South America Industrial Control & Factory Automation Market (2025-2030)

The South America Industrial Control & Factory Automation Market was valued at $26529.6 Million in 2025 and projected to reach to $34868.6 Million by 2030, representing a compound annual growth rate of 9.1%. South America's Industrial Control & Factory Automation market is poised for sustained growth as manufacturers increasingly adopt advanced automation technologies to enhance productivity and competitiveness.

| Market Size in | USD 26.32 MN |

| Market Forecast in | |

| CAGR | |

| Forecast Period | |

| Units Considered | Value (USD MN) |

South America Industrial Control & Factory Automation Market Trends and Insights

- Germany's strong manufacturing heritage and commitment to Industry 4.0 digital transformation initiatives position the country as a critical hub for advanced automation technologies.

- The market in Germany is driven by increasing demand for smart factory solutions, IoT-enabled control systems, and real-time production monitoring across automotive, chemical, and machinery sectors. Germany's industrial base continues to invest heavily in modernizing legacy systems and deploying next-generation automation platforms to enhance operational efficiency and reduce downtime.

- The forecast period from 2025 to 2030 reflects Germany's strategic focus on sustainable manufacturing and competitive advantage through technological innovation.

- Germany's market growth is supported by robust R&D spending, skilled workforce availability, and favorable government policies promoting digital manufacturing adoption across small, medium, and large enterprises..

Key Market Statistics

- CAGR (2025-2030) 9.1% CAGR

- Market Size, 2025 ~USD 26529.6 Million

- Forecast, 2030 ~USD 34868.6 Million

- Country South America

South America Industrial Control & Factory Automation Market Overview

Regional Growth Momentum :

South America's Industrial Control & Factory Automation market is expanding at 9.1% CAGR, driven by increasing manufacturing modernization and digital transformation initiatives across Brazil, Argentina, and Chile.

Market Valuation :

The region is valued at USD 26,529.6 million in 2025, with projections reaching USD 34,868.6 million by 2030, reflecting strong investment in automation infrastructure and smart factory technologies.

Manufacturing Sector Expansion :

South America's robust mining, automotive, and food processing industries are primary drivers of automation adoption, creating substantial demand for advanced control systems and IoT-enabled factory solutions.

Digital Transformation Adoption :

Increasing government support for Industry 4.0 initiatives and rising labor costs are accelerating the shift toward automated production systems across South American manufacturing hubs.

South America Industrial Control & Factory Automation Market Dynamics

- The region's diverse industrial base�spanning mining, automotive, food and beverage, and chemical sectors�creates multiple expansion opportunities for control systems and factory automation solutions.

- Brazil's dominance as the largest market is complemented by growing investments in Argentina and Chile, where digital transformation initiatives are gaining momentum.

- Rising labor costs and the need for operational efficiency are compelling manufacturers to invest in automated production lines and smart factory infrastructure.

- Government incentives and regional trade agreements further support market expansion through 2030..

Related Ecosystem

Locomotives And Rolling Stock

- Sensors

- Passenger Information System (PIS)

- Cartesian Robots

- Flow Sensors

- Gas Sensors

- Siemens ag

- Alstom s.a.

- Hitachi, Ltd.

- Knorr-bremse ag

- RAILPROS

Industrial Automation

- Sensors

- Image Sensors

- Manufacturing Execution System (MES)

- Actuators

- Flow Sensors

- Siemens ag

- ABB India Limited

- Emerson Electric Co.

- HONEYWELL INTERNATIONAL INC.

- SCHNEIDER ELECTRIC SE

Industrial Iot

- Sensors

- Pressure Sensors

- Flow Sensors

- Gas Sensors

- Image Sensors

- Siemens ag

- ABB India Limited

- HONEYWELL INTERNATIONAL INC.

- Emerson Electric Co.

- SCHNEIDER ELECTRIC SE

Key Takeaways

- Germany's Industrial Control & Factory Automation Market will expand from USD 26.5B (2025) to USD 34.9B (2030) at a 9.1% CAGR.

- Germany's Industry 4.0 initiatives and digital transformation roadmap are primary catalysts for market growth through 2030.

- Germany's automotive and machinery sectors drive the majority of control system and automation technology adoption.

- Germany's competitive advantage relies on innovation, skilled engineering talent, and integration of AI-powered predictive maintenance solutions.

Industrial Control & Factory Automation Market Report Scope

| Report Metric | Details |

|---|---|

| Base Year | 2025 |

| Fastest Growing Segment | INDUSTRIAL 3D PRINTING (Component) |

| Forecast Period | 2025�2030 |

| Growth Rate | CAGR of 9.6% from 2025 to 2030 |

| Largest Segment | INDUSTRIAL SOFTWARE (Component) |

| Market Size Base Year (Billions) | ~USD 275.22 (2025) |

| Revenue Forecast (Billions) | ~USD 435.24 (2030) |

| Segments Covered | Component, End-Use Industry, Type, Industry, Offering, Software, Service, Industrial Software, Industrial Robotics, Product Type, Hardware Type, Software Deployment Mode, Industrial Monitoring & Safety, Deployment, Tier Type, Software Deployment |

South America Industrial Control & Factory Automation Market Report Segmentation

16 segment dimensions are covered across the global market.

By Component

- Cnc Controller

- Cnc Controllers

- Field Instrumentation

- Flow Meter

- Flow Meters

- Industrial 3D Printing

- Industrial Communication

- Industrial Control Systems

- Industrial Monitoring & Safety

- Industrial Robotics

- Industrial Software

- Process Analyzer

- Process Analyzers

By End-Use Industry

- Aerospace

- Automotive

- Chemicals

- Energy & Power

- Food & Beverages

- Heavy Machinery

- Medical Devices

- Metal & Mining

- Metals & Mining

- Oil & Gas

- Other End-Use Industries

- Pharmaceutical

- Pulp & Paper

- Semiconductor & Electronics

By Type

- Cloud Enterprise Resource Planning

- Din Rail Ipcs

- Distributed Control Systems

- Embedded Ipcs

- Human Machine Interface

- Industrial Pcs

- Manufacturing Execution System

- Manufacturing Operation Management

- Panel Ipcs

- Plant Asset Management

- Programmable Logic Controllers

- Quality Management System

- Rack Mount Ipcs

- Supervisory Control And Data Acquisition Systems

- Warehouse Management System

By Industry

- Aerospace

- Automotive

- Chemicals

- Energy & Power

- Energy And Power

- Food & Beverages

- Food And Beverages

- Heavy Machinery

- Medical Devices

- Metal & Mining

- Metals & Mining

- Oil & Gas

- Other Industries

- Pharmaceuticals

- Pulp & Paper

- Semiconductors & Electronics

By Offering

- Hardware

- Professional Services

- Services

- Software

- Software & Services

By Software

- Cloud-Based

- On-Premises

By Service

- Managed Services

- Professional Services

By Industrial Software

- Cloud Enterprise Resource Planning (Erp)

- Manufacturing Execution System (Mes)

- Manufacturing Operation Management (Mom)

- Plant Asset Management (Pam)

- Quality Management Systems (Qms)

- Warehouse Management System (Wms)

By Industrial Robotics

- Industrial Robots

- Robot End Effector

By Product Type

- Collaborative Robot

- Traditional Robot

By Hardware Type

- Advanced Panel-Based Hmi

- Advanced Pc-Based Hmi

- Basic Hmi

- Others Hardware Types

By Software Deployment Mode

- Cloud-Based

- On-Premises

By Industrial Monitoring & Safety

- Industrial Sensor

- Machine Condition Monitoring

- Machine Safety

- Machine Vision

- Predictive Maintenance

- Solid State Relay

By Deployment

- Cloud

- Cloud-Based

- Hybrid

- On-Premises

By Tier Type

- Advanced (Tier 1)

- Basic (Tier 3)

- Intermediate (Tier 2)

By Software Deployment

- Hybrid

- Private

- Public

Target Audience

- Manufacturing Executives : Decision-makers in South American manufacturing need market data to justify automation investments, benchmark operational efficiency gains, and align capital expenditure with regional growth trends.

- Automation Technology Vendors : Suppliers of industrial control systems, PLCs, and factory automation solutions require detailed market sizing and growth forecasts to prioritize South American market entry and resource allocation.

- Investment & Private Equity Firms : Investors evaluating opportunities in South American industrial automation need comprehensive market analysis to assess portfolio company growth potential and sector attractiveness.

- Consulting & Systems Integrators : Systems integrators and consultants serving South American manufacturers need regional market intelligence to advise clients on automation strategies and identify emerging technology adoption areas.

- Government & Trade Organizations : Regional policymakers and trade bodies require market data to develop Industry 4.0 initiatives, assess manufacturing competitiveness, and design incentive programs supporting automation adoption.

Key Companies in the South America Industrial Control & Factory Automation Market

| Company | HQ | Ownership | Strongest segments |

|---|---|---|---|

| EMERSON ELECTRIC CO. | United States | Public Company | Final Control,Measurement & Analytical,Discrete Automation, |

| YOKOGAWA ELECTRIC CORPORATION | Japan | Public Company | Control Business (DCS, PLC, SCADA, software, lifecycle services),Field Instruments (flow, pressure, analyzers, recorders),Measuring Instruments (waveform, optical communications, signal generators), |

| FANUC CORPORATION | Japan | Public Company | Industrial robots,CNC systems and servo motors,Robomachines (machining centers, injection molding, wire EDM), |

| MITSUBISHI ELECTRIC CORPORATION | Japan | Public Company | Factory Automation (FA) systems and industrial solutions,Building systems, air conditioning, and refrigeration,Infrastructure, energy, and public utility systems, |

| OMRON CORPORATION | Japan | Public Company | Industrial Automation (sensors, safety, motion, robotics, control),Device & Module Solutions (relays, switches, connectors, components),Healthcare (cardiovascular, respiratory, pain, remote monitoring), |

| GE VERNOVA | United States | Public Company | Power (gas, nuclear, hydro, steam),Wind (onshore and offshore),Electrification (grid, power conversion, software, solar & storage), |

| FUJI ELECTRIC CO., LTD. | Japan | Public Company | Power Semiconductors,Drives, Motors, and Controls,Power Supply and UPS/Data Center Solutions, |

| HITACHI, LTD. | Japan | Public Company | Digital Systems & Services (IT, cloud, integration, ATMs),Green Energy & Mobility (power grids, energy, rail),Connective Industries (automation, industrial equipment, e-mobility), |

EMERSON ELECTRIC CO.

Emerson Electric Co. is a United States-based public company founded in 1890 with 71,000 employees. The company operates in industrial automation, climate technologies, and process management solutions.

YOKOGAWA ELECTRIC CORPORATION

Yokogawa Electric Corporation is a Japanese public company founded in 1915 with 18,313 employees. It specializes in industrial automation, control systems, and measurement technologies.

FANUC CORPORATION

FANUC Corporation is a Japanese public company founded in 1950 with 10,040 employees. The company is a leading manufacturer of industrial robots and factory automation systems.

MITSUBISHI ELECTRIC CORPORATION

Mitsubishi Electric Corporation is a Japanese public company founded in 1921 with 150,386 employees. It operates across multiple sectors including industrial automation, power systems, and electronic equipment manufacturing.

OMRON CORPORATION

Omron Corporation is a Japanese public company founded in 1933 with 26,050 employees. The company specializes in automation technology, sensing, and control systems for industrial applications.

GE VERNOVA

GE Vernova is a United States-based public company founded in 2023 with 78,000 employees. It focuses on energy infrastructure and industrial solutions.

FUJI ELECTRIC CO., LTD.

Fuji Electric Co., Ltd. is a Japanese public company founded in 1923 with 26,955 employees. The company manufactures power electronics, industrial systems, and automation equipment.

HITACHI, LTD.

Hitachi, Ltd. is a Japanese public company founded in 1910 with 287,901 employees. It is a diversified conglomerate operating in industrial systems, power generation, and digital solutions.

Reasons to Buy this Report

- Market Size & Growth Data : Access precise valuation metrics for South America's industrial automation market with detailed CAGR analysis, enabling accurate investment planning and competitive positioning in the region.

- Country-Level Insights : Gain granular understanding of market dynamics across Brazil, Argentina, Chile, and other South American nations to identify high-potential markets and localized growth opportunities.

- Sector-Specific Trends : Understand automation adoption patterns across mining, automotive, food processing, and chemical industries unique to South America's manufacturing landscape.

- Competitive Intelligence : Benchmark your market position against regional competitors and identify emerging players capitalizing on South America's digital transformation wave through 2030.

- Strategic Planning Support : Leverage comprehensive market forecasts and regional insights to develop targeted go-to-market strategies and resource allocation plans for South American expansion.

Frequently asked questions

What is the current market size of Industrial Control & Factory Automation in Germany?

Germany's Industrial Control & Factory Automation Market is valued at USD 26,529.6 million in 2025.

What is the projected market size for Germany by 2030?

Germany's market is forecast to reach USD 34,868.6 million by 2030, representing 31.4% growth over the forecast period.

What is the CAGR for Germany's Industrial Control & Factory Automation Market?

Germany's market is expected to grow at a compound annual growth rate (CAGR) of 9.1% from 2025 to 2030.

Which industries drive demand for automation solutions in Germany?

Germany's automotive, chemical processing, machinery manufacturing, and pharmaceutical sectors are the primary drivers of industrial control and factory automation adoption.

What factors support market growth in Germany through 2030?

Germany's market growth is supported by Industry 4.0 initiatives, IoT integration, predictive maintenance technologies, sustainability mandates, and government incentives for digital manufacturing transformation.

RESEARCH METHODOLOGY

The study involved major activities in estimating the current market size for the industrial control & factory automation market. Exhaustive secondary research was done to collect information on the industrial control & factory automation industry. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain using primary research. Different approaches, such as top-down and bottom-up, were employed to estimate the total market size. After that, the market breakup and data triangulation procedures were used to estimate the market size of the segments and subsegments of the industrial control & factory automation market.

Secondary Research

The market for the companies offering industrial control & factory automation solutions is arrived at by secondary data available through paid and unpaid sources, analyzing the product portfolios of the major companies in the ecosystem, and rating the companies by their performance and quality. Various sources were referred to in the secondary research process to identify and collect information for this study. The secondary sources include annual reports, press releases, investor presentations of companies, white papers, journals, certified publications, and articles from recognized authors, directories, and databases. In the secondary research process, various secondary sources were referred to for identifying and collecting information related to the study. Secondary sources included annual reports, press releases, and investor presentations of blockchain vendors, forums, certified publications, and whitepapers. The secondary research was used to obtain critical information on the industry's value chain, the total pool of key players, market classification, and segmentation from the market and technology-oriented perspectives.

Primary Research

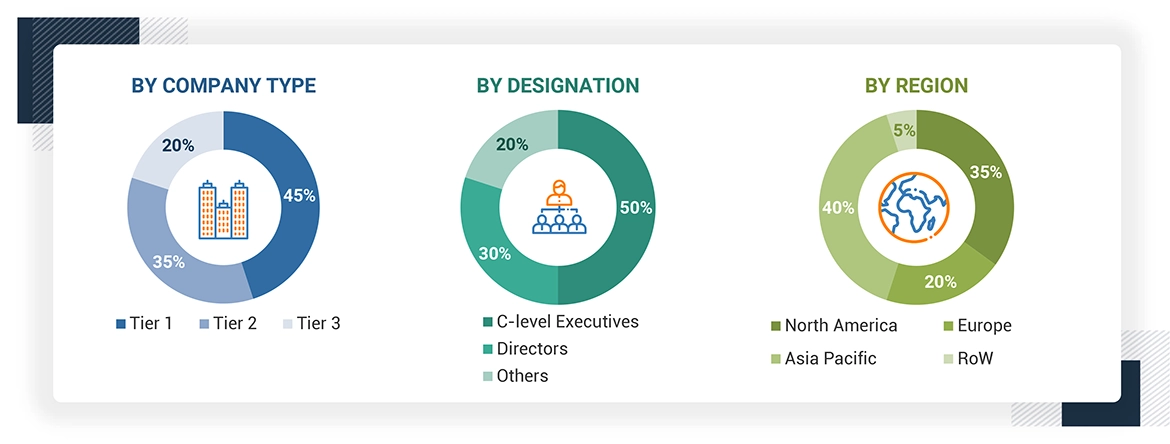

Extensive primary research has been conducted after understanding and analyzing the current scenario of the industrial control & factory automation market through secondary research. Several primary interviews have been conducted with the key opinion leaders from the demand and supply sides across four main regions—North America, Europe, Asia Pacific, and the Rest of Europe. Approximately 25% of the primary interviews were conducted with the demand-side respondents, while approximately 75% were conducted with the supply-side respondents. The primary data has been collected through questionnaires, emails, and telephone interviews.

After interacting with industry experts, brief sessions were conducted with highly experienced independent consultants to reinforce the findings from our primary. This, along with the in-house subject matter experts’ opinions, has led us to the findings as described in the remainder of this report. The breakdown of primary respondents is as follows:

About the assumptions considered for the study, To know download the pdf brochure

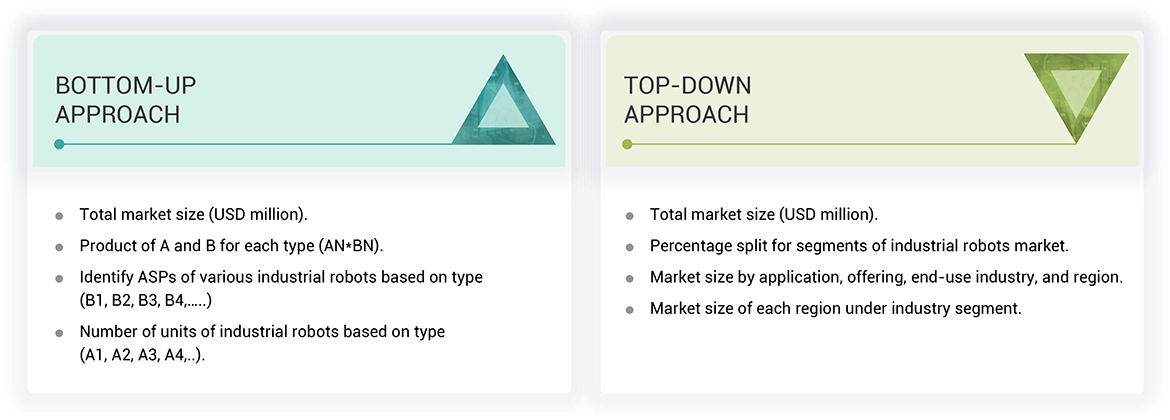

Market Size Estimation

Both top-down and bottom-up approaches wete used to estimate and validate the total size of the industrial control & factory automation market. These methods were also used extensively to estimate the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

Industrial Control & Factory Automation Market : Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall market size using the market size estimation processes as explained above, the market was split into several segments and subsegments. The data triangulation and market breakdown procedures were employed, wherever applicable, to complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment. The data was triangulated by studying various factors and trends from the demand and supply sides.

Market Definition

Industrial control & factory automation is a highly digitalized and connected production system that can self-optimize performance across a broad network, self-adapt in various conditions in real time, and autonomously run an entire production process. The major advantage of industrial control & factory automation is its ability to evolve with the changing needs of organizations. Industrial control & factory automation uses a network to connect the virtual and physical elements of production processes to actual manufacturing operations. It helps to create an autonomous manufacturing environment that can handle any technical issues during real-time production, using fragmented information and communication structures to optimize production processes.

Key Stakeholders

- End users

- Government bodies, venture capitalists, and private equity firms

- Manufacturers of industrial control & factory automation components

- Distributors of industrial control & factory automation components and solutions

- Industrial control & factory automation industry associations

- Professional service/solution providers

- Research institutions and organizations

- Standards organizations and regulatory authorities related to the industrial control & factory automation market

- System integrators

- Technology consultants

Report Objectives

- To describe and forecast the industrial control and factory automation market, in terms of value, based on component , and industry

- To forecast the industrial control and factory automation market, in terms of volume, by component

- To forecast the market size, in terms of value, for four main regions—North America, Europe, Asia Pacific, and the RoW.

- To provide detailed information regarding drivers, restraints, opportunities, and challenges influencing the market growth

- To provide a detailed overview of the value chain of the industrial control and factory automation ecosystem

- To strategically analyze micromarkets1 with respect to individual growth trends, prospects, and contributions to the total market

- To provide a detailed overview of the industrial control and factory automation market value chain

- To provide an ecosystem analysis, case study analysis, key conferences, patent analysis, trade analysis, technology analysis, average selling price (ASP) analysis, Porter’s five forces analysis, buying criteria, and regulations pertaining to the market

- To track and analyze competitive developments undertaken by key players in the industrial control and factory automation market

- To profile key players and analyze their market share, core competencies2, and detailed competitive landscape for market leaders

- To benchmark market players using the company evaluation matrix, analyzing players based on various parameters within broad business categories and product strategies.

- To analyze strategies, such as product launches, acquisitions, partnerships, and expansions, adopted by the players in the industrial control and factory automation market

- To study the impact of AI on the market under study, along with the macroeconomic outlook for each region

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to the specific requirements of companies. The following customization options are available for the report:

- Detailed analysis and profiling of additional market players based on various blocks of the supply chain

Get the Full Industrial Control & Factory Automation Market Report

Full forecast, segment splits, and company analysis for all Industrial Control & Factory Automation Market.

- North America Industrial Control & Factory Automation Market

- Europe Industrial Control & Factory Automation Market

- Asia Pacific Industrial Control & Factory Automation Market

- Rest of World Industrial Control & Factory Automation Market

- Scada Industrial Control & Factory Automation Market

- Dcs Industrial Control & Factory Automation Market

- Plc Industrial Control & Factory Automation Market

- Industrial Pc Industrial Control & Factory Automation Market

- Hmi Industrial Control & Factory Automation Market

- Mes Industrial Control & Factory Automation Market

- Pam Industrial Control & Factory Automation Market

- Wms Industrial Control & Factory Automation Market

- Mom Industrial Control & Factory Automation Market

- Cloud Erp Industrial Control & Factory Automation Market

- Qms Industrial Control & Factory Automation Market

- Canada Industrial Control & Factory Automation Market

- Mexico Industrial Control & Factory Automation Market

- US Industrial Control & Factory Automation Market

- Germany Industrial Control & Factory Automation Market

- France Industrial Control & Factory Automation Market

- Rest Of Europe Industrial Control & Factory Automation Market

- UK Industrial Control & Factory Automation Market

- China Industrial Control & Factory Automation Market

- India Industrial Control & Factory Automation Market

- Japan Industrial Control & Factory Automation Market

- Rest Of Asia Pacific Industrial Control & Factory Automation Market

- Italy Industrial Control & Factory Automation Market

- GCC Industrial Control & Factory Automation Market

- Brazil Industrial Control & Factory Automation Market

- Rest Of South America Industrial Control & Factory Automation Market

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report