Request Customisation

Request Customisation

Nematicide Market

Report Code

AGI 2533

Published in

Aug, 2025, By MarketsandMarkets™

Nematicide Market by Type (Chemical, Biological), Nematode Type (Root-knot, Cyst, Lesion), Mode of Application (Drenching, Soil Dressing, Seed Treatment, Fumigation), Formulation, Crop Type and Region - Global Forecast to 2030

USD 5.09 BN

MARKET SIZE, 2030

CAGR 10.7%

(2025-2030)

300

REPORT PAGES

280

MARKET TABLES

OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

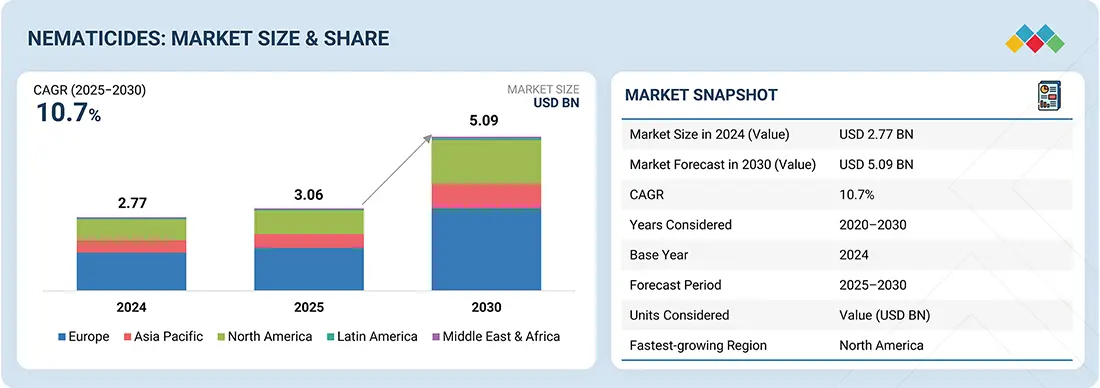

The nematicides market is projected to reach USD 5.09 billion by 2030 from USD 3.06 billion in 2025, at a CAGR of 10.7% from 2025 to 2030. The global nematicides market is growing due to increasing demand for effective solutions against plant-parasitic nematodes that impact crop yields. Adoption of chemical and biological nematicides is rising, driven by the shift toward sustainable and eco-friendly agricultural practices. Market growth is further supported by innovation in bio-nematicides and integrated pest management strategies.

Market Size and Forecast:

- Market Size Value in 2024: USD 2.77 Billion

- Market Size Value in 2025: USD 3.06 Billion

- Revenue Forecast in 2030: USD 5.09 Billion

- Growth Rate: CAGR of 10.7% from 2025 to 2030

- Base year: 2024

- Forecast period: 2025–2030

- North America dominated the nematicides market, accounting for a 38.5% share in 2024.

- The biological segment is expected to register the highest CAGR of 16.1%

Key Market Trends and Insights

- By Type: The Chemical Nematicides segment holds the largest market share due to their high effectiveness, broad-spectrum control, and extensive use in high-value crops.

- Growing Trends: Increasing adoption of integrated pest management (IPM), biological nematicides, and sustainable crop protection solutions is driving market growth.

- Growth Factors: Rising nematode-related crop losses, growing food demand, awareness of crop protection technologies, and advancements in biological formulations are fueling market expansion.

- Emerging Opportunities: Growth in bio-based nematicides, seed treatment solutions, precision agriculture, and high-value crop cultivation is creating new opportunities for market development.

KEY TAKEAWAYS

- North America dominated the nematicides market, accounting for a 38.5% share in 2024.

- By type, the biological segment is expected to register the highest CAGR of 16.1%.

- By nematode type, the lesion nematodes segment is projected to grow at the fastest rate from 2025 to 2030.

- By formulation, the granular segment will grow at the fastest rate during the forecast period.

- By mode of application, the soil dressing segment is expected to dominate the market, growing at the highest CAGR of 11.9%.

- By crop type, the fruits & vegetables segment is expected to dominate the market.

- Syngenta, UPL, Corteva, Bayer, and BASF are leading companies in the nematicides market, demonstrating a strong commitment to innovation, extensive industry coverage, and substantial operational and financial strength.

- IPL Biologicals, Vegalab, BioConsortia, and Bionema have distinguished themselves among startups and SMEs due to their strong product portfolios and business strategies.

The nematicides market is set for robust growth, driven by innovations in chemical and biological formulations that enhance nematode control and support sustainable agriculture. Increased adoption of integrated pest management practices, along with strategic collaborations among key industry players, is further fueling market expansion. Ongoing investment in eco-friendly solutions is expected to shape long-term market development.

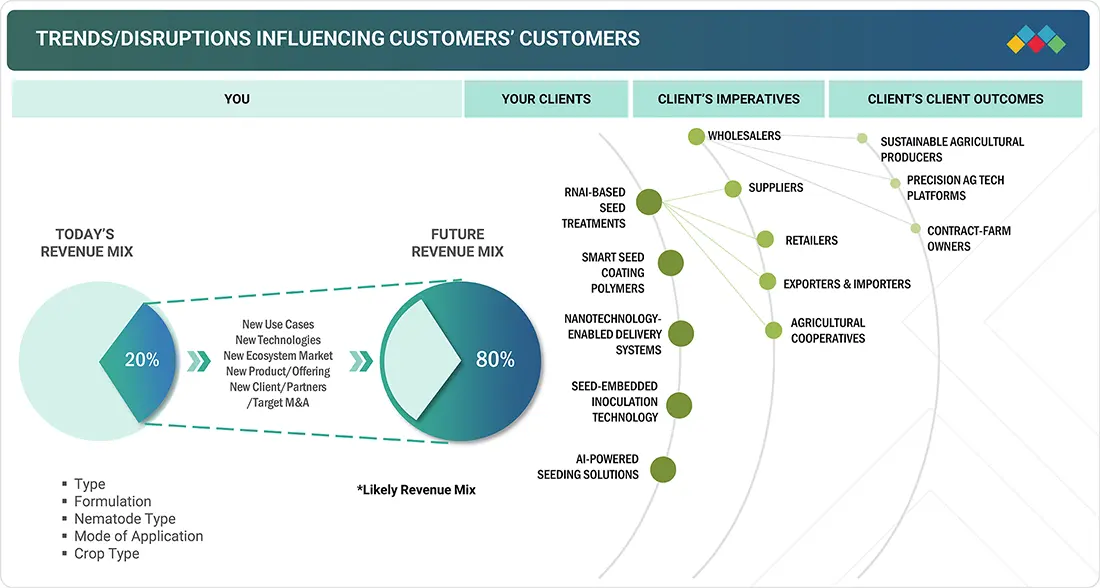

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The nematicides market is evolving with a strong focus on bio-based solutions, adoption of precision agriculture technologies, and sustainability-driven practices that enhance soil health and minimize chemical residues. Integration of nematicides with seed treatments and biostimulants is emerging as a value-added approach. Concurrently, the industry faces challenges from tightening regulatory frameworks, climate-induced variability in nematode pressure, entry of innovative bio-nematicide players, and supply chain constraints affecting product availability and pricing.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Strong demand for high-value crop

-

Demand for low-cost crop protection solutions

RESTRAINTS

Impact

Level

Level

-

Technological limitation in the use of biologicals

-

Varing government regulations

OPPORTUNITIES

Impact

Level

Level

-

Use of plant-based nematicides in organic agriculture and horticulture

-

Nematodes developing resistance to crop protection chemicals

CHALLENGES

Impact

Level

Level

-

Evolution of biotechnology and increasing accceptance of GM crops as alternatives to crop protection chemicals

-

Lack of awareness and low utlization of biologicals

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Strong demand for high-value crop

A major driver of the nematicides market is the increasing demand for high-value crops such as fruits, vegetables, and ornamentals, which are particularly susceptible to nematode damage. Protecting these crops is critical to maintaining yield, quality, and profitability, leading to greater adoption of advanced nematicide solutions. Growing consumer preference for premium produce and the economic importance of these crops further strengthen the demand for effective nematode management.

Restraint: Technological limitation in the use of biologicals

One of the key restraints in the nematicides market is the technological limitation of biological products. Despite their sustainability advantages, bio-nematicides often face challenges such as shorter shelf life, variable efficacy under field conditions, and sensitivity to environmental factors. These limitations can reduce their reliability compared to chemical alternatives, thereby restricting their wider adoption and slowing overall market growth.

Opportunity: Use of plant-based nematicides in organic agriculture and horticulture

A significant opportunity for the nematicides market is the increasing adoption of plant-based nematicides in organic agriculture and horticulture. These natural solutions support the rising demand for residue-free produce and environmentally sustainable crop protection. Their alignment with organic certification standards and consumer preference for eco-friendly farming practices positions plant-based nematicides as a strong growth driver for the industry.

Challenge: Evolution of biotechnology and increasing accceptance of GM crops as alternatives to crop protection chemicals

A key opportunity in the nematicides market is the advancement of biotechnology and the increasing acceptance of genetically modified (GM) crops as substitutes for traditional crop protection chemicals. Biotechnological innovations enable the development of nematode-resistant crops, reducing dependence on chemical solutions. The expanding adoption of GM crops highlights a shift toward sustainable and efficient farming practices, opening new pathways for integrated nematode management.

nematicides market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

|

Application of chemical nematicides for root-knot nematode control in vegetables and row crops | Provides rapid and effective nematode suppression, improving yield |

|

Bio-nematicide solutions for sustainable nematode management in high-value crops | Eco-friendly approach reduces chemical residues while maintaining crop protection |

|

Soil-applied granular nematicides for cereals and oilseeds | Offers long-lasting residual activity and ease of application |

|

Seed treatment nematicides for vegetables and pulses | Protects seedlings during early growth, enhancing crop establishment |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The nematicides market ecosystem encompasses manufacturers of chemical and biological solutions, distributors and retailers ensuring product availability, and farmers applying nematicides across key crops. It is further supported by regulatory authorities overseeing compliance, R&D and technology partners driving innovation in formulations and precision application, and agronomy service providers facilitating adoption and integrated pest management. This interconnected ecosystem is shaped by innovation, regulatory evolution, and increasing demand for sustainable nematode management solutions.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

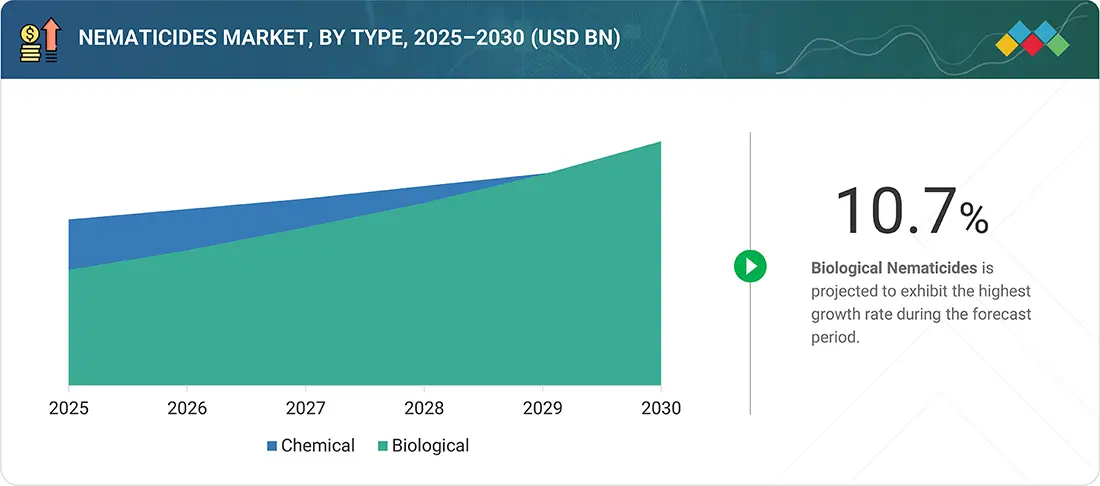

Nematicides Market, By Type

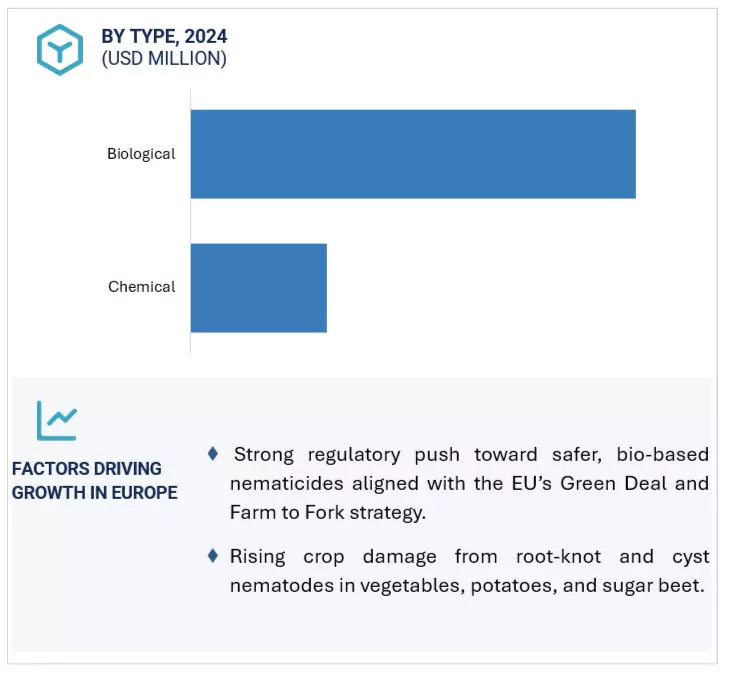

In the nematicides market, biological nematicides are expected to account for the largest share, driven by the increasing demand for sustainable and environmentally-friendly crop protection solutions. These products, derived from natural organisms or compounds, are preferred for their low environmental impact and compatibility with organic and integrated farming practices. Although chemical nematicides remain widely used for their high efficacy and fast action, regulatory restrictions and the growing demand for residue-free produce are accelerating the adoption of biological alternatives, supporting long-term market growth.

Nematicides Market, By Formulation

In the nematicides market's formulation segment, granular formulations are projected to hold the largest share, driven by their prolonged residual activity, ease of application, and precise nematode control. Liquid formulations remain in use for their rapid soil penetration and fast-acting results. Formulation choice is influenced by crop type, soil conditions, and application methods, with ongoing innovations supporting growth across both categories.

Nematicides Market, By Nematode Type

Lesion nematodes are expected to dominate the nematicides market segment due to their common occurrence and considerable impact on various crops. Other types, including root-knot and cyst nematodes, are also targeted based on specific crop susceptibility. The high prevalence of lesion nematodes and the need for effective control measures are driving demand for specialized nematicide solutions in this segment.

Nematicides Market, By Mode of Application

In the mode of application segment of the nematicides market, soil treatment (soil dressing) is projected to hold the largest share, owing to its direct and effective control of nematodes in the root zone. Other methods, including seed treatment and foliar application, are utilized depending on crop type and cultivation practices. The proven efficacy and widespread adoption of soil treatment underpin its leading position in this segment.

Nematicides Market, By Crop Type

The fruits and vegetables segment of the nematicides market is expected to have the largest share due to their high vulnerability to nematode infestations and the necessity of preserving yield quality and market value. While other crops such as cereals, grains, oilseeds, and pulses also contribute to nematicide demand, the economic significance and vulnerability of fruits and vegetables position them as the primary focus for effective nematode management solutions.

REGION

North America to be the fastest-growing region in the nematicides market during the forecast period

North America is anticipated to be the fastest-growing region in the nematicides market during the forecast period, driven by the adoption of advanced crop protection technologies and integrated pest management practices. The growth is supported by increasing emphasis on sustainable, high-yield agriculture and rising demand for high-value crops, including fruits, vegetables, and specialty grains, which require effective nematode management. Strong regulatory support and investment in innovative solutions further bolster market expansion in the region.

nematicides market: COMPANY EVALUATION MATRIX

A competitive landscape framework for the nematicides market classifies companies as Stars, Emerging Leaders, Participants, or Pervasive Players based on their innovation capabilities, market reach, and growth prospects. Syngenta is positioned as a Star, reflecting its strong portfolio and leadership in advanced nematicide solutions. Novonesis is identified as an Emerging Leader, supported by its focus on biological and sustainable approaches. Participants generally represent niche or regional players, while Pervasive Players maintain a broad market presence with established portfolios but limited innovation momentum.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2024 (Value) | USD 2.77 Billion |

| Market Forecast in 2030 (value) | USD 5.09 Billion |

| Growth Rate | CAGR of 10.7% during 2025-2030 |

| Years Considered | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Kiloton) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends. |

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, South America, RoW |

WHAT IS IN IT FOR YOU: nematicides market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| North America-based Crop Protection Company |

|

|

| European Agri-Biologicals Firm |

|

|

| APAC-based Agritech Firm |

|

|

| Global Agrochemical Distributor |

|

|

RECENT DEVELOPMENTS

- Febuary 2025 : BASF pre-launched Votivo Prime, a biological contact nematicide containing Bacillus firmus strain I-1582, at the fourth EnBio event in Argentina.

- January 2025 : American Vanguard Corporation, through its crop business unit AMVAC, entered into a regional distribution agreement with DPH Biologicals to expand its GreenSolutions portfolio, including BellaTrove Companion Maxx, an EPA-approved biocontrol product that provides both fungicidal and nematicidal activity.

- March 2025 : FMC Corporation expanded its biological crop protection platform in Canada by collaborating with Novonesis (formerly Novozymes A/S), a leader in plant biosolutions.

- December 2023 : Syngenta launched Certano, a microbiological bionematicide and the company's first biological product specifically designed for sugarcane cultivation.

- December 2022 : Corteva launched Lumialza, its first bionematicide for seed treatment in Brazil. The product contains Bacillus amyloliquefaciens strain PTA-4838.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

36

2

RESEARCH METHODOLOGY

42

3

EXECUTIVE SUMMARY

53

4

PREMIUM INSIGHTS

58

5

MARKET OVERVIEW

AI-driven innovations transform nematicide market, enhancing crop protection and reducing economic losses.

65

5.1

INTRODUCTION

5.2

MACROECONOMIC INDICATORS

5.2.1

ADOPTION OF PESTICIDES FOR DEFENSE AGAINST PEST ATTACKS

5.2.2

FOREIGN DIRECT INVESTMENTS

5.3

GLOBAL CROP LOSSES DUE TO NEMATODES

5.4

MARKET DYNAMICS

5.4.1

DRIVERS

5.4.1.1

Strong demand for high-value crops

5.4.1.2

Rising demand for low-cost crop protection solutions

5.4.1.3

Increasing damage to crop production due to nematode infestations

5.4.1.4

Integration of nematicides with modern farming practices

5.4.1.5

Advancements in biological nematicides

5.4.2

RESTRAINTS

5.4.2.1

Technological limitations in using biological products

5.4.2.2

Stringent government regulations

5.4.3

OPPORTUNITIES

5.4.3.1

Use of plant-based nematicides in organic agriculture and horticulture

5.4.3.2

Resistance to crop protection chemicals

5.4.3.3

Rising demand for biological solutions

5.4.4

CHALLENGES

5.4.4.1

Expanding adoption of GM crops to reduce dependence on conventional crop protection chemicals

5.4.4.2

Lack of awareness and low utilization of biologicals

5.4.4.3

Inconsistent field performance

5.5

IMPACT OF AI/GEN AI ON NEMATICIDES MARKET

5.5.1

INTRODUCTION

5.5.2

USE OF GEN AI IN NEMATICIDES MARKET

5.5.3

CASE STUDY ANALYSIS

5.5.3.1

Revolutionizing nematode management: Syngenta’s satellite-powered precision tool

5.5.3.2

Agmatix and BASF partnered to develop AI-powered detection of soybean cyst nematode

6

INDUSTRY TRENDS

Explore tariff impacts reshaping nematicide prices and technology trends across global markets.

79

6.1

INTRODUCTION

6.2

IMPACT OF 2025 US TARIFF – NEMATICIDES MARKET

6.2.1

INTRODUCTION

6.2.2

KEY TARIFF RATES

6.2.3

PRICE IMPACT ANALYSIS

6.2.4

IMPACT ON COUNTRY/REGION

6.2.4.1

US

6.2.4.2

Europe

6.2.4.3

Asia Pacific

6.2.5

IMPACT ON END-USE INDUSTRIES

6.3

VALUE CHAIN ANALYSIS

6.3.1

RESEARCH & DEVELOPMENT

6.3.2

MANUFACTURING

6.3.3

DISTRIBUTION

6.3.4

MARKETING & SALES

6.3.5

POST-SALE SERVICES

6.4

TRADE ANALYSIS

6.4.1

EXPORT SCENARIO OF HS CODE 3808

6.4.2

IMPORT SCENARIO OF HS CODE 3808

6.5

TECHNOLOGY ANALYSIS

6.5.1

KEY TECHNOLOGIES

6.5.1.1

RNAi-based nematicides

6.5.2

COMPLEMENTARY TECHNOLOGIES

6.5.2.1

Precision agriculture tools

6.5.3

ADJACENT TECHNOLOGIES

6.5.3.1

Seed treatment technologies

6.6

PRICING ANALYSIS

6.6.1

PRICING RANGE OF NEMATICIDE TYPES, BY KEY PLAYER, 2024

6.6.2

PRICING TREND, BY NEMATICIDE TYPE, 2020–2024

6.6.3

PRICING TREND OF NEMATICIDE PRODUCTS, BY REGION, 2020–2024

6.7

ECOSYSTEM ANALYSIS

6.7.1

DEMAND SIDE

6.7.2

SUPPLY SIDE

6.8

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

6.9

PATENT ANALYSIS

6.10

KEY CONFERENCES & EVENTS, 2025–2026

6.11

REGULATORY LANDSCAPE

6.11.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

6.11.2

NORTH AMERICA

6.11.2.1

US

6.11.2.2

Canada

6.11.3

EUROPE

6.11.3.1

UK

6.11.3.2

France

6.11.3.3

Russia

6.11.4

ASIA PACIFIC

6.11.4.1

India

6.11.4.2

China

6.11.4.3

Australia

6.11.5

SOUTH AMERICA

6.11.5.1

Brazil

6.11.6

REST OF WORLD

6.11.6.1

South Africa

6.11.6.2

UAE

6.12

PORTER’S FIVE FORCES ANALYSIS

6.12.1

THREAT OF NEW ENTRANTS

6.12.2

THREAT OF SUBSTITUTES

6.12.3

BARGAINING POWER OF BUYERS

6.12.4

BARGAINING POWER OF SUPPLIERS

6.12.5

INTENSITY OF COMPETITIVE RIVALRY

6.13

KEY STAKEHOLDERS AND BUYING CRITERIA

6.13.1

KEY STAKEHOLDERS IN BUYING PROCESS

6.13.2

BUYING CRITERIA

6.14

INVESTMENT AND FUNDING SCENARIO

6.15

CASE STUDY ANALYSIS

6.15.1

NUFARM LAUNCHED EVOLVANCE BIOLOGICAL BIONEMATICIDE TO ENHANCE CROP RESILIENCE

6.15.2

SYNGENTA LAUNCHED TYMIRIUM TECHNOLOGY FOR SUSTAINABLE NEMATODE AND FUNGAL DISEASE CONTROL

7

NEMATICIDES MARKET, BY TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Tons | 60 Data Tables

112

7.1

INTRODUCTION

7.2

CHEMICAL

7.2.1

LONGER RESIDUAL ACTIVITY AND QUICK MODE OF ACTION AGAINST NEMATODES TO DRIVE SEGMENT

7.2.2

FUMIGANTS

7.2.2.1

Broad-spectrum functionality of fumigants against nematodes to drive market

7.2.2.2

Methyl bromide

7.2.2.3

Metam sodium

7.2.2.4

1-3-Dichloropropene

7.2.2.5

Other fumigant types

7.2.3

NON-FUMIGANTS

7.2.3.1

Carbamates

7.2.3.2

Organophosphates

7.2.3.3

Abamectin (Next-gen)

7.2.3.4

SDHI (Next-gen)

7.2.4

OTHER CHEMICALS

7.2.4.1

Fluoroalkenyl compounds

7.2.4.2

Fluensulfone

7.2.4.3

Tioxazafen

7.2.4.4

Fluazaindolizine

7.3

BIOLOGICAL

7.3.1

STRINGENT REGULATORY POLICIES ON CONVENTIONAL AGROCHEMICALS TO DRIVE MARKET

7.3.2

MICROBIALS

7.3.2.1

High adoption of sustainable agricultural techniques to fuel growth

7.3.3

BIOCHEMICALS

7.3.3.1

Residue-free nematode management by biochemicals to propel growth

8

NEMATICIDES MARKET, BY NEMATODE TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 20 Data Tables

142

8.1

INTRODUCTION

8.2

ROOT-KNOT NEMATODES

8.2.1

RISING NEED TO REDUCE ECONOMIC LOSSES AND ENHANCE CROP QUALITY TO DRIVE DEMAND FOR NEMATICIDES

8.3

CYST NEMATODES

8.3.1

LARGE-SCALE ECONOMIC LOSSES AND LOWER YIELD QUALITY DUE TO CYST NEMATODE INFESTATION TO INCREASE DEMAND

8.4

LESION NEMATODES

8.4.1

WIDE HOST RANGE AND PRESENCE IN TEMPERATE AND TROPICAL ENVIRONMENTS TO DRIVE MARKET

8.5

OTHER NEMATODE TYPES

9

NEMATICIDES MARKET, BY FORMULATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 6 Data Tables

153

9.1

INTRODUCTION

9.2

GRANULAR

9.2.1

GOOD STORAGE VIABILITY TO DRIVE SEGMENT GROWTH

9.3

LIQUID

9.3.1

GREATER DEGREE OF DISPERSION PROPERTY OFFERED BY LIQUID NEMATICIDES TO DRIVE DEMAND

10

NEMATICIDES MARKET, BY MODE OF APPLICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Tons | 24 Data Tables

158

10.1

INTRODUCTION

10.2

FUMIGATION

10.2.1

LOWER COSTS INVOLVED IN FUMIGATION FOR NEMATODE CONTROL TO PROPEL GROWTH

10.3

DRENCHING

10.3.1

PRECISE APPLICATION AND DEEP PENETRATION OF NEMATICIDES ON TARGET NEMATODES TO DRIVE DEMAND

10.4

SOIL DRESSING

10.4.1

EFFECTIVE MANAGEMENT OF EARLY SEASON NEMATODE TO DRIVE DEMAND

10.5

SEED TREATMENT

10.5.1

SAFER APPLICATION AND EARLY SEASON PROTECTION AGAINST NEMATODE TO AUGMENT DEMAND

10.6

OTHER MODES OF APPLICATION

11

NEMATICIDES MARKET, BY CROP TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 17 Data Tables

172

11.1

INTRODUCTION

11.2

CEREALS & GRAINS

11.2.1

RISE IN CONSUMPTION AND EXTENSIVE CULTIVATION AREA TO DRIVE MARKET

11.2.2

CORN

11.2.3

WHEAT

11.2.4

RICE

11.2.5

OTHER CEREALS & GRAINS

11.3

OILSEEDS & PULSES

11.3.1

INCREASE IN CONSUMPTION OF PROTEIN- AND HEALTHY FAT-RICH MEALS TO DRIVE SEGMENTAL GROWTH

11.3.2

SOYBEAN

11.3.3

SUNFLOWER

11.3.4

OTHER OILSEEDS & PULSES

11.4

FRUITS & VEGETABLES

11.4.1

RISE IN EXPORTS OF FRESH, FROZEN, AND PROCESSED FRUITS & VEGETABLES FROM SOUTH ASIA TO DRIVE DEMAND

11.4.2

POME FRUITS

11.4.3

CITRUS FRUITS

11.4.4

LEAFY VEGETABLES

11.4.5

BERRIES

11.4.6

ROOTS & TUBERS VEGETABLES

11.4.7

OTHER FRUITS & VEGETABLES

11.5

OTHER CROP TYPES

12

NEMATICIDES MARKET, BY REGION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Tons | 377 Data Tables

188

12.1

INTRODUCTION

12.2

NORTH AMERICA

12.2.1

US

12.2.1.1

Research undertaken to introduce nematode-resistant vegetables and field crops to drive market

12.2.2

CANADA

12.2.2.1

Losses in high-value cash crops to drive adoption of nematicides

12.2.3

MEXICO

12.2.3.1

Increase in root-knot and root-lesion nematode infestation in wheat to fuel market

12.3

EUROPE

12.3.1

GERMANY

12.3.1.1

Environment-friendly and organic farming practices to cater to nematode attacks in field crops

12.3.2

UK

12.3.2.1

High demand for nematicides since farmers still use traditional farming methods

12.3.3

FRANCE

12.3.3.1

Extensive government funds in R&D to devise sustainable methods for nematode control

12.3.4

SPAIN

12.3.4.1

Surge in government initiatives to encourage use of biological nematicides

12.3.5

ITALY

12.3.5.1

Adoption of sustainable farming procedures to drive market

12.3.6

REST OF EUROPE

12.4

ASIA PACIFIC

12.4.1

CHINA

12.4.1.1

Rise in infestation by root-knot nematodes in crops to propel market

12.4.2

JAPAN

12.4.2.1

Rising demand for novel nematicides catering to long-term viability of crops to drive growth

12.4.3

INDIA

12.4.3.1

Protected environment in polyhouses to create favorable environment for root-knot nematodes

12.4.4

AUSTRALIA & NEW ZEALAND

12.4.4.1

Increase in canola losses due to nematode attacks to support adoption of nematicides

12.4.5

REST OF ASIA PACIFIC

12.5

SOUTH AMERICA

12.5.1

ARGENTINA

12.5.1.1

Increasing focus on soybean and corn cultivation to boost demand for nematicides

12.5.2

BRAZIL

12.5.2.1

High adoption of genetically modified crops to increase usage of nematicides

12.5.3

REST OF SOUTH AMERICA

12.6

REST OF THE WORLD (ROW)

12.6.1

MIDDLE EAST

12.6.1.1

Rise in population, high dependency on imports, and yield loss due to nematodes to boost market

12.6.2

AFRICA

12.6.2.1

Growth in demand for vegetable crops to drive growth

13

COMPETITIVE LANDSCAPE

Uncover how top players and startups are reshaping market dynamics with strategic expansions and innovations.

311

13.1

OVERVIEW

13.2

KEY PLAYERS’ STRATEGIES/RIGHT TO WIN

13.3

REVENUE ANALYSIS, 2020–2024

13.4

MARKET SHARE ANALYSIS, 2024

13.5

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

13.5.1

STARS

13.5.2

EMERGING LEADERS

13.5.3

PERVASIVE PLAYERS

13.5.4

PARTICIPANTS

13.5.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

13.5.5.1

Company footprint

13.5.5.2

Region footprint

13.5.5.3

Type footprint

13.5.5.4

Formulation footprint

13.5.5.5

Crop type footprint

13.6

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

13.6.1

PROGRESSIVE COMPANIES

13.6.2

RESPONSIVE COMPANIES

13.6.3

DYNAMIC COMPANIES

13.6.4

STARTING BLOCKS

13.6.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

13.6.5.1

Detailed list of key startups/SMEs

13.6.5.2

Competitive benchmarking of key startups/SMEs

13.7

COMPANY VALUATION AND FINANCIAL METRICS

13.8

BRAND/PRODUCT COMPARISON

13.9

COMPETITIVE SCENARIO AND TRENDS

13.9.1

PRODUCT LAUNCHES

13.9.2

DEALS

13.9.3

EXPANSIONS

14

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

333

14.1

KEY PLAYERS

14.1.1

BASF SE

14.1.1.1

Business overview

14.1.1.2

Products offered

14.1.1.3

Recent developments

14.1.1.4

MnM view

14.1.2

SYNGENTA

14.1.3

CORTEVA

14.1.4

UPL

14.1.5

BAYER AG

14.1.6

FMC CORPORATION

14.1.7

SUMITOMO CHEMICAL CO., LTD.

14.1.8

NUFARM

14.1.9

AMERICAN VANGUARD CORPORATION

14.1.10

NOVONESIS GROUP

14.1.11

BIOCERES CROP SOLUTIONS

14.1.12

GOWAN COMPANY

14.1.13

CERTIS USA L.L.C.

14.1.14

LALLEMAND INC

14.1.15

AECI PLANT HEALTH

14.2

OTHER PLAYERS

14.2.1

ANDERMATT GROUP AG

14.2.2

IPL BIOLOGICALS

14.2.3

PHERONYM, INC.

14.2.4

AGRILIFE

14.2.5

CROP IQ TECHNOLOGY

14.2.6

ROVENSA NEXT

14.2.7

BIONEMA

14.2.8

BIOCONSORTIA

14.2.9

VIVE CROP PROTECTION INC.

14.2.10

VEGALAB SA

15

ADJACENT AND RELATED MARKETS

389

15.1

INTRODUCTION

15.2

LIMITATIONS

15.3

CROP PROTECTION CHEMICALS MARKET

15.3.1

MARKET DEFINITION

15.3.2

MARKET OVERVIEW

15.4

BIORATIONAL PESTICIDES MARKET

15.4.1

MARKET DEFINITION

15.4.2

MARKET OVERVIEW

16

APPENDIX

394

16.1

DISCUSSION GUIDE

16.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

16.3

AVAILABLE CUSTOMIZATION

16.4

RELATED REPORTS

16.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

NEMATICIDES MARKET: INCLUSIONS AND EXCLUSIONS

TABLE 2

USD EXCHANGE RATES CONSIDERED, 2020–2024

TABLE 3

KEY DATA FROM PRIMARY SOURCES

TABLE 4

NEMATICIDES MARKET SNAPSHOT, 2025 VS. 2030

TABLE 5

AVERAGE ANNUAL MONETARY LOSS CAUSED BY PLANT PARASITIC NEMATODES TO ECONOMICALLY IMPORTANT CROPS

TABLE 6

US ADJUSTED RECIPROCAL TARIFF RATES

TABLE 7

EXPORT VALUE OF HS CODE 3808, BY KEY COUNTRY, 2020–2024 (USD THOUSAND)

TABLE 8

IMPORT VALUE OF HS CODE 3808, BY KEY COUNTRY, 2020–2024 (USD THOUSAND)

TABLE 9

PRICING RANGE OF NEMATICIDE TYPES, BY KEY PLAYER, 2024 (USD/KG)

TABLE 10

PRICING TREND, BY NEMATICIDE TYPE, 2020–2024 (USD/KG)

TABLE 11

PRICING TREND OF NEMATICIDE PRODUCTS, BY REGION, 2020–2024 (USD/KG)

TABLE 12

NEMATICIDES MARKET: ECOSYSTEM

TABLE 13

KEY PATENTS PERTAINING TO NEMATICIDES, 2015–2025

TABLE 14

NEMATICIDES MARKET: DETAILED LIST OF CONFERENCES AND EVENTS, 2025–2026

TABLE 15

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 16

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 17

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 18

SOUTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 19

REST OF WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 20

IMPACT OF PORTER’S FIVE FORCES ON NEMATICIDES MARKET

TABLE 21

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY MODE OF APPLICATION

TABLE 22

KEY BUYING CRITERIA, BY MODE OF APPLICATION

TABLE 23

NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 24

NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 25

NEMATICIDES MARKET, BY TYPE, 2020–2024 (TONS)

TABLE 26

NEMATICIDES MARKET, BY TYPE, 2025–2030 (TONS)

TABLE 27

CHEMICAL: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 28

CHEMICAL: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 29

CHEMICAL: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TONS)

TABLE 30

CHEMICAL: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TONS)

TABLE 31

CHEMICAL: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 32

CHEMICAL: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 33

CHEMICAL: NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 34

CHEMICAL: NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 35

FUMIGANTS APPLIED TO AGRONOMIC CROPS

TABLE 36

FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 37

FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 38

FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 39

FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 40

FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 41

FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 42

NON-FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 43

NON-FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 44

NON-FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 45

NON-FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 46

NON-FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 47

NON-FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 48

NON-FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TONS)

TABLE 49

NON-FUMIGANTS: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TONS)

TABLE 50

CROPS RECEIVING CARBAMATE APPLICATIONS

TABLE 51

CARBAMATES: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 52

CARBAMATES: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 53

CARBAMATES: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 54

CARBAMATES: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 55

ORGANOPHOSPHATES: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 56

ORGANOPHOSPHATES: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 57

ORGANOPHOSPHATES: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 58

ORGANOPHOSPHATES: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 59

ABAMECTIN: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 60

ABAMECTIN: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 61

ABAMECTIN: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 62

ABAMECTIN: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 63

SUCCINATE DEHYDROGENASE INHIBITORS: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 64

SUCCINATE DEHYDROGENASE INHIBITORS: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 65

SUCCINATE DEHYDROGENASE INHIBITORS: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 66

SUCCINATE DEHYDROGENASE INHIBITORS: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 67

SUCCINATE DEHYDROGENASE INHIBITORS: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 68

SUCCINATE DEHYDROGENASE INHIBITORS: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 69

OTHERS: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 70

OTHERS: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 71

OTHERS: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 72

OTHERS: NON-FUMIGANT NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 73

BIOLOGICAL: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 74

BIOLOGICAL: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 75

BIOLOGICAL: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 76

BIOLOGICAL: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 77

BIOLOGICAL: NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 78

BIOLOGICAL: NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 79

MICROBIALS: BIOLOGICAL NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 80

MICROBIALS: BIOLOGICAL NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 81

BIOCHEMICALS: BIOLOGICAL NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 82

BIOCHEMICALS: BIOLOGICAL NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 83

MOST COMMON NEMATODE SPECIES

TABLE 84

NEMATICIDES MARKET, BY NEMATODE TYPE, 2020–2024 (USD MILLION)

TABLE 85

NEMATICIDES MARKET, BY NEMATODE TYPE, 2025–2030 (USD MILLION)

TABLE 86

ROOT-KNOT NEMATODES: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 87

ROOT-KNOT NEMATODES: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 88

ROOT-KNOT NEMATODES: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 89

ROOT-KNOT NEMATODES: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 90

ECONOMIC LOSSES IN VEGETABLE CROPS DUE TO ROOT-KNOT NEMATODES

TABLE 91

CYST NEMATODES: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 92

CYST NEMATODES: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 93

CYST NEMATODES: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 94

CYST NEMATODES: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 95

LESION NEMATODES: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 96

LESION NEMATODES: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 97

LESION NEMATODES: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 98

LESION NEMATODES: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 99

OTHER NEMATODE TYPES: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 100

OTHER NEMATODE TYPES: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 101

OTHER NEMATODE TYPES: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 102

OTHER NEMATODE TYPES: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 103

NEMATICIDES MARKET, BY FORMULATION, 2020–2024 (USD MILLION)

TABLE 104

NEMATICIDES MARKET, BY FORMULATION, 2025–2030 (USD MILLION)

TABLE 105

GRANULAR NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 106

GRANULAR NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 107

LIQUID NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 108

LIQUID NEMATICIDES MARKET, BY REGION, 2025–2030(USD MILLION)

TABLE 109

NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (USD MILLION)

TABLE 110

NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (USD MILLION)

TABLE 111

NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (TONS)

TABLE 112

NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (TONS)

TABLE 113

FUMIGATION: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 114

FUMIGATION: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 115

FUMIGATION: NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 116

FUMIGATION: NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 117

DRENCHING: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 118

DRENCHING: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 119

DRENCHING: NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 120

DRENCHING: NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 121

SOIL DRESSING: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 122

SOIL DRESSING: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 123

SOIL DRESSING: NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 124

SOIL DRESSING: NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 125

SEED TREATMENT: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 126

SEED TREATMENT: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 127

SEED TREATMENT: NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 128

SEED TREATMENT: NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 129

OTHER MODES OF APPLICATION: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 130

OTHER MODES OF APPLICATION: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 131

OTHER MODES OF APPLICATION: NEMATICIDES MARKET, BY REGION, 2020–2024 (TONS)

TABLE 132

OTHER MODES OF APPLICATION: NEMATICIDES MARKET, BY REGION, 2025–2030 (TONS)

TABLE 133

NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 134

NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 135

CEREALS & GRAINS: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 136

CEREALS & GRAINS: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 137

CEREALS & GRAINS: NEMATICIDES MARKET, BY CROP SUB-TYPE, 2020–2024 (USD MILLION)

TABLE 138

CEREALS & GRAINS: NEMATICIDES MARKET, BY CROP SUB-TYPE, 2025–2030 (USD MILLION)

TABLE 139

NEMATODE TYPES AFFECTING CORN

TABLE 140

OILSEEDS & PULSES: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 141

OILSEEDS & PULSES: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 142

OILSEEDS & PULSES: NEMATICIDES MARKET, BY CROP SUB-TYPE, 2020–2024 (USD MILLION)

TABLE 143

OILSEEDS & PULSES: NEMATICIDES MARKET, BY CROP SUB-TYPE, 2025–2030 (USD MILLION)

TABLE 144

FRUITS & VEGETABLES: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 145

FRUITS & VEGETABLES: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 146

FRUITS & VEGETABLES: NEMATICIDES MARKET, BY CROP SUB-TYPE, 2020–2024 (USD MILLION)

TABLE 147

FRUITS & VEGETABLES: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 148

OTHER CROP TYPES: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 149

OTHER CROP TYPES: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 150

NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 151

NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 152

NEMATICIDES MARKET, BY REGION, 2020–2024 (TON)

TABLE 153

NEMATICIDES MARKET, BY REGION, 2025–2030 (TON)

TABLE 154

NORTH AMERICA: NEMATICIDES MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 155

NORTH AMERICA: NEMATICIDES MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 156

NORTH AMERICA: NEMATICIDES MARKET, BY COUNTRY, 2020–2024 (TON)

TABLE 157

NORTH AMERICA: NEMATICIDES MARKET, BY COUNTRY, 2025–2030 (TON)

TABLE 158

NORTH AMERICA: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 159

NORTH AMERICA: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 160

NORTH AMERICA: NEMATICIDES MARKET, BY NEMATODE TYPE, 2020–2024 (USD MILLION)

TABLE 161

NORTH AMERICA: NEMATICIDES MARKET, BY NEMATODE TYPE, 2025–2030 (USD MILLION)

TABLE 162

NORTH AMERICA: NEMATICIDES MARKET, BY FORMULATION, 2020–2024 (USD MILLION)

TABLE 163

NORTH AMERICA: NEMATICIDES MARKET, BY FORMULATION, 2025–2030 (USD MILLION)

TABLE 164

NORTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 165

NORTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 166

NORTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 167

NORTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 168

NORTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 169

NORTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 170

NORTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 171

NORTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 172

NORTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 173

NORTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 174

NORTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 175

NORTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 176

NORTH AMERICA: BIOLOGICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 177

NORTH AMERICA: BIOLOGICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 178

NORTH AMERICA: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (USD MILLION)

TABLE 179

NORTH AMERICA: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (USD MILLION)

TABLE 180

NORTH AMERICA: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (TON)

TABLE 181

NORTH AMERICA: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (TON)

TABLE 182

US: NEMATODE SPECIES AND THEIR PREVALENCE

TABLE 183

US: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 184

US: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 185

US: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 186

US: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 187

US: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 188

US: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 189

US: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 190

US: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 191

US: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 192

US: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 193

US: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 194

US: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 195

CANADA: CROPS INFESTED BY NEMATODES

TABLE 196

CANADA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 197

CANADA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 198

CANADA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 199

CANADA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 200

CANADA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 201

CANADA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 202

CANADA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 203

CANADA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 204

CANADA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 205

CANADA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 206

CANADA: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 207

CANADA: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 208

MEXICO: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 209

MEXICO: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 210

MEXICO: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 211

MEXICO: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 212

MEXICO: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 213

MEXICO: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 214

MEXICO: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 215

MEXICO: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 216

MEXICO: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 217

MEXICO: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 218

MEXICO: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 219

MEXICO: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 220

EUROPE: NEMATICIDES MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 221

EUROPE: NEMATICIDES MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 222

EUROPE: NEMATICIDES MARKET, BY COUNTRY, 2020–2024 (TON)

TABLE 223

EUROPE: NEMATICIDES MARKET, BY COUNTRY, 2025–2030 (TON)

TABLE 224

EUROPE: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 225

EUROPE: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 226

EUROPE: NEMATICIDES MARKET, BY NEMATODE TYPE, 2020–2024 (USD MILLION)

TABLE 227

EUROPE: NEMATICIDES MARKET, BY NEMATODE TYPE, 2025–2030 (USD MILLION)

TABLE 228

EUROPE: NEMATICIDES MARKET, BY FORMULATION, 2020–2024 (USD MILLION)

TABLE 229

EUROPE: NEMATICIDES MARKET, BY FORMULATION, 2025–2030 (USD MILLION)

TABLE 230

EUROPE: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 231

EUROPE: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 232

EUROPE: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 233

EUROPE: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 234

EUROPE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 235

EUROPE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 236

EUROPE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 237

EUROPE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 238

EUROPE: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 239

EUROPE: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 240

EUROPE: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 241

EUROPE: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 242

EUROPE: BIOLOGICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 243

EUROPE: BIOLOGICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 244

EUROPE: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (USD MILLION)

TABLE 245

EUROPE: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (USD MILLION)

TABLE 246

EUROPE: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (TON)

TABLE 247

EUROPE: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (TON)

TABLE 248

GERMANY: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 249

GERMANY: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 250

GERMANY: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 251

GERMANY: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 252

GERMANY: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 253

GERMANY: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 254

GERMANY: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 255

GERMANY: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 256

GERMANY: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 257

GERMANY: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 258

GERMANY: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 259

GERMANY: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 260

UK: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 261

UK: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 262

UK: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 263

UK: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 264

UK: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 265

UK: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 266

UK: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 267

UK: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 268

UK: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 269

UK: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 270

UK: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 271

UK: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 272

FRANCE: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 273

FRANCE: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 274

FRANCE: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 275

FRANCE: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 276

FRANCE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 277

FRANCE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 278

FRANCE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 279

FRANCE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 280

FRANCE: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 281

FRANCE: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 282

FRANCE: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 283

FRANCE: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 284

SPAIN: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 285

SPAIN: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 286

SPAIN: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 287

SPAIN: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 288

SPAIN: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 289

SPAIN: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 290

SPAIN: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 291

SPAIN: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 292

SPAIN: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 293

SPAIN: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 294

SPAIN: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 295

SPAIN: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 296

ITALY: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 297

ITALY: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 298

ITALY: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 299

ITALY: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 300

ITALY: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 301

ITALY: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 302

ITALY: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 303

ITALY: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 304

ITALY: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 305

ITALY: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 306

ITALY: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 307

ITALY: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 308

REST OF EUROPE: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 309

REST OF EUROPE: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 310

REST OF EUROPE: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 311

REST OF EUROPE: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 312

REST OF EUROPE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 313

REST OF EUROPE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 314

REST OF EUROPE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 315

REST OF EUROPE: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 316

REST OF EUROPE: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 317

REST OF EUROPE: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 318

REST OF EUROPE: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 319

REST OF EUROPE: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 320

ASIA PACIFIC: NEMATICIDES MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 321

ASIA PACIFIC: NEMATICIDES MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 322

ASIA PACIFIC: NEMATICIDES MARKET, BY COUNTRY, 2020–2024 (TON)

TABLE 323

ASIA PACIFIC: NEMATICIDES MARKET, BY COUNTRY, 2025–2030 (TON)

TABLE 324

ASIA PACIFIC: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 325

ASIA PACIFIC: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 326

ASIA PACIFIC: NEMATICIDES MARKET, BY NEMATODE TYPE, 2020–2024 (USD MILLION)

TABLE 327

ASIA PACIFIC: NEMATICIDES MARKET, BY NEMATODE TYPE, 2025–2030 (USD MILLION)

TABLE 328

ASIA PACIFIC: NEMATICIDES MARKET, BY FORMULATION, 2020–2024 (USD MILLION)

TABLE 329

ASIA PACIFIC: NEMATICIDES MARKET, BY FORMULATION, 2025–2030 (USD MILLION)

TABLE 330

ASIA PACIFIC: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 331

ASIA PACIFIC: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 332

ASIA PACIFIC: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 333

ASIA PACIFIC: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 334

ASIA PACIFIC: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 335

ASIA PACIFIC: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 336

ASIA PACIFIC: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 337

ASIA PACIFIC: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 338

ASIA PACIFIC: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 339

ASIA PACIFIC: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 340

ASIA PACIFIC: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 341

ASIA PACIFIC: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 342

ASIA PACIFIC: BIOLOGICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 343

ASIA PACIFIC: BIOLOGICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 344

ASIA PACIFIC: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (USD MILLION)

TABLE 345

ASIA PACIFIC: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (USD MILLION)

TABLE 346

ASIA PACIFIC: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (TON)

TABLE 347

ASIA PACIFIC: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (TON)

TABLE 348

CHINA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 349

CHINA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 350

CHINA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 351

CHINA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 352

CHINA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 353

CHINA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 354

CHINA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 355

CHINA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 356

CHINA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 357

CHINA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 358

CHINA: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 359

CHINA: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 360

JAPAN: MAJOR CROPS INFESTED BY NEMATODES

TABLE 361

JAPAN: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 362

JAPAN: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 363

JAPAN: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 364

JAPAN: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 365

JAPAN: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 366

JAPAN: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 367

JAPAN: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 368

JAPAN: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 369

JAPAN: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 370

JAPAN: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 371

JAPAN: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 372

JAPAN: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 373

INDIA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 374

INDIA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 375

INDIA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 376

INDIA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 377

INDIA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 378

INDIA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 379

INDIA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 380

INDIA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 381

INDIA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 382

INDIA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 383

INDIA: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 384

INDIA: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 385

AUSTRALIA & NEW ZEALAND: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 386

AUSTRALIA & NEW ZEALAND: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 387

AUSTRALIA & NEW ZEALAND: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 388

AUSTRALIA & NEW ZEALAND: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 389

AUSTRALIA & NEW ZEALAND: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 390

AUSTRALIA & NEW ZEALAND: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 391

AUSTRALIA & NEW ZEALAND: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 392

AUSTRALIA & NEW ZEALAND: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 393

AUSTRALIA & NEW ZEALAND: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 394

AUSTRALIA & NEW ZEALAND: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 395

AUSTRALIA & NEW ZEALAND: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 396

AUSTRALIA & NEW ZEALAND: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 397

REST OF ASIA PACIFIC: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 398

REST OF ASIA PACIFIC: NEMATICIDES MARKET, BY TYPE,2025–2030 (USD MILLION)

TABLE 399

REST OF ASIA PACIFIC: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 400

REST OF ASIA PACIFIC: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 401

REST OF ASIA PACIFIC: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 402

REST OF ASIA PACIFIC: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 403

REST OF ASIA PACIFIC: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 404

REST OF ASIA PACIFIC: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 405

REST OF ASIA PACIFIC: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 406

REST OF ASIA PACIFIC: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 407

REST OF ASIA PACIFIC: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 408

REST OF ASIA PACIFIC: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 409

SOUTH AMERICA: NEMATICIDES MARKET, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 410

SOUTH AMERICA: NEMATICIDES MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 411

SOUTH AMERICA: NEMATICIDES MARKET, BY COUNTRY, 2020–2024 (TON)

TABLE 412

SOUTH AMERICA: NEMATICIDES MARKET, BY COUNTRY, 2025–2030 (TON)

TABLE 413

SOUTH AMERICA: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 414

SOUTH AMERICA: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 415

SOUTH AMERICA: NEMATICIDES MARKET, BY NEMATODE TYPE, 2020–2024 (USD MILLION)

TABLE 416

SOUTH AMERICA: NEMATICIDES MARKET, BY NEMATODE TYPE, 2025–2030 (USD MILLION)

TABLE 417

SOUTH AMERICA: NEMATICIDES MARKET, BY FORMULATION, 2020–2024 (USD MILLION)

TABLE 418

SOUTH AMERICA: NEMATICIDES MARKET, BY FORMULATION,2025–2030 (USD MILLION)

TABLE 419

SOUTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 420

SOUTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 421

SOUTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 422

SOUTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 423

SOUTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 424

SOUTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 425

SOUTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 426

SOUTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 427

SOUTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 428

SOUTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 429

SOUTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 430

SOUTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 431

SOUTH AMERICA: BIOLOGICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 432

SOUTH AMERICA: BIOLOGICAL NEMATICIDES MARKET, BY TYPE,2025–2030 (USD MILLION)

TABLE 433

SOUTH AMERICA: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (USD MILLION)

TABLE 434

SOUTH AMERICA: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (USD MILLION)

TABLE 435

SOUTH AMERICA: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (TON)

TABLE 436

SOUTH AMERICA: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (TON)

TABLE 437

ARGENTINA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 438

ARGENTINA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 439

ARGENTINA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 440

ARGENTINA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 441

ARGENTINA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 442

ARGENTINA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 443

ARGENTINA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 444

ARGENTINA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 445

ARGENTINA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE,2020–2024 (USD MILLION)

TABLE 446

ARGENTINA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 447

ARGENTINA: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 448

ARGENTINA: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 449

BRAZIL: MOST PREVALENT NEMATODE SPECIES

TABLE 450

BRAZIL: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 451

BRAZIL: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 452

BRAZIL: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 453

BRAZIL: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 454

BRAZIL: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 455

BRAZIL: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 456

BRAZIL: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 457

BRAZIL: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 458

BRAZIL: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 459

BRAZIL: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 460

BRAZIL: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 461

BRAZIL: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 462

REST OF SOUTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 463

REST OF SOUTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 464

REST OF SOUTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 465

REST OF SOUTH AMERICA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 466

REST OF SOUTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE,2020–2024 (USD MILLION)

TABLE 467

REST OF SOUTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 468

REST OF SOUTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 469

REST OF SOUTH AMERICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 470

REST OF SOUTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 471

REST OF SOUTH AMERICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 472

REST OF SOUTH AMERICA: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 473

REST OF SOUTH AMERICA: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 474

ROW: NEMATICIDES MARKET, BY REGION, 2020–2024 (USD MILLION)

TABLE 475

ROW: NEMATICIDES MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 476

ROW: NEMATICIDES MARKET, BY REGION, 2020–2024 (TON)

TABLE 477

ROW: NEMATICIDES MARKET, BY REGION, 2025–2030 (TON)

TABLE 478

ROW: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 479

ROW: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 480

ROW: NEMATICIDES MARKET, BY NEMATODE TYPE, 2020–2024 (USD MILLION)

TABLE 481

ROW: NEMATICIDES MARKET, BY NEMATODE TYPE, 2025–2030 (USD MILLION)

TABLE 482

ROW: NEMATICIDES MARKET, BY FORMULATION, 2020–2024 (USD MILLION)

TABLE 483

ROW: NEMATICIDES MARKET, BY FORMULATION, 2025–2030 (USD MILLION)

TABLE 484

ROW: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 485

ROW: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 486

ROW: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 487

ROW: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 488

ROW: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 489

ROW: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 490

ROW: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 491

ROW: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 492

ROW: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 493

ROW: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 494

ROW: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 495

ROW: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 496

ROW: BIOLOGICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 497

ROW: BIOLOGICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 498

ROW: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (USD MILLION)

TABLE 499

ROW: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (USD MILLION)

TABLE 500

ROW: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2020–2024 (TON)

TABLE 501

ROW: NEMATICIDES MARKET, BY MODE OF APPLICATION, 2025–2030 (TON)

TABLE 502

MIDDLE EAST: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 503

MIDDLE EAST: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 504

MIDDLE EAST: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 505

MIDDLE EAST: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 506

MIDDLE EAST: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 507

MIDDLE EAST: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 508

MIDDLE EAST: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 509

MIDDLE EAST: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 510

MIDDLE EAST: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 511

MIDDLE EAST: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 512

MIDDLE EAST: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 513

MIDDLE EAST: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 514

SOUTH AFRICA: POPULAR WEED SPECIES AS HOSTS OF ROOT-KNOT NEMATODES

TABLE 515

AFRICA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 516

AFRICA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 517

AFRICA: NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 518

AFRICA: NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 519

AFRICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 520

AFRICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 521

AFRICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2020–2024 (TON)

TABLE 522

AFRICA: CHEMICAL NEMATICIDES MARKET, BY TYPE, 2025–2030 (TON)

TABLE 523

AFRICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2020–2024 (USD MILLION)

TABLE 524

AFRICA: NON-FUMIGANT NEMATICIDES MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 525

AFRICA: NEMATICIDES MARKET, BY CROP TYPE, 2020–2024 (USD MILLION)

TABLE 526

AFRICA: NEMATICIDES MARKET, BY CROP TYPE, 2025–2030 (USD MILLION)

TABLE 527

OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN NEMATICIDES MARKET, 2020–2025

TABLE 528

NEMATICIDES MARKET: DEGREE OF COMPETITION

TABLE 529

NEMATICIDES MARKET: REGION FOOTPRINT

TABLE 530

NEMATICIDES MARKET: TYPE FOOTPRINT

TABLE 531

NEMATICIDES MARKET: FORMULATION FOOTPRINT

TABLE 532

NEMATICIDES MARKET: CROP TYPE FOOTPRINT

TABLE 533

NEMATICIDES MARKET: KEY STARTUPS/SMES

TABLE 534

NEMATICIDES MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2024

TABLE 535

NEMATICIDES MARKET: PRODUCT/SERVICE LAUNCHES, JANUARY 2020– JULY 2025

TABLE 536

NEMATICIDES MARKET: DEALS, JANUARY 2020–JULY 2025

TABLE 537

NEMATICIDES MARKET: EXPANSIONS, JANUARY 2020–JULY 2025

TABLE 538

BASF SE: COMPANY OVERVIEW

TABLE 539

BASF SE: PRODUCTS OFFERED

TABLE 540