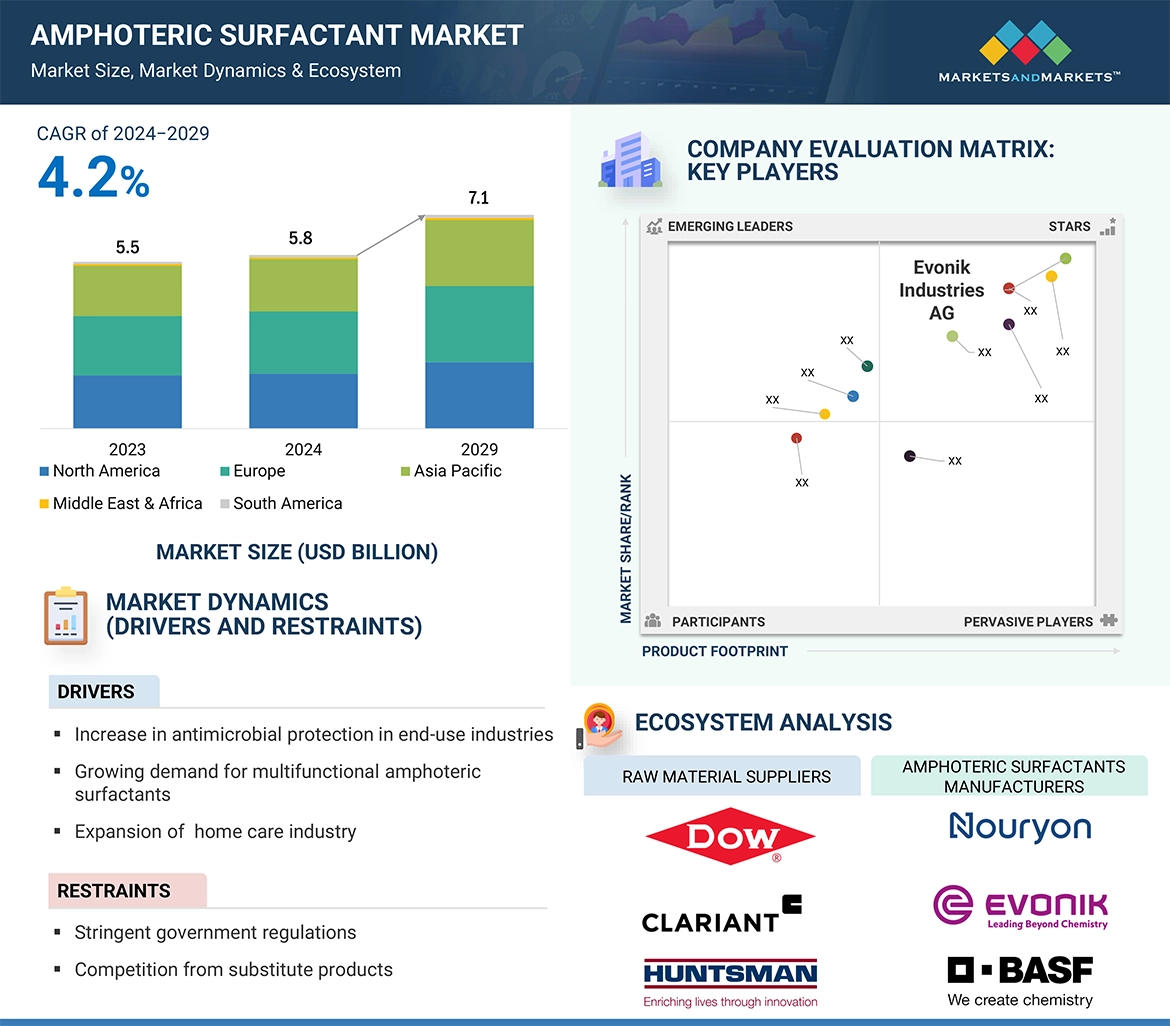

4.2 AMPHOTERIC SURFACTANTS MARKET, BY REGION

4.3 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION AND COUNTRY

4.4 AMPHOTERIC SURFACTANTS MARKET, TYPE VS REGION

4.5 AMPHOTERIC SURFACTANTS MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW (Page No. - 47)

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Pressing need for antimicrobial protection in end-use industries

5.2.1.2 Rising demand for multifunctional amphoteric surfactants

5.2.1.3 Expansion of home care industry

5.2.2 RESTRAINTS

5.2.2.1 Stringent government regulations

5.2.2.2 Competition from substitute products

5.2.3 OPPORTUNITIES

5.2.3.1 Pressing need for bio-based amphoteric surfactants and sustainable green surfactants

5.2.3.2 Growing demand for mild and hypoallergenic personal care products

5.2.4 CHALLENGES

5.2.4.1 Volatility in raw material prices

5.3 PORTER’S FIVE FORCES ANALYSIS

5.3.1 THREAT OF NEW ENTRANTS

5.3.2 THREAT OF SUBSTITUTES

5.3.3 BARGAINING POWER OF SUPPLIERS

5.3.4 BARGAINING POWER OF BUYERS

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 KEY STAKEHOLDERS & BUYING CRITERIA

5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.4.2 BUYING CRITERIA

5.5 MACROECONOMIC OUTLOOK

5.5.1 GDP TRENDS AND FORECAST FOR MAJOR ECONOMIES

6 INDUSTRY TRENDS (Page No. - 57)

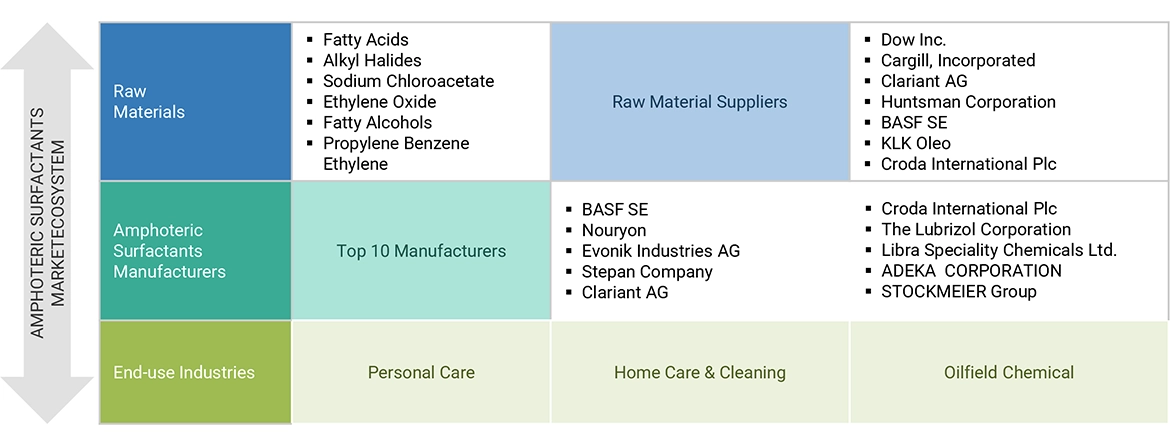

6.1 SUPPLY CHAIN ANALYSIS

6.1.1 RAW MATERIAL

6.1.2 AMPHOTERIC SURFACTANT MANUFACTURERS

6.1.3 DISTRIBUTION NETWORK

6.1.4 END-USE INDUSTRIES

6.2 PRICING ANALYSIS

6.2.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

6.2.2 AVERAGE SELLING PRICE TREND, BY REGION

6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.4 ECOSYSTEM ANALYSIS/ MARKET MAP

6.5 TECHNOLOGY ANALYSIS

6.5.1 KEY TECHNOLOGIES

6.5.1.1 Glucose-based surfactants with calcium chelating properties

6.5.2 COMPLEMENTARY TECHNOLOGIES

6.5.2.1 Amino acid soaps derived from dodecenyl succinic anhydride

6.6 CASE STUDY ANALYSIS

6.6.1 CASE STUDY ON CRODA INTERNATIONAL PLC

6.6.2 CASE STUDY OF EVONIK INDUSTRIES AG

6.6.3 CASE STUDY OF BASF SE

6.7 TRADE ANALYSIS

6.7.1 IMPORT SCENARIO (HS CODE 340290)

6.7.2 EXPORT SCENARIO (HS CODE 340290)

6.8 REGULATORY LANDSCAPE

6.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.9 KEY CONFERENCES & EVENTS IN 2024–2025

6.10 INVESTMENT AND FUNDING SCENARIO

6.11 PATENT ANALYSIS

6.11.1 APPROACH

6.11.2 DOCUMENT TYPES

6.11.3 TOP APPLICANTS

6.11.4 JURISDICTION ANALYSIS

6.12 IMPACT OF AI/GEN-AI ON AMPHOTERIC SURFACTANTS MARKET

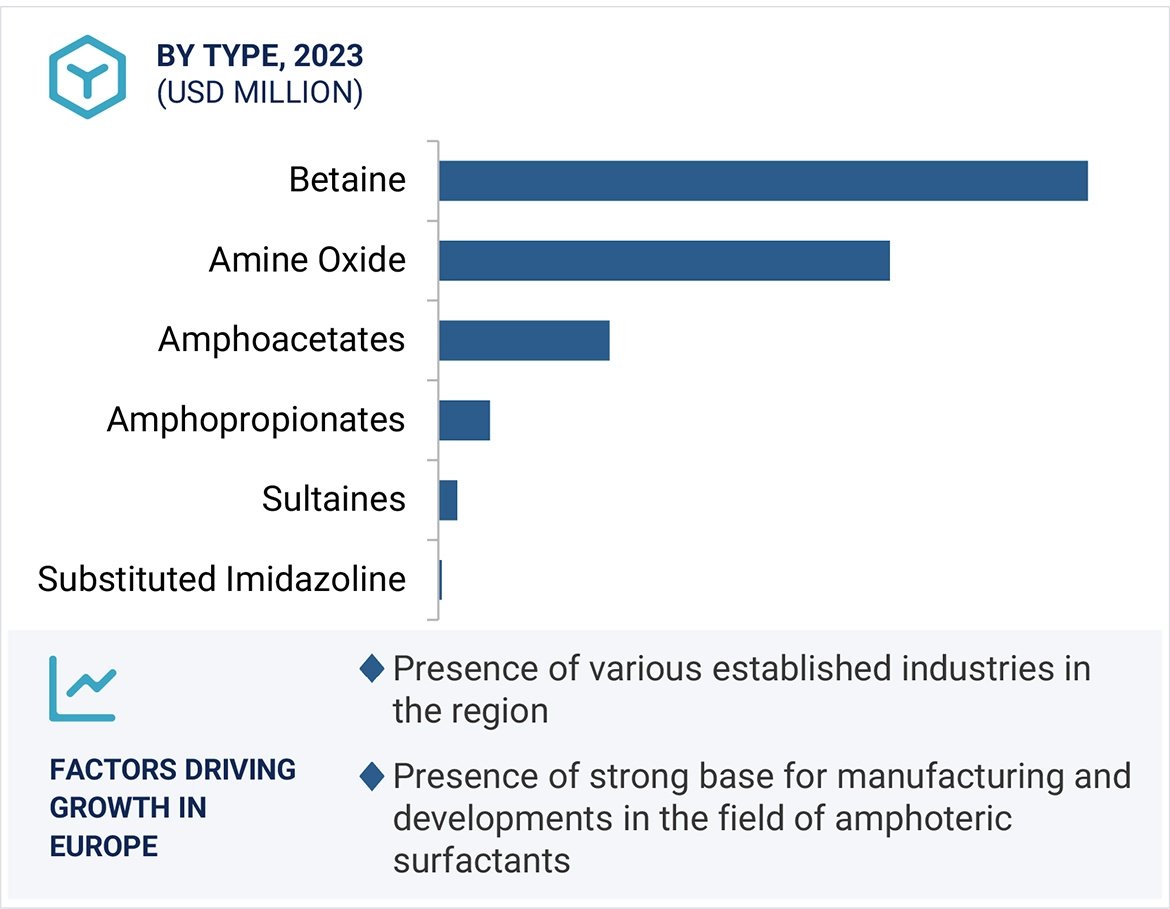

7 AMPHOTERIC SURFACTANTS MARKET, BY TYPE (Page No. - 80)

7.1 INTRODUCTION

7.2 BETAINES

7.2.1 INCREASING DEMAND IN PERSONAL CARE APPLICATIONS TO DRIVE MARKET

7.3 AMINE OXIDES

7.3.1 EXTENSIVE USE OF MILD AND GENTLE SURFACTANTS IN HOME CARE PRODUCTS TO DRIVE MARKET

7.4 AMPHOACETATES

7.4.1 COMPATIBILITY OF AMPHOACETATES WITH OTHER SURFACTANTS TO BOOST MARKET

7.5 AMPHOPROPIONATES

7.5.1 GROWING DEMAND FOR PERSONAL CARE PRODUCTS TO DRIVE MARKET

7.6 SULTAINES

7.6.1 PRESSING NEED FOR HOME CARE AND INDUSTRIAL CLEANING PRODUCTS TO BOOST MARKET

7.7 SUBSTITUTED IMIDAZOLINES

7.7.1 RISING HYGIENE AWARENESS TO DRIVE DEMAND FOR SUBSTITUTE IMIDAZOLINE-BASED SURFACTANTS

8 AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION (Page No. - 94)

8.1 INTRODUCTION

8.2 PERSONAL CARE

8.2.1 RISING CONSUMER SPENDING AND INCREASING DISPOSABLE INCOME TO DRIVE DEMAND

8.3 HOME CARE AND CLEANING

8.3.1 GROWING DEMAND FOR DETERGENTS, FABRIC SOFTENERS, AND DISHWASHING AGENTS TO DRIVE MARKET

8.4 OIL FIELD CHEMICALS

8.4.1 SURGE IN OIL EXPLORATION TO DRIVE DEMAND FOR AMPHOTERIC SURFACTANTS

8.5 AGRICULTURE

8.5.1 NEED FOR ADJUVANTS IN AGROCHEMICALS TO DRIVE MARKET

8.6 OTHER APPLICATIONS

9 AMPHOTERIC SURFACTANTS MARKET, BY REGION (Page No. - 109)

9.1 INTRODUCTION

9.2 ASIA PACIFIC

9.2.1 CHINA

9.2.1.1 Rising demand for skin and hair care products to drive market

9.2.2 JAPAN

9.2.2.1 Strong foothold of major home care manufacturers to drive market

9.2.3 INDIA

9.2.3.1 Increased demand for personal care products to drive market

9.3 EUROPE

9.3.1 FRANCE

9.3.1.1 Rising demand for personal care products to drive market

9.3.2 GERMANY

9.3.2.1 Increasing need for premium quality products to drive market

9.3.3 ITALY

9.3.3.1 Growth of homecare and cleaning industries to drive market

9.3.4 RUSSIA

9.3.4.1 Rising demand for oil recovery and drilling fluid additives from oil & gas industry to drive market

9.4 NORTH AMERICA

9.4.1 US

9.4.1.1 Presence of major personal care manufacturers to drive market

9.4.2 CANADA

9.4.2.1 Aging population and increase in self-care awareness to drive market

9.4.3 MEXICO

9.4.3.1 Increase in purchasing power and demand for grooming products to drive market

9.5 MIDDLE EAST & AFRICA

9.5.1 GCC COUNTRIES

9.5.1.1 Saudi Arabia

9.5.1.1.1 Surging demand for oil field chemicals to drive market

9.5.2 IRAN

9.5.2.1 Growing regulatory emphasis on safety and environmental standards to fuel demand for surfactants

9.5.3 TURKEY

9.5.3.1 Rapid economic revolution to drive market

9.6 SOUTH AMERICA

9.6.1 BRAZIL

9.6.1.1 Growth of agriculture sector to drive market

9.6.2 ARGENTINA

9.6.3 Increasing consumer expenditure on FMCG products to drive market

10 COMPETITIVE LANDSCAPE (Page No. - 165)

10.1 INTRODUCTION

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

10.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY AMPHOTERIC SURFACTANT MANUFACTURERS

10.3 MARKET SHARE ANALYSIS

10.4 REVENUE ANALYSIS OF TOP FIVE PLAYERS (2019–2023)

10.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

10.5.1 STARS

10.5.2 EMERGING LEADERS

10.5.3 PERVASIVE PLAYERS

10.5.4 PARTICIPANTS

10.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

10.5.5.1 Company footprint

10.5.5.2 Type footprint

10.5.5.3 Application footprint

10.5.5.4 Region footprint

10.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2023

10.6.1 PROGRESSIVE COMPANIES

10.6.2 RESPONSIVE COMPANIES

10.6.3 DYNAMIC COMPANIES

10.6.4 STARTING BLOCKS

10.6.5 COMPETITIVE BENCHMARKING: START-UPS/SMES, 2023

10.6.5.1 Detailed list of key start-ups/SMES

10.6.5.2 Competitive benchmarking of key start-ups/SMEs

10.7 BRAND/PRODUCT COMPARISON ANALYSIS

10.8 COMPANY VALUATION AND FINANCIAL METRICS

10.9 COMPETITIVE SCENARIO & TRENDS

10.9.1 DEALS

11 COMPANY PROFILES (Page No. - 183)

11.1 KEY PLAYERS

11.1.1 NOURYON

11.1.1.1 Business overview

11.1.1.2 Products/Solutions/Services offered

11.1.1.3 MnM view

11.1.1.3.1 Right to win

11.1.1.3.2 Strategic choices

11.1.1.3.3 Weaknesses and competitive threats

11.1.2 EVONIK INDUSTRIES AG

11.1.2.1 Business overview

11.1.2.2 Products/Solutions/Services offered

11.1.2.3 MnM view

11.1.2.3.1 Right to win

11.1.2.3.2 Strategic choices

11.1.2.3.3 Weaknesses and competitive threats

11.1.3 CLARIANT AG

11.1.3.1 Business overview

11.1.3.2 Products/Solutions/Services offered

11.1.3.3 MnM view

11.1.3.3.1 Right to win

11.1.3.3.2 Strategic choices

11.1.3.3.3 Weaknesses and competitive threats

11.1.4 CRODA INTERNATIONAL PLC

11.1.4.1 Business overview

11.1.4.2 Products/Solutions/Services offered

11.1.4.3 Recent developments

11.1.4.3.1 Deals

11.1.4.4 MnM view

11.1.4.4.1 Right to win

11.1.4.4.2 Strategic choices

11.1.4.4.3 Weaknesses and competitive threats

11.1.5 BASF SE

11.1.5.1 Business overview

11.1.5.2 Products/Solutions/Services offered

11.1.5.3 MnM view

11.1.5.3.1 Right to win

11.1.5.3.2 Strategic choices

11.1.5.3.3 Weaknesses and competitive threats

11.1.6 STEPAN COMPANY

11.1.6.1 Business overview

11.1.6.2 Products/Solutions/Services offered

11.1.7 THE LUBRIZOL CORPORATION

11.1.7.1 Business overview

11.1.7.2 Products/Solutions/Services offered

11.1.8 LIBRA SPECIALITY CHEMICALS LTD.

11.1.8.1 Business overview

11.1.8.2 Products/Solutions/Services offered

11.1.9 ADEKA CORPORATION

11.1.9.1 Business overview

11.1.9.2 Products/Solutions/Services offered

11.1.10 STOCKMEIER GROUP

11.1.10.1 Business overview

11.1.10.2 Products/Solutions/Services offered

11.2 OTHER PLAYERS

11.2.1 AK CHEMTECH CO., LTD.

11.2.2 ARXADA AG

11.2.3 INDORAMA VENTURES PUBLIC COMPANY LIMITED

11.2.4 TAIWAN SURFACTANT

11.2.5 PILOT CHEMICAL CORP.

11.2.6 NOF CORPORATION

11.2.7 SINO-JAPAN CHEMICAL CO., LTD.

11.2.8 LANKEM

11.2.9 ALPHA CHEMICALS PRIVATE LIMITED

11.2.10 STPP GROUP

11.2.11 KENSING

11.2.12 HENAN GP CHEMICALS CO., LTD.

11.2.13 NANJING CHEMICAL MATERIAL CORP.

11.2.14 SHANDONG KERUI CHEMICALS CO., LTD.

11.2.15 STERLING AUXILIARIES PVT. LTD.

12 ADJACENT & RELATED MARKETS (Page No. - 215)

12.1 INTRODUCTION

12.2 LIMITATIONS

12.3 BIOSURFACTANTS MARKET

12.3.1 MARKET DEFINITION

12.3.2 MARKET OVERVIEW

12.3.3 BIOSURFACTANTS MARKET, BY REGION

12.3.3.1 Europe

12.3.3.2 Asia Pacific

12.3.3.3 North America

12.3.3.4 Rest of the World (RoW)

13 APPENDIX (Page No. - 223)

13.1 DISCUSSION GUIDE

13.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

13.3 CUSTOMIZATION OPTIONS

13.4 RELATED REPORTS

13.5 AUTHOR DETAILS

LIST OF TABLES (268 TABLES)

TABLE 1 MARKET DEFINITION AND INCLUSIONS, BY TYPE

TABLE 2 MARKET DEFINITION AND INCLUSIONS, BY APPLICATION

TABLE 3 AMPHOTERIC SURFACTANTS MARKET: PORTER’S FIVE FORCES ANALYSIS

TABLE 4 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS (%)

TABLE 5 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

TABLE 6 GDP TRENDS AND FORECAST OF MAJOR ECONOMIES, 2021–2029 (USD BILLION)

TABLE 7 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR TOP 3 APPLICATIONS, USD/KG

TABLE 8 AVERAGE SELLING PRICE TREND, BY REGION (USD/KG)

TABLE 9 AMPHOTERIC SURFACTANTS MARKET: ROLE IN ECOSYSTEM

TABLE 10 IMPORT SCENARIO OF HS CODE 340290-COMPLIANT PRODUCTS, BY REGION, 2018–2023 (USD MILLION)

TABLE 11 EXPORT SCENARIO OF HS CODE 340290-COMPLIANT PRODUCTS, BY REGION, 2018–2023 (USD MILLION)

TABLE 12 NORTH AMERICA: REGULATIONS RELATED TO AMPHOTERIC SURFACTANTS

TABLE 13 EUROPE: REGULATIONS RELATED TO AMPHOTERIC SURFACTANTS

TABLE 14 ASIA PACIFIC: REGULATIONS RELATED TO AMPHOTERIC SURFACTANTS

TABLE 15 MIDDLE EAST & AFRICA: REGULATIONS RELATED TO AMPHOTERIC SURFACTANTS

TABLE 16 AMPHOTERIC SURFACTANTS MARKET: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 17 AMPHOTERIC SURFACTANTS MARKET: DETAILED LIST OF CONFERENCES & EVENTS, 2024–2025

TABLE 18 AMPHOTERIC SURFACTANTS MARKET: FUNDING/INVESTMENT

TABLE 19 TOTAL PATENT COUNT FOR AMPHOTERIC SURFACTANTS

TABLE 20 MAJOR PATENTS FOR AMPHOTERIC SURFACTANTS

TABLE 21 PATENTS BY PROCTER & GAMBLE

TABLE 22 PATENTS BY BASF SE

TABLE 23 PATENTS BY UNILEVER

TABLE 24 TOP 10 PATENT OWNERS IN CHINA, 2013–2023

TABLE 25 AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (USD MILLION)

TABLE 26 AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 27 AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (KILOTON)

TABLE 28 AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (KILOTON)

TABLE 29 BETAINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 30 BETAINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 31 BETAINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 32 BETAINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 33 AMINE OXIDES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 34 AMINE OXIDES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 35 AMINE OXIDES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 36 AMINE OXIDES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 37 AMPHOACETATES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 38 AMPHOACETATES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 39 AMPHOACETATES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 40 AMPHOACETATES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 41 AMPHOPROPIONATES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 42 AMPHOPROPIONATES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 43 AMPHOPROPIONATES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 44 AMPHOPROPIONATES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 45 SULTAINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 46 SULTAINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 47 SULTAINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 48 SULTAINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 49 SUBSTITUTED IMIDAZOLINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 50 SUBSTITUTED IMIDAZOLINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 51 SUBSTITUTED IMIDAZOLINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 52 SUBSTITUTED IMIDAZOLINES: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 53 SURFACTANTS: BREAKDOWN BY APPLICATION

TABLE 54 AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 55 AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 56 AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 57 AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 58 PERSONAL CARE: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 59 PERSONAL CARE: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 60 PERSONAL CARE: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 61 PERSONAL CARE: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 62 PERSONAL CARE: AMPHOTERIC SURFACTANTS MARKET, BY SUB-APPLICATION, 2018–2023 (USD MILLION)

TABLE 63 PERSONAL CARE: AMPHOTERIC SURFACTANTS MARKET, BY SUB-APPLICATION, 2024–2029 (USD MILLION)

TABLE 64 PERSONAL CARE: AMPHOTERIC SURFACTANTS MARKET, BY SUB-APPLICATION, 2018–2023 (KILOTON)

TABLE 65 PERSONAL CARE: AMPHOTERIC SURFACTANTS MARKET, BY SUB-APPLICATION, 2024–2029 (KILOTON)

TABLE 66 HOME CARE AND CLEANING: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 67 HOME CARE AND CLEANING: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 68 HOME CARE AND CLEANING: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 69 HOME CARE AND CLEANING: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 70 OIL FIELD CHEMICALS: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 71 OIL FIELD CHEMICALS: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 72 OIL FIELD CHEMICALS: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 73 OIL FIELD CHEMICALS: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 74 AGRICULTURE: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 75 AGRICULTURE: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 76 AGRICULTURE: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 77 AGRICULTURE: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 78 OTHER APPLICATIONS: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 79 OTHER APPLICATIONS: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 80 OTHER APPLICATIONS: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 81 OTHER APPLICATIONS: AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 82 AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (KILOTON)

TABLE 83 AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (KILOTON)

TABLE 84 AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2018–2023 (USD MILLION)

TABLE 85 AMPHOTERIC SURFACTANTS MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 86 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (KILOTON)

TABLE 87 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (KILOTON)

TABLE 88 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (USD MILLION)

TABLE 89 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 90 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 91 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 92 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 93 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 94 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (KILOTON)

TABLE 95 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (KILOTON)

TABLE 96 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (USD MILLION)

TABLE 97 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 98 CHINA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 99 CHINA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 100 CHINA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 101 CHINA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 102 JAPAN: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 103 JAPAN: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 104 JAPAN: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 105 JAPAN: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 106 INDIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 107 INDIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 108 INDIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 109 INDIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 110 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (KILOTON)

TABLE 111 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (KILOTON)

TABLE 112 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (USD MILLION)

TABLE 113 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 114 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 115 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 116 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 117 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 118 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (KILOTON)

TABLE 119 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (KILOTON)

TABLE 120 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (USD MILLION)

TABLE 121 EUROPE: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 122 FRANCE: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 123 FRANCE: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 124 FRANCE: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 125 FRANCE: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 126 GERMANY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 127 GERMANY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 128 GERMANY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 129 GERMANY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 130 ITALY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 131 ITALY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 132 ITALY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 133 ITALY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 134 RUSSIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 135 RUSSIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 136 RUSSIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 137 RUSSIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 138 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (KILOTON)

TABLE 139 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (KILOTON)

TABLE 140 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (USD MILLION)

TABLE 141 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 142 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 143 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 144 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 145 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 146 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (KILOTON)

TABLE 147 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (KILOTON)

TABLE 148 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (USD MILLION)

TABLE 149 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 150 US: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 151 US: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 152 US: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 153 US: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 154 CANADA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 155 CANADA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 156 CANADA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 157 CANADA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 158 MEXICO: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 159 MEXICO: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 160 MEXICO: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 161 MEXICO: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 162 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (USD MILLION)

TABLE 163 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 164 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (KILOTON)

TABLE 165 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (KILOTON)

TABLE 166 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 167 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 168 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 169 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 170 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (USD MILLION)

TABLE 171 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 172 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (KILOTON)

TABLE 173 MIDDLE EAST & AFRICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (KILOTON)

TABLE 174 SAUDI ARABIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 175 SAUDI ARABIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 176 SAUDI ARABIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 177 SAUDI ARABIA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 178 IRAN: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 179 IRAN: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 180 IRAN: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 181 IRAN: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 182 TURKEY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 183 TURKEY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 184 TURKEY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 185 TURKEY: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 186 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (USD MILLION)

TABLE 187 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 188 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2018–2023 (KILOTON)

TABLE 189 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY TYPE, 2024–2029 (KILOTON)

TABLE 190 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 191 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 192 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 193 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 194 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (USD MILLION)

TABLE 195 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 196 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2018–2023 (KILOTON)

TABLE 197 SOUTH AMERICA: AMPHOTERIC SURFACTANTS MARKET, BY COUNTRY, 2024–2029 (KILOTON)

TABLE 198 BRAZIL: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 199 BRAZIL: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 200 BRAZIL: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 201 BRAZIL: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 202 ARGENTINA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (USD MILLION)

TABLE 203 ARGENTINA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 204 ARGENTINA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2018–2023 (KILOTON)

TABLE 205 ARGENTINA: AMPHOTERIC SURFACTANTS MARKET, BY APPLICATION, 2024–2029 (KILOTON)

TABLE 206 AMPHOTERIC SURFACTANTS MARKET: DEGREE OF COMPETITION

TABLE 207 AMPHOTERIC SURFACTANTS MARKET: TYPE FOOTPRINT

TABLE 208 AMPHOTERIC SURFACTANTS MARKET: APPLICATION FOOTPRINT

TABLE 209 AMPHOTERIC SURFACTANTS MARKET: REGION FOOTPRINT

TABLE 210 AMPHOTERIC SURFACTANTS MARKET: DETAILED LIST OF KEY START-UPS/SMES

TABLE 211 AMPHOTERIC SURFACTANTS MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES (3 COMPANIES)

TABLE 212 AMPHOTERIC SURFACTANTS MARKET: DEALS, JANUARY 2019–MARCH 2024

TABLE 213 NOURYON: COMPANY OVERVIEW

TABLE 214 NOURYON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 215 EVONIK INDUSTRIES AG: COMPANY OVERVIEW

TABLE 216 EVONIK INDUSTRIES AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 217 CLARIANT AG: COMPANY OVERVIEW

TABLE 218 CLARIANT AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 219 CRODA INTERNATIONAL PLC: COMPANY OVERVIEW

TABLE 220 CRODA INTERNATIONAL PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 221 CRODA INTERNATIONAL PLC: DEALS

TABLE 222 BASF SE: COMPANY OVERVIEW

TABLE 223 BASF SE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 224 STEPAN COMPANY: COMPANY OVERVIEW

TABLE 225 STEPAN COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 226 THE LUBRIZOL CORPORATION: COMPANY OVERVIEW

TABLE 227 THE LUBRIZOL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 228 LIBRA SPECIALITY CHEMICALS LTD.: COMPANY OVERVIEW

TABLE 229 LIBRA SPECIALITY CHEMICALS LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 230 ADEKA CORPORATION: COMPANY OVERVIEW

TABLE 231 ADEKA CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 232 STOCKMEIER GROUP: COMPANY OVERVIEW

TABLE 233 STOCKMEIER GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 234 AK CHEMTECH CO., LTD.: COMPANY OVERVIEW

TABLE 235 ARXADA AG: COMPANY OVERVIEW

TABLE 236 INDORAMA VENTURES PUBLIC COMPANY LIMITED: COMPANY OVERVIEW

TABLE 237 TAIWAN SURFACTANT: COMPANY OVERVIEW

TABLE 238 PILOT CHEMICAL CORP.: COMPANY OVERVIEW

TABLE 239 NOF CORPORATION: COMPANY OVERVIEW

TABLE 240 SINO-JAPAN CHEMICAL CO., LTD.: COMPANY OVERVIEW

TABLE 241 LANKEM: COMPANY OVERVIEW

TABLE 242 ALPHA CHEMICALS PRIVATE LIMITED: COMPANY OVERVIEW

TABLE 243 STPP GROUP: COMPANY OVERVIEW

TABLE 244 KENSING: COMPANY OVERVIEW

TABLE 245 HENAN GP CHEMICALS CO., LTD.: COMPANY OVERVIEW

TABLE 246 NANJING CHEMICAL MATERIAL CORP.: COMPANY OVERVIEW

TABLE 247 SHANDONG KERUI CHEMICALS CO., LTD.: COMPANY OVERVIEW

TABLE 248 STERLING AUXILIARIES PVT. LTD.: COMPANY OVERVIEW

TABLE 249 BIOSURFACTANTS MARKET, BY REGION, 2017–2020 (USD THOUSAND)

TABLE 250 BIOSURFACTANTS MARKET, BY REGION, 2021–2027 (USD THOUSAND)

TABLE 251 BIOSURFACTANTS MARKET, BY REGION, 2017–2020 (TON)

TABLE 252 BIOSURFACTANTS MARKET, BY REGION, 2021–2027 (TON)

TABLE 253 EUROPE: BIOSURFACTANTS MARKET, BY COUNTRY, 2017–2020 (USD THOUSAND)

TABLE 254 EUROPE: BIOSURFACTANTS MARKET, BY COUNTRY, 2021–2027 (USD THOUSAND)

TABLE 255 EUROPE: BIOSURFACTANTS MARKET, BY COUNTRY, 2017–2020 (TON)

TABLE 256 EUROPE: BIOSURFACTANTS MARKET, BY COUNTRY, 2021–2027 (TON)

TABLE 257 ASIA PACIFIC: BIOSURFACTANTS MARKET, BY COUNTRY, 2017–2020 (USD THOUSAND)

TABLE 258 ASIA PACIFIC: BIOSURFACTANTS MARKET, BY COUNTRY, 2021–2027 (USD THOUSAND)

TABLE 259 ASIA PACIFIC: BIOSURFACTANTS MARKET, BY COUNTRY, 2017–2020 (TON)

TABLE 260 ASIA PACIFIC: BIOSURFACTANTS MARKET, BY COUNTRY, 2021–2027 (TON)

TABLE 261 NORTH AMERICA: BIOSURFACTANTS MARKET, BY COUNTRY, 2017–2020 (USD THOUSAND)

TABLE 262 NORTH AMERICA: BIOSURFACTANTS MARKET, BY COUNTRY, 2021–2027 (USD THOUSAND)

TABLE 263 NORTH AMERICA: BIOSURFACTANTS MARKET, BY COUNTRY, 2017–2020 (TON)

TABLE 264 NORTH AMERICA: BIOSURFACTANTS MARKET, BY COUNTRY, 2021–2027 (TON)

TABLE 265 ROW: BIOSURFACTANTS MARKET, BY COUNTRY, 2017–2020 (USD THOUSAND)

TABLE 266 ROW: BIOSURFACTANTS MARKET, BY COUNTRY,2021–2027 (USD THOUSAND)

TABLE 267 ROW: BIOSURFACTANTS MARKET, BY COUNTRY, 2017–2020 (TON)

TABLE 268 ROW: BIOSURFACTANTS MARKET, BY COUNTRY, 2021–2027 (TON)

LIST OF FIGURES (53 FIGURES)

FIGURE 1 AMPHOTERIC SURFACTANTS MARKET: RESEARCH DESIGN

FIGURE 2 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 (SUPPLY SIDE)—COLLECTIVE SHARE OF MAJOR PLAYERS

FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 2 (BOTTOM UP: SUPPLY SIDE)—COLLECTIVE REVENUE OF ALL PRODUCTS

FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 3—BOTTOM UP (DEMAND SIDE)

FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1—TOP-DOWN

FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 2—TOP-DOWN

FIGURE 7 AMPHOTERIC SURFACTANTS MARKET: DATA TRIANGULATION

FIGURE 8 SUPPLY-SIDE MARKET CAGR PROJECTIONS

FIGURE 9 DEMAND-SIDE MARKET GROWTH PROJECTIONS: DRIVERS AND OPPORTUNITIES

FIGURE 10 BETAINES TO DOMINATE AMPHOTERIC SURFACTANTS MARKET DURING FORECAST PERIOD

FIGURE 11 PERSONAL CARE SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 12 ASIA PACIFIC TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 13 RISING DEMAND FOR AMPHOTERIC SURFACTANTS IN ASIA PACIFIC TO DRIVE MARKET DURING FORECAST PERIOD

FIGURE 14 ASIA PACIFIC TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 15 CHINA AND APPLICATION SEGMENT DOMINATED MARKET IN 2023

FIGURE 16 BETAINES DOMINATED AMPHOTERIC SURFACTANTS MARKET ACROSS REGIONS IN 2023

FIGURE 17 INDIA TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN AMPHOTERIC SURFACTANTS MARKET

FIGURE 19 AMPHOTERIC SURFACTANTS MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 20 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP 3 APPLICATIONS

FIGURE 21 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

FIGURE 22 AMPHOTERIC SURFACTANTS MARKET: SUPPLY CHAIN ANALYSIS

FIGURE 23 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR TOP 3 APPLICATIONS

FIGURE 24 AVERAGE SELLING PRICE TREND OF AMPHOTERIC SURFACTANTS, BY REGION

FIGURE 25 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 26 AMPHOTERIC SURFACTANTS MARKET: ECOSYSTEM

FIGURE 27 IMPORT DATA FOR HS CODE 340290, BY KEY COUNTRY, 2018–2023

FIGURE 28 EXPORT DATA FOR HS CODE 340290, BY KEY COUNTRY, 2018–2023

FIGURE 29 LIST OF AMPHOTERIC SURFACTANT PATENTS

FIGURE 30 TOP PATENT OWNERS IN LAST 10 YEARS

FIGURE 31 LEGAL STATUS OF PATENTS

FIGURE 32 MAXIMUM PATENTS FILED BY COMPANIES IN CHINA

FIGURE 33 IMPACT OF AI/GEN AI ON AMPHOTERIC SURFACTANTS MARKET

FIGURE 34 BETAINES TO LEAD AMPHOTERIC SURFACTANTS MARKET DURING FORECAST PERIOD

FIGURE 35 PERSONAL CARE TO BE LARGEST APPLICATION OF AMPHOTERIC SURFACTANTS MARKET DURING FORECAST PERIOD

FIGURE 36 ASIA PACIFIC TO BE FASTEST-GROWING REGION FOR AMPHOTERIC SURFACTANTS DURING FORECAST PERIOD

FIGURE 37 ASIA PACIFIC: AMPHOTERIC SURFACTANTS MARKET SNAPSHOT

FIGURE 38 EUROPE: AMPHOTERIC SURFACTANTS MARKET SNAPSHOT

FIGURE 39 NORTH AMERICA: AMPHOTERIC SURFACTANTS MARKET SNAPSHOT

FIGURE 40 MARKET SHARE ANALYSIS OF TOP FIVE PLAYERS, 2023

FIGURE 41 REVENUE ANALYSIS OF KEY COMPANIES IN LAST FIVE YEARS

FIGURE 42 AMPHOTERIC SURFACTANTS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

FIGURE 43 AMPHOTERIC SURFACTANTS MARKET: COMPANY FOOTPRINT

FIGURE 44 AMPHOTERIC SURFACTANTS MARKET: COMPANY EVALUATION MATRIX (START-UPS/SMES), 2023

FIGURE 45 BRAND/PRODUCT COMPARISON

FIGURE 46 EV/EBITDA OF KEY MANUFACTURERS OF AMPHOTERIC SURFACTANTS

FIGURE 47 ENTERPRISE VALUATION (EV) OF KEY PLAYERS IN AMPHOTERIC SURFACTANTS MARKET

FIGURE 48 EVONIK INDUSTRIES AG: COMPANY SNAPSHOT

FIGURE 49 CLARIANT AG: COMPANY SNAPSHOT

FIGURE 50 CRODA INTERNATIONAL PLC: COMPANY SNAPSHOT

FIGURE 51 BASF SE: COMPANY SNAPSHOT

FIGURE 52 STEPAN COMPANY: COMPANY SNAPSHOT

FIGURE 53 ADEKA CORPORATION: COMPANY SNAPSHOT

Thomas

Apr, 2014

Natural betaine market trend and forecast for next five year.

Steve

Mar, 2015

Agrochemical application of surfactants, agrochemicals in general, surfactants in general, adjuvants, etc.

Sandra

May, 2015

Information on Global and European Amphoteric and non-ionic Surfactant.