Request Customisation

Request Customisation

Microfluidics Market

Report Code

AST 7541

Published in

Jan, 2026, By MarketsandMarkets™

Microfluidics Market by Product (Chip, Sensor, Valve, Pump, Needle), Material (Silicon, Polymer), Application [Diagnostics (Clinical, PoC), Research (Proteomics, Genomics, Cell), Therapeutics (Drug Delivery Wearables)], End User � Global forecast to 2030

$24.96B

MARKET SIZE, 2025

$37.19B

MARKET SIZE, 2030

8.3%

CAGR (2025-2030)

2025-2030

FORECAST PERIOD

OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

The global Microfluidics market, valued at US$23.71 billion in 2024, stood at US$24.96 billion in 2025 and is projected to advance at a resilient CAGR of 8.3% from 2025 to 2030, culminating in a forecasted valuation of US$37.19 billion by the end of the period. Several significant factors are driving the growth of the microfluidics market, thereby enhancing its expansion and applications. There is a growing demand for point-of-care diagnostics, which require fast, accurate, and cost-effective instruments. Moreover, the trend toward personalized medicine raises the requirement for precise biomarker analysis and high-throughput screening. An increase in research & development expenditure supports the research and investigation of novel and innovative technologies, which in turn supports market growth.

KEY TAKEAWAYS

-

MARKET SNAPSHOT:

Base Year Market Size (2024): USD 23.71 Billion

Current Market Size (2025): USD 24.96 Billion

Forecast Market Size (2030): USD 37.19 Billion

CAGR (2025–2030): 8.3% -

SEGMENT LEADERSHIP:

Regional Leader: North America accounted for the largest share of the global microfluidics market with a share of 40.6% in 2024.

Product Leader: Microfluidics-based devices accounted for the largest market share of 70.5% in 2024.

Application Leader: In vitro diagnostics is expected to dominate the overall market.

End User Leader: Hospitals and diagnostic centers are projected to register the highest growth during the forecast period. -

MARKET OUTLOOK & COMPETITIVE LANDSCAPE:

Thermo Fisher Scientific, Illumina Inc., and Bio-Rad Laboratories Inc. are identified as key players in the microfluidics market, given their strong market share and extensive product footprint.

Companies such as QuidelOrtho Corporation, Hologic, Inc., and Aignep s.p.a. have distinguished themselves among startups and SMEs by securing strong footholds in specialized niche areas, underscoring their potential as emerging market leaders.

Several significant reasons are driving the growth of the microfluidics market. There is a rising demand for point-of-care diagnostics, which require fast, accurate, and cost-efficient instruments. Moreover, the trend toward personalized medicine raises the requirement for precise biomarker analysis and high-throughput screening. An increase in research & development expenditure supports the research and investigation of novel and innovative technologies, which in turn supports market growth.

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The microfluidics market is being reshaped by the convergence of miniaturization, automation, and digital integration across healthcare and research applications. Hospitals, academic institutions, and pharmaceutical companies are increasingly adopting microfluidic technologies for rapid diagnostics, precise drug discovery, and advanced cell-based studies. These systems enable faster results using minimal samples and reagents, thereby improving cost efficiency and laboratory sustainability. The shift toward portable and point-of-care testing is further disrupting traditional laboratory workflows, allowing quicker clinical decisions and broader access to diagnostics. Collectively, these advancements are enhancing research productivity, accelerating therapeutic innovation, and driving the evolution of a more connected, data-driven healthcare ecosystem.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Growing requirement for point-of-care testing

-

Increasing focus on data precision and accuracy

RESTRAINTS

Impact

Level

Level

-

Stringent regulatory approval process

-

Integration of microfluidics into the current workflow

OPPORTUNITIES

Impact

Level

Level

-

Emergence of 3D cell culture systems

-

Growth potential of emerging economies

CHALLENGES

Impact

Level

Level

-

Low adoption of microfluidic devices among end users

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Rising technological advancements

Technological advancements in microfluidic components aim to make healthcare industry operational processes more reliable. These technological advancements have increased the throughput of device production, improved rapid prototyping efforts, and enabled researchers to enhance the complexity and sophistication of experiments that can be performed on a microfluidic chip. With technological advancements, microfluidic components are rapidly becoming a key technology in an expanding range of fields, including medical sciences, pharmaceuticals, biosensing, bioactuation, and chemical synthesis. This indicates the transition of microfluidics from a promising R&D tool to being utilized in data collection with AI during clinical trials. Lab-on-a-chip technology is a powerful platform for constructing and implementing AI in a large-scale, cost-effective, high-throughput, automated, and multiplexed manner. 3D printing has significantly transformed the field of microfluidics, enabling the creation of innovative devices that are often unattainable with traditional methods. A research team led by Imperial College London (UK) pioneered a 3D-printed wearable microfluidic device, which integrates FDA-approved clinical microdialysis probes and needle-type biosensors to continuously monitor metabolite levels in human tissues. Organ-on-a-Chip systems are microfluidic devices designed to replicate an intricate physiological environment for culturing and controlling cells within a 2D or 3D structure that mimics a specific organ in the body. Paper-based microfluidics focuses on devices constructed from paper or other porous materials that transport fluids through capillary action. The continual evolution of new materials and fabrication methods is expanding the potential applications of microfluidics, driving ongoing growth and innovation in the market.

Restraint: Integration of microfluidics into the current workflow

End users face various technical issues while incorporating microfluidic devices into existing workflows. Owing to this, the adoption of microfluidics into regularized drug screening and drug discovery processes is limited. Currently, microfluidics technology presents significant opportunities for the further miniaturization and integration of instruments and exhibits the potential for greater automation and cost reduction in drug discovery and development processes. However, as per a few industry experts in the market, although microfluidics adds value to the process and instruments, it will likely take about 10 to 15 years before this technology completely replaces conventional macro-scale research instrumentation. Until such a scenario presents itself, the market will witness irregular installments of microfluidic devices, owing to which conventional technology providers will sideline manufacturers to some extent.

Opportunity: Emergence of 3D cell culture systems

The organ-on-a-chip (OoC) represents a fascinating advancement in science and technology, combining biological systems with microtechnology to replicate essential features of human physiology. This device is a microfluidic system equipped with intricate networks of ultra-fine microchannels designed to control and manipulate minimal volumes of fluids, ranging from picoliters to milliliters. Recent advances in microfluidics for 3D cell culture have enabled the development of microenvironments that support tissue differentiation and replicate the tissue-tissue interface, spatiotemporal chemical gradients, and mechanical microenvironments of living organs. Organs-on-chips (OoCs) feature engineered or natural miniature tissues cultivated within microfluidic chips. These chips are designed to replicate human physiology by controlling cellular microenvironments and preserving tissue-specific functions. By integrating advancements in tissue engineering and microfabrication, OoCs have emerged as a cutting-edge experimental platform for exploring human pathophysiology and assessing the impact of therapeutics within the body. Given its potential, several research studies are being conducted to evaluate the performance of microfluidic chips in pharmaceutical studies. There are different types of organ-on-a-chip systems, such as lung-on-a-chip, liver-on-a-chip, heart-on-a-chip, brain-on-a-chip, and gut-on-a-chip models. A group of researchers developed U-IMPACT, a 3D microfluidic cell culture platform, a 96-well microfluidic platform engineered for culturing cells and spheroids, facilitating research on tumor microenvironments and neural cell development. Another team developed a hydrogel-based microfluidic cell culture platform, which enables the assessment of drug diffusion and efficacy, including for drugs such as temozolomide and carmustine, by producing dose-response curves and replicating the glioblastoma microenvironment for in vitro experimentation. The increasing applications of microfluidics in 3D cell culture will offer an array of opportunities for the growth of the microfluidics market.

Challenge: Low adoption of microfluidic devices among end users

Customer acceptance and market adoption are the two key factors that affect the commercialization of any product or technology in the market. There are academic publications providing proof of concept for microfluidic technology-embedded medical devices and equipment. Still, the incorporation of this technology in end-use products has been limited due to inadequate standards of microfluidic devices. The high costs associated with developing and producing microfluidic devices create financial hurdles, making them less accessible to smaller labs or organizations. The intricate design and manufacturing processes demand specialized knowledge and expertise, which can deter users from using the necessary resources. Additionally, a lack of awareness and understanding of the advantages and functions of microfluidic technology contributes to its slow adoption. Finally, concerns about the reliability and performance of these devices may lead users to hesitate, especially if the technology appears untested or more complicated than traditional methods. The limited adoption of microfluidic devices is owing to the development costs, complex manufacturing, regulatory challenges, integration difficulties, insufficient awareness, performance concerns, and the high cost of adoption for many users.

MICROFLUIDICS MARKET SIZE, GROWTH, SHARE & TRENDS ANALYSIS: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

The QuantStudio Absolute Q Digital PCR System leverages Microfluidic Array Plate (MAP) technology to deliver precise partitioning and analysis in a single, integrated workflow. | Streamlined digital PCR with higher accuracy, reproducibility, and ease of use | Reduced hands-on time and error rates through automated background correction and false-positive rejection |

|

It introduced the JSY3000-L/P valve manifold series with up to 64 stations for centralized control of solenoid valves and electro-pneumatic regulators. | Simplified control architecture with reduced wiring and assembly time, saving up to 28% space | Enhanced reliability through IP65/IP67 protection and remote diagnostics for higher uptime and easier maintenance |

|

It launched the Illumina Complete Long Read technology, enabling both long- and short-read sequencing on a single NovaSeq X Series platform. | Simplified sequencing workflow with high precision (F1 score 99.87%), reduced cost, and minimal sample requirements |

|

It enabled rapid, decentralized diagnostics with high accuracy and minimal hands-on time. It improved antibiotic stewardship and patient management by providing targeted results at the point of care. | Enabled rapid, decentralized diagnostics with high accuracy and minimal hands-on time |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The microfluidics market brings together a wide network of innovators—from manufacturers and researchers to distributors and end users—all working to transform diagnostics and analytical testing. Manufacturers develop and refine instruments, chips, and consumables, often partnering with contract developers and production specialists to scale new technologies efficiently. Research and product development are powered by academic labs, CROs, and in-house R&D teams that explore new applications, optimize designs, and push performance boundaries. Distributors, including third-party suppliers and online platforms, play a key role in connecting these innovations to global customers quickly and effectively. On the demand side, hospitals, diagnostic labs, and pharmaceutical and biotech companies rely on microfluidic systems for rapid testing, precision analysis, and drug discovery. Supporting this ecosystem are investors, funding agencies, and regulatory bodies that ensure quality, guide innovation, and help shape market direction. Together, they form a dynamic environment that continues to drive the evolution of microfluidic technologies.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Microfluidics Market, By Product

Based on product, the microfluidics market is segmented into microfluidics-based devices and microfluidic components. Microfluidics-based devices are advanced instruments that can regulate and analyze small volumes of fluids. They accurately manage fluid flow by etching or molding micro-scale channels and chambers into substrates. These devices are also used in organ-on-a-chip (OOC) platforms, which replicate human organ functions to aid in drug testing and disease-related research, as well as lab-on-a-chip (LoC) systems that combine multiple laboratory procedures into a single chip. These devices also include assays and microfluidic sensors that offer precise detection of pathogens, biomolecules, and other chemical compounds.

Microfluidics Market, By Application

In vitro diagnostics (IVD) have the ability to accurately regulate and analyze minute fluid volumes due to their integration with microfluidic technology. This inclusion increases the speed of the test, while also making it cheaper, more accurate, and more automated in IVD systems. This technique can be helpful for diagnostic purposes, from standard blood and urine tests to sophisticated assays for infectious and cancerous disorders. Furthermore, the growing demand for point-of-care testing is enhancing the use of microfluidics in IVD.

Microfluidics Market, By End User

Due to their potential to generate requirements for advanced diagnostic and analytical techniques, hospitals and diagnostic centers are the key end users of microfluidics. Faster, precise, and efficient testing is carried out by microfluidic devices, which is crucial in healthcare settings where faster results can significantly impact patient care. These instruments offer precise, high-throughput results with less volume of sample for numerous uses, such as point-of-care testing and disease diagnostics. Improved patient outcomes result from the application of microfluidics in workflows, which enhances the potential to conduct intricate assays and screenings. Hospitals and diagnostic centers play a significant role in the expansion and advancement of the microfluidics market due to their increasing application of microfluidic technologies.

REGION

By region, Asia Pacific is projected to grow at a significant CAGR during the forecast period

The microfluidics market in the Asia Pacific region is expanding significantly. This is attributed to the rapid infrastructure development in this region and the growing demand for advanced diagnostic and analytical technologies. The countries in this region are heavily investing in the advancement of their healthcare systems and the application of innovative medical technologies, like microfluidic devices. The growing prevalence of chronic disorders and the need for efficient diagnostic instruments are further propelling the growth of this market. The region has strong manufacturing capacity and can provide microfluidic technology at an affordable rate. Moreover, significant research and development initiatives, when combined with supportive financial help and governmental policies, foster innovation and accelerate market growth.

MICROFLUIDICS MARKET SIZE, GROWTH, SHARE & TRENDS ANALYSIS: COMPANY EVALUATION MATRIX

In the microfluidics market, leading companies are advancing miniaturized fluid-handling technologies that enable high-precision diagnostics, molecular analysis, and drug discovery applications. Thermo Fisher Scientific, Illumina Inc., and Bio-Rad Laboratories have established dominant positions through integrated microfluidic platforms for PCR, sequencing, and lab-on-chip diagnostics, supported by robust global distribution and R&D capabilities. Emerging players, such as QuidelOrtho Corporation, Hologic Inc., and Aignep S.p.A., are differentiating themselves through focused innovations in cartridge-based assays, portable testing modules, and fluid-control systems. Together, these players are shaping the evolution of microfluidic technologies—driving faster, more automated, and cost-efficient analytical solutions across research and clinical settings.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

- Abbott Laboratories (US)

- Agilent Technologies Inc. (US)

- Aignep S.P.A (Italy)

- bioMérieux (France)

- BD (US)

- Bio-Rad Laboratories Inc. (US)

- Danaher Corporation (US)

- Illumina Inc. (US)

- Parker Hannifin Corporation (US)

- Thermo Fisher Scientific Inc. (US)

- SMC Corporation (Japan)

- IDEX Corporation (US)

- Fortive Corporation (US)

- PerkinElmer Inc. (US)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Standard BioTools Inc. (US)

- QuidelOrtho Corporation (US)

- Hologic Inc. (US)

- Dolomite Microfluidics (UK)

- Elveflow (France)

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2025 (Value) | USD 24.96 BN |

| Market Forecast in 2030 (Value) | USD 37.19 BN |

| Growth Rate | CAGR of 8.3% from 2025-2030 |

| Years Considered | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Procedure) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered | Products (Microfluidics-Based Devices, Microfluidics Components), Application (IVD, Pharma & Life Science Research, Therapeutics), and End-user (Hospitals and Diagnostic Centers, Academia & Research Institutes, and Pharmaceutical & Biotechnology Companies) |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

WHAT IS IN IT FOR YOU: MICROFLUIDICS MARKET SIZE, GROWTH, SHARE & TRENDS ANALYSIS REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Evaluate commercialization pathways for lab-on-chip systems | Delivered a breakdown of commercialization models across diagnostic, pharma, and industrial segments, mapping product maturity, IP transfer mechanisms, and scalability barriers | Enabled the client to identify high-feasibility business models and partnership entry points for transitioning academic prototypes into market-ready solutions |

| Assess integration potential of AI and digital microfluidics |

|

Provided forward-looking intelligence on digital convergence, enabling the client to anticipate automation opportunities in next-generation device development |

RECENT DEVELOPMENTS

- 7/1/2024 12:00:00 AM : Illumina. Inc. (US) acquired Fluent BioSciences (US) to enhance its ability for single-cell analysis.

- 12/1/2023 12:00:00 AM : Danaher Corporation (US) acquired Abcam plc (UK) to expand its reach in the proteomics area.

- 6/1/2024 12:00:00 AM : bioMérieux (France) introduced the BIOFIRE SPOTFIRE R/ST Panel Mini, which is a specialized multiplex PCR test that identifies five of the most prevalent viral & bacterial pathogens responsible for respiratory or sore throat infections, delivering results in approximately 15 minutes.

- 3/1/2023 12:00:00 AM : Danaher (US) partnered with UPenn to develop new technologies that are expected to improve the consistency of clinical outcomes for patients. This partnership is also expected to overcome manufacturing bottlenecks in the delivery of next-gen engineered cell products.

- 6/1/2024 12:00:00 AM : The US FDA granted 510(k) clearance to Thermo Fisher Scientific's (US) SeCore CDx HLA A Sequencing System for use as a companion diagnostic with Adaptimmune's recently approved TCR therapy, TECELRA (afamitresgene autoleucel), targeting adults with unresectable or metastatic synovial sarcoma.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

30

2

EXECUTIVE SUMMARY

36

3

PREMIUM INSIGHTS

42

4

MARKET OVERVIEW

Microfluidics market poised for growth with 3D printing integration and rising precision medicine demand.

46

4.1

INTRODUCTION

4.2

MARKET DYNAMICS

4.2.1

DRIVERS

4.2.1.1

INTEGRATION OF MICROFLUIDICS WITH 3D PRINTING

4.2.2

E-HEALTH AND DIGITAL DIAGNOSTICS DRIVING MICROFLUIDICS ADOPTION

4.2.2.1

INCREASING PREVALENCE OF CHRONIC DISEASES FUELING POC TESTING

4.2.2.2

INCREASING FOCUS ON DATA PRECISION AND ACCURACY

4.2.3

RESTRAINTS

4.2.3.1

REGULATORY AND CLINICAL VALIDATION BARRIERS

4.2.3.2

MATERIAL SELECTION FOR MICROFLUIDIC DEVICES

4.2.4

OPPORTUNITIES

4.2.4.1

ADVANCING MICROFLUIDICS FOR REAL-TIME FOOD SAFETY MONITORING

4.2.4.2

RISING DEMAND FOR ORGAN-ON-A-CHIP PLATFORMS IN PRECISION MEDICINE

4.2.5

CHALLENGES

4.2.5.1

LIMITED ADOPTION OF MICROFLUIDIC DEVICES

4.2.5.2

TECHNICAL AND OPERATIONAL LIMITATIONS

4.3

UNMET NEEDS

4.4

INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.5

STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5

STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, AND AI ADOPTION

Harness AI-driven microfluidics innovations to unlock market potential and strategic patent advantages.

56

5.1

KEY TECHNOLOGIES

5.1.1

MICROFABRICATION

5.1.2

MATERIAL SCIENCE

5.1.3

OPTOFLUIDICS

5.2

COMPLEMENTARY TECHNOLOGIES

5.2.1

MICRO-ELECTRO-MECHANICAL SYSTEMS (MEMS)

5.2.2

WEARABLE & IMPLANTABLE MICROFLUIDICS

5.3

PATENT ANALYSIS

5.3.1

INNOVATIONS AND PATENT REGISTRATIONS

5.4

FUTURE APPLICATIONS

5.5

IMPACT OF AI/GENAI ON MICROFLUIDICS MARKET

5.5.1

TOP USE CASES AND MARKET POTENTIAL

5.5.2

BEST PRACTICES IN MICROFLUIDICS

5.5.3

CASE STUDIES OF AI IMPLEMENTATION IN MICROFLUIDICS MARKET

5.5.4

INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

5.5.5

CLIENT'S READINESS TO ADOPT GENERATIVE AI IN MICROFLUIDICS MARKET

5.6

SUCCESS STORIES AND REAL-WORLD APPLICATIONS

5.7

REGULATORY LANDSCAPE

5.7.1

NORTH AMERICA

5.7.1.1

US

5.7.1.2

CANADA

5.7.2

EUROPE

5.7.3

ASIA PACIFIC

5.7.3.1

JAPAN

5.7.3.2

CHINA

5.7.3.3

INDIA

5.7.4

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6

CUSTOMER LANDSCAPE & BUYER BEHAVIOR

Understand stakeholder influence and unmet needs to optimize microfluidic component purchasing decisions.

73

6.1

BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

6.1.1

KEY STAKEHOLDERS IN BUYING PROCESS

6.1.2

BUYING CRITERIA

6.2

DECISION-MAKING PROCESS

6.3

ADOPTION BARRIERS & INTERNAL CHALLENGES

6.4

UNMET NEEDS FROM END USERS

7

INDUSTRY TRENDS

Identify strategic opportunities in microfluidics through competitive forces and regional economic insights.

78

7.1

PORTER’S FIVE FORCES ANALYSIS

7.1.1

THREAT OF NEW ENTRANTS

7.1.2

THREAT OF SUBSTITUTES

7.1.3

BARGAINING POWER OF SUPPLIERS

7.1.4

BARGAINING POWER OF BUYERS

7.1.5

INTENSITY OF COMPETITIVE RIVALRY

7.2

MACROECONOMIC INDICATORS

7.2.1

INTRODUCTION

7.2.2

HEALTHCARE EXPENDITURE AND INFRASTRUCTURE OUTLOOK

7.2.3

MACROECONOMIC OUTLOOK FOR NORTH AMERICA

7.2.4

MACROECONOMIC OUTLOOK FOR EUROPE

7.2.5

MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

7.2.6

MACROECONOMIC OUTLOOK FOR LATIN AMERICA

7.2.7

MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

7.2.8

TRENDS IN GLOBAL MICROFLUIDICS INDUSTRY

7.3

VALUE CHAIN ANALYSIS

7.3.1

RESEARCH & DEVELOPMENT

7.3.2

RAW MATERIAL PROCUREMENT & MANUFACTURING

7.3.3

MARKETING & SALES, DISTRIBUTION, AND POST-SALES SERVICES

7.4

ECOSYSTEM ANALYSIS

7.5

PRICING ANALYSIS

7.5.1

AVERAGE SELLING PRICE TREND, BY REGION

7.5.2

AVERAGE SELLING PRICE OF MICROFLUIDIC COMPONENTS, BY KEY PLAYERS

7.6

TRADE DATA ANALYSIS

7.6.1

IMPORT DATA (HS CODE 3822)

7.6.2

EXPORT DATA (HS CODE 3822)

7.7

KEY CONFERENCES & EVENTS, 2026-2027

7.8

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

7.9

INVESTMENT & FUNDING SCENARIO

7.10

CASE STUDY ANALYSIS

7.10.1

CASE STUDY 1: MULTIPLEX MICROFLUIDIC CIRCUIT FOR BLOOD VESSEL-ON-A-CHIP PERFUSION USING FLOWEZ

7.10.2

CASE STUDY 2: MICROFLUIDIC SYSTEM FOR ROBOTIC HAND PLAYING NINTENDO

7.10.3

CASE STUDY 3: 3D-PRINTED MICROFLUIDIC DEVICES USING POLYJET TECHNOLOGY

7.11

IMPACT OF 2025 US TARIFFS ON MICROFLUIDICS MARKET

7.11.1

INTRODUCTION

7.11.2

KEY TARIFF RATES

7.11.3

PRICE IMPACT ANALYSIS

7.11.4

IMPACT ON COUNTRY/REGION

7.11.5

IMPACT ON END-USE INDUSTRIES

8

MICROFLUIDICS MARKET, BY PRODUCT

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 28 Data Tables

99

8.1

INTRODUCTION

8.2

MICROFLUIDICS-BASED DEVICES

8.2.1

HIGH UPTAKE OF POC TESTING AND ORGAN-ON-A-CHIP SYSTEMS TO DRIVE MARKET

8.2.2

POLYMERASE CHAIN REACTION (PCR) SYSTEMS

8.2.3

MICROFLUIDIC CAPILLARY ELECTROPHORESIS

8.2.4

NEXT-GENERATION SEQUENCING (NGS) SYSTEMS

8.2.5

DROPLET & PARTICLE PRODUCTION SYSTEMS

8.3

OTHER DEVICES

8.4

MICROFLUIDIC COMPONENTS

8.4.1

CRUCIAL FOR CONTINUOUS HEALTH MONITORING

8.4.2

MICROFLUIDIC COMPONENTS, BY TYPE

8.4.2.1

MICROFLUIDIC CHIPS

8.4.2.2

FLOW & PRESSURE SENSORS

8.4.2.3

FLOW & PRESSURE CONTROLLERS

8.4.2.4

MICROFLUIDIC VALVES

8.4.2.5

MICROPUMPS

8.4.2.6

MICRONEEDLES

8.4.2.7

OTHER MICROFLUIDIC COMPONENTS

8.4.3

MICROFLUIDIC COMPONENTS, BY MATERIAL

8.4.3.1

SILICON

8.4.3.2

POLYMETHYL METHACRYLATE (PMMA)

8.4.3.3

POLYDIMETHYLSILOXANE (PDMS)

8.4.3.4

CYCLIC OLEFIN COPOLYMER (COC)

8.4.3.5

GLASS

8.4.3.6

OTHER MATERIALS

9

MICROFLUIDICS MARKET, BY APPLICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 24 Data Tables

119

9.1

INTRODUCTION

9.2

IN VITRO DIAGNOSTICS (IVD)

9.2.1

CLINICAL DIAGNOSTICS

9.2.1.1

GROWING FOCUS ON EARLY DISEASE DETECTION TO DRIVE MARKET

9.2.2

POINT-OF-CARE TESTING (POCT)

9.2.2.1

INCREASING DEMAND FOR DECENTRALIZED INFECTIOUS DISEASE TESTING TO DRIVE MARKET

9.2.3

VETERINARY DIAGNOSTICS

9.2.3.1

RISING DEMAND FOR RAPID, FIELD-DEPLOYABLE VETERINARY DIAGNOSTICS TO DRIVE MARKET

9.3

THERAPEUTICS

9.3.1

DRUG DELIVERY

9.3.1.1

ABILITY TO ENABLE SCALABLE PRODUCTION OF POLYMER-BASED DRUG PARTICLES TO DRIVE MARKET

9.3.2

WEARABLE

9.3.2.1

ABILITY TO ENABLE PROACTIVE MANAGEMENT OF HYDRATION, METABOLIC STATUS, AND DISEASE BIOMARKERS TO DRIVE MARKET

9.4

PHARMACEUTICAL & LIFE SCIENCE RESEARCH

9.4.1

LAB ANALYTICS

9.4.1.1

PROTEOMIC ANALYSIS

9.4.1.1.1

UTILIZATION OF PROTEOMES-ON-A-CHIP DEVICES FOR THERAPEUTIC DEVELOPMENT TO DRIVE MARKET

9.4.1.2

GENOMIC ANALYSIS

9.4.1.2.1

HIGH-THROUGHPUT, COST-EFFECTIVE GENOMIC ANALYSIS ENABLED BY MICROFLUIDICS

9.4.1.3

CELL-BASED ASSAYS

9.4.1.3.1

MICROFLUIDIC CO-CULTURES ENABLE PRECISE, HIGH-THROUGHPUT MODELING OF COMPLEX TISSUES FOR DRUG TESTING AND DISEASE RESEARCH

9.4.1.4

CAPILLARY ELECTROPHORESIS

9.4.1.4.1

ENABLES HIGH-THROUGHPUT, PRECISE, AND COST-EFFICIENT PROTEIN AND NUCLEIC ACID ANALYSIS

9.4.2

MICRODISPENSING

9.4.2.1

SUITABILITY FOR LOW-VISCOSITY APPLICATIONS TO SUPPORT MARKET GROWTH

9.4.3

MICROREACTORS

9.4.3.1

GROWING ADOPTION OF CONTINUOUS FLOW SYNTHESIS IN RESEARCH & DEVELOPMENT TO DRIVE MARKET

10

MICROFLUIDICS MARKET, BY END USER

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 6 Data Tables

135

10.1

INTRODUCTION

10.2

HOSPITALS & DIAGNOSTIC CENTERS

10.2.1

RISING DEPENDENCE ON RAPID MICROFLUIDIC MOLECULAR DIAGNOSTICS TO DRIVE GROWTH

10.3

PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

10.3.1

STRONG ADOPTION OF MICROFLUIDIC TECHNOLOGIES FOR PRECISE FORMULATION, NANOPARTICLE PRODUCTION, AND TOXICITY TESTING TO DRIVE GROWTH

10.4

ACADEMIC & RESEARCH INSTITUTES

10.4.1

INVESTMENTS IN BIOMEDICAL & LIFE SCIENCE RESEARCH TO DRIVE GROWTH

11

MICROFLUIDICS MARKET, BY REGION

Comprehensive coverage of 8 Regions with country-level deep-dive of 14 Countries | 132 Data Tables.

141

11.1

INTRODUCTION

11.2

NORTH AMERICA

11.2.1

US

11.2.1.1

EXPANSION OF APPLICATIONS BEYOND TRADITIONAL DIAGNOSTICS TO DRIVE MARKET

11.2.2

CANADA

11.2.2.1

GOVERNMENT FUNDING AND COLLABORATIVE ECOSYSTEMS TO SUPPORT GROWTH

11.3

EUROPE

11.3.1

GERMANY

11.3.1.1

ONGOING INVESTMENTS IN SEMICONDUCTORS AND MICROELECTRONICS TO DRIVE MARKET

11.3.2

FRANCE

11.3.2.1

RISING DEMAND FOR ADVANCED LAB-ON-CHIP AND ORGAN-ON-CHIP SOLUTIONS TO DRIVE MARKET

11.3.3

UK

11.3.3.1

RISING CASES OF CHRONIC DISEASES AND INCREASING DEMAND FOR POC TESTING TO BOOST DEMAND

11.3.4

ITALY

11.3.4.1

SHIFT TOWARD COST-EFFICIENT MICROFLUIDIC PLATFORMS FOR DIAGNOSTICS, ENVIRONMENTAL TESTING, AND ADVANCED BIOMEDICAL RESEARCH TO DRIVE MARKET

11.3.5

SPAIN

11.3.5.1

INCREASING DEMAND FOR ACCESSIBLE POINT-OF-CARE AND LAB-ON-CHIP SOLUTIONS TO DRIVE MARKET

11.3.6

REST OF EUROPE

11.4

ASIA PACIFIC

11.4.1

CHINA

11.4.1.1

GOVERNMENT SUPPORT AND STRATEGIC PARTNERSHIPS TO DRIVE MARKET

11.4.2

JAPAN

11.4.2.1

GOVERNMENT SUPPORT, INNOVATION, AND INDUSTRY-ACADEMIA COLLABORATION TO DRIVE GROWTH

11.4.3

INDIA

11.4.3.1

GROWING BIOTECH STARTUP ECOSYSTEM AND RESEARCH FROM PREMIER INSTITUTIONS TO DRIVE MARKET

11.4.4

AUSTRALIA

11.4.4.1

INNOVATION ECOSYSTEM, R&D STRENGTH, AND PRECISION ENGINEERING TO SUPPORT GROWTH

11.4.5

SOUTH KOREA

11.4.5.1

ADVANCED RESEARCH, GLOBAL PARTNERSHIPS, AND NEXT-GEN TECHNOLOGIES TO DRIVE MARKET

11.4.6

REST OF ASIA PACIFIC

11.5

LATIN AMERICA

11.5.1

BRAZIL

11.5.1.1

RISING INVESTMENT IN HEALTHTECH AND EMPHASIS ON MOLECULAR DIAGNOSTICS TO DRIVE MARKET

11.5.2

MEXICO

11.5.2.1

GROWING DEMAND FOR ADVANCED DIAGNOSTICS AND BIOTECH INNOVATION TO DRIVE MARKET

11.5.3

REST OF LATIN AMERICA

11.6

MIDDLE EAST & AFRICA

11.6.1

GCC COUNTRIES

11.6.1.1

DISEASE BURDEN AND HEALTHCARE MODERNIZATION TO DRIVE MARKET

11.6.2

REST OF MIDDLE EAST & AFRICA

12

COMPETITIVE LANDSCAPE

Discover strategic insights and market positions of key players shaping the microfluidics industry.

203

12.1

INTRODUCTION

12.2

KEY PLAYER STRATEGIES/RIGHT TO WIN

12.3

OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN MICROFLUIDICS MARKET

12.4

REVENUE ANALYSIS, 2022–2024

12.5

MARKET SHARE ANALYSIS, 2024

12.6

RANKING OF KEY MARKET PLAYERS

12.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.7.1

STARS

12.7.2

EMERGING LEADERS

12.7.3

PERVASIVE PLAYERS

12.7.4

PARTICIPANTS

12.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.7.5.1

COMPANY FOOTPRINT

12.7.5.2

REGION FOOTPRINT

12.7.5.3

PRODUCT FOOTPRINT

12.7.5.4

APPLICATION FOOTPRINT

12.7.5.5

END USER FOOTPRINT

12.8

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

12.8.1

PROGRESSIVE COMPANIES

12.8.2

RESPONSIVE COMPANIES

12.8.3

DYNAMIC COMPANIES

12.8.4

STARTING BLOCKS

12.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

12.8.5.1

LIST OF KEY STARTUP/SME PLAYERS

12.8.5.2

COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

12.9

COMPANY VALUATION & FINANCIAL METRICS

12.9.1

FINANCIAL METRICS

12.9.2

COMPANY VALUATION

12.10

BRAND/PRODUCT COMPARATIVE ANALYSIS

12.11

COMPETITIVE SCENARIO

12.11.1

PRODUCT LAUNCHES & APPROVALS

12.11.2

DEALS

12.11.3

EXPANSIONS

12.11.4

OTHER DEVELOPMENTS

13

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

220

13.1

KEY PLAYERS

13.1.1

DANAHER CORPORATION

13.1.1.1

BUSINESS OVERVIEW

13.1.1.2

PRODUCTS OFFERED

13.1.1.3

RECENT DEVELOPMENTS

13.1.1.3.1

DEALS

13.1.1.3.2

EXPANSIONS

13.1.1.4

MNM VIEW

13.1.1.4.1

KEY STRENGTHS

13.1.1.4.2

STRATEGIC CHOICES

13.1.1.4.3

WEAKNESSES & COMPETITIVE THREATS

13.1.2

ILLUMINA, INC.

13.1.3

BIOMÉRIEUX

13.1.4

THERMO FISHER SCIENTIFIC INC.

13.1.5

ABBOTT LABORATORIES

13.1.6

PARKER HANNIFIN CORP

13.1.7

SMC CORPORATION

13.1.8

IDEX CORPORATION

13.1.9

FORTIVE

13.1.10

REVVITY, INC.

13.1.11

AGILENT TECHNOLOGIES, INC.

13.1.12

BIO-RAD LABORATORIES, INC.

13.1.13

BECTON, DICKINSON AND COMPANY

13.1.14

F. HOFFMANN-LA ROCHE LTD.

13.1.15

STANDARD BIOTOOLS

13.1.16

QUIDELORTHO CORPORATION

13.1.17

AIGNEP S.P.A.

13.1.18

DOLOMITE MICROFLUIDICS

13.1.19

ELVEFLOW

13.2

OTHER PLAYERS

13.2.1

NANOSTRING TECHNOLOGIES

13.2.2

INNOVATIVE BIOCHIPS, LLC

13.2.3

FLUIDIC ANALYTICS

13.2.4

HORIBA

13.2.5

MICRONIT B.V.

13.2.6

EMULATE, INC.

13.2.7

SPHERE BIO

13.2.8

ZEON CORPORATION

13.2.9

QIAGEN N.V.

14

RESEARCH METHODOLOGY

302

14.1

RESEARCH DATA

14.2

RESEARCH DESIGN

14.2.1

SECONDARY RESEARCH

14.2.1.1

OBJECTIVES OF SECONDARY RESEARCH

14.2.1.2

KEY DATA FROM SECONDARY SOURCES

14.2.2

PRIMARY RESEARCH

14.2.2.1

OBJECTIVES OF PRIMARY RESEARCH

14.2.2.2

KEY INDUSTRY INSIGHTS

14.3

MARKET SIZE ESTIMATION METHODOLOGY

14.3.1

BOTTOM-UP APPROACH

14.3.1.1

APPROACH 1: COMPANY REVENUE ESTIMATION APPROACH

14.3.1.2

APPROACH 2: CUSTOMER-BASED MARKET ESTIMATION

14.3.1.3

APPROACH 3: PRIMARY INTERVIEWS

14.3.2

TOP-DOWN APPROACH

14.4

MARKET BREAKDOWN AND DATA TRIANGULATION

14.5

MARKET SHARE ASSESSMENT

14.6

RESEARCH ASSUMPTIONS

14.7

RESEARCH LIMITATIONS

14.8

RISK ASSESSMENT

15

APPENDIX

316

15.1

DISCUSSION GUIDE

15.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

15.3

CUSTOMIZATION OPTIONS

15.4

RELATED REPORTS

15.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

MICROFLUIDICS MARKET: INCLUSIONS AND EXCLUSIONS

TABLE 2

MICROFLUIDICS MARKET: IMPACT ANALYSIS OF MARKET DYNAMICS

TABLE 3

DIFFERENT FABRICATION MATERIALS USED

TABLE 4

COMMERCIAL MICROFLUIDIC PCR ASSAYS FOR TB

TABLE 5

COMPARISON OF KEY MATERIALS USED IN MICROFLUIDIC DEVICES

TABLE 6

MICROFLUIDICS MARKET: UNMET NEEDS

TABLE 7

STRATEGIC MOVES BY TIER 1, TIER 2, AND TIER 3 PLAYERS IN MICROFLUIDICS MARKET

TABLE 8

MICROFLUIDICS MARKET: INNOVATIONS AND PATENT REGISTRATIONS, 2022–2024

TABLE 9

KEY COMPANIES IMPLEMENTING AI/GENAI IN MICROFLUIDICS MARKET

TABLE 10

US: CLASSIFICATION OF MICROFLUIDICS TECHNOLOGY-ASSOCIATED DIAGNOSTIC DEVICES

TABLE 11

CANADA: TIME, COST, AND COMPLEXITY OF REGISTRATION

TABLE 12

EUROPE: CLASSIFICATION OF MICROFLUIDICS ASSOCIATED WITH IVD DEVICES

TABLE 13

JAPAN: TIME, COST, AND COMPLEXITY OF REGISTRATION

TABLE 14

CHINA: TIME, COST, AND COMPLEXITY OF REGISTRATION

TABLE 15

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 16

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 17

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 18

LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 19

REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 20

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR MICROFLUIDIC COMPONENTS, BY MATERIAL

TABLE 21

KEY BUYING CRITERIA FOR MICROFLUIDIC COMPONENTS, BY MATERIAL

TABLE 22

MICROFLUIDICS MARKET: UNMET NEED ANALYSIS

TABLE 23

MICROFLUIDICS MARKET: IMPACT OF PORTER’S FIVE FORCES

TABLE 24

NORTH AMERICA: MACROECONOMIC OUTLOOK

TABLE 25

EUROPE: MACROECONOMIC OUTLOOK

TABLE 26

ASIA PACIFIC: MACROECONOMIC INDICATORS

TABLE 27

LATIN AMERICA: MACROECONOMIC OUTLOOK

TABLE 28

MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

TABLE 29

MICROFLUIDICS MARKET: ROLE IN ECOSYSTEM

TABLE 30

AVERAGE SELLING PRICE RANGE OF MICROFLUIDICS COMPONENTS, BY REGION, 2023–2025 (USD THOUSAND)

TABLE 31

AVERAGE SELLING PRICE TREND OF MICROFLUIDIC COMPONENTS, BY KEY PLAYERS, 2024 (USD)

TABLE 32

IMPORT DATA FOR HS CODE 3822, BY COUNTRY, 2020–2024 (USD THOUSAND)

TABLE 33

EXPORT DATA FOR HS CODE 3822, BY COUNTRY, 2020–2024 (USD THOUSAND)

TABLE 34

MICROFLUIDICS MARKET: KEY CONFERENCES & EVENTS (2026-2027)

TABLE 35

CASE STUDY 1: MULTIPLEX MICROFLUIDIC CIRCUIT FOR BLOOD VESSEL-ON-A-CHIP PERFUSION USING FLOWEZ

TABLE 36

CASE STUDY 2: MICROFLUIDIC SYSTEM FOR ROBOTIC HAND PLAYING NINTENDO

TABLE 37

CASE STUDY 3: 3D-PRINTED MICROFLUIDIC DEVICES USING POLYJET TECHNOLOGY

TABLE 38

US ADJUSTED RECIPROCAL TARIFF RATES

TABLE 39

TARIFF-INDUCED PRICE INCREASES FOR HEALTHCARE PRODUCTS

TABLE 40

MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 41

MICROFLUIDICS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 42

MICROFLUIDICS-BASED DEVICES MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 43

MICROFLUIDICS-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 44

PCR SYSTEMS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 45

MICROFLUIDIC CAPILLARY ELECTROPHORESIS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 46

NEXT-GENERATION SEQUENCING SYSTEMS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 47

DROPLET & PARTICLE PRODUCTION SYSTEMS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 48

OTHER DEVICES MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 49

MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 50

MICROFLUIDIC COMPONENTS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 51

MICROFLUIDIC CHIPS OFFERED BY KEY PLAYERS

TABLE 52

MICROFLUIDIC CHIPS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 53

FLOW & PRESSURE SENSORS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 54

FLOW & PRESSURE CONTROLLERS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 55

MICROFLUIDIC VALVES MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 56

MICROPUMPS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 57

MICRONEEDLES OFFERED BY KEY PLAYERS

TABLE 58

MICRONEEDLES MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 59

OTHER MICROFLUIDIC COMPONENTS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 60

MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 61

MATERIAL-BASED MICROFLUIDIC COMPONENTS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 62

SILICON-BASED MICROFLUIDIC COMPONENTS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 63

PMMA-BASED MICROFLUIDIC COMPONENTS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 64

PDMS-BASED MICROFLUIDIC COMPONENTS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 65

COC-BASED MICROFLUIDIC COMPONENTS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 66

GLASS-BASED MICROFLUIDIC COMPONENTS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 67

OTHER MATERIALS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 68

MICROFLUIDICS MARKET, BY APPLICATION, 2023–2030 (USD MILLION)

TABLE 69

MICROFLUIDICS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 70

MICROFLUIDICS MARKET FOR IVD APPLICATION, BY TYPE, 2023–2030 (USD MILLION)

TABLE 71

MICROFLUIDICS MARKET FOR IVD APPLICATION, BY REGION, 2023–2030 (USD MILLION)

TABLE 72

MICROFLUIDICS MARKET FOR CLINICAL DIAGNOSTICS, BY REGION, 2023–2030 (USD MILLION)

TABLE 73

MICROFLUIDICS MARKET FOR POCT, BY REGION, 2023–2030 (USD MILLION)

TABLE 74

MICROFLUIDICS MARKET FOR VETERINARY DIAGNOSTICS, BY REGION, 2023–2030 (USD MILLION)

TABLE 75

MICROFLUIDICS MARKET FOR THERAPEUTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 76

MICROFLUIDICS MARKET FOR THERAPEUTICS, BY REGION, 2023–2030 (USD MILLION)

TABLE 77

COMPARISON OF MICROFLUIDIC VS. TRADITIONAL API ENCAPSULATION

TABLE 78

MICROFLUIDICS MARKET FOR DRUG DELIVERY, BY REGION, 2023–2030 (USD MILLION)

TABLE 79

OVERVIEW OF WEARABLE MICROFLUIDIC PLATFORMS ACROSS BIOFLUIDS: TARGETS, APPLICATIONS, DETECTION STRATEGIES, AND TRANSLATIONAL STATUS

TABLE 80

MICROFLUIDICS MARKET FOR WEARABLE DEVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 81

MICROFLUIDICS MARKET FOR PHARMACEUTICAL & LIFE SCIENCE RESEARCH, BY TYPE, 2023–2030 (USD MILLION)

TABLE 82

MICROFLUIDICS MARKET FOR PHARMACEUTICAL & LIFE SCIENCE RESEARCH, BY REGION, 2023–2030 (USD MILLION)

TABLE 83

MICROFLUIDICS MARKET FOR LAB ANALYTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 84

MICROFLUIDICS MARKET FOR LAB ANALYTICS, BY REGION, 2023–2030 (USD MILLION)

TABLE 85

MICROFLUIDICS MARKET FOR PROTEOMIC ANALYSIS, BY REGION, 2023–2030 (USD MILLION)

TABLE 86

MICROFLUIDICS MARKET FOR GENOMIC ANALYSIS, BY REGION, 2023–2030 (USD MILLION)

TABLE 87

KEY ORGAN-ON-CHIP APPLICATIONS

TABLE 88

MICROFLUIDICS MARKET FOR CELL-BASED ASSAYS, BY REGION, 2023–2030 (USD MILLION)

TABLE 89

MICROFLUIDICS MARKET FOR CAPILLARY ELECTROPHORESIS, BY REGION, 2023–2030 (USD MILLION)

TABLE 90

MICROFLUIDICS MARKET FOR MICRODISPENSING, BY REGION, 2023–2030 (USD MILLION)

TABLE 91

MICROFLUIDICS MARKET FOR MICROREACTORS, BY REGION, 2023–2030 (USD MILLION)

TABLE 92

MICROFLUIDICS MARKET, BY END USER, 2023–2030 (USD MILLION)

TABLE 93

MICROFLUIDICS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 94

MICROFLUIDICS MARKET FOR HOSPITALS & DIAGNOSTIC CENTERS, BY REGION, 2023–2030 (USD MILLION)

TABLE 95

MICROFLUIDICS MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES, BY REGION, 2023–2030 (USD MILLION)

TABLE 96

LEADING MICROFLUIDICS RESEARCH INSTITUTES, BY AREA OF INTEREST

TABLE 97

MICROFLUIDICS MARKET FOR ACADEMIC & RESEARCH INSTITUTES, BY REGION, 2023–2030 (USD MILLION)

TABLE 98

MICROFLUIDICS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 99

NORTH AMERICA: MICROFLUIDICS MARKET, BY COUNTRY, 2023–2030 (USD MILLION)

TABLE 100

NORTH AMERICA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 101

NORTH AMERICA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 102

NORTH AMERICA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 103

NORTH AMERICA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 104

NORTH AMERICA: MICROFLUIDICS MARKET, BY APPLICATION, 2023–2030 (USD MILLION)

TABLE 105

NORTH AMERICA: MICROFLUIDICS MARKET FOR IVD APPLICATIONS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 106

NORTH AMERICA: MICROFLUIDICS MARKET FOR PHARMACEUTICAL & LIFE SCIENCE RESEARCH, BY TYPE, 2023–2030 (USD MILLION)

TABLE 107

NORTH AMERICA: MICROFLUIDICS MARKET FOR LAB ANALYTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 108

NORTH AMERICA: MICROFLUIDICS MARKET FOR THERAPEUTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 109

NORTH AMERICA: MICROFLUIDICS MARKET, BY END USER, 2023–2030 (USD MILLION)

TABLE 110

US: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 111

US: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 112

US: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 113

US: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 114

CANADA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 115

CANADA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 116

CANADA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 117

CANADA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 118

EUROPE: MICROFLUIDICS MARKET, BY COUNTRY, 2023–2030 (USD MILLION)

TABLE 119

EUROPE: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 120

EUROPE: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 121

EUROPE: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 122

EUROPE: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 123

EUROPE: MICROFLUIDICS MARKET, BY APPLICATION, 2023–2030 (USD MILLION)

TABLE 124

EUROPE: MICROFLUIDICS MARKET FOR IVD APPLICATIONS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 125

EUROPE: MICROFLUIDICS MARKET FOR PHARMACEUTICAL & LIFE SCIENCE RESEARCH, BY TYPE, 2023–2030 (USD MILLION)

TABLE 126

EUROPE: MICROFLUIDICS MARKET FOR LAB ANALYTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 127

EUROPE: MICROFLUIDICS MARKET FOR THERAPEUTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 128

EUROPE: MICROFLUIDICS MARKET, BY END USER, 2023–2030 (USD MILLION)

TABLE 129

GERMANY: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 130

GERMANY: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 131

GERMANY: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 132

GERMANY: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 133

FRANCE: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 134

FRANCE: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 135

FRANCE: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 136

FRANCE: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 137

UK: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 138

UK: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 139

UK: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 140

UK: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 141

ITALY: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 142

ITALY: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 143

ITALY: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 144

ITALY: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 145

SPAIN: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 146

SPAIN: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 147

SPAIN: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 148

SPAIN: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 149

REST OF EUROPE: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 150

REST OF EUROPE: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 151

REST OF EUROPE: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 152

REST OF EUROPE: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 153

ASIA PACIFIC: MICROFLUIDICS MARKET, BY COUNTRY, 2023–2030 (USD MILLION)

TABLE 154

ASIA PACIFIC: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 155

ASIA PACIFIC: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 156

ASIA PACIFIC: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 157

ASIA PACIFIC: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 158

ASIA PACIFIC: MICROFLUIDICS MARKET, BY APPLICATION, 2023–2030 (USD MILLION)

TABLE 159

ASIA PACIFIC: MICROFLUIDICS MARKET FOR IVD APPLICATIONS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 160

ASIA PACIFIC: MICROFLUIDICS MARKET FOR PHARMACEUTICAL & LIFE SCIENCE RESEARCH, BY TYPE, 2023–2030 (USD MILLION)

TABLE 161

ASIA PACIFIC: MICROFLUIDICS MARKET FOR LAB ANALYTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 162

ASIA PACIFIC: MICROFLUIDICS MARKET FOR THERAPEUTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 163

ASIA PACIFIC: MICROFLUIDICS MARKET, BY END USER, 2023–2030 (USD MILLION)

TABLE 164

CHINA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 165

CHINA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 166

CHINA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 167

CHINA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 168

JAPAN: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 169

JAPAN: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 170

JAPAN: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 171

JAPAN: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 172

INDIA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 173

INDIA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 174

INDIA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 175

INDIA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 176

AUSTRALIA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 177

AUSTRALIA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 178

AUSTRALIA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 179

AUSTRALIA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 180

SOUTH KOREA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 181

SOUTH KOREA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 182

SOUTH KOREA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 183

SOUTH KOREA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 184

REST OF ASIA PACIFIC: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 185

REST OF ASIA PACIFIC: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 186

REST OF ASIA PACIFIC: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 187

REST OF ASIA PACIFIC: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 188

LATIN AMERICA: MICROFLUIDICS MARKET, BY COUNTRY, 2023–2030 (USD MILLION)

TABLE 189

LATIN AMERICA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 190

LATIN AMERICA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 191

LATIN AMERICA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 192

LATIN AMERICA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 193

LATIN AMERICA: MICROFLUIDICS MARKET, BY APPLICATION, 2023–2030 (USD MILLION)

TABLE 194

LATIN AMERICA: MICROFLUIDICS MARKET FOR IVD APPLICATIONS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 195

LATIN AMERICA: MICROFLUIDICS MARKET FOR PHARMACEUTICAL & LIFE SCIENCE RESEARCH, BY TYPE, 2023–2030 (USD MILLION)

TABLE 196

LATIN AMERICA: MICROFLUIDICS MARKET FOR LAB ANALYTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 197

LATIN AMERICA: MICROFLUIDICS MARKET FOR THERAPEUTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 198

LATIN AMERICA: MICROFLUIDICS MARKET, BY END USER, 2023–2030 (USD MILLION)

TABLE 199

BRAZIL: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 200

BRAZIL: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 201

BRAZIL: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 202

BRAZIL: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 203

MEXICO: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 204

MEXICO: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 205

MEXICO: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 206

MEXICO: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 207

REST OF LATIN AMERICA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 208

REST OF LATIN AMERICA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 209

REST OF LATIN AMERICA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 210

REST OF LATIN AMERICA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 211

MIDDLE EAST & AFRICA: MICROFLUIDICS MARKET, BY COUNTRY, 2023–2030 (USD MILLION)

TABLE 212

MIDDLE EAST & AFRICA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 213

MIDDLE EAST & AFRICA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 214

MIDDLE EAST & AFRICA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 215

MIDDLE EAST & AFRICA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 216

MIDDLE EAST & AFRICA: MICROFLUIDICS MARKET, BY APPLICATION, 2023–2030 (USD MILLION)

TABLE 217

MIDDLE EAST & AFRICA: MICROFLUIDICS MARKET FOR IVD APPLICATIONS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 218

MIDDLE EAST & AFRICA: MICROFLUIDICS MARKET FOR PHARMACEUTICAL & LIFE SCIENCE RESEARCH, BY TYPE, 2023–2030 (USD MILLION)

TABLE 219

MIDDLE EAST & AFRICA: MICROFLUIDICS MARKET FOR LAB ANALYTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 220

MIDDLE EAST & AFRICA: MICROFLUIDICS MARKET FOR THERAPEUTICS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 221

MIDDLE EAST & AFRICA: MICROFLUIDICS MARKET, BY END USER, 2023–2030 (USD MILLION)

TABLE 222

GCC COUNTRIES: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 223

GCC COUNTRIES: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 224

GCC COUNTRIES: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 225

GCC COUNTRIES: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 226

REST OF MIDDLE EAST & AFRICA: MICROFLUIDICS MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 227

REST OF MIDDLE EAST & AFRICA: MICROFLUIDIC-BASED DEVICES MARKET, BY DEVICE, 2023–2030 (USD MILLION)

TABLE 228

REST OF MIDDLE EAST & AFRICA: MICROFLUIDIC COMPONENTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 229

REST OF MIDDLE EAST & AFRICA: MICROFLUIDIC COMPONENTS MARKET, BY MATERIAL, 2023–2030 (USD MILLION)

TABLE 230

OVERVIEW OF STRATEGIES DEPLOYED BY KEY MANUFACTURING COMPANIES

TABLE 231

MICROFLUIDICS MARKET: DEGREE OF COMPETITION

TABLE 232

MICROFLUIDICS MARKET: REGION FOOTPRINT

TABLE 233

MICROFLUIDICS MARKET: PRODUCT FOOTPRINT

TABLE 234

MICROFLUIDICS MARKET: APPLICATION FOOTPRINT

TABLE 235

MICROFLUIDICS MARKET: END USER FOOTPRINT

TABLE 236

MICROFLUIDICS MARKET: LIST OF KEY STARTUP/SME PLAYERS

TABLE 237

MICROFLUIDICS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 238

MICROFLUIDICS MARKET: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022−NOVEMBER 2025

TABLE 239

MICROFLUIDICS MARKET: DEALS, JANUARY 2022–NOVEMBER 2025

TABLE 240

MICROFLUIDICS MARKET: EXPANSIONS, JANUARY 2022–NOVEMBER 2025

TABLE 241

MICROFLUIDICS MARKET: OTHER DEVELOPMENTS, JANUARY 2022−NOVEMBER 2025

TABLE 242

DANAHER CORPORATION: COMPANY OVERVIEW

TABLE 243

DANAHER CORPORATION: PRODUCTS OFFERED

TABLE 244

DANAHER CORPORATION: DEALS

TABLE 245

DANAHER CORPORATION: EXPANSIONS

TABLE 246

ILLUMINA, INC.: COMPANY OVERVIEW

TABLE 247

ILLUMINA, INC.: PRODUCTS OFFERED

TABLE 248

ILLUMINA, INC.: PRODUCT LAUNCHES

TABLE 249

ILLUMINA, INC.: DEALS

TABLE 250

BIOMÉRIEUX: COMPANY OVERVIEW

TABLE 251

BIOMÉRIEUX: PRODUCTS OFFERED

TABLE 252

BIOMÉRIEUX: PRODUCT LAUNCHES/APPROVALS

TABLE 253

BIOMÉRIEUX: DEALS

TABLE 254

THERMO FISHER SCIENTIFIC INC.: COMPANY OVERVIEW

TABLE 255

THERMO FISHER SCIENTIFIC INC.: PRODUCTS OFFERED

TABLE 256

THERMO FISHER SCIENTIFIC INC.: PRODUCT LAUNCHES/APPROVALS

TABLE 257

THERMO FISHER SCIENTIFIC INC.: DEALS

TABLE 258

ABBOTT LABORATORIES: COMPANY OVERVIEW

TABLE 259

ABBOTT LABORATORIES: PRODUCTS OFFERED

TABLE 260

PARKER HANNIFIN CORP: COMPANY OVERVIEW

TABLE 261

PARK HANNIFIN CORP: PRODUCTS OFFERED

TABLE 262

SMC CORPORATION: COMPANY OVERVIEW

TABLE 263

SMC CORPORATION: PRODUCTS OFFERED

TABLE 264

SMC CORPORATION: PRODUCT LAUNCHES

TABLE 265

IDEX CORPORATION: COMPANY OVERVIEW

TABLE 266

IDEX CORPORATION: PRODUCTS OFFERED

TABLE 267

IDEX CORPORATION: DEALS

TABLE 268

FORTIVE: COMPANY OVERVIEW

TABLE 269

FORTIVE: PRODUCTS OFFERED

TABLE 270

REVVITY, INC.: COMPANY OVERVIEW

TABLE 271

REVVITY, INC.: PRODUCTS OFFERED

TABLE 272

REVVITY, INC.: DEALS

TABLE 273

AGILENT TECHNOLOGIES, INC.: COMPANY OVERVIEW

TABLE 274

AGILENT TECHNOLOGIES, INC.: PRODUCTS OFFERED

TABLE 275

AGILENT TECHNOLOGIES, INC. : PRODUCT APPROVALS/LAUNCHES

TABLE 276

AGILENT TECHNOLOGIES, INC.: DEALS

TABLE 277

AGILENT TECHNOLOGIES, INC.: EXPANSIONS

TABLE 278

BIO-RAD LABORATORIES, INC.: COMPANY OVERVIEW

TABLE 279

BIO-RAD LABORATORIES, INC.: PRODUCTS OFFERED

TABLE 280

BIO-RAD LABORATORIES, INC.: PRODUCT LAUNCHES

TABLE 281

BIO-RAD LABORATORIES, INC.: DEALS

TABLE 282

BECTON, DICKINSON AND COMPANY: COMPANY OVERVIEW

TABLE 283

BECTON, DICKINSON AND COMPANY: PRODUCTS OFFERED

TABLE 284

BECTON, DICKINSON AND COMPANY: PRODUCT LAUNCHES/APPROVALS,

TABLE 285

BECTON, DICKINSON AND COMPANY: DEALS

TABLE 286

BECTON, DICKINSON AND COMPANY: EXPANSIONS

TABLE 287

F. HOFFMANN-LA ROCHE LTD.: COMPANY OVERVIEW

TABLE 288

F. HOFFMANN-LA ROCHE LTD.: PRODUCTS OFFERED

TABLE 289

F. HOFFMANN-LA ROCHE LTD.: PRODUCT LAUNCHES/APPROVALS,

TABLE 290

F. HOFFMANN-LA ROCHE LTD.: DEALS

TABLE 291

STANDARD BIOTOOLS: COMPANY OVERVIEW

TABLE 292

STANDARD BIOTOOLS: PRODUCTS OFFERED

TABLE 293

STANDARD BIOTOOLS: PRODUCT LAUNCHES/APPROVALS

TABLE 294

STANDARD BIOTOOLS: DEALS

TABLE 295

QUIDELORTHO CORPORATION: COMPANY OVERVIEW

TABLE 296

QUIDELORTHO CORPORATION: PRODUCTS OFFERED

TABLE 297

QUIDELORTHO CORPORATION: PRODUCT APPROVALS

TABLE 298

QUIDELORTHO CORPORATION: DEALS

TABLE 299

QUIDELORTHO CORPORATION: EXPANSIONS

TABLE 300

AIGNEP S.P.A.: COMPANY OVERVIEW

TABLE 301

AIGNEP S.P.A.: PRODUCTS OFFERED

TABLE 302

AIGNEP S.P.A.: DEALS

TABLE 303

DOLOMITE MICROFLUIDICS: COMPANY OVERVIEW

TABLE 304

DOLOMITE MICROFLUIDICS: PRODUCTS OFFERED

TABLE 305

DOLOMITE MICROFLUIDICS: PRODUCT LAUNCHES

TABLE 306

DOLOMITE MICROFLUIDICS: DEALS

TABLE 307

DOLOMITE MICROFLUIDICS: OTHER DEVELOPMENTS

TABLE 308

ELVEFLOW: COMPANY OVERVIEW

TABLE 309

ELVEFLOW: PRODUCTS OFFERED

TABLE 310

NANOSTRING TECHNOLOGIES: COMPANY OVERVIEW

TABLE 311

INNOVATIVE BIOCHIPS, LLC: COMPANY OVERVIEW

TABLE 312

FLUIDIC ANALYTICS: COMPANY OVERVIEW

TABLE 313

HORIBA: COMPANY OVERVIEW

TABLE 314

MICRONIT B.V.: COMPANY OVERVIEW

TABLE 315

EMULATE, INC.: COMPANY OVERVIEW

TABLE 316

SPHERE BIO: COMPANY OVERVIEW

TABLE 317

ZEON CORPORATION: COMPANY OVERVIEW

TABLE 318

QIAGEN N.V.: COMPANY OVERVIEW

LIST OF FIGURES

FIGURE 1

MICROFLUIDICS MARKET SEGMENTATION

FIGURE 2

MARKET SCENARIO

FIGURE 3

GLOBAL MICROFLUIDICS MARKET, 2022–2030

FIGURE 4

MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN MICROFLUIDICS MARKET, 2020–2025

FIGURE 5

DISRUPTIONS INFLUENCING GROWTH OF MICROFLUIDICS MARKET

FIGURE 6

HIGH-GROWTH SEGMENTS IN MICROFLUIDICS MARKET, 2025–2030

FIGURE 7

ASIA PACIFIC TO REGISTER HIGHEST CAGR IN MICROFLUIDICS MARKET, IN TERMS OF VALUE, DURING FORECAST PERIOD

FIGURE 8

RISING ADOPTION OF LAB-ON-A-CHIP TECHNOLOGIES TO DRIVE MARKET

FIGURE 9

NORTH AMERICA TO COMMAND LARGEST MARKET SHARE IN 2030

FIGURE 10

NORTH AMERICA AND HOSPITALS & DIAGNOSTIC CENTERS ACCOUNTED FOR LARGEST MARKET SHARES IN 2024

FIGURE 11

CHINA TO REGISTER FASTEST GROWTH FROM 2025 TO 2030

FIGURE 12

MICROFLUIDICS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 13

PATENT ANALYSIS FOR MICROFLUIDICS MARKET, JANUARY 2015–NOVEMBER 2025

FIGURE 14

KEY AI USE CASES IN MICROFLUIDICS MARKET

FIGURE 15

US: REGULATORY PROCESS FOR TESTING DEVICES ASSOCIATED WITH MICROFLUIDICS TECHNOLOGY

FIGURE 16

CANADA: REGULATORY PROCESS FOR MICROFLUIDICS-ASSOCIATED IVD DEVICES

FIGURE 17

EUROPE: REGULATORY PROCESS FOR IVD DEVICES

FIGURE 18

INDIA: REGULATORY PROCESS FOR IVD DEVICES

FIGURE 19

INFLUENCE OF KEY STAKEHOLDERS ON BUYING PROCESS FOR MICROFLUIDIC COMPONENTS, BY MATERIAL

FIGURE 20

KEY BUYING CRITERIA FOR MICROFLUIDIC COMPONENTS, BY MATERIAL

FIGURE 21

MICROFLUIDICS MARKET: UNMET NEED ANALYSIS

FIGURE 22

MICROFLUIDICS MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 23

MICROFLUIDICS MARKET: VALUE CHAIN ANALYSIS

FIGURE 24

MICROFLUIDICS MARKET: ECOSYSTEM ANALYSIS

FIGURE 25

AVERAGE SELLING PRICE TREND OF MICROFLUIDIC COMPONENTS, BY REGION, 2023–2025 (USD)

FIGURE 26

AVERAGE SELLING PRICE TREND OF MICROFLUIDIC COMPONENTS, BY KEY PLAYERS, 2024 (USD)

FIGURE 27

MICROFLUIDICS MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 28

MICROFLUIDICS MARKET: FUNDING AND NUMBER OF DEALS, 2019–2023 (USD MILLION)

FIGURE 29

NUMBER OF DEALS IN MICROFLUIDICS MARKET, BY KEY PLAYERS, 2019–2023

FIGURE 30

VALUE OF DEALS IN MICROFLUIDICS MARKET, BY KEY PLAYERS, 2019–2023 (USD)

FIGURE 31

NORTH AMERICA: MICROFLUIDICS MARKET SNAPSHOT

FIGURE 32

ASIA PACIFIC: MICROFLUIDICS MARKET SNAPSHOT

FIGURE 33

REVENUE ANALYSIS OF KEY PLAYERS IN MICROFLUIDICS MARKET (2022−2024)

FIGURE 34

MARKET SHARE ANALYSIS OF KEY PLAYERS IN MICROFLUIDICS MARKET (2024)

FIGURE 35

RANKING OF KEY PLAYERS IN MICROFLUIDICS MARKET, 2024

FIGURE 36

MICROFLUIDICS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 37

MICROFLUIDICS MARKET: COMPANY FOOTPRINT

FIGURE 38

MICROFLUIDICS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 39

EV/EBITDA OF KEY VENDORS, 2025

FIGURE 40

YEAR-TO-DATE (YTD) PRICE, TOTAL RETURN, AND 5-YEAR STOCK BETA OF KEY VENDORS, 2025

FIGURE 41

MICROFLUIDICS MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS

FIGURE 42

DANAHER CORPORATION: COMPANY SNAPSHOT

FIGURE 43

ILLUMINA, INC.: COMPANY SNAPSHOT

FIGURE 44

BIOMÉRIEUX: COMPANY SNAPSHOT

FIGURE 45

THERMO FISHER SCIENTIFIC INC.: COMPANY SNAPSHOT

FIGURE 46

ABBOTT LABORATORIES: COMPANY SNAPSHOT

FIGURE 47

PARKER HANNIFIN CORP: COMPANY SNAPSHOT

FIGURE 48

SMC CORPORATION: COMPANY SNAPSHOT (2024)

FIGURE 49

IDEX CORPORATION: COMPANY SNAPSHOT

FIGURE 50

FORTIVE: COMPANY SNAPSHOT

FIGURE 51

REVVITY, INC.: COMPANY SNAPSHOT

FIGURE 52

AGILENT TECHNOLOGIES, INC.: COMPANY SNAPSHOT

FIGURE 53

BIO-RAD LABORATORIES, INC.: COMPANY SNAPSHOT

FIGURE 54

BECTON, DICKINSON AND COMPANY: COMPANY SNAPSHOT

FIGURE 55

F. HOFFMANN-LA ROCHE LTD.: COMPANY SNAPSHOT

FIGURE 56

STANDARD BIOTOOLS: COMPANY SNAPSHOT

FIGURE 57

QUIDELORTHO CORPORATION: COMPANY SNAPSHOT

FIGURE 58

MICROFLUIDICS MARKET: RESEARCH DATA

FIGURE 59

MICROFLUIDICS MARKET: RESEARCH DESIGN

FIGURE 60

PRIMARY SOURCES

FIGURE 61

BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

FIGURE 62

BREAKDOWN OF PRIMARY INTERVIEWS: SUPPLY-SIDE AND DEMAND-SIDE PARTICIPANTS

FIGURE 63

RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

FIGURE 64

MICROFLUIDICS MARKET SIZE ESTIMATION: APPROACH 1 (COMPANY REVENUE ESTIMATION)

FIGURE 65

MICROFLUIDICS MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

FIGURE 66

MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

FIGURE 67

DATA TRIANGULATION

Methodology

Four main studies were done to estimate the market size of microfluidics. Secondary research was carried out to obtain data associated with the market, peer markets, and parent markets. After that, data was obtained from 3-5 secondary sources; the findings, assumptions, and sizing were confirmed through primary sources. Top-down and bottom-up approaches were utilized to gain insights on complete market size. After that, market breakdown and data triangulation were used to determine the market size of segments and subsegments.

Secondary Research

Directories, databases like D&B Hoovers, Factiva, white papers, Bloomberg Businessweek, annual reports, SEC filings, business filings and investor presentations are few of the important sources used in the secondary research. This helps in gaining fundamental details about prominent companies and market segmentation as per the industry trends at numerous levels and technological viewpoints related with the Microfluidics market.

Primary Research

The primary research compromised performing interviews from both the supply and demand sides to obtain quantitative and qualitative data. CEOs, area sales managers, territory sales managers, regional sales managers and other important officials from top businesses are the primary sources from the supply side. Physicians, researchers, department heads, and staff members from diagnostic centers, hospitals and research institutes were the primary sources from the demand side. The target of this study was to verify the conclusions and assumptions from secondary research by interacting with stakeholders directly.

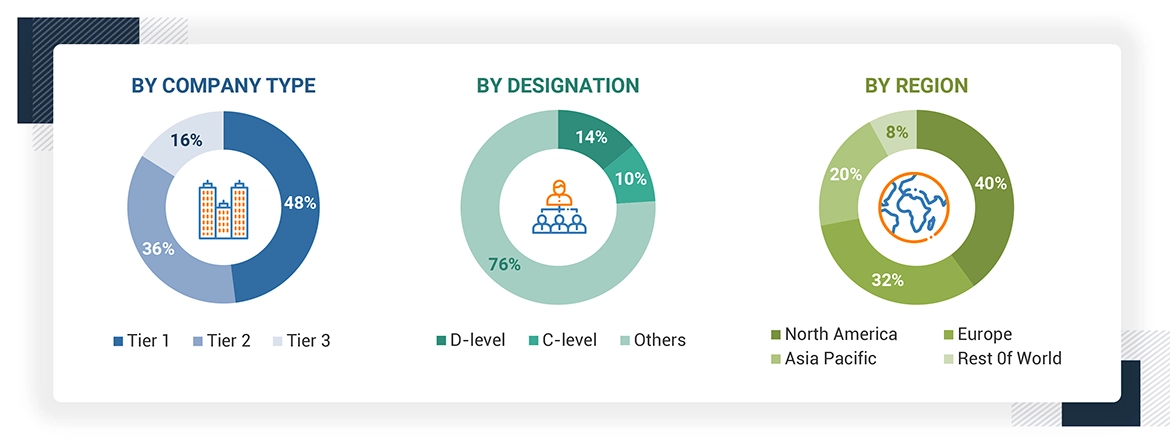

A breakdown of the primary respondents is provided below:

*Others include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

Note: Companies are classified into tiers based on their total revenue. As of 2023, Tier 1 = >USD 1 billion, Tier 2 = < USD 500 million, and Tier 3 = < USD 100 million.

To know about the assumptions considered for the study, download the pdf brochure

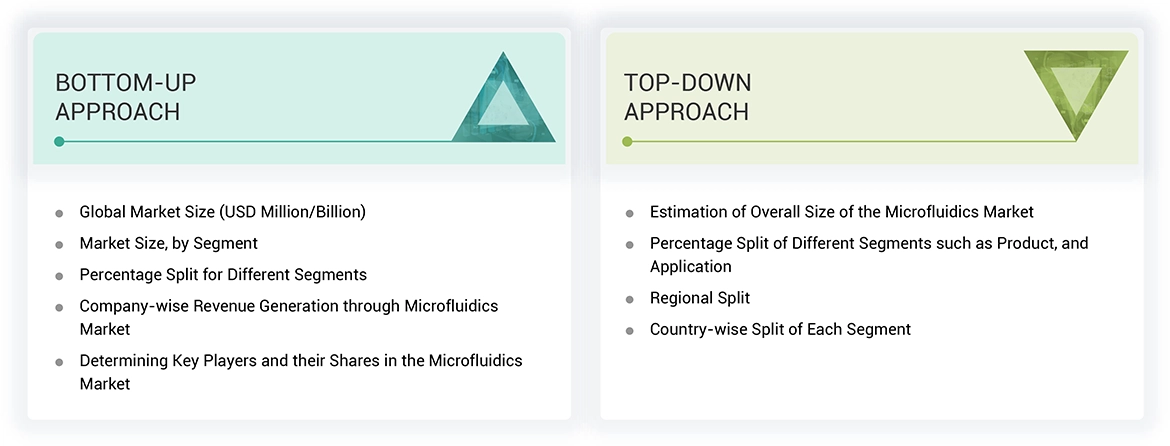

Market Size Estimation

The revenue share analysis of the major key players for the size of the Microfluidics market is given in this study. Primary and secondary research are used to find prominent players in the Microfluidics and to gain insights of their financials and market share. The primary research approach comprises extremely in-depth interviews with CEOs, directors, and senior marketing executives, while the secondary research procedure mostly relied on the annual and financial reports of major players. Segment-based technique was used to determine the global market value. The revenue details of significant solution and service suppliers was then applied to source these segmented revenues.

The steps in the procedure are

- List the key global companies that are associated with the Microfluidics industry. Note the annual revenues of the players in the Microfluidics industry or the product category/business division.

- As of 2024, it represents an important portion of the market based on revenue mapping of the key competitors. Extrapolation to the global value for the Microfluidics market.

Data Triangulation

The Microfluidics market was categorized into various segments and subsegments with the help of the above procedure. Then, data triangulation and the market segmentation process are carried out to ensure the accuracy of the data for each segment. Factors and trends from demand and supply sides were studied . Top-down and bottom-up approaches provide the outcome from the analysis of the Microfluidics market.

Market Definition

The microfluidics market includes products and technologies that are developed to analyse and regulate fluid volume through microfluidic devices and components. The market covers both the microfluidics components that are important for the working of microfluidics-based devices, such as lab-on-a-chip systems and diagnostic assays, as well as the devices. Microneedles, micropumps, flow and pressure sensors, controllers, and microfluidic valves are some of the important components of microfluidics-based device.Polymers, silicon, and glass are most often used in the development of these components. The market provides innovative technologies for effective and precise fluid management and analysis, which have beneficial applications in research and diagnostics.

Stakeholders

- Microfluidic product manufacturers

- Microfluidic product distributors

- Pharmaceutical companies

- IVD manufacturers

- In vitro diagnostic test (IVD) distributors

- Research institutes

- Contract manufacturing organizations (CMOs)

- Contract research organizations (CROs)

- Healthcare institutions (hospitals, medical schools, and outpatient clinics)

- Government associations

- Market research and consulting firms

- Venture capitalists and investors

Report Objectives

- To define, describe, and forecast the microfluidics market by product, application, end-user, and region

- To provide detailed information about the key factors influencing the market growth, such as drivers, restraints, opportunities, challenges, and industry trends

- To strategically analyze the regulatory scenario, Porter’s five force analysis, value chain analysis, supply chain analysis, ecosystem map, and patent analysis

- To analyze micromarkets with respect to individual growth trends, prospects, and contributions to the microfluidics market

- To analyze market opportunities for stakeholders and provide details of the competitive landscape for key players

- To profile the prominent players in this market and comprehensively analyze their market shares and core competencies

- To strategically analyze the microfluidics market in five regions: North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa

- To track and analyze competitive developments such as acquisitions, product launches, product approvals, partnerships, and expansions in the microfluidics market

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Microfluidics Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

JAYANT RAJPUROHIT

Director of Market Insights, Data and Analytics

SFI Health,

Leading Pharmaceutical Companywww.sfihealth.com/