Download PDF

Download PDF Request Customisation

Request Customisation

Radiation Hardened Electronics Market Size, Share & Trends

Report Code

SE 2934

Published in

Sep, 2025, By MarketsandMarkets™

Radiation Hardened Electronics Market Size, Share & Trends by Component (Mixed Signal ICs, Processors & Controllers, Memory, Power Management), Manufacturing Technique (RHBD, RHBP), Product Type (COTS, Custom), Application and Region - Global Forecast to 2030

USD 2.30 BN

MARKET SIZE, 2030

CAGR 5.4%

(2025-2030)

285

REPORT PAGES

233

MARKET TABLES

RADIATION HARDENED ELECTRONICS MARKET OVERVIEW

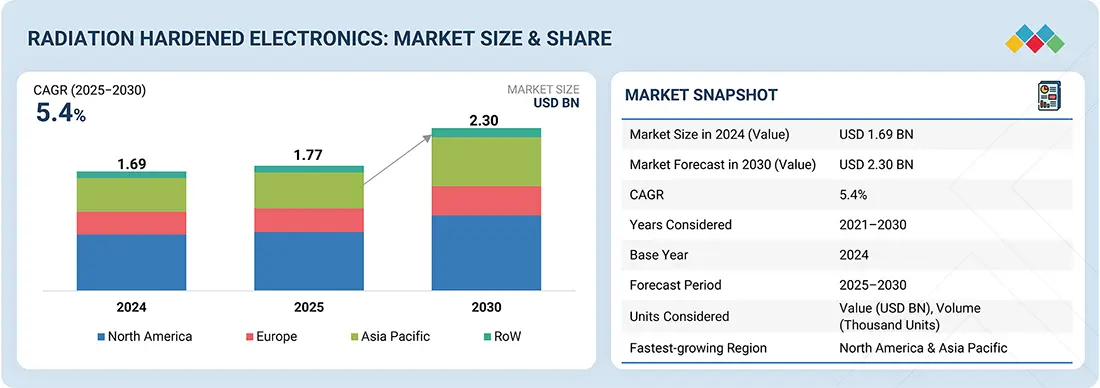

According to Marketsandmarkets, the Radiation Hardened Electronics Market Size was valued at USD 1.77 billion in 2025 and is projected to reach USD 2.30 billion in 2030, growing at a CAGR of 5.4% from 2025 to 2030. The market is growing steadily due to the rising intelligence, surveillance, and reconnaissance (ISR) activities, advancements in multicore processors for military and space applications, and the increasing demand from commercial satellites and nuclear-hardened systems. Governments and defense agencies invest heavily to ensure mission success in harsh environments, while global space missions fuel opportunities for reconfigurable rad-hard electronics and the adoption of commercial-off-the-shelf (COTS) components.

REPORT SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2025 (Value) | USD 1.77 billion |

| Market Forecast in 2030 (Value) | USD 2.30 billion |

| Growth Rate | CAGR of 5.4% from 2025-2030 |

| Years Considered | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion), Volume (Thousand Units) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Top Companies |

|

| Growth Driver |

|

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, RoW |

RADIATION HARDENED ELECTRONICS MARKET SIZE & FORECAST

• 2025 Market Size: USD 1.77 Billion

• 2030 Projected Market Size: USD 2.30 Billion

• CAGR (2025-2030): 5.4%

• Space (Satellites) Segment: Highest CAGR

• Asia Pacific: Fastest Growing Market

The Radiation Hardened Electronics Market Size is expanding steadily as demand grows for highly reliable electronic components capable of operating in extreme radiation environments such as space missions, nuclear facilities, and defense systems. This expansion is driven by the increasing number of satellite launches, growing intelligence, surveillance, and reconnaissance (ISR) activities, and rising investments in aerospace and defense technologies. As governments and private space companies continue to develop advanced spacecraft and communication satellites, the Radiation Hardened Electronics Industry is witnessing significant demand for processors, memory devices, and power management components that can withstand harsh radiation conditions.

The Radiation Hardened Electronics Market Share is largely dominated by North America due to strong investments from space agencies, defense organizations, and commercial space enterprises, while Asia Pacific is emerging as a rapidly growing region because of expanding space programs and semiconductor capabilities. Key Radiation Hardened Electronics Market Trends include the increasing adoption of radiation-hard-by-design (RHBD) manufacturing techniques, growing use of commercial-off-the-shelf (COTS) components in satellite systems, and the development of advanced multicore processors for mission-critical applications. These innovations are reshaping the Radiation Hardened Electronics Industry by improving system reliability and reducing development costs for space and defense platforms. With continued technological innovation and rising global investments in space exploration and defense infrastructure, the Radiation Hardened Electronics Market Growth is expected to strengthen further, enhancing the overall Radiation Hardened Electronics Market Share across aerospace, nuclear, and high-reliability electronics sectors worldwide.

RADIATION HARDENED ELECTRONICS MARKET KEY TAKEAWAYS

-

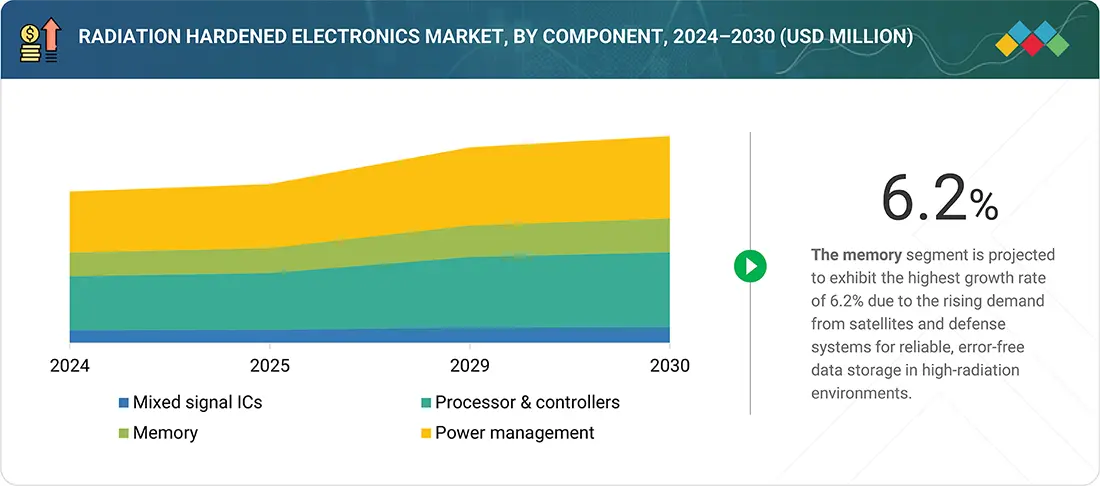

BY COMPONENTThe radiation hardened electronics market comprises of mixed signal ICs, processors & controllers, memory, and power management. The power management segment is estimated to account for the largest market share in 2030. The necessity of power management systems is a prominent driver of market growth, as well as their versatility and the need to ensure continued, efficient system performance.

-

BY MANUFACTURING TECHNIQUEThe market comprises radiation hardened by design and radiation hardened by process. The radiation-hardened-by-design segment is expected to dominate the overall market throughout the forecast period. These techniques involve different design strategies to offer superior resistance to radiation effects; as such, they may witness wide usage in satellites and defense.

-

BY PRODUCT TYPEThe market is segmented based on product type into commercial off-the-shelf products and custom-made products. The commercial off-the-shelf products segment is projected to lead the market throughout the forecast period. Their cost-effectiveness, versatility, and adaptability have made them highly sought after in the application areas for radiation-hardened electronics.

-

BY APPLICATIONBy application, the space (satellites) segment is projected to grow at the fastest rate during the forecast period, followed by the aerospace & defense segment. Space applications offer a sustained, growing demand for radiation-hardened electronics; satellites, probes, and other equipment must be able to withstand harsh conditions to ensure their feasibility and utility.

-

BY REGIONAsia Pacific is expected to be the fastest-growing market due to the increasing investments in space exploration, defense modernization, and nuclear energy.

-

COMPETITIVE LANDSCAPEThe major market players have adopted both organic and inorganic growth strategies, including partnerships and investments. The leading market players are Microchip, BAE Systems, and STMicroelectronics, leading with broad product portfolios. Niche companies such as Vorago Technologies and 3D Plus bring innovation in high-reliability designs.

The radiation-hardened electronics industry is expected to expand steadily over the coming decade, driven by rising investments in space exploration, defense modernization, and nuclear energy programs. These components are designed to withstand extreme radiation environments, ensuring reliable performance in satellites, military systems, and critical infrastructure. Growing satellite deployments for communication and earth observation, along with increasing demand for secure defense electronics, are fueling adoption. With technological advancements in design and manufacturing, Rad-Hard electronics are becoming more efficient and versatile, setting the stage for sustained global market growth.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

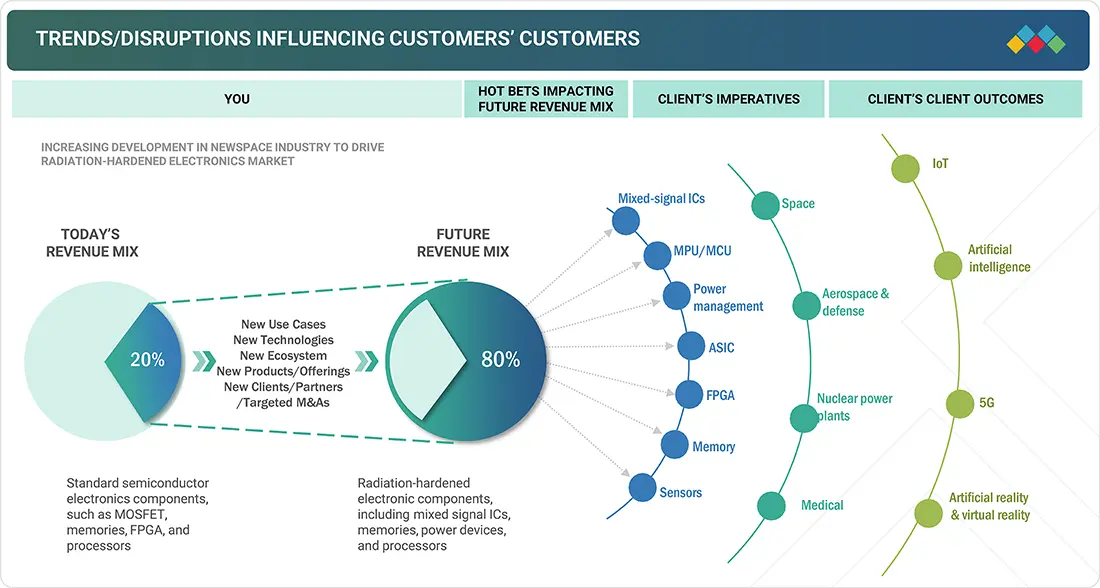

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

Increasing development in government and commercial satellites and the proliferation of several space missions, which include long-term satellites in high Earth orbit, are creating growth opportunities in the radiation-hardened electronics market. However, the major market driver for radiation-hardened electronics is low Earth orbit applications, such as reconnaissance orbiting and communication satellites, which use advanced radiation-hardened ICs for mission reliability.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

RADIATION HARDENED ELECTRONICS MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Rising intelligence, surveillance, and reconnaissance (ISR) activities

-

Technology advancements in multicore processors used for military and space applications

RESTRAINTS

Impact

Level

Level

-

Difficulties in creating real testing environments

-

High costs associated with development of radiation-hardened products

OPPORTUNITIES

Impact

Level

Level

-

Increasing space missions globally

-

Demand for reconfigurable radiation-hardened electronics

CHALLENGES

Impact

Level

Level

-

Customized requirements from high-end consumers

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Rising intelligence, surveillance, and reconnaissance (ISR) activities

The growing need for intelligence, surveillance, and reconnaissance systems in defense is fueling demand for radiation-hardened electronics, as these systems must operate reliably in space and high-radiation environments. This is pushing defense agencies to procure more Rad-Hard processors, sensors, and communication devices.

Restraint: High costs associated with development of radiation-hardened products

Developing Rad-Hard products requires specialized materials, testing facilities, and design techniques, which significantly raise costs. These high expenses limit adoption by smaller players and increase dependency on government funding and large-scale defense contracts.

Opportunity: Increasing space missions globally

With more countries and private firms launching satellites, lunar missions, and deep-space exploration projects, the need for robust Rad-Hard electronics is rising. This creates strong growth opportunities for suppliers to expand their portfolios and secure contracts with space agencies.

Challenge: Customized requirements from high-end consumers

Defense and space customers often demand highly tailored Rad-Hard solutions, such as unique processors or mission-specific FPGAs. Meeting these custom requirements increases design complexity, extends development timelines, and puts pressure on suppliers’ scalability.

RADIATION HARDENED ELECTRONICS MARKET SIZE, SHARE & GROWTH, 2030: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

The company is developing a 90 nm process hardening technique to create radiation-hardened ICs capable of withstanding extreme space radiation environments. This initiative is supported by the US Department of Defense through a USD 170 million investment. | The advancement enables higher circuit density, improved speed, and stronger performance in digital applications. It also positions SkyWater to deliver some of the most advanced radiation-hardened ICs for strategic space and defense missions. |

|

Everspin’s 4Mbit MRAM device was integrated into the SpriteSat (Rising) satellite’s magnetometer system to provide a compact, reliable memory solution capable of withstanding high temperatures and radiation conditions in space. | The MRAM replaces battery-backed SRAM and Flash, delivering non-volatile memory with long-term retention, unlimited endurance, and high reliability, ensuring consistent performance for rugged satellite operations. |

|

BAE Systems, through its FAST Labs R&D unit, is developing radiation-hardened by design (RHBD) microelectronics under a USD 60 million U.S. Army contract. The project leverages Intel’s commercial foundry process to create advanced design libraries for space and defense applications. | The initiative enables the use of advanced process nodes for RHBD ASICs, offering faster processing, low-power operation, and compact designs. It also strengthens the domestic US supply chain for next-generation aerospace and government missions. |

|

VORAGO’s Arm Cortex-M0 based microcontroller was selected by NASA and the Air Force Research Laboratory for the Radiation-Hardened Electronic Memory Experiment (RHEME). The MCU is being used to control and monitor tests on how radiation particles affect memory solutions in space. | The project supports the development of radiation-tolerant memory systems capable of detecting and correcting errors in spacecraft electronics. This enhances mission reliability and enables robust performance in extreme radiation and temperature environments. |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

RADIATION HARDENED ELECTRONICS MARKET ECOSYSTEM

The ecosystem of the radiation-hardened electronic market consists of material suppliers, radiation-hardened electronic manufacturers, fab facility providers, system integrators, distributors, and end users. Some of the major manufacturers of radiation-hardened electronics companies are Microchip Technology Inc. (US), Renesas Electronics Corporation (Japan), BAE Systems (UK), Infineon Technologies AG (Germany), STMicroelectronics (Switzerland), and AMD (US).

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

RADIATION HARDENED ELECTRONICS MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Radiation Hardened Electronics Market, By Component

The processors and controllers segment plays a vital role in the radiation-hardened electronics market, as these components are the backbone of mission-critical systems used in satellites, defense platforms, and nuclear facilities. Memory devices are witnessing the fastest growth due to increasing data storage needs in advanced space missions and defense applications. Power management solutions, on the other hand, are expected to command the largest market share by 2030, as they ensure uninterrupted and efficient system performance under extreme radiation conditions. Mixed-signal ICs continue to support communication and signal processing tasks, making the component segmentation essential for building robust, fault-tolerant systems.

Actuators Market, By Manufacturing Technique

Radiation Hardening by Design (RHBD) is expected to hold the largest market share by 2030 and also record the highest CAGR, reflecting its growing importance in building cost-effective and scalable solutions. RHBD techniques rely on circuit- and architecture-level design methods to improve resilience against radiation effects, making them suitable for a wide range of applications, including commercial satellites and defense systems. Radiation Hardening by Process (RHBP) continues to play a vital role in high-reliability missions, where specialized fabrication and materials are required, but RHBD’s balance of performance, flexibility, and cost efficiency is driving its stronger adoption.

Radiation Hardened Electronics Market, By Product Type

Commercial-off-the-Shelf (COTS) products are projected to account for the highest market share by 2030 and also register the highest growth, as they provide a cost-effective solution for commercial satellite programs and short to medium-duration space missions. Their adaptability and affordability make them attractive for new entrants in the space sector as well as for expanding constellations in low-earth orbit. In contrast, custom-made products remain essential for defense, nuclear, and deep-space missions where extreme reliability and long-term radiation resistance are critical. The growing shift toward COTS highlights the market’s preference for scalable and economical solutions without compromising basic performance requirements.

Radiation Hardened Electronics Market, By Application

The space segment is projected to hold the largest market share by 2030 and also record the highest CAGR, driven by the rising number of satellite launches, deep-space exploration programs, and commercial space ventures. Radiation-hardened electronics are indispensable in satellites, launch vehicles, and probes, as they must withstand intense cosmic radiation while ensuring long-term mission reliability. Aerospace and defense remain another key application area, with avionics, electronic warfare, and secure communications depending on fault-tolerant systems. Nuclear power plants and medical equipment, such as imaging devices used in radiation-intensive environments, are also emerging applications, showcasing the broadening utility of Rad-Hard technologies across industries

RADIATION HARDENED ELECTRONICS MARKET REGION

Asia Pacific to be fastest-growing region in global radiation hardened electronics market during forecast period

North America is expected to hold the largest market share by 2030, supported by significant investments from NASA, the US Department of Defense, and private space companies that consistently drive demand for radiation-hardened systems. Europe also maintains a strong position, aided by ESA programs and ongoing defense modernization efforts. Meanwhile, Asia Pacific is projected to register the highest CAGR, fueled by increasing space missions in China, India, and Japan, along with growing regional defense budgets and advancements in semiconductor manufacturing. The rest of the world continues to adopt these technologies in niche defense and energy projects.

RADIATION HARDENED ELECTRONICS MARKET SIZE, SHARE & GROWTH, 2030: COMPANY EVALUATION MATRIX

In the radiation-hardened electronics market matrix, BAE Systems (Star) stands out with a strong market presence and an extensive product portfolio, supporting critical defense and space programs worldwide. The company’s long-standing expertise in developing components that can withstand extreme environments positions it as a leader driving adoption across military, aerospace, and satellite applications. Texas Instruments (Emerging Leader), meanwhile, is steadily gaining momentum with its innovative rad-hard semiconductor solutions, catering to both government and commercial space missions. While BAE Systems dominate with scale and legacy programs, Texas Instruments shows strong growth potential to move into the leaders’ quadrant through its focus on advancing rad-hard microelectronics for next-generation platforms.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

RADIATION HARDENED ELECTRONICS MARKET KEY PLAYERS

WHAT IS IN IT FOR YOU: RADIATION HARDENED ELECTRONICS MARKET SIZE, SHARE & GROWTH, 2030 REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| US-based Aerospace & Defense Contractor | Detailed profiles of leading rad-hard component suppliers (product lines, technology focus), Benchmarking of suppliers by application fit (missiles, avionics, ISR systems), Ecosystem mapping of OEM–supplier partnerships | Identify reliable suppliers for mission-critical programs; Detect potential risks in supply continuity; Strengthen supplier qualification strategies |

| European Space Agency Supplier | Database of rad-hard IC vendors for satellite programs, Benchmarking of RHBD vs. RHBP adoption, Forecast of component demand for LEO/MEO/GEO missions | Insights into design choices impacting mission lifespan; Support procurement decisions for long-term satellite fleets; Enable selection of cost-effective COTS vs. custom components |

| Nuclear Power Plant Electronics Manufacturer | Assessment of rad-hard electronics adoption in reactor control & monitoring, Testing standards and regulatory compliance benchmarking, Competitive analysis of radiation-tolerant power management ICs | Ensure compliance with stringent safety standards; Minimize downtime with robust electronics integration; Enable positioning in high-barrier nuclear electronics market |

| Asian Semiconductor Company (Entering Rad-Hard Market) | Regional capacity benchmarking (US, EU, Asia), Pipeline analysis of space and defense programs driving demand, Identification of entry opportunities in COTS rad-hard ICs | Strengthen market entry roadmap; Spot high-growth demand clusters in space and defense; Assess competitive gaps for differentiation strategy |

RECENT DEVELOPMENTS

- April 2025 : BAE Systems collaborated with NEXT Semiconductor to develop space-qualified chips by integrating the NX450 ultra-wideband antenna processor unit (APU) into radiation-hardened subsystems. This integration, leveraging GlobalFoundries’ 12nm FinFET process, enhances digitization near sensors to improve performance, reduce SWaP, and strengthen satellite RF and electronic warfare systems.

- January 2024 : Infineon Technologies AG unveiled radiation-hardened asynchronous static random-access memory (SRAM) chips for space applications. Using RADSTOP technology, these chips are designed with proprietary methods for enhanced radiation hardness, ensuring high reliability and performance in harsh environments.

- October 2023 : Teledyne e2v collaborated with Microchip Technology to develop a pioneering space computing reference design, featuring Microchip’s Radiation-Tolerant Gigabit Ethernet PHYs. The innovative design focuses on high-speed data routing in space applications, presented at the EDHPC 2023.

- September 2023 : Microchip Technology Inc. launched the MPLAB Machine Learning Development Suite, a comprehensive solution supporting 8-bit, 16-bit, 32-bit MCUs and 32-MPUs for efficient ML at the edge. The integrated workflow streamlines ML model development across Microchip’s product portfolio.

- September 2023 : Infineon Technologies collaborated with Chinese firm Infypower in the new energy vehicle charger market, providing industry-leading 1200 V CoolSiC MOSFET power semiconductors. This partnership aimed to enhance efficiency in electric vehicle charging stations, offering a wide, constant power range, high density, minimal interference, and high reliability for Infypower’s 30 kW DC charging module.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

28

2

RESEARCH METHODOLOGY

33

3

EXECUTIVE SUMMARY

45

4

PREMIUM INSIGHTS

49

5

MARKET OVERVIEW

Rising ISR activities and space missions drive demand for affordable, reconfigurable radiation-hardened electronics.

52

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

Rising intelligence, surveillance, and reconnaissance (ISR) activities

5.2.1.2

Mounting demand for bandwidth, data processing, and memory components

5.2.1.3

Growing emphasis on affordable satellite communication

5.2.1.4

Increasing power generation from nuclear energy

5.2.2

RESTRAINTS

5.2.2.1

Issues in creating testing environments

5.2.2.2

High costs associated with developing radiation-hardened products

5.2.3

OPPORTUNITIES

5.2.3.1

Increasing global space missions

5.2.3.2

Rising demand for reconfigurable radiation-hardened electronics

5.2.3.3

Increasing use of commercial-off-the-shelf components in space satellites

5.2.4

CHALLENGES

5.2.4.1

Customization requirements from high-end consumers

5.3

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4

PRICING ANALYSIS

5.4.1

AVERAGE SELLING PRICE OF POWER MANAGEMENT PRODUCTS OFFERED BY KEY PLAYERS, BY COMPONENT TYPE, 2024

5.4.2

AVERAGE SELLING PRICE OF A/D & D/A CONVERTERS, BY KEY PLAYER, 2024

5.4.3

AVERAGE SELLING PRICE OF PROCESSORS & CONTROLLERS, BY KEY PLAYER, 2024

5.4.4

AVERAGE SELLING PRICE OF MEMORY PRODUCTS, BY KEY PLAYER, 2024

5.5

VALUE CHAIN ANALYSIS

5.6

ECOSYSTEM ANALYSIS

5.7

INVESTMENT AND FUNDING SCENARIO

5.8

TECHNOLOGY ANALYSIS

5.8.1

KEY TECHNOLOGIES

5.8.1.1

Radiation-hardened semiconductors

5.8.1.2

Rad-hard design techniques

5.8.1.3

Rad-hard packaging

5.8.2

COMPLEMENTARY TECHNOLOGIES

5.8.2.1

Radiation testing and simulation tools

5.8.2.2

Thermal management solutions

5.8.3

ADJACENT TECHNOLOGIES

5.8.3.1

Satellite and space systems

5.8.3.2

Defense electronics and avionics

5.8.3.3

Quantum and cryogenic electronics

5.9

PORTER’S FIVE FORCES ANALYSIS

5.9.1

INTENSITY OF COMPETITIVE RIVALRY

5.9.2

BARGAINING POWER OF SUPPLIERS

5.9.3

BARGAINING POWER OF BUYERS

5.9.4

THREAT OF SUBSTITUTES

5.9.5

THREAT OF NEW ENTRANTS

5.10

KEY STAKEHOLDERS AND BUYING CRITERIA

5.10.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.10.2

BUYING CRITERIA

5.11

CASE STUDY ANALYSIS

5.11.1

US DOD INVESTS IN SKYWATER TECHNOLOGY TO ADVANCE RADIATION-HARDENED TECHNOLOGY TO 90 MM PROCESS HARDENING TECHNIQUE

5.11.2

AAC MICROTEC AND TOHOKU UNIVERSITY INTEGRATE 4MBIT MRAM DEVICE FOR SATELLITES

5.11.3

ARMY CONTRACTING COMMAND INVESTS IN BAE SYSTEMS TO EXPEDITE DEVELOPMENT OF RHBD MICROELECTRONICS

5.11.4

NASA AND AIR FORCE RESEARCH LABORATORY CHOSE VORAGO TO PARTICIPATE IN RADIATION-HARDENED ELECTRONIC MEMORY EXPERIMENT

5.11.5

MERCURY SYSTEMS, INC. DEVELOPS 3U TRRUST-STOR VPX RT FOR TWO PROMINENT SUPPLIERS OF LOW EARTH ORBIT SATELLITES

5.12

TRADE ANALYSIS

5.12.1

IMPORT SCENARIO (HS CODE 8541)

5.12.2

EXPORT SCENARIO (HS CODE 8541)

5.13

PATENT ANALYSIS

5.14

KEY CONFERENCES AND EVENTS, 2025–2026

5.15

REGULATORY LANDSCAPE

5.15.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.15.2

STANDARDS AND REGULATIONS

5.16

IMPACT OF AI ON RADIATION HARDENED ELECTRONICS MARKET

5.16.1

INTRODUCTION

5.16.2

TOP USE CASES AND MARKET POTENTIAL

5.17

IMPACT OF 2025 US TARIFF ON MARKET

5.17.1

INTRODUCTION

5.17.2

KEY TARIFF RATES

5.17.3

PRICE IMPACT ANALYSIS

5.17.4

IMPACT ON COUNTRIES/REGIONS

5.17.4.1

US

5.17.4.2

Europe

5.17.4.3

Asia Pacific

5.17.5

IMPACT ON APPLICATIONS

6

RADIATION HARDENED ELECTRONIC MATERIALS AND PACKAGING TYPES

Explore advanced materials and packaging types enhancing durability in radiation-prone environments.

94

6.1

INTRODUCTION

6.2

MATERIALS

6.2.1

SILICON

6.2.2

SILICON CARBIDE (SIC)

6.2.3

GALLIUM NITRIDE (GAN)

6.2.4

GALLIUM ARSENIDE (GAAS)

6.3

PACKAGING TYPES

6.3.1

FLIP-CHIP

6.3.2

CERAMIC PACKAGES

7

RADIATION HARDENED ELECTRONICS MARKET, BY COMPONENT

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 78 Data Tables

98

7.1

INTRODUCTION

7.2

MIXED-SIGNAL ICS

7.2.1

A/D & D/A CONVERTERS

7.2.1.1

Increasing usage in space applications to bolster segmental growth

7.2.2

MULTIPLEXERS & RESISTORS

7.2.2.1

Rising need for data acquisition systems in space flights to augment segmental growth

7.3

PROCESSORS & CONTROLLERS

7.3.1

MPU

7.3.1.1

Mounting development of multicore processors for space & defense applications to fuel segmental growth

7.3.2

MCU

7.3.2.1

Widespread use in spacecraft subsystems to accelerate segmental growth

7.3.3

ASIC

7.3.3.1

Ability to address highly customized design requirements to contribute to segmental growth

7.3.4

FPGA

7.3.4.1

Use to eliminate costs related to electronic re-designing or manual updating to boost segmental growth

7.4

MEMORY

7.4.1

VOLATILE

7.4.1.1

DRAM

7.4.1.2

SRAM

7.4.2

NON-VOLATILE

7.4.2.1

MRAM

7.4.2.2

Flash

7.4.2.3

Other memory components

7.5

POWER MANAGEMENT

7.5.1

MOSFETS

7.5.1.1

Increasing adoption in outer space applications to foster segmental growth

7.5.2

DIODES

7.5.2.1

High voltage and improved electrical radiation performance to fuel segmental growth

7.5.3

THYRISTORS

7.5.3.1

Adoption in electronic converters for aerospace power systems to drive market

7.5.4

IGBTS

7.5.4.1

High current density and low power dissipation attributes to accelerate segmental growth

7.6

OTHER COMPONENTS (QUALITATIVE)

8

RADIATION HARDENED ELECTRONICS MARKET, BY MANUFACTURING TECHNIQUE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 22 Data Tables

126

8.1

INTRODUCTION

8.2

RADIATION HARDENED BY DESIGN (RHBD)

8.2.1

ABILITY TO IMPROVE RELIABILITY OF ELECTRONIC COMPONENTS IN EXTREME ENVIRONMENTS TO FOSTER SEGMENTAL GROWTH

8.2.2

TOTAL IONIZING DOSE (TID)

8.2.3

SINGLE EVENT EFFECT (SEE)

8.3

RADIATION HARDENED BY PROCESS (RHBP)

8.3.1

LESS SENSITIVITY TO DEGRADING EFFECTS CAUSED BY RADIATION TO BOOST SEGMENTAL GROWTH

8.3.2

SILICON ON INSULATOR (SOI)

8.3.3

SILICON ON SAPPHIRE (SOS)

8.4

RADIATION HARDENED BY SOFTWARE (RHBS) (QUALITATIVE)

9

RADIATION HARDENED ELECTRONICS MARKET, BY PRODUCT TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 23 Data Tables

136

9.1

INTRODUCTION

9.2

COMMERCIAL-OFF-THE-SHELF

9.2.1

INCREASING ADOPTION IN COMMERCIAL AND MILITARY SATELLITES DUE TO LOW-COST BENEFITS TO DRIVE MARKET

9.3

CUSTOM-MADE

9.3.1

HIGH PREFERENCE IN DEFENSE MISSION-CRITICAL APPLICATIONS TO EXPEDITE SEGMENTAL GROWTH

10

RADIATION HARDENED ELECTRONICS MARKET, BY APPLICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 18 Data Tables

145

10.1

INTRODUCTION

10.2

SPACE (SATELLITES)

10.2.1

COMMERCIAL

10.2.1.1

Widespread use of global positioning systems and navigation systems to contribute to segmental growth

10.2.1.2

Small satellites

10.2.1.3

New space

10.2.1.4

Nanosatellites

10.2.2

MILITARY

10.2.2.1

Requirement for high-quality components that withstand high levels of radiation to foster segmental growth

10.3

AEROSPACE & DEFENSE

10.3.1

WEAPONS & MISSILES

10.3.1.1

Deployment of reliable electronic components in defense applications to accelerate segmental growth

10.3.2

VEHICLES/AVIONICS

10.3.2.1

Focus on withstanding extreme radiation and temperature to contribute to segmental growth

10.4

NUCLEAR POWER PLANTS

10.4.1

EMPHASIS ON INCREASING POWER GENERATION TO AUGMENT SEGMENTAL GROWTH

10.5

MEDICAL

10.5.1

IMPLANTABLE MEDICAL DEVICES

10.5.1.1

Rapid technological advances to accelerate segmental growth

10.5.2

RADIOLOGY

10.5.2.1

Reliance of imaging techniques on ionizing radiation to fuel segmental growth

10.6

OTHER APPLICATIONS

11

RADIATION HARDENED ELECTRONICS MARKET, BY REGION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 12 Data Tables

158

11.1

INTRODUCTION

11.2

NORTH AMERICA

11.2.1

MACROECONOMIC OUTLOOK FOR NORTH AMERICA

11.2.2

US

11.2.2.1

Increasing space missions supported by government and private agencies to drive market

11.2.3

CANADA

11.2.3.1

Government initiatives related to space exploration to foster market growth

11.2.4

MEXICO

11.2.4.1

Expanding economy and commercial space satellite business to augment segmental growth

11.3

EUROPE

11.3.1

MACROECONOMIC OUTLOOK FOR EUROPE

11.3.2

UK

11.3.2.1

Increasing government initiatives to support space sector to fuel market growth

11.3.3

GERMANY

11.3.3.1

Proliferation of national space programs to boost demand for radiation-hardened electronics

11.3.4

FRANCE

11.3.4.1

Rising partnerships in space industry to contribute to market growth

11.3.5

REST OF EUROPE

11.4

ASIA PACIFIC

11.4.1

MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

11.4.2

CHINA

11.4.2.1

Increasing investment in military operations and technologies to accelerate market growth

11.4.3

INDIA

11.4.3.1

Growing focus on Earth observation, communication, and navigation satellites to drive market

11.4.4

JAPAN

11.4.4.1

Rise in funding for space programs to contribute to market growth

11.4.5

SOUTH KOREA

11.4.5.1

Increasing production of rockets to augment market growth

11.4.6

REST OF ASIA PACIFIC

11.5

ROW

11.5.1

MIDDLE EAST

11.5.1.1

Saudi Arabia

11.5.1.2

UAE

11.5.1.3

Rest of Middle East

11.5.2

SOUTH AMERICA

11.5.2.1

Growing support from foreign space agencies to fuel market growth

11.5.3

AFRICA

11.5.3.1

Increasing investment in satellite programs to accelerate market growth

12

COMPETITIVE LANDSCAPE

Uncover market leaders' strategies and competitive shifts shaping the industry's future landscape.

176

12.1

OVERVIEW

12.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, 2019–2025

12.3

REVENUE ANALYSIS, 2021–2024

12.4

MARKET SHARE ANALYSIS, 2024

12.5

COMPANY VALUATION AND FINANCIAL METRICS

12.6

BRAND COMPARISON

12.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.7.1

STARS

12.7.2

EMERGING LEADERS

12.7.3

PERVASIVE PLAYERS

12.7.4

PARTICIPANTS

12.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.7.5.1

Company footprint

12.7.5.2

Region footprint

12.7.5.3

Component footprint

12.7.5.4

Manufacturing technique footprint

12.7.5.5

Product type footprint

12.7.5.6

Application footprint

12.8

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

12.8.1

PROGRESSIVE COMPANIES

12.8.2

RESPONSIVE COMPANIES

12.8.3

DYNAMIC COMPANIES

12.8.4

STARTING BLOCKS

12.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

12.8.5.1

Detailed list of key startups/SMEs

12.8.5.2

Competitive benchmarking of key startups/SMEs

12.9

COMPETITIVE SCENARIO

12.9.1

PRODUCT LAUNCHES

12.9.2

DEALS

12.9.3

EXPANSIONS

13

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

203

13.1

KEY PLAYERS

13.1.1

MICROCHIP TECHNOLOGY INC.

13.1.1.1

Business overview

13.1.1.2

Products/Solutions/Services offered

13.1.1.3

Recent developments

13.1.1.4

MnM view

13.1.2

BAE SYSTEMS

13.1.3

RENESAS ELECTRONICS CORPORATION

13.1.4

INFINEON TECHNOLOGIES AG

13.1.5

STMICROELECTRONICS

13.1.6

ADVANCED MICRO DEVICES, INC.

13.1.7

TEXAS INSTRUMENTS INCORPORATED

13.1.8

HONEYWELL INTERNATIONAL INC.

13.1.9

TELEDYNE TECHNOLOGIES INCORPORATED

13.1.10

TTM TECHNOLOGIES INC.

13.2

OTHER PLAYERS

13.2.1

THALES

13.2.2

ANALOG DEVICES, INC.

13.2.3

DATA DEVICE CORPORATION

13.2.4

3D PLUS

13.2.5

MERCURY SYSTEMS, INC.

13.2.6

PCB PIEZOTRONICS, INC.

13.2.7

VORAGO TECHNOLOGIES

13.2.8

GSI TECHNOLOGY, INC.

13.2.9

EVERSPIN TECHNOLOGIES INC

13.2.10

SEMICONDUCTOR COMPONENTS INDUSTRIES, LLC

13.2.11

AITECH

13.2.12

MICROELECTRONICS RESEARCH DEVELOPMENT CORPORATION

13.2.13

TRIAD SEMICONDUCTOR

13.2.14

ZERO ERROR SYSTEMS

13.2.15

RESILIENT COMPUTING

14

APPENDIX

278

14.1

DISCUSSION GUIDE

14.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

14.3

CUSTOMIZATION OPTIONS

14.4

RELATED REPORTS

14.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

RADIATION HARDENED ELECTRONICS MARKET: INCLUSIONS AND EXCLUSIONS

TABLE 2

MAJOR SECONDARY SOURCES

TABLE 3

PRIMARY INTERVIEW PARTICIPANTS

TABLE 4

RADIATION HARDENED ELECTRONICS MARKET: RISK ANALYSIS

TABLE 5

AVERAGE SELLING PRICE OF POWER MANAGEMENT PRODUCTS OFFERED BY KEY PLAYERS, BY COMPONENT TYPE, 2024

TABLE 6

AVERAGE SELLING PRICE OF A/D & D/A CONVERTERS OFFERED BY KEY PLAYERS, 2024

TABLE 7

AVERAGE SELLING PRICE OF PROCESSORS & CONTROLLERS OFFERED BY KEY PLAYERS, 2024

TABLE 8

AVERAGE SELLING PRICE OF MEMORY PRODUCTS OFFERED BY KEY PLAYERS, 2024

TABLE 9

ROLE OF COMPANIES IN RADIATION HARDENED ELECTRONICS ECOSYSTEM

TABLE 10

IMPACT OF PORTER’S FIVE FORCES ANALYSIS

TABLE 11

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

TABLE 12

KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

TABLE 13

IMPORT DATA FOR HS CODE 8541-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 14

EXPORT DATA FOR HS CODE 8541-COMPLIANT PRODUCTS, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 15

LIST OF KEY PATENTS, 2021–2025

TABLE 16

LIST OF KEY CONFERENCES AND EVENTS, 2025–2026

TABLE 17

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 18

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 19

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 20

ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 21

US-ADJUSTED RECIPROCAL TARIFF RATES

TABLE 22

RADIATION HARDENED ELECTRONICS MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 23

RADIATION HARDENED ELECTRONICS MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 24

MIXED-SIGNAL ICS: MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 25

MIXED-SIGNAL ICS: MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 26

MIXED-SIGNAL ICS: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 27

MIXED-SIGNAL ICS: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 28

MIXED-SIGNAL ICS: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 29

MIXED-SIGNAL ICS: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 30

A/D & D/A CONVERTERS: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 31

A/D & D/A CONVERTERS: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 32

A/D & D/A CONVERTERS: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 33

A/D & D/A CONVERTERS: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 34

MULTIPLEXERS & RESISTORS: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 35

MULTIPLEXERS & RESISTORS: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 36

MULTIPLEXERS & RESISTORS: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 37

MULTIPLEXERS & RESISTORS: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 38

PROCESSORS & CONTROLLERS: MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 39

PROCESSORS & CONTROLLERS: MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 40

PROCESSORS & CONTROLLERS: MARKET, BY TYPE, 2021–2024 (THOUSAND UNITS)

TABLE 41

PROCESSORS & CONTROLLERS: MARKET, BY TYPE, 2025–2030 (THOUSAND UNITS)

TABLE 42

PROCESSORS & CONTROLLERS: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 43

PROCESSORS & CONTROLLERS: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 44

PROCESSORS & CONTROLLERS: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 45

PROCESSORS & CONTROLLERS: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 46

MPU: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 47

MPU: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 48

MPU: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 49

MPU: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 50

MCU: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 51

MCU: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 52

MCU: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 53

MCU: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 54

ASIC: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 55

ASIC: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 56

ASIC: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 57

ASIC: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 58

FPGA: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 59

FPGA: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 60

FPGA: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 61

FPGA: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 62

MEMORY: MARKET, BY TYPE, 2021–2024 (USD MILLION)

TABLE 63

MEMORY: MARKET, BY TYPE, 2025–2030 (USD MILLION)

TABLE 64

RADIATION HARDENED ELECTRONICS MARKET, BY MEMORY COMPONENT, 2021–2024 (USD MILLION)

TABLE 65

RADIATION HARDENED ELECTRONICS MARKET, BY MEMORY COMPONENT, 2025–2030 (USD MILLION)

TABLE 66

MEMORY: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 67

MEMORY: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 68

MEMORY: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 69

MEMORY: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 70

VOLATILE: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 71

VOLATILE: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 72

VOLATILE: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 73

VOLATILE: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 74

NON-VOLATILE: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 75

NON-VOLATILE: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 76

NON-VOLATILE: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 77

NON-VOLATILE: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 78

POWER MANAGEMENT: MARKET, BY COMPONENT TYPE, 2021–2024 (USD MILLION)

TABLE 79

POWER MANAGEMENT: MARKET, BY COMPONENT TYPE, 2025–2030 (USD MILLION)

TABLE 80

POWER MANAGEMENT: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 81

POWER MANAGEMENT: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 82

POWER MANAGEMENT: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 83

POWER MANAGEMENT: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 84

MOSFETS: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 85

MOSFETS: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 86

MOSFETS: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 87

MOSFETS: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 88

DIODES: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 89

DIODES: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 90

DIODES: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 91

DIODES: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 92

THYRISTORS: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 93

THYRISTORS: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 94

THYRISTORS: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 95

THYRISTORS: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 96

IGBTS: MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 97

IGBTS: MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 98

IGBTS: MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 99

IGBTS: MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 100

RADIATION HARDENED ELECTRONICS MARKET, BY MANUFACTURING TECHNIQUE, 2021–2024 (USD MILLION)

TABLE 101

RADIATION HARDENED ELECTRONICS MARKET, BY MANUFACTURING TECHNIQUE, 2025–2030 (USD MILLION)

TABLE 102

RADIATION HARDENED BY DESIGN (RHBD): MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 103

RADIATION HARDENED BY DESIGN (RHBD): MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 104

RADIATION HARDENED BY DESIGN (RHBD): MARKET FOR MIXED-SIGNAL ICS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 105

RADIATION HARDENED BY DESIGN (RHBD): MARKET FOR MIXED-SIGNAL ICS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 106

RADIATION HARDENED BY DESIGN (RHBD): MARKET FOR PROCESSORS & CONTROLLERS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 107

RADIATION HARDENED BY DESIGN (RHBD): MARKET FOR PROCESSORS & CONTROLLERS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 108

RADIATION HARDENED BY DESIGN (RHBD): MARKET FOR MEMORY, BY TYPE, 2021–2024 (USD MILLION)

TABLE 109

RADIATION HARDENED BY DESIGN (RHBD): MARKET FOR MEMORY, BY TYPE, 2025–2030 (USD MILLION)

TABLE 110

RADIATION HARDENED BY DESIGN (RHBD): MARKET FOR POWER MANAGEMENT, BY COMPONENT TYPE, 2021–2024 (USD MILLION)

TABLE 111

RADIATION HARDENED BY DESIGN (RHBD): MARKET FOR POWER MANAGEMENT, BY COMPONENT TYPE, 2025–2030 (USD MILLION)

TABLE 112

RADIATION HARDENED BY PROCESS (RHBP): MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 113

RADIATION HARDENED BY PROCESS (RHBP): MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 114

RADIATION HARDENED BY PROCESS (RHBP): MARKET FOR MIXED-SIGNAL ICS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 115

RADIATION HARDENED BY PROCESS (RHBP): MARKET FOR MIXED-SIGNAL ICS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 116

RADIATION HARDENED BY PROCESS (RHBP): MARKET FOR PROCESSORS & CONTROLLERS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 117

RADIATION HARDENED BY PROCESS (RHBP): MARKET FOR PROCESSORS & CONTROLLERS, BY TYPE,2025–2030 (USD MILLION)

TABLE 118

RADIATION HARDENED BY PROCESS (RHBP): MARKET FOR MEMORY, BY TYPE, 2021–2024 (USD MILLION)

TABLE 119

RADIATION HARDENED BY PROCESS (RHBP): MARKET FOR MEMORY, BY TYPE, 2025–2030 (USD MILLION)

TABLE 120

RADIATION HARDENED BY PROCESS (RHBP): MARKET FOR POWER MANAGEMENT, BY COMPONENT TYPE, 2021–2024 (USD MILLION)

TABLE 121

RADIATION HARDENED BY PROCESS (RHBP): MARKET FOR POWER MANAGEMENT, BY COMPONENT TYPE,2025–2030 (USD MILLION)

TABLE 122

RADIATION HARDENED ELECTRONICS MARKET, BY PRODUCT TYPE, 2021–2024 (USD MILLION)

TABLE 123

RADIATION HARDENED ELECTRONICS MARKET, BY PRODUCT TYPE, 2025–2030 (USD MILLION)

TABLE 124

COMMERCIAL OFF-THE-SHELF (COTS) PRODUCTS OFFER THE FOLLOWING BENEFITS:

TABLE 125

COMMERCIAL OFF-THE-SHELF: MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 126

COMMERCIAL OFF-THE-SHELF: MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 127

COMMERCIAL OFF-THE-SHELF: MARKET FOR MIXED-SIGNAL ICS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 128

COMMERCIAL OFF-THE-SHELF: MARKET FOR MIXED-SIGNAL ICS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 129

COMMERCIAL OFF-THE-SHELF: MARKET FOR PROCESSORS & CONTROLLERS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 130

COMMERCIAL OFF-THE-SHELF: MARKET FOR PROCESSORS & CONTROLLERS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 131

COMMERCIAL OFF-THE-SHELF: MARKET FOR MEMORY, BY TYPE, 2021–2024 (USD MILLION)

TABLE 132

COMMERCIAL OFF-THE-SHELF: MARKET FOR MEMORY, BY TYPE, 2025–2030 (USD MILLION)

TABLE 133

COMMERCIAL OFF-THE-SHELF: MARKET FOR POWER MANAGEMENT, BY COMPONENT TYPE, 2021–2024 (USD MILLION)

TABLE 134

COMMERCIAL OFF-THE-SHELF: MARKET FOR POWER MANAGEMENT, BY COMPONENT TYPE, 2025–2030 (USD MILLION)

TABLE 135

CUSTOM-MADE: MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 136

CUSTOM-MADE: MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 137

CUSTOM-MADE: MARKET FOR MIXED-SIGNAL ICS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 138

CUSTOM-MADE: MARKET FOR MIXED-SIGNAL ICS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 139

CUSTOM-MADE: MARKET FOR PROCESSORS & CONTROLLERS, BY TYPE, 2021–2024 (USD MILLION)

TABLE 140

CUSTOM-MADE: MARKET FOR PROCESSORS & CONTROLLERS, BY TYPE, 2025–2030 (USD MILLION)

TABLE 141

CUSTOM-MADE: MARKET FOR MEMORY, BY TYPE, 2021–2024 (USD MILLION)

TABLE 142

CUSTOM-MADE: MARKET FOR MEMORY, BY TYPE, 2025–2030 (USD MILLION)

TABLE 143

CUSTOM-MADE: MARKET FOR POWER MANAGEMENT, BY COMPONENT TYPE, 2021–2024 (USD MILLION)

TABLE 144

CUSTOM-MADE: MARKET FOR POWER MANAGEMENT, BY COMPONENT TYPE, 2025–2030 (USD MILLION)

TABLE 145

RADIATION HARDENED ELECTRONICS MARKET, BY APPLICATION, 2021–2024 (USD MILLION)

TABLE 146

RADIATION HARDENED ELECTRONICS MARKET, BY APPLICATION, 2025–2030 (USD MILLION)

TABLE 147

SPACE (SATELLITES): MARKET, BY APPLICATION TYPE, 2021–2024 (USD MILLION)

TABLE 148

SPACE (SATELLITES): MARKET, BY APPLICATION TYPE, 2025–2030 (USD MILLION)

TABLE 149

SPACE (SATELLITES): MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 150

SPACE (SATELLITES): MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 151

AEROSPACE & DEFENSE: MARKET, BY APPLICATION TYPE, 2021–2024 (USD MILLION)

TABLE 152

AEROSPACE & DEFENSE: MARKET, BY APPLICATION TYPE, 2025–2030 (USD MILLION)

TABLE 153

AEROSPACE & DEFENSE: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 154

AEROSPACE & DEFENSE: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 155

NUCLEAR POWER PLANTS: MARKET,BY REGION, 2021–2024 (USD MILLION)

TABLE 156

NUCLEAR POWER PLANTS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 157

MEDICAL: MARKET, BY APPLICATION TYPE, 2021–2024 (USD MILLION)

TABLE 158

MEDICAL: MARKET, BY APPLICATION TYPE, 2025–2030 (USD MILLION)

TABLE 159

MEDICAL: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 160

MEDICAL: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 161

OTHER APPLICATIONS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 162

OTHER APPLICATIONS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 163

RADIATION HARDENED ELECTRONICS MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 164

RADIATION HARDENED ELECTRONICS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 165

NORTH AMERICA: MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 166

NORTH AMERICA: MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 167

EUROPE: MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 168

EUROPE: MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 169

ASIA PACIFIC: MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 170

ASIA PACIFIC: MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 171

ROW: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 172

ROW: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 173

MIDDLE EAST: MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 174

MIDDLE EAST: MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 175

RADIATION HARDENED ELECTRONICS MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2019–JUNE 2025

TABLE 176

RADIATION HARDENED ELECTRONICS MARKET: DEGREE OF COMPETITION, 2024

TABLE 177

RADIATION HARDENED ELECTRONICS MARKET: REGION FOOTPRINT

TABLE 178

RADIATION HARDENED ELECTRONICS MARKET: COMPONENT FOOTPRINT

TABLE 179

RADIATION HARDENED ELECTRONICS MARKET: MANUFACTURINGTECHNIQUE FOOTPRINT

TABLE 180

RADIATION HARDENED ELECTRONICS MARKET: PRODUCT TYPE FOOTPRINT

TABLE 181

RADIATION HARDENED ELECTRONICS MARKET: APPLICATION FOOTPRINT

TABLE 182

RADIATION HARDENED ELECTRONICS MARKET: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 183

RADIATION HARDENED ELECTRONICS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 184

RADIATION HARDENED ELECTRONICS MARKET: PRODUCT LAUNCHES, JANUARY 2019–JUNE 2025

TABLE 185

RADIATION HARDENED ELECTRONICS MARKET: DEALS, JANUARY 2019–JUNE 2025

TABLE 186

RADIATION HARDENED ELECTRONICS MARKET: EXPANSIONS, JANUARY 2019–JUNE 2025

TABLE 187

MICROCHIP TECHNOLOGY INC.: COMPANY OVERVIEW

TABLE 188

MICROCHIP TECHNOLOGY INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 189

MICROCHIP TECHNOLOGY INC.: PRODUCT LAUNCHES

TABLE 190

MICROCHIP TECHNOLOGY INC.: DEALS

TABLE 191

MICROCHIP TECHNOLOGY INC.: EXPANSIONS

TABLE 192

BAE SYSTEMS: COMPANY OVERVIEW

TABLE 193

BAE SYSTEMS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 194

BAE SYSTEMS: PRODUCT LAUNCHES

TABLE 195

BAE SYSTEMS: DEALS

TABLE 196

BAE SYSTEMS: OTHER DEVELOPMENTS

TABLE 197

RENESAS ELECTRONICS CORPORATION: COMPANY OVERVIEW

TABLE 198

RENESAS ELECTRONICS CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 199

RENESAS ELECTRONICS CORPORATION: PRODUCT LAUNCHES

TABLE 200

RENESAS ELECTRONICS CORPORATION: DEALS

TABLE 201

RENESAS ELECTRONICS CORPORATION: OTHER DEVELOPMENTS

TABLE 202

INFINEON TECHNOLOGIES AG: COMPANY OVERVIEW

TABLE 203

INFINEON TECHNOLOGIES AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 204

INFINEON TECHNOLOGIES AG: PRODUCT LAUNCHES

TABLE 205

INFINEON TECHNOLOGIES AG: DEALS

TABLE 206

INFINEON TECHNOLOGIES AG: OTHER DEVELOPMENTS

TABLE 207

STMICROELECTRONICS: COMPANY OVERVIEW

TABLE 208

STMICROELECTRONICS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 209

STMICROELECTRONICS: PRODUCT LAUNCHES

TABLE 210

STMICROELECTRONICS: DEALS

TABLE 211

ADVANCED MICRO DEVICES, INC.: COMPANY OVERVIEW

TABLE 212

ADVANCED MICRO DEVICES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 213

ADVANCED MICRO DEVICES, INC.: PRODUCT LAUNCHES

TABLE 214

ADVANCED MICRO DEVICES, INC.: DEALS

TABLE 215

TEXAS INSTRUMENTS INCORPORATED: COMPANY OVERVIEW

TABLE 216

TEXAS INSTRUMENTS INCORPORATED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 217

TEXAS INSTRUMENTS INCORPORATED: PRODUCT LAUNCHES

TABLE 218

TEXAS INSTRUMENTS INCORPORATED: DEALS

TABLE 219

TEXAS INSTRUMENTS INCORPORATED: OTHER DEVELOPMENTS

TABLE 220

HONEYWELL INTERNATIONAL INC.: COMPANY OVERVIEW

TABLE 221

HONEYWELL INTERNATIONAL INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 222

HONEYWELL INTERNATIONAL INC.: PRODUCT LAUNCHES

TABLE 223

HONEYWELL INTERNATIONAL INC.: DEALS

TABLE 224

HONEYWELL INTERNATIONAL INC.: OTHER DEVELOPMENTS

TABLE 225

TELEDYNE TECHNOLOGIES INCORPORATED: COMPANY OVERVIEW

TABLE 226

TELEDYNE TECHNOLOGIES INCORPORATED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 227

TELEDYNE TECHNOLOGIES INCORPORATED: PRODUCT LAUNCHES

TABLE 228

TELEDYNE TECHNOLOGIES INCORPORATED: DEALS

TABLE 229

TELEDYNE TECHNOLOGIES INCORPORATED: OTHER DEVELOPMENTS

TABLE 230

TTM TECHNOLOGIES INC.: COMPANY OVERVIEW

TABLE 231

TTM TECHNOLOGIES INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 232

TTM TECHNOLOGIES INC.: PRODUCT LAUNCHES

TABLE 233

TTM TECHNOLOGIES INC.: OTHER DEVELOPMENTS

LIST OF FIGURES

FIGURE 1

RADIATION HARDENED ELECTRONICS MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

RADIATION HARDENED ELECTRONICS MARKET: DURATION CONSIDERED

FIGURE 3

RADIATION HARDENED ELECTRONICS MARKET: RESEARCH FLOW

FIGURE 4

RADIATION HARDENED ELECTRONICS MARKET: RESEARCH DESIGN

FIGURE 5

RADIATION HARDENED ELECTRONICS MARKET: RESEARCH APPROACH

FIGURE 6

DATA CAPTURED FROM SECONDARY SOURCES

FIGURE 7

CORE FINDINGS FROM INDUSTRY EXPERTS

FIGURE 8

BREAKDOWN OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

FIGURE 9

DATA CAPTURED FROM PRIMARY SOURCES

FIGURE 10

RADIATION HARDENED ELECTRONICS MARKET ESTIMATION

FIGURE 11

RADIATION HARDENED ELECTRONICS MARKET: BOTTOM-UP APPROACH

FIGURE 12

RADIATION HARDENED ELECTRONICS MARKET: TOP-DOWN APPROACH

FIGURE 13

RADIATION HARDENED ELECTRONICS MARKET: DATA TRIANGULATION

FIGURE 14

RADIATION HARDENED ELECTRONICS MARKET: RESEARCH ASSUMPTIONS

FIGURE 15

POWER MANAGEMENT SEGMENT TO HOLD LARGEST MARKET SHARE IN 2030

FIGURE 16

RADIATION HARDENED BY DESIGN (RHBD) TO DOMINATE MARKET FROM 2025 TO 2030

FIGURE 17

SPACE (SATELLITES) SEGMENT TO EXHIBIT HIGHEST CAGR BETWEEN 2025 AND 2030

FIGURE 18

NORTH AMERICA TO HOLD LARGEST MARKET SHARE IN 2025

FIGURE 19

INCREASING NUMBER OF COMMUNICATION SATELLITES TO PROPEL RADIATION HARDENED ELECTRONICS MARKET

FIGURE 20

COMMERCIAL-OFF-THE-SHELF SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE IN 2025

FIGURE 21

RADIATION HARDENED BY DESIGN (RHBD) SEGMENT TO DOMINATE MARKET FROM 2025 TO 2030

FIGURE 22

MEMORY SEGMENT TO COMMAND HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 23

CHINA TO RECORD HIGHEST CAGR IN GLOBAL RADIATION HARDENED ELECTRONICS MARKET FROM 2025 TO 2030

FIGURE 24

EVOLUTION OF RADIATION-HARDENED ELECTRONICS TECHNOLOGY

FIGURE 25

DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 26

DRIVERS: IMPACT ANALYSIS

FIGURE 27

RESTRAINTS: IMPACT ANALYSIS

FIGURE 28

OPPORTUNITIES: IMPACT ANALYSIS

FIGURE 29

CHALLENGES: IMPACT ANALYSIS

FIGURE 30

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 31

AVERAGE SELLING PRICE OF POWER MANAGEMENT COMPONENTS OFFERED BY KEY PLAYERS, 2024

FIGURE 32

VALUE CHAIN ANALYSIS

FIGURE 33

RADIATION HARDENED ELECTRONICS ECOSYSTEM

FIGURE 34

INVESTMENT AND FUNDING SCENARIO, 2019–2024

FIGURE 35

PORTER’S FIVE FORCES ANALYSIS

FIGURE 36

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

FIGURE 37

KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

FIGURE 38

IMPORT DATA FOR HS CODE 8541-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2020–2024

FIGURE 39

EXPORT DATA FOR HS CODE 8541-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2020–2024

FIGURE 40

PATENTS APPLIED AND GRANTED, 2015–2024

FIGURE 41

KEY AI USE CASES IN RADIATION HARDENED ELECTRONICS MARKET

FIGURE 42

POWER MANAGEMENT SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2030

FIGURE 43

RADIATION HARDENED BY DESIGN (RHBD) SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

FIGURE 44

COMMERCIAL-OFF-THE-SHELF SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

FIGURE 45

SPACE (SATELLITES) SEGMENT TO REGISTER HIGHEST CAGR BETWEEN 2025 AND 2030

FIGURE 46

CHINA TO GROW AT HIGHEST CAGR IN GLOBAL MARKET FROM 2025 TO 2030

FIGURE 47

NORTH AMERICA TO DOMINATE MARKET DURING FORECAST PERIOD

FIGURE 48

NORTH AMERICA: MARKET SNAPSHOT

FIGURE 49

EUROPE: MARKET SNAPSHOT

FIGURE 50

ASIA PACIFIC: MARKET SNAPSHOT

FIGURE 51

RADIATION HARDENED ELECTRONICS MARKET: REVENUE ANALYSIS OF TOP FOUR PLAYERS, 2021–2024

FIGURE 52

MARKET SHARE ANALYSIS OF COMPANIES OFFERING RADIATION HARDENED ELECTRONICS, 2024

FIGURE 53

COMPANY VALUATION

FIGURE 54

FINANCIAL METRICS (EV/EBITDA)

FIGURE 55

BRAND COMPARISON

FIGURE 56

RADIATION HARDENED ELECTRONICS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 57

RADIATION HARDENED ELECTRONICS MARKET: COMPANY FOOTPRINT

FIGURE 58

RADIATION HARDENED ELECTRONICS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 59

MICROCHIP TECHNOLOGY INC.: COMPANY SNAPSHOT

FIGURE 60

BAE SYSTEMS: COMPANY SNAPSHOT

FIGURE 61

RENESAS ELECTRONICS CORPORATION: COMPANY SNAPSHOT

FIGURE 62

INFINEON TECHNOLOGIES AG: COMPANY SNAPSHOT

FIGURE 63

STMICROELECTRONICS: COMPANY SNAPSHOT

FIGURE 64

ADVANCED MICRO DEVICES, INC.: COMPANY SNAPSHOT

FIGURE 65

TEXAS INSTRUMENTS INCORPORATED: COMPANY SNAPSHOT

FIGURE 66

HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

FIGURE 67

TELEDYNE TECHNOLOGIES INCORPORATED: COMPANY SNAPSHOT

FIGURE 68

TTM TECHNOLOGIES INC.: COMPANY SNAPSHOT

Methodology

The study involved four major activities in estimating the size of the radiation hardened electronics market. Exhaustive secondary research has been done to collect information on the market, peer market, and parent market. Validation of these findings, assumptions, and sizing with industry experts across the value chain through primary research has been the next step. Both top-down and bottom-up approaches have been employed to estimate the global market size. After that, market breakdown and data triangulation have been used to estimate the market sizes of segments and subsegments.

Secondary Research

The secondary research process has referred to various secondary sources to identify and collect necessary information for this study. The secondary sources include annual reports, press releases, and investor presentations of companies; white papers; journals and certified publications; and articles from recognized authors, websites, directories, and databases. Secondary research was conducted to obtain critical information about the industry’s supply chain, the market’s value chain, the total pool of key players, market segmentation according to the industry trends (to the bottom-most level), regional markets, and key developments from market- and technology-oriented perspectives. The secondary data was collected and analyzed to determine the overall market size, further validated by primary research.

Primary Research

Extensive primary research was conducted after gaining knowledge about the current scenario of the radiation hardened electronics market through secondary research. Several primary interviews were conducted with experts from the demand and supply sides across four major regions—North America, Europe, Asia Pacific, and RoW. This primary data was collected through questionnaires, emails, and telephonic interviews.

Note: Other designations include technology heads, media analysts, sales managers, marketing managers, and product managers.

The three tiers of the companies are based on their total revenues as of 2024 ? Tier 1: >USD 1 billion, Tier 2: USD 500 million–1 billion, and Tier 3: USD 500 million.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

In the complete market engineering process, top-down and bottom-up approaches and several data triangulation methods were used to estimate and forecast the overall market segments and subsegments listed in this report. Key players in the market were identified through secondary research, and their market shares in the respective regions were determined through primary and secondary research. This entire procedure includes the study of annual and financial reports of the top market players and extensive interviews for key insights (quantitative and qualitative) with industry experts (CEOs, VPs, directors, and marketing executives).

All percentage shares, splits, and breakdowns were determined using secondary sources and verified through primary sources. All the parameters affecting the markets covered in this research study were accounted for, viewed in detail, verified through primary research, and analyzed to obtain the final quantitative and qualitative data. This data was consolidated and supplemented with detailed inputs and analysis from MarketsandMarkets and presented in this report. The following figure represents this study’s overall market size estimation process.

Bottom-Up Approach

- Identifying the players in the radiation hardened electronics market that influence the global market, along with their offerings

- Analyzing major manufacturers of radiation-hardened electronics, studying their portfolios, and understanding several types of products based on their features and functions

- Analyzing trends pertaining to the usage of radiation-hardened electronics in end-use industries, such as space, aerospace & defense, nuclear power plants, medical, and others (scientific research and education)

- Tracking ongoing and upcoming developments in the market, such as investments made, R&D activities, product launches, acquisitions, partnerships, agreements, contracts, and expansions, and forecasting the market based on these developments and other critical parameters

- Conducting multiple discussions with key opinion leaders to understand different types of radiation-hardened electronic components, manufacturing techniques, product types, applications, and current trends in the market, and analyzing the breakup of the scope of work carried out by major manufacturing companies

- Arriving at market estimates by analyzing the revenue of these companies generated from different types of components and then combining the same to arrive at the market estimate by region

- Verifying and cross-checking the estimates at every level through discussions with key opinion leaders, such as CXOs, directors, and operations managers, and finally with the domain experts at MarketsandMarkets

- Studying various paid and unpaid sources of information, such as annual reports, press releases, white papers, and databases.

Top-Down Approach

- In the top-down approach, the overall market size was used to estimate the size of individual markets (mentioned in the market segmentation) through percentage splits obtained from secondary and primary research.

- For calculating the size of specific market segments, the parent market size was considered when implementing the top-down approach. The bottom-up approach was also implemented for data extracted from secondary research to validate the market size of different segments.

- The market share of each company was estimated to verify the revenue share used in the bottom-up approach earlier. With data triangulation and data validation through primaries, this study determined and confirmed the size of the parent market and each segment.

Radiation Hardened Electronics Market : Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall market size, the market was split into several segments and subsegments using the market size estimation processes explained above. Data triangulation and market breakdown procedures were employed to complete the entire market engineering process and determine each market segment’s and subsegment’s exact statistics. The data was triangulated by studying various factors and trends from the demand and supply sides in the radiation hardened electronics market.

Market Definition

Radiation hardening is the development of electronic components and systems resistant to destruction caused by ionizing radiation (particle radiation and high-energy electromagnetic radiation) occurring in outer space, high-altitude flights, around nuclear reactors, particle accelerators, during nuclear accidents, or nuclear warfare. Most semiconductor electronic components are susceptible to damage by radiation. Radiation-hardened components are based on hardened equivalents, with some design and manufacturing variations that reduce their susceptibility to damage by radiation. The ecosystem of the radiation hardened electronics market comprises manufacturers and distributors of radiation-hardened components. This market is competitive and diversified, with over 25 companies competing across its value chain to sustain their positions and increase their share. The market is expected to grow significantly in the coming years, owing to the increasing deployment of communication and military satellites in space.

Key Stakeholders

- Associations and Regulatory Authorities

- Government Bodies, Venture Capitalists, and Private Equity Firms

- Original Equipment Manufacturers (OEMs)

- Semiconductor Component Suppliers

- Radiation-hardened Equipment Distributors and Sales Firms

- Software Solution Providers

- Radiation-hardened Electronic Component and System Integrators

- Research Institutes and Organizations

Report Objectives

- To describe and forecast the size of the radiation hardened electronics market, by component, manufacturing technique, product type, and application, in terms of value

- To analyze the material selection and packaging types utilized in the market

- To describe and forecast the market size for various segments in four key regions, namely, North America, Europe, Asia Pacific, and RoW, in terms of value

- To provide detailed information regarding the key drivers, restraints, opportunities, and challenges influencing the growth of the radiation hardened electronics market

- To analyze micromarkets with respect to individual growth trends, prospects, and contribution to the total market

- To analyze the opportunities in the market for various stakeholders by identifying its high-growth segments

- To profile the key players and comprehensively analyze their ranking and core competencies, along with a detailed competitive landscape for market leaders

- To map competitive intelligence based on company profiles, key player strategies, and game-changing developments, such as product launches/developments, partnerships, collaborations, and acquisitions, undertaken in the market

- To understand and analyze the impact of the 2025 US tariff on the radiation hardened electronics market

- To understand and analyze the macroeconomic outlook for North America, Europe, Asia Pacific, and RoW regions

- To understand the impact of AI/Gen AI on radiation hardened electronics market

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

- Detailed analysis and profiling of additional market players based on various blocks of the supply chain

Key Questions Addressed by the Report

What is the current market size of the radiation hardened electronics market?

The market is valued at approximately USD 1.77 billion in 2025 (with ~USD 1.69 billion in 2024).

What is the projected market size by 2030?

The market is expected to reach USD 2.30 billion by 2030.

What is the CAGR of the radiation hardened electronics market?

The market is projected to grow at a CAGR of 5.4% from 2025 to 2030.

What are the key growth drivers of this market?

Growth is driven by increasing satellite launches, ISR (intelligence, surveillance & reconnaissance) activities, and rising investments in defense and space technologies.

Which industries are major users of radiation hardened electronics?

Key industries include space (satellites), aerospace & defense, nuclear power plants, and medical applications.

What are the major market trends?

Trends include adoption of radiation-hardened-by-design (RHBD), increasing use of commercial-off-the-shelf (COTS) components, and development of advanced multicore processors.

Which region dominates the market?

North America holds the largest share, while Asia Pacific is the fastest-growing region due to expanding space programs and defense investments.

Who are the key companies in the market?

Major players include Microchip Technology Inc., BAE Systems, Renesas Electronics Corporation, Infineon Technologies AG, and STMicroelectronics.

What are the key opportunities in the market?

Opportunities include growth in commercial satellite deployment, deep-space exploration, nuclear energy systems, and adoption of cost-effective COTS solutions.

What does the report analysis cover?

The report covers market size, forecasts, segmentation (component, application, product), regional analysis, competitive landscape, and strategic developments across 285 pages and 233 tables.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Radiation Hardened Electronics Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

Growth opportunities and latent adjacency in Radiation Hardened Electronics Market

Eric

Apr, 2026

Are emerging components such as MRAM and new FPGA/ASIC solutions analyzed for future growth potential?.

Zachary

Apr, 2026

What are the key emerging trends driving future growth (e.g., New Space programs, small satellites, nanosats, AI integration)?.

Sophia

Apr, 2026

Does the report provide ASP trends, pricing evolution, and margin impact for growth forecasting?.