China Industrial Control & Factory Automation Market (2025-2030)

The China Industrial Control & Factory Automation Market was valued at $50688.7 Million in 2025 and projected to reach to $68973.7 Million by 2030, representing a compound annual growth rate of CAGR 10.3%. China's Industrial Control & Factory Automation market is positioned for sustained high-growth trajectory through 2030, driven by structural economic shifts and technological modernization.

| Market Size in | USD 26.32 MN |

| Market Forecast in | |

| CAGR | |

| Forecast Period | |

| Units Considered | Value (USD MN) |

China Industrial Control & Factory Automation Market Trends and Insights

- This robust expansion reflects China's position as a global manufacturing powerhouse and its strategic investments in Industry 4.0 technologies.

- China's market growth outpaces the global average of 9.6%, driven by accelerating digital transformation across manufacturing sectors and government initiatives promoting smart factory adoption. The acceleration in China's industrial automation adoption is fueled by rising labor costs, supply chain resilience demands, and competitive pressures in export-oriented industries.

- China's manufacturing base increasingly integrates advanced control systems, IoT-enabled devices, and AI-driven automation solutions to enhance productivity and reduce operational costs.

- Between 2025 and 2030, China is expected to consolidate its leadership in factory automation deployment, with particular strength in automotive, electronics, and chemical processing sectors. China's market dynamics are shaped by both domestic consumption and export-driven manufacturing requirements.

- The country's emphasis on technological self-sufficiency and semiconductor localization further supports growth in industrial control systems.

- China's competitive advantage in cost-effective automation solutions positions it as both a major market and a key supplier to global industrial automation demand..

Key Market Statistics

- CAGR (2025-2030) CAGR 10.3%

- Market Size, 2025 ~USD 50688.7 Million

- Forecast, 2030 ~USD 68973.7 Million

- Country China

China Industrial Control & Factory Automation Market Overview

Market Leadership Position :

China dominates the global Industrial Control & Factory Automation market with a USD 50.7 billion valuation in 2025, driven by its status as the world's largest manufacturing hub and aggressive Industry 4.0 adoption across multiple sectors.

Outpacing Global Growth :

China's 10.3% CAGR significantly exceeds the global average of 9.6%, reflecting accelerated digital transformation initiatives, government support for smart manufacturing, and increased automation investments in traditional industries.

Substantial Market Expansion :

The market is projected to grow from USD 50.7 billion in 2025 to USD 69.0 billion by 2030, representing a USD 18.3 billion increase driven by rising labor costs, technological advancement, and competitive manufacturing pressures.

Strategic Government Initiatives :

China's Made in China 2025 and dual circulation strategy prioritize automation and intelligent manufacturing, creating favorable policy environments and substantial investments in factory automation technologies across automotive, electronics, and chemical sectors.

China Industrial Control & Factory Automation Market Dynamics

- The nation's manufacturing sector faces mounting pressure to increase productivity amid rising labor costs, making automation investments critical for competitiveness.

- Government policies actively supporting Industry 4.0 adoption, coupled with domestic technological capabilities in robotics and control systems, create a favorable ecosystem for market expansion. The forecast period will witness accelerated adoption of AI-enabled automation, IoT integration, and advanced process control systems across manufacturing verticals.

- Regional disparities between developed coastal regions and inland areas will drive uneven growth patterns, with eastern manufacturing hubs leading adoption.

- Strategic partnerships between domestic automation providers and multinational corporations will intensify, while supply chain resilience initiatives will further boost demand for sophisticated control systems and factory automation solutions..

Related Ecosystem

Locomotives And Rolling Stock

- Sensors

- Passenger Information System (PIS)

- Cartesian Robots

- Flow Sensors

- Gas Sensors

- Siemens ag

- Alstom s.a.

- Hitachi, Ltd.

- Knorr-bremse ag

- RAILPROS

Industrial Automation

- Sensors

- Image Sensors

- Manufacturing Execution System (MES)

- Actuators

- Flow Sensors

- Siemens ag

- ABB India Limited

- Emerson Electric Co.

- HONEYWELL INTERNATIONAL INC.

- SCHNEIDER ELECTRIC SE

Industrial Iot

- Sensors

- Pressure Sensors

- Flow Sensors

- Gas Sensors

- Image Sensors

- Siemens ag

- ABB India Limited

- HONEYWELL INTERNATIONAL INC.

- Emerson Electric Co.

- SCHNEIDER ELECTRIC SE

Key Takeaways

- China's Industrial Control & Factory Automation Market will grow from USD 50.7B (2025) to USD 69.0B (2030) at a 10.3% CAGR, outpacing global growth.

- China's market expansion is driven by Industry 4.0 adoption, rising labor costs, and government-backed smart manufacturing initiatives.

- China dominates automation deployment in automotive, electronics, and chemical processing sectors with advanced control and IoT integration.

- China's emphasis on semiconductor localization and supply chain resilience strengthens domestic industrial control system development and adoption.

Industrial Control & Factory Automation Market Report Scope

| Report Metric | Details |

|---|---|

| Base Year | 2025 |

| Fastest Growing Segment | INDUSTRIAL 3D PRINTING (Component) |

| Forecast Period | 2025�2030 |

| Growth Rate | CAGR of 9.6% from 2025 to 2030 |

| Largest Segment | INDUSTRIAL SOFTWARE (Component) |

| Market Size Base Year (Billions) | ~USD 275.22 (2025) |

| Revenue Forecast (Billions) | ~USD 435.24 (2030) |

| Segments Covered | Component, Type, Industry, Offering, Software, Service, Hardware Type, Software Deployment Mode, Deployment, Tier Type, Software Deployment |

China Industrial Control & Factory Automation Market Report Segmentation

11 segment dimensions are covered across the global market.

By Component

- Cnc Controllers

- Field Instrumentation

- Flow Meters

- Industrial 3D Printing

- Industrial Communication

- Industrial Control Systems

- Industrial Monitoring & Safety

- Industrial Robotics

- Industrial Software

- Process Analyzers

By Type

- Cloud Enterprise Resource Planning

- Din Rail Ipcs

- Distributed Control Systems

- Embedded Ipcs

- Human Machine Interface

- Industrial Pcs

- Manufacturing Execution System

- Manufacturing Operation Management

- Panel Ipcs

- Plant Asset Management

- Programmable Logic Controllers

- Quality Management System

- Rack Mount Ipcs

- Supervisory Control And Data Acquisition Systems

- Warehouse Management System

By Industry

- Aerospace

- Automotive

- Chemicals

- Energy & Power

- Energy And Power

- Food & Beverages

- Food And Beverages

- Heavy Machinery

- Medical Devices

- Metal & Mining

- Metals & Mining

- Oil & Gas

- Other Industries

- Pharmaceuticals

- Pulp & Paper

- Semiconductors & Electronics

By Offering

- Hardware

- Professional Services

- Services

- Software

- Software & Services

By Software

- Cloud-Based

- On-Premises

By Service

- Managed Services

- Professional Services

By Hardware Type

- Advanced Panel-Based Hmi

- Advanced Pc-Based Hmi

- Basic Hmi

- Others Hardware Types

By Software Deployment Mode

- Cloud-Based

- On-Premises

By Deployment

- Cloud

- Cloud-Based

- Hybrid

- On-Premises

By Tier Type

- Advanced (Tier 1)

- Basic (Tier 3)

- Intermediate (Tier 2)

By Software Deployment

- Hybrid

- Private

- Public

Target Audience

- Manufacturing Equipment Suppliers : Manufacturers of industrial control systems, PLCs, and factory automation equipment need China-specific market data to assess demand trajectories, competitive intensity, and regional growth opportunities within the world's largest manufacturing economy.

- Technology & Software Providers : Automation software, IoT platforms, and AI-enabled control system vendors require detailed China market insights to evaluate addressable market size, adoption rates, and integration opportunities with local manufacturing ecosystems.

- Investment & Private Equity Firms : Investors evaluating automation sector opportunities in Asia need China market valuations and growth forecasts to assess portfolio companies, identify acquisition targets, and benchmark returns against regional and global benchmarks.

- Strategic Consultants & Analysts : Management consultants advising manufacturing clients on digital transformation strategies require authoritative China market data to validate business cases, support investment recommendations, and guide Industry 4.0 implementation roadmaps.

- Government & Trade Organizations : Policy makers, trade associations, and economic development agencies need market intelligence on China's automation sector to inform industrial policy, identify competitive gaps, and support domestic technology provider development initiatives.

Key Companies in the China Industrial Control & Factory Automation Market

| Company | HQ | Ownership | Strongest segments |

|---|---|---|---|

| EMERSON ELECTRIC CO. | United States | Public Company | Final Control,Measurement & Analytical,Discrete Automation, |

| YOKOGAWA ELECTRIC CORPORATION | Japan | Public Company | Control Business (DCS, PLC, SCADA, software, lifecycle services),Field Instruments (flow, pressure, analyzers, recorders),Measuring Instruments (waveform, optical communications, signal generators), |

| FANUC CORPORATION | Japan | Public Company | Industrial robots,CNC systems and servo motors,Robomachines (machining centers, injection molding, wire EDM), |

| MITSUBISHI ELECTRIC CORPORATION | Japan | Public Company | Factory Automation (FA) systems and industrial solutions,Building systems, air conditioning, and refrigeration,Infrastructure, energy, and public utility systems, |

| OMRON CORPORATION | Japan | Public Company | Industrial Automation (sensors, safety, motion, robotics, control),Device & Module Solutions (relays, switches, connectors, components),Healthcare (cardiovascular, respiratory, pain, remote monitoring), |

| GE VERNOVA | United States | Public Company | Power (gas, nuclear, hydro, steam),Wind (onshore and offshore),Electrification (grid, power conversion, software, solar & storage), |

| FUJI ELECTRIC CO., LTD. | Japan | Public Company | Power Semiconductors,Drives, Motors, and Controls,Power Supply and UPS/Data Center Solutions, |

| HITACHI, LTD. | Japan | Public Company | Digital Systems & Services (IT, cloud, integration, ATMs),Green Energy & Mobility (power grids, energy, rail),Connective Industries (automation, industrial equipment, e-mobility), |

EMERSON ELECTRIC CO.

Emerson Electric Co. is a United States-based public company founded in 1890 with 71,000 employees. The company operates in industrial automation, climate technologies, and process management solutions.

YOKOGAWA ELECTRIC CORPORATION

Yokogawa Electric Corporation is a Japanese public company founded in 1915 with 18,313 employees. It specializes in industrial automation, control systems, and measurement technologies.

FANUC CORPORATION

FANUC Corporation is a Japanese public company founded in 1950 with 10,040 employees. The company is a leading manufacturer of industrial robots and factory automation systems.

MITSUBISHI ELECTRIC CORPORATION

Mitsubishi Electric Corporation is a Japanese public company founded in 1921 with 150,386 employees. It operates across multiple sectors including industrial automation, power systems, and electronic equipment manufacturing.

OMRON CORPORATION

Omron Corporation is a Japanese public company founded in 1933 with 26,050 employees. The company specializes in automation technology, sensing, and control systems for industrial applications.

GE VERNOVA

GE Vernova is a United States-based public company founded in 2023 with 78,000 employees. It focuses on energy infrastructure and industrial solutions.

FUJI ELECTRIC CO., LTD.

Fuji Electric Co., Ltd. is a Japanese public company founded in 1923 with 26,955 employees. The company manufactures power electronics, industrial systems, and automation equipment.

HITACHI, LTD.

Hitachi, Ltd. is a Japanese public company founded in 1910 with 287,901 employees. It is a diversified conglomerate operating in industrial systems, power generation, and digital solutions.

Reasons to Buy this Report

- Market Size & Growth Validation : Access precise market valuations for China (USD 50.7B in 2025, USD 69.0B in 2030) with verified CAGR of 10.3%, enabling accurate financial forecasting and investment decision-making specific to the Chinese market.

- Competitive Benchmarking : Compare China's 10.3% growth rate against the global 9.6% CAGR to identify market outperformance drivers and competitive advantages, informing strategic positioning and resource allocation in this high-growth region.

- Sector-Specific Opportunity Identification : Understand China's unique automation adoption patterns across automotive, electronics, chemicals, and other manufacturing verticals to identify high-potential segments and tailor product-market fit strategies accordingly.

- Policy & Regulatory Landscape Insights : Gain intelligence on Made in China 2025 initiatives and government support mechanisms driving automation investments, enabling proactive compliance strategies and identification of policy-backed growth opportunities.

- Regional Market Dynamics : Leverage China-specific data to understand coastal versus inland regional disparities, supply chain resilience trends, and domestic technology provider competition to optimize market entry and expansion strategies.

Frequently asked questions

What is the market size of Industrial Control & Factory Automation in China?

China's Industrial Control & Factory Automation Market is valued at USD 50,688.7 million in 2025 and is projected to reach USD 68,973.7 million by 2030.

What is the CAGR for China's Industrial Control & Factory Automation Market?

China's market is expected to grow at a compound annual growth rate (CAGR) of 10.3% from 2025 to 2030, exceeding the global CAGR of 9.6%.

What are the primary drivers of growth in China's industrial automation market?

China's growth is driven by Industry 4.0 adoption, rising labor costs, government smart manufacturing initiatives, supply chain resilience demands, and semiconductor localization efforts.

Which industries in China are leading automation adoption?

China's automotive, electronics, and chemical processing sectors are leading the adoption of advanced industrial control systems and factory automation technologies.

How does China's market growth compare to global trends?

China's 10.3% CAGR outpaces the global average of 9.6%, reflecting China's accelerated digital transformation and manufacturing modernization efforts.

RESEARCH METHODOLOGY

The study involved major activities in estimating the current market size for the industrial control & factory automation market. Exhaustive secondary research was done to collect information on the industrial control & factory automation industry. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain using primary research. Different approaches, such as top-down and bottom-up, were employed to estimate the total market size. After that, the market breakup and data triangulation procedures were used to estimate the market size of the segments and subsegments of the industrial control & factory automation market.

Secondary Research

The market for the companies offering industrial control & factory automation solutions is arrived at by secondary data available through paid and unpaid sources, analyzing the product portfolios of the major companies in the ecosystem, and rating the companies by their performance and quality. Various sources were referred to in the secondary research process to identify and collect information for this study. The secondary sources include annual reports, press releases, investor presentations of companies, white papers, journals, certified publications, and articles from recognized authors, directories, and databases. In the secondary research process, various secondary sources were referred to for identifying and collecting information related to the study. Secondary sources included annual reports, press releases, and investor presentations of blockchain vendors, forums, certified publications, and whitepapers. The secondary research was used to obtain critical information on the industry's value chain, the total pool of key players, market classification, and segmentation from the market and technology-oriented perspectives.

Primary Research

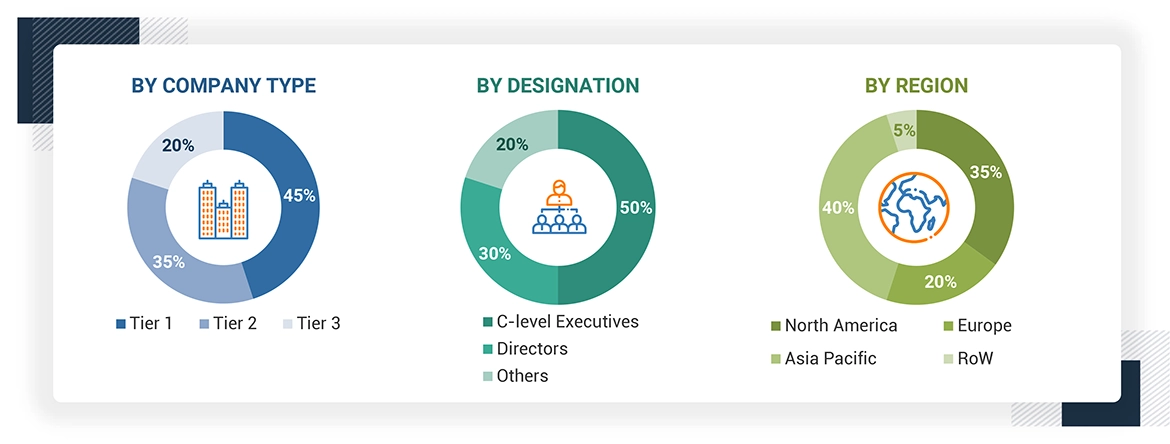

Extensive primary research has been conducted after understanding and analyzing the current scenario of the industrial control & factory automation market through secondary research. Several primary interviews have been conducted with the key opinion leaders from the demand and supply sides across four main regions—North America, Europe, Asia Pacific, and the Rest of Europe. Approximately 25% of the primary interviews were conducted with the demand-side respondents, while approximately 75% were conducted with the supply-side respondents. The primary data has been collected through questionnaires, emails, and telephone interviews.

After interacting with industry experts, brief sessions were conducted with highly experienced independent consultants to reinforce the findings from our primary. This, along with the in-house subject matter experts’ opinions, has led us to the findings as described in the remainder of this report. The breakdown of primary respondents is as follows:

About the assumptions considered for the study, To know download the pdf brochure

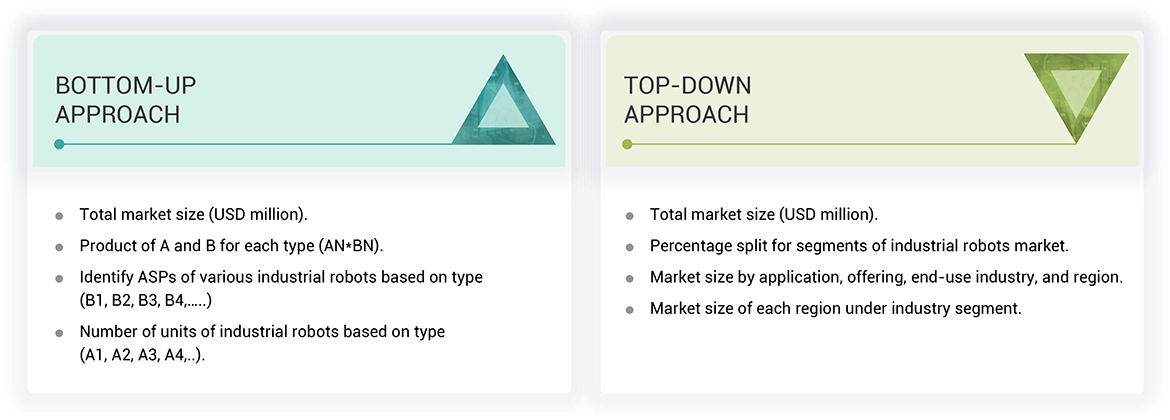

Market Size Estimation

Both top-down and bottom-up approaches wete used to estimate and validate the total size of the industrial control & factory automation market. These methods were also used extensively to estimate the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

Industrial Control & Factory Automation Market : Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall market size using the market size estimation processes as explained above, the market was split into several segments and subsegments. The data triangulation and market breakdown procedures were employed, wherever applicable, to complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment. The data was triangulated by studying various factors and trends from the demand and supply sides.

Market Definition

Industrial control & factory automation is a highly digitalized and connected production system that can self-optimize performance across a broad network, self-adapt in various conditions in real time, and autonomously run an entire production process. The major advantage of industrial control & factory automation is its ability to evolve with the changing needs of organizations. Industrial control & factory automation uses a network to connect the virtual and physical elements of production processes to actual manufacturing operations. It helps to create an autonomous manufacturing environment that can handle any technical issues during real-time production, using fragmented information and communication structures to optimize production processes.

Key Stakeholders

- End users

- Government bodies, venture capitalists, and private equity firms

- Manufacturers of industrial control & factory automation components

- Distributors of industrial control & factory automation components and solutions

- Industrial control & factory automation industry associations

- Professional service/solution providers

- Research institutions and organizations

- Standards organizations and regulatory authorities related to the industrial control & factory automation market

- System integrators

- Technology consultants

Report Objectives

- To describe and forecast the industrial control and factory automation market, in terms of value, based on component , and industry

- To forecast the industrial control and factory automation market, in terms of volume, by component

- To forecast the market size, in terms of value, for four main regions—North America, Europe, Asia Pacific, and the RoW.

- To provide detailed information regarding drivers, restraints, opportunities, and challenges influencing the market growth

- To provide a detailed overview of the value chain of the industrial control and factory automation ecosystem

- To strategically analyze micromarkets1 with respect to individual growth trends, prospects, and contributions to the total market

- To provide a detailed overview of the industrial control and factory automation market value chain

- To provide an ecosystem analysis, case study analysis, key conferences, patent analysis, trade analysis, technology analysis, average selling price (ASP) analysis, Porter’s five forces analysis, buying criteria, and regulations pertaining to the market

- To track and analyze competitive developments undertaken by key players in the industrial control and factory automation market

- To profile key players and analyze their market share, core competencies2, and detailed competitive landscape for market leaders

- To benchmark market players using the company evaluation matrix, analyzing players based on various parameters within broad business categories and product strategies.

- To analyze strategies, such as product launches, acquisitions, partnerships, and expansions, adopted by the players in the industrial control and factory automation market

- To study the impact of AI on the market under study, along with the macroeconomic outlook for each region

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

- Detailed analysis and profiling of additional market players based on various blocks of the supply chain

Get the Full Industrial Control & Factory Automation Market Report

Full forecast, segment splits, and company analysis for all Industrial Control & Factory Automation Market.

- North America Industrial Control & Factory Automation Market

- Europe Industrial Control & Factory Automation Market

- Asia Pacific Industrial Control & Factory Automation Market

- Rest of World Industrial Control & Factory Automation Market

- Scada Industrial Control & Factory Automation Market

- Dcs Industrial Control & Factory Automation Market

- Plc Industrial Control & Factory Automation Market

- Industrial Pc Industrial Control & Factory Automation Market

- Hmi Industrial Control & Factory Automation Market

- Mes Industrial Control & Factory Automation Market

- Pam Industrial Control & Factory Automation Market

- Wms Industrial Control & Factory Automation Market

- South America Industrial Control & Factory Automation Market

- Mom Industrial Control & Factory Automation Market

- Cloud Erp Industrial Control & Factory Automation Market

- Qms Industrial Control & Factory Automation Market

- Canada Industrial Control & Factory Automation Market

- Mexico Industrial Control & Factory Automation Market

- US Industrial Control & Factory Automation Market

- Germany Industrial Control & Factory Automation Market

- France Industrial Control & Factory Automation Market

- Rest Of Europe Industrial Control & Factory Automation Market

- UK Industrial Control & Factory Automation Market

- India Industrial Control & Factory Automation Market

- Japan Industrial Control & Factory Automation Market

- Rest Of Asia Pacific Industrial Control & Factory Automation Market

- Italy Industrial Control & Factory Automation Market

- South America Industrial Control & Factory Automation Market

- GCC Industrial Control & Factory Automation Market

- Brazil Industrial Control & Factory Automation Market

- Rest Of South America Industrial Control & Factory Automation Market

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report