Flexible Endoscopes Market Size, Growth, Share & Trends Analysis

Request Customisation

Request CustomisationFlexible Endoscopes Market by Type (Colonoscope, Laryngoscope, Bronchoscope, Other Types), Application (Laparoscopy, Mediastinoscopy, Obstetrics, Arthroscopy, Cystoscopy, Mediastinoscopy), End User (Hospitals, ASCs, Clinics), and Region � Global Forecast to 2030

OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

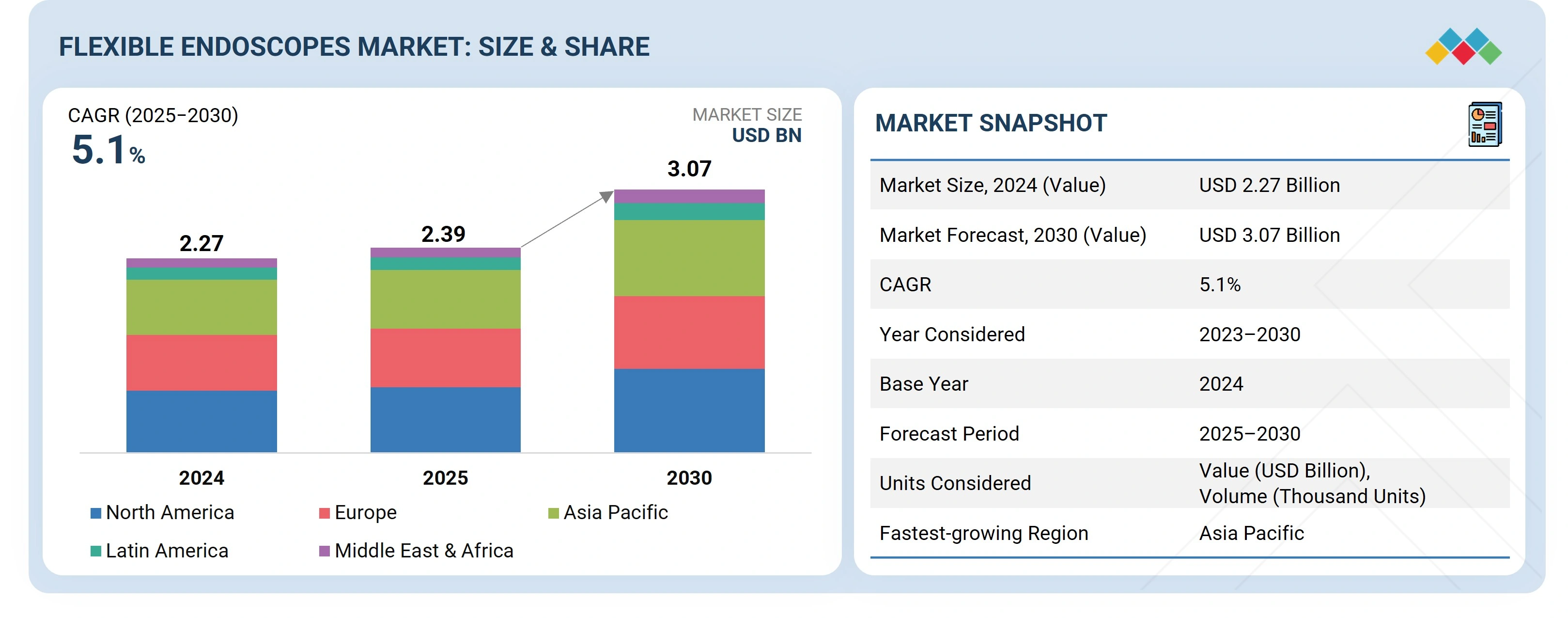

The flexible endoscopes market is projected to reach USD 3.07 billion by 2030 from USD 2.39 billion in 2025, at a CAGR of 5.1% during the forecast period. The growth of the flexible endoscopes market is driven by the rising demand for endoscopic procedures to diagnose and manage target conditions such as colorectal cancer and inflammatory bowel diseases. This demand is fueled by increasing disease prevalence and the need for early, minimally invasive interventions.

KEY TAKEAWAYS

-

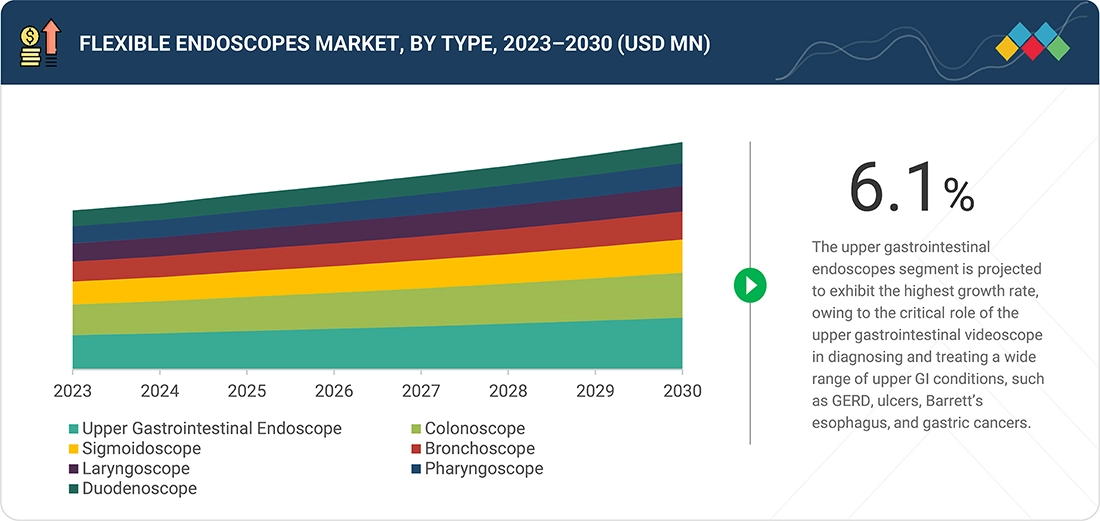

By TypeBased on type, the flexible endoscopes market is segmented into upper gastrointestinal endoscopes, colonoscopes, bronchoscopes, sigmoidoscopes, laryngoscopes, pharyngoscopes, duodenoscopes, nasopharyngoscopes, rhinoscopes, and other flexible endoscopes. Among these, in 2024, the upper gastrointestinal endoscopes segment accounted for the largest market share, owing to their critical role in diagnosing and treating a wide range of upper GI conditions such as GERD, ulcers, Barrett’s esophagus, and gastric cancers.

-

By ApplicationBased on applications, the flexible endoscopes market is segmented into gastrointestinal endoscopy, bronchoscopy, ENT endoscopy, urology endoscopy (cystoscopy), laparoscopy, obstetrics/gynecology endoscopy, arthroscopy, mediastinoscopy, and other applications. Among these, in 2024, the gastrointestinal endoscopy segment accounted for the highest share in the market. This is due to the rising prevalence of digestive disorders and the increasing clinical need for early, accurate, and minimally invasive diagnostic and therapeutic interventions.

-

By End UserBased on end users, the flexible endoscopes market is segmented into hospitals, ambulatory surgical centers, clinics, and others (diagnostic centers, mobile endoscopy facilities, and office-based endoscopy service providers). In 2024, the hospitals segment accounted for the largest market share, owing to the high patient inflow for diagnostic and therapeutic procedures, which demand advanced infrastructure and skilled medical professionals.

-

By RegionBased on region, the flexible endoscopes market is bifurcated into North America, Europe, Asia Pacific, Latin America, and the Middle east & Africa. Among these, during the forecast period, Asia Pacific is the fastest-growing regional market for flexible endoscopes. This is due to rapid healthcare infrastructure development, a large patient population, and increasing government focus on enhancing medical services.

-

Competitive LandscapeThe major market players have adopted both organic and inorganic strategies, including partnerships, collaborations, and approvals. In January 2024, Olympus Corporation (Japan) acquired Taewoong Medical Co., Ltd., a Korean manufacturer of medical devices. This acquisition helped Olympus strengthen its GI Endo Therapy product portfolio capabilities, contribute to improving patient outcomes through comprehensive solutions, and elevate the standard of care.

The flexible endoscopes market is driven by the rising need for endoscopy in diagnosing and treating critical diseases, increasing investments and grants from governments and organizations, and the growing prevalence of conditions such as inflammatory bowel disease and colorectal cancer. Additionally, hospitals are expanding their endoscopic capabilities, fueled by the increasing demand for minimally invasive procedures and ongoing technological advancements.

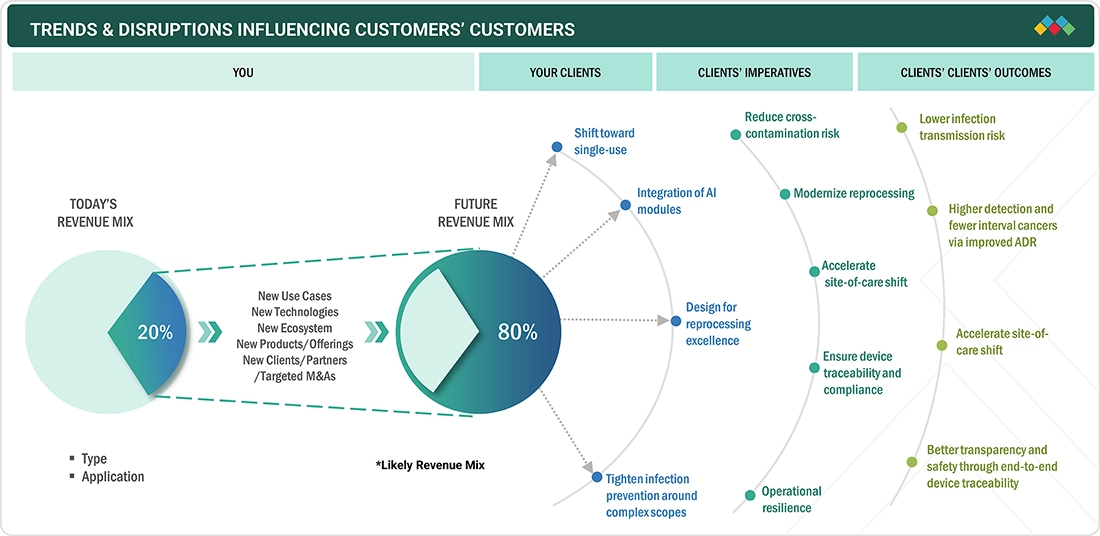

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The flexible endoscopes market is experiencing notable disruptions driven by global economic and regulatory pressures. Rising tariffs, supply chain instability, and stricter compliance requirements are increasing operational complexity and costs for customers. At the same time, evolving trends such as the shift toward AI-integrated imaging, growing demand for single-use scopes to reduce infection risks, and mounting pressure from healthcare providers to lower procedural costs are reshaping procurement decisions. Global competition and localization strategies are influencing pricing dynamics, while digital transformation and sustainability initiatives are altering R&D priorities. These disruptions and trends collectively push customers to seek solutions that balance innovation, affordability, and efficiency, ensuring high-quality patient care while optimizing hospital budgets and maintaining regulatory alignment.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Level

-

Rise in requirement for endoscopy to diagnose and treat target diseases

-

Rise in preference for minimally invasive surgeries

Level

-

High overhead costs of endoscopy procedures with limited reimbursement in emerging economies

-

Greater risk of viral infections during endoscopic procedures

Level

-

Rapidly developing healthcare sector in emerging economies

Level

-

Increase in number of product recalls

-

Lack of proper sterilization and reprocessing

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Rise in requirement for endoscopy to diagnose and treat target diseases

The rising requirement for endoscopy to diagnose and treat target diseases is a significant driver of the flexible endoscopes market, primarily due to the increasing preference for minimally invasive procedures. Endoscopic surgeries, performed through small incisions using flexible tubes and high-definition video cameras, offer numerous advantages over conventional open surgeries, including reduced pain, minimal hospital stays, quicker recovery, and lower risk of complications. These benefits translate into greater cost-efficiency, improved patient outcomes, and higher procedural volumes, prompting widespread adoption across various medical specialties. Flexible endoscopes are increasingly being used in the diagnosis and treatment of a wide range of critical conditions, such as cancer, orthopedic issues, gastrointestinal disorders, and neurological diseases. Their ability to provide real-time visualization, enable targeted biopsies, and support therapeutic interventions makes them indispensable tools in modern clinical practice. The growing burden of chronic diseases further accentuates this demand; for instance, the American Cancer Society projects over 2 million new cancer cases and 611,720 deaths in the US in 2024 alone. As healthcare providers focus on early diagnosis, better patient management, and enhanced surgical precision, the demand for flexible endoscopy solutions is set to accelerate, positioning them as a core element in future-ready healthcare delivery models.

Restraint: Greater risk of viral infections during endoscopic procedures

The increased risk of viral infections during endoscopic procedures is a critical restraint impacting the growth of the flexible endoscopes market. Endoscopy involves close physical interaction between patients and healthcare professionals, creating multiple avenues for infection transmission—through direct contact, respiratory droplets, or exposure to infected aerosols and contaminated instruments. Procedures such as gastroscopy, colonoscopy, and endoscopic retrograde cholangiopancreatography often require endoscopists to work in close proximity to the gastrointestinal tract, which may carry a high microbial load, including potentially transmissible viruses. Moreover, the risk is further elevated due to potential lapses in the sterilization of reusable endoscopic equipment and accessories. This increases concerns among healthcare professionals and institutions regarding occupational exposure and patient safety. As a result, some facilities may limit procedure volumes or delay elective endoscopies, thereby restricting the overall utilization of flexible endoscopes. Additionally, stringent infection control protocols and the need for advanced disinfection technologies increase operational complexity and costs for healthcare providers. These factors collectively act as a restraining factor to the widespread and routine adoption of flexible endoscopic procedures, particularly in resource-constrained settings, thereby restraining market growth.

Opportunity: Increase in adoption of single-use flexible endoscopes

The increasing adoption of single-use flexible endoscopes presents a significant opportunity for the growth of the flexible endoscopes market. These disposable devices are gaining traction due to their potential to eliminate the risk of cross-contamination and infection transmission, which remains a persistent concern with reusable endoscopes. Single-use endoscopes reduce the need for complex and costly reprocessing, sterilization, and storage protocols, offering a streamlined workflow and enhancing procedural efficiency. Hospitals and outpatient facilities are increasingly adopting these devices to ensure patient safety, improve turnaround time between procedures, and lower the risk of nosocomial infections. Additionally, advancements in material sciences and imaging technologies have improved the performance and cost-effectiveness of disposable endoscopes, making them viable alternatives for both routine and specialized procedures. Regulatory bodies and infection control committees are also showing strong support for single-use endoscopes, particularly in high-risk or immunocompromised patient populations. As healthcare systems shift toward value-based care and operational efficiency, the demand for disposable flexible endoscopes is expected to grow rapidly. This shift is also attracting the attention of major MedTech companies and new entrants, further intensifying innovation and expanding product portfolios. Consequently, the rising preference for single-use devices is opening new revenue streams and accelerating market expansion globally.

Challenge: Shortage of trained physicians and skilled endoscopists

The shortage of trained physicians and skilled endoscopists poses a significant challenge to the growth of the flexible endoscopes market. Endoscopic procedures require a high degree of technical expertise, precision, and clinical experience to ensure accurate diagnosis and effective treatment. However, many healthcare systems, especially in developing and underserved regions, face a substantial gap in the availability of qualified professionals capable of performing complex endoscopic interventions. This shortage limits the volume of procedures that can be safely conducted, thereby restricting the utilization of flexible endoscopes. Inadequate access to standardized training programs, limited exposure to advanced endoscopic techniques, and high costs associated with skill development further exacerbate the problem. Even in developed markets, growing patient volumes and the increasing complexity of cases are placing added pressure on a relatively limited workforce. This imbalance often leads to procedural delays, extended patient wait times, and suboptimal outcomes. Hospitals and clinics may hesitate to invest in new endoscopic technologies if they lack the personnel to operate them effectively. Consequently, the shortage of skilled endoscopy professionals acts as a bottleneck, hindering the broader adoption of flexible endoscopes and challenging the market’s ability to scale in response to rising global demand.

Flexible Endoscopes Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Offers a wide range of flexible endoscopes for gastrointestinal, urology, pulmonology, ENT, and gynecology applications | Integrated with advanced imaging, narrow-band imaging (NBI), and ergonomic designs to support minimally invasive procedures | Provides superior visualization and diagnostic accuracy, reduces patient discomfort during procedures, supports early disease detection, and enhances clinical workflow efficiency across diverse therapeutic areas |

|

Supplies high-performance flexible endoscopes for ENT, gastroenterology, and bronchoscopy, with modular systems and reusable components | Offers advanced video endoscopes with compatibility across multiple platforms. | Delivers consistent image quality, lowers operating costs through reusable solutions, ensures adaptability across specialties, and supports long-term hospital and outpatient use |

|

Focuses on flexible endoscopes for gastroenterology, pulmonology, and ENT, with advanced HD imaging, i-scan digital image enhancement, and therapeutic endoscopes for interventional procedures. | Improves diagnostic confidence with enhanced imaging, enables advanced therapeutic interventions, supports patient safety through infection prevention designs, and enhances physician comfort with ergonomic features |

|

Develops flexible endoscopes with advanced CMOS imaging, multi-light spectrum technology (Linked Color Imaging, Blue Light Imaging), and wide-field visualization for GI and respiratory care | Enhances mucosal visualization, facilitates early cancer detection, improves procedural outcomes, reduces complications, and offers innovative lightweight designs that improve ease of handling |

|

Provides flexible endoscopes and endoscopic solutions for gastroenterology and pulmonology, particularly for therapeutic procedures such as ERCP, EUS, and interventional bronchoscopy | Enables minimally invasive therapeutic procedures, reduces procedure time, expands clinical treatment options, and enhances patient outcomes through reliable device integration and innovation |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The flexible endoscopes business ecosystem comprises medical device manufacturers, component suppliers, healthcare providers, regulatory bodies, and research institutions. Manufacturers collaborate with OEMs and technology partners for innovations in optics, sensor integration, and AI-enabled diagnostics. Hospitals, ambulatory surgical centers, and specialty clinics serve as primary end users, driving demand through increasing adoption of minimally invasive procedures. Regulatory agencies such as the FDA and EMA ensure product safety and compliance, influencing product design and commercialization timelines. Strategic partnerships, R&D investments, and government healthcare funding further support market expansion. Additionally, medical training centers and professional associations play a key role in physician education, accelerating clinical adoption and strengthening the overall ecosystem.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Flexible Endoscopes Market, by Type

The upper gastrointestinal endoscope segment accounted for the largest market share in 2024. The upper gastrointestinal endoscopes segment is further divided into upper gastrointestinal videoscope and upper gastrointestinal fiberscope. Among these, the upper gastrointestinal videoscope segment accounted for a significant market share in 2024, owing to the critical role of the upper gastrointestinal videoscope in diagnosing and treating a wide range of upper GI conditions, such as GERD, ulcers, Barrett’s esophagus, and gastric cancers. These devices utilize advanced video chip technology that delivers high-resolution, real-time imaging, enabling accurate diagnosis and guided therapeutic interventions.

Flexible Endoscopes Market, by Application

The gastrointestinal endoscopy segment is projected to be the fastest-growing segment in the flexible endoscopes market, driven by the rising prevalence of digestive disorders and the increasing clinical need for early, accurate, and minimally invasive diagnostic and therapeutic interventions. With approximately 23.5 million GI endoscopies performed in 2022, as reported by the American Gastroenterological Association, the demand for flexible endoscopes in GI applications has surged significantly. These procedures are crucial for diagnosing and managing a wide range of gastrointestinal conditions, including ulcers, gastrointestinal bleeding, GERD, Crohn’s disease, and colorectal cancer. The growing number of emergency department visits—8.8 million in 2022—for digestive system diseases underscores the clinical urgency for GI-focused endoscopic equipment.

Flexible Endoscopes Market, by End User

Ambulatory Surgery Centers (ASCs) are the fastest-growing packaging segment in the flexible endoscopes market, driven by the growing role of ASCs in delivering cost-effective, efficient, and high-quality outpatient care. ASCs are increasingly preferred by patients and healthcare providers for performing diagnostic and therapeutic endoscopic procedures, such as colonoscopy, bronchoscopy, and upper GI endoscopy, as they offer reduced procedural costs, shorter wait times, faster recovery, and lower infection risks compared to hospitals. The flexibility of scheduling and lower overhead costs make ASCs attractive to both patients and physicians, especially in urban and semi-urban regions where patient throughput is high. Additionally, reimbursement models are increasingly favoring outpatient settings, encouraging healthcare systems to shift low-risk procedures to ASCs.

REGION

Asia Pacific to be fastest-growing region in flexible endoscopes market during forecast period

The Asia Pacific is projected to grow at the highest CAGR globally during the forecast period. This is primarily due to the healthcare infrastructure development, increasing healthcare expenditure, and rising adoption of minimally invasive surgeries across populous nations such as China and India. These countries are investing heavily to enhance diagnostic and surgical capabilities, particularly to manage the rising cases of chronic diseases. Japan’s well-established healthcare system with universal insurance coverage ensures wide accessibility to advanced endoscopic procedures. Increasing medical tourism, favorable government initiatives, and the rising adoption of minimally invasive technologies are accelerating market penetration, making Asia Pacific a high-growth region in the global flexible endoscopes market.

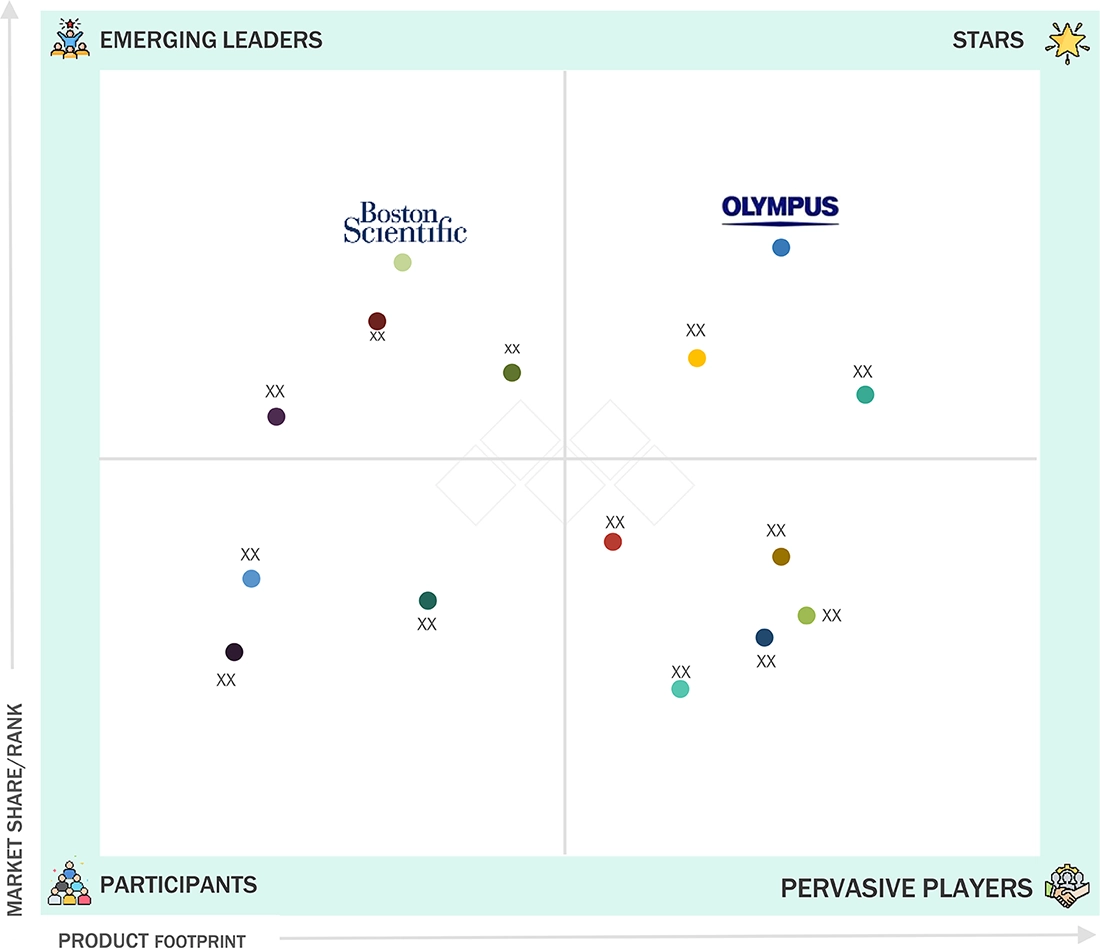

Flexible Endoscopes Market: COMPANY EVALUATION MATRIX

In the flexible endoscopes market matrix, Olympus Corporation (Japan) (Star) leads with scale, extensive distribution, and a broad endoscope portfolio. Boston Scientific Corporation (US) (Emerging Leader) is gaining momentum with innovative flexible endoscopes. FUJIFILM Corporation (Japan) and HOYA Corporation (Japan) stand out by offering advanced flexible endoscopes.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size, 2024 (Value) | USD 2.27 Billion |

| Market Forecast, 2030 (Value) | USD 3.07 Billion |

| Growth Rate (2025–2030) | CAGR of 5.1% from 2025 to 2030 |

| Years Considered | 2023–2030 |

| Base Year | 2024 |

| Forecast Period | 2025–2030 |

| Unit Considered | Value (USD Billion/Billion); Volume (Thousand Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, Latin America, and the Middle East & Africa |

WHAT IS IN IT FOR YOU: Flexible Endoscopes Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Product Analysis | Comparison of top flexible endoscopes: gastrointestinal endoscopes, colonoscopes, sigmoidoscopes, bronchoscopes, laryngoscopes, pharyngoscopes, duodenoscopes, nasopharyngoscopes, rhinoscopes, and other flexible endoscopes |

|

| Company Information |

|

Insights on revenue shifts toward emerging therapeutic applications and device innovations |

| Geographic Analysis |

|

Country-level demand mapping for new product launches and localization strategy planning |

RECENT DEVELOPMENTS

- May 2025 : Olympus Corporation (Japan) announced FDA 510 (k) clearance for its EZ1500 series endoscopes, which incorporate Extended Depth of Field (EDOF) technology to enhance visualization and diagnostic precision.

- January 2025 : KARL STORZ SE & Co. KG (Germany) announced the strategic acquisition of its long-standing Swiss distributor, ANKLIN, to strengthen its direct sales presence in Switzerland. This move enhanced customer proximity and supported its tailored product and service delivery in the MedTech sector.

- January 2024 : Olympus Corporation (Japan) acquired the Taewoong Medical Co., Ltd., a Korea-based manufacturer of medical devices. This acquisition helped Olympus strengthen its GI Endo Therapy product portfolio capabilities, contribute to improving patient outcomes through comprehensive solutions, and elevate the standard of care.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Methodology

The research study involved major activities in estimating the current size of the flexible endoscopes market. Exhaustive secondary research was done to collect information on the flexible endoscope industry. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain using primary research. Different approaches, such as top-down and bottom-up, were employed to estimate the total market size. After that, the market breakup and data triangulation procedures were used to estimate the market size of the segments and subsegments of the flexible endoscopes market.

Secondary Research

The secondary research process involved the widespread use of secondary sources, directories, databases (Bloomberg Businessweek, Factiva, and D&B Hoovers), white papers, annual reports, investor presentations, SEC filings of companies and publications from government sources, such as National Institutes of Health (NIH), US FDA, US Census Bureau, World Health Organization (WHO), International Trade Administration (ITA), Global Burden of Disease Study, and Centers for Medicare and Medicaid Services (CMS). These sources were referred to, to identify and collect information on the global flexible endoscopes market study. They were also used to obtain important information about the key players and market classification & segmentation according to industry trends and key developments related to market and technology perspectives. A database of the key industry leaders was also prepared using secondary research.

Primary Research

In the primary research process, various sources from the supply and demand sides were interviewed to obtain qualitative and quantitative information for this report. Primary sources from the supply side included industry experts, such as CEOs, vice presidents; marketing and sales directors; technology & innovation directors; and related key executives from various key companies and organizations in the flexible endoscopes market. Primary sources from the demand side included ambulatory surgical centers (ASCs), hospitals, clinics, and other end users. The research was conducted to validate the market segmentation, identify key players, and gather insights on key industry trends & key market dynamics.

A breakdown of the primary respondents involved in the research process is provided below:

C-level Primaries include CEOs, CFOs, COOs, and VPs.

Others include Sales Managers, Marketing Managers, Business Development Managers, Product Managers, Distributors, and Suppliers.

Companies are classified into tiers based on their total revenue. These tiers are as follows:

Tier 1 = > USD 10.00 billion, tier 2 = USD 1.00 billion to USD 10.00 billion, and tier 3 = < USD 1.00 billion

Source: MarketsandMarkets Analysis

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

For global market value, annual revenue figures were calculated based on the revenue mapping of major product manufacturers and OEMs active in the global flexible endoscopes market. All major product manufacturers were identified at the international/country/regional levels. Revenue mapping for the respective business segments/sub-segments was done for the major players.

The global flexible endoscopes market was split into various segments and sub-segments by taking the following into consideration:

- List of major players operating in the product market at the regional and/or country level

- Product mapping of various flexible endoscope manufacturers at the regional and/or country level

- Mapping of annual revenue generated by listed major players in the flexible endoscopes market (or the nearest reported business unit/product category)

- Extrapolation of the revenue mapping of the listed major players to derive the global market value of the respective segments/subsegments

- Summation of the market value of all segments/subsegments to arrive at the global flexible endoscopes market

- The above data was consolidated and added with detailed inputs and analysis from MarketsandMarkets and presented in this report.

Market Size Estimation (Bottom-up & Top-down Approaches)

Data Triangulation

After arriving at the overall size of the global flexible endoscopes market through the methodology mentioned above, the market was split into several segments and subsegments. Where applicable, the data triangulation and market breakdown procedures were employed to complete the overall market engineering process and arrive at the exact market value data for the key segments and subsegments. The extrapolated market data was triangulated by studying various macroindicators and regional trends from both demand- and supply-side participants.

Market Definition

Flexible endoscopes are medical devices designed with a bendable, tube-like structure that enables visual examination and therapeutic intervention within internal organs and cavities, particularly in hard-to-reach areas. These devices, integrated with high-resolution imaging, illumination, and accessory channels, support minimally invasive procedures across gastrointestinal, respiratory, urology, and other applications. Their flexibility, precision, and patient-friendly design make diagnostic accuracy and procedural efficiency essential in modern healthcare.

Stakeholders

- Manufacturers of endoscopes and related devices

- Suppliers and distributors of endoscopy devices

- Hospitals, diagnostic centers, and medical colleges

- Independent surgeons and private physicians

- Ambulatory surgery centers (ASCs)

- Teaching hospitals and academic medical centers

- Government bodies/Municipal corporations

- Business research and consulting service providers

- Venture capitalists

Report Objectives

- To define, describe, segment, and forecast the flexible endoscopes market by type, application, end user, and region

- To provide detailed information about the factors (Drivers, restraints, opportunities, and challenges) influencing market growth

- To analyze micromarkets1 with respect to individual growth trends, prospects, and contributions to the overall flexible endoscopes market

- To analyze market opportunities for stakeholders and provide details of the competitive landscape for key players

- To forecast the size of the flexible endoscopes market across five main regions (along with their respective key countries), namely North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa

- To profile the key players in the flexible endoscopes market and comprehensively analyze their core competencies and market share

- To track and analyze competitive developments, such as acquisitions, product launches, expansions, collaborations, agreements, partnerships, and R&D activities of leading players in the flexible endoscopes market

- To benchmark players within the flexible endoscopes market using the Competitive Leadership Mapping framework, which analyzes market players on various parameters within the broad categories of business strategy, market share, and product offerings

Key Questions Addressed by the Report

Which are the top industry players in the global flexible endoscopes market?

The prominent players in this market are Olympus Corporation (Japan), Karl Storz SE & CO. Kg (Germany), Boston (US), FUJIFILM Corporation (Japan), HOYA Corporation (Japan), Ambu A/S (Denmark), EndoMed Systems GmbH (Germany), Richard Wolf GmbH (Germany), and Stryker (US).

What are some of the major drivers of the flexible endoscopes market?

Major drivers of the flexible endoscopes market are the rising incidence of inflammatory bowel disease and colorectal cancer and increasing preference for minimally invasive surgeries.

Which end users have been included in the global flexible endoscopes market?

End users covered in the study include hospitals, ambulatory surgery centers, clinics, and other end users.

Which type segment accounted for the largest share of the flexible endoscopes market in 2024?

The upper gastrointestinal endoscopes segment accounted for the largest share of the flexible endoscopes market in 2024.

Which region is projected to dominate the flexible endoscopes market during the forecast period?

Asia Pacific is projected to dominate the flexible endoscopes market during the forecast period.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This ReportPersonalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Flexible Endoscopes Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

JAYANT RAJPUROHIT

Director of Market Insights, Data and Analytics

SFI Health,

Leading Pharmaceutical Companywww.sfihealth.com/

We at SFI Health approached MarketsandMarkets for an Opportunity Assessment on "Incidence and Prevalence of Focus Indications" as we wanted to know the most attractive HCPs like Physician, Functional MD, Naturopath and Pharmacist. The project was critical for us to ensure our focus on the right target which would enable sustainable growth and profitability for SFI Health. The business insights provided exceeded our expectations and we were extremely impressed. The team at MarketsandMarkets is highly professional and detail oriented and very well understood our business needs. MarketsandMarkets offers a unique combination of expertise and dedicated engagement model. We identified 2 new products to be launched in coming months, based on the research findings provided by MarketsandMarkets. We are happy with the services and would strongly recommend MarketsandMarkets to my peers in the industry.

BEATRIZ DE LA CALLE

Head of Commercial Analytics

Qualicaps,

Leading Pharmaceutical Companywww.qualicaps.com/

We partnered with MarketsandMarkets for an assessment study on hard empty capsules. The team was extremely professional in understanding our business requirements and we received timely responses to all our queries. The market intelligence and the recommendations has met our business requirements. We were extremely impressed to see the final study results; it really exceeded our expectations. The market intelligence offered by MarketsandMarkets, and clarity on next steps will help us achieve our business objective for the Year 2021. We are happy with the services and would strongly recommend MarketsandMarkets to my peers in the industry.

Bob Williams,

Senior Director Business Development & Innovation

Bracco Diagnostics Inc.,

Italian Multinational in life sciences sector and a World Leader in imaging diagnosticsimaging.bracco.com/us-en

We were pleased with targeted insights that MarketsandMarkets identified from a custom study on the 'Radiation Dose Management Solutions Market'. Your team identified and characterized the market participants as well as underlying trends accurately. This study was useful to Bracco in formulating business strategies for our dose monitoring product lines and we thank MarketsandMarkets for the job well done.

Cody Coonradt,

Market Development and Strategy Manager

3M Health Information Systems,

Leader in Health care Coding, Payment & Analytics Solutions.www.3m.com/3M/en_US/health-information-systems-us

The value for our organization comes from three things: depth of research, specificity of segments and being easy to work with. As important as the first two are, the third can't be underestimated. MarketsandMarkets, maybe more than any other research vendor, wants to know what is top of mind for our team and what big questions we are grappling to answer.

Their customer first approach and high value engagement model, have given us great analysis and excellent value for money

Growth opportunities and latent adjacency in Flexible Endoscopes Market