Download PDF

Download PDF Request Customisation

Request Customisation

Cryocooler Market Size, Share & Trends

Report Code

SE 4258

Published in

Sep, 2025, By MarketsandMarkets™

Cryocooler Market Size, Share & Trends by Recuperative Heat Exchanger, Regenerative Heat Exchanger, Heat Dissipation Pipe, Preventive Maintenance Services, Gifford-McMahon Cryocoolers, Stirling Cryocoolers, Joule Thomson Cryocoolers, Military, Space - Global Forecast to 2030

USD 4.90 BN

MARKET SIZE, 2030

CAGR 7.1%

(2025-2030)

265

REPORT PAGES

225

MARKET TABLES

CRYOCOOLER MARKET SIZE, SHARE & TRENDS

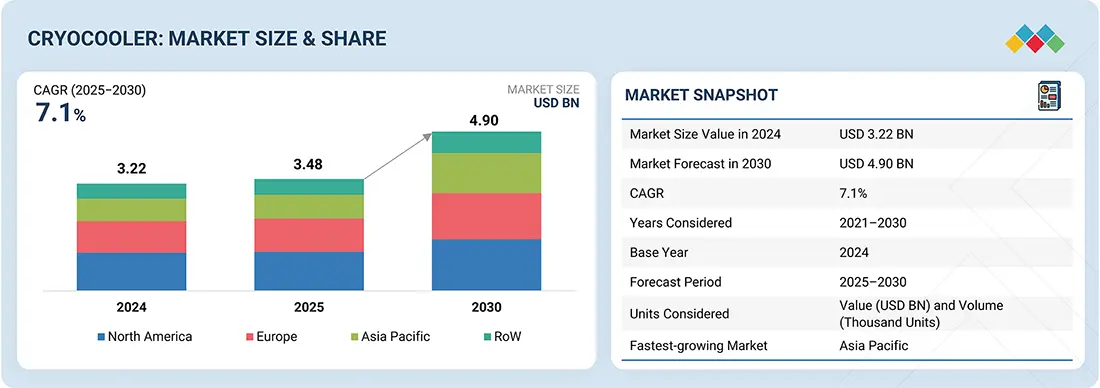

According to Marketsandmarkets; The cryocooler market is expected to be valued at USD 3.48 billion in 2025 and USD 4.90 billion by 2030. It is expected to register a CAGR of 7.1% during the forecast period. This is driven by the rising demand for compact, energy-efficient cooling technologies that support advanced aerospace, defense, and medical applications. Increasing focus on satellite missions, coupled with advancements in infrared detectors, superconducting magnets, and quantum devices, accelerate adoption. Cryocooler solutions offer improved thermal stability, vibration-free operation, and long operational lifespans, enabling reliable performance in critical environments.CRYOCOOLER MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size Value in 2025 | USD 3.48 BN |

| Revenue Forecast in 2030 | USD 4.90 BN |

| Growth Rate | 7.10% |

| Years Considered | 2021–2030 |

| Base Year | 2024 |

| Forecast Period | 2025–2030 |

| Units Considered | Value (USD Billion) and Volume (Thousand Units) |

| Report Coverage | Revenue Forecast, Company Ranking, Competitive Landscape, Growth Factors, and Trends |

| Top Companies |

|

| Growth Driver |

|

| Segments Covered | • By Cryocooler Type: Gifford-McMahon Cryocoolers, Pulse Tube Cryocoolers, Stirling Cryocoolers, Joule–Thomson Cryocoolers, and Brayton Cryocoolers • By Offering: Hardware and Services • By Heat Exchanger Type: Recuperative Heat Exchanger and Regenerative |

| Regional Scope | North America, Europe, Asia Pacific, and RoW |

CRYOCOOLER Market Size & Forecast

• 2025 Market Size: USD 3.48 Billion

• 2030 Projected Market Size: USD 4.90 Billion

• CAGR (2025-2030): 7.1%

• Military Applications Segments: Hold largest share

• North America: estimated share of 35.4%

KEY TAKEAWAYS

- By region, North America is estimated to dominate the cryocooler market with a share of 35.4% in 2024.

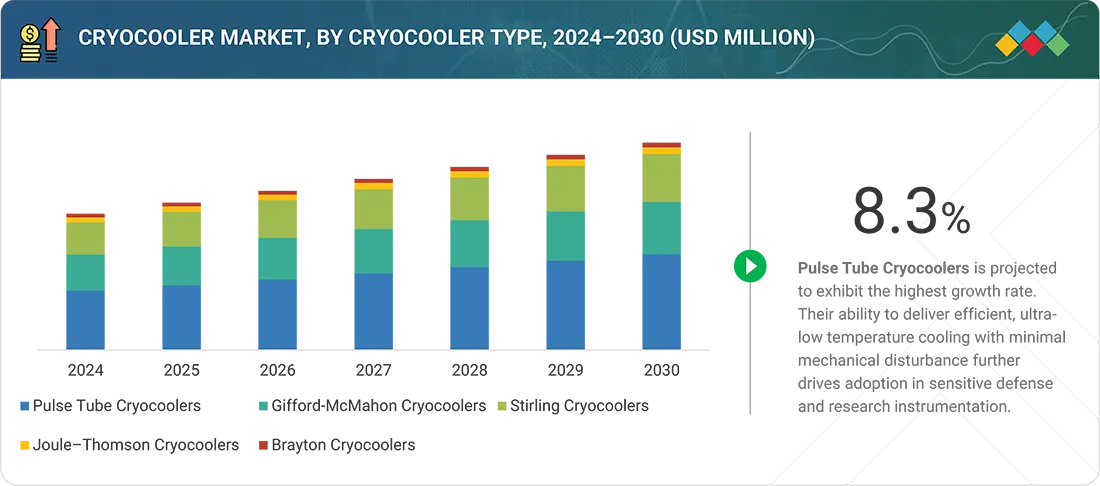

- By cryocooler type, the pulse tube cryocooler segment is projected to grow at the highest CAGR of 8.3% during the forecast period.

- By offering, the hardware segment is accounted for a share of 84% in 2024.

- By heat exchnager type, regenerative heat exchanger segment is estimated to dominate the cryocooler market with a share of 93.6% in 2024.

- By operating cycle, the closed-loop cycle segment is projected to grow at the highest CAGR o f7.5% during the forecast period.

- By temperature range, the 50K - 150K segment is accounted for a share of 55% in 2024.

- By application, the space segment is projected to grow at the highest CAGR of 10% during the forecast period.

- Thales (France), Northrop Grumman (US), AMETEK.Inc. (US) were identified as star players in the crycocooler market, given their strong global brand presence, extensive product portfolios, and continuous focus on innovation. Creare and Fabrum have emerged as the startups and SMEs driving technological innovation and market agility in the crycocooler market.

The cryocooler market is projected to expand significantly in the coming years, driven by the accelerating demand in the aerospace & defense space, which is catalyzing sustained cryocooler adoption, the rapid expansion of quantum computing, which is creating the need for advanced low-temperature thermal management solutions, and the transformation of the healthcare sector, which is fueling the adoption of helium-free MRI systems across global institutions. In addition, the strong focus on space exploration and satellite deployment, along with the rising importance of cryogenic cooling in superconducting technologies, is expected to create growth opportunities. Continuous technological advancements aimed at improving energy efficiency and reducing operational costs further strengthen the market adoption.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

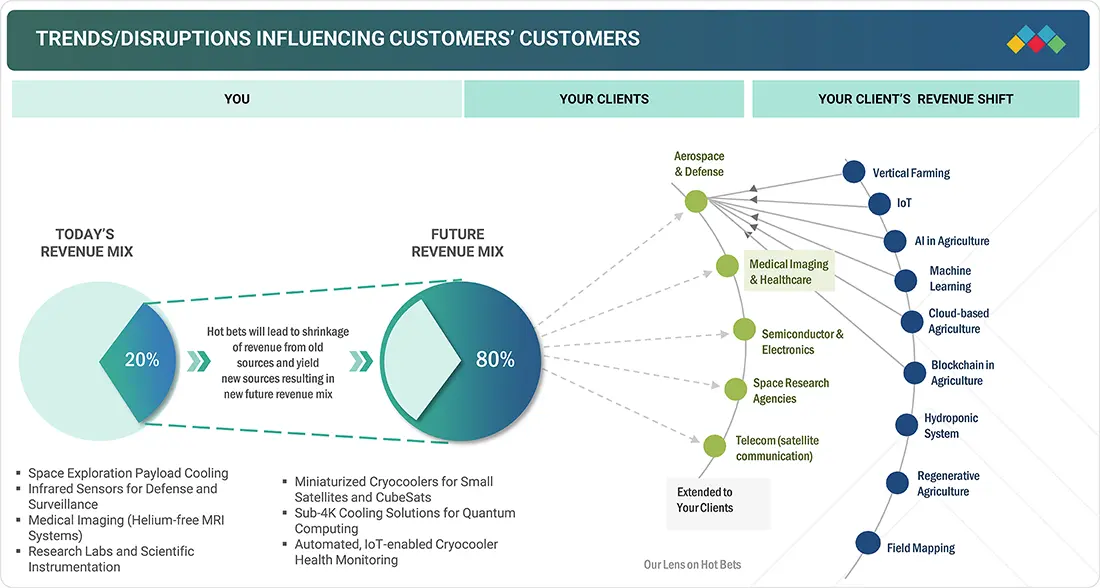

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

This section outlines the key trends and disruptions shaping customer operations in the cryocooler market. The growing demand for advanced cooling technologies in quantum computing, space exploration, and semiconductor manufacturing is expected to create strong growth opportunities for cryocooler manufacturers over the forecast period. Increasing investments in quantum computing infrastructure and the commercialization of large-scale quantum processors augment the need for ultra-low-temperature cryogenic systems. Additionally, the cryocooler market is witnessing expanded adoption in aerospace, defense, and satellite communication, where miniaturized cryocoolers enable enhanced infrared imaging, navigation, and surveillance capabilities. In the medical sector, the shift toward helium-free MRI systems and cryogenic solutions for advanced diagnostics reduces operational costs while improving energy efficiency. Cryocoolers are also becoming essential for supporting emerging applications, such as superconducting electronics, particle physics research, and hydrogen energy storage, reflecting their versatility across industries. As cryogenic R&D accelerates and IoT-enabled predictive maintenance technologies improve system performance, cryocooler suppliers will have increasing opportunities to expand their presence in high-tech and commercial markets globally.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

CRYOCOOLER MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Accelerating cryocooler demand from aerospace & defense and healthcare sectors

-

Surging adoption of quantum computing technology

RESTRAINTS

Impact

Level

Level

-

Low adoption in cost-sensitive markets due to high upfront costs and extended payback

-

Maintenance-driven expenditure and workforce skill gaps

OPPORTUNITIES

Impact

Level

Level

-

Emergence of sub-4K pre-coolers tailored for quantum data centers

-

Commercialization of small satellites

CHALLENGES

Impact

Level

Level

-

Limited thermal tolerance and reliability issues in high-density cryocooler arrays

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Accelerating cryocooler demand from aerospace & defense and healthcare sectors

Growing requirements for low-temperature applications in aerospace, defense, and healthcare fuel cryocooler demand. Increasing adoption in quantum computing, superconducting technologies, and medical imaging systems reinforces the need for reliable, compact, and energy-efficient cryocoolers across critical industries.

Restraint: High capital intensity constrains scalability across cost-sensitive customer segments

Despite ongoing innovation, high initial investment and complex integration requirements remain key barriers. Cost-sensitive customers, especially in emerging regions, face slower adoption due to limited subsidies or financing mechanisms. Performance constraints in thermal management, vibration control, and device longevity also restrict deployment in certain industrial and commercial applications.

Opportunity: Quantum computing scale-up driving sub-4K pre-cooler demand surges

The rapid scale-up of quantum computing boosts the demand for sub-4K cryocoolers. Increasing investments in quantum hardware require reliable low-temperature pre-cooling solutions. Growth in research labs and commercial quantum centers globally drives the adoption. Advancements in cryocooler efficiency further accelerate market uptake.

Challenge: Geopolitical risks destabilize specialized component sourcing across the critical region

Geopolitical tensions are disrupting the supply of specialized cryocooler components. Critical regions face export restrictions and supply chain uncertainties. Dependence on limited high-tech suppliers increases vulnerability. These factors can delay production and elevate costs, restraining market growth.

Cryocooler Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Deployed long-life cryocoolers on space telescopes and satellite instruments to achieve deep cryogenic cooling of infrared sensors | Enabled ultra-sensitive IR imaging | Reduced dependency on expendable cryogens | Extended mission lifetimes | Ensured reliable performance in harsh space environments |

|

Implemented sorption and mechanical cryocoolers in missions such as Herschel and Planck for sub-Kelvin detector cooling | Delivered stable low-temperature environments for astrophysics instruments | Improved measurement precision | Increased observational sensitivity | Supported multi-year mission operations |

|

Integrated cryogen-free cryocooler systems to maintain dilution refrigerators for quantum computing platforms | Provided continuous ultra-low temperature operation without liquid helium | Improved uptime and scalability of quantum processors | Reduced operating costs for superconducting qubit research |

|

Utilized miniature Stirling cryocoolers in cooled infrared imaging systems for defense, aerospace, and industrial monitoring | Achieved superior thermal sensitivity | Extended detection range | Enhanced image quality in challenging conditions | Improved reliability with compact, rugged cooling units |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

CRYOCOOLER MARKET ECOSYSTEM

The cryocooler market operates within a highly specialized and interconnected ecosystem that includes a range of stakeholders spanning multiple industries. From cryogenic component manufacturers, refrigeration system integrators, and material suppliers to software developers, automation solution providers, and service organizations, every participant plays a key role in advancing cryocooler design, deployment, and lifecycle management. This ecosystem also integrates research institutes, aerospace and defense contractors, semiconductor manufacturers, and healthcare providers, reflecting the technology’s cross-industry relevance. With rising demand for compact, energy-efficient, and high-reliability cooling systems across applications such as quantum computing, satellite payload cooling, superconducting systems, and advanced medical imaging, the ecosystem is rapidly evolving. Companies are increasingly incorporating AI-based performance monitoring, predictive maintenance platforms, and advanced simulation tools to optimize cryocooler performance and reliability. The market further involves collaborations between aerospace and defense firms, robotics and automation specialists, and niche cryogenic research service providers. This interconnected landscape emphasizes cross-domain synergies that drive innovation, reduce system complexity, and improve operational efficiency. By leveraging advancements in materials science, manufacturing precision, and smart diagnostics, stakeholders are creating a more resilient, scalable, and sustainable cryocooling infrastructure to meet future demands in space exploration, energy research, and healthcare innovation.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

CRYOCOOLER MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Cryocooler Market, By Cryocooler Type

The pulse tube cryocoolers segment accounted for a significant share in 2024. Its growth is due to the adoption in space research, medical imaging, and defense systems due to their vibration-free operation, high reliability, and long operational life. Their ability to deliver stable cooling without moving parts makes them especially suitable for sensitive instruments, ensuring lower maintenance costs and enhanced performance.

Cryocooler Market, By Offering

In 2024, hardware offering accounted for the largest share of the global market. These systems provide a balance of performance and cost, making them ideal for applications such as satellite instruments, medical diagnostics, defense technologies, and sensitive electronics cooling, with their adaptability ensuring sustained demand across industries.

Cryocooler Market, By Heat Exchanger Type

The regenerative heat exchanger segment held the largest share in 2024, driven by broad adoption in aerospace, healthcare, and research applications. Regenerative heat exchangers enable faster cooling, lower energy use, and improved reliability compared with conventional technologies, making them vital in advanced operational environments.

Cryocooler Market, By Operating Cycle

The closed-loop cycle segment captured the largest market share in 2024, backed by strong demand from aerospace, defense, and electronics industries. Closed-loop cryocoolers are favored for their energy efficiency, compact design, and seamless integration into automated systems, helping reduce costs while boosting output.

Cryocooler Market, By Temperature Range

The market for >50–150 K segment is capturing largest share in 2024. High demand from medical imaging, space exploration, and defense applications is driving adoption in the >50–150 K range, where cryocoolers deliver efficiency, compact sizing, and compatibility with automated systems translating to cost benefits and higher performance.

Cryocooler Market, By Application

The market for military segment held the largest share in 2024. In the military sector, cryocoolers are increasingly adopted for their efficiency, reliability, and ability to support mission-critical systems such as infrared sensors, satellite payloads, and surveillance equipment, enabling enhanced performance and cost-effective operation.

REGION

Asia Pacific to be fastest-growing region in global cryocooler market during forecast period

Asia Pacific is projected to capture the largest market share of the cryocooler industry in 2030. The regional growth is due to the rapid industrialization, growing aerospace and defense programs, rising demand in healthcare, and increasing investment in advanced research infrastructure. Additionally, government initiatives, such as India’s defense offset policies promoting local production of Stirling cryocoolers, and Japan’s AIST collaboration with Bluefors to co-develop advanced cryogenic refrigerators, accelerate innovation and regional self-reliance.

Cryocooler Market: COMPANY EVALUATION MATRIX

In the cryocooler companies matrix, Sumitomo Heavy Industries, Ltd. (Star) leads with a strong market presence and a broad portfolio serving applications in medical imaging, space research, and defense systems. The company drives large-scale adoption through continuous innovation, global partnerships, and extensive distribution networks. Air Liquide Advanced Technologies(Emerging Leader) is steadily strengthening its position by expanding offerings for industrial and research applications.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

WHAT IS IN IT FOR YOU: Cryocooler Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Aerospace & Defense Contractor | • Competitive benchmarking of cryocooler technologies (Stirling, Pulse Tube, Gifford-McMahon, and JT) • Mapping suppliers by defense-grade certifications • Lifecycle cost and | • Identify most cost-effective and reliable solutions for mission-critical payloads • Shortlist suppliers for long-term defense contracts • Support technology selection for satellite & infrared systems |

| Medical Imaging OEM (MRI Manufacturer) | • End-use adoption trends of cryocoolers in MRI • Evaluation of oil-free vs. conventional systems • Market sizing of helium-free cryocoolers | • Support strategic transition to helium-free systems • Enable competitive positioning vs. incumbents • Highlight growth opportunities in high-demand MRI markets |

| Cryocooler Component Supplier | • Supply chain mapping for compressors, heat exchangers, and cold heads • Cost–benefit analysis of localized vs. imported sourcing • Partnership and distribution network analysis | • Pinpoint niche opportunities for component supply • Build regional presence via strategic alliances • Optimize sourcing strategies to reduce costs |

| Energy & Industrial Gas Company | • Cryocooler adoption roadmap in LNG, hydrogen, and superconductivity applications • Technical feasibility study for large-scale deployments • ROI benchmarking across industrial verticals | • Support investment in emerging cryogenic applications • Enable diversification into clean energy and superconductivity markets • Identify high-growth regional demand pockets |

| Research Institution / University Lab | • Database of cryocooler suppliers offering R&D-grade units • Comparative performance analysis (cooling power, base temperature, vibration levels) • Funding & grant opportunity mapping | • Provide clarity for equipment procurement • Optimize R&D budgets with supplier benchmarking • Unlock collaboration opportunities in government-funded projects |

RECENT DEVELOPMENTS

- June 2025 : Sumitomo Heavy Industries released its highest-capacity single-stage cryocoolers, CH-160D3LT and CH-160D3 Series. These cryocoolers utilize Whisper technology for quieter operation and a Displex pneumatic drive system, which minimizes moving parts and wear

- March 2025 : Bluefors launched the PT205, a compact, high-performance two-stage pulse tube cryocooler designed specifically for advanced scientific applications and superconducting technologies like superconducting nanowire single-photon detectors.

- January 2024 : Sumitomo Heavy Industries launched the RJT-100 4K GM-JT Cryocooler, the highest-capacity 4 K cryocooler, delivering up to 9.0 W at 4.2 K (50/60 Hz). Its innovative hybrid design combines a Joule-Thomson cryocooler with a two-stage Gifford-McMahon cryocooler for pre-cooling helium gas, providing superior efficiency, temperature stability, and reduced maintenance needs compared to standard 4 K cryocoolers

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

26

2

RESEARCH METHODOLOGY

32

3

EXECUTIVE SUMMARY

44

4

PREMIUM INSIGHTS

50

5

MARKET OVERVIEW

Surging cryocooler demand driven by aerospace, quantum computing, and helium-free MRI innovations.

54

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

Accelerating cryocooler demand from aerospace & defense sector

5.2.1.2

Surging adoption of quantum computing technology

5.2.1.3

Escalating demand for helium-free MRI systems by healthcare providers

5.2.2

RESTRAINTS

5.2.2.1

Low adoption in cost-sensitive markets due to high upfront costs and extended payback

5.2.2.2

Maintenance-driven expenditure and workforce skill gaps

5.2.3

OPPORTUNITIES

5.2.3.1

Emergence of sub-4K pre-coolers tailored for quantum data centers

5.2.3.2

Commercialization of small satellites

5.2.4

CHALLENGES

5.2.4.1

Geopolitical risks impacting specialized component sourcing

5.2.4.2

Commercial-scale expansion barriers due to performance-cost trade-offs

5.3

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4

PRICING ANALYSIS

5.4.1

PRICING RANGE OF CRYOCOOLERS, BY KEY PLAYER, 2024

5.4.2

AVERAGE SELLING PRICE TREND OF CRYOCOOLERS, BY REGION, 2021–2024

5.5

VALUE CHAIN ANALYSIS

5.6

ECOSYSTEM ANALYSIS

5.7

TECHNOLOGY ANALYSIS

5.7.1

KEY TECHNOLOGIES

5.7.1.1

Pulse tube cryocoolers

5.7.1.2

Stirling cryocoolers

5.7.2

COMPLEMENTARY TECHNOLOGIES

5.7.2.1

Thermal management & insulation

5.7.2.2

Cryogenic sensors & instrumentation

5.7.3

ADJACENT TECHNOLOGIES

5.7.3.1

Thermoelectric coolers (Peltier devices)

5.7.3.2

Quantum technologies

5.8

PATENT ANALYSIS

5.9

TRADE ANALYSIS

5.9.1

IMPORT SCENARIO (HS CODE 8418)

5.9.2

EXPORT SCENARIO (HS CODE 8418)

5.10

KEY CONFERENCES AND EVENTS, 2025–2026

5.11

CASE STUDY ANALYSIS

5.11.1

SHI’S HIGH-CAPACITY 4 KGM-JT RJT-100 CRYOCOOLER SYSTEM FOR INDUSTRIAL SRF ACCELERATORS

5.11.2

CRYOR’S FLEXIBLE AND ADAPTABLE CRYOCOOLER SOLUTION FOR RESEARCH LABORATORIES

5.11.3

CREARE’S MECHANICAL CRYOCOOLER FOR NICMOS INFRARED VISION RECOVERY ON HUBBLE SPACE TELESCOPE

5.11.4

BLUEFOR’ PT450 PULSE TUBE CRYOCOOLER MEETING PERFORMANCE AND ENERGY EFFICIENCY GOALS

5.12

INVESTMENT AND FUNDING SCENARIO

5.13

REGULATORY LANDSCAPE

5.13.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.13.2

KEY REGULATIONS

5.14

PORTER’S FIVE FORCES ANALYSIS

5.14.1

INTENSITY OF COMPETITIVE RIVALRY

5.14.2

THREAT OF SUBSTITUTES

5.14.3

BARGAINING POWER OF BUYERS

5.14.4

BARGAINING POWER OF SUPPLIERS

5.14.5

THREAT OF NEW ENTRANTS

5.15

KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2

BUYING CRITERIA

5.16

IMPACT OF GEN AI/AI ON CRYOCOOLER MARKET

5.17

2025 US TARIFF IMPACT ON CRYOCOOLER MARKET

5.17.1

INTRODUCTION

5.17.2

KEY TARIFF RATES

5.17.3

PRICE IMPACT ANALYSIS

5.17.4

IMPACT ON COUNTRIES/REGIONS

5.17.4.1

US

5.17.4.2

Europe

5.17.4.3

Asia Pacific

5.17.5

IMPACT ON APPLICATIONS

6

CRYOCOOLER MARKET, BY OFFERING

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 8 Data Tables

92

6.1

INTRODUCTION

6.2

HARDWARE

6.2.1

COMPRESSOR

6.2.1.1

Ability to minimize vibration and acoustic interference in sensitive systems to accelerate demand

6.2.2

COLD HEAD

6.2.2.1

Extended maintenance-free operation to boost demand

6.2.3

HEAT DISSIPATION PIPE

6.2.3.1

Rising use of additive manufacturing to fabricate complex heat pipe geometries to fuel segmental growth

6.2.4

POWER CONDITIONING UNIT

6.2.4.1

Ability to withstand radiation and voltage fluctuations to propel market

6.2.5

OTHER HARDWARE TYPES

6.3

SERVICES

6.3.1

TECHNICAL SUPPORT

6.3.1.1

Need for on-demand expertise to ensure operational continuity to push segmental growth

6.3.2

PRODUCT REPAIR & REFURBISHMENT

6.3.2.1

Rising focus on extending product lifecycle and maximizing ROI to boost demand

6.3.3

PREVENTIVE MAINTENANCE

6.3.3.1

Significant focus on reducing downtime and avoiding costly system failures to surge demand

6.3.4

CUSTOMER TRAINING

6.3.4.1

Requirement to keep customers updated with latest operational practices to spike demand

7

CRYOCOOLER MARKET, BY HEAT EXCHANGER TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

102

7.1

INTRODUCTION

7.2

RECUPERATIVE HEAT EXCHANGER

7.2.1

INCREASING CRYOGENIC ADOPTION IN SPACE PROGRAMS TO SUPPORT SEGMENTAL GROWTH

7.3

REGENERATIVE HEAT EXCHANGER

7.3.1

SUPERIOR THERMAL STABILITY AND BETTER UNIFORMITY TO BOOST DEMAND

8

CRYOCOOLER MARKET, BY OPERATING CYCLE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

106

8.1

INTRODUCTION

8.2

OPEN-LOOP CYCLE

8.2.1

EXCELLENCE IN HANDLING HIGH THROUGHPUT AND ADAPTING TO VARYING PROCESS REQUIREMENTS TO SPIKE DEMAND

8.3

CLOSED-LOOP CYCLE

8.3.1

REDUCED VIBRATION, LOWER MAINTENANCE, AND HIGHER RELIABILITY THAN OPEN-LOOP SYSTEMS TO ACCELERATE ADOPTION

9

CRYOCOOLER MARKET, BY CRYOCOOLER TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 52 Data Tables

111

9.1

INTRODUCTION

9.2

GIFFORD–MCMAHON CRYOCOOLERS

9.2.1

SUITABILITY FOR APPLICATIONS REQUIRING CONTINUOUS AND STABLE COOLING TO BOOST DEMAND

9.3

PULSE TUBE CRYOCOOLERS

9.3.1

ABILITY TO DELIVER VIBRATION-FREE, MAINTENANCE-FREE, AND SPACE-COMPATIBLE COOLING SOLUTIONS TO INCREASE DEMAND

9.4

STIRLING CRYOCOOLERS

9.4.1

RISING USE IN SPACE APPLICATIONS TO DRIVE MARKET

9.5

JOULE–THOMSON CRYOCOOLERS

9.5.1

WIDESPREAD USE IN GAS LIQUEFACTION, CRYOGENIC RESEARCH, AND MEDICAL IMAGING TO PROPEL MARKET

9.6

BRAYTON CRYOCOOLERS

9.6.1

INCREASING DEMAND IN AEROSPACE, DEFENSE, AND HIGH-POWER INDUSTRIAL APPLICATIONS TO FOSTER MARKET GROWTH

10

CRYOCOOLER MARKET, BY TEMPERATURE RANGE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 2 Data Tables

136

10.1

INTRODUCTION

10.2

1–50 K

10.2.1

RISING USE IN ULTRA-LOW-NOISE DETECTION AND QUANTUM COMPUTING APPLICATIONS TO FACILITATE SEGMENTAL GROWTH

10.3

>50–150 K

10.3.1

ELEVATING DEMAND FOR FIELD-DEPLOYABLE DEFENSE SYSTEMS TO ACCELERATE SEGMENTAL GROWTH

10.4

ABOVE 150 K

10.4.1

ESCALATING USE IN INDUSTRIAL LIQUEFACTION AND HIGH-TEMPERATURE SUPERCONDUCTING APPLICATIONS TO BOOST SEGMENTAL GROWTH

11

CRYOCOOLER MARKET, BY APPLICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 24 Data Tables

140

11.1

INTRODUCTION

11.2

MILITARY

11.2.1

ESCALATING USE OF UAVS AND DRONES IN BATTLEFIELD SURVEILLANCE TO DRIVE MARKET

11.2.2

IR SENSORS FOR MISSILE GUIDANCE

11.2.3

IR SENSORS FOR SATELLITE-BASED SURVEILLANCE

11.3

MEDICAL

11.3.1

PRESSING NEED TO REDUCE DOWNTIME IN CRITICAL HEALTHCARE INFRASTRUCTURE TO CONTRIBUTE TO MARKET GROWTH

11.3.2

MRI SYSTEMS

11.3.3

LIQUEFACTION OF OXYGEN FOR STORAGE

11.3.4

CRYOSURGERY AND PROTON THERAPY

11.4

COMMERCIAL

11.4.1

EXPANSION OF INDUSTRIAL-SCALE GAS LIQUEFACTION PLANTS TO FACILITATE DEMAND

11.4.2

SEMICONDUCTOR FABRICATION

11.4.3

HIGH-TEMPERATURE SUPERCONDUCTORS FOR CELL PHONE BASE STATIONS

11.4.4

IR SENSORS FOR NDE AND PROCESS MONITORING

11.5

ENVIRONMENTAL

11.5.1

RISING FOCUS ON TRACKING POLLUTION SOURCES AND IMPROVING URBAN AIR QUALITY TO SUPPORT MARKET GROWTH

11.5.2

IR SENSORS FOR ATMOSPHERIC STUDIES ON OZONE HOLE AND GREENHOUSE EFFECT

11.5.3

IR SENSORS FOR POLLUTION MONITORING

11.6

ENERGY

11.6.1

GREATER EMPHASIS ON REDUCING ENERGY LOSSES DURING TRANSMISSION TO FOSTER MARKET GROWTH

11.6.2

IR SENSORS FOR THERMAL LOSS MEASUREMENTS

11.6.3

SUPERCONDUCTING MAGNETIC ENERGY STORAGE FOR PEAK SHAVING

11.7

TRANSPORT

11.7.1

ELEVATING DEMAND FOR HYDROGEN-POWERED SHIPS AND SUBMARINES TO CREATE GROWTH OPPORTUNITIES

11.7.2

SUPERCONDUCTING MAGNETS IN MAGLEV TRAINS

11.7.3

LNG FOR FLEET VEHICLES

11.8

RESEARCH & DEVELOPMENT

11.8.1

RAPID INNOVATIONS IN SENSORS, NANOTECHNOLOGY, AND SUPERCONDUCTING ELECTRONICS TO PROMOTE MARKET GROWTH

11.8.2

NUCLEAR MAGNETIC RESONANCE

11.8.3

ELECTRON PARAMAGNETIC RESONANCE

11.9

SPACE

11.9.1

EARTH OBSERVATION, ASTROPHYSICS, AND DEEP-SPACE EXPLORATION MISSIONS TO SPUR DEMAND

11.9.2

SPACE ASTRONOMY

11.9.3

PLANETARY SCIENCE

11.10

AGRICULTURE & BIOLOGY

11.10.1

REQUIREMENT TO PRESERVE SEEDS, GENETIC MATERIALS, AND BIOLOGICAL SAMPLES TO ENCOURAGE ADOPTION

11.10.2

STORAGE OF BIOLOGICAL CELLS AND SPECIMENS

11.11

MINING & METAL

11.11.1

LEVERAGING CRYOCOOLERS TO ENHANCE CORROSION RESISTANCE AND WEAR PERFORMANCE

11.11.2

METAL TEMPERING

11.11.3

SHRINK FITTING

11.12

OTHER APPLICATIONS

12

CRYOCOOLER MARKET, BY REGION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 80 Data Tables

161

12.1

INTRODUCTION

12.2

NORTH AMERICA

12.2.1

MACROECONOMIC OUTLOOK FOR NORTH AMERICA

12.2.2

US

12.2.2.1

Well-established military industry and high expenditure on healthcare equipment to drive market

12.2.3

CANADA

12.2.3.1

Growing medical and healthcare expenditure to spur demand

12.2.4

MEXICO

12.2.4.1

Emerging industrial applications to drive demand

12.3

EUROPE

12.3.1

MACROECONOMIC OUTLOOK FOR EUROPE

12.3.2

GERMANY

12.3.2.1

Thriving healthcare sector and government support for cryogenic research to foster market growth

12.3.3

UK

12.3.3.1

Government efforts toward defense system enhancement to fuel market growth

12.3.4

FRANCE

12.3.4.1

Emphasis on innovation and technological advancement to facilitate market growth

12.3.5

ITALY

12.3.5.1

Rising use of cryogenic technology in MRI and cancer treatment applications to support market growth

12.3.6

NETHERLANDS

12.3.6.1

Partnerships between cryogenic technology providers and research institutions to expedite market growth

12.3.7

POLAND

12.3.7.1

Surging deployment of cooling systems in electronic devices and automotive systems to accelerate market growth

12.3.8

NORDICS

12.3.8.1

Significant focus on sustainability and cryogenic research synergies to propel market

12.3.9

REST OF EUROPE

12.4

ASIA PACIFIC

12.4.1

MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

12.4.2

JAPAN

12.4.2.1

Surging demand from universities, national laboratories, and research centers to develop innovative products to drive market

12.4.3

CHINA

12.4.3.1

Adoption of clean energy objectives to promote demand for cooling systems

12.4.4

SOUTH KOREA

12.4.4.1

Escalating demand for cryopumps from semiconductor manufacturers to fuel market growth

12.4.5

INDIA

12.4.5.1

Booming healthcare industry to intensify demand

12.4.6

AUSTRALIA

12.4.6.1

Healthcare, space, and defense verticals to contribute most to market growth

12.4.7

INDONESIA

12.4.7.1

Introduction of I-NCAP plan to ensure sustainable cooling practices to stimulate demand

12.4.8

MALAYSIA

12.4.8.1

Rising focus on adopting energy-efficient cooling and modernizing air conditioning standards to spike demand

12.4.9

THAILAND

12.4.9.1

Heightened demand for high-performance cryogenic systems across industrial and healthcare sectors to propel market

12.4.10

VIETNAM

12.4.10.1

Expansion of digital infrastructure due to rapid industrialization to create growth opportunities

12.4.11

REST OF ASIA PACIFIC

12.5

ROW

12.5.1

MACROECONOMIC OUTLOOK FOR ROW

12.5.2

MIDDLE EAST

12.5.2.1

Bahrain

12.5.2.2

Kuwait

12.5.2.3

Oman

12.5.2.4

Qatar

12.5.2.5

Saudi Arabia

12.5.2.6

UAE

12.5.2.7

Rest of Middle East

12.5.3

AFRICA

12.5.3.1

South Africa

12.5.3.2

Other African countries

12.5.4

SOUTH AMERICA

12.5.4.1

Brazil

12.5.4.2

Argentina

12.5.4.3

Rest of South America

13

COMPETITIVE LANDSCAPE

Discover top strategies and market dominance of key players and emerging leaders.

209

13.1

OVERVIEW

13.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021–2025

13.3

MARKET SHARE ANALYSIS, 2024

13.4

REVENUE ANALYSIS, 2021–2024

13.5

COMPANY VALUATION AND FINANCIAL METRICS

13.6

BRAND COMPARISON

13.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

13.7.1

STARS

13.7.2

EMERGING LEADERS

13.7.3

PERVASIVE PLAYERS

13.7.4

PARTICIPANTS

13.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

13.7.5.1

Company footprint

13.7.5.2

Region footprint

13.7.5.3

Cryocooler type footprint

13.7.5.4

Temperature range footprint

13.7.5.5

Application footprint

13.8

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

13.8.1

PROGRESSIVE COMPANIES

13.8.2

RESPONSIVE COMPANIES

13.8.3

DYNAMIC COMPANIES

13.8.4

STARTING BLOCKS

13.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

13.8.5.1

Detailed list of key startups/SMEs

13.8.5.2

Competitive benchmarking of key startups/SMEs

13.9

COMPETITIVE SCENARIO

13.9.1

PRODUCT LAUNCHES

13.9.2

DEALS

14

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

224

14.1

KEY PLAYERS

14.1.1

SUMITOMO HEAVY INDUSTRIES, LTD.

14.1.1.1

Business overview

14.1.1.2

Products/Solutions/Services offered

14.1.1.3

Recent developments

14.1.1.4

MnM view

14.1.2

THALES

14.1.3

EDWARDS VACUUM (ATLAS COPCO GROUP)

14.1.4

AMETEK.INC.

14.1.5

CHART INDUSTRIES, INC.

14.1.6

BLUEFORS

14.1.7

NORTHROP GRUMMAN

14.1.8

ADVANCED RESEARCH SYSTEMS

14.1.9

RICOR

14.1.10

AIR LIQUIDE ADVANCED TECHNOLOGIES

14.2

OTHER PLAYERS

14.2.1

LAKE SHORE CRYOTRONICS

14.2.2

CREARE

14.2.3

LIHAN CRYOGENICS CO., LTD.

14.2.4

TRISTAN TECHNOLOGIES, INC.

14.2.5

VACREE TECHNOLOGIES CO., LTD.

14.2.6

HONEYWELL INTERNATIONAL INC.

14.2.7

BRIGHT INSTRUMENT CO. LTD.

14.2.8

ABSOLUT SYSTEM

14.2.9

FABRUM

14.2.10

CRYOSPECTRA GMBH

14.2.11

ULVAC CRYOGENICS INC.

14.2.12

OXFORD CRYOSYSTEMS LTD.

14.2.13

HYCON LTD.

14.2.14

RIX INDUSTRIES

14.2.15

AIM INFRAROT-MODULE GMBH

15

APPENDIX

258

15.1

INSIGHTS FROM INDUSTRY EXPERTS

15.2

DISCUSSION GUIDE

15.3

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

15.4

CUSTOMIZATION OPTIONS

15.5

RELATED REPORTS

15.6

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

CRYOCOOLER MARKET: INCLUSIONS AND EXCLUSIONS

TABLE 2

LIST OF SECONDARY SOURCES

TABLE 3

INTENDED PARTICIPANTS AND MAJOR OPINION LEADERS

TABLE 4

CRYOCOOLER MARKET: RISK ANALYSIS

TABLE 5

PRICING RANGE OF CRYOCOOLERS PROVIDED BY KEY PLAYERS, 2024 (USD)

TABLE 6

AVERAGE SELLING PRICE TREND OF CRYOCOOLERS, BY REGION, 2021–2024 (USD)

TABLE 7

ROLE OF KEY PLAYERS IN ECOSYSTEM

TABLE 8

LIST OF MAJOR PATENTS, 2022–2024

TABLE 9

IMPORT DATA FOR HS CODE 8418-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 10

EXPORT DATA FOR HS CODE 8418-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 11

MAJOR CONFERENCES AND EVENTS RELATED TO CRYOCOOLERS IN DIFFERENT REGIONS, 2025–2026

TABLE 12

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 13

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 14

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 15

ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 16

CRYOCOOLER MARKET: REGULATORY LANDSCAPE

TABLE 17

CRYOCOOLER MARKET: IMPACT OF PORTER’S FIVE FORCES

TABLE 18

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR OFFERINGS

TABLE 19

KEY BUYING CRITERIA, BY APPLICATION

TABLE 20

US-ADJUSTED RECIPROCAL TARIFF RATES

TABLE 21

CRYOCOOLER MARKET, BY OFFERING, 2021–2024 (USD MILLION)

TABLE 22

CRYOCOOLER MARKET, BY OFFERING, 2025–2030 (USD MILLION)

TABLE 23

CRYOCOOLER MARKET, 2021–2024 (THOUSAND UNITS)

TABLE 24

CRYOCOOLER MARKET, 2025–2030 (THOUSAND UNITS)

TABLE 25

CRYOCOOLER MARKET, BY HARDWARE TYPE, 2021–2024 (USD MILLION)

TABLE 26

CRYOCOOLER MARKET, BY HARDWARE TYPE, 2025–2030 (USD MILLION)

TABLE 27

CRYOCOOLER MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 28

CRYOCOOLER MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 29

CRYOCOOLER MARKET, BY HEAT EXCHANGER TYPE, 2021–2024 (USD MILLION)

TABLE 30

CRYOCOOLER MARKET, BY HEAT EXCHANGER TYPE, 2025–2030 (USD MILLION)

TABLE 31

CRYOCOOLER MARKET, BY OPERATING CYCLE, 2021–2024 (USD MILLION)

TABLE 32

CRYOCOOLER MARKET, BY OPERATING CYCLE, 2025–2030 (USD MILLION)

TABLE 33

CRYOCOOLER MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 34

CRYOCOOLER MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 35

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 36

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 37

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 38

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 39

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 40

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 41

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 42

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 43

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2021–2024 (USD MILLION)

TABLE 44

GIFFORD–MCMAHON CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2025–2030 (USD MILLION)

TABLE 45

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 46

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 47

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 48

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 49

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 50

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 51

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 52

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 53

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2021–2024 (USD MILLION)

TABLE 54

PULSE TUBE CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2025–2030 (USD MILLION)

TABLE 55

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 56

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 57

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 58

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 59

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 60

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 61

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 62

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 63

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2021–2024 (USD MILLION)

TABLE 64

STIRLING CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2025–2030 (USD MILLION)

TABLE 65

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 66

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 67

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 68

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 69

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 70

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 71

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 72

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 73

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2021–2024 (USD MILLION)

TABLE 74

JOULE–THOMSON CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2025–2030 (USD MILLION)

TABLE 75

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 76

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 77

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 78

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET IN NORTH AMERICA, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 79

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 80

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET IN EUROPE, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 81

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 82

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 83

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2021–2024 (USD MILLION)

TABLE 84

BRAYTON CRYOCOOLERS: CRYOCOOLER MARKET IN ROW, BY REGION, 2025–2030 (USD MILLION)

TABLE 85

CRYOCOOLER MARKET, BY TEMPERATURE RANGE, 2021–2024 (USD MILLION)

TABLE 86

CRYOCOOLER MARKET, BY TEMPERATURE RANGE, 2025–2030 (USD MILLION)

TABLE 87

CRYOCOOLER MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 88

CRYOCOOLER MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 89

MILITARY: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 90

MILITARY: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 91

MEDICAL: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 92

MEDICAL: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 93

COMMERCIAL: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 94

COMMERCIAL: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 95

ENVIRONMENTAL: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 96

ENVIRONMENTAL: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 97

ENERGY: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 98

ENERGY: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 99

TRANSPORT: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 100

TRANSPORT: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 101

RESEARCH & DEVELOPMENT: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 102

RESEARCH & DEVELOPMENT: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 103

SPACE: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 104

SPACE: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 105

AGRICULTURE & BIOLOGY: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 106

AGRICULTURE & BIOLOGY: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 107

MINING & METAL: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 108

MINING & METAL: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 109

OTHER APPLICATIONS: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 110

OTHER APPLICATIONS: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 111

CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 112

CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 113

NORTH AMERICA: CRYOCOOLER MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 114

NORTH AMERICA: CRYOCOOLER MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 115

NORTH AMERICA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 116

NORTH AMERICA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 117

NORTH AMERICA: CRYOCOOLER MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 118

NORTH AMERICA: CRYOCOOLER MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 119

US: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 120

US: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 121

CANADA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 122

CANADA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 123

MEXICO: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 124

MEXICO: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 125

EUROPE: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 126

EUROPE: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 127

EUROPE: CRYOCOOLER MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 128

EUROPE: CRYOCOOLER MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 129

EUROPE: CRYOCOOLER MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 130

EUROPE: CRYOCOOLER MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 131

GERMANY: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 132

GERMANY: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 133

UK: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 134

UK: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 135

FRANCE: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 136

FRANCE: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 137

ITALY: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 138

ITALY: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 139

NETHERLANDS: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 140

NETHERLANDS: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 141

POLAND: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 142

POLAND: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 143

NORDICS: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 144

NORDICS: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 145

REST OF EUROPE: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 146

REST OF EUROPE: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 147

ASIA PACIFIC: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 148

ASIA PACIFIC: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 149

ASIA PACIFIC: CRYOCOOLER MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 150

ASIA PACIFIC: CRYOCOOLER MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 151

ASIA PACIFIC: CRYOCOOLER MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 152

ASIA PACIFIC: CRYOCOOLER MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 153

JAPAN: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 154

JAPAN: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 155

CHINA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 156

CHINA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 157

SOUTH KOREA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 158

SOUTH KOREA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 159

INDIA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 160

INDIA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 161

AUSTRALIA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 162

AUSTRALIA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 163

INDONESIA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 164

INDONESIA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 165

MALAYSIA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 166

MALAYSIA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 167

THAILAND: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 168

THAILAND: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 169

VIETNAM: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 170

VIETNAM: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 171

REST OF ASIA PACIFIC: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 172

REST OF ASIA PACIFIC: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 173

ROW: CRYOCOOLER MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 174

ROW: CRYOCOOLER MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 175

ROW: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 176

ROW: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 177

ROW: CRYOCOOLER MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 178

ROW: CRYOCOOLER MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 179

MIDDLE EAST: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 180

MIDDLE EAST: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 181

MIDDLE EAST: CRYOCOOLER MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 182

MIDDLE EAST: CRYOCOOLER MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 183

AFRICA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 184

AFRICA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 185

AFRICA: CRYOCOOLER MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 186

AFRICA: CRYOCOOLER MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 187

SOUTH AMERICA: CRYOCOOLER MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 188

SOUTH AMERICA: CRYOCOOLER MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 189

SOUTH AMERICA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2021–2024 (USD MILLION)

TABLE 190

SOUTH AMERICA: CRYOCOOLER MARKET, BY CRYOCOOLER TYPE, 2025–2030 (USD MILLION)

TABLE 191

CRYOCOOLER MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2020–2025

TABLE 192

CRYOCOOLER MARKET: DEGREE OF COMPETITION, 2024

TABLE 193

CRYOCOOLER MARKET: REGION FOOTPRINT

TABLE 194

CRYOCOOLER MARKET: CRYOCOOLER TYPE FOOTPRINT

TABLE 195

CRYOCOOLER MARKET: TEMPERATURE RANGE FOOTPRINT

TABLE 196

CRYOCOOLER MARKET: APPLICATION FOOTPRINT

TABLE 197

CRYOCOOLER MARKET: LIST OF KEY STARTUPS/SMES

TABLE 198

CRYOCOOLER MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 199

CRYOCOOLER MARKET: PRODUCT LAUNCHES, JUNE 2021–JULY 2025

TABLE 200

CRYOCOOLER MARKET: DEALS, JUNE 2021–JULY 2025

TABLE 201

SUMITOMO HEAVY INDUSTRIES, LTD.: COMPANY OVERVIEW

TABLE 202

SUMITOMO HEAVY INDUSTRIES, LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 203

SUMITOMO HEAVY INDUSTRIES, LTD.: PRODUCT LAUNCHES

TABLE 204

THALES: COMPANY OVERVIEW

TABLE 205

THALES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 206

EDWARDS VACUUM: COMPANY OVERVIEW

TABLE 207

EDWARDS VACUUM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 208

AMETEK.INC.: COMPANY OVERVIEW

TABLE 209

AMETEK.INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 210

CHART INDUSTRIES, INC.: COMPANY OVERVIEW

TABLE 211

CHART INDUSTRIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 212

BLUEFORS: COMPANY OVERVIEW

TABLE 213

BLUEFORS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 214

BLUEFORS: PRODUCT LAUNCHES

TABLE 215

BLUEFORS: DEALS

TABLE 216

BLUEFORS: EXPANSIONS

TABLE 217

NORTHROP GRUMMAN: COMPANY OVERVIEW

TABLE 218

NORTHROP GRUMMAN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 219

NORTHROP GRUMMAN: DEALS

TABLE 220

ADVANCED RESEARCH SYSTEMS: COMPANY OVERVIEW

TABLE 221

ADVANCED RESEARCH SYSTEMS: PRODUCTS/SERVICES/SOLUTIONS OFFERED

TABLE 222

RICOR: COMPANY OVERVIEW

TABLE 223

RICOR: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 224

AIR LIQUIDE ADVANCED TECHNOLOGIES: COMPANY OVERVIEW

TABLE 225

AIR LIQUIDE ADVANCED TECHNOLOGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

LIST OF FIGURES

FIGURE 1

CRYOCOOLER MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

DURATION CONSIDERED

FIGURE 3

CRYOCOOLER MARKET: RESEARCH DESIGN

FIGURE 4

CRYOCOOLER MARKET: RESEARCH APPROACH

FIGURE 5

KEY DATA SOURCED FROM SECONDARY LITERATURE

FIGURE 6

PRIMARY BREAKDOWN, BY COMPANY TYPE, DESIGNATION, AND REGION

FIGURE 7

DATA DERIVED FROM PRIMARY SOURCES

FIGURE 8

KEY INSIGHTS FROM INDUSTRY EXPERTS

FIGURE 9

REVENUE OF KEY PLAYERS VS. REVENUE OF OTHER PLAYERS

FIGURE 10

REGIONAL MARKET SIZE ESTIMATION, BY OFFERING

FIGURE 11

CRYOCOOLER MARKET: SUPPLY-SIDE ANALYSIS

FIGURE 12

CRYOCOOLER MARKET: BOTTOM-UP APPROACH

FIGURE 13

CRYOCOOLER MARKET: TOP-DOWN APPROACH

FIGURE 14

CRYOCOOLER MARKET: DATA TRIANGULATION

FIGURE 15

CRYOCOOLER MARKET, 2021–2030 (USD BILLION)

FIGURE 16

PULSE TUBE CRYOCOOLERS TO WITNESS HIGHEST CAGR IN CRYOCOOLER MARKET FROM 2025 TO 2030

FIGURE 17

REGENERATIVE HEAT EXCHANGER SEGMENT TO RECORD HIGHER CAGR IN CRYOCOOLER MARKET FROM 2025 TO 2030

FIGURE 18

SERVICES SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

FIGURE 19

SPACE APPLICATIONS TO RECORD HIGHEST CAGR IN CRYOCOOLER MARKET DURING FORECAST PERIOD

FIGURE 20

CLOSED-LOOP CYCLE SEGMENT TO RECORD HIGHER CAGR IN CRYOCOOLER MARKET DURING FORECAST PERIOD

FIGURE 21

1–50 K SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 22

ASIA PACIFIC TO BE FASTEST-GROWING MARKET FOR CRYOCOOLERS FROM 2025 TO 2030

FIGURE 23

QUANTUM COMPUTING EXPANSION NECESSITATING ADVANCED LOW-TEMPERATURE THERMAL MANAGEMENT SOLUTIONS TO DRIVE MARKET

FIGURE 24

CLOSED-LOOP CYCLE TO COMMAND CRYOCOOLER MARKET IN 2025

FIGURE 25

1–50 K SEGMENT TO REGISTER HIGHEST CAGR IN CRYOCOOLER MARKET DURING FORECAST PERIOD

FIGURE 26

POWER CONDITIONING UNIT SEGMENT TO RECORD HIGHEST CAGR IN CRYOCOOLER MARKET FOR HARDWARE OFFERINGS FROM 2025 TO 2030

FIGURE 27

CRYOCOOLER MARKET IN INDIA TO EXPAND AT HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 28

ASIA PACIFIC TO SECURE LARGEST SHARE OF CRYOCOOLER MARKET, IN TERMS OF VALUE, IN 2030

FIGURE 29

INDIA TO RECORD HIGHEST CAGR IN GLOBAL CRYOCOOLER MARKET DURING FORECAST PERIOD

FIGURE 30

CRYOCOOLER MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 31

DRIVERS: CRYOCOOLER MARKET

FIGURE 32

RESTRAINTS: CRYOCOOLER MARKET

FIGURE 33

OPPORTUNITIES: CRYOCOOLER MARKET

FIGURE 34

CHALLENGES: CRYOCOOLER MARKET

FIGURE 35

TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

FIGURE 36

AVERAGE SELLING PRICE TREND OF CRYOCOOLERS, BY REGION, 2021–2024

FIGURE 37

CRYOCOOLER VALUE CHAIN ANALYSIS

FIGURE 38

KEY PLAYERS IN CRYOCOOLER ECOSYSTEM

FIGURE 39

NUMBER OF PATENTS GRANTED FOR CRYOCOOLERS, 2015–2024

FIGURE 40

JURISDICTION-BASED ANALYSIS OF CRYOCOOLER-RELATED PATENTS, 2015–2024

FIGURE 41

IMPORT SCENARIO FOR HS CODE 8418-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2020–2024

FIGURE 42

EXPORT SCENARIO FOR HS CODE 8418-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2020–2024

FIGURE 43

INVESTMENT AND FUNDING SCENARIO, 2021–2024

FIGURE 44

CRYOCOOLER MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 45

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR OFFERINGS

FIGURE 46

KEY BUYING CRITERIA FOR OFFERINGS

FIGURE 47

IMPACT OF GEN AI/AI ON CRYOCOOLER MARKET

FIGURE 48

SERVICES SEGMENT TO EXHIBIT HIGHER CAGR THAN HARDWARE SEGMENT DURING FORECAST PERIOD

FIGURE 49

REGENERATIVE HEAT EXCHANGERS TO DOMINATE CRYOCOOLER MARKET FROM 2025 TO 2030

FIGURE 50

CLOSED-LOOP CYCLE SEGMENT TO LEAD CRYOCOOLER MARKET THROUGHOUT FORECAST PERIOD

FIGURE 51

PULSE TUBE CRYOCOOLERS TO HOLD LARGEST MARKET SHARE IN 2025

FIGURE 52

>50–150 K SEGMENT TO LEAD CRYOCOOLER MARKET IN 2030

FIGURE 53

MILITARY APPLICATIONS TO HOLD LARGEST SHARE OF CRYOCOOLER MARKET IN 2030

FIGURE 54

ASIA PACIFIC TO LEAD CRYOCOOLER MARKET IN 2030

FIGURE 55

SNAPSHOT OF CRYOCOOLER MARKET IN NORTH AMERICA

FIGURE 56

PULSE TUBE CRYOCOOLERS TO CAPTURE LARGEST MARKET SHARE OF NORTH AMERICAN MARKET IN 2030

FIGURE 57

SNAPSHOT OF CRYOCOOLER MARKET IN EUROPE

FIGURE 58

STIRLING CRYOCOOLERS TO EXHIBIT HIGHEST CAGR IN EUROPEAN MARKET DURING FORECAST PERIOD

FIGURE 59

SNAPSHOT OF CRYOCOOLER MARKET IN ASIA PACIFIC

FIGURE 60

PULSE TUBE CRYOCOOLERS TO SECURE LARGEST MARKET SHARE OF ASIA PACIFIC IN 2030

FIGURE 61

SNAPSHOT OF CRYOCOOLER MARKET IN ROW

FIGURE 62

PULSE TUBE CRYOCOOLERS TO SECURE LARGEST MARKET SHARE OF ROW REGION IN 2030

FIGURE 63

CRYOCOOLER MARKET SHARE ANALYSIS, 2024

FIGURE 64

REVENUE ANALYSIS OF FIVE KEY PLAYERS IN CRYOCOOLER MARKET, 2020–2024

FIGURE 65

COMPANY VALUATION

FIGURE 66

FINANCIAL METRICS (EV/EBITDA)

FIGURE 67

BRAND COMPARISON

FIGURE 68

CRYOCOOLER MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 69

CRYOCOOLER MARKET: COMPANY FOOTPRINT

FIGURE 70

CRYOCOOLER MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 71

SUMITOMO HEAVY INDUSTRIES, LTD.: COMPANY SNAPSHOT

FIGURE 72

THALES: COMPANY SNAPSHOT

FIGURE 73

AMETEK.INC.: COMPANY SNAPSHOT

FIGURE 74

CHART INDUSTRIES, INC.: COMPANY SNAPSHOT

FIGURE 75

NORTHROP GRUMMAN: COMPANY SNAPSHOT

Methodology

The research study involved four major activities in estimating the size of the cryocooler market. Exhaustive secondary research has been done to collect important information about the market and peer markets. The validation of these findings, assumptions, and sizing with the help of primary research with industry experts across the value chain has been the next step. Both top-down and bottom-up approaches have been used to estimate the market size. The market breakdown and data triangulation have been adopted to estimate the market sizes of segments and sub-segments.

Secondary Research

In the secondary research process, various secondary sources have been referred to for identifying and collecting information required for this study. The secondary sources include annual reports, press releases, investor presentations of companies, white papers, and articles from recognized authors. Secondary research has been mainly done to obtain key information about the market’s value chain, the pool of key market players, market segmentation according to industry trends, regional outlook, and developments from both market and technology perspectives.

In the cryocooler market report, the global market size has been estimated using both the top-down and bottom-up approaches, along with several other dependent submarkets. The major players in the market were identified using extensive secondary research, and their presence in the market was determined using secondary and primary research. All the percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources. .

Primary Research

Extensive primary research has been conducted after understanding the cryocooler market scenario through secondary research. Several primary interviews have been conducted with key opinion leaders from demand- and supply-side vendors across four major regions—North America, Europe, Asia Pacific, and the Rest of the World. Approximately 25% of the primary interviews have been conducted with the demand-side vendors and 75% with the supply-side vendors. Primary data has been collected mainly through telephonic interviews, which consist of 80% of the total primary interviews; questionnaires and emails have also been used to collect the data.

After successfully interacting with industry experts, brief sessions were conducted with highly experienced independent consultants to reinforce the findings of our primary research. This, along with the opinions of the in-house subject matter experts, has led us to the findings described in the report.

Note: “Others” includes sales, marketing, and product managers.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

In the market engineering process, both top-down and bottom-up approaches, along with data triangulation methods, have been used to estimate and validate the size of the cryocooler market and other dependent submarkets. The research methodology used to estimate the market sizes includes the following:

- Identifying the players in the cryocooler market, along with their offerings

- Analyzing each country, along with the presence of related major companies and system integrators in the countries, and identifying the service providers in the cryocooler market

- Identifying the market for each type of cryocooler (Gifford-McMahon Cryocoolers, Pulse-Tube Cryocoolers, Stirling Cryocoolers, Joule Thomson Cryocoolers, Brayton Cryocoolers) in each country and globally

- Identifying the major applications of cryocoolers, along with the types of cryocoolers required for various applications

- Estimating total cryocooler unit shipment globally by adding regional data (North America, Europe, Asia Pacific, and RoW)

- Estimating the weighted average cost of cryocoolers

- Verifying and cross-checking the estimates at every level by discussing with key opinion leaders, such as CXOs, directors, and operations managers, and finally with the domain experts in MarketsandMarkets

- Studying various paid and unpaid sources of information, such as annual reports, press releases, white papers, and databases

Cryocooler Market: Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall market size through the market size estimation process explained in the earlier section, the overall cryocooler market has been divided into several segments and subsegments. To complete the overall market engineering process and arrive at the exact statistics for all segments, the data triangulation and market breakdown procedures have been used, wherever applicable. The data has been triangulated by studying various factors and trends from both the demand and supply sides. Along with data triangulation and market breakdown, the market has been validated through the top-down and bottom-up approaches.

Market Definition

A cryocooler is a device that provides active cooling at cryogenic temperatures. According to the Cryogenic Society of America, a cryocooler is designed to allow active cooling at a temperature of about -150 degrees centigrade or lower. A cryocooler system uses the flow of gas inside the closed tube, which absorbs the heat and radiates it outside.

It is a mechanical device that generates low temperatures, similar to a domestic refrigerator. It consists of a compressor, a heat exchanger, an expansion device, and an evaporator. Cryocoolers help in mitigating the usage of cryogens such as liquid helium and liquid nitrogen and are capable of producing temperatures as low as 77 K or 4.2 K. Some of the basic features of a cryocooler include less weight, fast cool-down time, and vibration-less operation. The popular types of cryocoolers available worldwide include Stirling cryocoolers, Gifford McMahon (G-M) cryocoolers, Pulse Tube cryocoolers, Joule Thomson (J-T) cryocoolers, and Brayton cryocoolers.

Key Stakeholders

- End users of cryocoolers in various sectors such as military, medical, transport and logistics, energy, agriculture and biology, and environmental

- Hardware component (valves, compressors, cold heads, and power circuit boards for cryocoolers) manufacturers

- Service providers of cryocooler equipment manufacturers

- Research organizations and consulting companies

- Associations, organizations, forums, and alliances related to cryocoolers

- Government bodies, such as regulating authorities and policymakers

Report Objectives

- To describe and forecast the size of the cryocooler market by offering, cryocooler type, heat exchanger type, operating cycle, temperature range, application, and region, in terms of value

- To describe and forecast the market size of various segments across four key regions—North America, Europe, Asia Pacific, and Rest of the World (RoW), in terms of value

- To forecast the size of the cryocooler market, in terms of volume

- To provide detailed information regarding the drivers, restraints, opportunities, and challenges influencing the growth of the cryocooler market

- To analyze the cryocooler value chain and ecosystem, along with the average selling price of cryocoolers

- To strategically analyze the regulatory landscape, tariffs, standards, patents, Porter’s five forces, import and export scenarios, AI/Gen AI impact, trade values, the 2025 US Tariff, and case studies pertaining to the market under study

- To strategically analyze micromarkets1 with regard to individual growth trends, prospects, and contributions to the overall market

- To analyze opportunities in the market for stakeholders by identifying high-growth segments

- To provide details of the competitive landscape for market leaders

- To provide details of the macroeconomic outlook for regions

- To analyze strategies such as product launches, collaborations, and acquisitions adopted by players in the cryocooler market

- To profile key players in the cryocooler market and comprehensively analyze their market ranking based on their revenue, market share, and core competencies2

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

Country-wise Information:

- Country-wise breakdown for North America, Europe, Asia Pacific, and Rest of the World

Company Information:

- Detailed analysis and profiling of additional market players (up to five)

Key Questions Addressed by the Report

1

What is the projected size of the Cryocooler Market by 2030?

2

What is driving the growth of the Cryocooler Market?

3

Which region dominates the Cryocooler Market?

4

Which region is expected to witness the fastest growth?

5

Which application segment holds the largest market share?

6

What is the fastest-growing cryocooler type?

7

Which heat exchanger segment dominates the market?

8

Who are the leading companies in the Cryocooler Market?

9

What are the major trends shaping the Cryocooler industry?

10

What opportunities exist in the Cryocooler Market?

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Cryocooler Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

- US Cryocooler Market

- Canada Cryocooler Market

- Mexico Cryocooler Market

- Germany Cryocooler Market

- UK Cryocooler Market

- France Cryocooler Market

- Italy Cryocooler Market

- Netherlands Cryocooler Market

- Poland Cryocooler Market

- Japan Cryocooler Market

- China Cryocooler Market

- South Korea Cryocooler Market

- India Cryocooler Market

- Australia Cryocooler Market

- Indonesia Cryocooler Market

- Malaysia Cryocooler Market

- Thailand Cryocooler Market

- Vietnam Cryocooler Market

- Nordics Cryocooler Market

- Rest Of Europe Cryocooler Market

- Rest Of Asia Pacific Cryocooler Market

Growth opportunities and latent adjacency in Cryocooler Market

Elijah

Apr, 2026

How does temperature range selection vary across industries such as healthcare, space, and industrial applications?.

Nathan

Apr, 2026

How is the cryocooler market expected to evolve over the next 5�10 years in terms of new applications, cost reductions, and technological breakthroughs.