Download PDF

Download PDF Request Customisation

Request Customisation

Chromatography Resin Market

Report Code

CH 2185

Published in

Jul, 2025, By MarketsandMarkets™

Chromatography Resin Market by Type (Natural, Synthetic, Inorganic Media), Technique ((Ion Exchange (Cation and Anion), Affinity (Hydrophobic Interaction, Mixed Mode)), Application (Pharmaceutical & Biotechnology), and Region - Global Forecast to 2030

USD 4.94 BN

MARKET SIZE, 2030

CAGR 8.62%

(2025-2030)

291

REPORT PAGES

298

MARKET TABLES

CHROMATOGRAPHY RESINS MARKET SIZE & TRENDS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis | Updated on : April 29, 2026

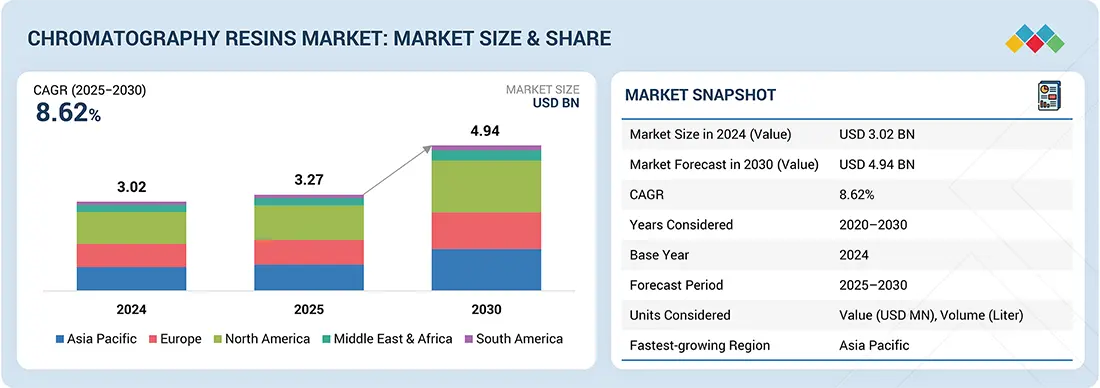

The global chromatography resins market size was valued at USD 3.27 billion in 2025 and is projected to reach USD 4.94 billion by 2030, growing at 8.62% cagr from 2025 to 2030. The chromatography resins market size is growing rapidly due to increasing biopharmaceutical production, rising demand for high-purity biomolecule separation, technological advancements in resin performance, expanding applications in food, diagnostics, and environmental analysis, and a growing focus on sustainable purification processes. Chromatography resin is a matrix of natural and synthetic polymers (dextran, cellulose, and agarose) or inorganic materials (silica and polyacrylamide). This matrix separates or purifies complex mixtures through a set of techniques.

KEY TAKEAWAYS

-

BY TYPEThe synthetic resins segment is growing at the fastest CAGR (8.70%) due to the superior chemical stability, customizable properties, and high efficiency of synthetic resins in separating complex biomolecules across various applications.

-

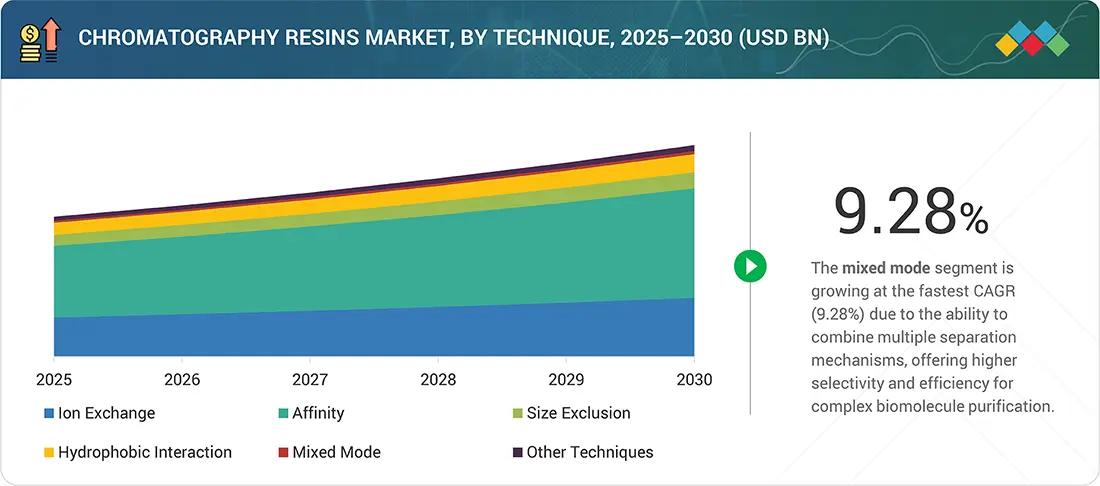

BY TECHNIQUEThe mixed mode technique is expanding at a CAGR of 9.28% as it offers versatile separation capabilities by combining multiple interaction mechanisms, improving purification of diverse and complex biological compounds.

-

BY APPLICATIONThe pharmaceutical & biotechnology application segment is growing at the fastest pace due to the surging demand for biologics, monoclonal antibodies, and vaccines, which require advanced chromatography resins for efficient and high-purity biomolecule separation.

-

BY REGIONAsia Pacific is growing at the fastest pace due to the rapid expansion of the biopharmaceutical industry, increasing healthcare investments, growing research activities, and rising demand for advanced purification technologies in emerging markets.

-

COMPETITIVE LANDSCAPEThe major market players have adopted both organic and inorganic strategies, including product launches, expansions, acquisitions, and investments. For instance, Purolite launched a product named Praesto CH1 Chromatography Resin (Affinity), a 70µm agarose-based resin developed for specialized purification processes in biopharmaceutical manufacturing. It is engineered for high flow rates and robust performance in demanding applications.

The chromatography resins market is experiencing substantial growth due to the increasing demand for high-purity biomolecules in pharmaceuticals, biotechnology, food and beverage, and environmental analysis. The rising production of monoclonal antibodies, vaccines, and recombinant proteins is intensifying the demand for effective purification solutions. Technological advancements, including mixed mode and synthetic resins, enhance selectivity, stability, and performance, facilitating superior separation of intricate compounds. Moreover, rigorous regulatory standards for product safety and quality enhance market adoption. Asia Pacific is experiencing rapid expansion owing to the burgeoning biopharmaceutical manufacturing sector, escalating healthcare investments, and heightened research initiatives. Sustainability trends are promoting the utilization of environmentally friendly and reusable resins. The market growth is driven by expanding applications, technological advancements, and rising demand in emerging economies.

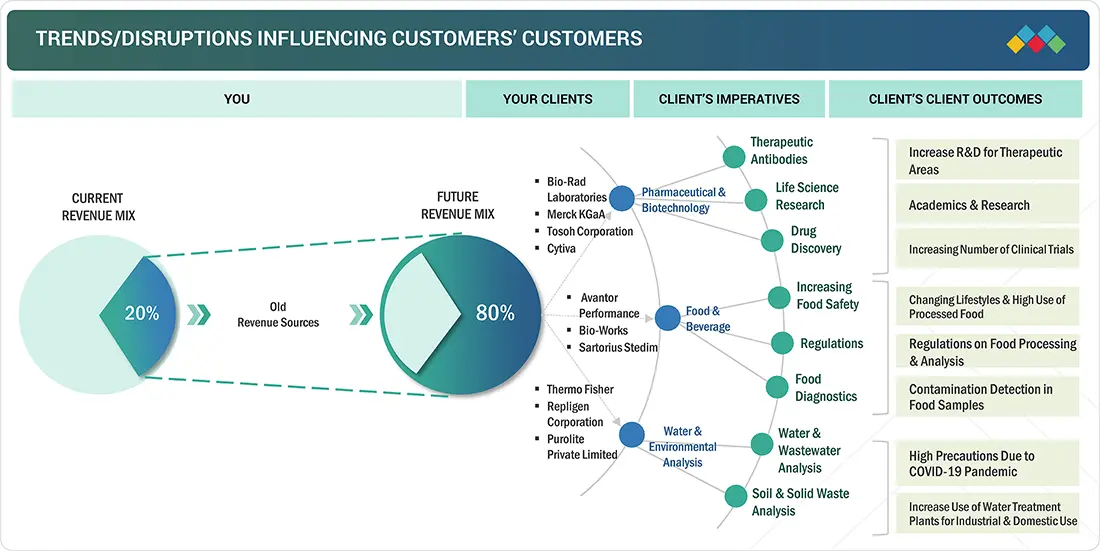

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

Clients’ shifting priorities in pharmaceutical, biotechnology, food & beverage, and environmental analysis are transforming market demands, with a growing focus on efficiency, sustainability, and regulatory compliance driving the adoption of advanced chromatography resins. These evolving needs are reshaping business strategies and will significantly impact the future revenue mix, emphasizing innovative solutions, diversified applications, and expansion into emerging regions.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

CHROMATOGRAPHY RESINS MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Growing pharmaceutical & biopharmaceutical R&D activities

-

Increasing demand for therapeutic antibodies

RESTRAINTS

Impact

Level

Level

-

Lack of skilled professionals

OPPORTUNITIES

Impact

Level

Level

-

Growing demand for chromatography in drug development & omics research

-

Growing demand for disposable pre-packed columns

CHALLENGES

Impact

Level

Level

-

Presence of alternative technologies to chromatography

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Growing pharmaceutical & biopharmaceutical R&D activities

The expansion of pharmaceutical and biopharmaceutical research and development activities is a primary catalyst for the chromatography resins market. With the rapid advancement of novel biologics, monoclonal antibodies, vaccines, and gene therapies, the demand for efficient and reliable purification processes is intensifying. Chromatography resins are essential for the separation and purification of complex biomolecules in both early-stage research & development and clinical manufacturing. Increasing investments by pharmaceutical firms in research & and development facilities, particularly in emerging markets, are enhancing the demand for high-performance resins that provide superior selectivity, stability, and scalability. Moreover, rigorous regulatory standards for product purity and consistency amplify the necessity for sophisticated chromatography solutions. The expansion of R&D activities is propelling innovation and growth in the chromatography resins market.

Restraint: Lack of skilled professionals

The shortage of skilled professionals is a considerable constraint on the chromatography resins market. The effective management and enhancement of chromatography processes necessitate skilled professionals capable of executing intricate separation methods and guaranteeing superior product quality. Nonetheless, the industry is encountering a deficiency of skilled labor, especially in burgeoning areas where the biopharmaceutical and analytical sectors are swiftly advancing. The talent deficit results in operational inefficiencies, increased likelihood of process errors, and delayed implementation of advanced resin technologies. Moreover, insufficient training and expertise impede effective troubleshooting and process development, constraining the full potential of chromatography applications. Consequently, companies encounter difficulties in optimizing throughput, ensuring regulatory compliance, and sustaining cost-efficient production. Surmounting this constraint is essential for maintaining market expansion and technological progress.

Opportunity: Growing demand for chromatography in drug development & omics research

The increasing demand for chromatography in pharmaceutical development and omics research offers a significant opportunity for the chromatography resins market. With the pharmaceutical industry placing greater emphasis on targeted therapies and personalized medicines, the efficient separation and purification of complex biomolecules have become essential. Chromatography resins are crucial in multiple phases of drug discovery, encompassing protein characterization, biomarker identification, and impurity elimination. Furthermore, the emergence of omics technologies—namely genomics, proteomics, and metabolomics—necessitates high-resolution separation techniques for the analysis of intricate biological samples. The broadening application scope presents substantial growth potential, prompting investments in advanced resin technologies that ensure enhanced selectivity, reproducibility, and scalability. Overall, the integration of chromatography in cutting-edge drug development and omics research is set to fuel market growth.

Challenge: Presence of alternative technologies to chromatography

One major obstacle facing the market for chromatography resins is the existence of substitute technologies. Because of their reduced costs, ease of use, and quicker processing times, methods like membrane filtration, precipitation, crystallization, and electrophoresis are being used more for the separation and purification of biomolecules. In certain applications where chromatography may be more costly or complex, these substitutes may provide competitive solutions. Furthermore, some sophisticated separation techniques are appealing for small-scale or low-budget operations since they call for less specialized equipment or operational knowledge. Chromatography resins must therefore contend with competition in markets where affordability and usability are crucial considerations. To overcome this obstacle, resin technology must be continuously innovated to improve performance, selectivity, and cost-effectiveness in comparison to other separation techniques.

Chromatography Resin Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Purification of monoclonal antibodies and recombinant proteins in drug manufacturing | High purity and consistency; critical for therapeutic protein production; regulatory compliance |

|

Protein purification and downstream processing in biopharmaceutical production | Efficient separation and high yield; large-scale production; enhanced product quality |

|

Purification and separation of sweeteners and flavor compounds | Improved product consistency; safety and quality; efficient processing |

|

Chromatography resins for heavy metal removal and water purification | Efficient contaminant removal; scalable process; quality water for industrial use |

|

Water treatment processes using ion exchange and chromatographic separation for contaminants | Clean water output; compliance with environmental standards; cost-effective treatment |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

CHROMATOGRAPHY RESINS MARKET ECOSYSTEM

The chromatography resins market ecosystem involves identifying and analyzing interconnected relationships among various stakeholders, including raw material suppliers, manufacturers, distributors, and end users. Raw material suppliers provide the key inputs required for resin production which further enables the manufacturers to develop chromatography resins using specialized technologies. Distributors and suppliers are the ones who establish contact between the manufacturing companies and end users to concentrate on the supply chain, increasing operational efficiency and profitability.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Chromatography Resin Market, by Type

The natural polymers segment commands the largest share of the chromatography resins market due to its extensive use in the food, biotechnology, and pharmaceutical industries. Because of their superior biocompatibility, chemical stability, and non-toxicity, natural polymers such as cellulose, agarose, and dextran are highly prized for sensitive biomolecule separation. Their functional versatility and porous structure enable effective small molecule analysis, nucleic acid separation, and protein purification. As the natural polymer-based resins are biodegradable and made from renewable resources, their use is also being fueled by the growing need for environmentally friendly and sustainable solutions. All of these elements work together to make natural polymers the go-to option for chromatography applications, which greatly propels market expansion.

Chromatography Resin Market, by Technique

The affinity technique segment commands the largest market share in the chromatography resins industry, due to its remarkable specificity and high selectivity in separating target biomolecules. Proteins, antibodies, enzymes, and nucleic acids can all be purified using affinity chromatography resins, especially in biotechnology and pharmaceutical applications. This method allows for a highly effective separation with little contamination by taking advantage of particular interactions between the target molecule and the ligand that is affixed to the resin. Affinity resin adoption is further fueled by the rising demand for therapeutic proteins, monoclonal antibodies, and vaccines, as well as strict regulatory requirements for product purity. Further supporting the segment's dominance and its crucial role in improving process efficiency and product quality across R&D and production workflows are continuous improvements in ligand technology and resin performance.

Chromatography Resin Market, by Application

Due to the increasing demand for high-purity ingredients such as flavors, sweeteners, and nutritional additives, the food & beverage application segment is the second largest in the chromatography resins market. Chromatography resins ensure product safety, consistency, and quality by effectively separating and purifying sugars, amino acids, vitamins, and organic acids. Advanced purification solutions are becoming more widely used as a result of tighter food safety laws and rising consumer demand for clean-label products. Additionally, the growing food and beverage manufacturing industry in developing nations contributes to the market's expansion. Together, these elements contribute to the food & beverage segment's robust presence in the chromatography resins market, making it a crucial application area following the biotechnology and pharmaceutical sectors.

REGION

Asia Pacific is projected to grow at the fastest CAGR, while North America is expected to be the largest chromatography resins market during the forecast period.

North America dominates the market for chromatography resins due to the region's established biotechnology and pharmaceutical sectors, sophisticated research facilities, and strict regulations that require high-quality and pure products. The dominance is further reinforced by major players and substantial R&D investments. The biopharmaceutical and life sciences industries' explosive growth, rising healthcare spending, and the growing need for sophisticated purification technologies in developing nations such as China and India are all contributing to Asia Pacific's fastest rate of growth. Its accelerated growth trajectory is largely due to the region's cost advantages, the rise in contract manufacturing organizations (CMOs), and the growing emphasis on local manufacturing capabilities.

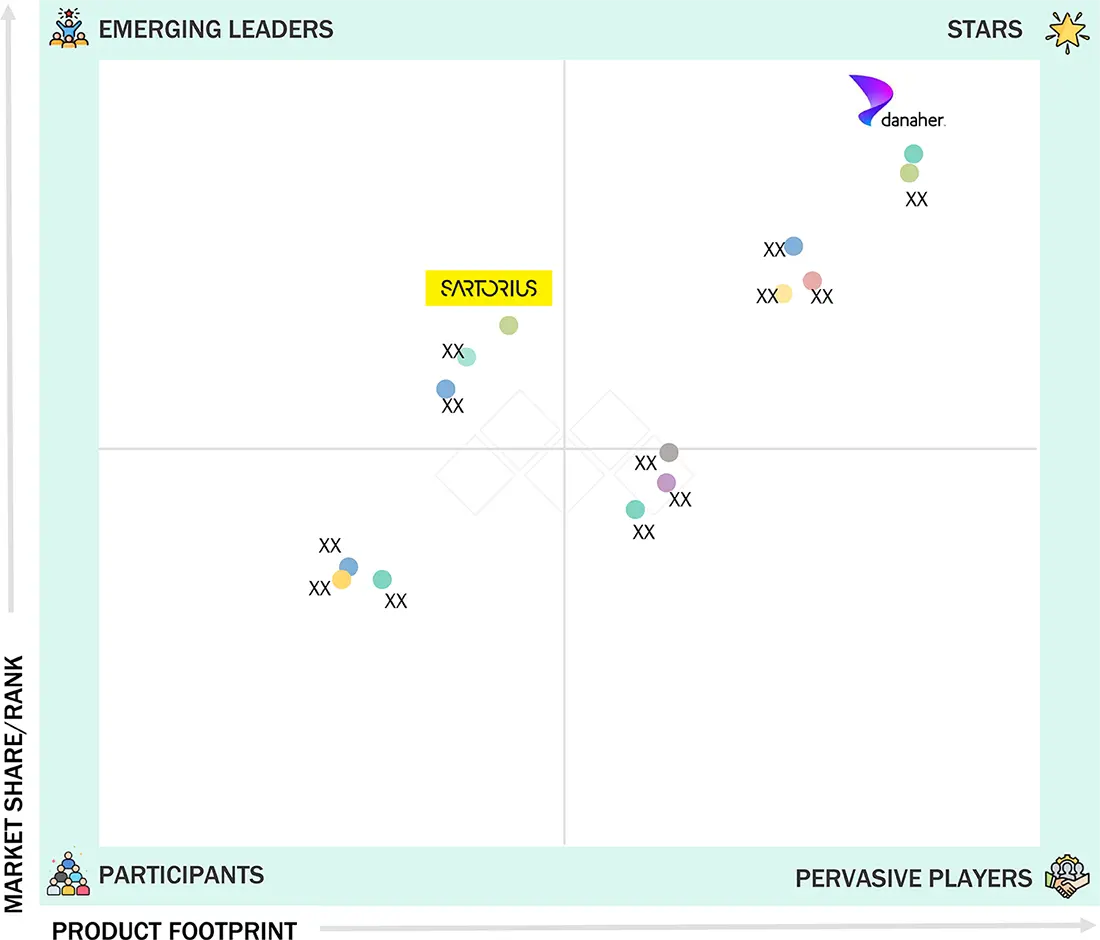

Chromatography Resin Market: COMPANY EVALUATION MATRIX

In the chromatography resins market matrix, Danaher Corporation (Star) leads with a strong market presence and wide product portfolio, driving large-scale adoption across industry. Sartorius Stedim Biotech S.A. (Emerging Leader) is gaining notable momentum within the chromatography resins market through the introduction of innovative solutions. These enhancements are positioning the company as a key player in the industry. While Danaher Corporation dominates with scale, Sartorius Stedim Biotech S.A. shows strong growth potential to advance toward the leaders’ quadrant.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size Value in 2024 | USD 3,02 BN |

| Revenue Forecast in 2030 | USD 4.94 BN |

| Growth Rate | CAGR of 8.62% from 2025−2030 |

| Actual Data | 2020−2030 |

| Base Year | 2024 |

| Forecast Period | 2025−2030 |

| Units Considered | Value (USD Billion), Volume (Liter) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Segments Covered | • By Type: Natural Polymers, Synthetic Resins, and Inorganic Media • By Technique: Ion Exchange (Cation and Anion), Affinity, Hydrophobic Interaction, Size Exclusion, Mixed Mode, Other Techniques • By Application: Pharmaceutical & Biotechnology (Producti |

| Regional Scope | Asia Pacific, North America, Europe, South America, and Middle East & Africa |

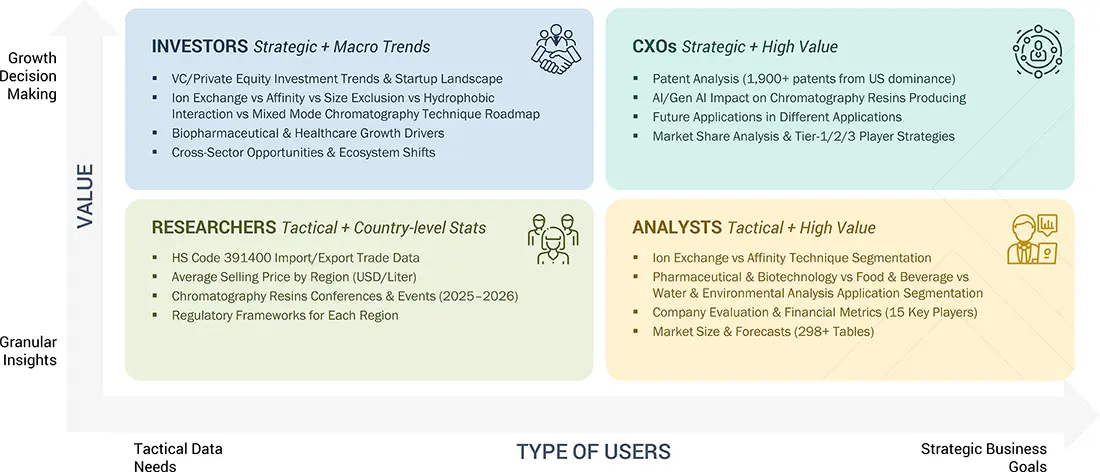

WHAT IS IN IT FOR YOU: Chromatography Resin Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| US-based Chromatography Resins Manufacturer | • Detailed US company profiles of competitors (financials, product portfolio) • Customer landscape mapping by end-use sector • Partnership ecosystem analysis | • Identify interconnections and supply chain blind spots • Detect customer migration trends across industries • Highlight untapped customer clusters for market entry |

| Asia Pacific-Based Chromatography Resins Manufacturer | • Global & regional production capacity benchmarking • Customer base profiling across the application industries | • Strengthen forward integration strategy • Identify high-demand customers for long-term supply contracts • Assess supply-demand gaps for competitive advantage |

RECENT DEVELOPMENTS

- May 2025 : Purolite launched a product called Praesto CH1 Chromatography Resin. The product is a 70µm agarose-based resin developed for specialized purification processes in biopharmaceutical manufacturing. It is engineered for high flow rates and robust performance in demanding applications.

- May 2024 : Sartorius Stedim Biotech S.A. launched Sartobind Rapid A resin, a high-flow membrane chromatography resin designed for rapid and efficient monoclonal antibody (mAb) purification. It enables faster processing times and scalability for large-scale biopharmaceutical production.

- October 2023 : Repligen Corporation acquired Sweden-based Metenova AB to strengthen its fluid management portfolio in bioprocessing. The acquisition brought advanced magnetic mixing technologies and the MixOne single-use platform into Repligen’s product lineup, enhancing its capabilities in both upstream and downstream applications.

- February 2022 : Sartorius Stedim Biotech acquired the Novasep chromatography division as of February 7, 2022, following approval by the US Federal Trade Commission. The portfolio acquired comprises chromatography systems primarily suited for smaller biomolecules, such as oligonucleotides, peptides, and insulin, as well as innovative systems for the continuous manufacturing of biologics.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

26

2

RESEARCH METHODOLOGY

33

3

EXECUTIVE SUMMARY

43

4

PREMIUM INSIGHTS

47

5

MARKET OVERVIEW

Surging demand for chromatography amid rising R&D, biosimilars, and proteomics opportunities.

50

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

Growing pharmaceutical and biopharmaceutical R&D activities

5.2.1.2

Increasing demand for therapeutic antibodies

5.2.1.3

Increasing demand for biosimilars

5.2.1.4

Rising food safety concerns

5.2.1.5

Increasing use of liquid chromatography-mass spectrometry in analytics and research

5.2.2

RESTRAINTS

5.2.2.1

Lack of skilled professionals

5.2.3

OPPORTUNITIES

5.2.3.1

Rise of CMOs and CROs in pharmaceutical industry

5.2.3.2

Growing demand for disposable pre-packed columns

5.2.3.3

Growing demand for chromatography in drug development and omics research

5.2.3.4

Growing use of chromatography in proteomics

5.2.4

CHALLENGES

5.2.4.1

Presence of alternative technologies to chromatography

5.3

PORTER'S FIVE FORCES ANALYSIS

5.3.1

THREAT OF SUBSTITUTES

5.3.2

BARGAINING POWER OF SUPPLIERS

5.3.3

BARGAINING POWER OF BUYERS

5.3.4

THREAT OF NEW ENTRANTS

5.3.5

INTENSITY OF COMPETITIVE RIVALRY

5.4

KEY STAKEHOLDERS & BUYING CRITERIA

5.4.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.4.2

BUYING CRITERIA

5.5

MACROECONOMIC INDICATORS

5.5.1

GDP TRENDS AND FORECAST FOR MAJOR ECONOMIES

6

INDUSTRY TRENDS

Navigate supply chain disruptions and tech innovations shaping chromatography resin markets globally.

66

6.1

SUPPLY CHAIN ANALYSIS

6.2

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.3

ECOSYSTEM ANALYSIS

6.4

TRADE ANALYSIS

6.4.1

IMPORT SCENARIO (HS CODE 391400)

6.4.2

EXPORT SCENARIO (HS CODE 391400)

6.5

PRICING ANALYSIS

6.5.1

AVERAGE SELLING PRICE OF CHROMATOGRAPHY RESINS OFFERED BY KEY PLAYERS, BY TECHNIQUE, 2024

6.5.2

AVERAGE SELLING PRICE TREND, BY REGION, 2022–2030

6.6

TECHNOLOGY ANALYSIS

6.6.1

KEY TECHNOLOGIES

6.6.1.1

Jetting

6.6.1.2

Microfluidics

6.6.2

COMPLEMENTARY TECHNOLOGIES

6.6.2.1

Surface modification via click chemistry

6.6.2.2

3D printing of chromatographic structures

6.7

CASE STUDY ANALYSIS

6.7.1

BIO-WORKS TECHNOLOGIES – WORKBEADS AFFIMAB FOR MONOCLONAL ANTIBODY PURIFICATION

6.7.2

CYTIVA – PROTEIN SELECT RESIN FOR TAG-BASED PROTEIN PURIFICATION

6.7.3

REPLIGEN – COVID-19 SPIKE PROTEIN AFFINITY RESIN FOR VACCINE DEVELOPMENT

6.8

REGULATORY LANDSCAPE

6.8.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.8.2

REGULATIONS

6.8.2.1

REACH Regulations (EC) No. 1907/2006 – European Union (ECHA)

6.8.2.2

USP <665>, <661.1>, and <661.2> – United States Pharmacopeia

6.8.2.3

WHO GMP Guidelines for Biological Products

6.8.2.4

ICH Q7 – GMP for Active Pharmaceutical Ingredients

6.8.2.5

21 CFR Part 210 & 211 – US (FDA)

6.8.2.6

EudraLex Volume 4 – EU GMP Guidelines (EMA)

6.9

KEY CONFERENCES AND EVENTS, 2025–2026

6.10

INVESTMENT AND FUNDING SCENARIO

6.11

PATENT ANALYSIS

6.11.1

APPROACH

6.11.2

PATENT TYPES

6.11.3

TOP APPLICANTS

6.11.4

JURISDICTION ANALYSIS

6.12

IMPACT OF AI/GEN AI ON CHROMATOGRAPHY RESINS MARKET

6.13

IMPACT OF 2025 US TARIFF ON CHROMATOGRAPHY RESINS MARKET

6.13.1

INTRODUCTION

6.13.2

KEY TARIFF RATES

6.13.3

PRICE IMPACT ANALYSIS

6.13.4

IMPACT ON COUNTRY/REGION

6.13.4.1

US

6.13.4.2

Europe

6.13.4.3

Asia Pacific

6.13.5

IMPACT ON END-USE INDUSTRY

6.13.5.1

Food & beverage industry

6.13.5.2

Pharmaceutical & biotechnology industry

7

CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Liters | 38 Data Tables

97

7.1

INTRODUCTION

7.2

ION EXCHANGE CHROMATOGRAPHY

7.2.1

HIGH DEMAND IN BIOPHARMACEUTICAL PROCESSES TO DRIVE MARKET

7.2.2

CATION EXCHANGE CHROMATOGRAPHY

7.2.3

ANION EXCHANGE CHROMATOGRAPHY

7.3

AFFINITY CHROMATOGRAPHY

7.3.1

INCREASING DEMAND FOR THERAPEUTIC PROTEINS TO DRIVE MARKET

7.3.2

BIOSPECIFIC LIGAND-BASED AFFINITY CHROMATOGRAPHY

7.3.2.1

Protein A affinity

7.3.2.2

Protein G affinity

7.3.2.3

Protein L affinity

7.3.2.4

Lectin affinity

7.3.2.5

Others

7.3.3

PSEUDO-BIOSPECIFIC LIGAND-BASED AFFINITY CHROMATOGRAPHY

7.3.3.1

IMAC

7.3.3.2

Dye-based ligands

7.3.3.3

Others

7.4

SIZE-EXCLUSION CHROMATOGRAPHY

7.4.1

WIDE APPLICATION IN LABORATORIES TO SUPPORT MARKET GROWTH

7.5

HYDROPHOBIC INTERACTION CHROMATOGRAPHY

7.5.1

RISING DEMAND FOR BIOSIMILARS TO DRIVE DEMAND

7.6

MIXED-MODE CHROMATOGRAPHY

7.6.1

BETTER DEGREE OF PURIFICATION THAN OTHER TECHNIQUES TO DRIVE MARKET

7.7

OTHER TECHNIQUES

7.7.1

PARTITION CHROMATOGRAPHY

7.7.2

ADSORPTION CHROMATOGRAPHY

8

CHROMATOGRAPHY RESINS MARKET, BY APPLICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 15 Data Tables

118

8.1

INTRODUCTION

8.2

PHARMACEUTICAL & BIOTECHNOLOGY

8.2.1

INCREASED R&D EXPENDITURE OF BIOTECHNOLOGY COMPANIES TO DRIVE DEMAND

8.2.2

PRODUCTION

8.2.3

ACADEMICS & RESEARCH

8.3

FOOD & BEVERAGE

8.3.1

STRINGENT REGULATIONS FOR FOOD SAFETY TO DRIVE MARKET

8.4

WATER & ENVIRONMENTAL ANALYSIS

8.4.1

RISING DEMAND FOR SAFE WATER AND STRINGENT REGULATIONS TO DRIVE GROWTH

8.5

OTHER APPLICATIONS

9

CHROMATOGRAPHY RESINS MARKET, BY REGION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Liters | 134 Data Tables

129

9.1

INTRODUCTION

9.2

ASIA PACIFIC

9.2.1

CHINA

9.2.1.1

Investments by companies in innovative drugs to drive market

9.2.2

JAPAN

9.2.2.1

Increasing demand for generic drugs and monoclonal antibody biosimilars to drive resin consumption

9.2.3

SOUTH KOREA

9.2.3.1

Government initiatives to boost production of biosimilars to drive market

9.2.4

INDIA

9.2.4.1

Growth of pharmaceutical & biotechnology industry to drive market

9.2.5

AUSTRALIA

9.2.5.1

Rising demand for monoclonal antibodies to drive market

9.2.6

NEW ZEALAND

9.2.6.1

Increasing demand for purification techniques in food industry to drive market

9.3

NORTH AMERICA

9.3.1

US

9.3.1.1

Increasing R&D investments in healthcare industry to drive demand

9.3.2

CANADA

9.3.2.1

Increased R&D activities in biopharmaceutical sector to support market growth

9.3.3

MEXICO

9.3.3.1

Initiatives to encourage biosimilars and biopharmaceutical research to drive demand

9.4

EUROPE

9.4.1

GERMANY

9.4.1.1

Increasing R&D investments by biotechnology companies to drive market

9.4.2

FRANCE

9.4.2.1

Increasing investments by pharmaceutical companies to drive market

9.4.3

UK

9.4.3.1

Top companies with therapeutic mAbs in different stages of R&D to drive market

9.4.4

ITALY

9.4.4.1

Established pharmaceutical industry to increase demand

9.4.5

SPAIN

9.4.5.1

Increasing R&D activities in pharmaceutical companies to drive market

9.4.6

SCANDINAVIA

9.4.6.1

Growing pharmaceutical industry to drive market

9.4.7

AUSTRIA

9.4.7.1

Increasing demand for monoclonal antibodies to drive market

9.4.8

SWITZERLAND

9.4.8.1

High investment in pharmaceutical research to have positive impact on market

9.5

MIDDLE EAST & AFRICA

9.5.1

GCC COUNTRIES

9.5.1.1

Saudi Arabia

9.5.1.2

UAE

9.6

SOUTH AMERICA

9.6.1

BRAZIL

9.6.1.1

Rising demand for low-cost biosimilars to drive demand

10

COMPETITIVE LANDSCAPE

Uncover strategic moves and market dominance of key players and startups in 2024.

197

10.1

INTRODUCTION

10.2

KEY PLAYER STRATEGIES/RIGHT TO WIN

10.3

MARKET SHARE ANALYSIS

10.4

REVENUE ANALYSIS

10.5

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.5.1

STARS

10.5.2

EMERGING LEADERS

10.5.3

PERVASIVE PLAYERS

10.5.4

PARTICIPANTS

10.5.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.5.5.1

Company footprint

10.5.5.2

Region footprint

10.5.5.3

Application footprint

10.5.5.4

Technique footprint

10.6

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

10.6.1

PROGRESSIVE COMPANIES

10.6.2

RESPONSIVE COMPANIES

10.6.3

DYNAMIC COMPANIES

10.6.4

STARTING BLOCKS

10.6.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

10.6.5.1

Detailed list of key startups/SMEs

10.6.5.2

Competitive benchmarking of key startups/SMEs

10.7

BRAND/PRODUCT COMPARISON ANALYSIS

10.8

COMPANY VALUATION AND FINANCIAL METRICS

10.9

COMPETITIVE SCENARIO

10.9.1

PRODUCT LAUNCHES

10.9.2

DEALS

10.9.3

EXPANSIONS

11

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

222

11.1

MAJOR PLAYERS

11.1.1

BIO-RAD LABORATORIES, INC.

11.1.1.1

Business overview

11.1.1.2

Products/Solutions/Services offered

11.1.1.3

Recent developments

11.1.1.4

MnM view

11.1.2

MERCK KGAA

11.1.3

DANAHER CORPORATION

11.1.4

TOSOH CORPORATION

11.1.5

SARTORIUS STEDIM BIOTECH S.A.

11.1.6

BIO-WORKS TECHNOLOGIES AB

11.1.7

AVANTOR, INC.

11.1.8

MITSUBISHI CHEMICAL GROUP CORPORATION

11.1.9

PUROLITE

11.1.10

REPLIGEN CORPORATION

11.1.11

THERMO FISHER SCIENTIFIC INC.

11.2

OTHER PLAYERS

11.2.1

SEPRAGEN CORPORATION

11.2.2

STEROGENE BIOSEPARATIONS, INC.

11.2.3

JACOBI GROUP

11.2.4

CHEMRA GMBH

11.2.5

SUNRESIN NEW MATERIALS CO. LTD.

11.2.6

BIOTOOLOMICS LIMITED

11.2.7

CUBE BIOTECH GMBH

11.2.8

JSR LIFE SCIENCES, LLC

11.2.9

NINGBO ZHENGGUANG RESIN CO., LTD.

11.2.10

CONCISE SEPARATIONS

11.2.11

GENSCRIPT BIOTECH CORPORATION

11.2.12

EICHROM TECHNOLOGIES, LLC

11.2.13

AGILENT TECHNOLOGIES, INC.

11.2.14

KANEKA CORPORATION

12

ADJACENT & RELATED MARKETS

280

12.1

INTRODUCTION

12.2

LIMITATIONS

12.3

CHROMATOGRAPHY REAGENTS MARKET

12.3.1

MARKET DEFINITION

12.3.2

MARKET OVERVIEW

12.4

CHROMATOGRAPHY REAGENTS MARKET, BY REGION

12.4.1

NORTH AMERICA

12.4.2

EUROPE

12.4.3

ASIA PACIFIC

12.4.4

LATIN AMERICA

12.4.5

MIDDLE EAST & AFRICA

13

APPENDIX

284

13.1

DISCUSSION GUIDE

13.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

13.3

CUSTOMIZATION OPTIONS

13.4

RELATED REPORTS

13.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

CHROMATOGRAPHY RESINS MARKET: INCLUSIONS AND EXCLUSIONS OF STUDY

TABLE 2

CHROMATOGRAPHY RESINS MARKET: DEFINITION AND INCLUSIONS, BY TYPE

TABLE 3

CHROMATOGRAPHY RESINS MARKET: DEFINITION AND INCLUSIONS, BY TECHNIQUE

TABLE 4

CHROMATOGRAPHY RESINS MARKET: DEFINITION AND INCLUSIONS, BY APPLICATION

TABLE 5

CHROMATOGRAPHY RESINS MARKET: RISK ASSESSMENT

TABLE 6

KEY BIOLOGICS UNDER THREAT OF PATENT EXPIRY

TABLE 7

APPLICATIONS OF LC-MS

TABLE 8

ADVANTAGES OF PRE-PACKED COLUMNS

TABLE 9

CHROMATOGRAPHY RESINS MARKET: PORTER’S FIVE FORCES ANALYSIS

TABLE 10

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS (%)

TABLE 11

KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

TABLE 12

GDP TRENDS AND FORECAST OF MAJOR ECONOMIES, 2021–2030 (USD BILLION)

TABLE 13

ROLE OF COMPANIES IN CHROMATOGRAPHY RESINS ECOSYSTEM

TABLE 14

IMPORT DATA RELATED TO HS CODE 391400-COMPLIANT PRODUCTS, BY REGION, 2019–2024 (USD MILLION)

TABLE 15

EXPORT DATA RELATED TO HS CODE 391400-COMPLIANT PRODUCTS, BY REGION, 2019–2024 (USD MILLION)

TABLE 16

AVERAGE SELLING PRICE TREND OF CHROMATOGRAPHY RESINS OFFERED BY KEY PLAYERS, BY TECHNIQUE, 2024 (USD/LITER)

TABLE 17

GLOBAL: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 18

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 19

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 20

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 21

SOUTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 22

MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 23

CHROMATOGRAPHY RESINS MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2025–2026

TABLE 24

CHROMATOGRAPHY RESINS MARKET: FUNDING/INVESTMENT SCENARIO

TABLE 25

CHROMATOGRAPHY RESINS MARKET: PATENT STATUS, 2014–2024

TABLE 26

CHROMATOGRAPHY RESINS MARKET: LIST OF MAJOR PATENTS, 2014–2024

TABLE 27

PATENTS BY DOW GLOBAL TECHNOLOGIES, LLC

TABLE 28

PATENTS BY AGC INC.

TABLE 29

US: ADJUSTED RECIPROCAL TARIFF RATES

TABLE 30

CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 31

CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 32

CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 33

CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 34

ION EXCHANGE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 35

ION EXCHANGE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 36

ION EXCHANGE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (LITER)

TABLE 37

ION EXCHANGE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (LITER)

TABLE 38

ION EXCHANGE: CHROMATOGRAPHY RESINS MARKET, BY TYPE OF CHARGE, 2020–2024 (USD MILLION)

TABLE 39

ION EXCHANGE: CHROMATOGRAPHY RESINS MARKET, BY TYPE OF CHARGE, 2025–2030 (USD MILLION)

TABLE 40

ION EXCHANGE: CHROMATOGRAPHY RESINS MARKET, BY TYPE OF CHARGE, 2020–2024 (LITER)

TABLE 41

ION EXCHANGE: CHROMATOGRAPHY RESINS MARKET, BY TYPE OF CHARGE, 2025–2030 (LITER)

TABLE 42

CATION EXCHANGE CHROMATOGRAPHY RESINS: LIGAND FUNCTIONAL GROUPS

TABLE 43

ANION EXCHANGE CHROMATOGRAPHY RESINS: LIGAND FUNCTIONAL GROUPS

TABLE 44

AFFINITY CHROMATOGRAPHY RESINS: LIGANDS

TABLE 45

AFFINITY: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 46

AFFINITY: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 47

AFFINITY: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (LITER)

TABLE 48

AFFINITY: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (LITER)

TABLE 49

AFFINITY CHROMATOGRAPHY: LIGANDS

TABLE 50

AFFINITY: CHROMATOGRAPHY RESINS MARKET, BY TYPE OF LIGAND INTERACTION, 2020–2024 (USD MILLION)

TABLE 51

AFFINITY: CHROMATOGRAPHY RESINS MARKET, BY TYPE OF LIGAND INTERACTION, 2025–2030 (USD MILLION)

TABLE 52

SIZE EXCLUSION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 53

SIZE EXCLUSION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 54

SIZE EXCLUSION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (LITER)

TABLE 55

SIZE EXCLUSION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (LITER)

TABLE 56

HYDROPHOBIC INTERACTION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 57

HYDROPHOBIC INTERACTION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 58

HYDROPHOBIC INTERACTION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (LITER)

TABLE 59

HYDROPHOBIC INTERACTION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (LITER)

TABLE 60

MIXED MODE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 61

MIXED MODE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 62

MIXED MODE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (LITER)

TABLE 63

MIXED MODE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (LITER)

TABLE 64

OTHER TECHNIQUES: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 65

OTHER TECHNIQUES: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 66

OTHER TECHNIQUES: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (LITER)

TABLE 67

OTHER TECHNIQUES: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (LITER)

TABLE 68

CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 69

CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 70

PHARMACEUTICAL & BIOTECHNOLOGY: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 71

PHARMACEUTICAL & BIOTECHNOLOGY: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 72

PHARMACEUTICAL & BIOTECHNOLOGY PRODUCTION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 73

PHARMACEUTICAL & BIOTECHNOLOGY PRODUCTION: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 74

PHARMACEUTICAL & BIOTECHNOLOGY ACADEMICS & RESEARCH: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 75

PHARMACEUTICAL & BIOTECHNOLOGY ACADEMICS & RESEARCH: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 76

FOOD & BEVERAGE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 77

FOOD & BEVERAGE: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 78

CHEMICAL CONTAMINANTS AND CHROMATOGRAPHY TECHNOLOGIES

TABLE 79

WATER & ENVIRONMENTAL ANALYSIS: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 80

WATER & ENVIRONMENTAL ANALYSIS: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 81

OTHER APPLICATIONS: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 82

OTHER APPLICATIONS: CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 83

CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 84

CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 85

CHROMATOGRAPHY RESINS MARKET, BY REGION, 2020–2024 (LITER)

TABLE 86

CHROMATOGRAPHY RESINS MARKET, BY REGION, 2025–2030 (LITER)

TABLE 87

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 88

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 89

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 90

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 91

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 92

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 93

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 94

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 95

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (LITER)

TABLE 96

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (LITER)

TABLE 97

CHINA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 98

CHINA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 99

CHINA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 100

CHINA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 101

JAPAN: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 102

JAPAN: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE,2025–2030 (USD MILLION)

TABLE 103

JAPAN: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 104

JAPAN: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 105

SOUTH KOREA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 106

SOUTH KOREA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 107

SOUTH KOREA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 108

SOUTH KOREA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 109

INDIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 110

INDIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 111

INDIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 112

INDIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 113

AUSTRALIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 114

AUSTRALIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 115

AUSTRALIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 116

AUSTRALIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 117

NEW ZEALAND: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 118

NEW ZEALAND: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 119

NEW ZEALAND: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE,2020–2024 (LITER)

TABLE 120

NEW ZEALAND: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 121

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 122

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 123

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 124

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 125

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 126

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 127

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 128

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 129

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (LITER)

TABLE 130

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (LITER)

TABLE 131

US: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 132

US: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 133

US: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 134

US: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 135

CANADA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 136

CANADA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 137

CANADA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 138

CANADA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 139

MEXICO: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 140

MEXICO: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 141

MEXICO: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 142

MEXICO: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 143

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 144

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 145

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 146

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 147

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 148

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 149

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 150

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 151

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (LITER)

TABLE 152

EUROPE: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (LITER)

TABLE 153

GERMANY: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 154

GERMANY: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 155

GERMANY: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 156

GERMANY: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 157

FRANCE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 158

FRANCE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 159

FRANCE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 160

FRANCE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 161

UK: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 162

UK: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 163

UK: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 164

UK: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 165

ITALY: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 166

ITALY: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 167

ITALY: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 168

ITALY: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 169

SPAIN: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 170

SPAIN: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 171

SPAIN: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 172

SPAIN: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 173

SCANDINAVIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 174

SCANDINAVIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 175

SCANDINAVIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 176

SCANDINAVIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 177

AUSTRIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 178

AUSTRIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 179

AUSTRIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 180

AUSTRIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 181

SWITZERLAND: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 182

SWITZERLAND: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 183

SWITZERLAND: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 184

SWITZERLAND: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 185

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 186

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 187

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 188

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 189

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 190

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 191

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 192

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 193

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (LITER)

TABLE 194

MIDDLE EAST & AFRICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (LITER)

TABLE 195

SAUDI ARABIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 196

SAUDI ARABIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 197

SAUDI ARABIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 198

SAUDI ARABIA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 199

UAE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 200

UAE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 201

UAE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 202

UAE: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 203

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 204

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 205

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 206

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 207

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2020–2024 (USD MILLION)

TABLE 208

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 209

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 210

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 211

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2020–2024 (LITER)

TABLE 212

SOUTH AMERICA: CHROMATOGRAPHY RESINS MARKET, BY COUNTRY, 2025–2030 (LITER)

TABLE 213

BRAZIL: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (USD MILLION)

TABLE 214

BRAZIL: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 215

BRAZIL: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2020–2024 (LITER)

TABLE 216

BRAZIL: CHROMATOGRAPHY RESINS MARKET, BY TECHNIQUE, 2025–2030 (LITER)

TABLE 217

CHROMATOGRAPHY RESINS MARKET: KEY STRATEGIES ADOPTED BY MAJOR PLAYERS

TABLE 218

CHROMATOGRAPHY RESINS MARKET: DEGREE OF COMPETITION, 2024

TABLE 219

CHROMATOGRAPHY RESINS MARKET: REGION FOOTPRINT

TABLE 220

CHROMATOGRAPHY RESINS MARKET: APPLICATION FOOTPRINT

TABLE 221

CHROMATOGRAPHY RESINS MARKET: TECHNIQUE FOOTPRINT

TABLE 222

CHROMATOGRAPHY RESINS MARKET: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 223

CHROMATOGRAPHY RESINS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 224

CHROMATOGRAPHY RESINS MARKET: PRODUCT LAUNCHES, JANUARY 2020–MAY 2025

TABLE 225

CHROMATOGRAPHY RESINS MARKET: DEALS, JANUARY 2020–MAY 2025

TABLE 226

CHROMATOGRAPHY RESINS MARKET: EXPANSIONS, JANUARY 2020–MAY 2025

TABLE 227

BIO-RAD LABORATORIES, INC.: COMPANY OVERVIEW

TABLE 228

BIO-RAD LABORATORIES, INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 229

BIO-RAD LABORATORIES, INC.: PRODUCT LAUNCHES

TABLE 230

BIO-RAD LABORATORIES, INC.: DEALS

TABLE 231

BIO-RAD LABORATORIES, INC.: EXPANSIONS

TABLE 232

MERCK KGAA: COMPANY OVERVIEW

TABLE 233

MERCK KGAA: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 234

MERCK KGAA: PRODUCT LAUNCHES

TABLE 235

MERCK KGAA: DEALS

TABLE 236

MERCK KGAA: EXPANSIONS

TABLE 237

DANAHER CORPORATION: COMPANY OVERVIEW

TABLE 238

DANAHER CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 239

DANAHER CORPORATION: PRODUCT LAUNCHES

TABLE 240

DANAHER CORPORATION: DEALS

TABLE 241

DANAHER CORPORATION: EXPANSIONS

TABLE 242

TOSOH CORPORATION: COMPANY OVERVIEW

TABLE 243

TOSOH CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 244

TOSOH CORPORATION: PRODUCT LAUNCHES

TABLE 245

TOSOH CORPORATION: DEALS

TABLE 246

TOSOH CORPORATION: EXPANSIONS

TABLE 247

SARTORIUS STEDIM BIOTECH S.A.: COMPANY OVERVIEW

TABLE 248

SARTORIUS STEDIM BIOTECH S.A.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 249

SARTORIUS STEDIM BIOTECH S.A.: PRODUCT LAUNCHES

TABLE 250

SARTORIUS STEDIM BIOTECH S.A.: DEALS

TABLE 251

BIO-WORKS TECHNOLOGIES AB: COMPANY OVERVIEW

TABLE 252

BIO-WORKS TECHNOLOGIES AB: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 253

BIO-WORKS TECHNOLOGIES AB: PRODUCT LAUNCHES

TABLE 254

BIO-WORKS TECHNOLOGIES AB: DEALS

TABLE 255

AVANTOR, INC.: COMPANY OVERVIEW

TABLE 256

AVANTOR, INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 257

AVANTOR, INC.: PRODUCT LAUNCHES

TABLE 258

AVANTOR, INC.: DEALS

TABLE 259

AVANTOR, INC.: EXPANSIONS

TABLE 260

MITSUBISHI CHEMICAL GROUP CORPORATION: COMPANY OVERVIEW

TABLE 261

MITSUBISHI CHEMICAL GROUP CORPORATION: PRODUCTS/SERVICES/ SOLUTIONS OFFERED

TABLE 262

MITSUBISHI CHEMICAL GROUP CORPORATION: PRODUCT LAUNCHES

TABLE 263

MITSUBISHI CHEMICAL GROUP CORPORATION: EXPANSIONS

TABLE 264

PUROLITE: COMPANY OVERVIEW

TABLE 265

PUROLITE: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 266

PUROLITE: PRODUCT LAUNCHES

TABLE 267

PUROLITE: DEALS

TABLE 268

PUROLITE: EXPANSIONS

TABLE 269

REPLIGEN CORPORATION: COMPANY OVERVIEW

TABLE 270

REPLIGEN CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 271

REPLIGEN CORPORATION: PRODUCT LAUNCHES

TABLE 272

REPLIGEN CORPORATION: DEALS

TABLE 273

REPLIGEN CORPORATION: EXPANSIONS

TABLE 274

THERMO FISHER SCIENTIFIC INC.: COMPANY OVERVIEW

TABLE 275

THERMO FISHER SCIENTIFIC INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 276

THERMO FISHER SCIENTIFIC INC.: PRODUCT LAUNCHES

TABLE 277

THERMO FISHER SCIENTIFIC INC.: DEALS

TABLE 278

THERMO FISHER SCIENTIFIC INC.: EXPANSIONS

TABLE 279

SEPRAGEN CORPORATION: COMPANY OVERVIEW

TABLE 280

STEROGENE BIOSEPARATIONS, INC.: COMPANY OVERVIEW

TABLE 281

JACOBI GROUP: COMPANY OVERVIEW

TABLE 282

CHEMRA GMBH: COMPANY OVERVIEW

TABLE 283

SUNRESIN NEW MATERIALS CO. LTD.: COMPANY OVERVIEW

TABLE 284

BIOTOOLOMICS LIMITED: COMPANY OVERVIEW

TABLE 285

CUBE BIOTECH GMBH: COMPANY OVERVIEW

TABLE 286

JSR LIFE SCIENCES, LLC: COMPANY OVERVIEW

TABLE 287

NINGBO ZHENGGUANG RESIN CO., LTD.: COMPANY OVERVIEW

TABLE 288

CONCISE SEPARATIONS: COMPANY OVERVIEW

TABLE 289

GENSCRIPT BIOTECH CORPORATION: COMPANY OVERVIEW

TABLE 290

EICHROM TECHNOLOGIES, LLC: COMPANY OVERVIEW

TABLE 291

AGILENT TECHNOLOGIES, INC.: COMPANY OVERVIEW

TABLE 292

KANEKA CORPORATION: COMPANY OVERVIEW

TABLE 293

CHROMATOGRAPHY REAGENTS MARKET, BY REGION, 2022–2029 (USD MILLION)

TABLE 294

NORTH AMERICA: CHROMATOGRAPHY REAGENTS MARKET, BY TYPE, 2022–2029 (USD MILLION)

TABLE 295

EUROPE: CHROMATOGRAPHY REAGENTS MARKET, BY TYPE, 2022–2029 (USD MILLION)

TABLE 296

ASIA PACIFIC: CHROMATOGRAPHY REAGENTS MARKET, BY TYPE, 2022–2029 (USD MILLION)

TABLE 297

LATIN AMERICA: CHROMATOGRAPHY REAGENTS MARKET, BY TYPE, 2022–2029 (USD MILLION)

TABLE 298

MIDDLE EAST & AFRICA: CHROMATOGRAPHY REAGENTS MARKET, BY TYPE, 2022–2029 (USD MILLION)

LIST OF FIGURES

FIGURE 1

CHROMATOGRAPHY RESINS MARKET: SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

CHROMATOGRAPHY RESINS MARKET: RESEARCH DESIGN

FIGURE 3

MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 (SUPPLY SIDE): COMBINED REVENUE OF MAJOR PLAYERS

FIGURE 4

MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 - BOTTOM-UP (SUPPLY SIDE): COLLECTIVE REVENUE AND SHARE OF MAJOR PLAYERS

FIGURE 5

MARKET SIZE ESTIMATION: APPROACH 2 - BOTTOM-UP (SUPPLY SIDE): COLLECTIVE REVENUE FROM SALE OF CHROMATOGRAPHY RESINS

FIGURE 6

MARKET SIZE ESTIMATION: APPROACH 2 - BOTTOM-UP (DEMAND SIDE): PRODUCTS SOLD AND THEIR AVERAGE SELLING PRICE

FIGURE 7

CHROMATOGRAPHY RESINS MARKET: DATA TRIANGULATION

FIGURE 8

MARKET CAGR PROJECTIONS FROM SUPPLY SIDE

FIGURE 9

MARKET GROWTH PROJECTIONS FROM DEMAND SIDE DRIVERS AND OPPORTUNITIES

FIGURE 10

PHARMACEUTICAL & BIOTECHNOLOGY SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

FIGURE 11

NATURAL POLYMERS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

FIGURE 12

AFFINITY CHROMATOGRAPHY TECHNIQUE TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 13

NORTH AMERICA ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

FIGURE 14

GROWING DEMAND FROM PHARMACEUTICAL & BIOTECHNOLOGY SEGMENT TO DRIVE MARKET

FIGURE 15

NORTH AMERICA TO DOMINATE CHROMATOGRAPHY RESINS MARKET DURING FORECAST PERIOD

FIGURE 16

ION EXCHANGE SEGMENT ACCOUNTED FOR LARGEST SHARE OF NORTH AMERICAN CHROMATOGRAPHY RESINS MARKET IN 2024

FIGURE 17

ION EXCHANGE TO BE MOST WIDELY ADOPTED TECHNIQUE DURING FORECAST PERIOD

FIGURE 18

ION EXCHANGE SEGMENT LED CHROMATOGRAPHY RESINS MARKET ACROSS ALL REGIONS IN 2024

FIGURE 19

INDIA TO REGISTER HIGHEST CAGR BETWEEN 2025 AND 2030

FIGURE 20

CHROMATOGRAPHY RESINS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 21

GLOBAL PHARMACEUTICAL R&D SPENDING, 2014–2024 (USD BILLION)

FIGURE 22

WORLDWIDE GENERIC DRUG SALES, 2014–2024 (USD BILLION)

FIGURE 23

PORTER'S FIVE FORCES ANALYSIS: CHROMATOGRAPHY RESINS MARKET

FIGURE 24

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS

FIGURE 25

KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

FIGURE 26

CHROMATOGRAPHY RESINS MARKET: SUPPLY CHAIN ANALYSIS

FIGURE 27

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 28

CHROMATOGRAPHY RESINS MARKET: KEY PLAYERS IN ECOSYSTEM

FIGURE 29

IMPORT DATA FOR HS CODE 391400-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2019–2024 (USD MILLION)

FIGURE 30

EXPORT DATA FOR HS CODE 391400-COMPLIANT PRODUCTS, BY KEY COUNTRY, 2019–2024 (USD MILLION)

FIGURE 31

AVERAGE SELLING PRICE OF CHROMATOGRAPHY RESINS OFFERED BY KEY PLAYERS, BY TECHNIQUE, 2024

FIGURE 32

AVERAGE SELLING PRICE TREND OF CHROMATOGRAPHY RESINS, BY REGION, 2022–2030 (USD/LITER)

FIGURE 33

PATENTS REGISTERED RELATED TO CHROMATOGRAPHY RESINS, 2014–2024

FIGURE 34

TOP PATENT OWNERS, 2014–2024

FIGURE 35

LEGAL STATUS OF PATENTS FILED FOR CHROMATOGRAPHY RESINS, 2014–2024

FIGURE 36

MAJOR PATENTS FILED IN US JURISDICTION, 2014–2024

FIGURE 37

CHROMATOGRAPHY RESINS MARKET: IMPACT OF AI/GEN AI

FIGURE 38

MIXED MODE TECHNIQUE TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 39

PHARMACEUTICAL & BIOTECHNOLOGY SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 40

ASIA PACIFIC TO REGISTER FASTEST GROWTH DURING FORECAST PERIOD

FIGURE 41

ASIA PACIFIC: CHROMATOGRAPHY RESINS MARKET SNAPSHOT

FIGURE 42

NORTH AMERICA: CHROMATOGRAPHY RESINS MARKET SNAPSHOT

FIGURE 43

EUROPE: CHROMATOGRAPHY RESINS MARKET SNAPSHOT

FIGURE 44

CHROMATOGRAPHY RESINS MARKET SHARE ANALYSIS, 2024

FIGURE 45

CHROMATOGRAPHY RESINS MARKET: REVENUE ANALYSIS OF KEY COMPANIES, 2020–2024 (USD MILLION)

FIGURE 46

CHROMATOGRAPHY RESINS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 47

CHROMATOGRAPHY RESINS MARKET: COMPANY FOOTPRINT

FIGURE 48

CHROMATOGRAPHY RESINS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 49

CHROMATOGRAPHY RESINS MARKET: BRAND/PRODUCT COMPARISON

FIGURE 50

CHROMATOGRAPHY RESINS MARKET: EV/EBITDA OF KEY COMPANIES

FIGURE 51

CHROMATOGRAPHY RESINS MARKET: ENTERPRISE VALUATION (EV) OF KEY PLAYERS

FIGURE 52

BIO-RAD LABORATORIES, INC.: COMPANY SNAPSHOT

FIGURE 53

MERCK KGAA: COMPANY SNAPSHOT

FIGURE 54

DANAHER CORPORATION: COMPANY SNAPSHOT

FIGURE 55

TOSOH CORPORATION: COMPANY SNAPSHOT

FIGURE 56

SARTORIUS STEDIM BIOTECH S.A.: COMPANY SNAPSHOT

FIGURE 57

BIO-WORKS TECHNOLOGIES AB: COMPANY SNAPSHOT

FIGURE 58

AVANTOR, INC.: COMPANY SNAPSHOT

FIGURE 59

MITSUBISHI CHEMICAL GROUP CORPORATION: COMPANY SNAPSHOT

FIGURE 60

REPLIGEN CORPORATION: COMPANY SNAPSHOT

FIGURE 61

THERMO FISHER SCIENTIFIC INC.: COMPANY SNAPSHOT

Methodology

The study involved four major activities in estimating the market size for the chromatography resin market. Exhaustive secondary research was done to collect information on the market, the peer market, and the parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, the market breakdown and data triangulation procedures were used to estimate the market size of the segments and subsegments.

Secondary Research

Secondary sources used in this study included annual reports, press releases, and investor presentations of companies; white papers; certified publications; articles from recognized authors; and gold standard & silver standard websites such as Factiva, ICIS, Bloomberg, and others. The findings of this study were verified through primary research by conducting extensive interviews with key officials such as CEOs, VPs, directors, and other executives. The breakdown of profiles of the primary interviewees is illustrated in the figure below:

Primary Research

The chromatography resin market comprises several stakeholders, such as raw material suppliers, end-product manufacturers, and regulatory organizations in the supply chain. The demand side of this market is characterized by key opinion leaders in various applications for the chromatography resin market. The supply side is characterized by advancements in technology and diverse application industries. Various primary sources from both the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information.

Breakdown of Primary Participants

Note: Tier 1, Tier 2, and Tier 3 companies are classified based on their market revenue in 2024/2025, available in the public domain, product portfolios, and geographical presence.

Other designations include consultants and sales, marketing, and procurement managers.

To know about the assumptions considered for the study, download the pdf brochure

| COMPANY NAME | DESIGNATION | |

|---|---|---|

| Danaher Corporation | Senior Manager | |

| Bio-Rad Laboratories, Inc. | Innovation Manager | |

| Bio-Works Technologies AB | Vice-President | |

| Tosoh Corporation | Production Supervisor | |

| Thermo Fisher Scientific Inc. | Sales Manager | |

Market Size Estimation

Both top-down and bottom-up approaches were used to estimate and validate the total size of the chromatography resin market. These methods were also used extensively to estimate the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

- The key players in the industry have been identified through extensive secondary research.

- The supply chain of the industry has been determined through primary and secondary research.

- All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

- All possible parameters that affect the markets covered in this research study have been accounted for, viewed in extensive detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data.

Data Triangulation

After arriving at the overall market size—using the market size estimation processes as explained above—the market was split into several segments and subsegments. To complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment, data triangulation, and market breakdown procedures were employed, wherever applicable. The data was triangulated by studying various factors and trends from both the demand and supply sides in the chromatography resin industry.

Market Definition

Chromatography resins are insoluble matrix materials used in chromatography procedures to resolve, purify, or characterize complex mixtures of biological or chemical compounds. Different types of these resins have stationary phases designed to be natural polymers (agarose or cellulose), synthetic polymers, and inorganic media. They interact with target molecules, and this allows their accurate separation and purification by mechanisms that include ion exchange, affinity, hydrophobic interaction, size exclusion, and others. Chromatography resins find extensive use in industries like pharmaceutical industries, biotechnology industries, food & beverage manufacturing industries, environmental testing, and research laboratories. They are of paramount importance in single small-scale manufacturing of biopharmaceutical products, including monoclonal antibodies, vaccines, and recombinant proteins. The chromatography resin market includes areas of production and development of these resins as well as their distribution, which have been motivated by the modernization in the bioseparation technologies, regulatory requirements, and the growing investment in the life sciences and analytical testing.

Stakeholders

- Chromatography Resin Manufacturers

- Chromatography Resin Distributors

- Raw Material Suppliers

- Service Providers

- Packaging Companies

- Government and Research Organizations

Report Objectives

- To define, describe, segment, and forecast the transfection technologies market by product type, method, application, end user, and region

- To provide detailed information about the major factors (such as drivers, restraints, opportunities, and challenges) influencing the market growth

- To strategically analyze micromarkets1 with respect to individual growth trends, prospects, and contributions to the overall market

- To analyze market opportunities for stakeholders and provide details of the competitive landscape for key players

- To forecast the size of the transfection technologies market in five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, along with their respective key countries

- To profile the key players in the transfection technologies market and comprehensively analyze their core competencies2 and market shares

- To track and analyze competitive developments, such as product launches, acquisitions, expansions, collaborations, agreements, and partnerships of the leading players in the transfection technologies market

- To benchmark players within the transfection technologies market using the ‘Competitive Leadership Mapping’ framework, which analyzes market players based on various parameters, including product portfolio, geographic reach, and market share/rank

Key Questions Addressed by the Report

Who are the major players in the chromatography resin market?

Major players include Bio-Rad Laboratories, Inc. (US), Merck KGaA (Germany), Danaher Corporation (US), Tosoh Corporation (Japan), Sartorius Stedim Biotech S.A. (France), Bio-Works Technologies AB (Sweden), Avantor, Inc. (US), and Purolite (US), among others.

What are the drivers and opportunities for the chromatography resin market?

Key drivers include increased pharmaceutical and biotech R&D, growing demand for therapeutic antibodies and biosimilars, concern for food safety, and rising adoption of LC-MS in analytics. Opportunities lie in the growth of contract manufacturing and CROs, demand for disposable pre-packed columns, and increasing use in drug development, omics research, and proteomics.

Which strategies are the key players focusing on in the chromatography resin market?

The main strategies include product launches, partnerships, mergers & acquisitions, agreements, and geographical expansions to increase global market presence.

What is the expected growth rate of the chromatography resin market between 2025 and 2030?

The market is projected to grow at a CAGR of 8.6% during the forecast period (2025–2030).

Which major factors are expected to restrain the growth of the chromatography resin market?

Growth restraints include performance limitations in harsh environments, high costs, and significant equipment investment requirements.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Chromatography Resin Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

We at Nissan Chemicals Corporation have been clients of MarketsandMarkets for more than a year now. We recently consulted MarketsandMarkets for a study, the team at MarketsandMarkets was extremely professional and organized. The business insights were very detailed and aligned well with our expectations that really helped us formulate the Business Plans and device new strategies for development themes. MarketsandMarkets offers a unique combination of expertise and dedicated engagement model. Their research findings have helped us in designing our Pricing Strategy which will make it easier for us to predict the future sales and profits for the next ten years. We look forward to working with MarketsandMarkets in the future.

VP of Strategy & New Business Development

Leading Specialty Chemical Company

The MarketsandMarkets Engagement Model, composed of both the Knowledge Store and advisory custom research, has greatly helped us in understanding our markets and making strategic decisions. The Knowledge Store is a fast way to allow everyone in our organization to understand more about most any market they are interested in. The ability to then get custom research done and get answers to specific strategic questions and market insight has been spectacular. The Markets and Markets team feel more like colleagues than vendors and their services have helped us change our culture where statements of things like growth opportunities and competitive position are always backed by industry research.

Rich Gibson,

Director, Corporate Strategy

Milliken & Company,

Leading Industrial Manufacturer of specialty chemical, floor covering, performance and protective textile materials, and healthcaremilliken.com

MarketsandMarkets is a trusted resource that helps us to better understand markets that are near-adjacencies-whether its technology, value chain or geography. Their Knowledge Store platform provides a dashboard of markets and their characteristics which is easy to use and saves us time.

Adam Shaw,

Market Development and Strategy Manager

AdvanSix Inc. USA,

An American Leader in Chemicalswww.advansix.com

The Knowledge Store from MarketsandMarkets is a valuable tool which has helped my team acquire greater insight in to the end markets that our business serves. This has enabled us to help our company build stronger strategies throughout our planning process.

TOSHIO KINOSHITA

Senior Chif Consultion Research & Consulting Division

Mitsubishi Chemical Research Corporation,

Leading Manufacturer of Chemical Productswww.mitsubishichem-res.co.jp/en/

We recently engaged with MarketsandMarkets for a study, the team not only clearly understood our business objectives but was also extremely professional in the way they handled the entire project. The study was efficiently conducted in a phase-wise manner, and the engagement model furnished us with high-quality business insights that far exceeded our expectations at each phase. We were especially happy that MarketsandMarkets could provide us with both, an English as well as a Japanese version of the study. A special thanks to the Analyst Team and Client Services Team, whose fluency in Japanese enhanced our comfort level, as we could converse with them in our preferred language.

Independent entrepreneurs

Arrow Precision

We approached MarketsandMarkets for study on Proppants Market, and their work exceeded our expectations. The study conducted was comprehensive and enabled us to view the market through the various dimensions. In addition, the team was extraordinarily responsive throughout the process and resolved our queries on time. I strongly recommend MarketsandMarkets and will certainly consider them for additional market assessments we will need in the future.

Global engineering company, Japan

Deputy Manager,

Strategic Planning OfficeThe high-quality insights shared by the MarketsandMarkets team helped us understand the pharmaceutical plant designers in a specific geography. It also captured the risks that we may likely face in communicating with our potential partners. The study would enable us identify partners, which would impact our future growth.

- China Chromatography Resin Market

- Japan Chromatography Resin Market

- South Korea Chromatography Resin Market

- India Chromatography Resin Market

- Australia Chromatography Resin Market

- New Zealand Chromatography Resin Market

- US Chromatography Resin Market

- Canada Chromatography Resin Market

- Mexico Chromatography Resin Market

- Germany Chromatography Resin Market

- France Chromatography Resin Market

- UK Chromatography Resin Market

- Italy Chromatography Resin Market

- Spain Chromatography Resin Market

- Austria Chromatography Resin Market

- Switzerland Chromatography Resin Market

- Saudi Arabia Chromatography Resin Market

- UAE Chromatography Resin Market

- Brazil Chromatography Resin Market

- Rest Of Europe Chromatography Resin Market

- Scandinavia Chromatography Resin Market

- Rest Of Asia Pacific Chromatography Resin Market

Growth opportunities and latent adjacency in Chromatography Resin Market