Download PDF

Download PDF Request Customisation

Request Customisation

More Electric Aircraft Market Size, Share & Growth

Report Code

AS 2769

Published in

Nov, 2024, By MarketsandMarkets™

More Electric Aircraft Market by System (Propulsion, Airframe), Component (Power Source, Actuators, Electric Pump, Power Electronics, Generator, Valves), Platform (Narrow Body, Wide Body, Regional Jet, Fighter Jet), Application, End Use - Forecast to 2029

USD 8.01 BN

MARKET SIZE, 2029

CAGR 7.6%

(2024-2029)

283

REPORT PAGES

338

MARKET TABLES

MORE ELECTRIC AIRCRAFT MARKET OVERVIEW

The more electric aircraft market is projected to grow from USD 5.56 Billion in 2024 and reach USD 8.01 Billion by 2029, at a CAGR of 7.6% during the forecast period.The More Electric Aircraft (MEA) market is experiencing robust growth driven by increasing environmental regulations, technological advancements, and the need for operational efficiency.

KEY TAKEAWAYS

-

By RegionThe European market accounted for a 38.5% revenue share in 2024.

-

By End UserBy end user, the Civil segment is expected to dominate the market.

-

By ApplicationBy application, the Power Conversion segment is projected to grow at the fastest rate from 2024 to 2029, registering the highest CAGR of 8.3%.

-

By PlatformBy platform, the Rotary Wing segment is projected to grow at the fastest rate from 2024 to 2029, registering the highest CAGR of 12.8%.

-

COMPETITIVE LANDSCAPE- Key PlayersSAFRAN S.A., Honeywell International Inc., and RTX were identified as some of the star players in the more electric aircraft market (global), given their strong market share and product footprint.

-

COMPETITIVE LANDSCAPE- StartupsPBS AEROSPACE, AVIONIC INSTRUMENTS, LLC,and EAGLEPICHER TECHNOLOGIES LLC among others, have distinguished themselves among startups and SMEs by securing strong footholds in specialized niche areas, underscoring their potential as emerging market leaders

More electric aircraft involve using electric power for all non-propulsive systems in an aircraft instead of pneumatic and hydraulic power sources. The More Electric Aircraft Industry is witnessing rapid growth due to environmental, regulatory, operational, and technological factors. An important reason for the growth of the market is the aviation industry's focus on carbon emission reduction and fuel consumption reduction.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The impact on customers' customers in the more electric aircraft market stems from evolving use cases, new technologies, and a rapidly shifting ecosystem. Airlines, commercial operators, military aviation, and government bodies are adopting electric and hybrid-electric platforms, with energy management and power electronics becoming core focus areas. These shifts toward advanced batteries, electric motor systems, and immersive technologies directly influence client operations and revenue models, driving the market's transition toward high-energy density and next-generation aircraft.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MORE ELECTRIC AIRCRAFT MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Development of high-density battery solutions for more electric aircraft

-

Increasing use of electric technology to optimize aircraft performance

RESTRAINTS

Impact

Level

Level

-

High capital requirements and longer clearance periods

-

Potential for overheating of electrical systems

OPPORTUNITIES

Impact

Level

Level

-

Introduction of alternative power sources for electric power generation

-

Advancements in power electronic components

CHALLENGES

Impact

Level

Level

-

Requirement for reliable cable systems

-

Significant increase in maximum take-off weight

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Development of high-density battery solutions for more electric aircraft

The market is gaining momentum as OEMs invest in high-density battery systems that enhance energy efficiency and support longer mission profiles. These advancements enable higher power availability for electric subsystems, accelerating adoption across commercial and military platforms.

Restraint: High capital requirements and longer clearance periods

High upfront investment for electrification technologies, coupled with lengthy certification and regulatory approval cycles, slows program timelines. These constraints make it challenging for OEMs and suppliers to scale deployment at the pace required by the market.

Opportunity: Introduction of alternative power sources for electric power generation

The emergence of fuel cells, hybrid-electric architectures, and next-generation power electronics presents new pathways for improving aircraft efficiency. These technologies expand the addressable market and enable OEMs to diversify propulsion strategies beyond conventional electrical systems.

Challenge: Requirement for reliable cable systems

As aircraft subsystems become increasingly electrified, the demand for high-integrity, lightweight, and heat-resistant cable systems grows significantly. Ensuring reliability under high loads and harsh operating conditions remains a critical engineering challenge for suppliers.

MORE ELECTRIC AIRCRAFT MARKET SIZE, SHARE & GROWTH: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Optimization of more electric aircraft architecture to shift systems from hydraulic to electric for improved operational efficiency. | Reduces aircraft weight, lowers per-passenger operating costs, enhances maneuverability, and improves survivability due to fewer failure-prone components. |

|

|

Development of the 131-9D auxiliary power unit (APU) and high-efficiency mode (HEM) upgrade for single-aisle aircraft. | Provides faster engine starts, higher power output, improved fuel efficiency, and lower environmental footprint, backed by over 100 million in-service hours. |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MORE ELECTRIC AIRCRAFT MARKET ECOSYSTEM

The more electric aircraft ecosystem consists of OEM manufacturers (Safran, AMETEK, BAE Systems, Parker, Honeywell, RTX) and service and solution providers (Woodward, Moog, Pioneer Magnetics, magniX). OEMs develop advanced electric systems, power electronics, and actuation technologies that form the core of next-generation aircraft architectures. Service providers supply specialized components such as electric drives, converters, and power management units that enable efficient and reliable system integration.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MORE ELECTRIC AIRCRAFT MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

More Electric Aircraft Market, By End User

As of 2024, the civil segment held the largest share of the more electric aircraft market and is expected to maintain its lead through 2025, driven by rising commercial air travel and stronger sustainability mandates. Airlines are increasingly adopting electric subsystems to reduce fuel consumption, improve operational efficiency, and meet emission regulations. This sustained investment in fleet modernization reinforces the dominance of civil aviation in the market.

More Electric Aircraft Market, By Application

As of 2024, power distribution systems accounted for the largest share of the more electric aircraft market owing to their critical role in managing electrical loads across the aircraft architecture. These systems support the transition from pneumatic and hydraulic mechanisms to electric alternatives, enhancing efficiency and reliability. Growing adoption of high-voltage systems further strengthens the leadership of the power distribution segment.

More Electric Aircraft Market, By Platform

As of 2024, fixed-wing aircraft led the more electric aircraft market and will continue dominating through 2025 due to extensive electrification initiatives across both commercial and military platforms. New-generation aircraft and long-term fleet replacement programs rely heavily on electric actuation, power electronics, and advanced energy systems. The scale of global fixed-wing operations firmly positions this platform at the forefront of market demand.

More Electric Aircraft Market, By System

As of 2024, aircraft systems held the largest market share, driven by increased adoption of electric propulsion support units, environmental control systems, and advanced actuation technologies. OEMs are prioritizing the electrification of core aircraft functions to improve performance, reduce weight, and enhance energy efficiency. This focus ensures the aircraft system segment remains central to the industry’s electrification roadmap.

More Electric Aircraft Market, By Component

As of 2024, generators represented the largest share of the component segment due to growing demand for high-output, lightweight electrical generation units. These systems provide the necessary power to support electric flight controls, avionics, and environmental systems. Advancements in high-efficiency generators strengthen their role as a critical enabling technology in next-generation electric aircraft architectures.

MORE ELECTRIC AIRCRAFT MARKET REGION

Europe to be fastest-growing region in global more electric aircraft market during forecast period

Europe is expected to lead in the more electric aircraft market, driven by strong regulatory pressures, substantial investment in sustainable aviation, and a well-established aerospace industry dedicated to electric and hybrid-electric innovations. The region is aiming at net-zero carbon emissions by 2050, with specific mandates for reducing aviation emissions.

MORE ELECTRIC AIRCRAFT MARKET SIZE, SHARE & GROWTH: COMPANY EVALUATION MATRIX

In the more electric aircraft market matrix, Honeywell (Star) leads with a strong market share and extensive product footprint, driven by its advanced power electronics, electric actuation systems, and high-efficiency generators widely adopted across commercial and defense aviation. BAE Systems (Emerging Leader) is gaining visibility with its expanding electric propulsion support technologies and tailored solutions for aircraft electrification, strengthening its position through innovation and niche subsystem offerings. While Honeywell dominates through scale and a diverse portfolio, BAE Systems shows significant potential to move toward the leaders’ quadrant as demand for next-generation electric aircraft systems continues to rise.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS - TOP MORE ELECTRIC AIRCRAFT COMPANIES

- Safran S.A ( France)

- Honeywell International Inc. (US)

- RTX (US)

- General Electric (US)

- Parker Hannifin Corporation (US)

- Bae Systems plc (UK)

- Bomardier Inc. (Canada)

- Embraer S.A (Brazil)

- Liebherr (Switzerland)

- Ametek Inc. (US)

- Astronics Corporation (US)

- Moog inc. (US)

- Rolls-Royce Plc (UK)

- Amphenol Corporation (US)

- Eaton (Ireland)

MORE ELECTRIC AIRCRAFT MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2024 (Value) | USD 5.56 Billion |

| Market Forecast in 2030 (Value) | USD 8.01 Billion |

| Growth Rate | CAGR of 7.6% from 2024-2029 |

| Years Considered | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Million/Billion) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, Middle East & Africa, Latin America |

WHAT IS IN IT FOR YOU: MORE ELECTRIC AIRCRAFT MARKET SIZE, SHARE & GROWTH REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Leading Manufacturer | Additional segment breakdown for countries | Additional country-level market sizing tables for segments/sub-segments covered at the regional/global level to gain an understanding of market potential by each country |

| Emerging Leader | Additional company profiles | Competitive information on targeted players to gain granular insights on direct competition |

| Regional Market Leader | Additional country market estimates | Additional country-level deep dive for a more targeted understanding of the total addressable market |

RECENT DEVELOPMENTS

- June 2024 : GE Aerospace (US) partnered with NASA to develop a hybrid electric demonstrator engine that will embed electric motors/generators in a high-bypass commercial turbofan to supplement power during different phases of operation.

- August 2023 : Astronics Corporation (US) won a contract from Bell Textron Inc (US) to support the development of the V-280 Valor for the US Army Future Long Range Assault Aircraft (FLRAA) program.

- June 2023 : Safran Helicopter Engines (France) and AURA AERO (France) signed a partnership agreement for Electric Regional Aircraft (ERA) propulsion.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

30

2

RESEARCH METHODOLOGY

35

3

EXECUTIVE SUMMARY

46

4

PREMIUM INSIGHTS

50

5

MARKET OVERVIEW

Explore how electric advancements are revolutionizing aircraft efficiency, cost, and environmental impact.

53

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

DEVELOPMENT OF HIGH-DENSITY BATTERY SOLUTIONS FOR MORE ELECTRIC AIRCRAFT

5.2.1.2

INCREASING USE OF ELECTRIC TECHNOLOGY TO OPTIMIZE AIRCRAFT PERFORMANCE

5.2.1.3

LOWERING OF OPERATIONAL AND MAINTENANCE COSTS

5.2.1.4

REDUCTION IN EMISSIONS AND AIRCRAFT NOISE

5.2.1.5

TECHNOLOGICAL ADVANCEMENTS IN ELECTRIC SYSTEMS

5.2.2

RESTRAINTS

5.2.2.1

HIGH CAPITAL REQUIREMENTS AND LONGER CLEARANCE PERIODS

5.2.2.2

POTENTIAL FOR OVERHEATING OF ELECTRICAL SYSTEMS

5.2.3

OPPORTUNITIES

5.2.3.1

INTRODUCTION OF ALTERNATIVE POWER SOURCES FOR ELECTRIC POWER GENERATION

5.2.3.2

ADVANCEMENTS IN POWER ELECTRONIC COMPONENTS

5.2.3.3

ADOPTION OF URBAN AIR MOBILITY (UAM) TECHNOLOGIES

5.2.4

CHALLENGES

5.2.4.1

REQUIREMENT FOR RELIABLE CABLE SYSTEMS

5.2.4.2

SIGNIFICANT INCREASE IN MAXIMUM TAKE-OFF WEIGHT

5.3

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.3.1

REVENUE SHIFTS AND NEW REVENUE POCKETS FOR MORE ELECTRIC AIRCRAFT MARKET

5.4

VALUE CHAIN ANALYSIS

5.5

ECOSYSTEM ANALYSIS

5.5.1

PROMINENT COMPANIES

5.5.2

PRIVATE AND SMALL ENTERPRISES

5.5.3

END USERS

5.6

TECHNOLOGY ANALYSIS

5.6.1

KEY TECHNOLOGIES

5.6.1.1

TURBOGENERATORS FOR POWERING ELECTRIC MOTORS AND BATTERIES

5.6.1.2

ELECTRIC ACTUATORS

5.6.2

ADJACENT TECHNOLOGIES

5.6.2.1

FLY-BY-WIRE

5.7

CASE STUDY ANALYSIS

5.7.1

HONEYWELL OPTIMIZES MORE ELECTRIC ARCHITECTURE

5.7.2

HONEYWELL SUCCESSFULLY DESIGNS AUXILIARY POWER UNIT FOR BOEING

5.7.3

ELECTRIC TAXI SYSTEMS

5.8

PRICING ANALYSIS

5.8.1

AVERAGE SELLING PRICE RANGE, BY COMPONENT

5.8.2

INDICATIVE PRICING ANALYSIS, BY COMPONENT

5.8.3

AVERAGE SELLING PRICE RANGE, BY PLATFORM, 2023

5.9

MORE ELECTRIC AIRCRAFT, BY AIRCRAFT TYPE

5.10

KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2

BUYING CRITERIA

5.11

REGULATORY LANDSCAPE

5.11.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.12

TRADE ANALYSIS

5.13

KEY CONFERENCES AND EVENTS, 2024–2025

5.14

BUSINESS MODEL

5.15

TOTAL COST OF OWNERSHIP

5.16

INVESTMENT AND FUNDING SCENARIO

5.17

BILL OF MATERIALS

5.18

TECHNOLOGY ROADMAP

5.19

IMPACT OF GENERATIVE AI

5.19.1

INTRODUCTION

5.19.2

ADOPTION OF AI IN AVIATION BY TOP COUNTRIES

5.19.3

IMPACT OF AI ON AVIATION: USE CASES

5.19.4

IMPACT OF AI ON MORE ELECTRIC AIRCRAFT MARKET

5.20

MACROECONOMIC OUTLOOK

5.20.1

NORTH AMERICA

5.20.2

EUROPE

5.20.3

ASIA PACIFIC

5.20.4

MIDDLE EAST

5.20.5

LATIN AMERICA

5.20.6

AFRICA

6

INDUSTRY TRENDS

Electric aviation advances with smart systems, sustainable fuels, and cutting-edge battery innovations.

88

6.1

INTRODUCTION

6.2

TECHNOLOGY TRENDS

6.2.1

SHIFT FROM HYDRAULIC TO ELECTRIC LANDING GEAR

6.2.2

USE OF ELECTRICAL AND ELECTRONICS TECHNOLOGIES IN MORE ELECTRIC AIRCRAFT

6.2.2.1

MACHINE TECHNOLOGIES

6.2.2.2

POWER ELECTRONICS

6.2.2.3

ENERGY MANAGEMENT

6.2.3

ADVANCED BATTERIES

6.2.3.1

LITHIUM-SULFUR (LI-S)

6.2.4

ELECTRIC MOTOR-DRIVEN SMART PUMPS

6.2.5

HIGH-VOLTAGE POWER DISTRIBUTION

6.2.6

ELECTRIC ACTUATION SYSTEMS (FLY-BY-WIRE)

6.2.7

3D PRINTING

6.3

SUPPLY CHAIN ANALYSIS

6.4

IMPACT OF MEGATRENDS

6.4.1

SUSTAINABLE AVIATION FUEL

6.5

PATENT ANALYSIS

7

MORE ELECTRIC AIRCRAFT MARKET, BY END USER

Market Size & Growth Rate Forecast Analysis to 2029 in USD Million | 2 Data Tables

96

7.1

INTRODUCTION

7.2

CIVIL

7.2.1

FOCUS ON REDUCING EMISSIONS TO PROPEL MARKET

7.3

MILITARY

7.3.1

INCREASED DEFENSE SPENDING TO DRIVE MARKET

8

MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION

Market Size & Growth Rate Forecast Analysis to 2029 in USD Million | 2 Data Tables

99

8.1

INTRODUCTION

8.2

POWER GENERATION

8.2.1

INCREASING DEMAND FOR MORE ELECTRIC ARCHITECTURE TO FUEL MARKET

8.3

POWER DISTRIBUTION

8.3.1

ABILITY TO DETECT VOLTAGE AND PROVIDE PROMPT LOAD SHUT-OFF TO DRIVE DEMAND

8.4

POWER CONVERSION

8.4.1

NEED TO INCREASE OPERATIONAL EFFICIENCY TO GENERATE DEMAND

8.5

ENERGY STORAGE

8.5.1

INCREASED USE OF ADVANCED BATTERY AND FUEL CELL SYSTEMS TO BOOST MARKET

9

MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM

Market Size & Growth Rate Forecast Analysis to 2029 in USD Million | 4 Data Tables

103

9.1

INTRODUCTION

9.2

FIXED-WING

9.2.1

IMPROVED FUEL CONSUMPTION AND RELIABILITY TO DRIVE DEMAND

9.2.2

NARROW-BODY AIRCRAFT (NBA)

9.2.2.1

REDUCTION IN WEIGHT FACTOR TO DRIVE MARKET

9.2.3

WIDE-BODY AIRCRAFT (WBA)

9.2.3.1

NEED TO LOWER CARBON FOOTPRINT TO FUEL MARKET

9.2.4

REGIONAL AIRCRAFT

9.2.4.1

INCREASE IN AIR PASSENGER TRAFFIC TO FUEL DEMAND

9.2.5

FIGHTER JETS

9.2.5.1

INCREASING MILITARY BUDGETS TO BOOST MARKET

9.3

ROTARY-WING

9.3.1

NEED FOR INCREASED OPERATIONAL EFFICIENCY TO DRIVE MARKET

10

MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM

Market Size & Growth Rate Forecast Analysis to 2029 in USD Million | 6 Data Tables

109

10.1

INTRODUCTION

10.2

PROPULSION SYSTEMS

10.2.1

FUEL MANAGEMENT SYSTEMS

10.2.1.1

HELP REDUCE FUEL USAGE

10.2.2

THRUST REVERSER SYSTEMS

10.2.2.1

FACILITATE REDUCED BRAKE WEAR

10.3

AIRFRAME SYSTEMS

10.3.1

ENVIRONMENTAL CONTROL SYSTEMS

10.3.1.1

ENSURE COMFORTABLE CABIN ENVIRONMENT

10.3.2

ACCESSORY DRIVE SYSTEMS

10.3.2.1

HELP INCREASE POWER TRANSMISSION CAPABILITIES

10.3.3

POWER MANAGEMENT SYSTEMS

10.3.3.1

INCREASE ENERGY EFFICIENCY IN AIRCRAFT

10.3.4

CABIN INTERIOR SYSTEMS

10.3.4.1

USED TO ENHANCE CUSTOMER EXPERIENCE

10.3.5

FLIGHT CONTROL SYSTEMS

10.3.5.1

EMPLOYED TO CONTROL AIRCRAFT DIRECTION

10.3.6

LANDING GEAR SYSTEMS

10.3.6.1

FACILITATE TAKE-OFF AND LANDING

11

MORE ELECTRIC AIRCRAFT MARKET, BY COMPONENT

Market Size & Growth Rate Forecast Analysis to 2029 in USD Million | 12 Data Tables

115

11.1

INTRODUCTION

11.2

POWER SOURCES

11.2.1

BATTERIES

11.2.1.1

NICKEL-BASED BATTERIES

11.2.1.1.1

HIGH CAPACITY AND QUICK-CHARGING CAPABILITIES

11.2.1.2

LEAD-ACID BATTERIES

11.2.1.2.1

INCREASING USE DUE TO LOW COST AND LIMITED MAINTENANCE

11.2.1.3

LITHIUM-BASED BATTERIES

11.2.1.3.1

WIDE ADOPTION IN FUTURISTIC APPLICATIONS REQUIRING HIGH ENERGY DENSITY AND LOW WEIGHT

11.2.2

FUEL CELLS

11.2.2.1

INCREASE EFFICIENCY AND HELP TO REDUCE FUEL LOAD

11.2.3

SOLAR CELLS

11.2.3.1

ELIMINATE REQUIREMENT FOR LIQUID FUEL

11.3

ACTUATORS

11.3.1

ELECTRIC

11.3.2

OFFER GREATER RELIABILITY

11.3.3

HYBRID ELECTRIC

11.3.4

HELP SAVE ENERGY

11.3.4.1

ELECTRO-HYDROSTATIC ACTUATORS (EHA)

11.3.4.2

ELECTRO-MECHANICAL ACTUATORS (EMA)

11.3.4.3

ELECTRICAL-BACKUP HYDRAULIC ACTUATORS

11.4

ELECTRIC PUMPS

11.4.1

SUITED TO NEXT-GENERATION AIRCRAFT

11.5

POWER ELECTRONICS

11.5.1

RECTIFIERS

11.5.1.1

USED FOR AC TO DC CONVERSION

11.5.2

INVERTERS

11.5.2.1

FACILITATE DC TO AC CONVERSION

11.5.3

CONVERTERS

11.5.3.1

PROVIDE HIGH-QUALITY DC ELECTRICAL POWER FOR AEROSPACE NETWORKS

11.6

DISTRIBUTION DEVICES

11.6.1

WIRES & CABLES

11.6.1.1

INCREASING DEMAND DUE TO SHIFT TOWARD MORE ELECTRIC AIRCRAFT

11.6.2

CONNECTORS & CONNECTOR ACCESSORIES

11.6.2.1

RISING NEED FOR WELL-CONNECTED WIRING SYSTEMS TO BOOST DEMAND

11.6.3

BUSBARS

11.6.3.1

EASY INSTALLATION TO INCREASE ADOPTION

11.7

GENERATORS

11.7.1

STARTER GENERATORS

11.7.1.1

ACTS AS PARALLEL ELECTRICAL POWER SUPPLY UNITS

11.7.2

AUXILIARY POWER UNITS (APU)

11.7.2.1

PROVIDE BACK-UP ELECTRICAL SUPPLY FOR AIRCRAFT

11.7.3

VARIABLE SPEED CONSTANT FREQUENCY (VSCF) GENERATORS

11.7.3.1

OFFER MORE FLEXIBLE ELECTRICAL SYSTEM ARCHITECTURE

11.8

VALVES

11.8.1

REGULATE GAS LEVELS IN MEA ENGINES

12

MORE ELECTRIC AIRCRAFT MARKET, BY REGION

Comprehensive coverage of 7 Regions with country-level deep-dive of 17 Countries | 228 Data Tables.

126

12.1

INTRODUCTION

12.2

NORTH AMERICA

12.2.1

NORTH AMERICA: PESTLE ANALYSIS

12.2.2

US

12.2.2.1

PRESENCE OF LEADING OEMS TO DRIVE MARKET

12.2.3

CANADA

12.2.3.1

INCREASING R&D ACTIVITIES TO BOOST MARKET

12.3

EUROPE

12.3.1

EUROPE: PESTLE ANALYSIS

12.3.2

UK

12.3.2.1

PRESENCE OF PROMINENT AIRCRAFT OEMS TO FUEL MARKET

12.3.3

FRANCE

12.3.3.1

HIGH INVESTMENTS IN AEROSPACE INDUSTRY TO DRIVE MARKET

12.3.4

GERMANY

12.3.4.1

DEVELOPMENTS IN ELECTRIC PROPULSION TECHNOLOGIES TO DRIVE DEMAND

12.3.5

RUSSIA

12.3.5.1

GROWING AVIATION SECTOR TO BOOST MARKET

12.3.6

ITALY

12.3.6.1

INCREASING DEMAND FOR AIRCRAFT TO FUEL MARKET

12.3.7

REST OF EUROPE

12.4

ASIA PACIFIC

12.4.1

ASIA PACIFIC: PESTLE ANALYSIS

12.4.2

CHINA

12.4.2.1

GROWING DEMAND FOR AEROSPACE PRODUCTS TO FUEL MARKET

12.4.3

INDIA

12.4.3.1

RAPIDLY EXPANDING AVIATION SECTOR TO SPUR MARKET GROWTH

12.4.4

JAPAN

12.4.4.1

INCREASING IN-HOUSE DEVELOPMENT OF AIRCRAFT TO DRIVE DEMAND

12.4.5

SOUTH KOREA

12.4.5.1

PRESENCE OF ELECTRIC COMPONENT MANUFACTURERS TO SUPPORT MARKET

12.4.6

AUSTRALIA

12.4.6.1

INCREASING AIR TRAFFIC TO BOOST DEMAND

12.4.7

REST OF ASIA PACIFIC

12.5

MIDDLE EAST & AFRICA

12.5.1

MIDDLE EAST & AFRICA: PESTLE ANALYSIS

12.5.2

UAE

12.5.2.1

PRESENCE OF LEADING GLOBAL AIRLINES TO DRIVE MARKET

12.5.3

SAUDI ARABIA

12.5.3.1

SIGNIFICANT GROWTH IN ADVANCED POWER ELECTRONICS TO DRIVE MARKET

12.5.4

ISRAEL

12.5.4.1

GROWING NEED TO RAMP UP AIRCRAFT FLEET TO ACCELERATE MARKET

12.5.5

SOUTH AFRICA

12.5.5.1

EXPANDING TOURISM SECTOR TO FUEL MARKET

12.5.6

REST OF MIDDLE EAST & AFRICA

12.6

LATIN AMERICA

12.6.1

LATIN AMERICA: PESTLE ANALYSIS

12.6.2

BRAZIL

12.6.2.1

PRESENCE OF LEADING AIRLINES TO BOOST MARKET

12.6.3

MEXICO

12.6.3.1

GOVERNMENT INITIATIVES TO DRIVE MARKET

12.6.4

REST OF LATIN AMERICA

13

COMPETITIVE LANDSCAPE

Uncover top strategies and market dominance of key players and startups in electric aircraft.

204

13.1

INTRODUCTION

13.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020–2024

13.3

RANKING ANALYSIS

13.4

REVENUE ANALYSIS OF TOP 5 PLAYERS, 2020–2023

13.5

MARKET SHARE ANALYSIS, 2023

13.6

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

13.6.1

STARS

13.6.2

EMERGING LEADERS

13.6.3

PERVASIVE PLAYERS

13.6.4

PARTICIPANTS

13.6.5

COMPANY FOOTPRINT

13.7

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

13.7.1

PROGRESSIVE COMPANIES

13.7.2

RESPONSIVE COMPANIES

13.7.3

DYNAMIC COMPANIES

13.7.4

STARTING BLOCKS

13.7.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

13.8

COMPANY VALUATION AND FINANCIAL METRICS

13.9

BRAND/PRODUCT COMPARISON

13.10

COMPETITIVE SCENARIO

13.10.1

PRODUCT LAUNCHES

13.10.2

DEALS

14

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

228

14.1

INTRODUCTION

14.2

KEY PLAYERS

14.2.1

SAFRAN S.A.

14.2.1.1

BUSINESS OVERVIEW

14.2.1.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

14.2.1.3

RECENT DEVELOPMENTS

14.2.1.3.1

DEALS

14.2.1.4

MNM VIEW

14.2.1.4.1

KEY STRENGTHS

14.2.1.4.2

STRATEGIC CHOICES

14.2.1.4.3

WEAKNESSES AND COMPETITIVE THREATS

14.2.2

HONEYWELL INTERNATIONAL, INC.

14.2.3

RTX

14.2.4

GENERAL ELECTRIC

14.2.5

PARKER HANNIFIN CORPORATION

14.2.6

BAE SYSTEMS PLC

14.2.7

BOMBARDIER INC.

14.2.8

EMBRAER S.A.

14.2.9

LIEBHERR

14.2.10

AMETEK, INC.

14.2.11

NABTESCO CORPORATION

14.2.12

MOOG INC.

14.2.13

ASTRONICS CORPORATION

14.2.14

ROLLS-ROYCE PLC

14.2.15

EATON

14.2.16

AMPHENOL CORPORATION

14.3

OTHER PLAYERS

14.3.1

PBS AEROSPACE

14.3.2

AVIONIC INSTRUMENTS, LLC

14.3.3

EAGLEPICHER TECHNOLOGIES LLC

14.3.4

PIONEER MAGNETICS

14.3.5

WRIGHT ELECTRIC

14.3.6

MAGNIX

14.3.7

RADIANT POWER CORPORATION

14.3.8

AMPAIRE

14.3.9

WOODWARD

15

APPENDIX

281

15.1

DISCUSSION GUIDE

15.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

15.3

CUSTOMIZATION OPTIONS

15.4

RELATED REPORTS

15.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

MORE ELECTRIC AIRCRAFT MARKET: INCLUSIONS AND EXCLUSIONS

TABLE 2

USD EXCHANGE RATES

TABLE 3

KEY PRIMARY SOURCES

TABLE 4

MORE ELECTRIC AIRCRAFT MARKET: ROLE OF COMPANIES IN ECOSYSTEM

TABLE 5

AVERAGE SELLING PRICING RANGE FOR HYBRID ACTUATORS, 2023 (USD)

TABLE 6

AVERAGE SELLING PRICE RANGE, BY PLATFORM (USD MILLION), 2023

TABLE 7

MORE ELECTRIC AIRCRAFT: VOLUME DATA, BY AIRCRAFT TYPE

TABLE 8

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF END USERS (%)

TABLE 9

KEY BUYING CRITERIA FOR END USERS

TABLE 10

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 11

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 12

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 13

MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 14

LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 15

MORE ELECTRIC MARKET: CONFERENCES AND EVENTS, 2024–2025

TABLE 16

MORE ELECTRIC AIRCRAFT MARKET: TOTAL COST OF OWNERSHIP

TABLE 17

PENETRATION OF ELECTRICAL SYSTEMS, BY AIRCRAFT TYPE

TABLE 18

TYPES OF ADVANCED AIRCRAFT BATTERIES: COMPARATIVE STUDY

TABLE 19

MORE ELECTRIC AIRCRAFT MARKET: INNOVATIONS AND PATENT REGISTRATIONS, 2020–2023

TABLE 20

MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 21

MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 22

MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 23

MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 24

MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 25

MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 26

FIXED-WING: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 27

FIXED-WING: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 28

MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 29

MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 30

PROPULSION SYSTEMS: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2020–2023 (USD MILLION)

TABLE 31

PROPULSION SYSTEMS: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 32

AIRFRAME SYSTEMS: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2020–2023 (USD MILLION)

TABLE 33

AIRFRAME SYSTEMS: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 34

MORE ELECTRIC AIRCRAFT MARKET, BY COMPONENT, 2020–2023 (USD MILLION)

TABLE 35

MORE ELECTRIC AIRCRAFT MARKET, BY COMPONENT, 2024–2029 (USD MILLION)

TABLE 36

ACTUATORS: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2020–2023 (USD MILLION)

TABLE 37

ACTUATORS: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 38

HYBRID ELECTRIC: MORE ELECTRIC AIRCRAFT MARKET FOR ACTUATORS, BY TYPE, 2020–2023 (USD MILLION)

TABLE 39

HYBRID ELECTRIC: MORE ELECTRIC AIRCRAFT MARKET FOR ACTUATORS, BY TYPE, 2024–2029 (USD MILLION)

TABLE 40

POWER ELECTRONICS: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2020–2023(USD MILLION)

TABLE 41

POWER ELECTRONICS: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2024–2029(USD MILLION)

TABLE 42

DISTRIBUTION DEVICES: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2020–2023 (USD MILLION)

TABLE 43

DISTRIBUTION DEVICES: MORE ELECTRIC AIRCRAFT MARKET, BY TYPE, 2024–2029 (USD MILLION)

TABLE 44

GENERATORS: MORE ELECTRIC AIRCRAFT MARKET, BY COMPONENT, 2020–2023 (USD MILLION)

TABLE 45

GENERATORS: MORE ELECTRIC AIRCRAFT MARKET, BY COMPONENT, 2024–2029 (USD MILLION)

TABLE 46

MORE ELECTRIC AIRCRAFT MARKET, BY REGION, 2020–2023 (USD MILLION)

TABLE 47

MORE ELECTRIC AIRCRAFT MARKET, BY REGION, 2024–2029 (USD MILLION)

TABLE 48

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 49

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 50

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 51

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 52

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 53

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 54

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 55

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 56

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 57

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 58

US: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 59

US: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 60

US: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 61

US: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 62

US: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 63

US: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 64

US: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 65

US: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 66

CANADA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 67

CANADA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 68

CANADA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 69

CANADA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 70

CANADA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 71

CANADA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 72

CANADA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 73

CANADA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 74

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 75

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 76

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 77

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 78

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 79

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 80

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 81

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 82

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 83

EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 84

UK: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 85

UK: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 86

UK: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 87

UK: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 88

UK: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 89

UK: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 90

UK: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 91

UK: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 92

FRANCE: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 93

FRANCE: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 94

FRANCE: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 95

FRANCE: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 96

FRANCE: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 97

FRANCE: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 98

FRANCE: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 99

FRANCE: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 100

GERMANY: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 101

GERMANY: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 102

GERMANY: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 103

GERMANY: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 104

GERMANY: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 105

GERMANY: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 106

GERMANY: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 107

GERMANY: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 108

RUSSIA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 109

RUSSIA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 110

RUSSIA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 111

RUSSIA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 112

RUSSIA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 113

RUSSIA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 114

RUSSIA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 115

RUSSIA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 116

ITALY: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 117

ITALY: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 118

ITALY: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 119

ITALY: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 120

ITALY: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 121

ITALY: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 122

ITALY: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 123

ITALY: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 124

REST OF EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 125

REST OF EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 126

REST OF EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 127

REST OF EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 128

REST OF EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 129

REST OF EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 130

REST OF EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 131

REST OF EUROPE: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 132

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 133

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 134

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 135

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 136

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 137

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 138

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 139

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 140

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 141

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 142

CHINA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 143

CHINA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 144

CHINA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 145

CHINA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 146

CHINA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 147

CHINA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 148

CHINA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 149

CHINA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 150

INDIA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 151

INDIA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 152

INDIA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 153

INDIA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 154

INDIA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 155

INDIA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 156

INDIA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 157

INDIA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 158

JAPAN: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 159

JAPAN: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 160

JAPAN: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 161

JAPAN: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 162

JAPAN: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 163

JAPAN: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 164

JAPAN: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 165

JAPAN: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 166

SOUTH KOREA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 167

SOUTH KOREA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 168

SOUTH KOREA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 169

SOUTH KOREA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 170

SOUTH KOREA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 171

SOUTH KOREA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 172

SOUTH KOREA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 173

SOUTH KOREA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 174

AUSTRALIA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 175

AUSTRALIA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 176

AUSTRALIA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 177

AUSTRALIA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 178

AUSTRALIA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 179

AUSTRALIA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 180

AUSTRALIA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 181

AUSTRALIA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 182

REST OF ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 183

REST OF ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 184

REST OF ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 185

REST OF ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 186

REST OF ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 187

REST OF ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 188

REST OF ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 189

REST OF ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 190

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 191

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 192

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 193

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 194

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 195

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 196

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 197

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 198

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 199

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 200

UAE: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 201

UAE: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 202

UAE: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 203

UAE: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 204

UAE: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 205

UAE: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 206

UAE: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 207

UAE: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 208

SAUDI ARABIA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 209

SAUDI ARABIA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 210

SAUDI ARABIA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 211

SAUDI ARABIA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 212

SAUDI ARABIA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 213

SAUDI ARABIA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 214

SAUDI ARABIA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 215

SAUDI ARABIA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 216

ISRAEL: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 217

ISRAEL: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 218

ISRAEL: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 219

ISRAEL: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 220

ISRAEL: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 221

ISRAEL: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 222

ISRAEL: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 223

ISRAEL: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 224

SOUTH AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 225

SOUTH AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 226

SOUTH AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 227

SOUTH AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 228

SOUTH AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 229

SOUTH AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 230

SOUTH AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 231

SOUTH AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 232

REST OF MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 233

REST OF MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 234

REST OF MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 235

REST OF MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 236

REST OF MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 237

REST OF MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 238

REST OF MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 239

REST OF MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 240

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 241

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 242

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 243

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 244

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 245

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 246

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 247

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 248

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2020–2023 (USD MILLION)

TABLE 249

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY COUNTRY, 2024–2029 (USD MILLION)

TABLE 250

BRAZIL: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 251

BRAZIL: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 252

BRAZIL: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 253

BRAZIL: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 254

BRAZIL: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 255

BRAZIL: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 256

BRAZIL: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 257

BRAZIL: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 258

MEXICO: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 259

MEXICO: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 260

MEXICO: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 261

MEXICO: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 262

MEXICO: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 263

MEXICO: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 264

MEXICO: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 265

MEXICO: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 266

REST OF LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2020–2023 (USD MILLION)

TABLE 267

REST OF LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

TABLE 268

REST OF LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2020–2023 (USD MILLION)

TABLE 269

REST OF LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

TABLE 270

REST OF LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2020–2023 (USD MILLION)

TABLE 271

REST OF LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

TABLE 272

REST OF LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2020–2023 (USD MILLION)

TABLE 273

REST OF LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

TABLE 274

KEY DEVELOPMENTS BY LEADING MARKET PLAYERS, JANUARY 2020–SEPTEMBER 2024

TABLE 275

MORE ELECTRIC AIRCRAFT MARKET: DEGREE OF COMPETITION

TABLE 276

END USER FOOTPRINT

TABLE 277

SYSTEM FOOTPRINT

TABLE 278

REGION FOOTPRINT

TABLE 279

MORE ELECTRIC AIRCRAFT MARKET: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 280

MORE ELECTRIC AIRCRAFT MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 281

MORE ELECTRIC AIRCRAFT MARKET: PRODUCT LAUNCHES, JANUARY 2020–SEPTEMBER 2024

TABLE 282

MORE ELECTRIC AIRCRAFT MARKET: DEALS, JANUARY 2020–SEPTEMBER 2024

TABLE 283

MORE ELECTRIC AIRCRAFT: OTHER DEVELOPMENTS, JANUARY 2020–SEPTEMBER 2024

TABLE 284

SAFRAN S.A.: COMPANY OVERVIEW

TABLE 285

SAFRAN S.A.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 286

SAFRAN S.A.: DEALS

TABLE 287

HONEYWELL INTERNATIONAL, INC.: COMPANY OVERVIEW

TABLE 288

HONEYWELL INTERNATIONAL, INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 289

HONEYWELL INTERNATIONAL, INC.: PRODUCT LAUNCHES

TABLE 290

HONEYWELL INTERNATIONAL, INC.: DEALS

TABLE 291

HONEYWELL INTERNATIONAL, INC.: OTHER DEVELOPMENTS

TABLE 292

RTX: COMPANY OVERVIEW

TABLE 293

RTX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 294

RTX: DEALS

TABLE 295

RTX: OTHER DEVELOPMENTS

TABLE 296

GENERAL ELECTRIC: COMPANY OVERVIEW

TABLE 297

GENERAL ELECTRIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 298

GENERAL ELECTRIC: DEALS

TABLE 299

GENERAL ELECTRIC: OTHER DEVELOPMENTS

TABLE 300

PARKER HANNIFIN CORPORATION: COMPANY OVERVIEW

TABLE 301

PARKER HANNIFIN CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 302

PARKER HANNIFIN CORPORATION: DEALS

TABLE 303

BAE SYSTEMS PLC: COMPANY OVERVIEW

TABLE 304

BAE SYSTEMS PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 305

BAE SYSTEMS PLC: OTHER DEVELOPMENTS

TABLE 306

BOMBARDIER INC.: COMPANY OVERVIEW

TABLE 307

BOMBARDIER INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 308

EMBRAER S.A.: COMPANY OVERVIEW

TABLE 309

EMBRAER S.A.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 310

LIEBHERR: COMPANY OVERVIEW

TABLE 311

LIEBHERR: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 312

AMETEK, INC.: COMPANY OVERVIEW

TABLE 313

AMETEK, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 314

AMETEK, INC.: DEALS

TABLE 315

NABTESCO CORPORATION: COMPANY OVERVIEW

TABLE 316

NABTESCO CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 317

MOOG INC.: COMPANY OVERVIEW

TABLE 318

MOOG INC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 319

MOOG INC.: DEALS

TABLE 320

ASTRONICS CORPORATION: COMPANY OVERVIEW

TABLE 321

ASTRONICS CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 322

ASTRONICS CORPORATION: OTHER DEVELOPMENTS

TABLE 323

ROLLS-ROYCE PLC: COMPANY OVERVIEW

TABLE 324

ROLLS-ROYCE PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 325

ROLLS-ROYCE PLC: PRODUCT LAUNCHES

TABLE 326

EATON: COMPANY OVERVIEW

TABLE 327

EATON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 328

AMPHENOL CORPORATION: COMPANY OVERVIEW

TABLE 329

AMPHENOL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 330

PBS AEROSPACE: COMPANY OVERVIEW

TABLE 331

AVIONIC INSTRUMENTS, LLC: COMPANY OVERVIEW

TABLE 332

EAGLEPICHER TECHNOLOGIES LLC: COMPANY OVERVIEW

TABLE 333

PIONEER MAGNETICS: COMPANY OVERVIEW

TABLE 334

WRIGHT ELECTRIC: COMPANY OVERVIEW

TABLE 335

MAGNIX: COMPANY OVERVIEW

TABLE 336

RADIANT POWER CORPORATION: COMPANY OVERVIEW

TABLE 337

AMPAIRE: COMPANY OVERVIEW

TABLE 338

WOODWARD: COMPANY OVERVIEW

LIST OF FIGURES

FIGURE 1

YEARS CONSIDERED

FIGURE 2

MORE ELECTRIC AIRCRAFT MARKET: RESEARCH PROCESS FLOW

FIGURE 3

MORE ELECTRIC AIRCRAFT MARKET: RESEARCH DESIGN

FIGURE 4

BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

FIGURE 5

RESEARCH METHODOLOGY

FIGURE 6

MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

FIGURE 7

MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

FIGURE 8

DATA TRIANGULATION

FIGURE 9

ASSUMPTIONS FOR RESEARCH STUDY

FIGURE 10

AUXILIARY POWER UNITS (APU) SEGMENT TO DOMINATE MORE ELECTRIC AIRCRAFT MARKET FOR GENERATORS DURING FORECAST PERIOD

FIGURE 11

RECTIFIERS SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE FROM 2024 TO 2029

FIGURE 12

HYBRID ELECTRIC SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 13

EUROPE TO ACCOUNT FOR LARGEST SHARE OF MORE ELECTRIC AIRCRAFT MARKET IN 2024

FIGURE 14

TECHNOLOGICAL ADVANCEMENTS IN POWER ELECTRONICS TO DRIVE MARKET

FIGURE 15

POWER DISTRIBUTION SEGMENT TO ACCOUNT FOR LARGEST MARKET SIZE DURING FORECAST PERIOD

FIGURE 16

CIVIL SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 17

PROPULSION SYSTEMS SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

FIGURE 18

SOUTH KOREA, RUSSIA, AND GERMANY TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 19

MORE ELECTRIC AIRCRAFT MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 20

REVENUE SHIFTS IN MORE ELECTRIC AIRCRAFT MARKET

FIGURE 21

MORE ELECTRIC AIRCRAFT MARKET: VALUE CHAIN ANALYSIS

FIGURE 22

MORE ELECTRIC AIRCRAFT MARKET: ECOSYSTEM MAP

FIGURE 23

AVERAGE SELLING PRICE RANGE, BY COMPONENT

FIGURE 24

AVERAGE SELLING PRICE RANGE FOR HYBRID ACTUATORS, 2023

FIGURE 25

MORE ELECTRIC AIRCRAFT MARKET: INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF END USERS

FIGURE 26

MORE ELECTRIC AIRCRAFT MARKET: KEY BUYING CRITERIA FOR END USERS

FIGURE 27

IMPORT DATA OF HS CODE 8802, BY COUNTRY, 2020–2023 (USD THOUSAND)

FIGURE 28

EXPORT DATA OF HS CODE 8802, BY COUNTRY, 2020–2023 (USD THOUSAND)

FIGURE 29

MORE ELECTRIC AIRCRAFT MARKET: TOTAL COST OF OWNERSHIP

FIGURE 30

INVESTMENT AND FUNDING SCENARIO, 2020–2024

FIGURE 31

EVOLUTION OF MORE ELECTRIC TECHNOLOGIES

FIGURE 32

ADOPTION OF MORE ELECTRIC TECHNOLOGIES

FIGURE 33

AI IN AVIATION

FIGURE 34

ADOPTION OF AI IN AVIATION BY TOP COUNTRIES

FIGURE 35

IMPACT OF AI ON MORE ELECTRIC AIRCRAFT COMPONENTS

FIGURE 36

IMPACT OF AI ON MORE ELECTRIC AIRCRAFT MARKET

FIGURE 37

MORE ELECTRIC AIRCRAFT MARKET: SUPPLY CHAIN ANALYSIS

FIGURE 38

PATENT ANALYSIS, 2013–2023

FIGURE 39

MORE ELECTRIC AIRCRAFT MARKET, BY END USER, 2024–2029 (USD MILLION)

FIGURE 40

MORE ELECTRIC AIRCRAFT MARKET, BY APPLICATION, 2024–2029 (USD MILLION)

FIGURE 41

MORE ELECTRIC AIRCRAFT MARKET, BY PLATFORM, 2024–2029 (USD MILLION)

FIGURE 42

MORE ELECTRIC AIRCRAFT MARKET, BY SYSTEM, 2024–2029 (USD MILLION)

FIGURE 43

MORE ELECTRIC AIRCRAFT MARKET, BY COMPONENT, 2024–2029 (USD MILLION)

FIGURE 44

EUROPE TO ACCOUNT FOR LARGEST SHARE OF MORE ELECTRIC AIRCRAFT MARKET IN 2024

FIGURE 45

NORTH AMERICA: MORE ELECTRIC AIRCRAFT MARKET SNAPSHOT

FIGURE 46

EUROPE: MORE ELECTRIC AIRCRAFT MARKET SNAPSHOT

FIGURE 47

ASIA PACIFIC: MORE ELECTRIC AIRCRAFT MARKET SNAPSHOT

FIGURE 48

MIDDLE EAST & AFRICA: MORE ELECTRIC AIRCRAFT MARKET SNAPSHOT

FIGURE 49

LATIN AMERICA: MORE ELECTRIC AIRCRAFT MARKET SNAPSHOT

FIGURE 50

MARKET RANKING OF KEY PLAYERS, 2023

FIGURE 51

REVENUE ANALYSIS OF TOP 5 PLAYERS, 2020–2023

FIGURE 52

MARKET SHARE ANALYSIS OF MORE ELECTRIC AIRCRAFT MARKET, 2023

FIGURE 53

MORE ELECTRIC AIRCRAFT MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

FIGURE 54

COMPANY FOOTPRINT

FIGURE 55

MORE ELECTRIC AIRCRAFT MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

FIGURE 56

MORE ELECTRIC AIRCRAFT MARKET: COMPANY VALUATION, 2023

FIGURE 57

MORE ELECTRIC AIRCRAFT MARKET: FINANCIAL METRICS, 2023

FIGURE 58

MORE ELECTRIC AIRCRAFT MARKET: PRODUCT COMPARISON OF KEY PLAYERS

FIGURE 59

SAFRAN S.A.: COMPANY SNAPSHOT

FIGURE 60

HONEYWELL INTERNATIONAL, INC.: COMPANY SNAPSHOT

FIGURE 61

RTX: COMPANY SNAPSHOT

FIGURE 62

GENERAL ELECTRIC: COMPANY SNAPSHOT

FIGURE 63

PARKER HANNIFIN CORPORATION: COMPANY SNAPSHOT

FIGURE 64

BAE SYTEMS PLC: COMPANY SNAPSHOT

FIGURE 65

BOMBARDIER INC: COMPANY SNAPSHOT

FIGURE 66

EMBRAER S.A.: COMPANY SNAPSHOT

FIGURE 67

LIEBHERR: COMPANY SNAPSHOT

FIGURE 68

AMETEK, INC.: COMPANY SNAPSHOT

FIGURE 69

MOOG INC.: COMPANY SNAPSHOT

FIGURE 70

ASTRONICS CORPORATION: COMPANY SNAPSHOT

FIGURE 71

ROLLS-ROYCE PLC: COMPANY SNAPSHOT

FIGURE 72

EATON: COMPANY SNAPSHOT

FIGURE 73

AMPHENOL CORPORATION: COMPANY SNAPSHOT

Methodology

This research study on the more electric aircraft market involved the extensive use of secondary sources, directories, and databases such as D&B Hoovers, Bloomberg BusinessWeek, and Factiva to identify and collect information relevant to the market. Primary sources considered included industry experts, service providers, manufacturers, solution providers, technology developers, alliances, and organizations related to all segments of this industry's value chain. In-depth interviews with various primary respondents, including key industry participants, subject matter experts (SMEs), industry consultants, and C-level executives, were conducted to obtain and verify critical qualitative and quantitative information about the market and assess its growth prospects.

Secondary Research

The ranking analysis of companies in the more electric aircraft market was determined using secondary data from paid and unpaid sources and analyzing the product portfolios and service offerings of major companies operating in the market. These companies were rated based on the performance and quality of their products. Primary sources further validated these data points.

Secondary sources for this research study included financial statements of companies offering aircraft electric components for all technology stages, such as more electric aircraft, hybrid electric aircraft, and fully electric aircraft, along with various trade, business, and professional associations. The secondary data was collected and analyzed to determine the market's overall size, which primary respondents validated.

Primary Research

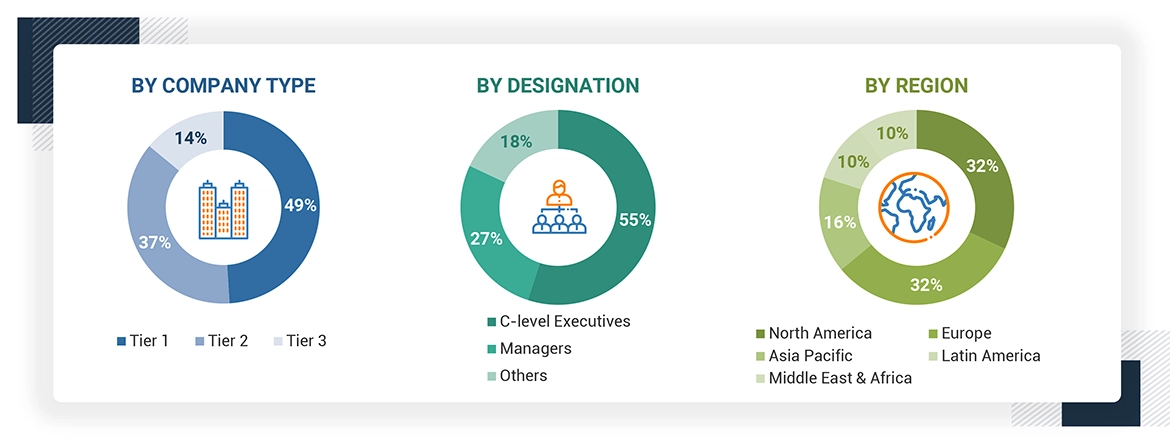

Through secondary research, extensive primary research was conducted after obtaining information about the more electric aircraft market's current scenario. Several primary interviews were conducted with market experts from both the demand and supply sides across five regions: North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America. This primary data was collected through questionnaires, emails, and telephonic interviews.

Note: C-level Executives include the CEO, COO, and CTO, among others.

*Others include Sales Managers, Marketing Managers, and Product Managers.

The tiers of the companies have been defined based on their total revenue as of 2022.

Tier 1 = > USD 1 billion, Tier 2 = USD 100 million to USD 1 billion, and Tier 3 = < USD 100 million.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

The top-down and bottom-up approaches have been used to estimate and validate the more electric aircraft market size. The following figure in this subsection represents the overall market size estimation process employed for this study.

The research methodology used to estimate the market size also includes the following details:

- Key players in the market have been identified through secondary research, and their market shares have been determined through primary and secondary research. This included a study of annual and financial reports of the top market players and extensive interviews with leaders, including CEOs, directors, and marketing executives.

- All percentage shares split and breakdowns have been determined using secondary sources and verified through primary sources.

- All possible parameters that affect the markets covered in this study have been accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data.

This data has been consolidated, added with detailed inputs, analyzed by MarketsandMarkets, and presented in this report.

In the top-down approach, the overall market size has been used to estimate the size of individual subsegments (mentioned in the market segmentation) through percentage splits acquired from secondary and primary research. For the calculation of specific market segments, the most appropriate immediate parent market size has been used to implement the top-down approach. The bottom-up approach has been implemented to validate the market segment revenues obtained.

Market shares have been estimated for each company to verify the revenue shares used earlier in the bottom-up approach. With data triangulation and validation of data through primaries, the overall parent market size and each market size have been determined and confirmed in this study. The data triangulation used for this study is explained in the next section.

Data Triangulation

After arriving at the overall market size from the market size estimation process, the total market has been split into several segments and subsegments. In order to complete the overall market engineering process and arrive at the exact statistics for market segments and subsegments, data triangulation and market breakdown procedures explained below have been implemented, wherever applicable. The data has been triangulated by studying various factors and trends from both the demand and supply sides. Additionally, the market size has been validated using both top-down and bottom-up approaches.

Market Definition

More electric aircraft (MEA) is a concept that involves the use of electric power (as opposed to pneumatic and hydraulic sources of power) for all non-propulsive systems in an aircraft. The use of electric power helps reduce the overall weight, fuel consumption, and greenhouse emissions of an aircraft. Electrical systems also help cut down the assembly and maintenance costs of aircraft and facilitate faster manufacturing.

Stakeholders

- Airport developers

- Software developers

- Research bodies.

- Governmental bodies

- More electric aircraft system manufacturers

- More electric aircraft regulators

- Investors and financial community professionals

- Ministry of Defense of relevant nations

- Technology support providers

- Software/hardware/service and solution providers

Report Objectives

- To define, describe, segment, and forecast the size of the more electric aircraft market based on system, component, application, platform, end user, and region.

- To forecast the size of various segments of the market with respect to five major regions, namely North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, along with major countries in each of these regions.

- To identify and analyze key drivers, restraints, opportunities, and challenges influencing the growth of the market across the globe.

- To identify industry trends, market trends, and technology trends currently prevailing in the market.

- To provide an overview of the regulatory landscape with respect to more electric aircraft regulations across regions

- To analyze micromarkets1 with respect to individual growth trends, prospects, and their contribution to the overall market

- To analyze opportunities in the market for stakeholders by identifying key market trends

- To profile key market players and comprehensively analyze their market share and core competencies2.

- To analyze the degree of competition in the market by identifying key growth strategies, such as, agreements, acquisitions, contracts, and partnerships, adopted by leading market players.

- To identify detailed financial positions, key products, and unique selling points of leading companies in the market

- To provide a detailed competitive landscape of the market, along with market ranking analysis, market share analysis, and revenue analysis of key players

Key Questions Addressed by the Report

What is the current size of the more electric aircraft market?

The more electric aircraft market is projected to grow from USD 5.56 Billion in 2024 and reach USD 8.01 Billion by 2029 at a CAGR of 7.6% during the forecast period.

Who are the key players in the more electric aircraft market?

Safran S.A ( France), Honeywell International Inc. (US), RTX (US), General Electric (US), Parker Hannifin Corporation (US), Bae Systems plc (UK), Bomardier Inc. (Canada), Embraer S.A (Brazil), Liebherr (Switzerland), Ametek Inc. (US), Astronics Corporation (US), Moog inc. (US), Rolls-Royce Plc (UK), Amphenol Corporation (US), and Eaton (Ireland) are among the key market players.

What are some of the technological advancements in the market?

Liquid cooling systems are increasingly popular in more electric aircraft as they can absorb and transfer heat more effectively than air cooling. Liquid cooling can offer cooling even for high-heat loads, especially in tightly confined areas. It has been commonly applied in high-power electric actuators and inverters where liquid cooling enables the necessary temperature regulation, hence giving reliability to its parts. The electric taxi system (ETS) enables aircraft to taxi around the ground without relying on their main jet engines and using electric motors. Normally, taxis with jet engines consume much fuel even when proceeding at low speeds between a gate and the runway. ETS replaces this function with electrically powered systems, which are usually situated in the wheels of the landing gear, allowing the aircraft to move around with no external tugs or even jet engines.

What are the disruptive trends in the more electric aircraft market?

The more electric aircraft market is witnessing many disruptive trends that are transforming the future of aviation. High-voltage power systems are developing at a breakneck speed, and the transition to 270V and higher voltage architectures is making power distribution much more efficient for aircraft systems. This trend will continue to support the electrification of traditional hydraulic and pneumatic systems, such as flight control, landing gear, and environmental control, to achieve greater efficiency and weight savings. The emergence of advanced battery and energy storage solutions - such as solid-state batteries with significantly higher energy densities and improvements in safety over traditional lithium-ion batteries - is another disrupting trend.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the More Electric Aircraft Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

- Canada More Electric Aircraft Market

- US More Electric Aircraft Market

- UK More Electric Aircraft Market

- France More Electric Aircraft Market

- Germany More Electric Aircraft Market

- Russia More Electric Aircraft Market

- Italy More Electric Aircraft Market

- China More Electric Aircraft Market

- India More Electric Aircraft Market

- Japan More Electric Aircraft Market

- South Korea More Electric Aircraft Market

- Australia More Electric Aircraft Market

- Brazil More Electric Aircraft Market

- Mexico More Electric Aircraft Market

- UAE More Electric Aircraft Market

- Saudi Arabia More Electric Aircraft Market

- Israel More Electric Aircraft Market

- South Africa More Electric Aircraft Market

Growth opportunities and latent adjacency in More Electric Aircraft Market

Gareth

Apr, 2026

Does the study provide insights into electric propulsion, energy storage systems, and power distribution technologies across aircraft platforms?.

Sean

Apr, 2026

Does the report analyze regulatory frameworks and certification challenges impacting electric aircraft adoption globally?.