4

MARKET OVERVIEW

Provides a snapshot of current market scenario, value chain context, and factors impacting competitive intensity.

4.2.1.1

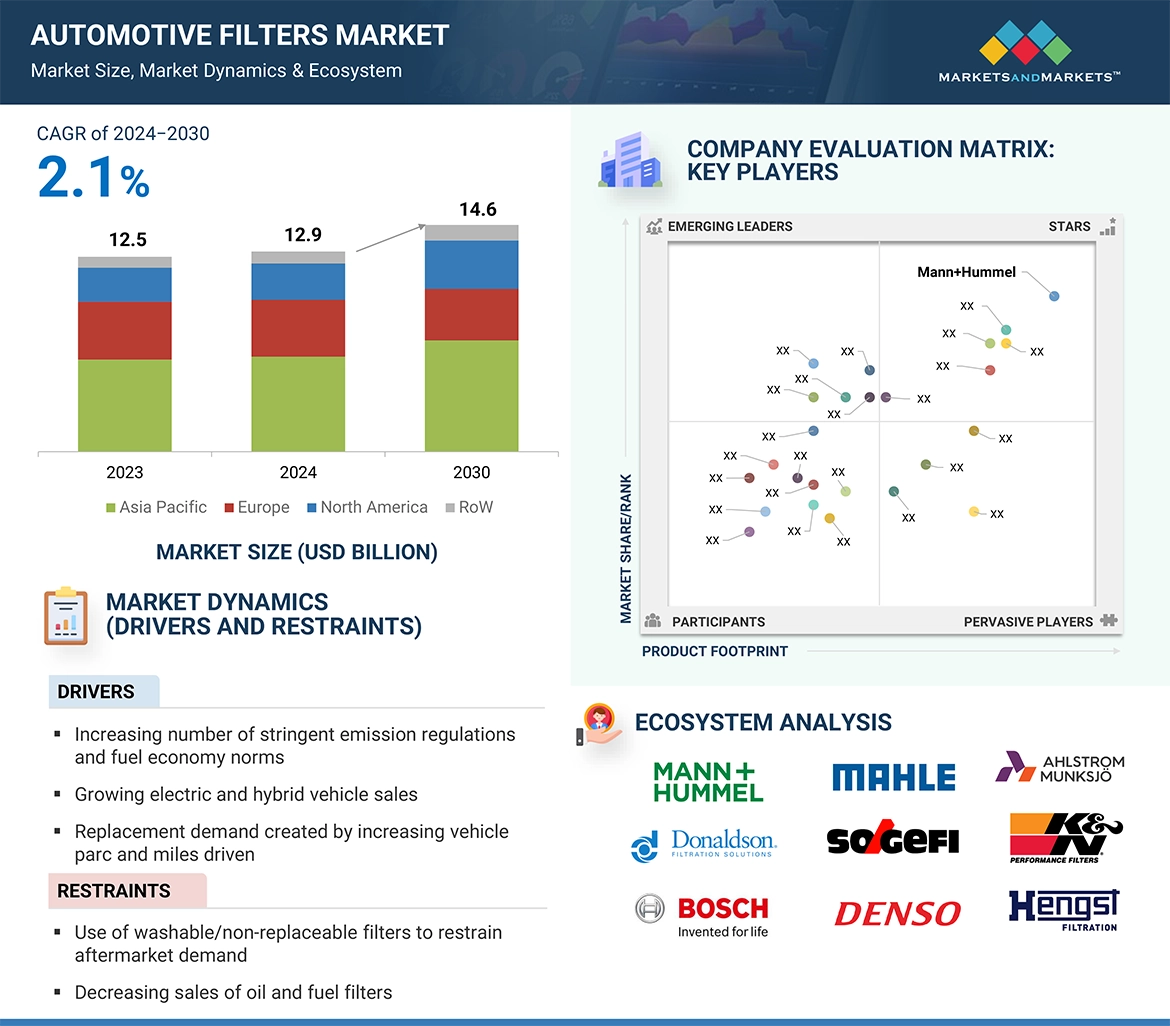

INCREASING NUMBER OF STRINGENT EMISSION REGULATIONS AND FUEL ECONOMY NORMS

4.2.1.2

GROWING ELECTRIC AND HYBRID VEHICLE SALES

4.2.1.3

REPLACEMENT DEMAND CREATED BY INCREASING VEHICLE PARC AND MILES DRIVEN

4.2.2.1

USE OF WASHABLE/NON-REPLACEABLE FILTERS TO RESTRAIN AFTERMARKET DEMAND

4.2.2.2

DECREASING SALES OF OIL AND FUEL FILTERS

4.2.3.1

ADVANCEMENTS IN FILTRATION MEDIA TECHNOLOGY

4.2.4.1

AVAILABILITY OF LOCAL PRODUCTS TO HINDER DEMAND FOR OE FILTERS

4.2.4.2

FLUCTUATING RAW MATERIAL COSTS

4.3

UNMET NEEDS AND WHITE SPACES

4.4

INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.5

STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5

INDUSTRY TRENDS

Outlines emerging trends, technology impact, and regulatory signals affecting growth trajectory and stakeholder decisions.

5.1

MACROECONOMIC OUTLOOK

5.1.2

GDP TRENDS AND FORECAST

5.1.3

TRENDS IN THE GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

5.2

SUPPLY CHAIN ANALYSIS

5.4.1

AVERAGE SELLING PRICE TREND, BY FILTER TYPE (2022-2025)

5.4.2

AVERAGE SELLING PRICE TREND, BY REGION (2022-2025)

5.5.1

IMPORT SCENARIO (HS CODE 842123)

5.5.2

EXPORT SCENARIO (HS CODE 842123)

5.6

KEY CONFERENCES AND EVENTS, 2025–2026

5.7

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.8

INVESTMENT AND FUNDING SCENARIO

5.9

FUNDING BY USE CASE APPLICATION

5.12

TOTAL COST OF OWNERSHIP

5.13

IMPACT OF 2025 US TARIFF – AUTOMOTIVE FILTERS MARKET

5.13.3

PRICE IMPACT ANALYSIS

5.13.4

IMPACT ON COUNTRIES/REGIONS

5.13.5

IMPACT ON THE AUTOMOTIVE INDUSTRY

6

TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE STRATEGIC APPLICATIONS

6.1.2

COMPLEMENTARY TECHNOLOGIES

6.1.3

ADJACENT TECHNOLOGIES

6.2

TECHNOLOGY/PRODUCT ROADMAP

6.5

IMPACT OF AI/GEN AI ON THE AUTOMOTIVE FILTERS MARKET

6.5.1

TOP USE CASES AND MARKET POTENTIAL

6.5.2

BEST PRACTICES IN ELECTRIC VEHICLE DEVELOPMENT

6.5.3

CASE STUDIES OF AI IMPLEMENTATION IN THE AUTOMOTIVE FILTERS MARKET

6.5.4

INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

6.5.5

CLIENTS’ READINESS TO ADOPT GENERATIVE AI IN THE AUTOMOTIVE FILTERS MARKET

6.5

SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7.1

REGIONAL REGULATIONS AND COMPLIANCE

7.1.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

7.1.2

FILTRATION STANDARDS

7.1.3

EMISSION REGULATIONS

7.1.3.1

ON-ROAD VEHICLE EMISSION REGULATIONS

7.1.3.2

OFF-ROAD VEHICLE EMISSION REGULATIONS

8

CUSTOMER LANDSCAPE & BUYER BEHAVIOR

8.1

DECISION-MAKING PROCESS

8.2

BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

8.3

ADOPTION BARRIERS & INTERNAL CHALLENGES

8.4

UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9

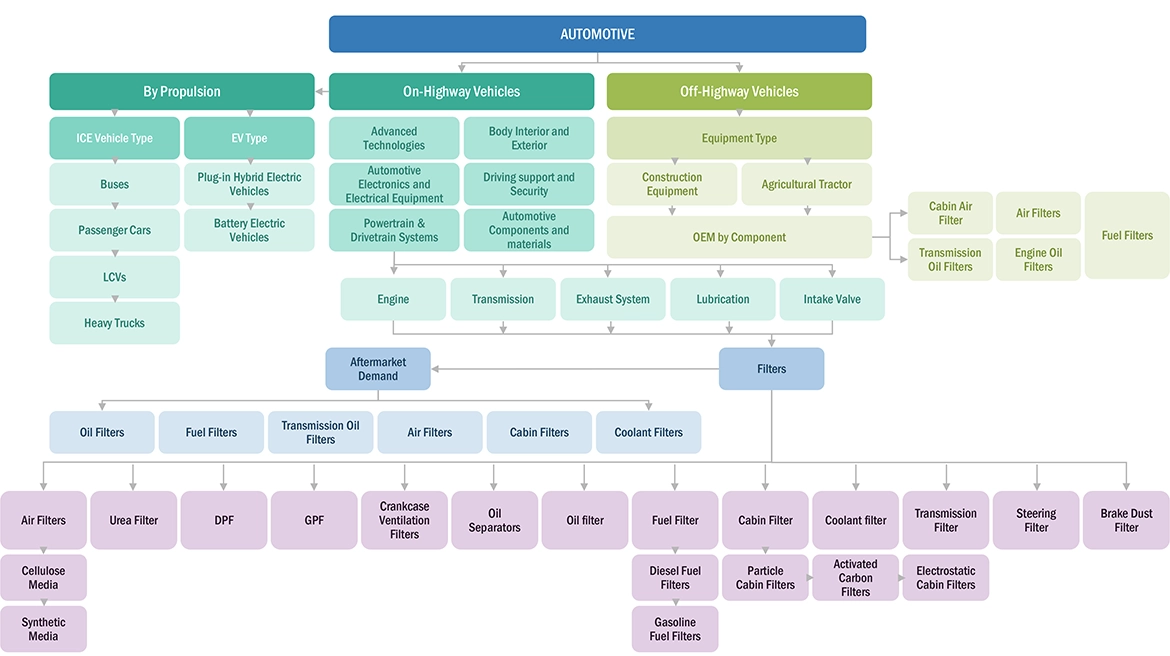

AUTOMOTIVE FILTERS MARKET, BY FILTER TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

COMPARATIVE ASSESSMENT OF KEY AUTOMOTIVE FILTER TYPES, THEIR MARKET POTENTIAL, AND DEMAND PATTERNS BY VARIOUS SUPPLIER COMPANIES

Market Size, Volume & Forecast – USD Million

9.2.1

INCREASING DEMAND FOR PASSENGER AND COMMERCIAL VEHICLES TO DRIVE THE MARKET

9.3.1

INCREASING STRINGENT EMISSION NORMS AND ADVANCEMENT IN FILTRATION MEDIA TO DRIVE THE MARKET

9.4.1

INCREASING THE ENGINE SIZE OF HEAVY TRUCKS AND SUVS TO DRIVE THE MARKET

9.5.1

RISING AWARENESS ABOUT IN-CABIN AIR QUALITY TO DRIVE THE MARKET

9.6.1

GROWING AWARENESS ABOUT POLLUTION CAUSED BY DISC BRAKES TO DRIVE THE MARKET

9.7.1

RISING ADOPTION OF AUTOMATIC, CONTINUOUS VARIABLE, AND DUAL-CLUTCH TRANSMISSION SYSTEMS TO DRIVE THE MARKET

9.8.1

RISING NUMBER OF HEAVY-DUTY VEHICLES WITH LARGER ENGINE CAPACITY TO DRIVE THE MARKET

9.9.1

INCREASING DEMAND FOR LUXURY AND PREMIUM CARS TO DRIVE THE MARKET

9.10.1

INCREASING DEMAND FOR SUVS AND HEAVY-DUTY VEHICLES WITH HYDRAULIC POWER STEERING TO DRIVE THE MARKET

9.11.1

STRINGENT EMISSION NORMS RELATED TO CO2 AND NOX TO DRIVE MARKET

9.12

DIESEL PARTICULATE FILTER (DPF)

9.12.1

INSTALLATION OF DPF IN ALL DIESEL VEHICLES ACROSS EUROPE AND NORTH AMERICA TO DRIVE THE MARKET

9.13

GASOLINE PARTICULATE FILTER (GPF)

9.13.1

ENGINE DOWNSIZING TREND TO DRIVE MARKET

9.14

CRANKCASE VENTILATION

9.14.1

RISING DEMAND FOR HEAVY-DUTY TRUCKS AND BUSES TO DRIVE THE MARKET

9.15

KEY PRIMARY INSIGHTS

10

AUTOMOTIVE AIR FILTERS MARKET, BY MEDIA TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

VEHICLE-WISE DEMAND POTENTIAL AND GROWTH PATHWAYS SHAPING AUTOMOTIVE FILTERS ADOPTION IN DIVERSE INDUSTRIES

10.2.1

COST-EFFECTIVENESS TO DRIVE MARKET

10.3.1

INCREASING DEMAND FOR PREMIUM VEHICLES TO DRIVE THE MARKET

10.4

KEY PRIMARY INSIGHTS

11

AUTOMOTIVE CABIN FILTERS MARKET, BY MATERIAL TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

SYSTEM-WISE DEMAND POTENTIAL AND GROWTH PATHWAYS SHAPING AUTOMOTIVE FILTERS ADOPTION IN DIVERSE INDUSTRIES

11.2

PARTICLE CABIN FILTERS

11.2.1

COST-EFFECTIVENESS AND BETTER PERFORMANCE TO DRIVE THE MARKET

11.3

ACTIVATED CARBON CABIN FILTERS

11.3.1

RISING DEMAND FOR MID-RANGE AND ECONOMY CARS IN EMERGING ECONOMIES TO DRIVE THE MARKET

11.4

ELECTROSTATIC CABIN FILTERS

11.4.1

GROWING SALES OF PREMIUM AND LUXURY VEHICLES TO DRIVE THE MARKET

11.5

KEY PRIMARY INSIGHTS

12

AUTOMOTIVE FUEL FILTERS MARKET, BY FUEL TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

SECTOR-SPECIFIC ADOPTION DRIVERS, DEMAND DYNAMICS, AND MARKET POTENTIAL ACROSS EACH ACTUATION

12.2.1

INCREASING SALES OF GASOLINE-FUELED VEHICLES COMPARED TO DIESEL-POWERED VEHICLES TO DRIVE THE MARKET

12.3.1

STRINGENT EMISSION NORMS ON DIESEL ENGINES TO REDUCE DEMAND

12.4

KEY PRIMARY INSIGHTS

13

OFF-HIGHWAY VEHICLE FILTERS MARKET, BY EQUIPMENT TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

SECTOR-SPECIFIC ADOPTION DRIVERS, DEMAND DYNAMICS, AND MARKET POTENTIAL ACROSS EACH COMPONENT

13.2

AGRICULTURAL TRACTOR

13.2.1

ADOPTION OF MECHANIZED FARMING TO DRIVE THE MARKET

13.3

CONSTRUCTION EQUIPMENT

13.3.1

INCREASED CONSTRUCTION ACTIVITIES AND INDUSTRIAL DEVELOPMENTS TO DRIVE THE MARKET

13.4

KEY PRIMARY INSIGHTS

14

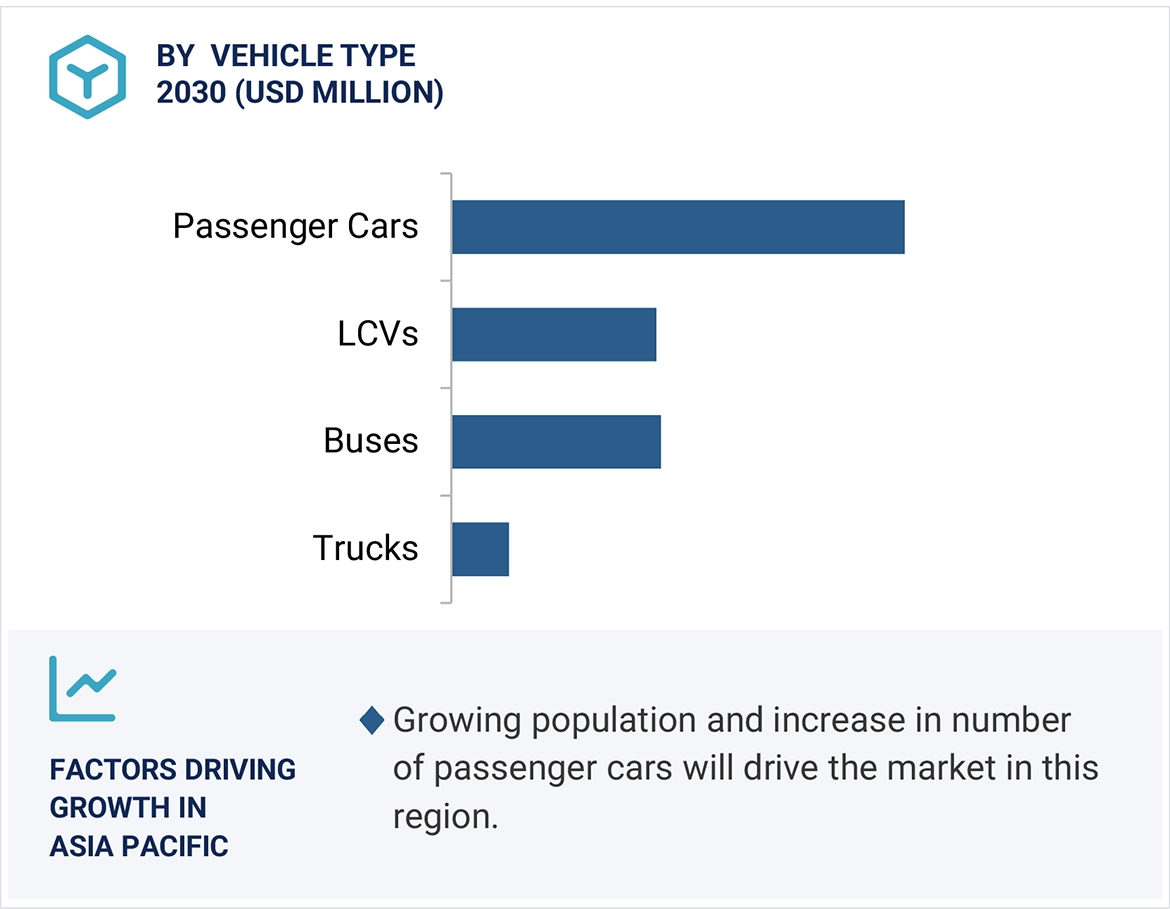

AUTOMOTIVE FILTERS MARKET (ICE), BY VEHICLE TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

SECTOR-SPECIFIC ADOPTION DRIVERS, DEMAND DYNAMICS, AND MARKET POTENTIAL ACROSS EACH COMPONENT

14.2.1

NEED FOR FUEL EFFICIENCY TO DRIVE THE MARKET

14.3

LIGHT COMMERCIAL VEHICLE (LCV)

14.3.1

HIGH DEMAND IN NORTH AMERICA TO DRIVE THE MARKET

14.4.1

GROWTH OF LARGE-SCALE INDUSTRIES TO DRIVE THE MARKET

14.5.1

HIGH DEPENDENCY ON PUBLIC TRANSPORT TO DRIVE THE MARKET

14.6

KEY PRIMARY INSIGHTS

15

ELECTRIC & HYBRID VEHICLE FILTERS MARKET (OE),

BY VEHICLE TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

SECTOR-SPECIFIC ADOPTION DRIVERS, DEMAND DYNAMICS, AND MARKET POTENTIAL ACROSS EACH COMPONENT

15.2

BATTERY ELECTRIC VEHICLE (BEV)

15.2.1

GOVERNMENT SUBSIDIES AND INVESTMENTS IN CHARGING INFRASTRUCTURE TO DRIVE THE MARKET

15.3

PLUG-IN HYBRID ELECTRIC VEHICLE (PHEV)

15.3.1

BENEFITS OF THE HIGHER RANGE TO DRIVE THE MARKET

15.4

KEY PRIMARY INSIGHTS

16

AUTOMOTIVE FILTERS AFTERMARKET (ICE), BY FILTER TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

COMPARATIVE ASSESSMENT OF KEY AUTOMOTIVE FILTER TYPES, THEIR MARKET POTENTIAL, AND DEMAND PATTERNS BY VARIOUS SUPPLIER COMPANIES

16.2.1

INCREASING PROPORTION OF PASSENGER AND COMMERCIAL VEHICLES IN EMERGING ECONOMIES TO DRIVE THE MARKET

16.3.1

INCREASING DEMAND FOR GASOLINE FUEL FILTERS TO DRIVE THE MARKET

16.4.1

RISING DEMAND FOR MID & FULL-SIZE VEHICLES TO DRIVE MARKET

16.5.1

RISING DEMAND FOR IN-CABIN COMFORT TO DRIVE THE MARKET

16.6.1

GROWING PREMIUM VEHICLE PARC TO DRIVE MARKET

16.7.1

INCREASING CITY TRAFFIC AND LONG-DISTANCE TRAVEL TO DRIVE THE MARKET

16.8

KEY PRIMARY INSIGHTS

17

ELECTRIC & HYBRID VEHICLE FILTERS MARKET (OE),

BY FILTER TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

COMPARATIVE ASSESSMENT OF KEY AUTOMOTIVE FILTER TYPES, THEIR MARKET POTENTIAL, AND DEMAND PATTERNS BY VARIOUS SUPPLIER COMPANIES

17.2.1

RISING SALES OF PHEVS TO DRIVE THE MARKET

17.3.1

GROWING SALES OF PHEVS AND STRINGENT EMISSION NORMS TO DRIVE THE MARKET

17.4.1

EXCLUSIVE BLEND OF NATURAL AND SYNTHETIC MATERIALS IN ENGINE OIL FILTERS TO DRIVE THE MARKET

17.5.1

RISING PREMIUM VEHICLE RANGE WITH ENHANCED IN-CABIN AMBIANCE TO DRIVE MARKET

17.6.1

EXPECTED INTRODUCTION OF BRAKE DUST FILTERS BY AUDI AND BMW TO DRIVE THE MARKET

17.7.1

INCREASING DEMAND FOR ELECTRIC & HYBRID VEHICLES IN AUTOMATIC, CVT, AND DCT TRANSMISSIONS TO DRIVE THE MARKET

17.8.1

GROWING DEMAND FOR EFFICIENT PERFORMANCE OF POWER ELECTRONICS IN VEHICLES TO DRIVE THE MARKET

17.9

COOLING AIR PARTICLE

17.9.1

GROWING DEMAND FOR EFFICIENT BATTERY PERFORMANCE TO DRIVE THE MARKET

17.10

KEY PRIMARY INSIGHTS

18

OFF-HIGHWAY VEHICLE FILTERS MARKET (OE), BY FILTER TYPE (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

COMPARATIVE ASSESSMENT OF KEY FILTER TYPES, THEIR MARKET POTENTIAL, AND DEMAND PATTERNS BY VARIOUS SUPPLIER COMPANIES

Market Size, Volume & Forecast – USD Million

18.2.1

R&D INVESTMENTS TO IMPROVE AIR FILTRATION TECHNOLOGY TO DRIVE THE MARKET

18.3.1

GROWING RESIDENTIAL, COMMERCIAL, HIGHWAY, AND DAM CONSTRUCTION ACTIVITIES TO DRIVE THE MARKET

18.4.1

INCREASING DEMAND FOR HEAVY EQUIPMENT DUE TO RISING INFRASTRUCTURAL DEVELOPMENTS IN EMERGING ECONOMIES

18.5.1

HIGH ADOPTION RATE OF SMALL-SIZED TRACTORS IN THE ASIA PACIFIC AND NORTH AMERICA TO DRIVE THE MARKET

18.6.1

GROWING TRACTION OF POWER-SHIFT AND AUTOMATIC TRANSMISSION TECHNOLOGY TO DRIVE THE MARKET

18.7

KEY PRIMARY INSIGHTS

19

AUTOMOTIVE FILTERS MARKET, BY REGION (MARKET SIZE & FORECAST TO 2032 – IN VALUE, USD THOUSAND & VOLUME)

ASSESSING GROWTH PATTERNS, INDUSTRY FORCES, REGULATORY LANDSCAPE, AND MARKET POTENTIAL ACROSS KEY GEOGRAPHIES AND COUNTRIES

19.2.1.1

RISING PASSENGER VEHICLE DEMAND TO DRIVE THE MARKET

19.2.2.1

GROWING USE OF TECHNOLOGICALLY ADVANCED FILTRATION SOLUTIONS TO DRIVE THE MARKET

19.2.3.1

INCREASING DEMAND FOR LUXURY CARS TO DRIVE THE MARKET

19.2.4.1

GROWTH IN VEHICLE SALES TO DRIVE THE MARKET

19.2.5.1

GROWING DEMAND FOR AUTOMOTIVE COMPONENTS TO DRIVE THE MARKET

19.2.6

REST OF ASIA PACIFIC

19.2.6.1

DEVELOPING COUNTRIES WITH RISING DISPOSABLE INCOME

19.3.1.1

HIGH DEMAND FOR PREMIUM CARS TO DRIVE THE MARKET

19.3.2.1

INCREASE IN PRODUCTION OF HIGH-END VEHICLES TO DRIVE THE MARKET

19.3.3.1

PRESENCE OF A WELL-ESTABLISHED LUXURY CAR MARKET TO DRIVE THE MARKET

19.3.4.1

INCREASING PRODUCTION OF PASSENGER CARS TO DRIVE THE MARKET

19.3.5.1

RISING SALES OF PREMIUM VEHICLES TO DRIVE THE MARKET

19.3.6.1

RISING FOCUS ON EXPORTS TO DRIVE MARKET

19.3.7.1

INCREASING SALES OF PASSENGER CARS TO DRIVE THE MARKET

19.3.8.1

ROBUST GROWTH IN PRODUCTION CAPACITIES

19.4.1.1

INCREASING PRODUCTION OF SUVS TO DRIVE THE MARKET

19.4.2.1

RISING GOVERNMENT REGULATIONS TO DRIVE THE MARKET

19.4.3.1

GROWING DEMAND FOR ADVANCED FILTRATION TECHNOLOGY TO DRIVE THE MARKET

19.5.1.1

HEAVY INVESTMENTS IN THE AUTOMOTIVE SECTOR TO DRIVE THE MARKET

19.5.2.1

PRESENCE OF MAJOR AUTOMOTIVE COMPANIES TO DRIVE THE MARKET

19.5.3.1

GROWING DEMAND FOR ADVANCED FILTRATION TECHNOLOGY TO DRIVE THE MARKET

STRATEGIC ASSESSMENT OF LEADING PLAYERS, MARKET RANKING/SHARE, REVENUE ANALYSIS, COMPANY POSITIONING, AND COMPETITIVE BENCHMARKS INFLUENCING MARKET POTENTIAL

20.2

KEY PLAYER COMPETITIVE STRATEGIES/ RIGHT TO WIN

20.3

REVENUE ANALYSIS (2022-2024)

20.4

MARKET SHARE ANALYSIS,

20.6

COMPANY EVALUATION MATRIX: KEY PLAYERS,

20.6.5

COMPANY FOOTPRINT: KEY PLAYERS,

20.6.5.1

COMPANY FOOTPRINT

20.6.5.2

REGION FOOTPRINT

20.7

COMPANY EVALUATION MATRIX (ELECTRIC & HYBRID VEHICLE FILTER MANUFACTURERS): KEY PLAYERS,

20.7.5

COMPANY FOOTPRINT: KEY PLAYERS,

20.8

COMPANY VALUATION AND FINANCIAL METRICS

20.10

COMPETITIVE SCENARIO

IN-DEPTH REVIEW OF COMPANIES, PRODUCTS, RECENT INITIATIVES, AND POSITIONING STRATEGIES IN THE AUTOMOTIVE FILTERS MARKET LANDSCAPE

21.1.1.1

BUSINESS OVERVIEW

21.1.1.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.1.3.1

KEY STRENGTHS/RIGHT TO WIN

21.1.1.3.2

STRATEGIC CHOICES

21.1.1.3.3

WEAKNESSES/COMPETITIVE THREATS

21.1.2

DONALDSON COMPANY, INC.

21.1.2.1

BUSINESS OVERVIEW

21.1.2.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.2.3

RECENT DEVELOPMENTS

21.1.2.4

PRODUCT LAUNCHES

21.1.2.5.1

KEY STRENGTHS/RIGHT TO WIN

21.1.2.5.2

STRATEGIC CHOICES

21.1.2.5.3

WEAKNESSES/COMPETITIVE THREATS

21.1.3.1

BUSINESS OVERVIEW

21.1.3.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.3.3

RECENT DEVELOPMENTS

21.1.3.3.1

PRODUCT LAUNCHES

21.1.3.4.1

KEY STRENGTHS/RIGHT TO WIN

21.1.3.4.2

STRATEGIC CHOICES

21.1.3.4.3

WEAKNESSES/COMPETITIVE THREATS

21.1.4.1

BUSINESS OVERVIEW

21.1.4.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.4.3

RECENT DEVELOPMENTS

21.1.4.3.1

PRODUCT LAUNCHES

21.1.4.4.1

KEY STRENGTHS/RIGHT TO WIN

21.1.4.4.2

STRATEGIC CHOICES

21.1.4.4.3

WEAKNESSES/COMPETITIVE THREATS

21.1.5.1

BUSINESS OVERVIEW

21.1.5.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.5.3

RECENT DEVELOPMENTS

21.1.5.3.1

PRODUCT LAUNCHES

21.1.5.4.1

KEY STRENGTHS/RIGHT TO WIN

21.1.5.4.2

STRATEGIC CHOICES

21.1.5.4.3

WEAKNESSES/COMPETITIVE THREATS

21.1.6.1

BUSINESS OVERVIEW

21.1.6.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.6.3

RECENT DEVELOPMENTS

21.1.6.3.1

PRODUCT LAUNCHES

21.1.7.1

BUSINESS OVERVIEW

21.1.7.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.7.3

RECENT DEVELOPMENTS

21.1.7.3.1

PRODUCT LAUNCHES

21.1.8

TOYOTA BOSHOKU CORPORATION

21.1.8.1

BUSINESS OVERVIEW

21.1.8.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.8.3

RECENT DEVELOPMENTS

21.1.8.3.1

PRODUCT LAUNCHES

21.1.9.1

BUSINESS OVERVIEW

21.1.9.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.9.3

RECENT DEVELOPMENTS

21.1.9.3.1

PRODUCT LAUNCHES

21.1.10.1

BUSINESS OVERVIEW

21.1.10.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.10.3

RECENT DEVELOPMENTS

21.1.10.3.1

PRODUCT LAUNCHES

21.1.11.1

BUSINESS OVERVIEW

21.1.11.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

21.1.11.3

RECENT DEVELOPMENTS

21.1.11.3.1

PRODUCT LAUNCHES

21.2.3

K&N ENGINEERING, INC.

21.2.5

DALE FILTER SYSTEMS

22.1.1.1

KEY DATA FROM SECONDARY SOURCES

22.1.2.1

KEY DATA FROM PRIMARY SOURCES

22.1.2.2

KEY PRIMARY PARTICIPANTS

22.1.2.3

BREAKDOWN OF PRIMARY INTERVIEWS

22.1.2.4

KEY INDUSTRY INSIGHTS

22.2

MARKET SIZE ESTIMATION

22.2.1

BOTTOM-UP APPROACH

22.2.3

BASE NUMBER CALCULATION

22.3

MARKET FORECAST APPROACH

22.6

RESEARCH ASSUMPTIONS

22.7

RESEARCH LIMITATIONS AND RISK ASSESSMENT

23.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

23.3

CUSTOMIZATION OPTIONS

Amey

Nov, 2019

Up to date (2017) Off highway filter marketplace Globally and by region for all types - Oil, Fuel, prefuel, hydraulic, transmission.

Amey

Nov, 2019

I would appreciate to have a sample of market research of the Brazilian Oil,Fuel,Air and HVAC market, production and market players split.

Amey

Nov, 2019

Air , Oil and Fuel filter Market at Canada , who is suppliers what size is it in aoutomotive including buses,trucks and business heavy equipments market .

Amey

Nov, 2019

Hello, I am interested in receiving reports for Aftermarket data for filters in the United States. Specifically, I would like to locate Vehicle in Operation information, or demands for Heavy Duty Filters. Any information provided would be much appreciated. Thank you.

Amey

Nov, 2019

What is the expected evolution of filter markets considering that the reliability of vehicles and quality of oils is continuously improving and enable to space out visits?.

Amey

Nov, 2019

yes Fuel Filters especially the Diesel Market size. I would like to see if you have info specifically units and dollars for the diesel fuel filter market in the u.s.

Amey

Nov, 2019

Interested to Know market potential for Fuel Filter Cum Water Separator for Ashok leyland Vehicles and current After market share held by various competetions in India.

Amey

Nov, 2019

we are conducting a final career project on filters for motorbikes. Your study migth help us. Regards.

Amey

Nov, 2019

I am seeking an air filter market report with a narrow focus. Specifically, the focus is medium and heavy vehicle in the North America markets (US and Canada data). May I please have a quote and a table of contents for a report with this focus? Thank you, Megan .

Amey

Nov, 2019

I'm specifically interested in automotive-filter manufacturers based in China and the markets/regions they supply to/support. .

Amey

Nov, 2019

I want to get a sense of how Mahle are doing in the UK and Europe within the Aftermarket compared to the leader. If I can get this, I will be able understand the full value of the report.

User

Jul, 2019

Hi, I am looking for specific information on Capacitive dividers for EVT, Testing, RC Dividers, Grading AIS, Grading GIS, TRV AIS, TRV GIS, Thyristor Valve, HVDC Bypass, Filter capacitor, EVT For the following countries and region - Europe. U.S., Canada, India, China, South America, and Middle East Can you please help me with a quote and timeline for the same?.

User

Jul, 2019

Diesel and Gasoline Particulate Filters, Catalysts for the automotive industry globally and all vehicle segments(i.e PC HCV). Thanks.

Swati

Jun, 2019

Hello, I am a consultant/investor in the North America Automotive Aftermarket space and would like a sample report to determine if it can add value for my filter manufacturer client. Regards, Frank.

Atul

May, 2019

We would be interested in purchasing the Report on automotive filters. Could you please provide us with some information prior to the purchase: Is there an extended table of content that you can share with us? Could you share with us the forecast model that is underlying the report? .

Atul

May, 2019

What is the source of the data used in the forecast? (Is it based on IHS data when it comes to volumes for instance?) .

Atul

May, 2019

Can you give us details regarding the methodology? We would need datapoints going back to 2013. Could you provide these? Many thanks in advance! .