North America Polymer Foam Market

Download PDF

Download PDF Request Customisation

Request CustomisationNorth America Polymer Foam Market by Resin Type (PU, PS, PO, Phenolic), Foam Type (Flexible and Rigid), End-use Industry (Building & Construction, Bedding & Furniture, Packaging, Automotive, Footwear, Sports & Recreational), and Country - Forecast to 2030

OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

The North America polymer foam market is projected to grow from USD 20.74 billion in 2023 to USD 29.42 billion by 2030, at a CAGR of 5.1% during the forecast period. The market growth is driven by the trend of utilizing lighter and more energy-efficient materials across various industries, including automotive, construction, packaging, and furniture. Moreover, the region has been able to adopt high-performance polyurethanes, polystyrenes, and polyolefin foams due to its considerable environmental consciousness and advanced processing technologies, which enable the production of these materials in a more sustainable manner. The automotive industry is increasingly using lightweight, impact-resistant foams in electric cars and futuristic mobility designs. In the construction industry, the transition to energy-efficient buildings, along with the stringent insulation standards set by programs such as ENERGY STAR, is leading to an increased use of rigid polyurethane and expanded polystyrene foams. Additionally, the online shopping boom and sophisticated logistics networks are fueling the demand for foam packaging that is both protective and recyclable. The continuous development of bio-based formulations, compliance support for low-emission materials, and gradual industrial growth will all contribute to North America becoming a major player in the polymer foam market over the next decade.

KEY TAKEAWAYS

-

BY REGIONThe US was the largest polymer foam market in North America, in terms of value, in 2023. The market in the country is projected to register a CAGR of 5.5%, in terms of value, between 2024 and 2030.

-

BY Resin TypePolyurethane is projected to be the fastest-growing segment of the North America polymer foam market, registering a CAGR of 5.2% during the forecast period, in terms of value.

-

BY Foam TypeIn the North American polymer foam market, flexible foam is the fastest-growing segment, driven by its expanding use in automotive, furniture, and packaging applications due to its lightweight, durable, and energy-absorbing properties.

-

BY End-use IndustryThe building & construction industry led the North American polymer foam market in 2023, accounting for a share of 25.7% in value.

The North America polymer foam market is set to grow steadily owing to the strong demand from the automobile, construction, packaging, and furniture industries. The US and Canada are leading the region due to their excellent manufacturing infrastructure, technological innovations, and the increasing use of energy-efficient materials. Electric and hybrid vehicles are becoming increasingly common in the automotive sector, resulting in a significant increase in the use of polyurethane and polyolefin foams for thermal management, acoustic insulation, and lightweight interior components. The construction industry is also growing rapidly, and the rigid polyurethane and polystyrene foams are being used in building insulation and energy-efficient housing projects. Supportive policies, such as the US Department of Energy’s Better Buildings Initiative and Canada’s green construction standards, are promoting the use of recyclable and low-emission foams. Furthermore, the swift growth of e-commerce and logistics is increasing the need for high-performance protective packaging solutions. All these factors, along with improvements in foam formulation, recycling technology, and sustainable production practices, will drive the North America polymer foam market during the forecast period.

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The North America polymer foam market is witnessing new material innovations, sustainability regulations, and performance-driven design trends in major industries like automotive, construction, and packaging, which is driving the demand for lightweight, energy-efficient, and recyclable materials. For instance, the development of low-emission formulations, closed-cell technologies, and the integration of recycled feedstock not only prolongs the life of the material but also enhances its insulation and energy performance. End users are no longer considering foams for electric vehicles, infrastructure retrofits, or even high-efficiency buildings solely to comply with environmental standards. They are becoming increasingly accustomed to the idea of using foams in these categories. Partnerships among foam manufacturers, OEMs, and technology providers are making way for the expansion of applications in mobility, logistics, and consumer goods. All these factors are making North America a center for sustainable and high-performance polymer foam innovation.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Level

-

Rising use of lightweight foams in automotive and transport

-

Expanding construction demand for energy-efficient insulation

Level

-

Volatility in petrochemical raw material prices

-

Limited recycling infrastructure and environmental concerns

Level

-

Increasing adoption of bio-based and CO2-derived foams

-

Expansion of high-performance insulation solutions in construction and data centers

Level

-

Strict EPA and state-level environmental regulations

-

Competition from alternative sustainable materials

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Rising use of lightweight foams in automotive and transport

The focus on lightweighting in the automotive & transport industry is a major factor driving the growth in demand for polymer foam. The automotive industry is turning to the use of polyurethane, polyolefin, and polystyrene foams to reduce vehicle weight, improve fuel economy, and comply with the stringent emission regulations. These foams possess excellent power-to-weight ratios and also exhibit very good qualities, such as energy absorption and soundproofing, which make them highly compatible and ideal for applications in seating, headliners, door panels, and thermal management components. Moreover, powerful insulation and passenger comfort are some of the reasons why EV battery foams are in high demand. The US and Canada are increasing their electric vehicle production and also investing in eco-friendly transportation. This is expected to drive the demand for lightweight polymer foams.

Restraint: Volatility in petrochemical raw material prices

One of the biggest restraints facing the North American polymer foam market is the fluctuating cost of petrochemical feedstocks, such as propylene, ethylene, and toluene. Most foams are made from crude oil or natural gas, and their production costs depend significantly on fluctuations in the global energy market. The instability in oil and gas prices caused by supply chain troubles, geopolitical tensions, and changing refinery output affects the manufacturer's profits and pricing reliability. Moreover, rising energy costs and inflation put extra pressure on producers. This situation deters the establishment of long-term supply contracts and generates uncertainty for downstream industries like automotive, construction, and packaging.

Opportunity: Increasing adoption of bio-based and CO2-derived foams

The shift toward sustainable materials is driving the growing adoption of bio-based and CO2-derived polymer foams across North America. Manufacturers are putting their money on renewable feedstocks and carbon capture technologies to eliminate the use of petroleum and reduce their carbon footprints significantly. Plant-based and waste CO2-derived foams are not only good for the environment, but also the manufacturers are finding them suitable in terms of performance. Governmental support, corporate sustainability commitments, and consumer preferences for non-hazardous materials are driving this change. Furthermore, leading chemical manufacturers in the US and Canada are working on the development of large-scale production capabilities for carbon-free foam formulas to ensure availability. This development is taking place in the construction, automotive, and packaging sectors, where the adoption of sustainable polymer foam is increasing in line with decarbonization and circular economy initiatives.

Challenge: Strict EPA and state-level environmental regulations

The North America polymer foam market faces a major challenge in the form of stringent environmental regulations that are enforced by the Environmental Protection Agency (EPA) and various state authorities. The increasing restrictions on VOC emissions, the use of fluorinated blowing agents, and the disposal of non-recyclable foam materials are really taking the production plants to their limits. Hence, manufacturers have no option but to reformulate their products and upgrade their technologies. Moreover, compliance with these constantly changing sustainability standards, such as low-emission manufacturing and extended producer responsibility programs, increases operational complexity and cost. For example, California and New York are among the states setting the most stringent benchmarks for chemical safety and environmental performance, making it necessary for producers to accelerate the transition to environmentally friendly alternatives. In the long run, these regulations will result in a more sustainable industry; however, they will also necessitate a large amount of investment in R&D, supply chain transformation, and certification processes, which will make regulatory compliance a major challenge for producers of polymer foam.

NORTH AMERICA POLYMER FOAM MARKET: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Produces polyurethane and polystyrene foam insulation products for residential, commercial, and industrial buildings | Improves energy efficiency and thermal insulation; supports sustainable and low-carbon construction |

|

Manufactures flexible elastomeric and polyethylene foams for HVAC, refrigeration, and mechanical systems | Reduces heat loss and condensation; enhances system performance and energy savings |

|

Develops polyurethane and polyolefin foams for automotive, aerospace, and packaging applications | Reduces vehicle weight and improves fuel efficiency; ensures impact resistance and durability |

|

Supplies polyurethane and expanded polypropylene foams for automotive seating, bedding, and interior comfort systems | Enhances comfort, sound absorption, and recyclability; supports sustainable foam innovation |

|

Produces technical foams and thermal management materials for electronics, mobility, and industrial equipment | Improves heat dissipation and vibration control; enables lightweight and durable designs |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The North American polymer foam market is characterized by a highly integrated ecosystem among manufacturers, distributors, raw material suppliers, and end users. Major producers, such as Owens Corning, Huntsman Corporation, and Woodbridge, are instrumental in the production of polyurethane, polystyrene, and polyolefin, which are mainly used in the construction, automotive, and packaging sectors. These companies rely on large raw material suppliers, such as Dow Inc. and ExxonMobil, which provide essential inputs like polyols, isocyanates, and polyolefins, the foundation of foam production. The distribution network, consisting of, among others, Worldwide Foam and Foam Factory, provides support to the supply chain in the region by offering user-friendly industrial solutions. On the demand side, major users such as General Motors, Steelcase, and WestRock utilize polymer foams for lightweight, thermal insulation, cushioning, and protective packaging applications. The interconnectedness of all these elements depicts North America as a place with a very strong manufacturing infrastructure, advanced technology, and the ever-increasing drive for energy-efficient and eco-friendly foam products in various industries.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Polymer Foam Market, By End-use Industry

The furniture & bedding segment is expected to witness the fastest growth in the North America polymer foam market, driven by the consumers' demand for comfort, durability, and eco-friendly materials. Flexible polyurethane foams are widely used in this end-use segment as they provide superior cushioning and durability in mattresses, upholstered furniture, and seating. The development of e-commerce platforms and direct-to-consumer mattress brands has significantly increased the demand for foams. The growing concern for indoor air quality and the use of low-VOC, CertiPUR-US certified, and bio-based foams are also driving the market growth. Further, the improvement of foam technology with temperature-regulating and pressure-relief formulations is leading to better product performance and increasing user comfort. The rise in disposable incomes, the trend of home renovations, and the expansion of the hospitality sector across the US and Canada are driving demand for polymer foams in the furniture & bedding industry.

Polymer foam market, By Resin Type

The polyurethane segment, by resin type, is expected to register the fastest CAGR in the North America polymer foam market during the forecast period. Polyurethane's mechanical strength, adaptability, and diverse applications in various industries, such as construction, automotive, furniture, bedding, and packaging, are the major drivers of growth for this segment. Both rigid and flexible polyurethane foams are widely used due to their excellent insulation, cushioning, and lightweight properties. In the construction industry, rigid polyurethane foams are gaining popularity for wall and roof insulation to meet the strict energy standards across the US, Canada, and Mexico. The rapid increase in electric vehicle production in the US and Mexico, alongside Canada’s strong commitment to green building initiatives, is further driving the market for this segment. Moreover, innovation in the development of bio-based and CO2-derived polyurethane formulations is supporting sustainability goals, thereby making polyurethane the most preferred resin type in the North America polymer foam market.

REGION

The US is expected to register the highest CAGR in the North America polymer foam market during the forecast period.

The US is anticipated to be the fastest-growing market for polymer foam in North America during the forecast period. This is driven by the expansion of residential construction, rising automotive production, and investment in high-performance insulation materials. The recovery of the housing construction and infrastructure projects in the country is increasing the demand for polyurethane and polystyrene foams, especially in wall and roof insulation. Rising household incomes, low unemployment rates, and favorable lending conditions are also supporting the steady growth of the building & construction sector. The rapid expansion of hyperscale data centers across major hubs such as Virginia, Texas, and Oregon is also driving the demand for thermally stable polymer foams used in insulation and cooling systems. The automotive industry is increasingly adopting lightweight foam materials to enhance fuel economy and comply with stringent emission standards. Companies like Owens Corning are paving the way for foam innovation with environmentally friendly insulation technologies and enhanced material efficiency.

NORTH AMERICA POLYMER FOAM MARKET: COMPANY EVALUATION MATRIX

Owens Corning is the leading player in the North America polymer foam market due to its large range of top-quality foam insulation materials for thermal management, acoustic control, and structural efficiency. The company primarily focuses on the construction, automotive, and industrial manufacturing sectors. Owens Corning's commitment to sustainability, lightweight construction, and energy efficiency has made it a trusted innovator in the insulation and building materials market. In addition, the company’s continuous development of recyclable and low-emission foam technologies supports its market position. Woodbridge (Emerging Leader) is expanding its position in the polymer foam industry through innovative solutions tailored for automotive seating, mattresses, and wheelchair accessibility by developing new polyurethane foam solutions. Woodbridge further promises to be an environmentally friendly and technologically advanced company by adopting the principles of material science, recyclability, and design innovation with the circular economy. Woodbridge is developing its next-generation product line for North America's polymer foam market by combining performance-driven product engineering with a commitment to environmental responsibility.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

- Owens Corning (US)

- Aeroflex USA, Inc. (US)

- Huntsman International LLC. (US)

- FXI (US)

- Woodbridge (US)

- Boyd (US)

- Carpenter Co. (US)

- UFP Technologies, Inc. (US)

- FXI (US)

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2023 (Value) | USD 20.74 BN |

| Market Forecast in 2030 | USD 29.42 BN |

| CAGR (2024–2030) | 5.10% |

| Years Considered | 2019–2030 |

| Base Year | 2023 |

| Forecast Period | 2024–2030 |

| Units Considered | Value (USD BN) |

| Report Coverage | The report defines, segments, and projects the polymer foam market based on resin type, foam type, end-use industry, and region. It provides detailed information regarding the major factors influencing the market's growth, such as drivers, restraints, opportunities, and challenges. It strategically profiles polymer foam manufacturers, comprehensively analyzes their market shares and core competencies, and tracks and analyzes competitive developments they undertake in the market, such as expansions, partnerships, and new product launches. |

| Segments Covered | Resin Type (Polyurethane, Polystyrene, Polyolefin, Phenolic, Other Resin Types) |

| Regional Scope | US, Canada, Mexico |

WHAT IS IN IT FOR YOU: NORTH AMERICA POLYMER FOAM MARKET REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Automotive Manufacturers | Conduct comparative benchmarking of polyurethane and polyolefin foams for lightweight vehicle interiors and thermal insulation | Enables OEMs to select optimal foam materials that improve fuel efficiency and acoustic performance |

| Construction & Insulation Companies | Provide in-depth evaluation of foam insulation systems for building energy codes under ASHRAE and LEED standards | Helps builders and architects meet stringent US energy efficiency requirements |

| Furniture & Bedding Manufacturers | Assess comfort, density, and emission characteristics of flexible polyurethane foams for furniture and mattresses | Enhances product comfort, indoor air quality, and environmental compliance |

| Packaging & Logistics Companies | Evaluate cushioning, resilience, and recyclability performance of expanded and extruded polystyrene packaging foams | Reduces packaging waste and aligns with circular economy goals in North America |

| Data Center & Electronics Cooling System Providers | Analyze thermal and dielectric performance of polymer foams in immersion cooling and electronic enclosure systems | Enhances data center efficiency and heat management reliability |

| Regulatory & Sustainability Teams | Develop sustainability benchmarking models for polymer foam recycling and emissions management | Ensures compliance with EPA and state-level environmental frameworks |

RECENT DEVELOPMENTS

- September 2023 : Aeroflex USA, Inc. introduced AEROFLEX Breathe-EZ, a fiber-free EPDM closed-cell elastomeric duct insulation designed for the North American market. This duct liner and wrap application targets energy conservation, condensation control, and acoustic attenuation. AEROFLEX Breathe-EZ complies with flame spread and smoke development requirements set forth by the International Mechanical Code for duct coverings and linings within building plenums.

- August 2020 : Owens Corning announced a new product line: FOAMULAR NGX. The proprietary blowing agent in this new line of extruded polystyrene (XPS) foam products delivers a $90\%$ reduction in global warming potential (GWP) without sacrificing product performance.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Methodology

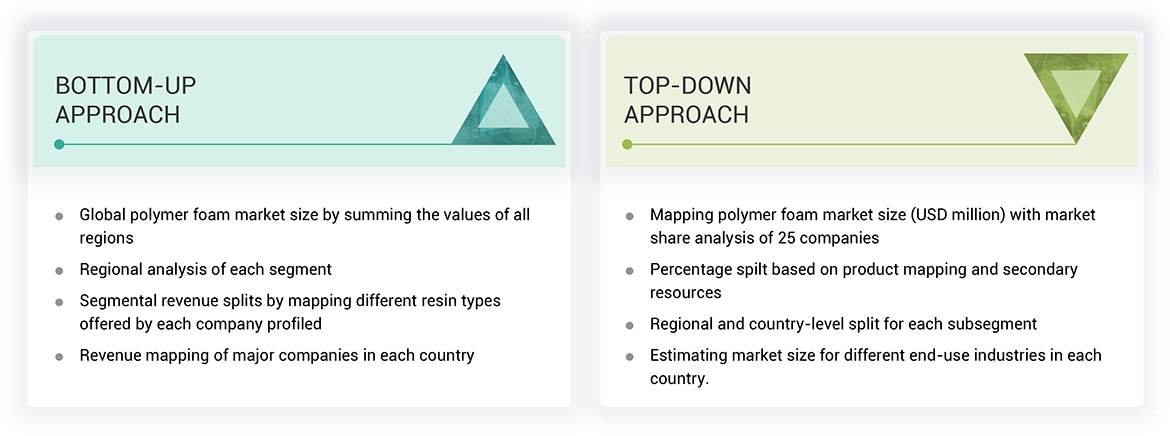

The study involved four major activities in estimating the current size of the North America polymer foam market—exhaustive secondary research collected information on the market, peer markets, and parent markets. The next step was to validate these findings, assumptions, and sizing with the industry experts across the North America polymer foam value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation were used to estimate the market size of segments and subsegments.

Secondary Research

Secondary sources for this research study include annual reports, press releases, and investor presentations of companies; white papers; certified publications; and articles by recognized authors; gold- and silver-standard websites; North America polymer foam manufacturing companies, regulatory bodies, trade directories, and databases. The secondary research was mainly used to obtain critical information about the industry’s supply chain, the pool of key players, market classification, and segmentation according to industry trends to the bottom-most level and regional markets. It has also been used to obtain information about key developments from a market-oriented perspective.

Primary Research

The North America polymer foam market comprises several stakeholders, such as raw material suppliers, technology support providers, manufacturers, and regulatory organizations in the supply chain. Various primary sources from the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information. Primary sources from the supply side included industry experts such as Chief Executive Officers (CEOs), vice presidents, marketing directors, technology and innovation directors, and related key executives from various companies and organizations operating in the north america polymer foam market. Primary sources from the demand side included directors, marketing heads, and purchase managers from various sourcing industries.

Market Size Estimation

Both the top-down and bottom-up approaches have been used to estimate and validate the total size of the North America polymer foam market. These approaches have also been used extensively to estimate the size of various dependent market subsegments. The research methodology used to estimate the market size included the following:

The following segments provide details about the overall market size estimation process employed in this study

- The key players in the market were identified through secondary research.

- The market shares in the respective regions were identified through primary and secondary research.

- The value chain and market size of the North America polymer foam market, in terms of value, were determined through primary and secondary research.

- All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources.

- All possible parameters that affect the market covered in this research study were accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data.

- The research included the study of annual and financial reports of the top market players and interviews with industry experts, such as CEOs, VPs, directors, sales managers, and marketing executives, for critical insights, both quantitative and qualitative

Data Triangulation

The market was split into several segments and sub-segments after arriving at the overall market size using the market size estimation processes as explained above. Data triangulation and market breakdown procedures were employed to complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment. The data was triangulated by studying various factors and trends from both the demand and supply sides in the North America polymer foam sector.

Market Definition

Polymer foams are made of polymers, blowing agents, and additives. They are produced using different processing methods, such as slab-stock by pouring, extrusion, and other molding forms. They are used in various industries, such as packaging, furniture and bedding, building and construction, and automotive. These foams are classified based on their structures as closed and open cells. Closed-cell foam is rigid, whereas open-cell foam is flexible.

Stakeholders

- Raw material manufacturers

- Technology support providers

- Manufacturers of polymer foam

- Traders, distributors, and suppliers

- Regulatory Bodies and Government Agencies

- Research & Development (R&D) Institutions

- End-use Industries

- Consulting Firms, Trade Associations, and Industry Bodies

- Investment Banks and Private Equity Firms

Report Objectives

- To analyze and forecast the market size of the North America polymer foam market in terms of value

- To provide detailed information regarding the major factors (drivers, restraints, challenges, and opportunities) influencing the regional market

- To analyze and forecast the North America polymer foam market based on foam type, resin type, end-use industry, and region

- To analyze the opportunities in the market for stakeholders and provide details of a competitive landscape for market leaders

- To track and analyze the competitive developments, such as acquisitions, partnerships, collaborations, agreements, and expansions in the market

- To strategically profile the key players and comprehensively analyze their market shares and core competencies

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This ReportPersonalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the North America Polymer Foam Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

We at Nissan Chemicals Corporation have been clients of MarketsandMarkets for more than a year now. We recently consulted MarketsandMarkets for a study, the team at MarketsandMarkets was extremely professional and organized. The business insights were very detailed and aligned well with our expectations that really helped us formulate the Business Plans and device new strategies for development themes. MarketsandMarkets offers a unique combination of expertise and dedicated engagement model. Their research findings have helped us in designing our Pricing Strategy which will make it easier for us to predict the future sales and profits for the next ten years. We look forward to working with MarketsandMarkets in the future.

VP of Strategy & New Business Development

Leading Specialty Chemical Company

The MarketsandMarkets Engagement Model, composed of both the Knowledge Store and advisory custom research, has greatly helped us in understanding our markets and making strategic decisions. The Knowledge Store is a fast way to allow everyone in our organization to understand more about most any market they are interested in. The ability to then get custom research done and get answers to specific strategic questions and market insight has been spectacular. The Markets and Markets team feel more like colleagues than vendors and their services have helped us change our culture where statements of things like growth opportunities and competitive position are always backed by industry research.

Rich Gibson,

Director, Corporate Strategy

Milliken & Company,

Leading Industrial Manufacturer of specialty chemical, floor covering, performance and protective textile materials, and healthcaremilliken.com

MarketsandMarkets is a trusted resource that helps us to better understand markets that are near-adjacencies-whether its technology, value chain or geography. Their Knowledge Store platform provides a dashboard of markets and their characteristics which is easy to use and saves us time.

Adam Shaw,

Market Development and Strategy Manager

AdvanSix Inc. USA,

An American Leader in Chemicalswww.advansix.com

The Knowledge Store from MarketsandMarkets is a valuable tool which has helped my team acquire greater insight in to the end markets that our business serves. This has enabled us to help our company build stronger strategies throughout our planning process.

TOSHIO KINOSHITA

Senior Chif Consultion Research & Consulting Division

Mitsubishi Chemical Research Corporation,

Leading Manufacturer of Chemical Productswww.mitsubishichem-res.co.jp/en/

We recently engaged with MarketsandMarkets for a study, the team not only clearly understood our business objectives but was also extremely professional in the way they handled the entire project. The study was efficiently conducted in a phase-wise manner, and the engagement model furnished us with high-quality business insights that far exceeded our expectations at each phase. We were especially happy that MarketsandMarkets could provide us with both, an English as well as a Japanese version of the study. A special thanks to the Analyst Team and Client Services Team, whose fluency in Japanese enhanced our comfort level, as we could converse with them in our preferred language.

Independent entrepreneurs

Arrow Precision

We approached MarketsandMarkets for study on Proppants Market, and their work exceeded our expectations. The study conducted was comprehensive and enabled us to view the market through the various dimensions. In addition, the team was extraordinarily responsive throughout the process and resolved our queries on time. I strongly recommend MarketsandMarkets and will certainly consider them for additional market assessments we will need in the future.

Global engineering company, Japan

Deputy Manager,

Strategic Planning OfficeThe high-quality insights shared by the MarketsandMarkets team helped us understand the pharmaceutical plant designers in a specific geography. It also captured the risks that we may likely face in communicating with our potential partners. The study would enable us identify partners, which would impact our future growth.

Growth opportunities and latent adjacency in North America Polymer Foam Market