Download PDF

Download PDF Request Customisation

Request Customisation

Infrared Imaging Market Size, Share & Trends

Report Code

SE 3270

Published in

Jul, 2025, By MarketsandMarkets™

Infrared Imaging Market Size, Share, Growth & Trends by Type (Reflective, Thermal), Wavelength (NIR, SWIR, MWIR, LWIR), Component (Cameras, Scopes, Modules), Technology (Cooled, Uncooled), Application (Condition Monitoring, Detection, Security & Surveillance)- Global Forecast to 2030

USD 11.65 BN

MARKET SIZE, 2030

CAGR 6.2%

(2025-2030)

260

REPORT PAGES

225

MARKET TABLES

INFRARED IMAGING MARKET OVERVIEW

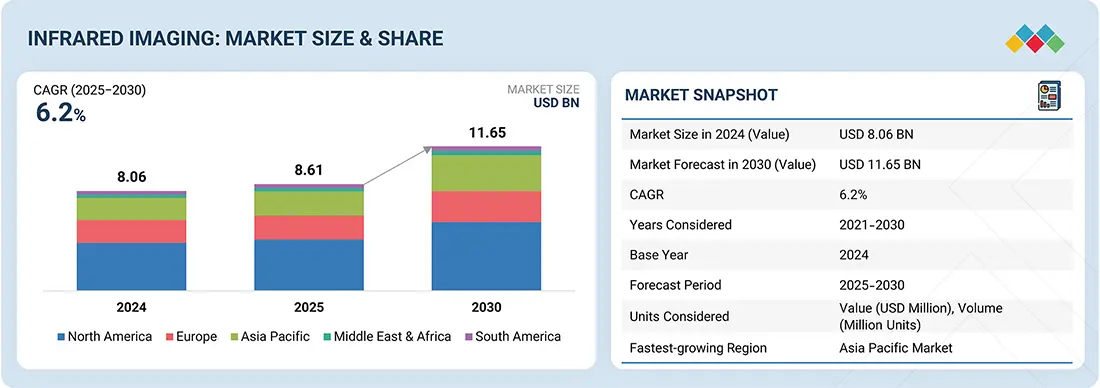

According to Marketsandmarkets, the global infrared imaging market size was valued at USD 8.61 billion in 2025 and is projected to reach USD 11.65 billion by 2030, growing at a CAGR of 6.2% from 2025 to 2030. The infrared imaging market is propelled by rising demand in defence, industrial automation, healthcare diagnostics, and surveillance applications. Growing security threats and the need for enhanced visibility in low-light conditions are accelerating the adoption of thermal imaging across military and law enforcement agencies. In parallel, industries use infrared cameras for predictive maintenance, reducing downtime and improving safety. The Infrared Imaging Market size has been expanding rapidly due to the increasing demand for advanced thermal detection technologies across industries such as defense, healthcare, manufacturing, and security.

The Infrared Imaging Market growth is primarily driven by the rising adoption of thermal cameras for predictive maintenance, surveillance, and medical diagnostics. In recent years, the Infrared Imaging Market share has been influenced by technological advancements in sensor miniaturization and improved image resolution. Additionally, the expanding applications of the IR Camera Market in smart infrastructure, automotive driver assistance systems, and industrial inspection are creating strong momentum for industry expansion. As companies continue investing in research and development, the Infrared IR Sensing Market is expected to experience steady technological innovation and wider commercial adoption.

Furthermore, emerging Infrared Imaging Market trends indicate increasing integration of artificial intelligence and machine learning with thermal imaging systems to improve accuracy and automation. The Infrared Imaging Market growth is also supported by the growing need for contactless temperature monitoring, particularly in healthcare and public safety environments. As a result, the IR Camera Market is witnessing significant demand in sectors such as building inspection, firefighting, and environmental monitoring. At the same time, the Infrared IR Sensing Market is gaining traction in consumer electronics, enabling features like gesture recognition and smart home automation. With continuous advancements in sensor technology and expanding industrial applications, the Infrared Imaging Market size and Infrared Imaging Market share are expected to grow significantly over the coming years.

REPORT SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2025 (Value) | USD 8.61 billion |

| Market Forecast in 2030 (Value) | USD 11.65 Billion |

| Growth Rate | CAGR of 6.2% from 2025–2030 |

| Years Considered | 2021–2030 |

| Base Year | 2024 |

| Forecast Period | 2025–2030 |

| Units Considered | Value (USD Billion) and Volume (Million Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Top Companies |

|

| Growth Drivers |

|

| Segments Covered | By Type: Reflective, Thermal By Component: Camera, Scopes, Modules By Wavelength: NIR, SWIR, MWIR, LWIR By Application: Security & Surveillance, Monitoring & Inspection, Detection By Technology: Cooled, Uncooled By Vertical: Industrial (Aerospace, Electro |

| Regional Scope | North America, Europe, Asia Pacific, and RoW |

Market Size & Forecast

• 2025 Market Size: USD 8.61 billion

• 2030 Projected Market Size: USD 11.65 billion

• CAGR (2025-2030): 6.2%

• Reflective segment: Expected to account the highest CAGR of 7.2%

• North America: Accounted for a 47.1% revenue share

INFRARED IMAGING MARKET KEY TAKEAWAYS

- The North American Infrared Imaging market accounted for a 47.1% revenue share in 2025.

- By Type, the reflective segment is expected to account the highest CAGR of 7.2%

- By Component, the cameras segment is projected to grow at fastest rate from 2025-2030

- By Technology, the uncooled segment is expected to dominate the market

- By Application, the monitoring & inspection segment will grow the fastest during the forecast period

- Teledyne FLIR LLC, Fluke Corporation, and L3 Harris Technologies were identified as star players in the infrared imaging market, as they have focused on innovation and have brought industry coverage and strong operational and financial strength

- Seek Thermal, INFRARED CAMERAS INC., and Tonbo Imaging have distinguished themselves among startups and SMEs due to their strong product portfolio and business strategy

The infrared imaging industry is projected to grow rapidly over the next decade, driven by the demand for infrared imaging systems is driven by the need for accurate, non-contact thermal monitoring across defence, manufacturing, healthcare, and energy sectors. Rising concerns about equipment failures, process inefficiencies, and public safety are prompting industries to deploy infrared imaging solutions for real-time diagnostics and surveillance. Market growth is further supported by increasing investments in smart infrastructure, automation, and advanced safety systems.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

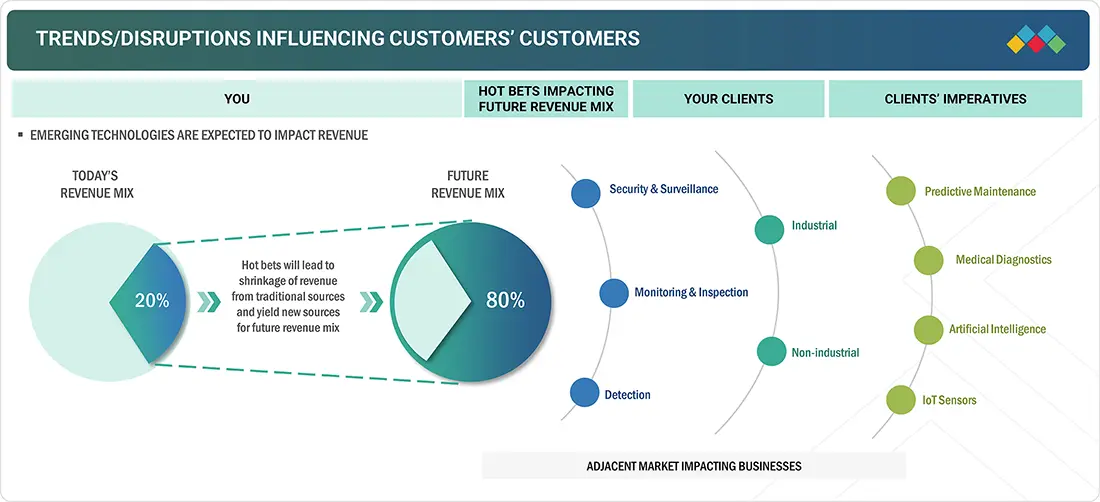

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

Infrared imaging technology captures and visualizes thermal energy emitted by objects and environments, finding extensive use across defence, industrial, and surveillance sectors. Market growth is fuelled by rising adoption in security and surveillance applications, along with the increasing demand for uncooled infrared cameras. Additionally, expanding applications of SWIR cameras and the growing integration of infrared imaging in aerospace systems are creating significant opportunities for industry players.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

INFRARED IMAGING MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Increasing use of infrared imaging products in security & surveillance applications

-

Rising adoption of infrared cameras in quality control and inspection applications

RESTRAINTS

Impact

Level

Level

-

Stringent import and export regulations for selling infrared cameras in US

-

Limitations associated with image resolution and sensitivity of infrared cameras

OPPORTUNITIES

Impact

Level

Level

-

Emerging applications of IR imaging technology in automotive sector

-

Integration of infrared imaging technology into consumer electronics

CHALLENGES

Impact

Level

Level

-

Integration and compatibility challenges pertaining to infrared imaging technology

-

Crafting precision-engineered IR imaging products requires advanced design expertise.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Increasing use of infrared imaging products in security & surveillance applications

The increasing use of infrared imaging products in security and surveillance applications is a significant growth driver for the market. Rising global concerns over safety, border security, and crime prevention fuel demand for advanced imaging solutions. Infrared cameras enable enhanced visibility in low-light or no-light conditions, providing critical support for law enforcement, military, and civilian security operations. This trend is expected to accelerate adoption across both developed and emerging economies.

Restraint: Stringent import and export regulations for selling infrared cameras in US

Stringent import and export regulations in the U.S. for selling infrared cameras pose a significant barrier for market players. Restrictions on advanced infrared technology due to national security concerns limit global trade, making it difficult for manufacturers to expand their international footprint and capitalize on cross-border opportunities.

Opportunity: Emerging applications of IR imaging technology in automotive sector

The automotive sector presents a significant opportunity for infrared imaging technology, particularly with the rise of advanced driver assistance systems (ADAS) and autonomous vehicles. Infrared cameras enhance driver safety by detecting pedestrians, animals, and obstacles in low visibility conditions such as night or fog. Growing investments by automotive OEMs in thermal imaging for collision avoidance, smart navigation, and driver monitoring systems are expected to accelerate demand, creating lucrative avenues for infrared imaging providers worldwide.

Challenge: Integration and compatibility challenges pertaining to infrared imaging technology

Integration and compatibility challenges remain a key hurdle in the infrared imaging market. Aligning infrared systems with existing digital platforms, sensors, and industrial setups requires specialized expertise. High costs of integration and interoperability issues hinder seamless adoption, particularly across emerging industries, slowing down large-scale deployment of infrared imaging solutions.

Infrared Imaging Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Thermal imaging cameras for military surveillance and border security applications | Enhanced threat detection| Real-time monitoring| Improved operational safety in low-visibility conditions |

|

Handheld IR thermography for electrical and mechanical predictive maintenance | Reduced downtime| Early fault identification| Cost savings through preventive repairs |

|

Cooled MWIR/LWIR sensors in aerospace platforms for target acquisition and tracking | High-resolution imaging| Extended detection range| Superior performance in adverse weather |

|

Integrated IR cameras in IP video surveillance systems for perimeter security | 24/7 monitoring| Low-light visibility| Seamless integration with network analytics |

|

Uncooled IR modules for missile guidance and defense electronics | Compact design| Reliable performance|Enhanced accuracy in guidance systems |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

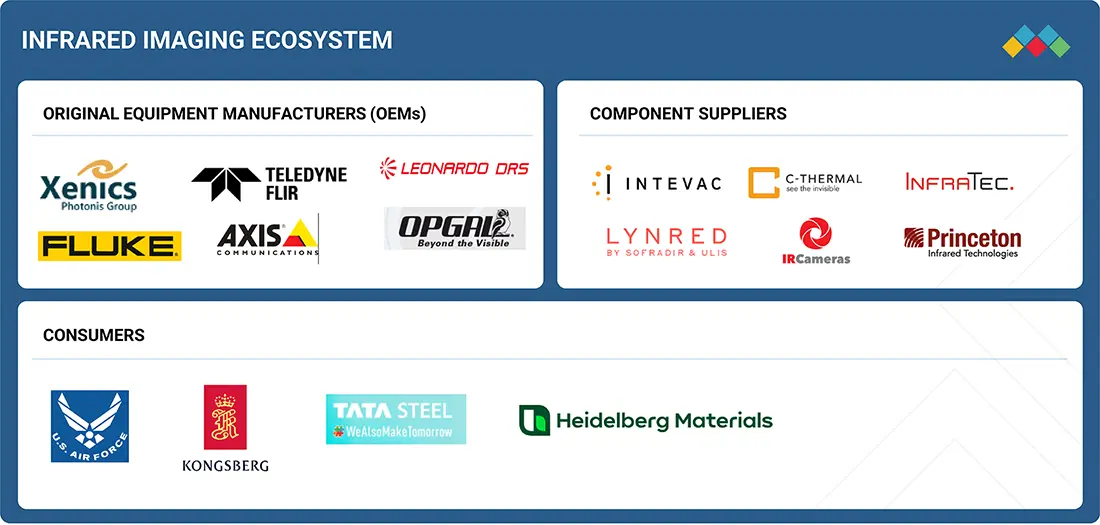

INFRARED IMAGING MARKET ECOSYSTEM

The infrared imaging market ecosystem features a robust network of stakeholders driving innovation in thermal and reflective technologies. OEMs like Xenics, Teledyne FLIR, Leonardo DRS, Fluke, Axis, and Opgal develop integrated imaging solutions for security and industrial applications. Component suppliers, including Intevac, C-Thermal, InfraTec, Lynred, IR Cameras, and Princeton Infrared Technologies, provide essential sensors and lenses. Software providers such as HGH Infrared Systems and New Imaging Technologies enable advanced analytics and AI integration. End consumers, notably the U.S. Air Force and Kongsberg, leverage these for defense, surveillance, and aerospace needs, fostering market growth across sectors.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

INFRARED IMAGING MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Infrared Imaging Market, By Type

The reflective segment is expected to grow at the highest CAGR, driven by its increasing use in scientific research, industrial testing, and material inspection. Its ability to provide high-precision imaging in laboratory and field applications is fuelling adoption, supported by advancements in sensor technology and cost-efficient optical solutions.

Infrared Imaging Market, By Component

The camera segment is projected to hold the largest share, owing to their wide applications in security, defence, industrial inspection, and healthcare. Continuous innovations, miniaturization, and cost reduction of infrared cameras have expanded adoption across industries, while rising demand for surveillance and monitoring in both military and civil applications boosts growth.

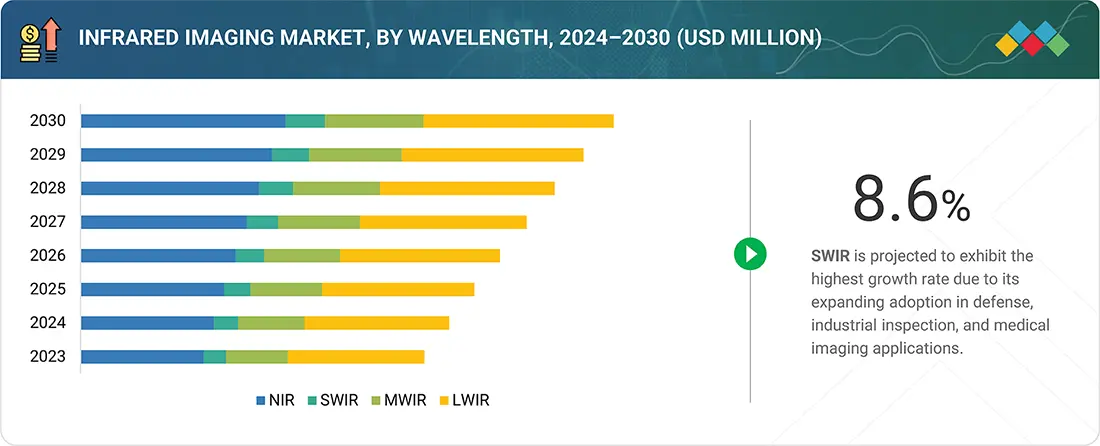

Infrared Imaging Market, By Wavelength

In 2024, the LWIR (Long-Wave Infrared) segment accounted for the largest share, owing to its strong suitability for night vision, surveillance, and thermal monitoring. LWIR cameras operate effectively in total darkness and through atmospheric obscurants, making them essential in defence, security, and industrial inspection applications.

Infrared Imaging Market, By Application

The security & surveillance segment captured the highest market share due to rising global security concerns, border monitoring needs, and critical infrastructure protection. Infrared imaging provides round-the-clock monitoring in low-light or obscured environments. Growing adoption by defence forces, airports, and smart cities initiatives has further accelerated the dominance of this segment.

Infrared Imaging Market, By Technology

The uncooled technology segment captured the highest market share, fuelled by lower costs, compact design, and maintenance-free operation. Uncooled infrared cameras are increasingly deployed in industrial monitoring, firefighting, and commercial surveillance applications, as they provide reliable imaging performance while being energy-efficient and more affordable than cooled counterparts.

Infrared Imaging Market, By Vertical

Between 2025 and 2030, the non-industrial segment is expected to register the highest CAGR, driven by rapid adoption in defence, civil infrastructure, medical, and research applications. In scientific studies, demand for enhanced security, early disease detection, and thermal monitoring will accelerate market growth globally across non-industrial sectors.

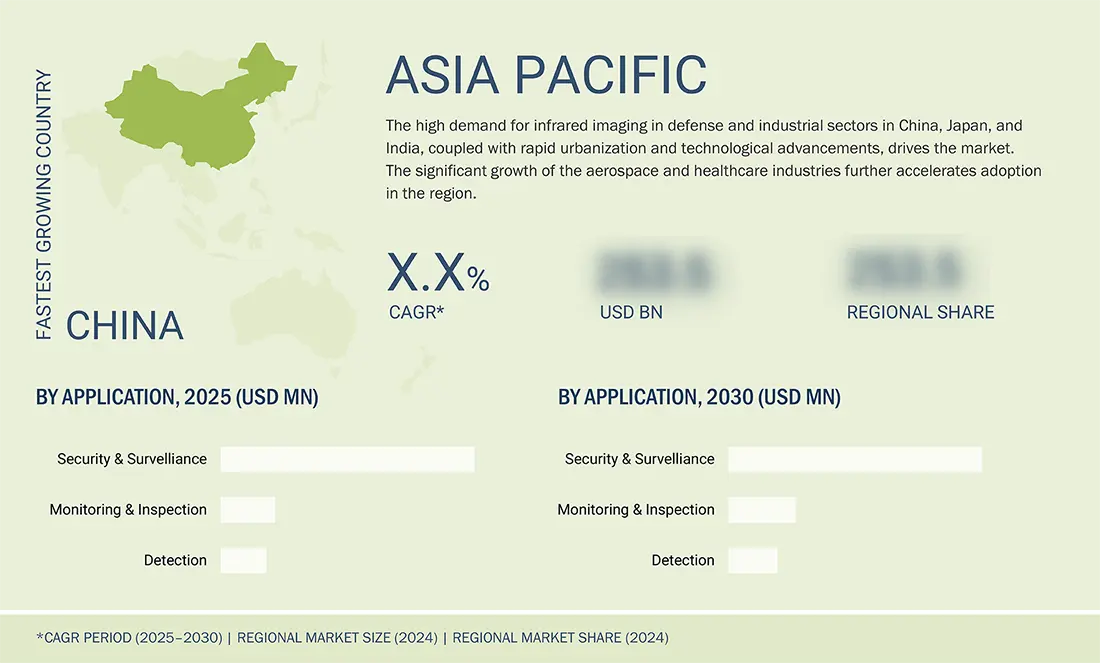

INFRARED IMAGING MARKET BY REGION

Asia Pacific to be the fastest-growing region in the global prinfrared imaging market during the forecast period

The Asia Pacific region is projected to grow at the highest CAGR during the forecast period, driven by increasing defense budgets, rising industrial automation, and the adoption of surveillance solutions in countries like China, India, and Japan. Expanding aerospace, electronics, and semiconductor sectors also contribute significantly to infrared imaging demand in the region.

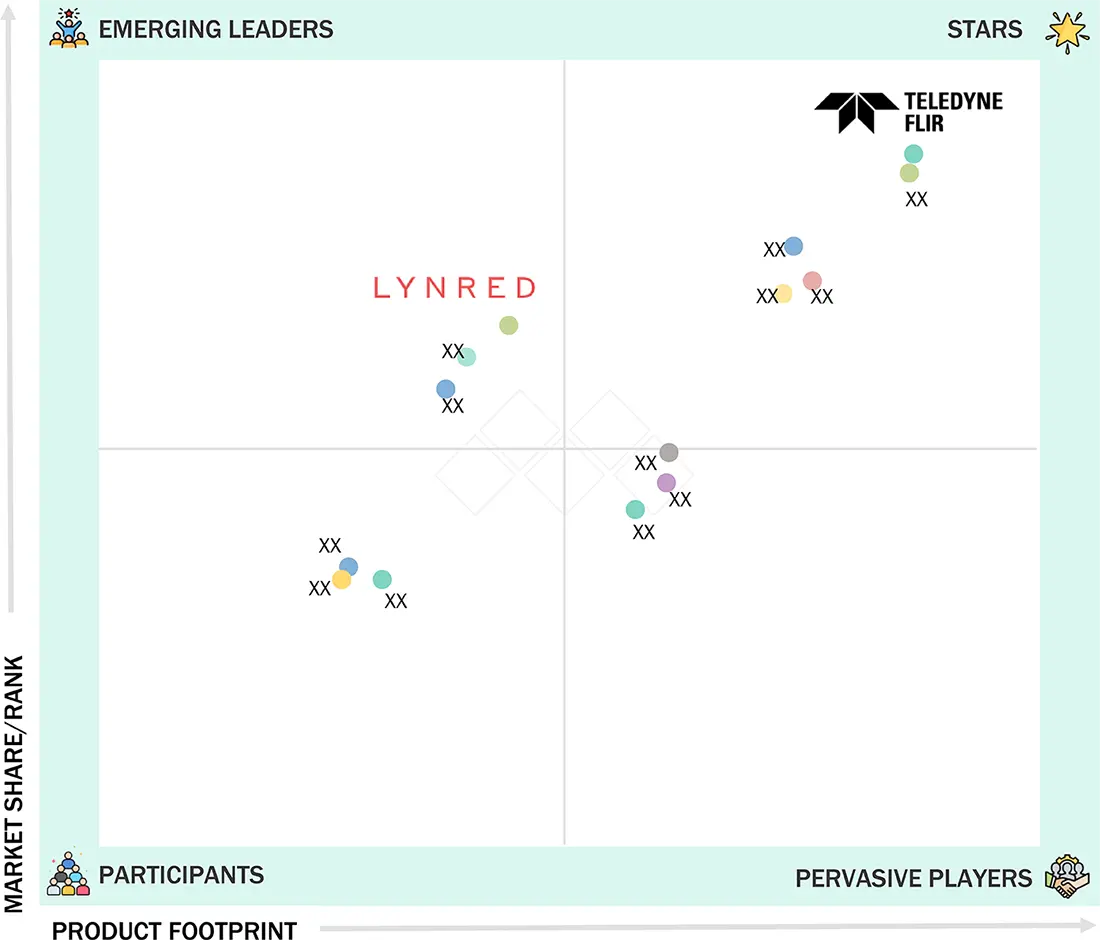

Infrared Imaging Market: COMPANY EVALUATION MATRIX

Teledyne FLIR LLC (Star) leads with a strong market presence and a wide portfolio in the infrared imaging market matrix, driving large-scale adoption across industries like defence and industrial inspection. Lynred (Emerging Leader) is gaining traction with advanced cooled IR detectors in aerospace and security applications. While Teledyne FLIR dominates with scale, Lynred shows strong growth potential to advance toward the leaders' quadrant.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS - Top Infrared Imaging Companies

WHAT IS IN IT FOR YOU: Infrared Imaging Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| US-based Infrared Imaging Manufacturer |

|

|

| Thermal Imaging-Based Manufacturer |

|

|

| Security & Surveillance Infrared Imaging Manufacturer |

|

|

| US-based Infrared Imaging Raw Material Supplier |

|

|

| Aerospace Infrared Imaging Customer |

|

|

RECENT DEVELOPMENTS

- June 2024 : Teledyne FLIR LLC (US) completed its acquisition of Adimec (Netherlands), a developer of high-performance industrial and scientific cameras. Known for delivering precise imaging for critical applications in life sciences and semiconductor inspection, Adimec joins Teledyne’s portfolio to strengthen its digital imaging capabilities across niche, accuracy-driven markets.

- September 2024 : Fluke Corporation (US) introduced the iSee Mobile Thermal Camera, a compact, smartphone-compatible tool designed for electricians, HVAC technicians, and contractors. Real-time thermal imaging capabilities enhance on-the-go inspections, enabling accurate temperature measurements in hard-to-reach areas while improving safety, portability, and convenience in professional thermal diagnostics.

- May 2024 : Axis Communications AB (Sweden) introduced the AXIS Q1961-XTE, the world’s first explosion-protected thermometric camera for Zone and Division 2 hazardous areas. Building on their 2023 innovation, this launch demonstrates Axis’ continued expansion in explosion-protected solutions, offering safer and cost-efficient temperature monitoring for high-risk industrial environments.

- September 2023 : Leonardo S.p.A. (US) unveiled its STAG-5 LLD, a next-gen 5-inch EO/IR stabilized gimbal designed for Group 1 UAS platforms. Equipped with high-definition LWIR, SWIR, EO sensors, and the TENUM 1280 core, it enhances military airborne ISR operations with superior imaging, reduced weight, and MOSA compatibility.

- December 2024 : RTX (US) launched its advanced PC5 series thermal cameras, designed for forest fire prevention and perimeter surveillance. With multi-spectral capabilities, real-time analytics, and long-range detection, the compact PC5 enhances environmental safety and security with high-resolution thermal and visible imaging, making it ideal for 24/7 outdoor monitoring.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

26

2

RESEARCH METHODOLOGY

31

3

EXECUTIVE SUMMARY

42

4

PREMIUM INSIGHTS

47

5

MARKET OVERVIEW

Infrared imaging revolutionizes security, inspection, and consumer electronics despite regulatory and cost hurdles.

51

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

INCREASING USE OF INFRARED IMAGING PRODUCTS IN SECURITY & SURVEILLANCE APPLICATIONS

5.2.1.2

RISING ADOPTION OF INFRARED CAMERAS IN QUALITY CONTROL AND INSPECTION APPLICATIONS

5.2.1.3

GROWING POPULARITY OF UNCOOLED INFRARED CAMERAS

5.2.1.4

BOOSTING DEMAND FOR SWIR CAMERAS IN MACHINE VISION APPLICATIONS

5.2.2

RESTRAINTS

5.2.2.1

STRINGENT IMPORT AND EXPORT REGULATIONS FOR SELLING INFRARED CAMERAS IN US

5.2.2.2

LIMITATIONS ASSOCIATED WITH IMAGE RESOLUTION AND SENSITIVITY OF INFRARED CAMERAS

5.2.3

OPPORTUNITIES

5.2.3.1

EMERGING APPLICATIONS OF IR IMAGING TECHNOLOGY IN AUTOMOTIVE SECTOR

5.2.3.2

NEWER APPLICATION AREAS OF SWIR CAMERAS

5.2.3.3

INTEGRATION OF INFRARED IMAGING TECHNOLOGY INTO CONSUMER ELECTRONICS

5.2.4

CHALLENGES

5.2.4.1

HIGH COST ASSOCIATED WITH INFRARED CAMERAS

5.2.4.2

DESIGNING HIGHLY ACCURATE IR IMAGING PRODUCTS

5.2.4.3

INTEGRATION AND COMPATIBILITY CHALLENGES PERTAINING TO INFRARED IMAGING TECHNOLOGY

5.3

SUPPLY CHAIN ANALYSIS

5.4

INFRARED IMAGING ECOSYSTEM

5.5

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.6

PRICING ANALYSIS

5.6.1

AVERAGE SELLING PRICE OF INFRARED IMAGING CAMERA TYPES, BY KEY PLAYER, 2024

5.6.2

AVERAGE SELLING PRICE TREND OF REFLECTIVE INFRARED IMAGING CAMERAS, BY REGION, 2021–2024

5.6.3

AVERAGE SELLING PRICE TREND OF THERMAL INFRARED IMAGING CAMERAS, BY REGION, 2021–2024

5.7

TECHNOLOGY TRENDS

5.7.1

USE OF IR IMAGING TECHNOLOGY TO ANALYZE ORGANIC COMPOST

5.7.2

IMPLEMENTATION OF VIBRATIONAL SPECTROSCOPIC TECHNIQUES TO ANALYZE TEA QUALITY AND SAFETY

5.7.3

ADOPTION OF THERMAL CAMERAS IN SECURITY AND INSPECTION APPLICATIONS

5.7.4

TRANSFORMATION IN INFRARED IMAGING TECHNOLOGY WITH CLOUD INTEGRATION

5.7.5

ADVANCEMENTS IN AI-BASED INFRARED IMAGING

5.8

IMPACT OF AI/GEN AI ON INFRARED IMAGING MARKET

5.8.1

TOP USE CASES AND MARKET POTENTIAL

5.8.1.1

ANOMALY DETECTION

5.8.1.2

MEDICAL DIAGNOSTICS FEVER SCREENING

5.8.1.3

SURVEILLANCE & BORDER SECURITY

5.8.1.4

SMART CITY INFRASTRUCTURE MONITORING

5.8.1.5

AUTOMOTIVE DRIVER-ASSISTANCE AND EV BATTERY MONITORING

5.9

PORTER’S FIVE FORCES ANALYSIS

5.9.1

THREAT OF NEW ENTRANTS

5.9.2

THREAT OF SUBSTITUTES

5.9.3

BARGAINING POWER OF SUPPLIERS

5.9.4

BARGAINING POWER OF BUYERS

5.9.5

INTENSITY OF COMPETITIVE RIVALRY

5.10

KEY STAKEHOLDERS IN BUYING PROCESS AND BUYING CRITERIA

5.10.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2

BUYING CRITERIA

5.11

CASE STUDY ANALYSIS

5.11.1

ROCKWOOL GROUP USED TELEDYNE FLIR’S THERMAL IMAGING TECHNOLOGY TO ASSESS INSULATION EFFECTIVENESS AND CONDUCT BUILDING ANALYSIS

5.11.2

VICENZA COURT RESOLVED CONSTRUCTION DISPUTE BY HIRING SERVICES OF THERMAL IMAGING EXPERTS FROM MULTITES SRL

5.11.3

HIGHLAND HELICOPTERS DEPLOYED THERMAL CAMERAS FROM INFRATEC TO COMBAT WILDFIRES

5.12

PATENT ANALYSIS

5.13

KEY CONFERENCES AND EVENTS, 2025–2026

5.14

TRADE ANALYSIS

5.14.1

IMPORT SCENARIO (HS 902750)

5.14.2

EXPORT SCENARIO (HS 902750)

5.15

TARIFF ANALYSIS

5.16

STANDARDS AND REGULATORY LANDSCAPE

5.16.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.16.2

GOVERNMENT REGULATIONS

5.16.3

REGULATORY LANDSCAPE

5.16.4

GOVERNMENT STANDARDS

5.17

2025 US TARIFF IMPACT ON INFRARED IMAGING MARKET

5.17.1

INTRODUCTION

5.17.2

KEY TARIFF RATES

5.17.3

PRICE IMPACT ANALYSIS

5.17.4

KEY IMPACTS ON VARIOUS COUNTRIES/REGIONS

5.17.4.1

US

5.17.4.2

EUROPE

5.17.4.3

ASIA PACIFIC

5.17.5

IMPACT ON VERTICALS

6

INFRARED IMAGING DEVICE TYPES

Discover versatile infrared imaging devices enhancing inspection efficiency from portable to fixed applications.

95

6.1

INTRODUCTION

6.2

PORTABLE

6.2.1

USE OF PORTABLE CAMERAS FOR CONVENIENCE AND EFFORTLESS IMAGING

6.2.2

AERIAL

6.2.2.1

DEPLOYMENT OF AERIAL CAMERAS FOR THERMOGRAPHIC VIEW AND IMPROVED VISIBILITY OF OBJECTS TO BE MONITORED OR INSPECTED

6.2.3

HANDHELD

6.2.3.1

IMPLEMENTATION OF HANDHELD CAMERAS IN BUILDINGS TO INSPECT HEAT LOSS AND DETECT INSULATION ISSUES

6.3

FIXED

6.3.1

ADOPTION OF FIXED CAMERAS TO ENSURE CONSISTENT AND RELIABLE IMAGING OUTPUT

7

INFRARED IMAGING MARKET, BY TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 14 Data Tables

97

7.1

INTRODUCTION

7.2

REFLECTIVE

7.2.1

RISING USE IN SEMICONDUCTOR INSPECTION AND SECURITY APPLICATIONS TO SUPPORT MARKET GROWTH

7.3

THERMAL

7.3.1

PRESSING NEED FOR ENHANCED SAFETY AND OPERATIONAL EFFICIENCY ACROSS INDUSTRIES TO BOOST DEMAND

8

INFRARED IMAGING MARKET, BY COMPONENT

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 10 Data Tables

103

8.1

INTRODUCTION

8.2

CAMERAS

8.2.1

SIGNIFICANT USE IN PUBLIC SAFETY, MEDICAL, AND INDUSTRIAL APPLICATIONS TO FUEL SEGMENTAL GROWTH

8.3

SCOPES

8.3.1

DEFENSE, OUTDOOR SPORTS, AND TACTICAL SURVEILLANCE APPLICATIONS TO CONTRIBUTE TO SEGMENTAL GROWTH

8.4

MODULES

8.4.1

SURGING USE OF MODULAR INFRARED IMAGING SYSTEMS IN DRONES, ROBOTICS, AND SMART DEVICES TO FOSTER SEGMENTAL GROWTH

9

INFRARED IMAGING MARKET, BY TECHNOLOGY

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 10 Data Tables

109

9.1

INTRODUCTION

9.2

COOLED

9.2.1

NEED TO REDUCE SENSOR NOISE AND IMPROVE SENSITIVITY TO ENCOURAGE ADOPTION

9.3

UNCOOLED

9.3.1

INCREASING ADOPTION IN HIGH-VOLUME APPLICATIONS OWING TO LOW COST AND EASY INSTALLATION TO FOSTER SEGMENTAL GROWTH

10

INFRARED IMAGING MARKET, BY WAVELENGTH

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 18 Data Tables

114

10.1

INTRODUCTION

10.2

NIR

10.2.1

HIGH ADOPTION OF NIR CCTV CAMERAS FOR SECURITY & SURVEILLANCE TO DRIVE MARKET

10.3

SWIR

10.3.1

INCREASED USE OF SWIR IMAGING TECHNOLOGY IN NON-DESTRUCTIVE TESTING TO PROPEL MARKET

10.4

MWIR

10.4.1

RAPID TECHNOLOGICAL ADVANCEMENTS IN MWIR TO BOOST SEGMENTAL GROWTH

10.5

LWIR

10.5.1

SIGNIFICANT USE IN WEARABLES, DRONES, AND HANDHELD DEVICES TO FUEL SEGMENTAL GROWTH

11

INFRARED IMAGING MARKET, BY APPLICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 20 Data Tables

123

11.1

INTRODUCTION

11.2

SECURITY & SURVEILLANCE

11.2.1

SURGING DEPLOYMENT OF INFRARED CAMERAS DUE TO INCREASED TERRORISM TO DRIVE MARKET

11.3

MONITORING & INSPECTION

11.3.1

RISING USE OF INFRARED CAMERAS IN ENERGY AUDITS, BUILDING DIAGNOSTICS, AND INDUSTRIAL FAULT DETECTION TO PROPEL MARKET

11.3.2

CONDITION MONITORING

11.3.3

STRUCTURAL HEALTH MONITORING

11.3.4

QUALITY CONTROL

11.4

DETECTION

11.4.1

INCREASING IMPORTANCE OF SITUATIONAL AWARENESS TO SPIKE DEMAND

11.4.2

GAS DETECTION

11.4.3

FIRE/FLARE DETECTION

11.4.4

BODY TEMPERATURE MEASUREMENT

12

INFRARED IMAGING MARKET, BY VERTICAL

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 6 Data Tables

134

12.1

INTRODUCTION

12.2

INDUSTRIAL

12.2.1

ELEVATING USE OF SWIR CAMERAS TO ENSURE PRECISION IN GLASS, SEMICONDUCTOR, AND METAL PROCESSING TO FAVOR MARKET GROWTH

12.2.2

AUTOMOTIVE

12.2.3

AEROSPACE

12.2.4

ELECTRONICS & SEMICONDUCTOR

12.2.5

OIL & GAS

12.2.6

FOOD & BEVERAGES

12.2.7

GLASS

12.2.8

OTHER INDUSTRIAL VERTICALS

12.3

NON-INDUSTRIAL

12.3.1

RISING ADOPTION IN PUBLIC SAFETY, RESEARCH, AND HEALTHCARE TO PROPEL MARKET

12.3.2

MILITARY & DEFENSE

12.3.3

CIVIL INFRASTRUCTURE

12.3.4

MEDICAL

12.3.5

SCIENTIFIC RESEARCH

13

INFRARED IMAGING MARKET, BY REGION

Comprehensive coverage of 8 Regions with country-level deep-dive of 13 Countries | 74 Data Tables.

142

13.1

INTRODUCTION

13.2

NORTH AMERICA

13.2.1

MACROECONOMIC OUTLOOK FOR NORTH AMERICA

13.2.2

US

13.2.2.1

GOVERNMENT FOCUS ON SAFETY AND SECURITY OF COUNTRY TO FUEL MARKET GROWTH

13.2.3

CANADA

13.2.3.1

GROWING FOCUS ON SAFEGUARDING ASSETS AND ENSURING PUBLIC SAFETY TO BOOST DEMAND

13.2.4

MEXICO

13.2.4.1

INCREASING CHALLENGES RELATED TO BORDER SECURITY, DRUG TRAFFICKING, AND ORGANIZED CRIME TO SPIKE DEMAND

13.3

EUROPE

13.3.1

MACROECONOMIC OUTLOOK FOR EUROPE

13.3.2

GERMANY

13.3.2.1

BOOMING AUTOMOTIVE SECTOR TO ACCELERATE DEMAND

13.3.3

UK

13.3.3.1

MEDICAL AND PHARMACEUTICAL COMPANIES TO CONTRIBUTE MOST TO MARKET GROWTH

13.3.4

FRANCE

13.3.4.1

TECHNOLOGY ADVANCEMENTS IN AUTOMOTIVE SECTOR TO PROPEL MARKET GROWTH

13.3.5

ITALY

13.3.5.1

GOVERNMENT FOCUS ON STRENGTHENING MILITARY SURVEILLANCE CAPABILITIES TO PROPEL MARKET

13.3.6

REST OF EUROPE

13.4

ASIA PACIFIC

13.4.1

MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

13.4.2

CHINA

13.4.2.1

BORDER CONTROL, CRITICAL INFRASTRUCTURE PROTECTION, AND PUBLIC SAFETY APPLICATIONS TO CREATE OPPORTUNITIES

13.4.3

JAPAN

13.4.3.1

CONSUMER ELECTRONICS, AUTOMOTIVE, AND HEALTHCARE SECTORS TO STRENGTHEN MARKET MOMENTUM

13.4.4

INDIA

13.4.4.1

INCREASING USE IN PREDICTIVE MAINTENANCE AND QUALITY CONTROL APPLICATIONS BY INDUSTRY PLAYERS TO SUPPORT MARKET GROWTH

13.4.5

REST OF ASIA PACIFIC

13.5

ROW

13.5.1

MACROECONOMIC OUTLOOK FOR ROW

13.5.2

SOUTH AMERICA

13.5.2.1

GREATER EMPHASIS ON ADDRESSING URBAN CRIME AND SUPPORTING BORDER SECURITY OPERATIONS TO STIMULATE DEMAND

13.5.3

MIDDLE EAST

13.5.3.1

BAHRAIN

13.5.3.1.1

GOVERNMENT INITIATIVES TO MODERNIZE SURVEILLANCE AND BORDER CONTROL TO DRIVE MARKET

13.5.3.2

KUWAIT

13.5.3.2.1

STRONG FOCUS ON MODERNIZING OIL, DEFENSE, AND HEALTH INFRASTRUCTURE TO ACCELERATE DEMAND

13.5.3.3

OMAN

13.5.3.3.1

RISING EMPHASIS ON ADVANCED SAFETY PROTOCOLS AND SUSTAINABLE OPERATIONS TO CREATE OPPORTUNITIES

13.5.3.4

QATAR

13.5.3.4.1

SMART CITY DEVELOPMENT INITIATIVES TO FUEL MARKET GROWTH

13.5.3.5

SAUDI ARABIA

13.5.3.5.1

PRESSING NEED TO MONITOR HIGH-TEMPERATURE PROCESSES IN OIL AND PETROCHEMICAL PLANTS TO BOOST DEMAND

13.5.3.6

UAE

13.5.3.6.1

VISION OF BECOMING GLOBAL INNOVATION HUB TO SUPPORT MARKET GROWTH

13.5.3.7

REST OF MIDDLE EAST

13.5.4

AFRICA

13.5.4.1

URBAN INFRASTRUCTURE DEVELOPMENT TO CREATE OPPORTUNITIES

14

COMPETITIVE LANDSCAPE

Uncover top strategies and emerging leaders shaping the competitive edge in infrared imaging.

179

14.1

OVERVIEW

14.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020–2025

14.3

REVENUE ANALYSIS, 2020–2024

14.4

MARKET SHARE ANALYSIS, 2024

14.5

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

14.5.1

STARS

14.5.2

EMERGING LEADERS

14.5.3

PERVASIVE PLAYERS

14.5.4

PARTICIPANTS

14.5.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

14.5.5.1

COMPANY FOOTPRINT

14.5.5.2

REGION FOOTPRINT

14.5.5.3

TYPE FOOTPRINT

14.5.5.4

VERTICAL FOOTPRINT

14.6

STARTUPS/SMES, 2024

14.6.1

PROGRESSIVE COMPANIES

14.6.2

RESPONSIVE COMPANIES

14.6.3

DYNAMIC COMPANIES

14.6.4

STARTING BLOCKS

14.6.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

14.6.5.1

DETAILED LIST OF KEY STARTUPS/SMES

14.6.5.2

COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

14.7

COMPETITIVE SCENARIOS

14.7.1

PRODUCT LAUNCHES

14.7.2

DEALS

14.7.3

OTHER DEVELOPMENTS

15

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

197

15.1

KEY PLAYERS

15.1.1

TELEDYNE FLIR LLC

15.1.1.1

BUSINESS OVERVIEW

15.1.1.2

PRODUCTS/SERVICES/SOLUTIONS OFFERED

15.1.1.3

RECENT DEVELOPMENTS

15.1.1.3.1

PRODUCT LAUNCHES

15.1.1.3.2

DEALS

15.1.1.3.3

OTHER DEVELOPMENTS

15.1.1.4

MNM VIEW

15.1.1.4.1

KEY STRENGTHS/RIGHT TO WIN

15.1.1.4.2

STRATEGIC CHOICES

15.1.1.4.3

WEAKNESSES/COMPETITIVE THREATS

15.1.2

FLUKE CORPORATION

15.1.3

LEONARDO S.P.A.

15.1.4

AXIS COMMUNICATIONS AB

15.1.5

RTX

15.1.6

L3HARRIS TECHNOLOGIES, INC.

15.1.7

EXOSENS

15.1.8

OPGAL OPTRONIC INDUSTRIES LTD.

15.1.9

LYNRED

15.1.10

ALLIED VISION TECHNOLOGIES GMBH

15.1.11

BAE SYSTEMS

15.1.12

TESTO SE & CO. KGAA

15.2

OTHER KEY PLAYERS

15.2.1

INTEVAC, INC.

15.2.2

ZHEJIANG DALI TECHNOLOGY CO., LTD.

15.2.3

C-THERM TECHNOLOGIES LTD.,

15.2.4

IRCAMERAS LLC

15.2.5

HGH

15.2.6

RAPTOR PHOTONICS

15.2.7

EPISENSORS

15.2.8

INFRATEC GMBH

15.2.9

PRINCETON INFRARED TECHNOLOGIES, INC.

15.2.10

SIERRA-OLYMPIA TECH.

15.2.11

COX CO., LTD.

15.2.12

TONBO IMAGING

15.2.13

OPTOTHERM, INC.

15.2.14

SEEK THERMAL

15.2.15

INFRARED CAMERAS, INC.

15.2.16

LAND INSTRUMENTS INTERNATIONAL LTD

15.2.17

DIAS INFRARED GMBH

15.2.18

MOVITHERM

16

APPENDIX

256

16.1

INSIGHTS FROM INDUSTRY EXPERTS

16.2

DISCUSSION GUIDE

16.3

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

16.4

CUSTOMIZATION OPTIONS

16.5

RELATED REPORTS

16.6

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

RESEARCH LIMITATIONS

TABLE 2

PRICING RANGE OF INFRARED IMAGING CAMERAS OFFERED BY MAJOR PLAYERS, BY TYPE, 2024 (USD)

TABLE 3

AVERAGE SELLING PRICE TREND OF REFLECTIVE INFRARED IMAGING CAMERAS, BY REGION, 2021–2024 (USD MILLION)

TABLE 4

AVERAGE SELLING PRICE OF THERMAL INFRARED IMAGING CAMERAS, BY REGION, 2021–2024 (USD MILLION)

TABLE 5

IMPACT OF FORCES ON INFRARED IMAGING MARKET

TABLE 6

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR APPLICATIONS (%)

TABLE 7

KEY BUYING CRITERIA FOR APPLICATIONS

TABLE 8

INFRARED IMAGING MARKET: KEY PATENTS

TABLE 9

INFRARED IMAGING MARKET: LIST OF CONFERENCES AND EVENTS, 2025–2026

TABLE 10

IMPORT DATA FOR HS 902750-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 11

EXPORT DATA FOR HS 902750-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 12

MFN TARIFF FOR HS CODE 902750-COMPLIANT PRODUCTS EXPORTED BY US

TABLE 13

MFN TARIFF FOR HS CODE 902750-COMPLIANT PRODUCTS EXPORTED BY CHINA

TABLE 14

MFN TARIFF FOR HS CODE 902750-COMPLIANT PRODUCTS EXPORTED BY GERMANY

TABLE 15

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 16

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 17

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 18

ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 19

US-ADJUSTED RECIPROCAL TARIFF RATES

TABLE 20

ANTICIPATED CHANGE IN PRICES AND IMPACT ON VERTICALS DUE TO TARIFF

TABLE 21

INFRARED IMAGING MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 22

INFRARED IMAGING MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 23

REFLECTIVE: INFRARED IMAGING MARKET, BY WAVELENGTH, 2021–2024 (USD MILLION)

TABLE 24

REFLECTIVE: INFRARED IMAGING MARKET, BY WAVELENGTH, 2025–2030 (USD MILLION)

TABLE 25

REFLECTIVE: INFRARED IMAGING MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 26

REFLECTIVE: INFRARED IMAGING MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 27

REFLECTIVE: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 28

REFLECTIVE: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 29

THERMAL: INFRARED IMAGING MARKET, BY WAVELENGTH, 2021–2024 (USD MILLION)

TABLE 30

THERMAL: INFRARED IMAGING MARKET, BY WAVELENGTH, 2025–2030 (USD MILLION)

TABLE 31

THERMAL: INFRARED IMAGING MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 32

THERMAL: INFRARED IMAGING MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 33

THERMAL: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 34

THERMAL: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 35

INFRARED IMAGING MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 36

INFRARED IMAGING MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 37

CAMERAS: INFRARED IMAGING MARKET, BY TYPE, 2021–2024 (THOUSAND UNITS)

TABLE 38

CAMERAS: INFRARED IMAGING MARKET, BY TYPE, 2025–2030 (THOUSAND UNITS)

TABLE 39

CAMERAS: INFRARED IMAGING MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 40

CAMERAS: INFRARED IMAGING MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 41

SCOPES: INFRARED IMAGING MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 42

SCOPES: INFRARED IMAGING MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 43

MODULES: INFRARED IMAGING MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 44

MODULES: INFRARED IMAGING MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 45

INFRARED IMAGING MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 46

INFRARED IMAGING MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 47

COOLED: INFRARED IMAGING MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 48

COOLED: INFRARED IMAGING MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 49

COOLED: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 50

COOLED: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 51

UNCOOLED: INFRARED IMAGING MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 52

UNCOOLED: INFRARED IMAGING MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 53

UNCOOLED: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 54

UNCOOLED: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 55

INFRARED IMAGING MARKET, BY WAVELENGTH, 2021–2024 (USD MILLION)

TABLE 56

INFRARED IMAGING MARKET, BY WAVELENGTH, 2025–2030 (USD MILLION)

TABLE 57

NIR: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 58

NIR: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 59

NIR: INFRARED IMAGING MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 60

NIR: INFRARED IMAGING MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 61

SWIR: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 62

SWIR: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 63

SWIR: INFRARED IMAGING MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 64

SWIR: INFRARED IMAGING MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 65

MWIR: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 66

MWIR: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 67

MWIR: INFRARED IMAGING MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 68

MWIR: INFRARED IMAGING MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 69

LWIR: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 70

LWIR: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 71

LWIR: INFRARED IMAGING MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 72

LWIR: INFRARED IMAGING MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 73

INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 74

INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 75

SECURITY & SURVEILLANCE: INFRARED IMAGING MARKET, BY WAVELENGTH, 2021–2024 (USD MILLION)

TABLE 76

SECURITY & SURVEILLANCE: INFRARED IMAGING MARKET, BY WAVELENGTH, 2025–2030 (USD MILLION)

TABLE 77

SECURITY & SURVEILLANCE: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 78

SECURITY & SURVEILLANCE: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 79

SECURITY & SURVEILLANCE: INFRARED IMAGING MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 80

SECURITY & SURVEILLANCE: INFRARED IMAGING MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 81

MONITORING & INSPECTION: INFRARED IMAGING MARKET, BY WAVELENGTH, 2021–2024 (USD MILLION)

TABLE 82

MONITORING & INSPECTION: INFRARED IMAGING MARKET, BY WAVELENGTH, 2025–2030 (USD MILLION)

TABLE 83

MONITORING & INSPECTION: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 84

MONITORING & INSPECTION: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 85

MONITORING & INSPECTION: INFRARED IMAGING MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 86

MONITORING & INSPECTION: INFRARED IMAGING MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 87

DETECTION: INFRARED IMAGING MARKET, BY WAVELENGTH, 2021–2024 (USD MILLION)

TABLE 88

DETECTION: INFRARED IMAGING MARKET, BY WAVELENGTH, 2025–2030 (USD MILLION)

TABLE 89

DETECTION: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2021–2024 (USD MILLION)

TABLE 90

DETECTION: INFRARED IMAGING MARKET, BY TECHNOLOGY, 2025–2030 (USD MILLION)

TABLE 91

DETECTION: INFRARED IMAGING MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 92

DETECTION: INFRARED IMAGING MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 93

INFRARED IMAGING MARKET, BY VERTICAL, 2021–2024 (USD MILLION)

TABLE 94

INFRARED IMAGING MARKET, BY VERTICAL, 2025–2030 (USD MILLION)

TABLE 95

INDUSTRIAL: INFRARED IMAGING MARKET, BY WAVELENGTH, 2021–2024 (USD MILLION)

TABLE 96

INDUSTRIAL: INFRARED IMAGING MARKET, BY WAVELENGTH, 2025–2030 (USD MILLION)

TABLE 97

NON-INDUSTRIAL: INFRARED IMAGING MARKET, BY WAVELENGTH, 2021–2024 (USD MILLION)

TABLE 98

NON-INDUSTRIAL: INFRARED IMAGING MARKET, BY WAVELENGTH, 2025–2030 (USD MILLION)

TABLE 99

INFRARED IMAGING MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 100

INFRARED IMAGING MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 101

NORTH AMERICA: INFRARED IMAGING MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 102

NORTH AMERICA: INFRARED IMAGING MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 103

NORTH AMERICA: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 104

NORTH AMERICA: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 105

NORTH AMERICA: INFRARED IMAGING MARKET FOR SECURITY & SURVEILLANCE APPLICATIONS, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 106

NORTH AMERICA: INFRARED IMAGING MARKET FOR SECURITY & SURVEILLANCE APPLICATIONS, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 107

NORTH AMERICA: INFRARED IMAGING MARKET FOR MONITORING & INSPECTION APPLICATIONS, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 108

NORTH AMERICA: INFRARED IMAGING MARKET FOR MONITORING & INSPECTION APPLICATIONS, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 109

NORTH AMERICA: INFRARED IMAGING MARKET FOR DETECTION APPLICATIONS, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 110

NORTH AMERICA: INFRARED IMAGING MARKET FOR DETECTION APPLICATIONS, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 111

US: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 112

US: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 113

CANADA: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 114

CANADA: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 115

MEXICO: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 116

MEXICO: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 117

EUROPE: INFRARED IMAGING MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 118

EUROPE: INFRARED IMAGING MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 119

EUROPE: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 120

EUROPE: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 121

EUROPE: INFRARED IMAGING MARKET FOR SECURITY & SURVEILLANCE APPLICATIONS, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 122

EUROPE: INFRARED IMAGING MARKET FOR SECURITY & SURVEILLANCE APPLICATIONS, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 123

EUROPE: INFRARED IMAGING MARKET FOR MONITORING & INSPECTION APPLICATIONS, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 124

EUROPE: INFRARED IMAGING MARKET FOR MONITORING & INSPECTION APPLICATIONS, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 125

EUROPE: INFRARED IMAGING MARKET FOR DETECTION APPLICATIONS, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 126

EUROPE: INFRARED IMAGING MARKET FOR DETECTION APPLICATIONS, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 127

GERMANY: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 128

GERMANY: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 129

UK: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 130

UK: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 131

FRANCE: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 132

FRANCE: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 133

ITALY: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 134

ITALY: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 135

REST OF EUROPE: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 136

REST OF EUROPE: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 137

ASIA PACIFIC: INFRARED IMAGING MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 138

ASIA PACIFIC: INFRARED IMAGING MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 139

ASIA PACIFIC: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 140

ASIA PACIFIC: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 141

ASIA PACIFIC: INFRARED IMAGING MARKET FOR SECURITY & SURVEILLANCE APPLICATIONS, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 142

ASIA PACIFIC: INFRARED IMAGING MARKET FOR SECURITY & SURVEILLANCE APPLICATIONS, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 143

ASIA PACIFIC: INFRARED IMAGING MARKET FOR MONITORING & INSPECTION APPLICATIONS, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 144

ASIA PACIFIC: INFRARED IMAGING MARKET FOR MONITORING & INSPECTION APPLICATIONS, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 145

ASIA PACIFIC: INFRARED IMAGING MARKET FOR DETECTION APPLICATIONS, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 146

ASIA PACIFIC: INFRARED IMAGING MARKET FOR DETECTION APPLICATIONS, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 147

CHINA: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 148

CHINA: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 149

JAPAN: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 150

JAPAN: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 151

INDIA: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 152

INDIA: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 153

REST OF ASIA PACIFIC: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 154

REST OF ASIA PACIFIC: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 155

ROW: INFRARED IMAGING MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 156

ROW: INFRARED IMAGING MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 157

ROW: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 158

ROW: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 159

ROW: INFRARED IMAGING MARKET FOR SECURITY & SURVEILLANCE APPLICATIONS, BY REGION, 2021–2024 (USD MILLION)

TABLE 160

ROW: INFRARED IMAGING MARKET FOR SECURITY & SURVEILLANCE APPLICATIONS, BY REGION, 2025–2030 (USD MILLION)

TABLE 161

ROW: INFRARED IMAGING MARKET FOR MONITORING & INSPECTION APPLICATIONS, BY REGION, 2021–2024 (USD MILLION)

TABLE 162

ROW: INFRARED IMAGING MARKET FOR MONITORING & INSPECTION APPLICATIONS, BY REGION, 2025–2030 (USD MILLION)

TABLE 163

ROW: INFRARED IMAGING MARKET FOR DETECTION APPLICATIONS, BY REGION, 2021–2024 (USD MILLION)

TABLE 164

ROW: INFRARED IMAGING MARKET FOR DETECTION APPLICATIONS, BY REGION, 2025–2030 (USD MILLION)

TABLE 165

SOUTH AMERICA: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 166

SOUTH AMERICA: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 167

MIDDLE EAST: INFRARED IMAGING MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 168

MIDDLE EAST: INFRARED IMAGING MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 169

MIDDLE EAST: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 170

MIDDLE EAST: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 171

AFRICA: INFRARED IMAGING MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 172

AFRICA: INFRARED IMAGING MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 173

OVERVIEW OF STRATEGIES FOLLOWED BY TOP 5 PLAYERS IN INFRARED IMAGING MARKET, JULY 2020–JUNE 2025

TABLE 174

INFRARED IMAGING MARKET: DEGREE OF COMPETITION

TABLE 175

INFRARED IMAGING MARKET: REGION FOOTPRINT

TABLE 176

INFRARED IMAGING MARKET: TYPE FOOTPRINT

TABLE 177

INFRARED IMAGING MARKET: VERTICAL FOOTPRINT

TABLE 178

INFRARED IMAGING MARKET: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 179

INFRARED IMAGING MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 180

INFRARED IMAGING MARKET: PRODUCT LAUNCHES, JULY 2020–JUNE 2025

TABLE 181

INFRARED IMAGING MARKET: DEALS, JULY 2020–JUNE 2025

TABLE 182

INFRARED IMAGING MARKET: OTHER DEVELOPMENTS, JULY 2020–JUNE 2025

TABLE 183

TELEDYNE FLIR LLC: COMPANY OVERVIEW

TABLE 184

TELEDYNE FLIR LLC: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 185

TELEDYNE FLIR LLC: PRODUCT LAUNCHES

TABLE 186

TELEDYNE FLIR LLC: DEALS

TABLE 187

TELEDYNE FLIR LLC: OTHER DEVELOPMENTS

TABLE 188

FLUKE CORPORATION: COMPANY OVERVIEW

TABLE 189

FLUKE CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 190

FLUKE CORPORATION: PRODUCT LAUNCHES

TABLE 191

LEONARDO S.P.A.: COMPANY OVERVIEW

TABLE 192

LEONARDO S.P.A.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 193

LEONARDO S.P.A.: PRODUCT LAUNCHES

TABLE 194

LEONARDO S.P.A.: DEALS

TABLE 195

LEONARDO S.P.A.: OTHER DEVELOPMENTS

TABLE 196

AXIS COMMUNICATIONS AB: COMPANY OVERVIEW

TABLE 197

AXIS COMMUNICATIONS AB: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 198

AXIS COMMUNICATIONS AB: PRODUCT LAUNCHES

TABLE 199

AXIS COMMUNICATIONS AB: DEALS

TABLE 200

RTX: COMPANY OVERVIEW

TABLE 201

RTX: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 202

RTX: PRODUCT LAUNCHES

TABLE 203

RTX: DEALS

TABLE 204

L3HARRIS TECHNOLOGIES, INC.: COMPANY OVERVIEW

TABLE 205

L3HARRIS TECHNOLOGIES, INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 206

L3HARRIS TECHNOLOGIES, INC.: DEALS

TABLE 207

EXOSENS: COMPANY OVERVIEW

TABLE 208

EXOSENS: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 209

EXOSENS: PRODUCT LAUNCHES

TABLE 210

EXOSENS: DEALS

TABLE 211

OPGAL OPTRONIC INDUSTRIES LTD.: COMPANY OVERVIEW

TABLE 212

OPGAL OPTRONIC INDUSTRIES LTD.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 213

OPGAL OPTRONIC INDUSTRIES LTD.: PRODUCT LAUNCHES

TABLE 214

LYNRED: COMPANY OVERVIEW

TABLE 215

LYNRED: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 216

LYNRED: PRODUCT LAUNCHES

TABLE 217

LYNRED: DEALS

TABLE 218

ALLIED VISION TECHNOLOGIES: COMPANY OVERVIEW

TABLE 219

ALLIED VISION TECHNOLOGIES: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 220

ALLIED VISION TECHNOLOGIES: PRODUCT LAUNCHES

TABLE 221

BAE SYSTEMS: COMPANY OVERVIEW

TABLE 222

BAE SYSTEMS: PRODUCTS OFFERED

TABLE 223

BAE SYSTEMS: PRODUCT LAUNCHES

TABLE 224

BAE SYSTEMS: DEALS

TABLE 225

TESTO SE & CO. KGAA: COMPANY OVERVIEW

TABLE 226

TESTO SE & CO. KGAA: PRODUCTS OFFERED

TABLE 227

TESTO SE & CO. KGAA: PRODUCT LAUNCHES

LIST OF FIGURES

FIGURE 1

INFRARED IMAGING MARKET SEGMENTATION

FIGURE 2

INFRARED IMAGING MARKET: RESEARCH DESIGN

FIGURE 3

PROCESS FLOW OF MARKET SIZE ESTIMATION

FIGURE 4

INFRARED IMAGING MARKET: BOTTOM-UP APPROACH

FIGURE 5

INFRARED IMAGING MARKET: TOP-DOWN APPROACH

FIGURE 6

MARKET SIZE ESTIMATION METHODOLOGY: APPROACH (SUPPLY SIDE)— REVENUE GENERATED FROM SALES OF INFRARED IMAGING PRODUCTS

FIGURE 7

DATA TRIANGULATION

FIGURE 8

THERMAL SEGMENT TO HOLD MAJORITY OF MARKET SHARE IN 2030

FIGURE 9

CAMERAS SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2030

FIGURE 10

NIR SEGMENT TO CAPTURE PROMINENT MARKET SHARE IN 2030

FIGURE 11

SECURITY & SURVEILLANCE SEGMENT TO HOLD LARGEST MARKET SHARE IN 2030

FIGURE 12

UNCOOLED SEGMENT TO COMMAND INFRARED IMAGING MARKET THROUGHOUT FORECAST PERIOD

FIGURE 13

NON-INDUSTRIAL SEGMENT TO HOLD LARGER SHARE OF INFRARED IMAGING MARKET IN 2030

FIGURE 14

ASIA PACIFIC TO BE FASTEST-GROWING MARKET FOR INFRARED IMAGING DURING FORECAST PERIOD

FIGURE 15

INCREASING ADOPTION OF INFRARED IMAGING TECHNOLOGY IN ASIA PACIFIC TO DRIVE MARKET

FIGURE 16

THERMAL TYPE TO HOLD LARGER SHARE OF INFRARED IMAGING MARKET IN 2025

FIGURE 17

CAMERAS TO CAPTURE LARGEST SHARE OF INFRARED IMAGING MARKET IN 2025

FIGURE 18

SECURITY & SURVEILLANCE APPLICATIONS TO HOLD LARGEST SHARE OF INFRARED IMAGING MARKET IN 2025

FIGURE 19

NIR WAVELENGTH TO ACCOUNT FOR LARGEST MARKET SHARE IN 2025

FIGURE 20

US AND SECURITY & SURVEILLANCE APPLICATIONS TO HOLD LARGEST SHARE OF NORTH AMERICAN MARKET IN 2030

FIGURE 21

CHINA TO REGISTER HIGHEST CAGR IN GLOBAL INFRARED IMAGING MARKET DURING FORECAST PERIOD

FIGURE 22

DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: INFRARED IMAGING MARKET

FIGURE 23

ANALYSIS OF IMPACT OF DRIVERS ON INFRARED IMAGING MARKET

FIGURE 24

ANALYSIS OF IMPACT OF RESTRAINTS ON INFRARED IMAGING MARKET

FIGURE 25

ANALYSIS OF IMPACT OF OPPORTUNITIES ON INFRARED IMAGING MARKET

FIGURE 26

ANALYSIS OF IMPACT OF CHALLENGES ON INFRARED IMAGING MARKET

FIGURE 27

VALUE CHAIN ANALYSIS: INFRARED IMAGING MARKET

FIGURE 28

INFRARED IMAGING ECOSYSTEM

FIGURE 29

TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

FIGURE 30

AVERAGE SELLING PRICE OF INFRARED IMAGING CAMERAS OFFERED BY MAJOR PLAYERS, BY TYPE, 2024

FIGURE 31

AVERAGE SELLING PRICE TREND OF REFLECTIVE INFRARED IMAGING CAMERAS, BY REGION, 2021–2024

FIGURE 32

AVERAGE SELLING PRICE TREND OF THERMAL INFRARED IMAGING CAMERAS, BY REGION, 2021–2024

FIGURE 33

IMPACT OF AI/GEN AI ON INFRARED IMAGING MARKET

FIGURE 34

PORTER’S FIVE FORCES ANALYSIS

FIGURE 35

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY APPLICATION

FIGURE 36

KEY BUYING CRITERIA FOR APPLICATIONS

FIGURE 37

PATENTS GRANTED AND APPLIED FOR INFRARED IMAGING PRODUCTS, 2016–2025

FIGURE 38

IMPORT SCENARIO FOR HS CODE 902750-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2020–2024

FIGURE 39

EXPORT SCENARIO FOR HS CODE 902750-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2020–2024

FIGURE 40

THERMAL SEGMENT TO ACCOUNT FOR MAJORITY OF MARKET SHARE IN 2030

FIGURE 41

CAMERAS TO DOMINATE MARKET THROUGHOUT FORECAST PERIOD

FIGURE 42

UNCOOLED SEGMENT TO DOMINATE MARKET THROUGHOUT FORECAST PERIOD

FIGURE 43

SWIR SEGMENT TO WITNESS HIGHEST CAGR IN INFRARED IMAGING MARKET DURING FORECAST PERIOD

FIGURE 44

MONITORING & INSPECTION SEGMENT TO WITNESS HIGHEST CAGR IN INFRARED IMAGING MARKET DURING FORECAST PERIOD

FIGURE 45

NON-INDUSTRIAL SEGMENT TO COMMAND INFRARED IMAGING MARKET THROUGHOUT FORECAST PERIOD

FIGURE 46

ASIA PACIFIC TO WITNESS HIGHEST CAGR IN INFRARED IMAGING MARKET DURING FORECAST PERIOD

FIGURE 47

NORTH AMERICA: INFRARED IMAGING MARKET SNAPSHOT

FIGURE 48

EUROPE: INFRARED IMAGING MARKET SNAPSHOT

FIGURE 49

ASIA PACIFIC: INFRARED IMAGING MARKET SNAPSHOT

FIGURE 50

ROW: INFRARED IMAGING MARKET SNAPSHOT

FIGURE 51

INFRARED IMAGING MARKET: REVENUE ANALYSIS, 2020–2024

FIGURE 52

INFRARED IMAGING MARKET: MARKET SHARE ANALYSIS, 2024

FIGURE 53

INFRARED IMAGING MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 54

INFRARED IMAGING MARKET: COMPANY FOOTPRINT

FIGURE 55

INFRARED IMAGING MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 56

TELEDYNE FLIR LLC: COMPANY SNAPSHOT

FIGURE 57

LEONARDO S.P.A.: COMPANY SNAPSHOT

FIGURE 58

AXIS COMMUNICATIONS AB: COMPANY SNAPSHOT

FIGURE 59

RTX: COMPANY SNAPSHOT

FIGURE 60

L3HARRIS TECHNOLOGIES, INC.: COMPANY SNAPSHOT

FIGURE 61

BAE SYSTEMS: COMPANY SNAPSHOT

Methodology

The study involved four major activities in estimating the current size of the infrared imaging market—exhaustive secondary research collected information on the market, peer, and parent markets. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation were used to estimate the market size of segments and subsegments.

Secondary Research

The secondary research process involved referring to various secondary sources to identify and collect necessary information for this study. The secondary sources include annual reports, press releases, and investor presentations of companies; white papers; journals and certified publications; and articles from recognized authors, websites, directories, and databases. Secondary research was conducted to obtain critical information about the industry’s supply chain, the market’s value chain, the total pool of key players, market segmentation according to the industry trends (to the bottom-most level), regional markets, and key developments from market- and technology-oriented perspectives. The secondary data was collected and analyzed to determine the overall market size, further validated by primary research.

List of major secondary sources

|

Source |

Web Link |

|

Company Blogs |

https://www.lynred.com/blog/what-makes-infrared-market-unique |

|

News |

|

|

Infrared Commission on Non-ionizing Radiation Protection |

Primary Research

In the primary research process, various primary sources from both the supply and demand sides were interviewed to obtain qualitative and quantitative information for this report. The primary sources from the supply side included industry experts, such as chief executive officers (CEOs), vice presidents (VPs), marketing directors, technology and innovation directors, and related key executives from various key companies and organizations operating in the infrared imaging market. After the complete market engineering (calculations for market statistics, market breakdown, market size estimations, market forecasting, and data triangulation), extensive primary research was conducted to gather information and verify and validate the critical numbers arrived at. Primary research was also conducted to identify the segmentation types, industry trends, competitive landscape of infrared imaging solutions offered by various market players, and key market dynamics, such as drivers, restraints, opportunities, challenges, industry trends, and key player strategies.

In the complete market engineering process, the top-down and bottom-up approaches and several data triangulation methods were extensively used to perform the market estimation and market forecasting for the overall market segments and subsegments listed in this report. Extensive qualitative and quantitative analysis was performed on the complete market engineering process to list the key information/insights throughout the report.

Note: Other designations include sales, marketing, and product managers.

The three tiers of the companies were defined based on their total revenue as of 2024: tier 1: revenue greater than USD 1 billion, tier 2: revenue between USD 500 million and USD 1 billion, and tier 3: revenue less than USD 500 million.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

In the complete market engineering process, top-down and bottom-up approaches and several data triangulation methods were used to estimate and forecast the overall market segments and subsegments listed in this report. Key players in the market were identified through secondary research, and their market shares in the respective regions were determined through primary and secondary research. This entire procedure includes the study of annual and financial reports of the top market players and extensive interviews for key insights (quantitative and qualitative) with industry experts (CEOs, VPs, directors, and marketing executives).

All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources. All the parameters affecting the markets covered in this research study were accounted for, viewed in detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data. This data was consolidated and supplemented with detailed inputs and analysis from MarketsandMarkets and presented in this report. The following figure represents this study’s overall market size estimation process.

Infrared Imaging Market : Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall market size from the above estimation process, the market was split into several segments and subsegments. The data triangulation procedure was employed wherever applicable to complete the overall market engineering process and arrive at the exact statistics for all segments and subsegments. The data was triangulated by studying various factors and trends from both the demand and supply sides. Additionally, the market size was validated using top-down and bottom-up approaches.

Market Definition

Infrared imaging is an advanced technology that captures images of the infrared (IR) spectrum beyond the visible light range. Infrared Cameras convert IR radiation into visible images using detectors from materials such as indium gallium arsenide (InGaAs) and mercury cadmium telluride (MCT or HgCdTe). This technology enables the detection of heat signatures and temperature variations, allowing users to identify heat leaks in buildings, electrical faults, and locate people or animals in low-light conditions. Infrared imaging is also widely applied in astronomy, medical diagnostics, industrial inspection, and environmental monitoring, making it a versatile tool across diverse sectors.

Key Stakeholders

- Infrared imaging product manufacturers

- Infrared imaging product traders/suppliers

- Raw material suppliers and distributors

- Research organizations and consulting companies

- Associations, organizations, forums, and alliances related to infrared technology

- Technology investors

- Governments, regulatory bodies, and financial institutions

- Venture capitalists, private equity firms, and startups

- End users

Report Objectives

- To define, describe, and forecast the infrared imaging market, in terms of value, by type, component, technology, wavelength, application, vertical, and region

- To provide the market size estimation for North America, Europe, Asia Pacific, and Rest of the World (RoW), along with their respective country-level market sizes, in terms of value

- To describe and forecast the infrared imaging market for reflective and thermal cameras, in terms of volume

- To provide information about two types of infrared imaging products: Portable and fixed

- To provide detailed information regarding the drivers, restraints, opportunities, and challenges that influence market growth

- To provide a detailed overview of the infrared imaging value chain, ecosystem analysis, Porter’s five forces analysis, case studies, tariff analysis, regulations, pricing analysis, patent analysis, AI impact, and US tariff impact

- To strategically analyze micromarkets with respect to individual growth trends, prospects, and contributions to the total market

- To analyze key trends related to components, connectivity technologies, and applications that shape and influence the global infrared imaging market

- To profile key players and comprehensively analyze their ranking based on their revenues and core competencies

- To analyze opportunities in the market for stakeholders and provide a detailed competitive landscape of the market

- To analyze competitive developments in the infrared imaging market, such as expansions, agreements, partnerships, contracts, product developments, and research and development (R&D) activities

Available customizations:

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

- Detailed analysis and profiling of additional market players (up to 5)

- Additional country-level analysis of the infrared imaging market

Product Analysis

- The product matrix provides a detailed comparison of the product portfolio of each company in the infrared imaging market.

Key Questions Addressed by the Report

What is the current size of the global infrared imaging market?

The global infrared imaging market is estimated at USD 8.61 billion in 2025. (MarketsandMarkets)

What will be the projected size of the infrared imaging market by 2030?

The market is projected to reach USD 11.65 billion by 2030, driven by increased adoption in defense, industrial, and surveillance applications. (MarketsandMarkets)

What is the growth rate (CAGR) of the infrared imaging market?

The infrared imaging market is expected to grow at a CAGR of 6.2% during 2025–2030. (MarketsandMarkets)

What are the major growth drivers of the infrared imaging market?

Key drivers include rising demand for non-contact thermal monitoring, predictive maintenance, defense surveillance, healthcare diagnostics, and industrial automation. (MarketsandMarkets)

What are the major trends in the infrared imaging industry?

Key trends include AI-integrated thermal imaging, miniaturized sensors, improved image resolution, drone-based surveillance, and smart infrastructure applications. (MarketsandMarkets)

Which industries use infrared (IR) sensing and imaging technology?

Major industries include defense & military, healthcare, automotive, manufacturing, energy, electronics, and security & surveillance. (MarketsandMarkets)

Which companies are leading in the infrared imaging market?

Key players include Teledyne FLIR LLC, Fluke Corporation, L3Harris Technologies, Leonardo S.p.A., Axis Communications AB, RTX, Opgal Optronic Industries, Lynred, Allied Vision Technologies, and BAE Systems. (MarketsandMarkets)

Which segment is expected to grow fastest in the infrared imaging market?

The reflective segment is expected to register the highest growth, while cameras dominate the component segment due to expanding industrial and security applications. (MarketsandMarkets)

Which region dominates the infrared imaging market?

North America leads with 47.1% market share in 2025, driven by strong defense spending and industrial adoption. (MarketsandMarkets)

What does the MarketsandMarkets infrared imaging report cover?

The report includes market sizing (2025–2030), segmentation by type, wavelength, component, technology, application, regional analysis, and competitive landscape with 260+ pages and 225+ tables. (MarketsandMarkets)

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Infrared Imaging Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

- US Infrared Imaging Market

- Canada Infrared Imaging Market

- Mexico Infrared Imaging Market

- Germany Infrared Imaging Market

- UK Infrared Imaging Market

- France Infrared Imaging Market

- Italy Infrared Imaging Market

- China Infrared Imaging Market

- Japan Infrared Imaging Market

- India Infrared Imaging Market

- Rest Of Europe Infrared Imaging Market

- Rest Of Asia Pacific Infrared Imaging Market

- Bahrain Infrared Imaging Market

- Kuwait Infrared Imaging Market

- Oman Infrared Imaging Market

- Qatar Infrared Imaging Market

Growth opportunities and latent adjacency in Infrared Imaging Market

Nicholas

Apr, 2026

What are the latest technological trends in infrared imaging, including cloud integration, AI-based imaging, and advancements in thermal cameras?.

Cary

Apr, 2026

How are different wavelength technologies (NIR, SWIR, MWIR, LWIR) used in infrared imaging, and which industries benefit most from each type?.

User

Sep, 2019

Thermal hyperspectral imagers provide information that conventional spectral imagers cannot. A broader range of materials can be detected, mapped, and sorted by thermal hyperspectral imagers. We are planning to expand our offerings in this area so wanted to know if insights on thermal hyperspectral imaging present in the report..

User

Sep, 2019

I can see that the SWIR technology is witnessing significant growth in the infrared imaging market. We are planning include SWIR technology based products in our product portfolio, so would like to have an estimate of the SWIR market in China, and South Korea..

User

Sep, 2019

We are into the business of providing infrared cameras, and want to explore the market for infrared sensors. We are particularly interested in volume data of IR sensors, is it covered in the study?.

User

Nov, 2019

LWIR and MWIR are the prominent technologies in the infrared market, while NIR and SWIR are the emerging ones. Can you tell me if the report analyzes the market between NIR, LWIR, MWIR, and SWIR technologies? .

User

Mar, 2019

My company is engaged in providing hardware and software solutions for infrared camera. Our solutions are aimed at automated process monitoring application. Is the information on this application available in the report?.