The study involved four major activities in estimating the current market size of nanocellulose. Exhaustive secondary research was done to collect information on the market, peer, and parent markets. The next step was to validate these findings, assumptions, and sizes with industry experts across the value chain of nanocellulose through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation were used to estimate the size of the market's segments and sub-segments.

Secondary Research

The research methodology used to estimate and forecast the access control market begins with capturing data on the revenues of key vendors in the market through secondary research. In the secondary research process, various secondary sources, such as Hoovers, Bloomberg BusinessWeek, Factiva, World Bank, and Industry Journals, were referred to for identifying and collecting information for this study. These secondary sources included annual reports, press releases & investor presentations of companies, white papers, certified publications, articles by recognized authors, notifications by regulatory bodies, trade directories, and databases. Vendor offerings have also been taken into consideration to determine market segmentation.

Primary Research

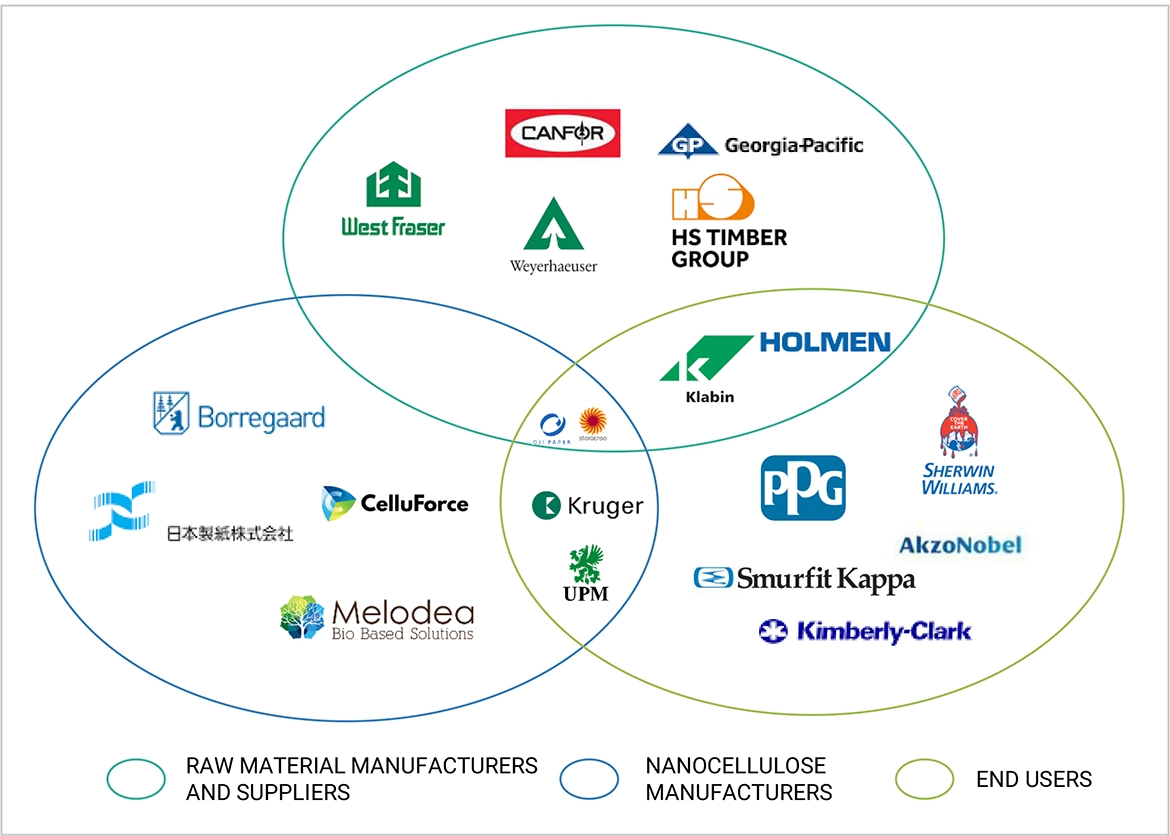

The nanocellulose market comprises several stakeholders, such as raw material suppliers, processors, end-product manufacturers, and regulatory organizations, in the supply chain. The demand side of this market is characterized by the development of pulp & paper, composites, biomedical & pharmaceutical, paints & Coatings, electronics & sensors, and other applications. Advancements in technology characterize the supply side. Various primary sources from the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information. Following is the breakdown of the primary respondents:

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

The top-down and bottom-up approaches were used to estimate and validate the total size of the nanocellulose market. These methods were also used extensively to determine the size of various sub-segments in the market. The research methodology used to estimate the market size included the following:

-

The key players were identified through extensive primary and secondary research.

-

The value chain and market size of the industrial evaporators market, in terms of value, were determined through primary and secondary research.

-

All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources.

-

All possible parameters that affect the market covered in this research study were accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data.

-

The research included the study of reports, reviews, and newsletters of top market players, along with extensive interviews for opinions from key leaders, such as CEOs, directors, and marketing executives.

Global Nanocellulose Market Size: Bottom-Up Approach

To know about the assumptions considered for the study, Request for Free Sample Report

Global Nanocellulose Market Size: Top-Down Approach

Data Triangulation

The market was split into several segments and sub-segments after arriving at the overall market size using the market size estimation processes as explained above. Data triangulation and market breakdown procedures were employed to complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment. The data was triangulated by studying various factors and trends from both the demand and supply sides in the pulp & paper, composites, paints & coatings, biomedical & pharmaceuticals, electronic & sensors, and other industries.

Market Definition

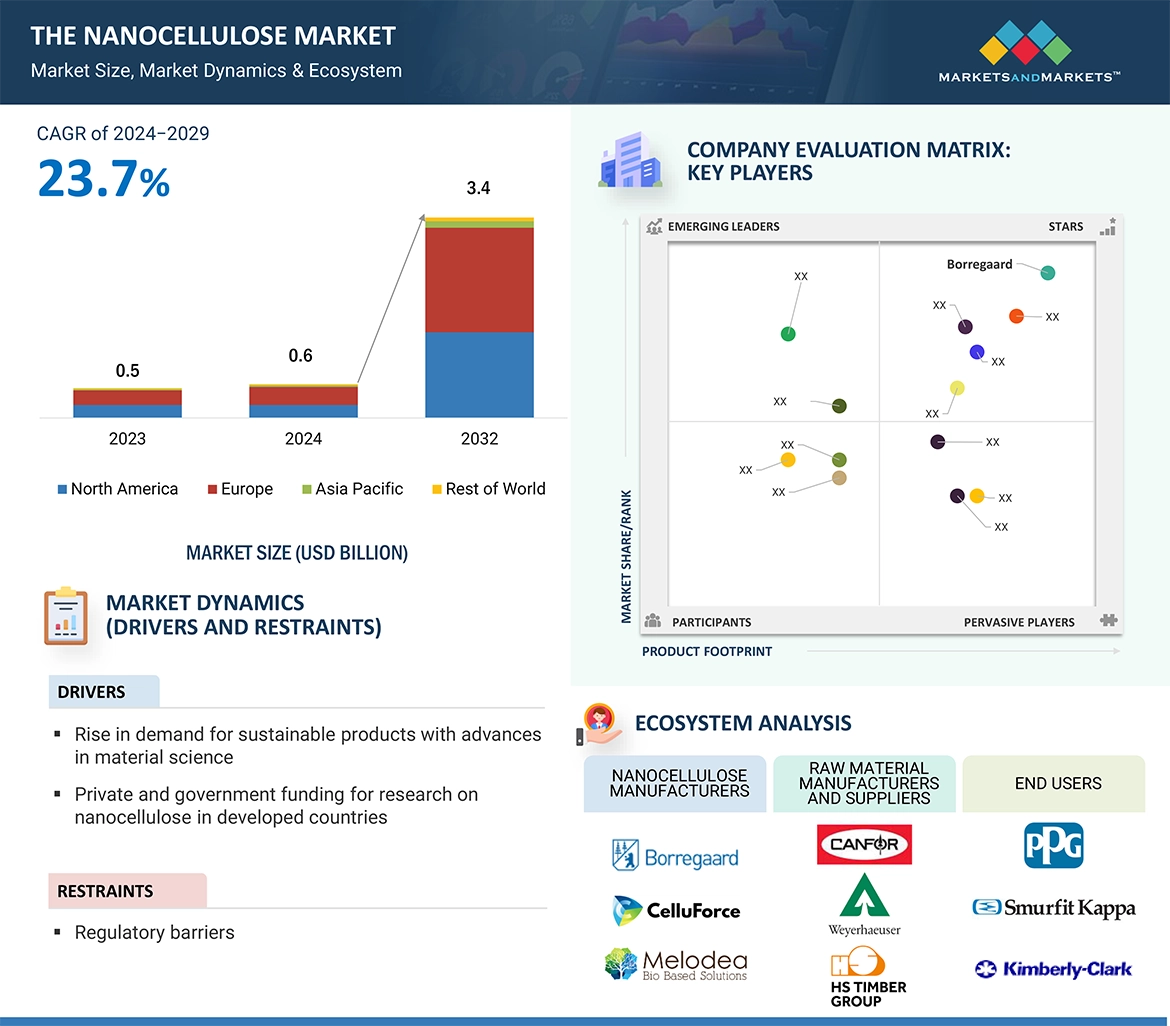

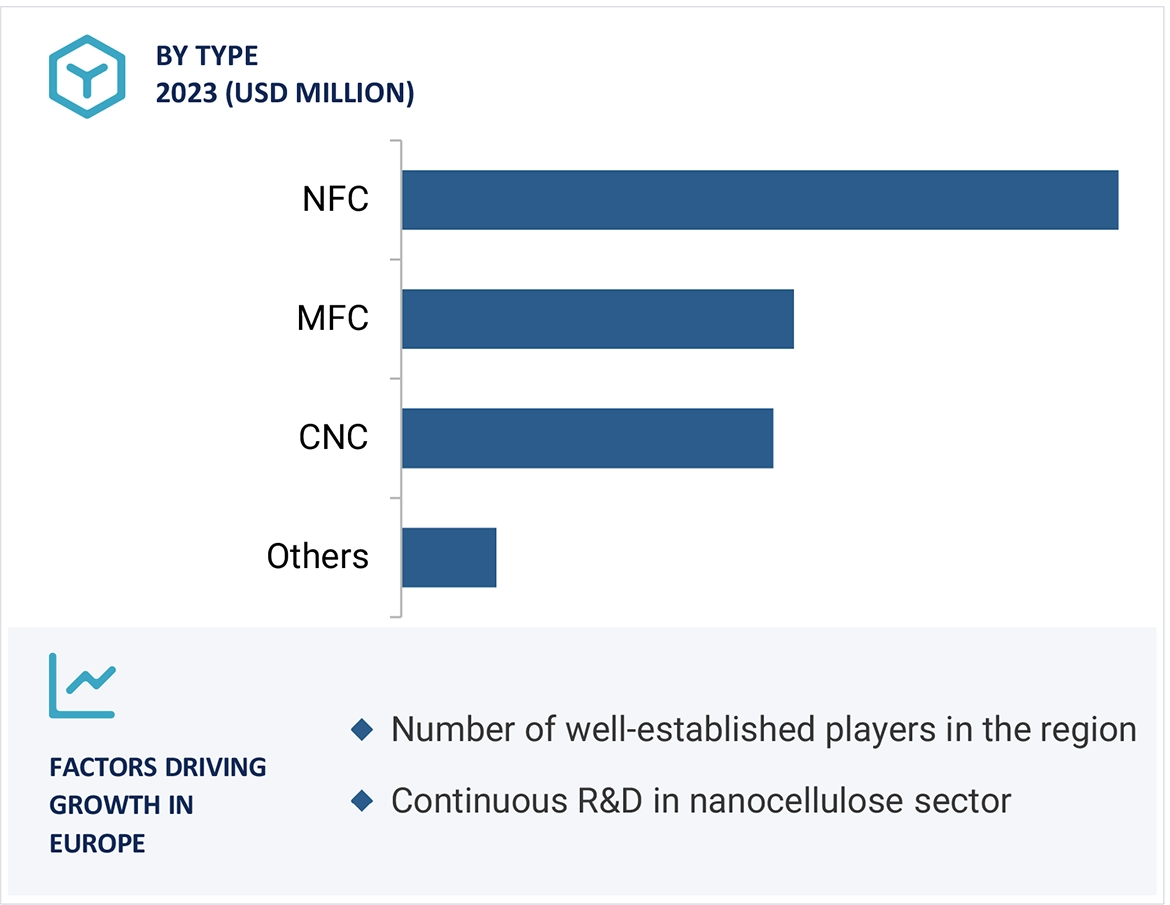

Nanocellulose is a bio-based nanomaterial also called nanostructured cellulose. This pseudoplastic material acts like certain gels or fluids thick or viscous in normal conditions but thin out or flow over time. The main types of nanocellulose include microfibrillated cellulose (MFC), nanofibrillated cellulose (NFC), and crystalline nanocellulose or nanocrystalline cellulose (CNC/NCC). Other types of nanocellulose include bacterial nanocellulose and cellulose filaments. Nanocellulose has the potential to take the place of or add to plastic and parts of oil and fracking drilling fluids and emulsifiers.

Key Stakeholder

-

Manufacturers of dimethyl carbonate

-

Traders, distributors, and suppliers of nanocellulose

-

Government and research organizations

-

Associations and industrial bodies

-

Research and consulting firms

-

R&D institutions

-

Environment support agencies

-

Investment banks and private equity firms

Report Objectives:

-

To analyze and forecast the nanocellulose market by type, raw material, and application in terms of value and volume.

-

To forecast the market size for various segments concerning four main regions: Asia Pacific, Europe, North America, Rest of the World, along with their key countries

-

To provide detailed information regarding drivers, restraints, opportunities, and challenges influencing market growth

-

To analyze the opportunities in the market for stakeholders by identifying the high-growth segments of the nanocellulose market

-

To strategically analyze the micromarkets1 concerning individual growth trends, growth prospects, and their contribution to the overall market

-

To benchmark players within the market using competitive leadership mapping, which analyses market players on various parameters within the broad categories of business and product strategies.

-

To map the competitive intelligence based on company profiles, key player strategies, and game-changing developments, such as product launches and developments, expansions, mergers and acquisitions, and contracts and agreements

-

To strategically profile the key players and analyze their market shares and core competencies2.

Available Customizations:

With the given market data, MarketsandMarkets offers customizations according to client-specific needs. The following customization options are available for the report:

-

Additional country-level analysis of the dimethyl carbonate market

-

Profiling of additional market players (up to 5)

-

Product matrix, which gives a detailed comparison of the product portfolio of each company.

Seyedeh

Jan, 2019

Looking for major applications of nano cellulose and also interested in list of potential customers for nano cellulose.

CK

Jun, 2019

Interested in nanocellulose market.

Ayl�n

Apr, 2019

Working on thesis:nanocellulose production.

Daniel

May, 2022

Looking for more information on nanocellulose market size having forecasts 2022 - 2027.

Ema

May, 2019

Information related to cellulosic materials, especially nanocellulose..

SUSHIL

Sep, 2019

Nanocellulose market .

Dakuri

Feb, 2020

Need information on nanocellulose market applications in the field of active packaging. .

Yushin

May, 2019

Global nanocellulose market for pulp and papermaking applications.

Shally

Dec, 2022

The Nanocellulose Market Report, on the market segmentation front, is broken down into market Type (MFC & NFC, CNC/NCC, and Others), Application (Pulp&paper, composites, biomedical & pharmaceutical, electronics & sensors, and others). The Market estimation has been provided both in USD Value and KT in consumption..

Raluca

Oct, 2018

General information on cellulose nanocrystals.

Qingbin

Sep, 2015

Interested in Nanocellulose market report.

Qingbin

Sep, 2015

Nanocellulose Market and insights.

ANTONIO

Jun, 2019

Understand the scope of Green Coconut Fibers along with available technologies, cost, and business partnership opportunity.

Susan

Mar, 2015

looking for market projections, manufacturers, and applications of non-fibers.

Brianna

Feb, 2017

Specific information on Cellulose nanocrystals and cellulose nanofibers for application in the pulp and paper process.