TABLE OF CONTENTS

1 INTRODUCTION (Page No. - 23)

1.1 STUDY OBJECTIVES

1.2 COMPETITIVE INTELLIGENCE

1.3 MARKET DEFINITION

1.3.1 INCLUSIONS AND EXCLUSIONS

1.4 MARKET SCOPE

1.4.1 REGIONAL SCOPE

1.4.2 YEARS CONSIDERED

1.4.3 CURRENCY CONSIDERED

1.5 LIMITATIONS

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY (Page No. - 28)

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Breakdown of primary interviews

2.2 MATRIX CONSIDERED FOR DEMAND-SIDE ANALYSIS

2.3 MARKET SIZE ESTIMATION

2.3.1 BOTTOM-UP APPROACH

2.3.2 TOP-DOWN APPROACH

2.3.2.1 Calculations for supply-side analysis

2.4 GROWTH RATE ASSUMPTIONS/GROWTH FORECAST

2.5 DATA TRIANGULATION

2.6 IMPACT OF RECESSION

2.7 KEY ASSUMPTIONS WHILE CALCULATING DEMAND- SIDE MARKET SIZE

2.8 RESEARCH LIMITATIONS

2.9 RISK ANALYSIS

3 EXECUTIVE SUMMARY (Page No. - 38)

4 PREMIUM INSIGHTS (Page No. - 41)

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL BATTERIES MARKET

4.2 INDUSTRIAL BATTERIES MARKET, BY REGION

4.3 INDUSTRIAL BATTERIES MARKET, BY MAJOR COUNTRIES

5 MARKET OVERVIEW (Page No. - 43)

5.1 INTRODUCTION

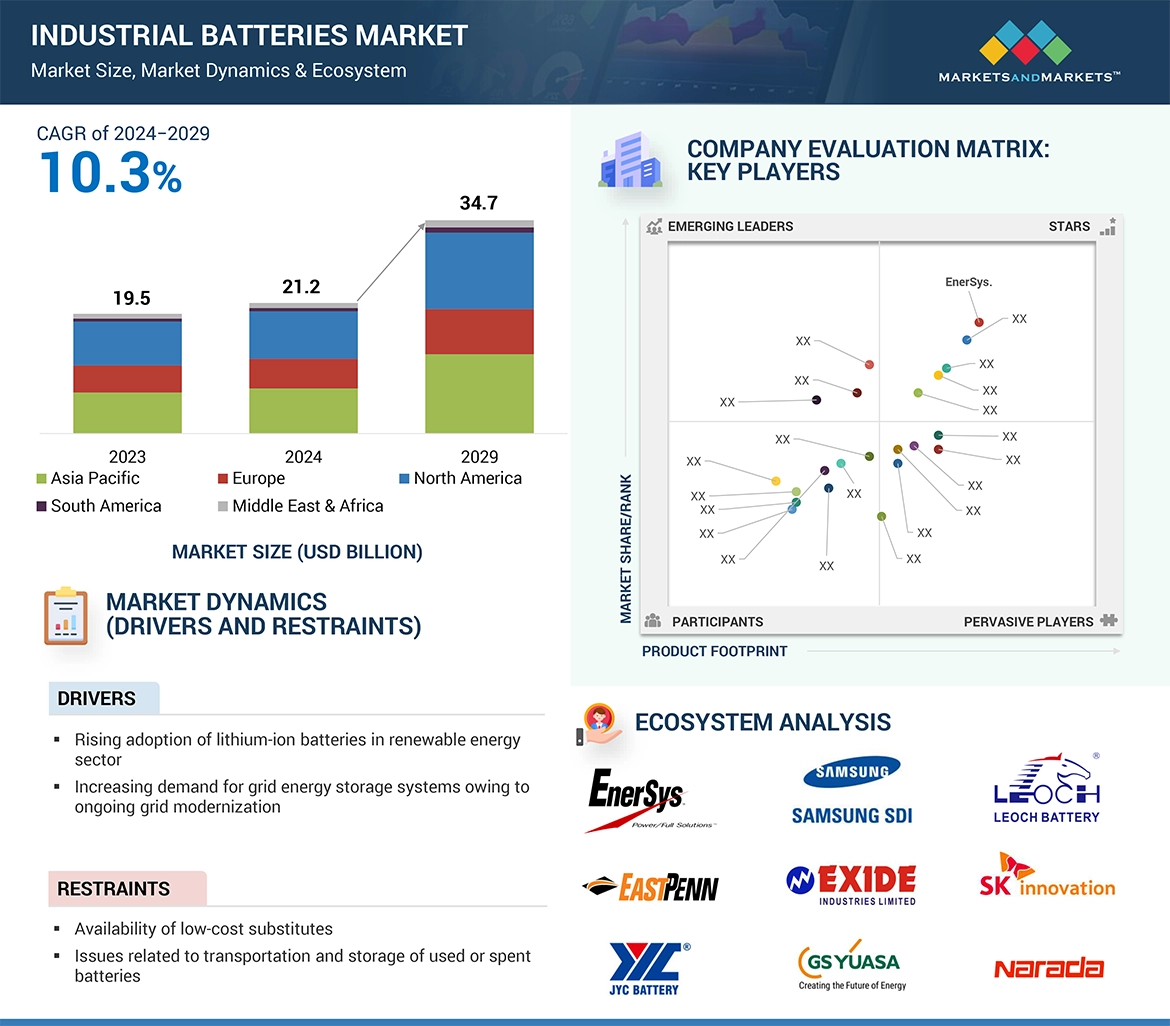

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising adoption of lithium-ion batteries in renewable energy sector

5.2.1.2 Increasing demand for grid energy storage systems owing to ongoing grid modernization

5.2.2 RESTRAINTS

5.2.2.1 Availability of low-cost substitutes

5.2.2.2 Issues related to transportation and storage of used or spent batteries

5.2.3 OPPORTUNITIES

5.2.3.1 Advancements in telecommunications sector

5.2.3.2 Increasing battery innovation initiatives by established players

5.2.4 CHALLENGES

5.2.4.1 Limited usage and overheating

5.3 PORTER’S FIVE FORCES ANALYSIS

5.3.1 BARGAINING POWER OF SUPPLIERS

5.3.2 BARGAINING POWER OF BUYERS

5.3.3 THREAT OF NEW ENTRANTS

5.3.4 THREAT OF SUBSTITUTES

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

6 INDUSTRY TRENDS (Page No. - 51)

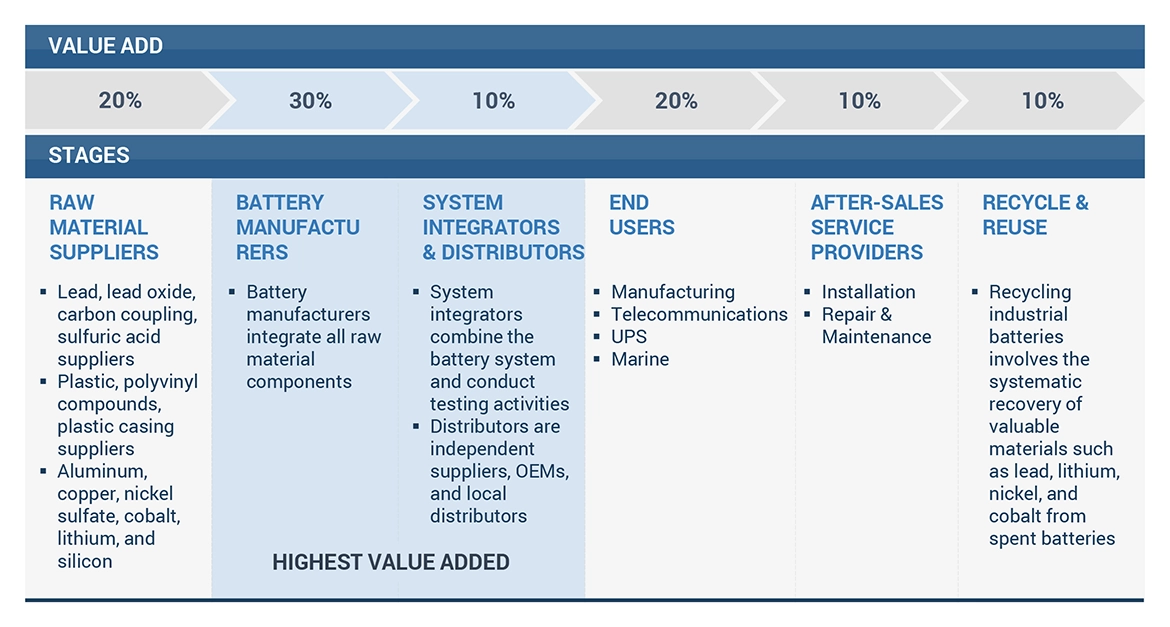

6.1 VALUE CHAIN ANALYSIS

6.2 ECOSYSTEM ANALYSIS

6.3 PRICING ANALYSIS

6.3.1 AVERAGE SELLING PRICE OF LITHIUM-ION BATTERIES, BY REGION

6.3.2 AVERAGE SELLING PRICE OF LITHIUM-ION BATTERIES, BY CHEMISTRY

6.4 TARIFF AND REGULATORY LANDSCAPE

6.4.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.5 KEY CONFERENCES AND EVENTS

6.6 KEY STAKEHOLDERS AND BUYING CRITERIA

6.6.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.6.2 BUYING CRITERIA

6.7 PATENT ANALYSIS

6.7.1 METHODOLOGY

6.7.2 MAJOR PATENTS

6.8 CASE STUDY ANALYSIS

6.8.1 GRID-CONNECTED LITHIUM-ION BATTERY ENERGY STORAGE SYSTEM BY NEXCHARGE AND TATA POWER DELHI DISTRIBUTION

6.8.2 DEPLOYMENT OF OFF-GRID BATTERY ENERGY STORAGE SYSTEMS FOR RENEWABLE ENERGY PROJECT

6.9 TECHNOLOGY ANALYSIS

6.9.1 KEY TECHNOLOGIES

6.9.1.1 Lithium metal battery

6.9.1.2 Sodium-sulfur batteries

6.9.1.3 Metal-air batteries

6.9.1.4 Liquid-metal batteries

6.9.2 ADJACENT TECHNOLOGIES

6.9.2.1 Modern off-grid technology

6.10 TRADE ANALYSIS

6.10.1 IMPORT DATA

6.10.2 EXPORT DATA

6.11 TRENDS/ DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.12 INVESTMENT AND FUNDING SCENARIO

7 INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE (Page No. - 68)

7.1 INTRODUCTION

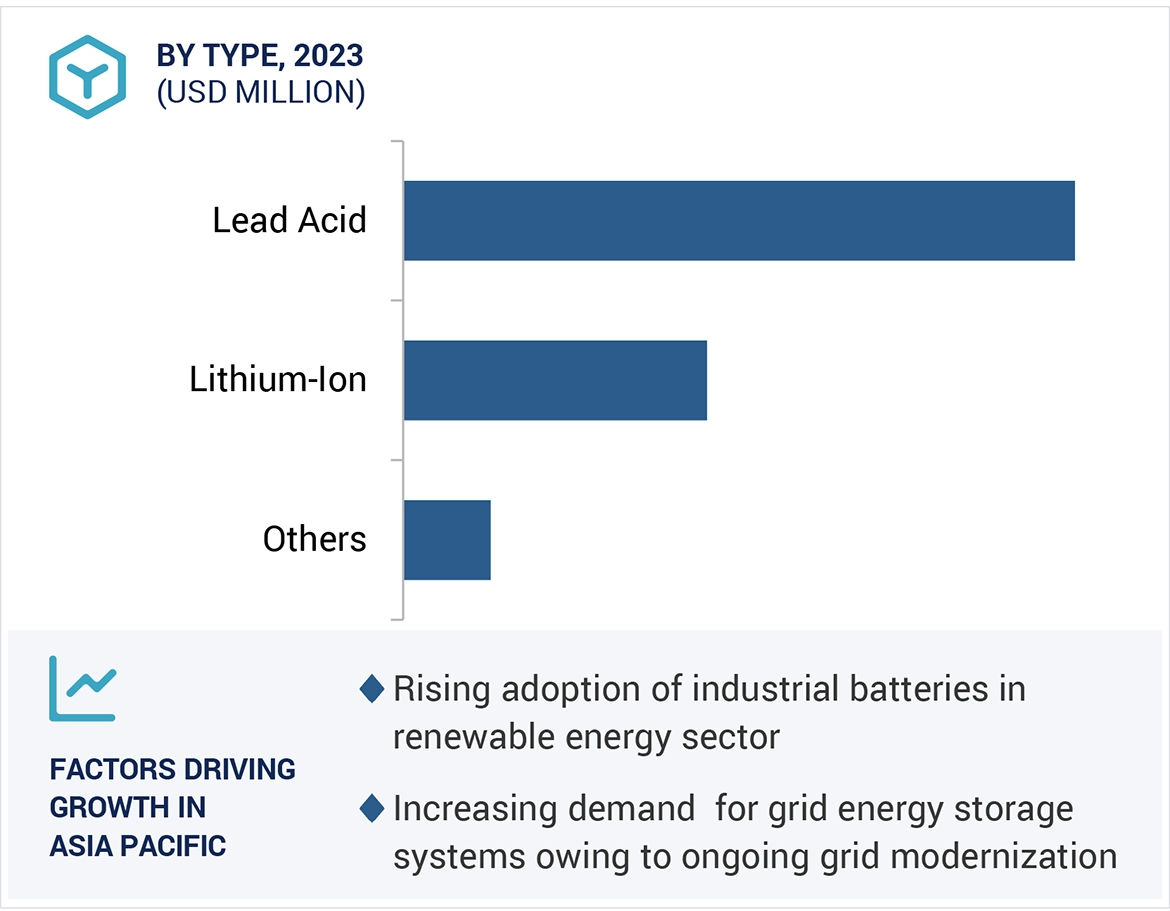

7.2 LEAD-ACID

7.2.1 INCREASING ADOPTION IN GRID ENERGY STORAGE TO DRIVE GROWTH

7.3 LITHIUM-ION

7.3.1 DECREASE IN PRICES TO DRIVE GROWTH

7.4 OTHERS

8 INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY (Page No. - 81)

8.1 INTRODUCTION

8.2 STATIONARY BATTERY

8.2.1 INCREASING GRID-LEVEL APPLICATIONS TO DRIVE GROWTH

8.2.2 TELECOMMUNICATIONS

8.2.3 UNINTERRUPTIBLE POWER SUPPLY

8.2.4 GRID LEVEL

8.3 MOTIVE BATTERY

8.3.1 EFFICIENT STORAGE OF ELECTRICITY FROM RENEWABLE ENERGY SOURCES TO DRIVE GROWTH

8.3.2 LOW-SPEED ELECTRIC VEHICLE

8.3.3 FLOOR SCRUBBER

8.3.4 MATERIAL HANDLING

8.3.5 MARINE

8.3.6 RECREATIONAL VEHICLE

9 INDUSTRIAL BATTERIES MARKET, BY REGION (Page No. - 89)

9.1 INTRODUCTION

9.2 NORTH AMERICA

9.2.1 US

9.2.1.1 Increasing demand for batteries in grid-level energy storage to drive growth

9.2.2 CANADA

9.2.2.1 Innovations in grid-connected solutions to drive growth

9.2.3 MEXICO

9.2.3.1 Expansion of domestic automotive sector to drive growth

9.3 ASIA PACIFIC

9.3.1 CHINA

9.3.1.1 Increasing production of electric vehicles to drive growth

9.3.2 JAPAN

9.3.2.1 Expansion of R&D resources by battery giants to drive growth

9.3.3 INDIA

9.3.3.1 Rising adoption of electric vehicles to drive growth

9.3.4 REST OF ASIA PACIFIC

9.4 EUROPE

9.4.1 GERMANY

9.4.1.1 Increasing expansion of residential energy storage sector to drive growth

9.4.2 UK

9.4.2.1 Investments in lithium-ion battery materials for electric vehicles to drive growth

9.4.3 FRANCE

9.4.3.1 Diversified electricity production goals to drive growth

9.4.4 REST OF EUROPE

9.5 MIDDLE EAST & AFRICA

9.5.1 GCC

9.5.1.1 Saudi Arabia

9.5.1.1.1 Government initiatives toward renewable energy sector to drive growth

9.5.1.2 UAE

9.5.1.2.1 Development of telecom & data communications sector to drive growth

9.5.2 SOUTH AFRICA

9.5.2.1 Rising demand for portable devices to drive growth

9.5.3 REST OF MIDDLE EAST & AFRICA

9.6 SOUTH AMERICA

9.6.1 BRAZIL

9.6.1.1 Rising demand for consumer and automotive batteries to drive growth

9.6.2 REST OF SOUTH AMERICA

10 COMPETITIVE LANDSCAPE (Page No. - 123)

10.1 INTRODUCTION

10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

10.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY MARKET PLAYERS

10.3 REVENUE ANALYSIS

10.4 MARKET SHARE ANALYSIS

10.4.1 MARKET RANKING ANALYSIS

10.4.1.1 EnerSys. (US)

10.4.1.2 GS Yuasa International Ltd. (Japan)

10.4.1.3 Leoch International Technology Limited Inc (China)

10.4.1.4 Exide Industries Ltd. (India)

10.4.1.5 C&D Technologies, Inc. (US)

10.5 BRAND/PRODUCT COMPARISON

10.5.1 DATASAFE XE BATTERIES

10.5.2 LCT-HP FLOODED BATTERY

10.5.3 NP SERIES

10.5.4 EXIDE POWERSAFE EHP

10.5.5 PU UPS SHORT-TIME BACKUP POWER SERIES

10.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

10.6.1 STARS

10.6.2 EMERGING LEADERS

10.6.3 PERVASIVE PLAYERS

10.6.4 PARTICIPANTS

10.6.5 COMPANY FOOTPRINT

10.7 COMPANY EVALUATION MATRIX: START-UP/SMES, 2023

10.7.1 PROGRESSIVE COMPANIES

10.7.2 RESPONSIVE COMPANIES

10.7.3 DYNAMIC COMPANIES

10.7.4 STARTING BLOCKS

10.7.5 COMPETITIVE BENCHMARKING

10.8 COMPANY VALUATION AND FINANCIAL METRICS

10.9 COMPETITIVE SCENARIOS AND TRENDS

10.9.1 PRODUCT LAUNCHES

10.9.2 DEALS

11 COMPANY PROFILES (Page No. - 142)

11.1 MAJOR PLAYERS

11.1.1 ENERSYS.

11.1.1.1 Business overview

11.1.1.2 Products offered

11.1.1.3 MnM view

11.1.1.3.1 Right to win

11.1.1.3.2 Strategic choices

11.1.1.3.3 Weaknesses and competitive threats

11.1.2 C&D TECHNOLOGIES, INC.

11.1.2.1 Business overview

11.1.2.2 Products offered

11.1.2.3 Recent developments

11.1.2.4 MnM view

11.1.2.4.1 Right to Win

11.1.2.4.2 Strategic choices

11.1.2.4.3 Weaknesses and competitive threats

11.1.3 GS YUASA INTERNATIONAL LTD.

11.1.3.1 Business overview

11.1.3.2 Products offered

11.1.3.3 MnM view

11.1.3.3.1 Right to Win

11.1.3.3.2 Strategic choices

11.1.3.3.3 Weaknesses and competitive threats

11.1.4 EXIDE INDUSTRIES LTD.

11.1.4.1 Business overview

11.1.4.2 Products offered

11.1.4.3 MnM view

11.1.4.3.1 Right to win

11.1.4.3.2 Strategic choices

11.1.4.3.3 Weaknesses and competitive threats

11.1.5 LEOCH INTERNATIONAL TECHNOLOGY LIMITED INC

11.1.5.1 Business overview

11.1.5.2 Products offered

11.1.5.3 Recent developments

11.1.5.4 MnM view

11.1.5.4.1 Right to Win

11.1.5.4.2 Strategic choices

11.1.5.4.3 Weaknesses and competitive threats

11.1.6 CROWN BATTERY

11.1.6.1 Business overview

11.1.6.2 Products offered

11.1.7 EAST PENN MANUFACTURING COMPANY

11.1.7.1 Business overview

11.1.7.2 Products offered

11.1.8 SAMSUNG SDI CO., LTD.

11.1.8.1 Business overview

11.1.8.2 Products offered

11.1.9 SK INNOVATION CO., LTD

11.1.9.1 Business overview

11.1.9.2 Products offered

11.1.10 NARADA POWER

11.1.10.1 Business overview

11.1.10.2 Products offered

11.1.10.3 Recent developments

11.1.11 VISION GROUP

11.1.12 LG CHEM

11.1.13 YUASA BATTERY (THAILAND) PUBLIC COMPANY LTD.

11.1.14 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED

11.1.15 HOPPECKE BATTERIEN GMBH & CO. KG

11.1.15.3.1 Others

11.1.15.3.2 Deals

11.1.16 THE SUNLIGHT GROUP

11.1.16.3.1 Product launches

11.1.16.3.2 Deals

11.1.17 TAB

11.1.17.3.1 Deals

11.1.18 RITAR INTERNATIONAL GROUP

11.1.19 U.S. BATTERY

11.1.19.1 Business overview

11.1.19.2 Products offered

11.1.19.3 Recent developments

11.1.19.3.1 Product launches

11.1.19.3.2 Deals

11.1.20 AMARA RAJA ENERGY & MOBILITY LIMITED

11.1.20.1 Business overview

11.1.20.2 Products offered

11.1.20.3 Recent developments

11.1.21 IPOWER BATTERIES

11.1.21.1 Business overview

11.1.21.2 Products offered

11.1.21.3 Recent developments

11.1.21.3.1 Product launches

11.1.21.3.2 Deals

11.1.22 JYC BATTERY MANUFACTURER CO., LTD

11.1.22.1 Business overview

11.1.22.2 Products offered

11.1.22.3 Recent developments

11.1.22.3.1 Product launches

11.2 OTHER PLAYERS

11.2.1 AMARON BATTERIES

11.2.2 SAFT GROUPE

11.2.2.1 Recent developments

11.2.3 ROLLS BATTERY

11.2.4 VICTRON ENERGY

11.2.5 NORTHVOLT AB

11.2.5.1 Recent developments

12 ADJACENT AND RELATED MARKETS (Page No. - 233)

12.1 INTRODUCTION

12.2 LIMITATIONS

12.3 INTERCONNECTED MARKETS

12.4 LITHIUM-ION BATTERY MARKET

12.4.1 MARKET DEFINITION

12.4.2 MARKET OVERVIEW

12.4.3 LITHIUM-ION BATTERY MARKET, BY VOLTAGE

12.4.3.1 Low voltage

12.4.3.2 Medium voltage

12.4.3.3 High voltage

13 APPENDIX (Page No. - 236)

13.1 DISCUSSION GUIDE

13.2 KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

13.3 CUSTOMIZATION OPTIONS

13.4 RELATED REPORTS

13.5 AUTHOR DETAILS

LIST OF TABLES (228 TABLES)

TABLE 1 INDUSTRIAL BATTERIES MARKET: INCLUSIONS AND EXCLUSIONS

TABLE 2 INDUSTRIAL BATTERIES MARKET SNAPSHOT: 2024 VS. 2029

TABLE 3 PORTER’S FIVE FORCES ANALYSIS

TABLE 4 ROLE OF COMPANIES IN ECOSYSTEM

TABLE 5 TARIFF DATA

TABLE 6 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 7 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 8 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 9 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 10 INDUSTRIAL BATTERIES MARKET: KEY CONFERENCES AND EVENTS, 2024−2025

TABLE 11 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USES (%)

TABLE 12 KEY BUYING CRITERIA FOR TOP END USES

TABLE 13 IMPORT DATA ON LITHIUM CELLS AND BATTERIES (USD BILLION), 2019−2022

TABLE 14 EXPORT DATA ON LITHIUM CELLS AND BATTERIES (USD BILLION), 2019−2022

TABLE 15 INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2019–2022 (USD MILLION)

TABLE 16 INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2023–2029 (USD MILLION)

TABLE 17 LEAD-ACID BATTERY MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 18 LEAD-ACID BATTERY MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 19 LEAD-ACID BATTERY MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 20 LEAD-ACID BATTERY MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 21 LEAD-ACID BATTERY MARKET IN STATIONARY BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 22 LEAD-ACID BATTERY MARKET IN STATIONARY BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 23 STATIONARY LEAD-ACID BATTERY MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 24 STATIONARY LEAD-ACID BATTERY MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 25 MOTIVE LEAD-ACID BATTERY MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 26 MOTIVE LEAD-ACID BATTERY MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 27 LITHIUM-ION BATTERY MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 28 LITHIUM-ION BATTERY MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 29 LITHIUM-ION BATTERY MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 30 LITHIUM-ION BATTERY MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 31 LITHIUM-ION BATTERY MARKET IN STATIONARY BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 32 LITHIUM-ION BATTERY MARKET IN STATIONARY BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 33 STATIONARY LITHIUM-ION BATTERY MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 34 STATIONARY LITHIUM-ION BATTERY MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 35 MOTIVE LITHIUM-ION BATTERY MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 36 MOTIVE LITHIUM-ION BATTERY MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 37 OTHER INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 38 OTHER INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 39 OTHER INDUSTRIAL BATTERIES MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 40 OTHER INDUSTRIAL BATTERIES MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 41 OTHER INDUSTRIAL BATTERIES MARKET IN STATIONARY BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 42 OTHER INDUSTRIAL BATTERIES MARKET IN STATIONARY BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 43 OTHER STATIONARY INDUSTRIAL BATTERIES MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 44 OTHER STATIONARY INDUSTRIAL BATTERIES MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 45 OTHER MOTIVE INDUSTRIAL BATTERIES MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 46 OTHER MOTIVE INDUSTRIAL BATTERIES MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 47 INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 48 INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 49 STATIONARY INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 50 STATIONARY INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 51 STATIONARY INDUSTRIAL BATTERIES MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 52 STATIONARY INDUSTRIAL BATTERIES MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 53 STATIONARY INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2019–2022 (USD MILLION)

TABLE 54 STATIONARY INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2023–2029 (USD MILLION)

TABLE 55 MOTIVE INDUSTRIAL BATTERIES MARKET, BY APPLICATION, 2019–2022 (USD MILLION)

TABLE 56 MOTIVE INDUSTRIAL BATTERIES MARKET, BY APPLICATION, 2023–2029 (USD MILLION)

TABLE 57 MOTIVE INDUSTRIAL BATTERIES MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 58 MOTIVE INDUSTRIAL BATTERIES MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 59 MOTIVE INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2019–2022 (USD MILLION)

TABLE 60 MOTIVE INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2023–2029 (USD MILLION)

TABLE 61 INDUSTRIAL BATTERIES MARKET, BY REGION, 2019–2022 (USD MILLION)

TABLE 62 INDUSTRIAL BATTERIES MARKET, BY REGION, 2023–2029 (USD MILLION)

TABLE 63 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2019–2022 (USD MILLION)

TABLE 64 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2023–2029 (USD MILLION)

TABLE 65 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 66 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 67 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 68 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 69 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 70 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 71 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2019–2022 (USD MILLION)

TABLE 72 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2023–2029 (USD MILLION)

TABLE 73 US: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 74 US: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 75 CANADA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 76 CANADA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 77 MEXICO: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 78 MEXICO: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 79 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2019–2022 (USD MILLION)

TABLE 80 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2023–2029 (USD MILLION)

TABLE 81 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 82 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 83 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 84 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 85 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 86 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 87 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2019–2022 (USD MILLION)

TABLE 88 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2023–2029 (USD MILLION)

TABLE 89 CHINA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 90 CHINA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 91 JAPAN: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 92 JAPAN: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 93 INDIA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 94 INDIA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 95 REST OF ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 96 REST OF ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 97 EUROPE: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2019–2022 (USD MILLION)

TABLE 98 EUROPE: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2023–2029 (USD MILLION)

TABLE 99 EUROPE: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 100 EUROPE: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 101 EUROPE: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 102 EUROPE: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 103 EUROPE: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 104 EUROPE: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 105 EUROPE: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2019–2022 (USD MILLION)

TABLE 106 EUROPE: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2023–2029 (USD MILLION)

TABLE 107 GERMANY: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 108 GERMANY: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 109 UK: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 110 UK: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 111 FRANCE: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 112 FRANCE: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 113 REST OF EUROPE: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 114 REST OF EUROPE: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 115 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2019–2022 (USD MILLION)

TABLE 116 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2023–2029 (USD MILLION)

TABLE 117 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 118 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 119 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 120 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 121 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 122 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 123 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2019–2022 (USD MILLION)

TABLE 124 MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2023–2029 (USD MILLION)

TABLE 125 SAUDI ARABIA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 126 SAUDI ARABIA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 127 UAE: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 128 UAE: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 129 SOUTH AFRICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 130 SOUTH AFRICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 131 REST OF MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 132 REST OF MIDDLE EAST & AFRICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 133 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2019–2022 (USD MILLION)

TABLE 134 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY COUNTRY, 2023–2029 (USD MILLION)

TABLE 135 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 136 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 137 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 138 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY MOTIVE BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 139 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 140 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY STATIONARY BATTERY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 141 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2019–2022 (USD MILLION)

TABLE 142 SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY BATTERY TYPE, 2023–2029 (USD MILLION)

TABLE 143 BRAZIL: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 144 BRAZIL: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 145 REST OF SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2019–2022 (USD MILLION)

TABLE 146 REST OF SOUTH AMERICA: INDUSTRIAL BATTERIES MARKET, BY END-USE INDUSTRY, 2023–2029 (USD MILLION)

TABLE 147 DEGREE OF COMPETITION: INDUSTRIAL BATTERIES MARKET

TABLE 148 INDUSTRIAL BATTERIES MARKET: REGION FOOTPRINT (21 COMPANIES)

TABLE 149 INDUSTRIAL BATTERIES MARKET: BATTERY TYPE FOOTPRINT (21 COMPANIES)

TABLE 150 INDUSTRIAL BATTERIES MARKET: END-USE INDUSTRY FOOTPRINT (21 COMPANIES)

TABLE 151 INDUSTRIAL BATTERIES MARKET: LIST OF KEY START-UPS/SMES

TABLE 152 INDUSTRIAL BATTERIES MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

TABLE 153 INDUSTRIAL BATTERIES MARKET: PRODUCT LAUNCHES (JANUARY 2021–APRIL 2024)

TABLE 154 INDUSTRIAL BATTERIES MARKET: DEALS (JANUARY 2021–DECEMBER 2023)

TABLE 155 ENERSYS.: COMPANY OVERVIEW

TABLE 156 ENERSYS.: PRODUCTS OFFERED

TABLE 157 C&D TECHNOLOGIES, INC.: COMPANY OVERVIEW

TABLE 158 C&D TECHNOLOGIES, INC.: PRODUCTS OFFERED

TABLE 159 C&D TECHNOLOGIES, INC.: PRODUCT LAUNCHES

TABLE 160 GS YUASA INTERNATIONAL LTD.: COMPANY OVERVIEW

TABLE 161 GS YUASA INTERNATIONAL LTD.: PRODUCTS OFFERED

TABLE 162 EXIDE INDUSTRIES LTD.: COMPANY OVERVIEW

TABLE 163 EXIDE INDUSTRIES LTD.: PRODUCTS OFFERED

TABLE 164 LEOCH INTERNATIONAL TECHNOLOGY LIMITED INC: COMPANY OVERVIEW

TABLE 165 LEOCH INTERNATIONAL TECHNOLOGY LIMITED INC: PRODUCTS OFFERED

TABLE 166 LEOCH INTERNATIONAL TECHNOLOGY LIMITED INC: PRODUCT LAUNCHES

TABLE 167 CROWN BATTERY: COMPANY OVERVIEW

TABLE 168 CROWN BATTERY: PRODUCTS OFFERED

TABLE 169 EAST PENN MANUFACTURING COMPANY: COMPANY OVERVIEW

TABLE 170 EAST PENN MANUFACTURING COMPANY: PRODUCTS OFFERED

TABLE 171 SAMSUNG SDI CO., LTD.: COMPANY OVERVIEW

TABLE 172 SAMSUNG SDI CO., LTD.: PRODUCTS OFFERED

TABLE 173 SK INNOVATION CO., LTD: COMPANY OVERVIEW

TABLE 174 SK INNOVATION CO., LTD: PRODUCTS OFFERED

TABLE 175 NARADA POWER: COMPANY OVERVIEW

TABLE 176 NARADA POWER: PRODUCTS OFFERED

TABLE 177 NARADA POWER: OTHERS

TABLE 178 NARADA POWER: PRODUCT LAUNCHES

TABLE 179 VISION GROUP: COMPANY OVERVIEW

TABLE 180 VISION GROUP: PRODUCTS OFFERED

TABLE 181 LG CHEM: COMPANY OVERVIEW

TABLE 182 LG CHEM: PRODUCTS OFFERED

TABLE 183 LG CHEM: DEALS

TABLE 184 LG CHEM: OTHERS

TABLE 185 YUASA BATTERY (THAILAND) PUBLIC COMPANY LTD.: COMPANY OVERVIEW

TABLE 186 YUASA BATTERY (THAILAND) PUBLIC COMPANY LTD.: PRODUCTS OFFERED

TABLE 187 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: COMPANY OVERVIEW

TABLE 188 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: PRODUCTS OFFERED

TABLE 189 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: PRODUCT LAUNCHES

TABLE 190 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: DEALS

TABLE 191 HOPPECKE BATTERIEN GMBH & CO. KG.: COMPANY OVERVIEW

TABLE 192 HOPPECKE BATTERIEN GMBH & CO. KG.: PRODUCTS OFFERED

TABLE 193 HOPPECKE BATTERIEN GMBH & CO. KG: OTHERS

TABLE 194 HOPPECKE BATTERIEN GMBH & CO. KG.: DEALS

TABLE 195 THE SUNLIGHT GROUP: COMPANY OVERVIEW

TABLE 196 THE SUNLIGHT GROUP: PRODUCTS OFFERED

TABLE 197 THE SUNLIGHT GROUP: PRODUCT LAUNCHES

TABLE 198 THE SUNLIGHT GROUP: DEALS

TABLE 199 TAB: COMPANY OVERVIEW

TABLE 200 TAB: PRODUCTS OFFERED

TABLE 201 TAB: DEALS

TABLE 202 RITAR INTERNATIONAL GROUP: COMPANY OVERVIEW

TABLE 203 RITAR INTERNATIONAL GROUP: PRODUCTS OFFERED

TABLE 204 RITAR INTERNATIONAL GROUP: OTHERS

TABLE 205 U.S. BATTERY: COMPANY OVERVIEW

TABLE 206 U.S. BATTERY: PRODUCT OFFERED

TABLE 207 U.S. BATTERY.: PRODUCT LAUNCHES

TABLE 208 U.S. BATTERY.: DEALS

TABLE 209 AMARA RAJA ENERGY & MOBILITY LIMITED: COMPANY OVERVIEW

TABLE 210 AMARA RAJA ENERGY & MOBILITY LIMITED.: PRODUCTS OFFERED

TABLE 211 AMARA RAJA ENERGY & MOBILITY LIMITED: OTHERS

TABLE 212 IPOWER BATTERIES: COMPANY OVERVIEW

TABLE 213 IPOWER BATTERIES: PRODUCTS OFFERED

TABLE 214 IPOWER BATTERIES.: PRODUCT LAUNCHES

TABLE 215 IPOWER BATTERIES.: DEALS

TABLE 216 JYC BATTERY MANUFACTURER CO., LTD.: COMPANY OVERVIEW

TABLE 217 JYC BATTERY MANUFACTURER CO., LTD.: PRODUCT OFFERINGS

TABLE 218 JYC BATTERY MANUFACTURER CO., LTD.: PRODUCT LAUNCHES

TABLE 219 AMARON BATTERIES: COMPANY OVERVIEW

TABLE 220 SAFT GROUPE: COMPANY OVERVIEW

TABLE 221 SAFT GROUPE: DEALS

TABLE 222 SAFT GROUPE: OTHERS

TABLE 223 ROLLS BATTERY: COMPANY OVERVIEW

TABLE 224 VICTRON ENERGY: COMPANY OVERVIEW

TABLE 225 NORTHVOLT AB: COMPANY OVERVIEW

TABLE 226 NORTHVOLT AB: PRODUCT LAUNCHES

TABLE 227 LITHIUM-ION BATTERY MARKET, BY VOLTAGE, 2019–2022 (USD BILLION)

TABLE 228 LITHIUM-ION BATTERY MARKET, BY VOLTAGE, 2023–2032 (USD BILLION)

LIST OF FIGURES (51 FIGURES)

FIGURE 1 INDUSTRIAL BATTERIES MARKET: MARKET SEGMENTATION

FIGURE 2 INDUSTRIAL BATTERIES MARKET: RESEARCH DESIGN

FIGURE 3 MAIN MATRIX CONSIDERED WHILE CONSTRUCTING AND ASSESSING DEMAND IN INDUSTRIAL BATTERIES MARKET

FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

FIGURE 6 METHODOLOGY FOR SUPPLY-SIDE SIZING OF INDUSTRIAL BATTERIES MARKET (1/2)

FIGURE 7 METHODOLOGY FOR SUPPLY-SIDE SIZING OF INDUSTRIAL BATTERIES MARKET (2/2)

FIGURE 8 INDUSTRIAL BATTERIES MARKET: DATA TRIANGULATION

FIGURE 9 LEAD-ACID SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

FIGURE 10 STATIONARY SEGMENT TO ACCOUNT FOR DOMINANT MARKET SHARE DURING FORECAST PERIOD

FIGURE 11 ASIA PACIFIC TO REGISTER FASTEST GROWTH DURING FORECAST PERIOD

FIGURE 12 SHIFT TO SUSTAINABLE ENERGY TO DRIVE MARKET

FIGURE 13 ASIA PACIFIC TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

FIGURE 14 CHINA TO GROW AT HIGHEST RATE DURING FORECAST PERIOD

FIGURE 15 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN INDUSTRIAL BATTERIES MARKET

FIGURE 16 LITHIUM-ION BATTERY PACK PRICE, 2018−2023

FIGURE 17 INDUSTRIAL BATTERIES MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 18 VALUE CHAIN ANALYSIS FOR INDUSTRIAL BATTERIES MARKET

FIGURE 19 ECOSYSTEM OF INDUSTRIAL BATTERIES MARKET

FIGURE 20 AVERAGE SELLING PRICE OF LITHIUM-ION BATTERIES, BY REGION, 2019−2023

FIGURE 21 AVERAGE SELLING PRICE OF LITHIUM-ION BATTERIES, BY CHEMISTRY, 2023

FIGURE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USES

FIGURE 23 KEY BUYING CRITERIA FOR TOP END USES

FIGURE 24 LIST OF MAJOR PATENTS FOR INDUSTRIAL BATTERIES

FIGURE 25 TRENDS/ DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 26 INVESTMENT AND FUNDING SCENARIO FOR STARTUPS/SMES IN INDUSTRIAL BATTERIES MARKET

FIGURE 27 LEAD-ACID SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

FIGURE 28 STATIONARY BATTERY END-USE INDUSTRY TO LEAD INDUSTRIAL BATTERIES MARKET DURING FORECAST PERIOD

FIGURE 29 ASIA PACIFIC TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 30 NORTH AMERICA: INDUSTRIAL BATTERIES MARKET SNAPSHOT

FIGURE 31 ASIA PACIFIC: INDUSTRIAL BATTERIES MARKET SNAPSHOT

FIGURE 32 EUROPE: INDUSTRIAL BATTERIES MARKET SNAPSHOT

FIGURE 33 REVENUE ANALYSIS OF KEY COMPANIES, 2019–2023

FIGURE 34 INDUSTRIAL BATTERIES MARKET SHARE ANALYSIS, 2023

FIGURE 35 RANKING OF TOP 5 PLAYERS IN INDUSTRIAL BATTERIES MARKET, 2023

FIGURE 36 BRAND/PRODUCT COMPARISON

FIGURE 37 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

FIGURE 38 INDUSTRIAL BATTERIES MARKET: COMPANY FOOTPRINT (21 COMPANIES)

FIGURE 39 START-UP/SME EVALUATION MATRIX, 2023

FIGURE 40 COMPANY VALUATION

FIGURE 41 COMPANY FINANCIAL METRICS

FIGURE 42 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY MANUFACTURERS

FIGURE 43 ENERSYS.: COMPANY SNAPSHOT

FIGURE 44 GS YUASA INTERNATIONAL LTD.: COMPANY SNAPSHOT

FIGURE 45 EXIDE INDUSTRIES LTD.: COMPANY SNAPSHOT

FIGURE 46 LEOCH INTERNATIONAL TECHNOLOGY LIMITED INC: COMPANY SNAPSHOT

FIGURE 47 SAMSUNG SDI CO., LTD.: COMPANY SNAPSHOT

FIGURE 48 SK INNOVATION CO., LTD: COMPANY SNAPSHOT

FIGURE 49 LG CHEM: COMPANY SNAPSHOT

FIGURE 50 YUASA BATTERY (THAILAND) PUBLIC COMPANY LTD.: COMPANY SNAPSHOT

FIGURE 51 CONTEMPORARY AMPEREX TECHNOLOGY CO., LIMITED: COMPANY SNAPSHOT

Growth opportunities and latent adjacency in Industrial Batteries Market